Live Comments

Canada GDP Beats Expectations, June Estimate Points to Strong Q2 Growth

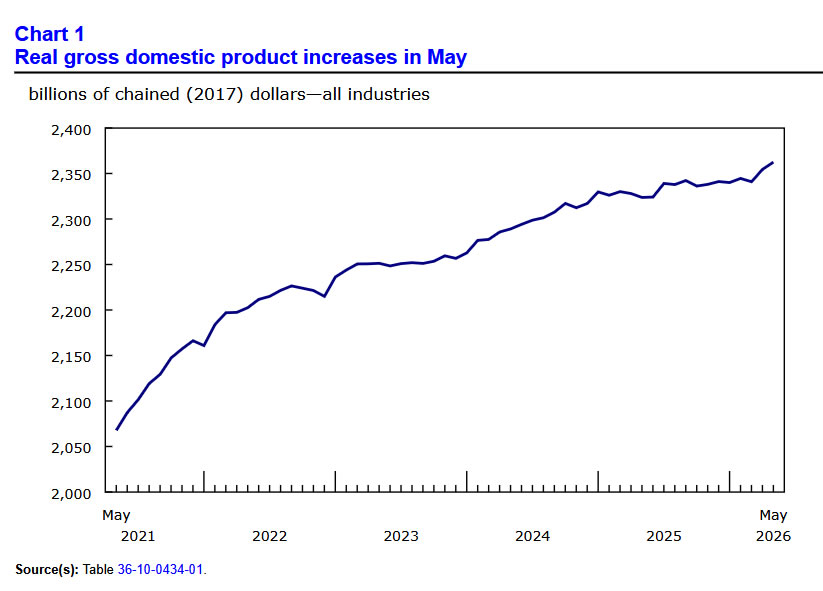

Canada's economy expanded 0.3% month-over-month in May, beating expectations of 0.2% and marking a second consecutive monthly increase. Growth was broad-based, with 13 of 20 industrial sectors posting gains as both goods-producing and services-producing industries contributed to the expansion. Statistics Canada also estimated that real GDP rose a further 0.2% in June, pointing to annualized growth of 0.8% for the second quarter based on industry data.

The goods-producing sector led the way with a 0.6% increase in May, supported by widespread gains across most industries. Mining, quarrying and oil and gas extraction advanced 1.0%, extending April's recovery as two of its three subsectors posted a second straight monthly increase. Manufacturing also grew 0.3%, with most subsectors expanding during the month. On the services side, output rose 0.2%, driven primarily by gains in real estate and rental and leasing as well as public administration. Real estate activity increased 0.4%, with all subsectors contributing to the advance.

The latest figures suggest the Canadian economy maintained solid momentum through the second quarter despite an uncertain external backdrop. The advance estimate for June indicates growth remained supported by wholesale trade, finance and insurance, and retail trade, although weaker utilities and agriculture partially offset those gains. With domestic activity continuing to broaden across both goods and services sectors, the data point to an economy that has proved more resilient than expected heading into the second half of the year.

Economic Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| GDP M/M (May) | 0.3% | 0.2% | 0.5% |

| GDP M/M (June Advance) | 0.2% | — | — |

| Q2 2026 GDP (Industry-Based Estimate) | 0.8% | — | — |

Sector Breakdown

| Component | Current | Trend |

|---|---|---|

| Goods-producing industries | 0.6% | ↑ Broad-based growth |

| Services-producing industries | 0.2% | ↑ Continued expansion |

| Mining, quarrying & oil and gas | 1.0% | ↑ Second consecutive gain |

| Manufacturing | 0.3% | ↑ Majority of subsectors higher |

| Real estate & rental and leasing | 0.4% | ↑ Broad-based gains |

Key Takeaways

- Canada's economy outperformed expectations in May. Real GDP rose 0.3% month-over-month, beating the 0.2% consensus forecast and marking a second consecutive monthly increase.

- Growth was broad-based. Thirteen of twenty industrial sectors expanded, with both goods-producing and services-producing industries contributing to the overall gain.

- Goods production led the expansion. Goods-producing industries grew 0.6%, supported by stronger mining, oil and gas extraction, and manufacturing output.

- Mining and energy remained key drivers. The mining, quarrying and oil and gas extraction sector increased 1.0%, posting a second straight monthly gain.

- Services continued to provide support. Services-producing industries rose 0.2%, led by real estate and rental and leasing (0.4%) together with public administration.

- June appears to have maintained the momentum. Statistics Canada's advance estimate points to another 0.2% increase in June, driven by wholesale trade, finance and insurance, and retail trade.

- Second-quarter growth looks solid. Based on May data and the June advance estimate, real GDP by industry is on track to have expanded 0.8% in Q2, suggesting the Canadian economy entered the second half of the year with steady momentum.

