Sample Category Title

May CPI Preview: Test of Tariffs

Summary

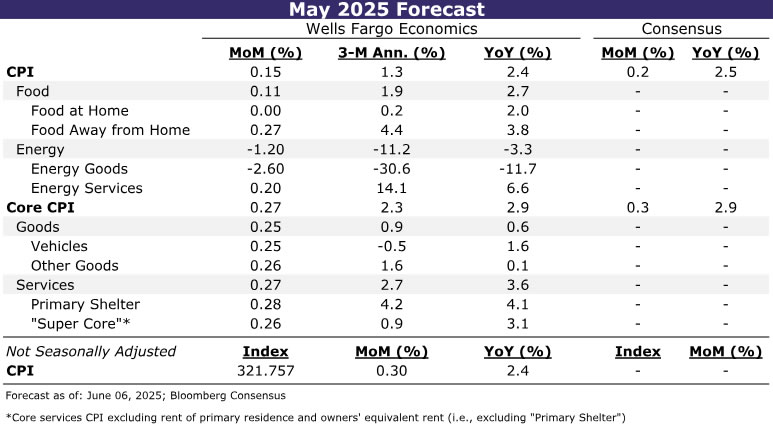

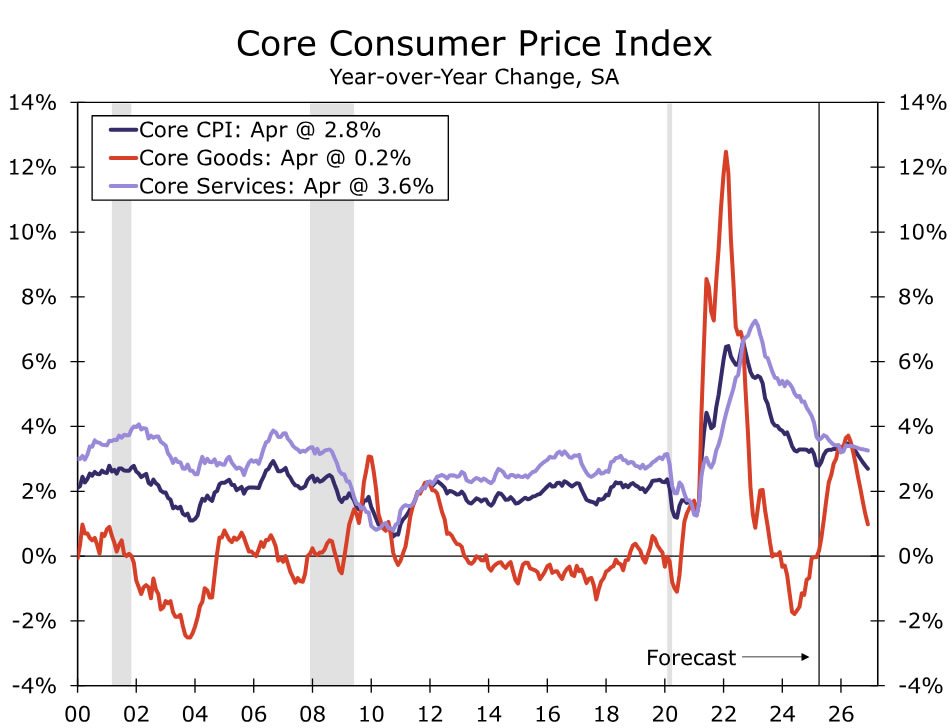

May's CPI report will be an important test of the speed and magnitude to which higher tariff rates are being passed along to the consumer. We expect to see only a moderate advance in headline CPI (0.15%) in May as gasoline prices fell on a seasonally adjusted basis and food inflation appeared tame. But excluding food and energy, inflation looks to have firmed on the back of higher goods prices. We estimate the core CPI rose 0.27% in May.

Front-loading of inventories and efforts to avoid alienating customers—especially as it remains to be seen where tariff rates eventually land—are mitigating the early effects of higher import duties on consumer prices. That said, we expect to see the inflationary effects ramp up more in the coming months as the higher tariff environment persists. We estimate core CPI will advance at an average monthly pace of 0.30% in the second half of the year, which would push the year-over-year rate back up to 3.3% in Q4 from April's year-over-year rate of 2.8%.

The Rebound Begins

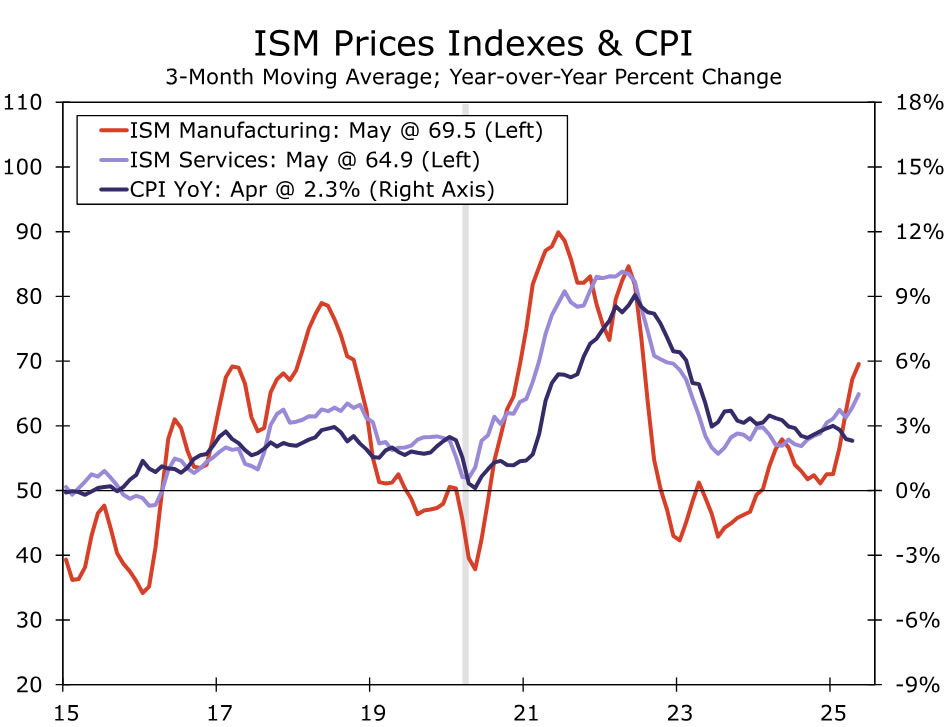

The May CPI report will test whether April's potential signs of tariffs were early glimmers of inflation effects to come or more typical monthly noise. We estimate consumer prices rose 0.2% (0.15% unrounded), in line with the current Bloomberg consensus. If realized, the increase would push up the year-over-year rate up a tenth to 2.4% and follow soft data in showing that the downward trend in inflation is beginning to reverse (Figure 1). Core categories are expected to drive the advance. Excluding food and energy, we estimate prices increased 0.3% (0.27% unrounded) in May and 2.9% over the past year.

