Sample Category Title

ECB officials signal pause yesterday’s rate cut, emphasize flexibility

One day after ECB delivered its eighth rate cut in this easing cycle, a coordinated message emerged from several Governing Council members: ECB is not committing to further immediate action.

Latvian central banker Martins Kazaks was particularly blunt, stating that markets should not expect a rate cut at every meeting. He emphasized the value of preserving "policy space".

"We don’t get much data between now and the July meeting so it may well be the case that we pause," Kazaks said. "But uncertainty remains very high, the political situation may change every day. So forward guidance isn’t your friend in these circumstances."

Greek central bank chief Yannis Stournaras echoed this sentiment, calling ECB’s work on inflation “nearly done,” while warning that further cuts would require growth to fall short of current forecasts.

Estonian Governor Madis Muller also struck a cautious tone, suggesting the rate-cutting cycle may be “almost finished,” but acknowledged that visibility is limited. All three policymakers stressed that decisions ahead would remain data-driven, and that it was too early to rule out any scenario.

French Governor François Villeroy de Galhau and Lithuania’s Gediminas Šimkus declared victory over inflation. However, both underlined the importance of maintaining flexibility in the face of mounting global uncertainty. Villeroy also reassured that “We have tools to react if there's deflation.”

Elliott Wave Update: Silver (XAGUSD) Breaks Out – What’s the Paths Forward?

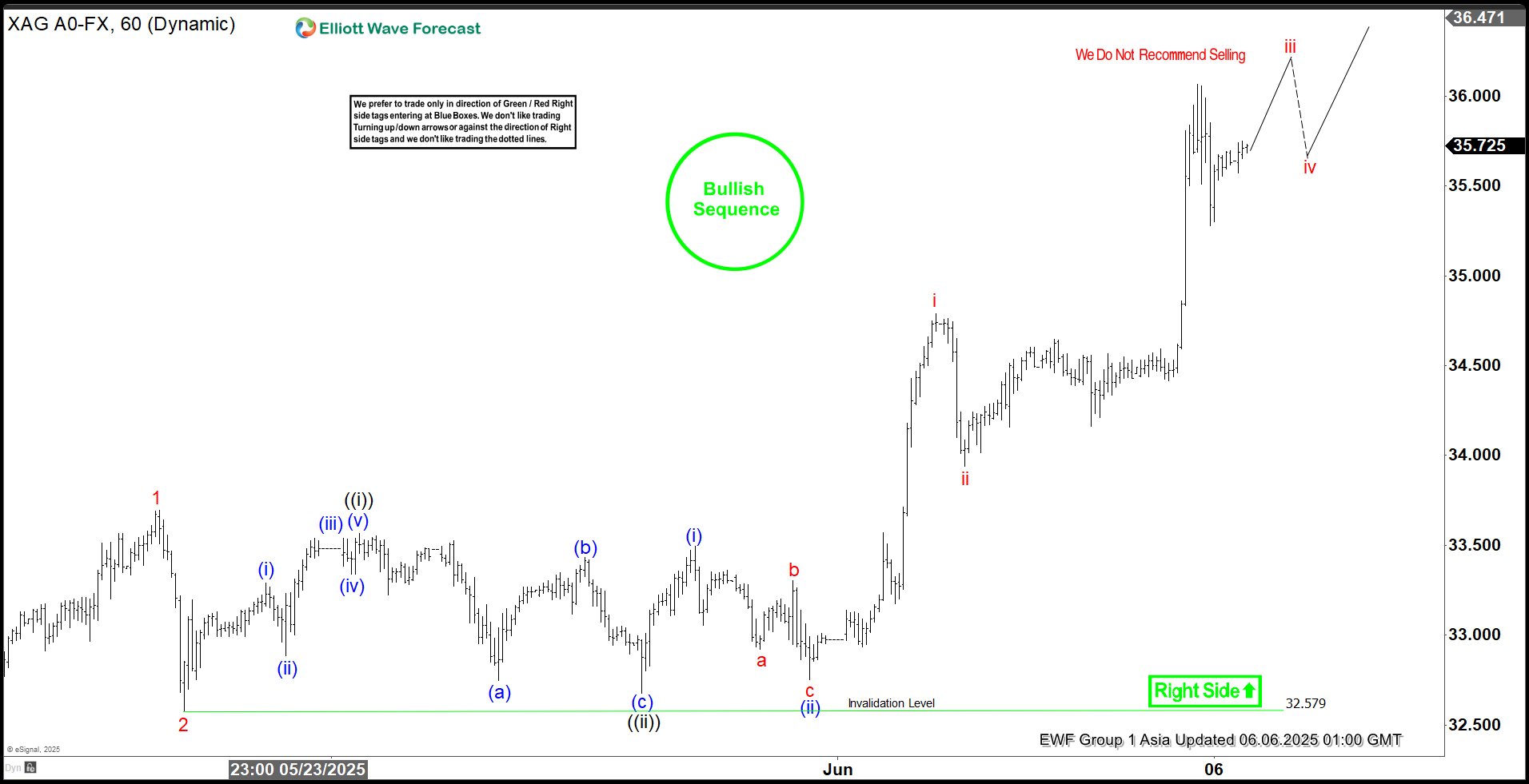

Silver has experienced a significant breakout, decisively surpassing its previous high from October 2024. This signals the start of the next upward leg in its price trajectory. From the last notable low on April 7, 2025, the rally has been unfolding as an impulsive wave with an extended structure, often referred to as a “nest.” Beginning from the April 7, 2025 low, wave (1) reached its peak at 33.684. It was then followed by a corrective pullback in wave (2), which concluded at 31.635. From this point, silver resumed its upward momentum in wave (3). The metal displays an internal subdivision characteristic of another impulsive wave.

