Sample Category Title

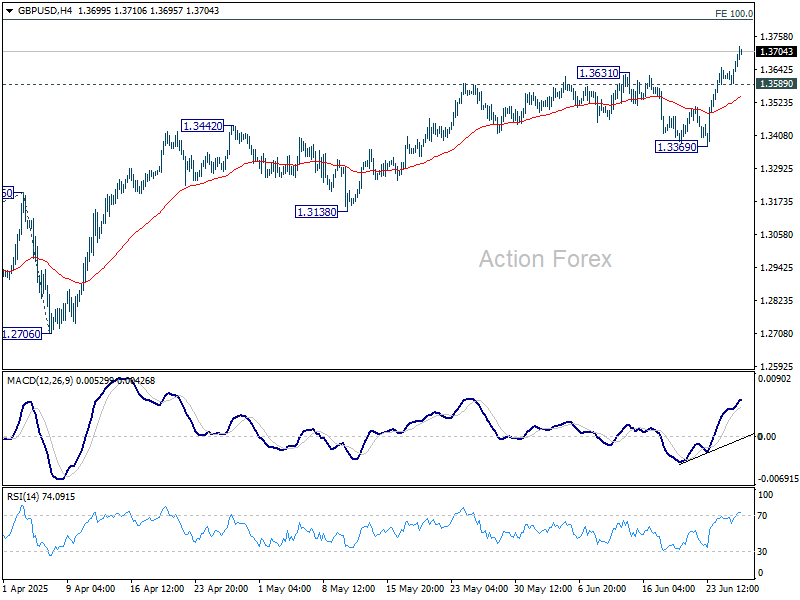

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3613; (P) 1.3642; (R1) 1.3694; More...

GBP/USD's rally continues today and intraday bias stays on the upside. Current rise from 1.2099 should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813 next. On the downside, below 1.3589 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.3369 support to bring another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

Dollar Slides to Multi-Year Lows Against Euro, Pound on NATO Spending Boost

Dollar weakness deepened in Asian session, with the greenback falling to multi-year lows against both Euro and Sterling. For now, downside pressure remains concentrated against European majors. The latest catalyst is a show of fiscal resolve from NATO allies, who agreed to more than double their defense spending target to 5% of GDP by 2035, seen as a long-term fiscal and industrial boost to Europe’s economy and security posture.

The NATO decision breaks down into 3.5% spending on traditional military capabilities and 1.5% on broader resilience like cyber and infrastructure. While symbolic in the short term, the commitment highlights the region’s renewed strategic coherence and investment direction—drawing investor confidence at a time when the US outlook is clouded by trade policy and inflation uncertainty.

Meanwhile, Dollar has now fully reversed its recent safe-haven gains after last week's escalation in the Middle East. With the Israel-Iran ceasefire holding, even amid minor violations, markets are turning back to broader US vulnerabilities, especially fiscal risks, tariffs, and the greenback's trustworthiness as a haven asset.

Monetary policy divergence is also weighing on Dollar. While ECB may be near the end of its cycle, Fed is still expected to resume cuts later this year. Markets are increasingly convinced that a September cut is likely. And after all, Fed’s latest dot plot reflects two cuts this year, with the 2025 median rate at 3.9%,

In the currency markets, Dollar is back as the worst performer of the week, followed by the Loonie and Yen. European currencies are clearly benefiting, with Sterling leading gains, followed by Swiss franc and Euro. Aussie and Kiwi are stuck in the middle.