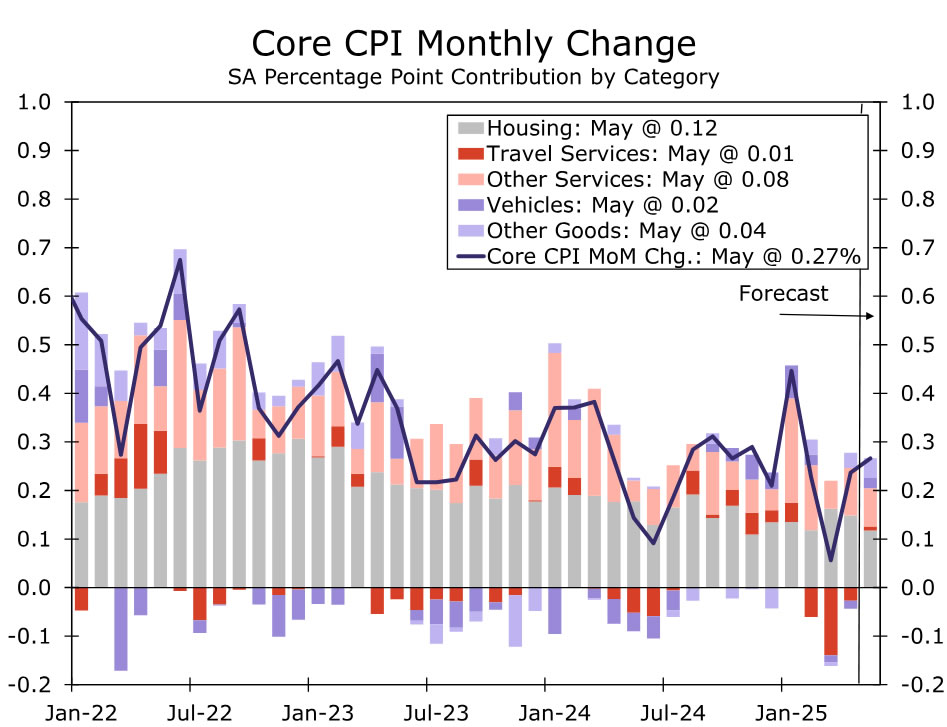

Last month's CPI report showed a modest (0.1%) rise in core goods prices, as a drop in vehicle prices was more than offset by a rise in other core goods categories. Core goods ex-new and used autos matched its largest monthly rise in more than a year in April, with notable strength among household, recreational and IT goods. Whether these categories deliver a repeat performance will help to determine if higher import duties are indeed being passed on to consumers, or if April's strength was merely a function of volatility in the data. The risk of the latter seems higher than usual, as the BLS noted it temporarily reduced data collections in April due to staffing shortages. But the jump in tariff rates over the past few months—collections are up 80% year-to-date through June 4—generates significant potential for April's strength to continue. We expect to see core goods prices rise about 0.25%, with similarly sized gains in vehicles and remaining core goods.

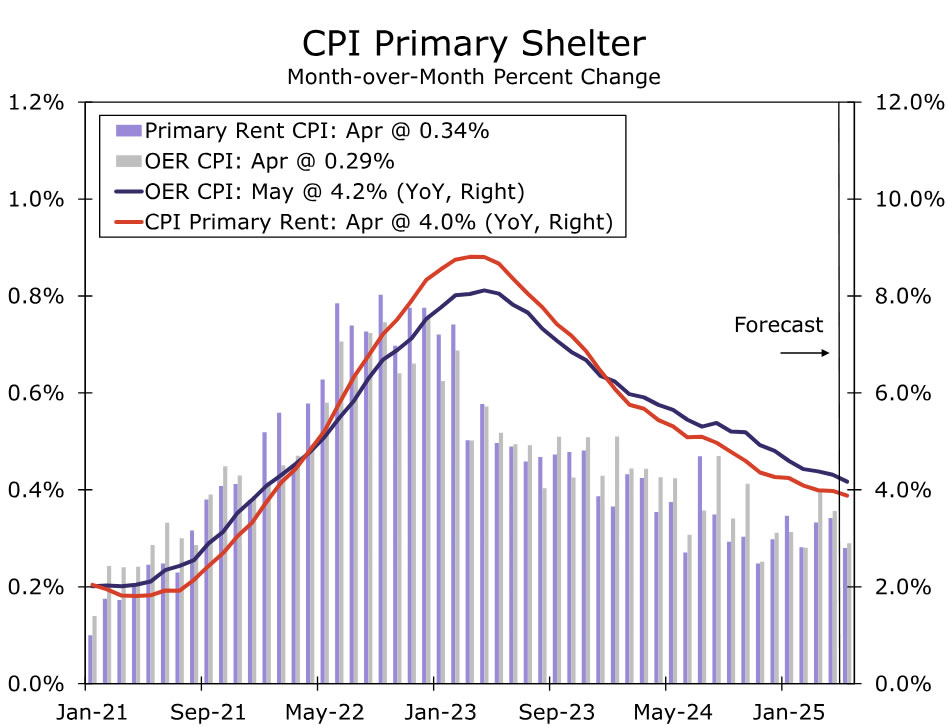

While the changing trade policy environment has put goods inflation back in the spotlight, service-sector disinflation slowly continues. We estimate core services inflation was little changed in May, with a 0.3% monthly increase keeping the year-ago rate at 3.6%. Beneath the steady monthly gain, the drivers are likely to shift. Primary shelter inflation is anticipated to moderate after a couple of months of above-trend gains (Figure 3). But travel-related services prices should rise slightly in May after falling sharply the past three months. Although recent weakness in travel categories highlights more cautious spending by consumers, we expect to see a modest lift in prices amid the early timing of Memorial Day.

Consumers look to have gotten a bit more breathing room when it came to gas prices last month, however. We estimate energy prices declined a little more than 1% last month. Along with a roughly 0.1% rise in food prices, this leads us to expect headline inflation will rise less than the core index in May.

While May's Consumer Price Index is not expected to deliver a stand-out increase, we look for inflation to pick up through the second half of the year. Higher tariff rates lie behind the expected uptrend. In our view, the administration remains committed to meaningfully higher import duties despite the current pause on "reciprocal" tariffs and legal challenges of the current section of the Trade Act used to employ them. Pre-tariff inventory building and hope that the current scale of tariffs may be reduced have helped to restrain cost increases thus far. Consumer-facing companies in particular seem hesitant to immediately pass on the full costs of tariffs due to concerns about the underlying strength of low- and middle-income households. As a result, we expect some of the tariff costs to be absorbed via margins, which remain noticeably higher than before the 2018 trade war. That said, as the higher tariff regime persists, shielding consumers from the costs is likely to become more challenging. We anticipate the three-month annualized rate of core goods inflation to peak around 4%-5% in early fall, a little lower and later than our previous forecast published May 8 ahead of the 90-day pause on "reciprocal" tariffs on China.

