Live Comments

BoJ Holds Steady, Hawkish Dissent and Outlook Keep October Hike in Focus

Bank of Japan left its policy rate unchanged at 1.00%, as widely expected, but delivered a policy package that reinforced its gradual normalization message. The decision was approved by an 8-1 vote, with Takata Hajime dissenting in favor of an immediate 25 basis point hike to 1.25%. Takata argued that Japan had entered "a new phase" requiring "a nimble approach" to address upside inflation risks arising from overseas demand shocks and changes in global financial conditions. While the majority opted to wait, the dissent underscored growing confidence within the Policy Board that inflation risks are becoming increasingly skewed to the upside.

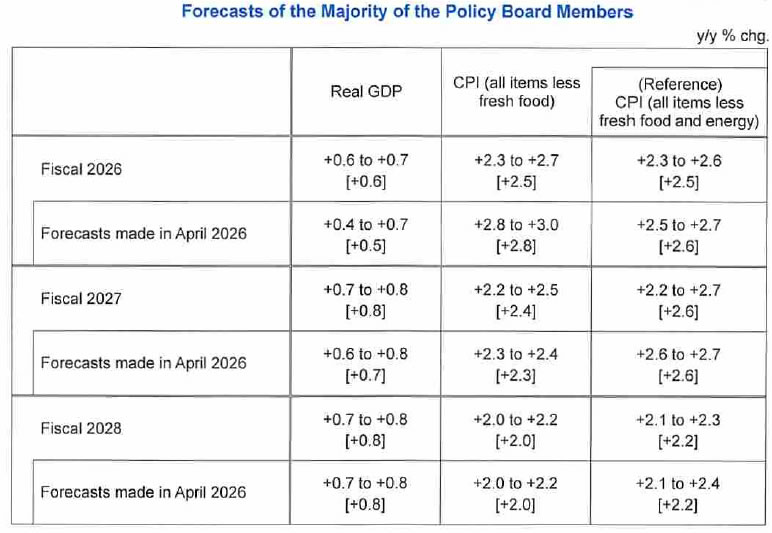

The updated Outlook Report painted a nuanced but constructive picture. The BoJ modestly raised its median GDP forecasts for fiscal 2026 and 2027 while lowering its fiscal 2026 core CPI projection to 2.5% from 2.8%, reflecting an expectation that the impact of higher crude oil prices will gradually fade. At the same time, the Bank lifted its fiscal 2027 inflation forecast to 2.4% from 2.3%, suggesting policymakers see inflation becoming more durable rather than simply driven by temporary energy shocks.

The report stated that CPI inflation is "likely to accelerate to a level clearly above 2 percent" in the second half of fiscal 2026 before easing toward the target as oil effects fade. More importantly, it emphasized that "the mechanism in which wages and prices rise moderately in interaction with each other will be maintained," allowing underlying inflation to gradually converge with the Bank's price stability objective.

Perhaps the strongest signal came from the Bank's forward guidance. The BoJ reiterated that "risks to the outlook for the CPI are skewed to the upside" and warned of the risk that inflation could "deviate upward to a level above the 2 percent price stability target" as firms continue raising wages and prices. It also stated explicitly that it "will continue to raise the policy interest rate and adjust the degree of monetary accommodation" while assessing economic activity, prices and financial conditions. Policymakers highlighted the Middle East, AI-related global demand and exchange-rate developments as key uncertainties.

Taken together, the decision was less about today's unchanged rate than reinforcing the direction of travel. The BoJ stopped short of signaling when the next move will come, but it made clear that further normalization remains the baseline rather than merely a possibility.

Key Takeaways

- BoJ kept the policy rate unchanged at 1.00%, as widely expected. The decision was approved by an 8-1 vote, but the lone dissent made the meeting more hawkish than the headline suggests.

- Takata Hajime voted for an immediate rate hike to 1.25%. He argued Japan has entered "a new phase" requiring "a nimble approach" to address upside inflation risks stemming from overseas demand shocks and changes in global financial conditions.