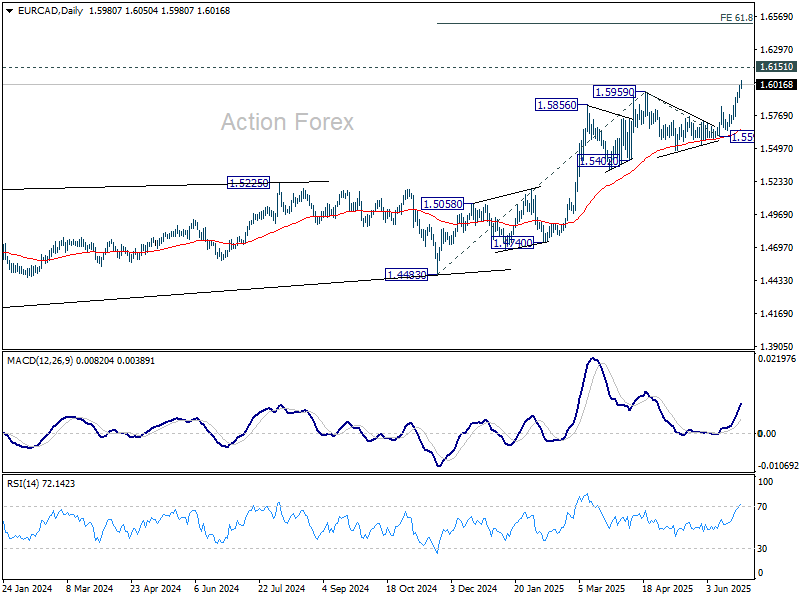

Technically, EUR/CAD's strong break of 1.5959 resistance this week confirms long term up trend resistance. Based on current momentum, there shouldn't be much difficulty in breaking through 1.6151 long term resistance (2018 higher). Next near term target is 61.8% orojection of 1.4483 to 1.5959 from 1.5598 at 1.6510.

In Asia, at the time of writing, Nikkei is up 1.49%. Hong Kong HSI is down -0.65%. China Shanghai SSE is up 0.10%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is up 0.014 at 1.418. Overnight, DOW fell -0.25%. S&P 500 fell -0.00%. NASDAQ rose 0.31%. 10-year yield closed flat at 4.293.

Fed's Powell: No modern precedent for Trump's tariff, must proceed carefully

Fed Chair Jerome Powell defended the central bank’s cautious stance on interest rates during day two of his Congressional testimony, citing significant uncertainty around the inflationary impact of tariffs. While Powell acknowledged tariff-driven price hikes could ultimately be transitory, he said Fed must prepare for the possibility that inflation proves more persistent. “As the people who are supposed to keep stable prices, we need to manage that risk,” Powell emphasized.

Powell emphasized that the Fed is operating in largely uncharted territory, warning that the magnitude of potential new tariffs dwarfs those imposed during Trump’s first term, and those earlier measures came when inflation was subdued. “There is not a modern precedent,” he said, cautioning against prematurely adjusting policy without a clearer picture of the economic impact.

“If it comes in quickly and it is over and done, then yes, very likely it is a one-time thing,” he said of tariff inflation. But if the Fed misjudges the situation, “people will pay the cost for a long time.”

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3613; (P) 1.3642; (R1) 1.3694; More...

GBP/USD's rally continues today and intraday bias stays on the upside. Current rise from 1.2099 should target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813 next. On the downside, below 1.3589 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained above 1.3369 support to bring another rally.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

Bypassing Powell

Trump denied earlier intelligence reports suggesting that the US strikes on Iranian nuclear sites caused only limited damage. On the contrary, he claimed the operation was a historic success and even declared the war over — ‘except that it could maybe restart soon.’ Still, the US and Iran are scheduled to meet for diplomatic talks in Iran this weekend, which appears to be a signal that Trump genuinely wants to de-escalate tensions in the Middle East.

US crude is consolidating near its 100-DMA, just above the critical $65pb level — a major Fibonacci retracement of this year’s decline. This line distinguishes between a continuation of the latest rally and a return to the bearish trend that has been building since the start of the year.

But geopolitics aside, the supply-demand dynamics continue to favour softer oil prices. Global demand prospects are weakening due to trade uncertainties, while supply is ample thanks to faster production restoration from OPEC+. Russia said yesterday it’s open to another output hike at the next OPEC+ meeting due on July 6th. So, if Middle East tensions are truly done and dusted, oil is more likely than not to fall back toward, or even below, the $60pb level.

That’s good news for the Federal Reserve’s (Fed) inflation battle — but unfortunately, it’s not the only risk factor. The real threat to US inflation now is tariffs, and there’s been little progress on that front. Fed Chair Powell keeps insisting the US doesn’t need to rush into rate cuts until there’s more clarity on trade policy. But no one listens — even less so now, as there’s growing concern that Trump could prematurely appoint the next Fed Chair to sideline Powell, who has resisted rate cuts. A new Trump-approved Chair would likely be more willing to cut rates, pleasing Trump, who insists the U.S has no inflation problem. Technically, that’s true — for now. But it could, and that’s the problem.