Yet, spillovers into the service sector are still expected to be limited. The jobs market is no longer experiencing historic labor shortages, and the weakening backdrop for workers points to employment cost growth slowing further this year. The monthly pace of shelter inflation is close to settling to around a 0.28%-0.30% monthly pace over the remainder of the year, which should help to drive the current year-over-year rate of 4.2% down to 3.6% next spring. Meantime, service providers face the same concerns as companies directly impacted by tariffs about consumers' ability and willingness to spend. As a result, we look for services inflation to recede a bit more throughout the year and to mitigate the increase to goods inflation fueled by tariffs.

U.S. Inflation and Canadian Industry Sales for May in Focus for Trade Woes

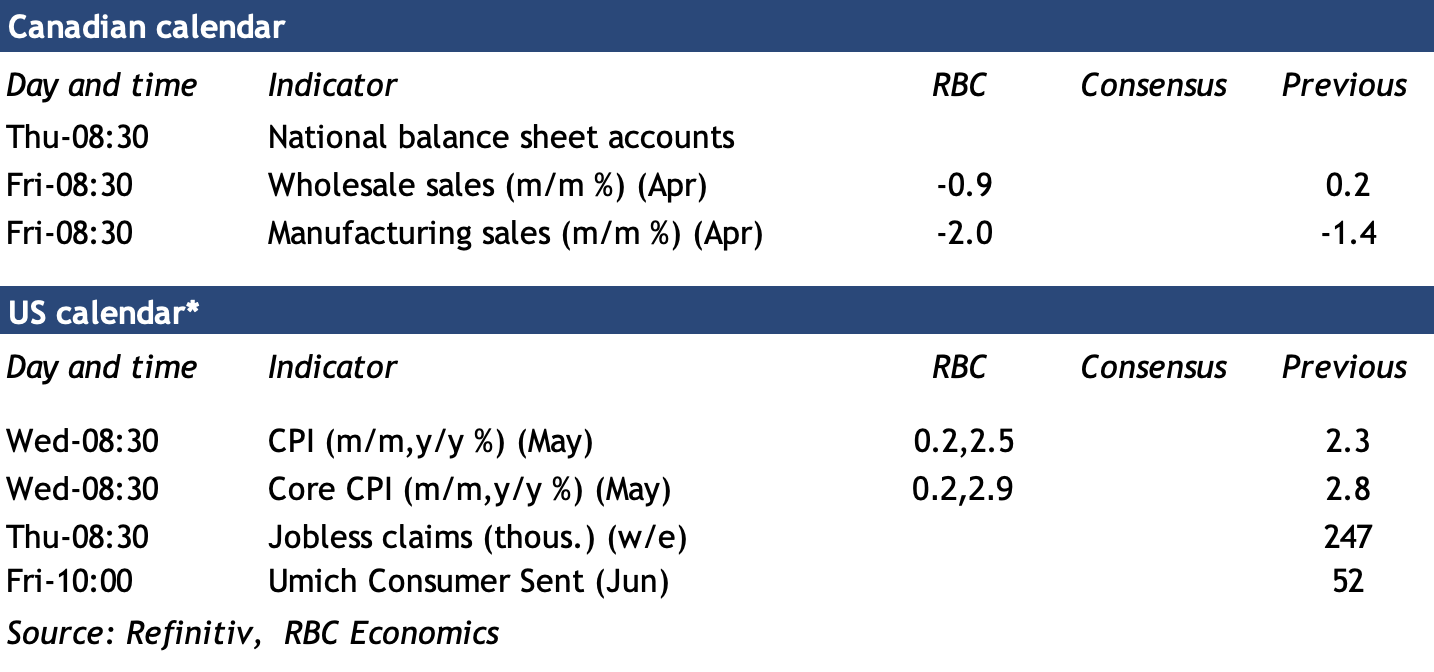

Economic data in the coming week will continue to highlight how trade disruptions in its early stages are impacting the Canadian and U.S. economies.

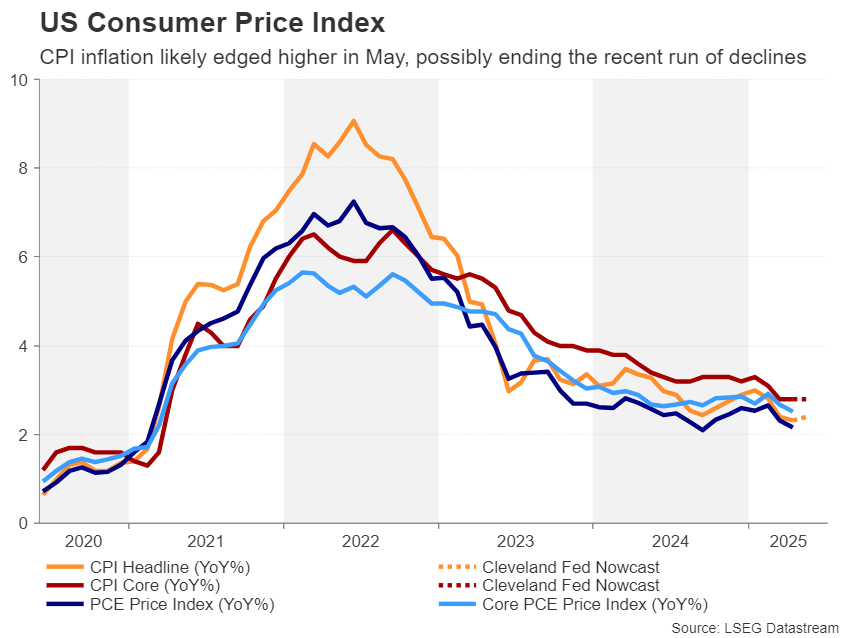

Inflation reports in the U.S. so far have failed to show the impact of tariffs on consumer prices. Core goods inflation in April was the first positive yearly reading since December 2023, mostly due to larger monthly increases earlier this year with a relatively subdued 0.06% month-over-month rise in April.

Nevertheless, tensions are brewing. Used car prices in the U.S. rose 4.4% from a year ago in May, according to the Manheim Used Vehicle Value Index—but it may be taking some time to appear in official consumer price index. Factoring in a slightly firmer monthly increase in core goods prices, we expect headline and core CPI in May to tick up 2.5% from 2.3% in April, and to 2.9% from 2.8%, respectively. Food and energy inflation likely held near the same levels with energy still below year-ago prices and food prices up almost 3%.

In Canada, early reports from Statistics Canada indicate manufacturing sales contracted by 2% in April. Separately reported industry price data shows that three quarters of that decline was likely price related. Oil prices were lower, reducing the nominal value of petroleum sales. But, the early estimate also flagged a softening in auto manufacturing. The decline coincides with 55k, or 2.9% job losses in the sector since January.

Wholesale sales in Canada were also estimated to have declined in April, but retail sales rose by 0.5%, according to StatsCan’s advanced estimate. Going forward, we expect additional softening in Canadian industrial sectors as tariffs reduce U.S. demand for Canadian exports, especially for auto and parts, steel, and aluminum products that are disproportionately targeted by U.S. tariffs. Offsetting some of that weakness will be resilience in domestic services consumption that has broadly held up.

