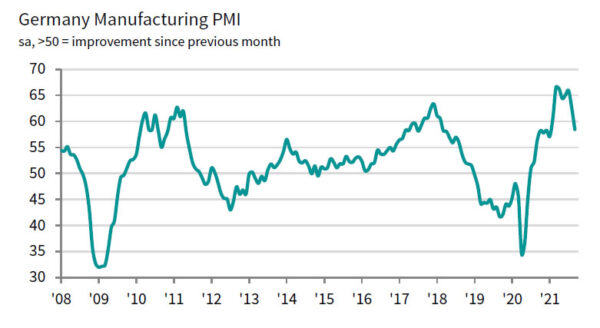

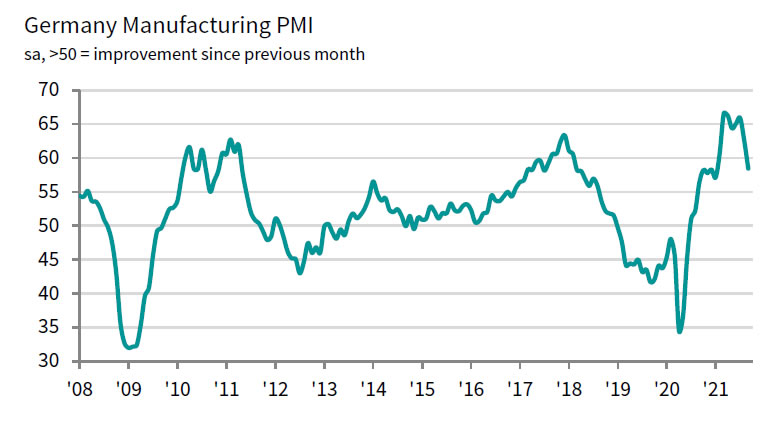

Germany PMI Manufacturing was finalized at 58.4 in September, down from August’s 62.6. Markit said output and new orders rose at slowest rate in 15 months. Input shortages continued to push up costs, leading to higher output prices. Pace of job creation slowed as growth expectations dipped to 13-month low.

Phil Smith, Associate Economics Director at IHS Markit, said:

“At 58.4, the latest headline PMI reading gives a false impression as to the manufacturing sector’s current performance, with the suppliers’ delivery times component continuing to distort the picture. Trends in output and new orders are weaker than the headline number suggests.

“The unprecedented supply shortages we’ve seen in recent months have been holding back production levels for some time now, and we’re increasingly seeing this disruption feed back up the supply chain and resulting in reduced demand for intermediate goods as orders are either postponed or cancelled. As a result, overall growth in new orders dropped to a 15-month low in September.

“At the same time, supply bottlenecks continue to drive up input costs and, in turn, put pressure on manufacturers to raise prices, which is acting as another headwind to growth. The rate of input price inflation looks like it might have peaked but is still running close to the fastest in the survey’s history, leading to near-record numbers of goods producers raising prices.

“Manufacturers’ optimism towards the outlook is steadily ebbing away, down in September to its lowest for 13 months, with many firms concerned that supply shortages will persist into next year.”

Full release here.

