Live Comments

Canada Retail Sales Rise 1.0% in May, June Momentum Seen Continuing

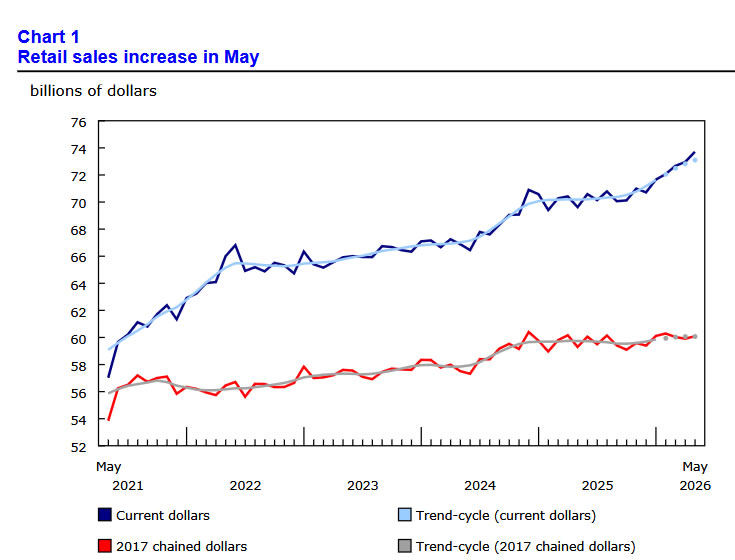

Canada's retail sales rose 1.0% mom to CAD 73.7B in May, marking a broad-based improvement in consumer spending as all nine retail subsectors posted gains. The increase was led by gasoline stations and fuel vendors, reflecting higher fuel prices, while motor vehicle and parts dealers also contributed with a second consecutive monthly increase. Excluding the more volatile gasoline and auto categories, core retail sales still advanced a solid 0.9%, suggesting household demand remained resilient beyond energy-related spending.

The composition of the report painted a slightly more nuanced picture. Sales at gasoline stations and fuel vendors rose 3.1% in value terms, but volumes fell -2.7%, indicating that higher prices rather than stronger demand drove much of the increase. Meanwhile, motor vehicle and parts dealers recorded a 0.7% gain, with new car dealers leading the advance. Overall retail sales volumes rose 0.3%, pointing to modest but positive growth in the quantity of goods purchased after adjusting for price changes.

The outlook also remained constructive. Statistics Canada's advance estimate suggests retail sales increased a further 0.4% in June, indicating consumer spending continued to expand heading into the second quarter's close.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Retail Sales (May, m/m) | +1.0% | +0.7% | +0.3% |

| Core Retail Sales (May, m/m) | +0.9% | — | +0.2% |

| Retail Sales Volume (May, m/m) | +0.3% | — | +0.5% |

| Advance Estimate – Retail Sales (Jun, m/m) | +0.4% | — | — |

Key Takeaways

- Broad-based strength: Retail sales rose 1.0% m/m, with all nine retail subsectors recording gains, indicating consumer spending remained resilient.

- Underlying demand improved: Core retail sales, excluding autos and gasoline, increased 0.9%, showing the strength extended beyond volatile sectors.

- Energy prices boosted headline sales: Sales at gasoline stations rose 3.1%, but volumes fell -2.7%, indicating higher fuel prices rather than stronger demand drove much of the increase.

- Real spending still expanded: Overall retail sales volumes increased 0.3%, suggesting consumers purchased more goods even after adjusting for price effects.

- Auto sector remained supportive: Motor vehicle and parts dealers posted a second consecutive monthly gain, led by higher new vehicle sales.

- Momentum carried into June: Statistics Canada's advance estimate points to another 0.4% increase in June retail sales, indicating household spending remained on a firm footing heading into Q2's close.