- The medium-term inflation outlook improved despite a lower FY2026 forecast. While the median FY2026 core CPI forecast was lowered from 2.8% to 2.5%, the FY2027 projection was raised from 2.3% to 2.4%, indicating the BoJ sees inflation becoming more durable rather than merely driven by temporary energy shocks.

- The BoJ expects inflation to stay above target in the near term. The Outlook Report said CPI is "likely to accelerate to a level clearly above 2 percent" in the second half of fiscal 2026 before gradually easing toward the target as oil-price effects fade.

- The wage-price cycle remains central to the BoJ's confidence. The Bank said "the mechanism in which wages and prices rise moderately in interaction with each other will be maintained," supporting a gradual rise in underlying inflation.

- Policy guidance became more explicit. The BoJ stated it "will continue to raise the policy interest rate and adjust the degree of monetary accommodation" while assessing economic activity, prices and financial conditions, reinforcing that further normalization remains the baseline scenario.

- Inflation risks are now explicitly tilted upward. The Bank said risks to economic activity are "generally balanced," but "risks to the outlook for the CPI are skewed to the upside," citing the Middle East, AI-related global demand and exchange-rate developments as key uncertainties.

China NBS Manufacturing PMI Falls Back Into Contraction at 49.2 as Domestic Demand Weakens

China's manufacturing activity slipped back into contraction in July, suggesting the recovery seen during the second quarter has lost momentum. The official NBS Manufacturing PMI fell from 50.3 to 49.2, below market expectations of 49.9 and marking the lowest reading since February. The decline also erased four consecutive months of expansion, indicating factories entered the third quarter on a weaker footing amid softening demand and a more challenging external environment.

The deterioration was broad-based. The production index dropped -1.5 points to 49.9, while the new orders index fell -2.7 points to 48.5, highlighting a renewed loss of domestic demand. New export orders also weakened to 49.6, while purchasing activity, imports and order backlogs all deteriorated, suggesting manufacturers became increasingly cautious about production plans. Although finished goods inventories and employment edged higher, business confidence softened, with the production and business activity expectations index slipping to 54.1. The National Bureau of Statistics' accompanying analysis emphasized that weak domestic demand remains the primary constraint on production and called for stronger fiscal support and infrastructure investment to revive private-sector activity.

The weakness extended beyond manufacturing. The official non-manufacturing PMI also fell back below the expansion threshold to 49.0 from 50.2, indicating slower activity in the broader services and construction sectors. Together, the surveys point to a broad loss of economic momentum at the start of the third quarter and reinforce expectations that policymakers may need to introduce additional measures to support domestic demand if growth continues to soften.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| NBS Manufacturing PMI (Jul) | 49.2 | 49.9 | 50.3 |

| NBS Non-Manufacturing PMI (Jul) | 49.0 | 50.0 | 50.2 |

| Production Index | 49.9 | — | 51.4 |

| New Orders Index | 48.5 | — | 51.2 |

| New Export Orders Index | 49.6 | — | 50.1 |

| Purchasing Volume Index | 49.4 | — | 51.4 |

| Imports Index | 47.5 | — | 49.6 |

| Employment Index | 49.0 | — | 48.5 |

| Output Price Index | 47.8 | — | 48.2 |

| Input Price Index | 53.2 | — | 54.2 |

| Business Expectations Index | 54.1 | — | 54.3 |

Key Takeaways

- China's manufacturing sector slipped back into contraction. The official Manufacturing PMI fell from 50.3 to 49.2, below both the 50 expansion threshold and market expectations of 49.9, marking the weakest reading since February.

- Demand weakened noticeably. The new orders index dropped 2.7 points to 48.5, the largest decline among the major sub-indices, highlighting softer domestic demand. New export orders also slipped back below 50, indicating external demand remained subdued.

- Production lost momentum. The production index fell from 51.4 to 49.9, while purchasing activity and imports also weakened, suggesting manufacturers scaled back production plans in response to softer orders.