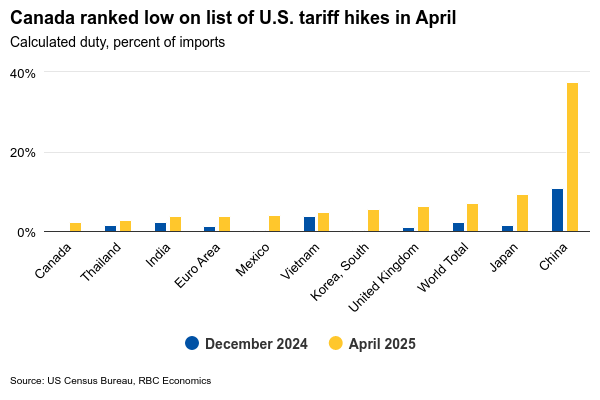

Overall, April’s international trade data confirmed that U.S. tariff increases on Canada, while significant, have been smaller than for other major U.S. trade partners. Barring more significant changes to existing U.S. tariffs, we expect growth in both Canada and the U.S. to slow this year, but expect both to avoid a recession. We anticipate a more pronounced impact on inflation in the U.S. where the average import tariff rate is now substantially higher than in Canada.

Week ahead data watch

We expect Canadian household net worth was little-changed in Q1 with both debt and asset levels holding around levels at the end of 2024. A pullback in equity markets in Q1 likely weighed on household financial asset holdings but house prices edged higher. Household debt service ratios (ratio of debt payments to household disposable income) likely remained elevated, but with little change from Q4/2024 at 14.4%, and still below the 15.1% peak in Q3 2023.

Gold Fails to Break Resistance in Risk-On Market Environment

Gold had been climbing steadily despite the overall risk-on sentiment this week. However, this morning’s stronger-than-expected Non-Farm Payrolls report failed to give the safe-haven asset any additional lift.

The rejection at higher levels suggests a lower likelihood of a retest of the all-time highs, which remain at $3,500 - although with this year's volatility, everything is possible.

The Bullion, which was up 3% at its weekly highs is now up only 1.26% - Let's dive into a technical analysis as we stand on the current pivot.

Gold Technical Analysis from Daily to Hourly charts

Gold Daily Chart

XAUUSD Daily Chart, June 6, 2025. Source: TradingView

Gold broke out of its descending daily channel on Monday, supported by early-week US Dollar weakness. However, the streak of consecutive bearish daily candles is undermining momentum toward its all-time highs.

The Daily RSI is neutral though above its 50 level, which still gives it a somewhat bullish bias.

The MA 50 on the daily is still catching up to the rise that occured through the latter part of May.

Standing right at the current pivot of $3,330, we still have to observe if a prolongation of the rejection leads to a re-entering of the Daily Channel.

Gold 4H Chart

XAUUSD 4H Chart, June 6, 2025. Source: TradingView

Gold prices are looking to retest the higher band of the Daily Channel, located at 3,310 as it rejects the 4H MA 20.

One hurdle to look at that may slow a potential down-move within the Channel would be the MA 200 located at the confluence with the 3,300 psychological zone.

Prices which are contained within these 2 key MAs infer some indecision, however we may expect some more clarity throughout the weekly close.

A bounce on the upper channel line will hint to another test of the 3,375 to 3,390 Resistance zone, while a break below the 200 MA points toward the 3,275 to 3,290 Support Zone

Watch the market sentiment, as a further move towards all-time highs in US stock indices may just add to more pressure for the Bullion.

Gold 1H Chart

XAUUSD 1H Chart, June 6, 2025. Source: TradingView

Gold is entering an oversold level as we approach the immediate support zone located between 3,305 and 3,315.

The descent is still fairly strong, therefore watch for any particular switch in market sentiment:

A positive tone may give more strength to sellers, while a risk-off move towards the week-end will provide support; things are still unclear for now but the current mood is positive.

We can observe some harmonic patterns towards the correction in the precious metal as the move up happened after an inverted Head and Shoulders, touching the $3,400 psychological zone before reverting on the Trump-Xi conversation headlines.

We are now observing another potential measured move on the way down (purple squares).

Also watch for potential consolidation around the 3,330 pivot.

Safe Trades!

Week Ahead – US CPI to Take Centre Stage as Fed Rate Cut Bets Gather Pace

- US inflation may edge up in May but unlikely to dent Fed rate cut bets.

- Focus also on trade negotiations and US appeals court tariff decision.

- Chinese trade data eyed amid tariff war.

- UK employment and GDP also on the agenda.

Will US CPI add to Fed rate cut hopes?

Expectations that the Federal Reserve may cut interest rates by more than 50 basis points received a boost over the past week following a weak batch of economic indicators that pointed to a slowing US economy. The first signs of cracks from President Trump’s global trade war appear to be forming within the labour market, manufacturing, consumer spending as well as the broader services sector.

However, after the recent months’ declines in the key inflation metrics, investors are hoping that the Fed will not hesitate to cut rates now that the economy is possibly stumbling. Yet, there’s also a case to remain on pause for a while longer, at least until after the July 9 deadline for reciprocal tariffs where there should be more clarity about potential trade deals.

With inflation still hovering above the Fed’s 2% target, policymakers may not want to make the mistake of lowering borrowing costs prematurely, as a fresh flareup in trade tensions cannot be ruled out at this stage.

Wednesday’s CPI report will put the improved rate cut optimism to the test as it might show a stalling in the recent disinflation trend. According to the Cleveland Fed’s Nowcast model, headline CPI is estimated at 2.4% y/y in May, up from 2.3% in the prior month, while core CPI is projected to stay unchanged at 2.8% y/y.

Producer prices for the same month will follow on Thursday and will also be important in gauging underlying price pressures. Wrapping up the week will be the University of Michigan’s closely watched preliminary consumer sentiment survey, which includes consumer inflation expectations.

Any softness in the incoming data would likely further bolster rate cut bets, adding to the US dollar’s woes, but shares on Wall Street would probably cheer a downside surprise and head higher.

Tariff ruling and trade deals might also set market tone

However, it’s not going to be just inflation data driving sentiment next week. The US Court of Appeals could decide in the coming days whether to permanently overturn the US International Court’s ruling to block Trump’s reciprocal tariffs. The appeals court will have heard from both sides by June 9, but in either outcome, the case could still end up in the Supreme Court, delaying a final ruling on the matter.

Still, should in the meantime the appeals court rule in favour of the Trump administration, it won’t change the status quo and the market impact will be negligible. But should it side with the lower court that the reciprocal tariffs are unlawful, there could be a limited boost to risk appetite.

Investors will also be keeping an eye on any developments in the trade negotiations as it’s not just the US President that’s getting impatient about the slow progress. Doubts are creeping into the markets about how quickly the US will be able to reach trade agreements with its main trading partners, as there’s just one month left until the 90-day pause on reciprocal tariffs expires on July 9.