Eurozone Core Inflation Unexpectedly Accelerates to 2.5%, Reinforcing ECB Hawkishness

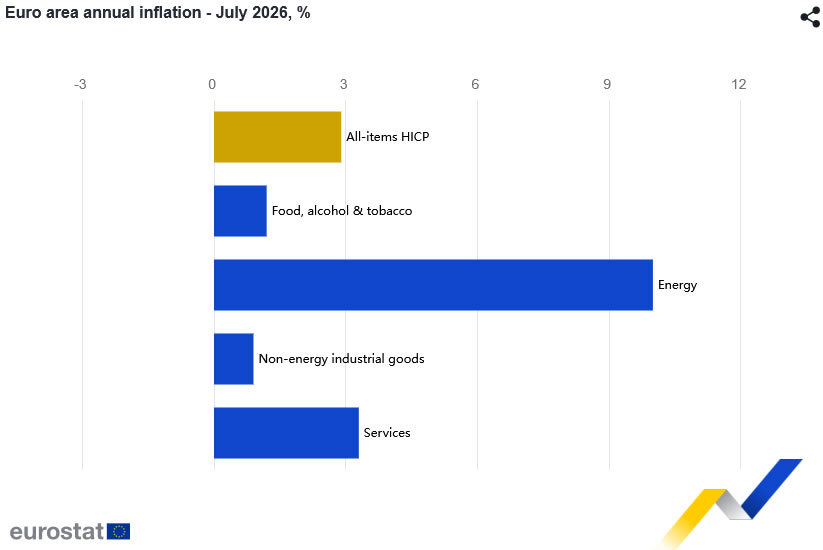

Eurozone inflation remained elevated in July, with headline CPI holding at 2.9% year-over-year, matching expectations and edging up from 2.8% in June. The bigger surprise came from core inflation, which accelerated to 2.5% from 2.4%, beating expectations for an unchanged reading. While the headline increase was largely driven by higher energy prices, the pickup in core inflation suggests underlying price pressures are proving more persistent than markets had anticipated.

The details of the report reinforced that message. Energy inflation accelerated sharply from 8.5% to 10.0% as higher oil prices fed into consumer prices. More importantly for the European Central Bank, services inflation edged up from 3.2% to 3.3%, highlighting continued domestic price pressures linked to wages and labor costs. Non-energy industrial goods inflation also firmed from 0.7% to 0.9%, while food, alcohol and tobacco inflation eased further from 1.5% to 1.2%. The combination suggests inflation is becoming broader, with cooling food prices masking renewed firmness elsewhere in the basket.

For the ECB, the report lends further support to the cautious hawkish tone struck after last week's policy meeting. President Christine Lagarde warned that inflation is likely to remain above target well into 2027, while policymakers such as Peter Kazimir have argued that another rate increase may still be needed. With underlying inflation firming before the full second-round effects of higher energy costs have filtered through the economy, today's data lower the hurdle for a September "insurance hike", even if they stop short of making another increase a foregone conclusion.

Economic Data Summary

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Headline CPI Y/Y (Jul P) | 2.9% | 2.9% | 2.8% |

| Core CPI Y/Y (Jul P) | 2.5% | 2.4% | 2.4% |

Inflation Components

| Component | Current | Previous | Trend |

|---|---|---|---|

| Energy | 10.0% | 8.5% | ↑ Accelerated sharply |

| Services | 3.3% | 3.2% | ↑ Sticky, edged higher |

| Non-energy industrial goods | 0.9% | 0.7% | ↑ Firmed |

| Food, alcohol & tobacco | 1.2% | 1.5% | ↓ Continued easing |

Key Takeaways

- Headline inflation edged higher while core inflation surprised to the upside. Eurozone headline CPI rose from 2.8% to 2.9%, matching expectations, while core CPI accelerated unexpectedly from 2.4% to 2.5%.

- Services inflation remains stubbornly elevated. Services CPI increased from 3.2% to 3.3%, indicating domestic price pressures linked to wages continue to prove persistent.

- Energy inflation is reaccelerating. Energy inflation jumped from 8.5% to 10.0% as higher oil prices began feeding into consumer prices.

- Goods inflation also strengthened. Non-energy industrial goods inflation rose from 0.7% to 0.9%, suggesting price pressures are broadening beyond energy alone.

- Food continues to be the main disinflation driver. Food, alcohol and tobacco inflation slowed from 1.5% to 1.2%, helping contain the rise in headline CPI.

- The composition matters more than the headline. Stronger services, energy and goods inflation outweighed easing food prices, pointing to broader underlying inflationary pressures.

- The report supports the ECB's hawkish bias. While not guaranteeing a September rate hike, the upside surprise in core inflation strengthens the case for another "insurance hike" if inflation remains persistent.

