Live Comments

China Exports Rise 23.9% YoY as High-Tech Demand Defies Tariffs

China's exports remained a major source of economic strength in July, supported by booming global demand for high-tech products even as growth moderated from June's rapid pace. Exports rose 23.9% yoy in US dollar terms, slowing from 27.0% but beating expectations of 22.2%. Imports also remained strong, though growth eased from 36.0% to 27.5%, broadly matching forecasts. Trade surplus consequently narrowed from $125.6B to $112.5B, but still exceeded expectations of around $107B.

High-tech manufacturing continued to drive export performance. Semiconductor exports nearly doubled in value over first seven months of year, while overall high-tech exports surged 40.7%. Chip exports alone jumped 117% yoy in July, while cars, electric vehicles, batteries and other advanced manufacturing products also recorded strong overseas demand. But strength was increasingly uneven: ceramic exports plunged 28.3% and toy shipments fell 9.7%, highlighting widening divergence between advanced manufacturers benefiting from global AI and electrification investment and traditional industries facing much softer demand.

Trade with US also remained resilient, with Chinese exports rising 17% yoy in July, accelerating from around 14% in June. However, part of that strength likely reflected exporters front-loading shipments ahead of higher US tariffs, raising questions over whether current growth can be sustained. Exports to EU increased 16%, providing another source of external support. With domestic consumption and investment still subdued, exports remain crucial to China's growth outlook, but increasing dependence on high-tech demand and escalating trade barriers leave external sector exposed to both global technology cycle and further protectionist measures.

Data Summary

| Indicator | July 2026 | Expected |

|---|---|---|

| Exports (yoy, USD) | +23.9% | +22.2% |

| Imports (yoy, USD) | +27.5% | +27.9% |

| Trade Surplus | $112.5B | $107B |

| Exports to US (yoy) | +17.0% | — |

| Exports to EU (yoy) | +16.0% | — |

| High-Tech Exports (Jan–Jul, yoy) | +40.7% | — |

| Semiconductor Exports (Jan–Jul, value) | Nearly +100% | — |

| Chip Exports (July, yoy) | +117% | — |

Key Takeaways

- China's exports grew 23.9% yoy in July, slowing from 27.0% in June but comfortably beating expectations of 22.2%. External demand remains an important support for economy amid subdued domestic consumption and investment.

- Imports increased 27.5% yoy, down from 36.0% in June and broadly matching expectations, while trade surplus narrowed from $125.6B to $112.5B.

- AI and advanced manufacturing remain major engines of export growth. High-tech exports surged 40.7% during first seven months of 2026, while semiconductor exports nearly doubled in value.

- July chip exports surged 117% yoy, while auto exports increased by more than 50%, highlighting strength in sectors benefiting from global AI infrastructure spending and China's advanced manufacturing expansion.

- Performance remains uneven. Ceramic exports fell 28.3% and toy exports dropped 9.7%, showing traditional industries are not sharing equally in export boom.

- Exports to US accelerated to 17% yoy, but some strength likely reflected front-loading ahead of higher US tariffs, making it harder to extrapolate July's pace into coming months.

- Overall, trade data remain supportive for China's growth, but increasing reliance on high-tech exports and mounting protectionism create risks for sustainability of export-led momentum.

Fed’s Musalem: It’s Okay to Surprise Markets With a Rate Move

St. Louis Fed President Alberto Musalem said he favored raising interest rates by 25bps at last week's FOMC meeting, arguing that acting gradually now would be preferable to risking more aggressive tightening later. Musalem is not a voting member of FOMC this year, so his preference was not among the three formal dissents against the decision to hold rates steady. Speaking in Brazil on Thursday, Musalem said inflation is likely to remain too high relative to Fed's 2% target over coming year if policy stays unchanged. "Earlier gradual incremental interest rate increases are preferable, less disruptive, less costly than potentially later, more abrupt interest rate changes," he said.

Musalem also pushed back against idea that Fed should hesitate simply because financial markets are not positioned for higher rates. While acknowledging that he closely monitors market signals, he said policymakers should follow their economic assessment regardless of prevailing expectations. "If you think that now is the time to change policy in whatever direction, you ought to change that policy, irrespective of what's priced into markets," Musalem said, adding that "there are times or moments when it's okay to surprise the market." His comments are particularly relevant as investors have moved toward pricing a September hold following falling oil prices and optimism over reopening Strait of Hormuz.

Musalem's broader argument was that Fed has little reason to tolerate elevated inflation in hope that stronger productivity eventually resolves price pressures. "It is crucial that monetary policy put a meaningful restraint on underlying inflation, rather than tolerating somewhat higher inflation today to pursue productivity growth tomorrow," he said, warning there is "fertile ground for inflation expectations to potentially become unanchored." With financial conditions supportive, asset prices elevated and labor market characterized by "solid payroll growth," Musalem sees room to tighten policy before inflation becomes harder to contain. His stance therefore adds to hawkish pressure inside Fed just as markets increasingly bet that September will bring another hold.