Japan and India remain the most likely countries to next reach a trade deal with the White House, especially Japan, which is hoping to conclude talks before Prime Minister Ishiba meets with Trump on the sidelines of the G7 summit in Canada that starts on June 15. However, a surprise deal is also possible with the G7 hosts, amid reports that Canadian Prime Minister Carney has been in direct talks with Trump to settle the trade row between the two countries.

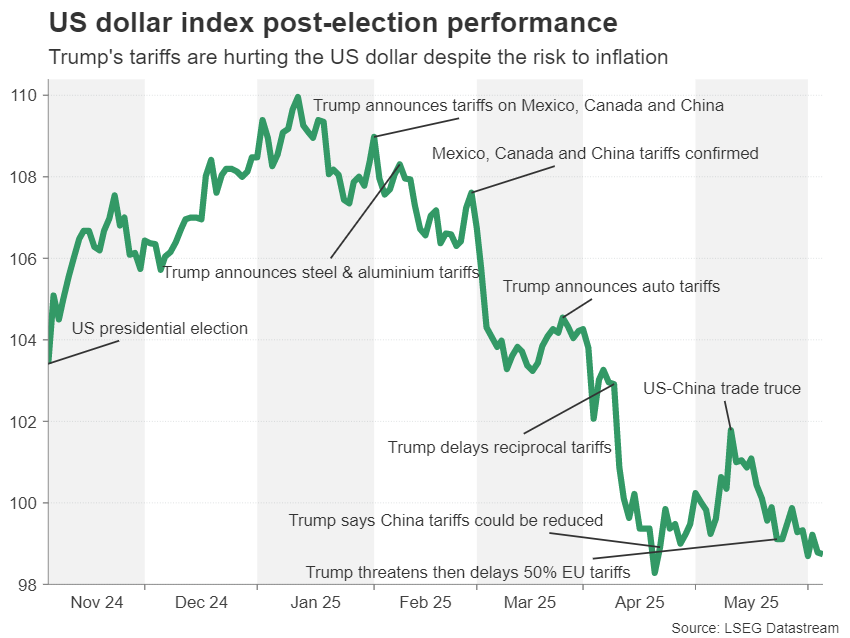

Tracking the fallout of the US-China tariff war

But as far as trade talks with China are concerned, there is some ambiguity about how much progress is being made despite the call this week between Presidents Trump and Xi. At this point, the only real progress is that there is an open dialogue between Washington and Beijing and that Trump will soon travel to China on a state visit. But an actual deal could be months away, with more setbacks likely until there is a final agreement, and this can only mean more bumps on the road for markets.

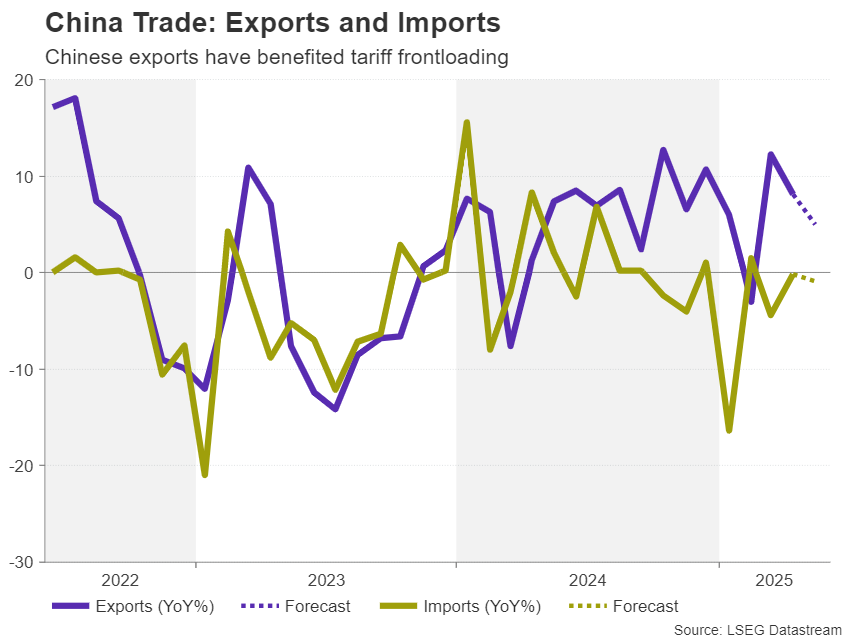

Next week’s trade figures out of China could slightly smoothen the ride, however, as the truce struck with the US on May 12 to temporarily lower the tariffs on each other possibly lifted exports during the month. Though, it might be difficult to get a clear picture given that the tariff relief came during the middle of the month.

The May trade data is out on Monday alongside the consumer and producer price indices for the same period.

Equities and the Australian dollar are likely to rise the most from a strong bounce in Chinese exports and imports.

Pound aims high, might shrug off UK data

Over in the United Kingdom, Prime Minister Keir Starmer’s success in being the only leader to sign a preliminary trade pact with America hasn’t earned him much praise on his home turf. Starmer’s Labour government is under fire by both Labour MPs as well as voters for making steep cuts to some benefits, not doing enough to stimulate the economy and for not negotiating a better deal with Trump.

Financial markets are somewhat more impressed of his handling of the economy, as the pound is trading at more than three-year highs, testing the $1.36 handle.

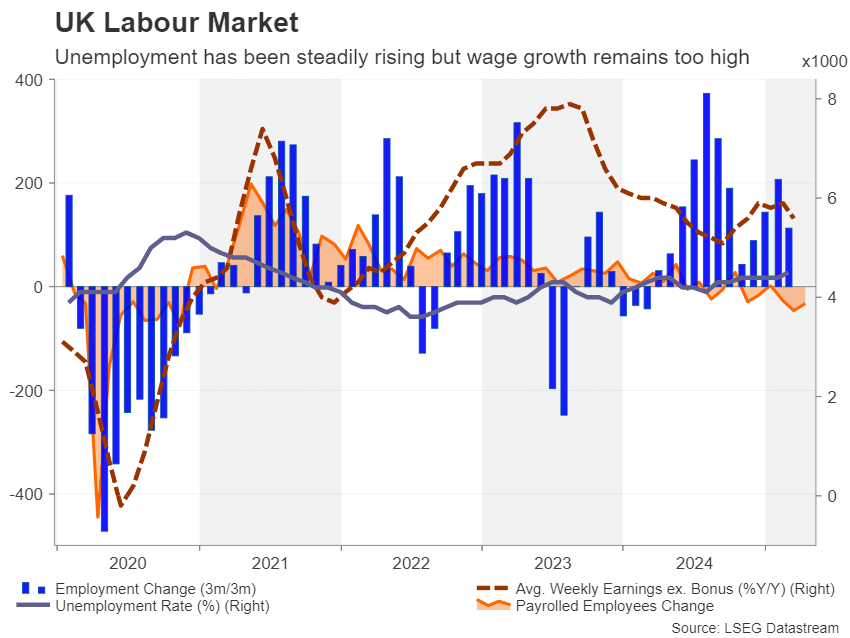

Nevertheless, despite the UK economy defying the predictions of doom and gloom, there are some worries about the labour market. The government’s hike in employers’ national insurance contributions on top of the rise in minimum wage and demands of higher pay, has overburdened companies with higher costs.