BoJ Holds Steady, Hawkish Dissent and Outlook Keep October Hike in Focus

Bank of Japan left its policy rate unchanged at 1.00%, as widely expected, but delivered a policy package that reinforced its gradual normalization message. The decision was approved by an 8-1 vote, with Takata Hajime dissenting in favor of an immediate 25 basis point hike to 1.25%. Takata argued that Japan had entered "a new phase" requiring "a nimble approach" to address upside inflation risks arising from overseas demand shocks and changes in global financial conditions. While the majority opted to wait, the dissent underscored growing confidence within the Policy Board that inflation risks are becoming increasingly skewed to the upside.

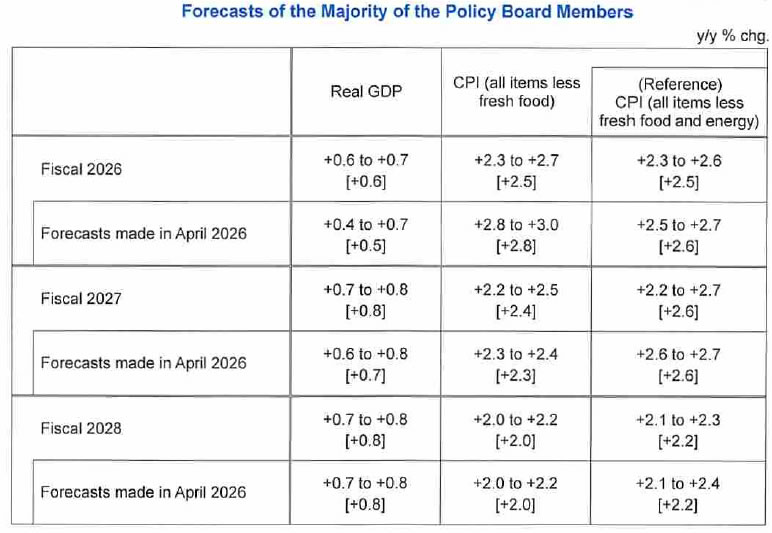

The updated Outlook Report painted a nuanced but constructive picture. The BoJ modestly raised its median GDP forecasts for fiscal 2026 and 2027 while lowering its fiscal 2026 core CPI projection to 2.5% from 2.8%, reflecting an expectation that the impact of higher crude oil prices will gradually fade. At the same time, the Bank lifted its fiscal 2027 inflation forecast to 2.4% from 2.3%, suggesting policymakers see inflation becoming more durable rather than simply driven by temporary energy shocks.

The report stated that CPI inflation is "likely to accelerate to a level clearly above 2 percent" in the second half of fiscal 2026 before easing toward the target as oil effects fade. More importantly, it emphasized that "the mechanism in which wages and prices rise moderately in interaction with each other will be maintained," allowing underlying inflation to gradually converge with the Bank's price stability objective.

Perhaps the strongest signal came from the Bank's forward guidance. The BoJ reiterated that "risks to the outlook for the CPI are skewed to the upside" and warned of the risk that inflation could "deviate upward to a level above the 2 percent price stability target" as firms continue raising wages and prices. It also stated explicitly that it "will continue to raise the policy interest rate and adjust the degree of monetary accommodation" while assessing economic activity, prices and financial conditions. Policymakers highlighted the Middle East, AI-related global demand and exchange-rate developments as key uncertainties.

Taken together, the decision was less about today's unchanged rate than reinforcing the direction of travel. The BoJ stopped short of signaling when the next move will come, but it made clear that further normalization remains the baseline rather than merely a possibility.

Key Takeaways

- BoJ kept the policy rate unchanged at 1.00%, as widely expected. The decision was approved by an 8-1 vote, but the lone dissent made the meeting more hawkish than the headline suggests.

- Takata Hajime voted for an immediate rate hike to 1.25%. He argued Japan has entered "a new phase" requiring "a nimble approach" to address upside inflation risks stemming from overseas demand shocks and changes in global financial conditions.

- The medium-term inflation outlook improved despite a lower FY2026 forecast. While the median FY2026 core CPI forecast was lowered from 2.8% to 2.5%, the FY2027 projection was raised from 2.3% to 2.4%, indicating the BoJ sees inflation becoming more durable rather than merely driven by temporary energy shocks.

- The BoJ expects inflation to stay above target in the near term. The Outlook Report said CPI is "likely to accelerate to a level clearly above 2 percent" in the second half of fiscal 2026 before gradually easing toward the target as oil-price effects fade.

- The wage-price cycle remains central to the BoJ's confidence. The Bank said "the mechanism in which wages and prices rise moderately in interaction with each other will be maintained," supporting a gradual rise in underlying inflation.

- Policy guidance became more explicit. The BoJ stated it "will continue to raise the policy interest rate and adjust the degree of monetary accommodation" while assessing economic activity, prices and financial conditions, reinforcing that further normalization remains the baseline scenario.

- Inflation risks are now explicitly tilted upward. The Bank said risks to economic activity are "generally balanced," but "risks to the outlook for the CPI are skewed to the upside," citing the Middle East, AI-related global demand and exchange-rate developments as key uncertainties.