- Weakness was broad-based across company sizes. PMI fell below 50 for large (49.5), medium-sized (49.7) and small enterprises (47.4), with small firms continuing to face the greatest pressure.

- Business confidence softened but remained positive. The production and business activity expectations index eased slightly to 54.1, suggesting manufacturers still expect growth over the coming months despite weaker current conditions.

- Services also moved into contraction. The Non-Manufacturing PMI unexpectedly fell from 50.2 to 49.0, indicating economic weakness has broadened beyond factories into services and construction.

- The official assessment focused on domestic demand. The NBS noted that weakening domestic demand remains the main constraint on production and called for stronger fiscal support, infrastructure investment and measures to boost employment and household income.

Japan Factory Output Beats Forecasts as Retail Sales Lose Momentum

Japan's industrial sector delivered another encouraging performance in June, while household spending showed signs of losing momentum. Industrial production rose 1.3% m/m, accelerating from 0.1% in May and comfortably beating expectations of 0.7%. It marked the third consecutive monthly increase and the strongest gain since January, with output also rising 4.2% y/y, reversing May's -2.1% decline to record the fastest annual growth in nearly four years. In contrast, retail sales increased just 0.5% y/y, slowing sharply from a revised 5.0% and missing expectations of 3.1%.

The improvement in factory activity was broad enough to suggest manufacturing continues to recover. Production machinery rebounded 7.6% after falling -3.5% in May, while electrical machinery and information and communication electronics equipment rose 5.8% following a -5.1% decline. General-purpose and business-oriented machinery also recovered strongly. Manufacturers remain optimistic, projecting production to increase 1.2% in July and a further 4.5% in August, indicating confidence that the recovery still has momentum.

The retail figures, however, painted a more cautious picture of domestic demand. Although automobile sales remained strong and spending on clothing and personal goods increased, weakness was widespread elsewhere, with declines in food and beverages, department stores, machinery, fuel and pharmaceuticals. Retail sales also fell -4.1% m/m, the steepest monthly decline since April 2021.

Taken together, the data suggest Japan's recovery remains uneven. Manufacturing continues to benefit from improving external conditions and stronger business investment, while household consumption appears to be facing increasing pressure from higher living costs.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Industrial Production M/M (Jun P) | 1.3% | 0.7% | 0.1% |

| Industrial Production Y/Y (Jun) | 4.2% | — | -2.1% |

| Retail Sales Y/Y (Jun) | 0.5% | 3.1% | 5.0% |

| Retail Sales M/M (Jun) | -4.1% | — | 1.7% |

| Manufacturers' Output Forecast (Jul) | 1.2% | — | — |

| Manufacturers' Output Forecast (Aug) | 4.5% | — | — |

Key Takeaways

- Japan's manufacturing recovery gathered pace. Industrial production rose 1.3% m/m, beating expectations of 0.7% and marking the third consecutive monthly increase. Annual output rebounded from -2.1% to 4.2%, the strongest growth in nearly four years.

- Capital goods industries led the rebound. Production machinery, electrical machinery and business-oriented equipment all recorded strong gains, suggesting business investment and factory activity remain resilient.

- Manufacturers remain optimistic. The Ministry of Economy, Trade and Industry survey showed firms expect production to rise 1.2% in July and 4.5% in August, pointing to continued momentum in the industrial sector.

- Consumer spending weakened sharply. Retail sales slowed from 5.0% to 0.5% y/y, well below expectations of 3.1%, while sales fell 4.1% m/m, the steepest monthly decline since April 2021.

- Retail weakness was broad-based. Apart from strong automobile and apparel sales, most categories—including food and beverages, department stores, machinery, fuel, and pharmaceuticals—recorded declines.

- The data present a mixed picture for the BoJ. Strong factory activity supports confidence in the economic recovery and ongoing policy normalization, but weaker household spending suggests domestic demand remains fragile, arguing for a gradual rather than aggressive tightening path.