Live Comments

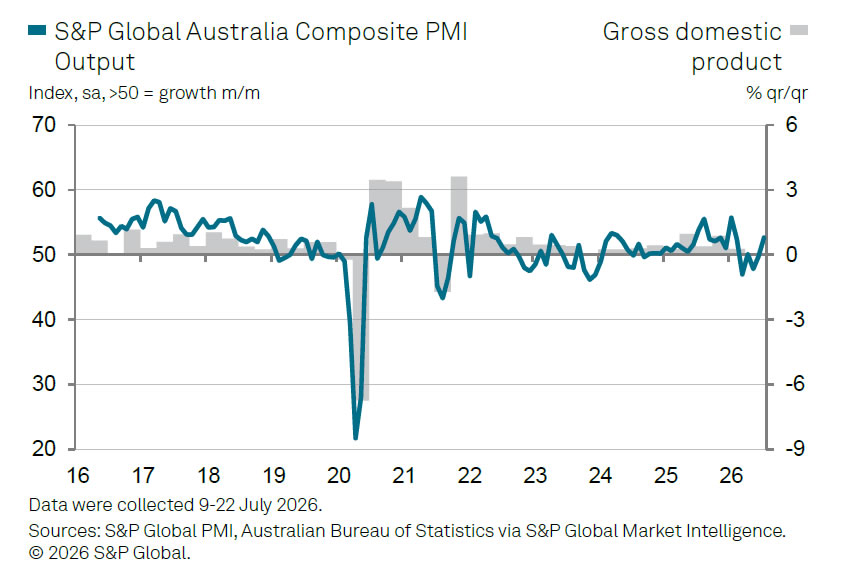

Australia PMI Composite Hits 2026 High at 52.6 as Domestic Demand Rebounds

Australia's private sector gained momentum in July, with the S&P Global Flash Composite PMI rising from 50.4 to 52.6, its highest reading since the start of the year. The improvement was driven primarily by the services sector, where the Services PMI Business Activity Index climbed from 50.5 to 53.0, while Manufacturing PMI edged up from 51.5 to 51.7. The data point to a firmer pace of economic expansion at the start of the third quarter, with overall business activity growing at a rate above the survey's long-run average.

A notable feature of the report was the improvement in demand. New orders increased for the first time in five months, indicating that domestic demand is beginning to recover despite continued weakness in overseas markets. While services remained the main engine of growth, manufacturing also showed signs of stabilizing. Factory output remained slightly below the expansion threshold at 49.9, but improved from June's 49.5, suggesting the sector's downturn is gradually easing rather than deepening.

The survey also offered encouraging news on inflation. Input cost pressures continued to moderate, providing further evidence that disinflation remains on track even as demand strengthens. At the same time, firms became more willing to protect profit margins as business conditions improved. Looking ahead, however, businesses remained cautious about the outlook, reflecting uncertainty surrounding the global economy and trade environment.

Economic Data

| Indicator | Actual | Previous |

|---|---|---|

| Flash Composite PMI Output Index (Jul) | 52.6 | 50.4 |

| Flash Services PMI Business Activity Index (Jul) | 53.0 | 50.5 |

| Flash Manufacturing PMI (Jul) | 51.7 | 51.5 |

| Flash Manufacturing PMI Output Index (Jul) | 49.9 | 49.5 |

Key Takeaways

- Private sector growth accelerated: Australia's Flash Composite PMI rose from 50.4 to 52.6, the strongest reading of 2026 and above the survey's long-run average, signaling a firmer pace of economic expansion.

- Services remained the growth engine: The Services PMI Business Activity Index climbed from 50.5 to 53.0, accounting for most of the improvement in overall business activity.

- Manufacturing continued to stabilize: The headline Manufacturing PMI edged up from 51.5 to 51.7, while the Manufacturing Output Index improved from 49.5 to 49.9, suggesting factory activity is nearing stabilization despite remaining slightly below the expansion threshold.

- Domestic demand improved: New orders increased for the first time in five months, indicating a recovery in domestic demand even as export sales weakened further.

- Disinflation trend continued: Businesses reported easing input cost pressures, providing further evidence that inflationary pressures are moderating despite stronger activity.

- Margin protection improved: More stable demand enabled firms to pass through costs more effectively and better protect profitability.

- Outlook remained cautious: Despite stronger current conditions, businesses continued to express uncertainty about the year ahead, reflecting concerns over the global economic and trade environment.

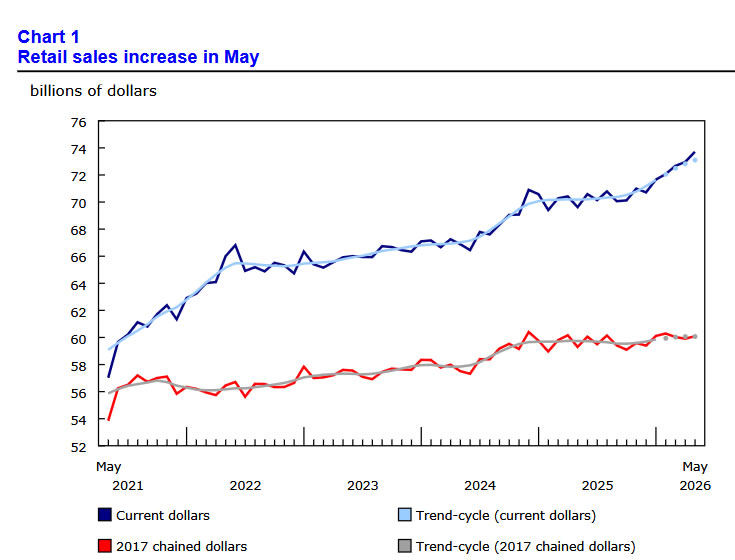

Canada Retail Sales Rise 1.0% in May, June Momentum Seen Continuing

Canada's retail sales rose 1.0% mom to CAD 73.7B in May, marking a broad-based improvement in consumer spending as all nine retail subsectors posted gains. The increase was led by gasoline stations and fuel vendors, reflecting higher fuel prices, while motor vehicle and parts dealers also contributed with a second consecutive monthly increase. Excluding the more volatile gasoline and auto categories, core retail sales still advanced a solid 0.9%, suggesting household demand remained resilient beyond energy-related spending.