The employment report for the three months to April will be watched on Tuesday for any signs of increased layoffs. The latest wage growth numbers will also be scrutinized as the very slow cooling in pay pressures is keeping the Bank of England on the cautious side when it comes to its readiness to cut rates.

There will be more data on Thursday with the release of the April GDP print, including the sectoral growth in services, manufacturing and overall industrial production.

Unless the jobs and GDP figures are very strong or very poor, reaction in the pound will probably be muted, with broader risk sentiment and the dollar’s own performance being bigger drivers.

Weekly Focus – ECB Nearing the End of Rate Cuts

We published our latest economic forecasts this week, with notable downgrade to the US outlook but relatively stable view for euro area growth. Arguing that uncertainty is exceptionally high might feel like a cliché these days, but the forecasts are naturally subject to significant tariff uncertainty. As a base case, we assume that tariffs will remain near current levels in the foreseeable future, with the US average trade-weighted tariff rate hovering around 15%. This means we think the 10% universal rate as well as the current product-specific tariffs will remain in place, but that majority of the so-called 'reciprocal tariffs' will not be reinstated. We foresee euro area GDP growth at 0.9% in 2025 (unchanged), US at 1.6% (from 2.3%) and China at 4.7% (unchanged). Read more from Nordic Outlook - Normalisation with tariff risks, 4 June.

The ECB cut its policy rates by 25bp as widely expected. Lagarde delivered a more hawkish rhetoric than markets had anticipated. She underscored that the central bank is now well positioned for the current environment, and that ECB is 'getting to the end' of its cutting cycle. Euro area inflation slowed down to 1.9% y/y in May and ECB adjusted their inflation forecast to just 1.6% for 2026, but Lagarde downplayed its significance and emphasized the shift mostly reflected lower energy prices and stronger EUR FX rate. We adjusted our ECB call and now foresee only one final rate cut in September, when previously we expected cuts in both July and September. Short-end rates ticked somewhat higher as markets pulled back their rate cut expectations as well. Read more from ECB review: In a good position, close to or at the end, 5 June.

Market sentiment has generally remained calm despite Trump's increased 50% steel and aluminium tariffs coming into effect this week. Equities ticked modestly higher on both sides of the Atlantic while long-end bond yields stabilized lower. EUR/USD shifted up above 1.14, and we think the persistent distrust towards the US combined with structurally slowing growth will take the cross towards 1.20 in one year's time.

Incoming macro data has been to the soft side, with both US ISM manufacturing and services indices falling short of expectations. The services index showed a concerning combination of weaker new orders yet still increasing price pressures. The stagflationary tone offers no clear guidance for the Fed. On the other side of the Pacific, China's Caixin manufacturing index also fell sharply in May to 48.3, from 50.4. Read more from our latest China Headlines, 6 June.

Next week will be relatively light in terms of macro data. We think US CPI inflation remained steady in May at +0.2% m/m SA in both headline and core terms. University of Michigan's preliminary June consumer sentiment survey will provide markets with clearer sense of inflation expectations. The revised May survey showed that inflation expectations had declined after the US-China trade deal was announced. From the euro area, the Sentix indicator will offer a sense of how investor confidence has evolved in early June. The indicator rebounded sharply in May following the post-liberation day plunge in April and we think there is further room for a small increase in June.

Cliff Notes: Responsive Policy

Key insights from the week that was.

In Australia, Q1 GDP confirmed that the economy started the year on a weak footing, rising just 0.2% to be up 1.3% over the year. Compositionally, the roll-off of energy rebates saw a portion of spending re-allocated from governments to households; but overall, the pulse in the domestic economy remains faint. Having just experienced one of the most prolonged and deep contractions in real per capita disposable incomes on record, households continue to preference rebuilding savings buffers over discretionary spending. While public spending remains elevated, the support it offers to economic growth is starting to wane as large infrastructure projects move towards completion. Growth in housing construction was a bright spot amongst the GDP detail, but new business investment was mixed – non-residential construction accelerating as equipment spending fell to its lowest level in two years.

Prior to the GDP release, the RBA Minutes made clear that current trends in domestic economic conditions alone justified a further reduction in policy restrictiveness in May, with the added downside risks from global developments raising the possibility for a 50bp cut (which was ultimately dismissed). With growth now having stalled at 1.3%yr over the past six months, it is important to consider how the RBA might reach its terminal policy rate and where that terminal policy rate might be. This week’s essay from Chief Economist Luci Ellis explores these questions.

Coming back to the GDP detail, the external sector proved to be a slight drag on activity, with real net exports detracting –0.1ppts from Q1 GDP. Highlighting the volatility at present, weather-related disruptions to coal production and port activity more than offset the gold export rush, while travel-related services exports surprised materially to the downside. Some of these goods trade dynamics started to unwind over April, but we are likely to see further volatility in coming months.

Before moving offshore, it is worth noting that the latest Cotality (formerly CoreLogic) data showcased another bumper gain in house price growth, up 0.5% in May. Seasonality may be overstating the scale of recent gains; regardless, the data reflects a clear rapid response to RBA rate cuts which will be tested against affordability in coming quarters. For more detail on our views around the housing market, see our latest Housing Pulse.

In the US, the May ISM reports painted a sombre picture of the economy. The manufacturing index fell 0.3pts to 48.5pts, with most components below the 50 expansion/contraction divide. Of particular note, the production and new export orders sub-indexes both posted sizeable falls and remain more than 10pts below their pre-COVID 5-year average. Both the prices and supplier deliveries sub-indexes rose strongly, however, reflecting the impact of tariffs – increased import costs and a hoarding of inputs ahead of feared tariff escalation. On the services side, the headline index surprised, falling from 51.6pts to 49.9pts. In the detail, there was a substantial drop in the new orders, order backlog and export components. On the bright side, the services employment index regained momentum to 50.7, consistent with balance between labour demand and supply. The Federal Reserve’s latest Beige Book highlighted similar concerns over prices and uncertainty regarding the outlook for both activity and the labour market.

Further north, the Bank of Canada maintained its policy rate at 2.75% at their June meeting, seeking further information on the implications of US trade policy for the Canadian economy. Post-meeting communications noted that the labour market has weakened, particularly in trade-related sectors; however, inflation has been modestly stronger than anticipated. Activity growth has shown resilience amid uncertainty, however; although this is partly due to exports and inventory building to avoid tariffs. The Bank of Canada noted they intend to be less forward looking in the months ahead, amid considerable uncertainty over trade policy and with the policy rate near neutral.