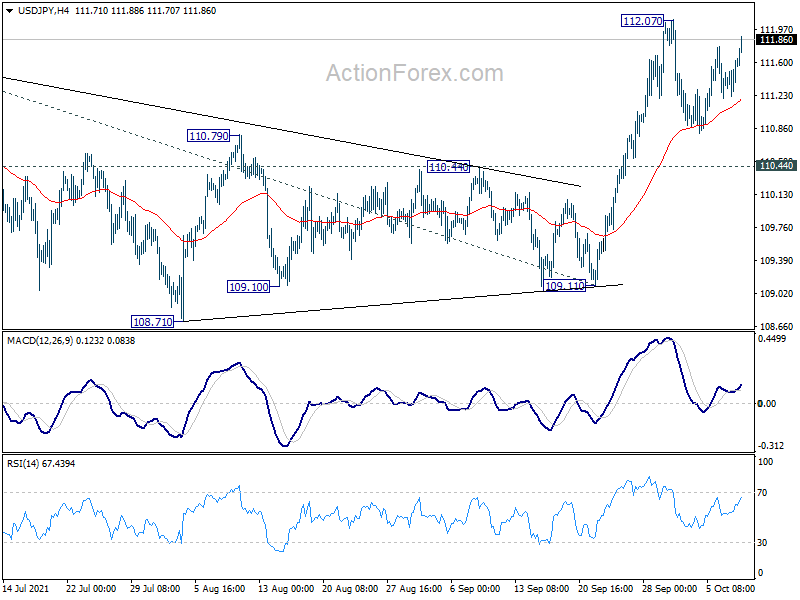

Dollar index staying bearish, FOMC previews

Fed is widely expected to keep monetary policy unchanged today. Despite recent resurgence in coronavirus infections and the economic impact, roll-out of more fiscal stimulus and positive vaccination progress would keep policy makers in a wait-and-see mode. Federal funds rate will be held at 0-0.25% while asset purchase will continue at current pace of USD 120B per month. Chair Jerome Powell would likely re-emphasize that Fed is in no position to even start discussing tapering of quantitative easing yet.

Here are some suggested readings:

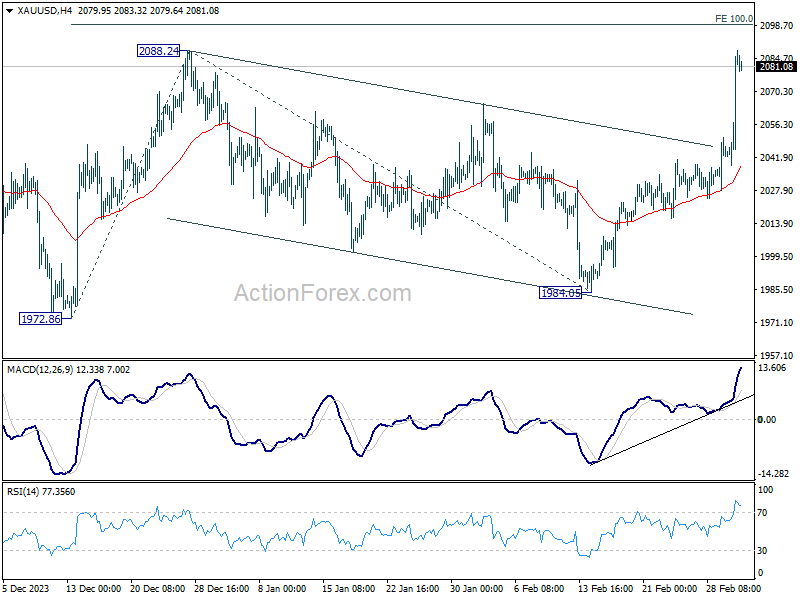

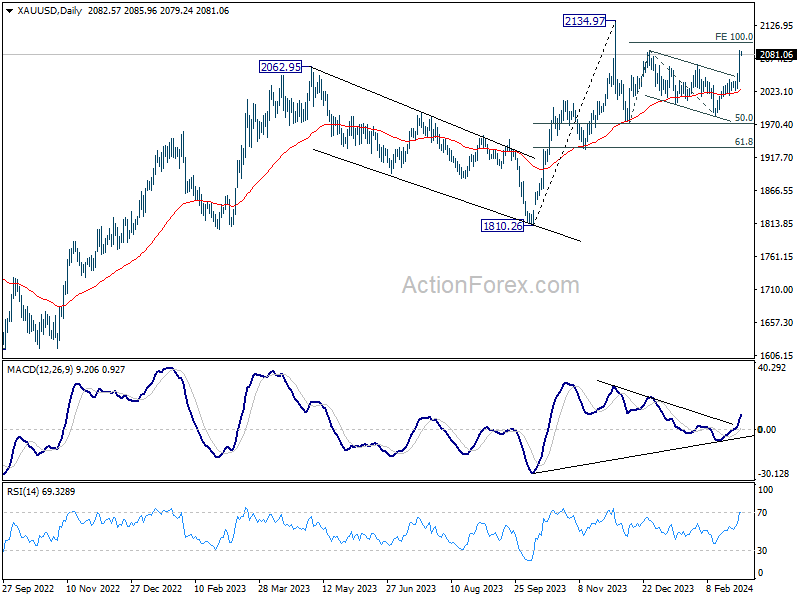

Dollar Index is staying in range trading for now, reflecting the consolidation in most Dollar pairs. DXY is held below falling 55 day EMA, as well as 91.01 near term resistance, keeping outlook bearish. The down trend from 102.99 would more likely extend lower than not. Though, downside momentum has been clearly diminishing as seen in daily MACD. Hence, we’d expect strong support from 61.8% projection of 102.99 to 91.74 from 94.74 at 87.88 to contain downside and bring sustainable rebound, even in case of another down move.