Key Takeaways

- St. Louis Fed President Alberto Musalem favored a 25bps rate hike at last week's FOMC meeting, arguing current policy may not be restrictive enough to bring inflation sustainably back to 2%.

- Musalem favors earlier, gradual tightening, saying incremental increases now would be "less disruptive" and "less costly" than potentially larger rate moves later.

- He stressed that market pricing should not dictate Fed decisions, saying policymakers should act when warranted "irrespective of what's priced into markets."

- Musalem added that "there are times or moments when it's okay to surprise the market," a notable warning as investors increasingly lean toward a September hold.

- He rejected tolerating above-target inflation in hope that future productivity gains will solve the problem, warning such an approach could put Fed credibility and anchored inflation expectations at risk.

- With economy resilient, financial conditions supportive and labor market stable, Musalem sees room for Fed to focus on inflation rather than wait for clearer economic weakness before tightening.

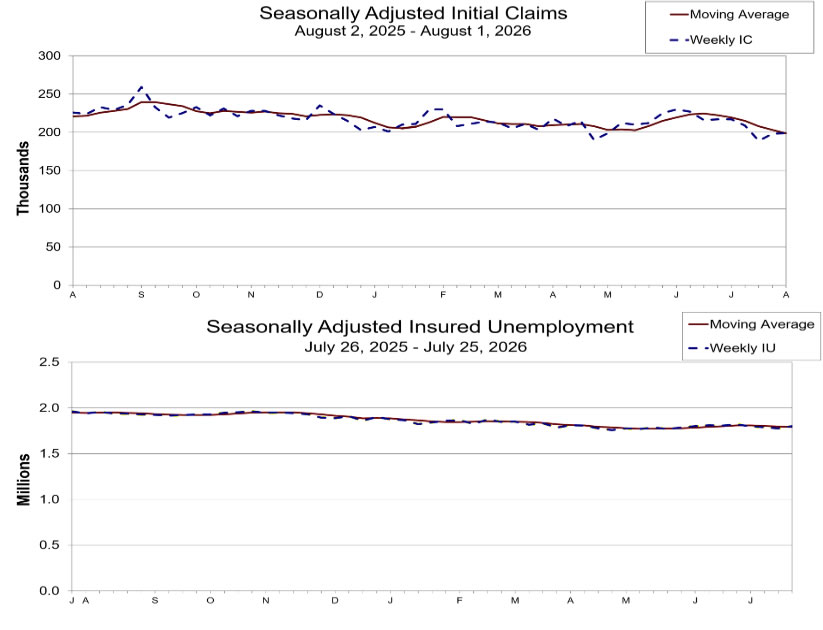

US Initial Jobless Claims Edge Up to 119k, but Layoffs Remain Limited

US initial jobless claims remained near historically low levels in the latest week, reinforcing the view that layoffs continue to be limited despite signs of slower hiring elsewhere in the labor market. Initial claims rose by just 1,000 to 199,000 in the week ended August 1, slightly below market expectations of 203,000. The previous week's figure was revised up modestly to 198,000, while the four-week moving average declined to 198,750, suggesting underlying labor market conditions remain broadly stable.

Continuing claims painted a slightly softer picture, rising 24,000 to 1.801 million in the week ended July 25, although the insured unemployment rate held steady at 1.2%. The increase suggests unemployed workers may be taking slightly longer to find new jobs, but the overall level remains consistent with a labor market that is cooling gradually rather than weakening abruptly.

The latest figures fit with other recent labor market indicators showing a "low-hire, low-fire" environment. While ADP employment and the ISM Services Employment Index pointed to softer hiring momentum, weekly claims continue to show employers are reluctant to shed workers.

Data Summary

| Indicator | Latest | Previous |

|---|---|---|

| Initial Jobless Claims | 199K | 198K |

| Market Expectation | 203K | — |

| 4-Week Average | 198.8K | 203.3K |

| Continuing Claims | 1.801M | 1.777M |

| 4-Week Avg. Continuing Claims | 1.791M | 1.796M |

| Insured Unemployment Rate | 1.2% | 1.2% |

Key Takeaways

- Initial jobless claims edged up to 199K, remaining below the 200K mark and beating expectations of 203K, indicating layoffs remain historically low.

- The four-week moving average fell to 198.8K, suggesting there has been no meaningful deterioration in underlying labor market conditions.

- Continuing claims rose by 24K to 1.801 million, hinting that unemployed workers may be taking slightly longer to secure new jobs.

- The insured unemployment rate held steady at 1.2%, reinforcing the picture of a labor market that remains fundamentally resilient.

- The report supports the recent "low-hire, low-fire" narrative emerging from JOLTS, ADP and Fed officials—hiring has slowed, but employers are generally reluctant to lay off workers.