That said, don’t forget: cutting rates doesn’t guarantee yields will fall. If markets perceive a policy mistake, yields could disconnect from the policy rate — that’s called a loss of credibility. So lower rates — if not justified — aren’t necessarily good news for sovereign bonds. US debt is exploding, and Trump’s spending cuts on social programs don’t come close to offsetting the tax benefits granted to the wealthiest Americans. Debt will rise, and the US must ensure global markets absorb this additional issuance — essentially, to keep funding a policy that makes rich Americans richer. The problem? Investors are backing off. There’s growing appetite for ex-US sovereign bonds, especially in Europe.

In short, Trump has power to do a lot, but he still needs funding. Investors will have the final say.

Dollar pain, equity gain

The US dollar remains heavily unloved. The dollar index continues to slide, despite Powell’s cautiously hawkish tone. But a weaker dollar supports major US equities, as about 40% of S&P 500 revenues come from abroad, including 10–12% from Europe and around 8–10% from Asia. As the dollar weakens (or other currencies strengthen), overseas revenues translate into higher dollar earnings for S&P 500 companies.

Still, a recent Bloomberg Intelligence analysis — factoring in Treasury yields, earnings, and the equity risk premium — warns that S&P 500 earnings would need to rise by as much as 30% over the next year for current valuations to be considered ‘fair.’ Is that possible? It seems stretched for the S&P 493 — but perhaps not for the AI leaders.

Micron just announced stronger-than-expected revenue and gave an upbeat forecast for the current quarter, driven by AI demand. Its high-bandwidth memory chips — essential for running AI tools — are selling like petits pains, as the French say. The company is betting on rising demand for increasingly complex chips to fuel further growth. Micron shares have doubled since their April dip, though they remain below last summer’s highs.

Elsewhere, Nvidia hit a fresh record yesterday. CEO Jensen Huang is now looking beyond both the US and AI — toward robotics — to expand market share. The Middle East and Europe may become the next big markets to help fill the gap left by Trump’s export restrictions to China.

But stepping back to the S&P 500 more broadly, trade risks loom and could hurt sentiment in the short run.

On the geopolitical front, Trump is now furious with Spain, which declined to raise its military budget to 5% of GDP, unlike several other NATO members this week. European stocks fell yesterday, with the Spanish IBEX underperforming. Meanwhile, defense stocks rallied nearly 2% after Babcock announced its first-ever buyback — a move that confirms the boom in European military spending. The company also raised its dividend and boosted medium-term guidance, sending the stock up more than 10%.

The EUR/USD traded past 1.17, and Cable climbed above 1.37. The next natural targets are 1.20 for euro bulls, and 1.40 for Cable. Pullbacks may offer attractive dip-buying opportunities — not because the European economies are particularly strong, but because spending plans are solidly funded… and the dollar is weakening.

RBA Cut Likely in July, But No Shoo-in

July RBA cash rate cut now expected, moved forward from August, but this is no shoo-in.

- We now expect the next RBA rate cut to be in July rather than August, but this is not the shoo-in the market seems to think it is.

- The RBA has sometimes defied market pricing if offshore risks are being over-weighted, but now is the time to bring forward a move it knows it will likely make soon anyway.

- The RBA’s outlook is still shaped by concerns about the tight labour market, slow economy-wide productivity growth and the pricing implications of recovering demand. Thus we expect non-committal, even grudging, language in the post-meeting communication.

- We continue to expect a terminal rate of 2.85% (three further cuts after the upcoming one), but the RBA is unlikely to give any forward guidance in that vein.

The next RBA rate cut is now expected to be in July rather than August, but this is not the shoo-in that markets seem to think it is. Yes, the May monthly CPI indicator came in below even the low number that we expected. That helps bring forward inflation’s return to the 2.5% target midpoint and keep it there, which is what the RBA is trying to achieve. The detail around housing and market services was also a promising sign that core inflation is seeing a sustained moderation. But the June quarterly inflation numbers are still likely to print on the high side, so some caution on the inflation outlook is likely and warranted.