Also facing considerable uncertainty from offshore, the European Central Bank cut its deposit rate by 25bps to 2.0%. Revised forecasts show inflation is now anticipated to be 2.0% in 2025 then 1.6% in 2026 (both 0.3ppts below the prior forecast) and 2.0% in 2027. Their GDP forecasts were broadly unchanged, with growth expected to come in at 0.9% in 2025, 1.1% in 2026 and 1.3% for 2027. Accompanying these baseline forecasts were staff scenarios. A “further escalation of trade tensions over the coming months would result in growth and inflation being below the baseline projections. By contrast, if trade tensions were resolved with a benign outcome, growth and, to a lesser extent, inflation would be higher than in the baseline projections.”

In terms of the path ahead, President Lagarde emphasised the uncertain terrain the ECB are navigating and consequently that they will “follow a data-dependent and meeting-by-meeting approach” in determining policy. That said, President Lagarde mentioned the central bank was in a "good place" and that "they were getting to the end of a monetary-policy cycle". On balance, the hawkish tone on the inflation outlook increases the probability of a pause in interest rate cuts at the next meeting in July, but it does not rule out a further cut in September or later in the year, particularly if near term uncertainty and tariff effects prove to be a bigger issue than the ECB expects.

Cautiously, Predictably Evolving Their Beliefs

Soft activity data highlight that risks around the path for the RBA cash rate are skewed down. This has less to do with changes to the RBA’s models of the neutral interest rate and more about the risk that it will again be surprised by the domestic economy.

Soft GDP data for Q1 has again raised questions of whether the RBA is behind the curve and has left policy too tight for too long. As we have been highlighting for some time, underlying growth in Australia remains weak and sensitive to pauses in the expansion in the care economy. With inflation in the 2–3% target range already, and likely to stay there, why wouldn’t the RBA cut further and faster than previously believed?

Certainly, this is the question we keep asking ourselves and are hearing from clients. The risks to our current policy view are clearly to the downside, as we have previously highlighted. Yet a headlong switch into a more dovish near-term path for policy sits awkwardly against the Board’s own words in the minutes. The Board expressed ‘a preference to move cautiously and predictably when withdrawing some of the current policy restriction.’ And just before that sentence: ‘They also judged that it was not yet time to move monetary policy to an expansionary stance, taking account of the range of estimates involved, given that inflation was yet to return sustainably to the midpoint of the target range and the staff’s assessment that the labour market was still tight.’

Recall also the Governor’s response to Michael Pascoe’s question at the media conference, ‘We get quarterly inflation rates in this. We don’t get monthly. We get the monthly indicator, which is very volatile. We get four readings on inflation a year. Other countries get them 12 times a year.’ We read this as saying that the Board (or at least the Governor) wants to wait for the June quarter CPI, ahead of the August meeting, not the July meeting. The irony is that by late this year, Australia will have a full monthly CPI.

Predicting the movement of the stars

Part of the art of predicting what central banks will do with their policy rates goes beyond forming a view about where the economy is headed. There is also an element of forecasting future shifts in the central bank’s beliefs about how the economy works. This includes their beliefs about where the ‘star variables’ such as the neutral real interest rate (r*) and full-employment rate of unemployment (NAIRU) are, and the weight they put on these assessments in their policy deliberations. Both the location of and the reliance on these estimates can change, sometimes quite abruptly.

Ideally, the policymaker would communicate these evolving beliefs. Some of the detail is only for the aficionados, though, and therefore is sometimes – understandably – left on the cutting-room floor when putting together flagship documents intended for a broader audience. It is therefore left to those aficionados to interpret, and indeed forecast, where policymakers’ views are headed.

For example, at the beginning of this year, our views about the path of Fed policy was partly shaped by our assessment that the Fed staff view of the neutral rate was still too low and that they would progressively revise it up. There was therefore some chance that the Fed would end up lowering the Fed funds rate below neutral and have to backtrack as this view was revised. In the event, the Fed view caught up with our expectations soon enough that this backtrack did not occur. But the underlying (and out-of-consensus) view that the Fed would not end up cutting as far as had previously been priced in was sound.

Of course this was not just about judgements about where neutral is. As that earlier note discussed, there is also the question of whether there are other factors working against a ‘glide to neutral’ path for policy. Differing fiscal stances across countries is an obvious example, particularly when the parlous state of the US fiscal position is such an outlier. Working in the other direction, policy uncertainty around tariffs and other chaotic policy decisions of the Trump administration is clearly weighing on US growth prospects more than they do on countries such as Australia.

In Australia, these assessments and their likely direction of travel are also key inputs into any view of future RBA policy. For example, it is hard to shake the impression that, whatever more nuanced language about full employment being multidimensional, the RBA’s view of the upside risks to inflation are coloured by their model-based assessments (released under FOI) that the unemployment rate is below the NAIRU. The revision of the RBA’s forecasts for trimmed mean inflation from not-good-enough-dead-flat-at-2.7% to good-enough-now-dead-flat-at-2.6% is absolutely a judgement. And while it was not directly driven by models, that judgement to write down 2.6% and not 2.5% anywhere in the forecast horizon was likely shaped by the RBA’s view that the labour market is still tight and productivity growth weak.

Against that, though, we have been getting questions about an apparent downward shift in the RBA’s view of where neutral is, evident through a comparison of graphs showing estimates of the nominal neutral in a sequence of documents. A year ago, the RBA’s view was coloured by surprisingly convergent estimates of r* well above 3%, implying that monetary policy was restrictive, but perhaps not that restrictive. This, along with its analysis of productivity trends, contributed to the hawkishness of RBA decisions and communications in the latter half of last year and at the February meeting.

However, new models were introduced between November last year and February this year that were at the lower end of the existing range of models. (We understand that these were based on recent work at the New York Fed.) And unlike all the other models, these new ones did not show an upturn in estimates post-pandemic. The average of all these estimates is now in the high 2s rather than the low-to-mid 3s range we have favoured for both the US and Australia. This means that the neutral real cash rate is estimated to be barely above zero. You don’t need to look at 700 years of data to worry that such an estimate is on the low side.

At this stage, though, we assess that, while the weight of those r* estimates is indeed lower than a year ago, the weight that the policymakers put on the central estimate has also declined. There are a couple of straws in the wind supporting this conclusion, including comments by the Deputy Governor following the February Board meeting. We will be watching closely for signs that the RBA is taking these models more seriously than we currently think. More pertinently, though, we will also be watching for signs that the labour market and inflation are softer than the RBA currently expects. If the downside risks around the policy path are to come true, it will require the RBA to change its mind about how the economy is traveling.