US Jobless Claims Fall Sharply to 187k vs exp 212k

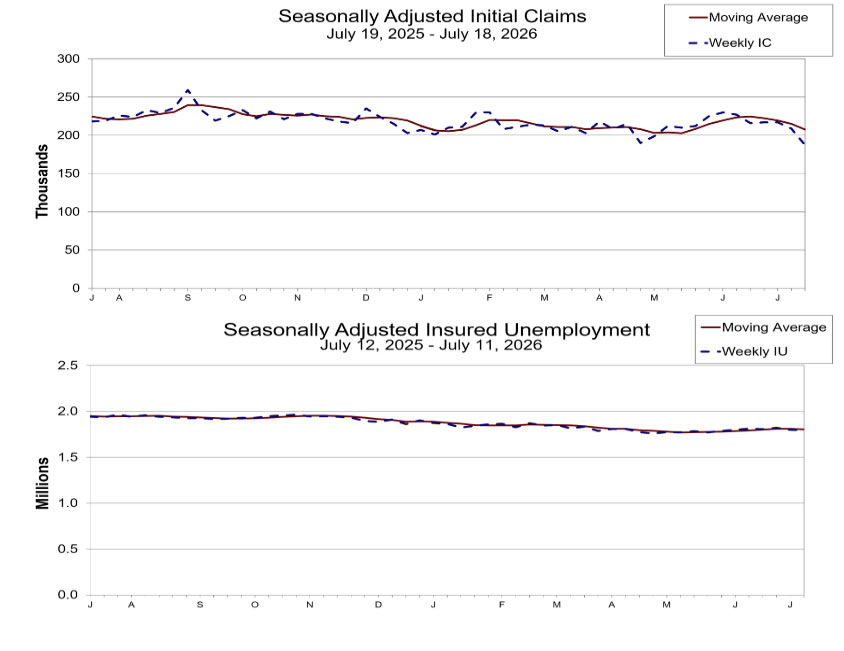

US initial jobless claims fell sharply by -22k to 187k in the week ended July 18, well below expectations of 212k. The prior week's figure was revised slightly higher to 209k from 208k, while the four-week moving average declined by -7.25k to 207.5k. The data point to continued resilience in the labor market despite mounting uncertainty surrounding energy prices and global geopolitical tensions.

The improvement was also reflected in continuing claims, which edged down by -2k to 1.796m in the week ended July 11, while the insured unemployment rate held steady at 1.2%. Although the decline was modest, it suggests workers who lose their jobs are still finding new employment relatively quickly, reinforcing the view that labor market conditions remain tight rather than deteriorating. The four-week average of continuing claims also fell, indicating that broader labor market momentum has remained intact.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Initial Jobless Claims (Jul 18) | 187K | 212K | 209K |

| 4-Week Average | 207.5K | — | 214.75K |

| Continuing Claims (Jul 11) | 1.796M | — | 1.798M |

| Insured Unemployment Rate | 1.2% | — | 1.2% |

ECB Holds Rates, Closely Watches Energy Shock and Inflation Spillovers

The European Central Bank left its key interest rates unchanged as widely expected, keeping the deposit rate at 2.25%, while acknowledging that renewed energy market volatility has complicated the inflation outlook. Rather than signalling any change in policy direction, the Governing Council emphasized that the "outlook for energy prices, while highly volatile," remains well above levels seen before the Middle East conflict, adding that "the full inflationary impact of the energy shock has yet to play out." The statement reinforces that policymakers are focused on how persistent higher energy costs could feed through to broader inflation.

The ECB said it is "closely monitoring the intensity and duration of the shock, as well as its indirect and second-round effects," highlighting concerns that sustained increases in energy prices could eventually spill over into wages and underlying inflation. At the same time, policymakers stressed that they remain "committed to setting monetary policy to ensure that inflation stabilizes at its 2% target in the medium term." The statement stopped short of endorsing expectations for another rate hike, instead reiterating that the Governing Council will continue to determine policy on a "data-dependent and meeting-by-meeting approach" and is "not pre-committing to a particular rate path."

Overall, the statement leans mildly hawkish without materially changing the ECB's policy framework. By explicitly acknowledging that the energy shock is still unfolding while avoiding any guidance on future rate moves, the Governing Council has left itself maximum flexibility as geopolitical developments continue to evolve. Attention now shifts to President Christine Lagarde's press conference, where markets will look for clues on whether she validates growing expectations that renewed energy-driven inflation could keep the door open to another rate hike later this year.