One month’s data ordinarily wouldn’t – and shouldn’t – determine the RBA’s forecast and decision-making. We also note the Governor’s particular caution about the monthly CPI indicator expressed in the May post-meeting media conference. This was an explicit steer that the RBA’s thinking in May was that it did not plan to do back-to-back cuts but would wait for the quarterly CPI ahead of its August meeting. And they still might do that, but it is harder to justify now.

Moving more quickly than the ‘cautious and predictable’ path flagged in May implies that the RBA’s forecasts need to shift. The May SMP showed a forecast for trimmed mean inflation flat as a pancake at 2.6% as far as the forecasts went, never touching the 2.5% midpoint. No model produces a forecast like that. It was more of a message than a true forecast.

That message was that they are still worried about domestic inflation pressures. They think the labour market is still too tight – and productivity growth too weak – to move quickly. Last week’s labour force and today’s job vacancies data would have reinforced this view. Neither is the RBA planning to bring monetary policy to an expansionary stance – this point was also explicitly mentioned in the Minutes.

That 2.6% forecast was the RBA saying it thought it would end up cutting by less than the market was pricing in May, the path on which the RBA’s forecasts were based. Discussion of a 50 basis point cut at the May meeting was just that – discussion. Recall that the Board also discussed keeping the cash rate on hold.

We expect that the inflation evidence will overtake the RBA’s thesis of domestic tightness over time. But we do not think they are going to start singing from an entirely different song sheet just yet. It would be an extraordinary pivot to let go of an analysis of the economy that it has held on to for so long – even in the face of widespread criticism – without any prior communication. And it would be inconsistent with the RBA’s recent pattern of taking a couple of quarters and a bit of counter-arguing before it comes back from a view that is well outside market consensus. (Though with more than a week to go until the next Board meeting still, perhaps an event will be rustled up beforehand.)

Rather, what we are about to see is an RBA that was planning to cut rates soon anyway deciding it may as well get on with it rather than make a contestable argument for further delay.

Note that this is not just about validating market pricing. The RBA is not the Fed: it is less worried about ‘surprising the market’, as we saw in May 2023. If it really did not think it should cut the cash rate soon, it would not be swayed by the market. Indeed, the RBA has form for not cutting rates when markets are pricing a cut, especially if market pricing is keying off assumed negative implications of shocks from offshore that the RBA thinks are overdone. There is an element of that situation currently, a point alluded to in the Deputy Governor’s remarks in late May.

In short, only because the RBA sees itself on a path of cutting rates soon will it decide to validate market pricing and get on with the next cut at its July meeting. But this is not the timing it previously thought it would be on. Given the lingering uncertainties and the RBA’s concerns about a tight labour market, expect its post-meeting language to be non-committal, even a little grudging about the decision to cut.

We still think there are three further cuts after the next one (terminal rate 2.85%), but the timing will depend on the RBA’s post-meeting tone. As flagged when we first added the third and fourth cuts to our call, the risks are that they come sooner than February and May next year.