The composition of the report painted a slightly more nuanced picture. Sales at gasoline stations and fuel vendors rose 3.1% in value terms, but volumes fell -2.7%, indicating that higher prices rather than stronger demand drove much of the increase. Meanwhile, motor vehicle and parts dealers recorded a 0.7% gain, with new car dealers leading the advance. Overall retail sales volumes rose 0.3%, pointing to modest but positive growth in the quantity of goods purchased after adjusting for price changes.

The outlook also remained constructive. Statistics Canada's advance estimate suggests retail sales increased a further 0.4% in June, indicating consumer spending continued to expand heading into the second quarter's close.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Retail Sales (May, m/m) | +1.0% | +0.7% | +0.3% |

| Core Retail Sales (May, m/m) | +0.9% | — | +0.2% |

| Retail Sales Volume (May, m/m) | +0.3% | — | +0.5% |

| Advance Estimate – Retail Sales (Jun, m/m) | +0.4% | — | — |

Key Takeaways

- Broad-based strength: Retail sales rose 1.0% m/m, with all nine retail subsectors recording gains, indicating consumer spending remained resilient.

- Underlying demand improved: Core retail sales, excluding autos and gasoline, increased 0.9%, showing the strength extended beyond volatile sectors.

- Energy prices boosted headline sales: Sales at gasoline stations rose 3.1%, but volumes fell -2.7%, indicating higher fuel prices rather than stronger demand drove much of the increase.

- Real spending still expanded: Overall retail sales volumes increased 0.3%, suggesting consumers purchased more goods even after adjusting for price effects.

- Auto sector remained supportive: Motor vehicle and parts dealers posted a second consecutive monthly gain, led by higher new vehicle sales.

- Momentum carried into June: Statistics Canada's advance estimate points to another 0.4% increase in June retail sales, indicating household spending remained on a firm footing heading into Q2's close.

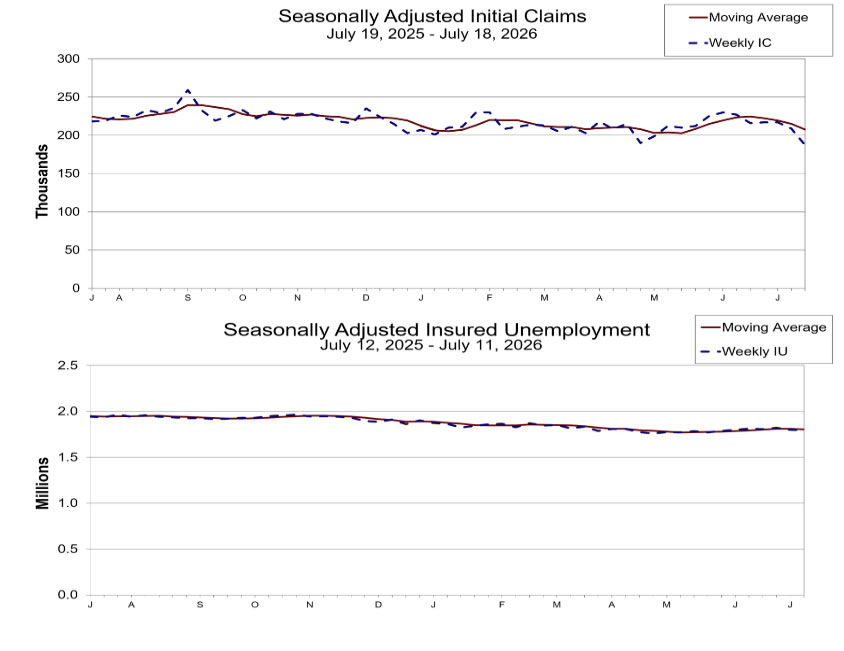

US Jobless Claims Fall Sharply to 187k vs exp 212k

US initial jobless claims fell sharply by -22k to 187k in the week ended July 18, well below expectations of 212k. The prior week's figure was revised slightly higher to 209k from 208k, while the four-week moving average declined by -7.25k to 207.5k. The data point to continued resilience in the labor market despite mounting uncertainty surrounding energy prices and global geopolitical tensions.

The improvement was also reflected in continuing claims, which edged down by -2k to 1.796m in the week ended July 11, while the insured unemployment rate held steady at 1.2%. Although the decline was modest, it suggests workers who lose their jobs are still finding new employment relatively quickly, reinforcing the view that labor market conditions remain tight rather than deteriorating. The four-week average of continuing claims also fell, indicating that broader labor market momentum has remained intact.

Economic Data

| Indicator | Actual | Expected | Previous |

|---|---|---|---|

| Initial Jobless Claims (Jul 18) | 187K | 212K | 209K |

| 4-Week Average | 207.5K | — | 214.75K |

| Continuing Claims (Jul 11) | 1.796M | — | 1.798M |

| Insured Unemployment Rate | 1.2% | — | 1.2% |