Sunset Market Commentary

Markets

The May US payrolls report wrapped up a week of overall disappointing economic data. US JOLTS (job openings) were the proverbial exception to the rule. Monday’s manufacturing ISM and Wednesday’s services gauge painted an ugly stagflationary picture. And the poor ADP job report (a mere +37k) on Wednesday and Thursday’s higher-than-expected weekly jobless claims did not go unnoticed either. In fact, the data posed downside risks for today’s payrolls report. Those didn’t quite materialize with a job growth of 139k. The slight beat of consensus (126k) was offset by the -95k two-month revision though. The services sector (+145k) provided for all of the jobs created, led by private education & health and leisure & hospitality. The federal government shed another 22k jobs, the fourth decline in a row. Earnings growth came in to the high end of expectations (+0.4% m/m and 3.9% y/y) while the participation rate eased to 62.4%. The unemployment rate was at an unchanged 4.2%. This metric is getting close attention ever since the Fed last year started cutting rates aggressively after rising unemployment triggered the Sahm rule.

The labour report was except for next week’s CPI the final input for the Fed June 18 meeting. All in all it offered nothing spectacular and won’t nudge the debate in either direction. It’s “hold your horses” for the time being and “go all in” if needed. That was the Fed’s playbook end 2024 and the preferred approach by amongst others Fed’s Hammack. In an interview with the New York Times she said she “would rather wait and move quickly to play catch-up if I really don’t know what the right next move is”. And for the record: she really doesn’t know what the right next move is. Yet, US yields surge more than 8 bps at the front end of the curve. This is more of a kneejerk reaction than anything else. Following the ADP and jobless claims, markets were bracing for a softer than expected reading. Some extra market optimism creeped in as well after US trade advisor Navarro flagged a meeting between US and Chinese officials potentially already next week. Just yesterday, the respective presidents had their first formal contact since Trump took office. The dollar strengthens to sub EUR/USD 1.14 but the short-term upward sloping trend channel remains in tact for now. DXY bounces back to 99.17 and USD/JPY aims for 145.

News & Views

Czech industrial production (adjusted for the number of working days ) in April rose 0.9% M/M and 2.0% Y/Y, it’s statistical office reported. Admittedly, the improvement was mainly due to a strong performance of electricity producers and the improved situation in the mining industry. The manufacturing industry is lagging, stagnating year‐on‐year. Even so, the trend for the most cyclical parts of the Czech industry, led by engineering and basic metals producers, also shows a slow reversal for the better. This is confirmed by new orders ‐ base metal producers +3.2% YoY, engineering +2.0% and fabricated metal products +8.6%. On the other hand, production in the automotive segment will undoubtedly grow more slowly this year as it is bumping up against a relatively high comparison base versus last year and relatively high‐capacity utilization. Overall, the better industrial figures in April, together with very strong retail sales, show that, at least at the start of Q2, the Czech economy has been still in good shape. This comes on the back of a very strong first quarter, when it grew by 0.8% Q/Q. So, for now, we haven’t seen a significant impact of the higher US tariffs. The Czech koruna remains well bid, with EUR/CZK at 24.75, touching the best levels in almost a year’s time.

According to Bloomberg reporting referring to people familiar with the matter, Bank of Japan officials are likely considering slowing the pace of its pullback from buying government debt at the June 17 policy meeting. Officials are said discussing making smaller reductions to the BOJ’s bond buying program from current pace reducing net purchases by JPY 400 bln per quarter scheduled to be in place until March next year. From then, aside from keeping current pace of a JPY 400 bln reduction, options of reducing the pace of the slowdown to JPY 200 bln or between JPY 200 bln and 400 bln are said to be on the table. The debate on the pace/amount of BOJ bond buying recently intensified due to rising pressure at the long end of the Japanese government bond curve as investor appetite was low to pick supply in these longer tenors, sharply rising yields at those longer maturities.

Canadian Job Market Treads Water in May, Tariff Affected Areas Show Strain

The Canadian labour market basically tread water again in May, adding only 8.8k net new positions (+0.0% month/month). The details were slightly better, with the private sector up 61k positions (+0.4% m/m), and solid gains in full-time jobs (58k). However, these were mostly offset by losses in part-time jobs (-49k).

The unemployment rate rose for the third consecutive month to 7.0%, the highest rate since September 2016 (apart from the pandemic). The labour force grew by 0.2% m/m. Growth in the labour supply has slowed in recent months, but employment growth has slowed further.

The job market is even tougher for students. The unemployment rate for returning students (aged 15-24) was 20.1% -- the highest since the 2009 recession (excluding the pandemic).

The impact of tariffs shows up in the industry pattern and regional unemployment pattern. The manufacturing sector was down (-12.2k), as was transportation and warehousing (-15.5k). Manufacturing has lost jobs for four months now, totaling 55k. That said, the wholesale and retail trade sector recouped some (+43k) of the 55k jobs lost through march and April. The highest unemployment rates across CMAs were in Windsor (10.8%), Oshawa (9.1%) (three-month moving averages), which have both seen significant increases since January.

Wage growth was steady in May. Average hourly wages rose 3.4% versus a year ago, matching April's pace. Lastly, total hours worked were flat.

Key Implications

Canada's labour market continued to soften in May. The unemployment rate continued to rise, and the impact of U.S. tariffs is clearly evident in industry and regional patterns. Wage gains were steady in May but have cooled from a roughly 5% pace a year ago.

On Wednesday, the Bank of Canada opted to wait and see how tariffs would impact the Canadian economy, while also weighing recent hotter than expected inflation readings. May's jobs report puts another mark in the economic weakness tally. We think this will ultimately lead to further rate cuts from the Bank of Canada.

US: Payrolls Rise 139k in May, Unemployment Rate Holds at 4.2%

The U.S. economy added 139k jobs in May, slightly above the consensus forecast of 125k. But revisions for the prior two months subtracted a meaningful 95k jobs.

- Smoothing through the volatility, non-farm payrolls averaged 135k over the last three-months, only a touch lower than the 144k averaged over the twelve-month period.

Private payrolls rose 140k – nearly matching April's downwardly revised gain of 147k (previously 167k) – with the largest gains seen in health care & social assistance (+78.3k) and leisure & hospitality (+48k). Trade exposed industries like manufacturing (-8k) and retail trade (-6.5k) both shed jobs. Federal hiring declined by 22k and has now lost 59k jobs since February.

In the household survey, both civilian employment (-696k) and the labor force (-625k) plummeted, resulting in the unemployment rate holding steady at 4.2%. The labor force participation rate ticked down 0.2 percentage points to 62.4%.

Average hourly earnings (AHE) rose 0.4% month-on-month (m/m) – following a gain of 0.2% m/m in April. On a twelve-month basis, AHE earnings are up 3.9%.

Aggregate weekly hours rose 0.1% m/m, down from April's gain of 0.2% m/m.

Key Implications

Non-farm payrolls remained resilient last month despite heightened trade policy uncertainty. While weakness in the household survey coupled with the significant downward revisions to prior months helped to take some of the shine off the headline payrolls print, it's fair to say that the labor market is holding up better than expected.

Heightened uncertainty surrounding trade and fiscal policy alongside still elevated inflation has left policymakers in no rush to cut rates. While the labor market is showing signs of cooling, job creation is still running at a healthy pace and underscores the ongoing need for patience. Interest rate futures are currently pricing in just 20 bps of policy easing by September and only two quarter-point cuts by year-end.