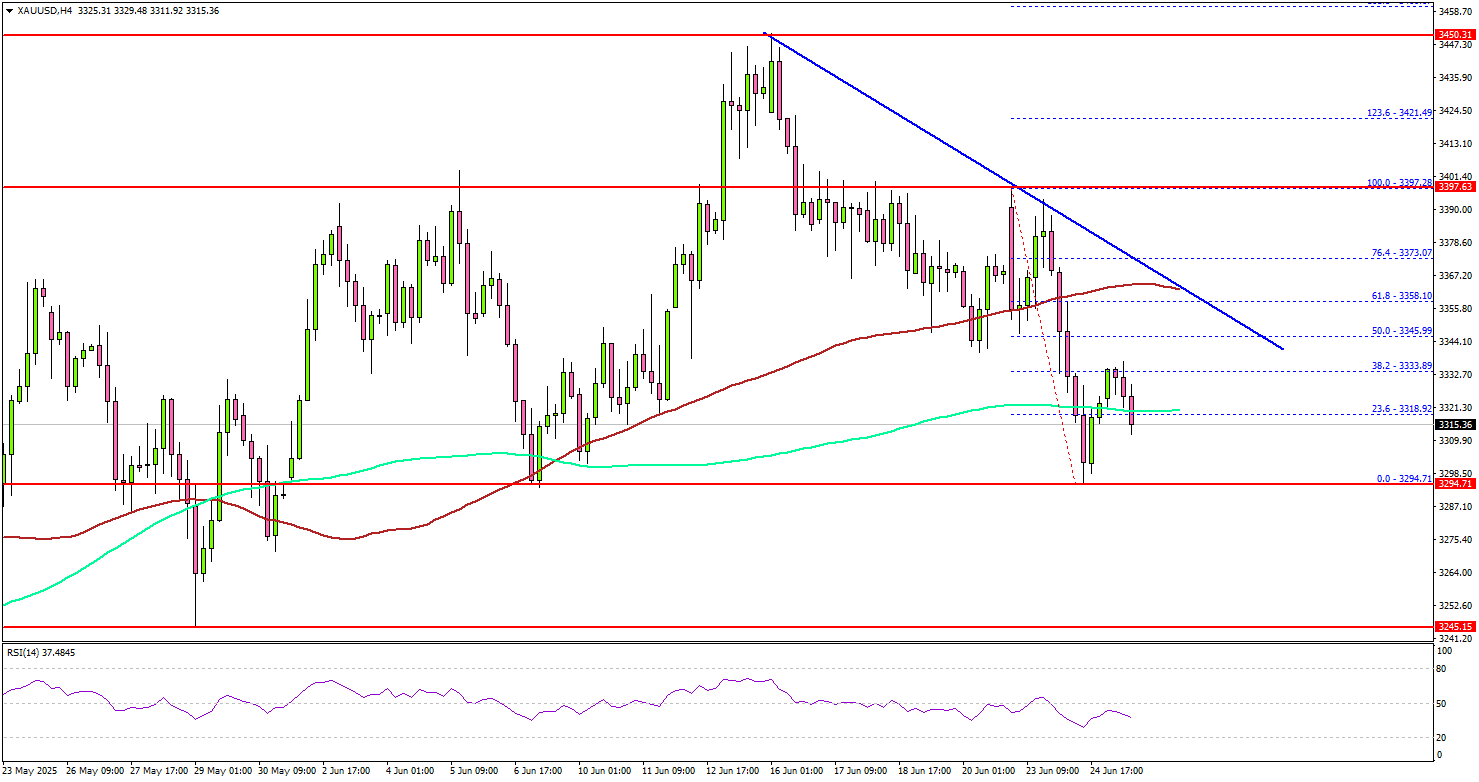

Gold Slips Lower — Downside Risk Builds Below Key Support

Key Highlights

- Gold started a fresh decline from the $3,450 resistance.

- A key bearish trend line is forming with resistance at $3,360 on the 4-hour chart.

- WTI Crude Oil prices dipped sharply below the $68.00 support.

- The US GDP could contract by 0.2% in Q1 2025.

Gold Price Technical Analysis

Gold prices failed to extend gains above $3,450 and reacted to the downside. There was a steady decline below the $3,400 and $3,380 support levels.

The 4-hour chart of XAU/USD indicates that the price settled below the $3,350 level and the 100 Simple Moving Average (red, 4 hours). The decline was such that the price spiked below the $3,300 level and the 200 Simple Moving Average (green, 4 hours).

On the downside, initial support is near the $3,295 level. The first key support is $3,275. The next major support is near the $3,450 level. The main support is now $3,230. A downside break below the $3,230 support might call for more downsides. The next major support is near the $3,200 level.

On the upside, immediate resistance is near the $3,335 level. The next major resistance sits near the $3,350 level. The main barrier could be $3,360.

There is also a key bearish trend line forming with resistance at $3,360 on the same chart. A clear move above the $3,360 resistance could open the doors for more upsides. The next major resistance could be $3,400, above which the price could rally toward the milestone level of $3,450.

Looking at WTI Crude Oil, the bears took control and were able to push the price below the $68.00 support zone.

Economic Releases to Watch Today

- US Initial Jobless Claims - Forecast 245K, versus 245K previous.

- US Gross Domestic Product for Q1 2025 – Forecast -0.2% versus previous -0.2%.

- US Durable Goods Orders for May 2025 – Forecast +8.5% versus -6.3% previous.

Fed’s Powell: No modern precedent for Trump’s tariff, must proceed carefully

Fed Chair Jerome Powell defended the central bank’s cautious stance on interest rates during day two of his Congressional testimony, citing significant uncertainty around the inflationary impact of tariffs. While Powell acknowledged tariff-driven price hikes could ultimately be transitory, he said Fed must prepare for the possibility that inflation proves more persistent. “As the people who are supposed to keep stable prices, we need to manage that risk,” Powell emphasized.

Powell emphasized that the Fed is operating in largely uncharted territory, warning that the magnitude of potential new tariffs dwarfs those imposed during Trump’s first term, and those earlier measures came when inflation was subdued. “There is not a modern precedent,” he said, cautioning against prematurely adjusting policy without a clearer picture of the economic impact.

“If it comes in quickly and it is over and done, then yes, very likely it is a one-time thing,” he said of tariff inflation. But if the Fed misjudges the situation, “people will pay the cost for a long time.”

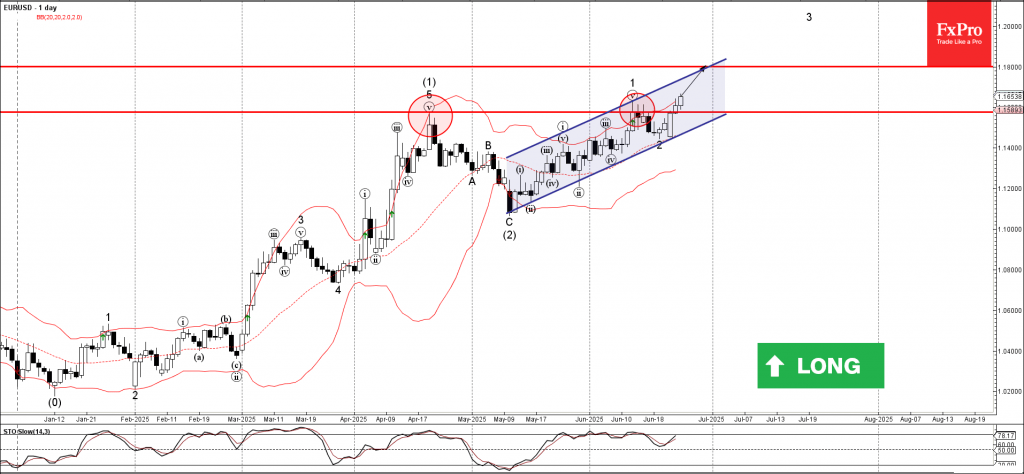

EURUSD Wave Analysis

EURUSD: ⬆️ Buy

- EURUSD broke resistance level 1.1575

- Likely to rise to resistance level 1.1800

EURUSD currency pair recently broke the resistance level 1.1575 , which is the former monthly high from the middle of April.

The breakout of the resistance level 1.1575 continues the active short-term impulse wave 3 of the intermediate impulse wave (3) from the start of May.

Given the strong daily uptrend, EURUSD currency pair can be expected to rise to the next resistance level 1.1800, which intersects with the daily up channel from May.

GBPUSD Wave Analysis

GBPUSD: ⬆️ Buy

- GBPUSD broke resistance level 1.3590

- Likely to rise to resistance level 1.3880

GBPUSD currency pair recently broke the resistance level 1.3590, which is the upper border of the narrow sideways price range inside which the price has been moving from May.

The breakout of the resistance level 1.3590 accelerated the active intermediate impulse wave (3).

Given the clear daily uptrend and the strong US dollar sales seen today, GBPUSD currency pair can be expected to rise to the next resistance level 1.3880.

Fed’s Collins: “Active patience” warranted as tariff uncertainty clouds outlook

Boston Fed President Susan Collins expressed her preference for what she termed an “actively patient” approach to monetary policy, saying it remains appropriate amid rising uncertainty. Speaking today, Collins pointed to the fluidity in tariff developments and broader government policy shifts, which she said “validate the careful approach” Fed has taken so far in 2025. While she still expects gradual policy normalization to resume later this year, she warned her view "could change significantly as events unfold".

Collins emphasized that much hinges on the nature of the “price shock” driven by tariffs. If price pressures fade quickly without unanchoring inflation expectations, and if the hit to real activity remains limited, she said it could support easing later in the year. However, if those conditions are not met, policy adjustments may be delayed.

For now, Collins views current monetary policy as “modestly restrictive,” and well-positioned to deal with a range of potential outcomes.