Breaking down the progression from wave (2) low, the initial wave 1 advanced to 33.69. A subsequent dip in wave 2 found support at 32.58, as illustrated in the accompanying 1-hour chart. The metal then continued its ascent, nesting higher once again. From the wave 2 low, the sub-wave ((i)) peaked at 33.56. A pullback in wave ((ii)) then followed which bottomed out at 32.67. Silver then resumed its upward trend in wave ((iii)). Wave (i) of ((iii)) concluded at 33.49 and wave (ii) of ((iii)) ended at 32.75.

Looking ahead, silver is expected to achieve two additional highs to complete wave (iii) before encountering a corrective pullback in wave (iv). Afterwards, the upward trajectory should resume. In the near term, as long as the pivotal low at 32.58 remains intact, any dips are likely to attract buyers in 3, 7, or 11 swings, setting the stage for further upside potential. This technical analysis suggests a bullish outlook for silver, with the current structure supporting continued gains in the near future.

Silver (XAGUSD) 60-Minute Elliott Wave Technical Chart

XAGUSD Elliott Wave Technical Video

https://www.youtube.com/watch?v=pgT5TRbkU24

Euro Strengthens, Yen Consolidates Ahead of Nonfarm Payrolls Report

The major currency pairs, EUR/USD and USD/JPY, are showing restrained movement as markets await the release of key US employment data. Investors remain cautious, assessing the outlook for monetary policy in light of recent central bank decisions.

Today, market participants will focus on the release of the monthly US Nonfarm Payrolls (NFP) report. According to the consensus forecast, employment is expected to increase by 127K jobs in May, down from 177K in April and below the 12-month average of 156,800. The unemployment rate is projected to remain steady at 4.2%, consistent with recent months.

The anticipated slowdown in job growth is likely tied to ongoing economic uncertainty driven by trade tensions and the imposition of new tariffs. Weak ADP employment data, which showed a gain of only 37K jobs in May, has further raised concerns about the labour market. If the NFP data comes in below expectations, it may reinforce forecasts of potential interest rate cuts by the Federal Reserve in the coming months.

EUR/USD

Yesterday, the European Central Bank (ECB) cut its interest rate by 25 basis points to 2.15%. This marks the eighth rate reduction since May 2024, driven by a slowdown in eurozone inflation to 1.9%, below the ECB’s 2% target. ECB President Christine Lagarde noted that the bank is in a “strong position” to navigate the current global economic uncertainty, including trade tensions with the United States. This contributed to the strengthening of the EUR/USD pair to the 1.1490 level. Technical analysis of EUR/USD suggests a potential retest of the April high around 1.1570.

Key events that may impact EUR/USD pricing today include:

09:00 (GMT+3): Germany Industrial Production

11:30 (GMT+3): Speech by ECB President Christine Lagarde

12:00 (GMT+3): Eurozone GDP

12:00 (GMT+3): Eurozone Retail Sales for April

USD/JPY

USD/JPY is trading around 143.80, showing signs of consolidation after a recent decline. Yields on 30-year Japanese government bonds have dropped to 2.88%, and 10-year yields to 1.46%, reflecting rising bond prices. The decline in yields is linked to expectations of reduced issuance of ultra-long bonds by Japan’s Ministry of Finance following weak demand at recent auctions. This has strengthened the yen and weighed on the USD/JPY pair.

Nevertheless, buyers are managing to hold the price above the 142.50 support level, which could support a renewed upward move.

Key events that may influence USD/JPY pricing today:

15:30 (GMT+3): US Average Hourly Earnings

15:30 (GMT+3): US Nonfarm Payrolls

15:30 (GMT+3): US Unemployment Rate

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

ECB Cuts Rates. EUR/USD Spikes to 1.5-Month High

Yesterday, as widely expected, the European Central Bank (ECB) cut interest rates for the eighth time since May 2024. According to ForexFactory, the main refinancing rate was lowered from 2.40% to 2.15% (having stood at 4.50% in May 2024).

According to Reuters:

→ ECB President Christine Lagarde stated that interest rates are now at a “good level”, despite the extremely high uncertainty caused by tariff threats from President Donald Trump.

→ Following the press conference, markets interpreted the message as a sign that the ECB is unlikely to cut rates again at its next meeting in July.

In response to the ECB's decision, the EUR/USD rate jumped to its highest level in a month and a half, but later retreated (as indicated by the arrow) back to previous levels.

Technical Analysis of the EUR/USD Chart

Four days ago, while analysing the EUR/USD chart, we:

→ drew an ascending channel;

→ suggested that bullish momentum could push the EUR/USD rate up to the psychological level of 1.1500 during the current week.

In fact, at yesterday’s peak, the rate came very close to 1.1500. However, a candlestick with a long upper shadow had formed on the EUR/USD chart, by the end of the day. Additionally, this morning, the 1.1450 level has acted as a resistance zone.

This suggests bearish activity, which could pull the rate down towards the lower boundary of the local channel (outlined in black), and possibly even attempt a breakout below it.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

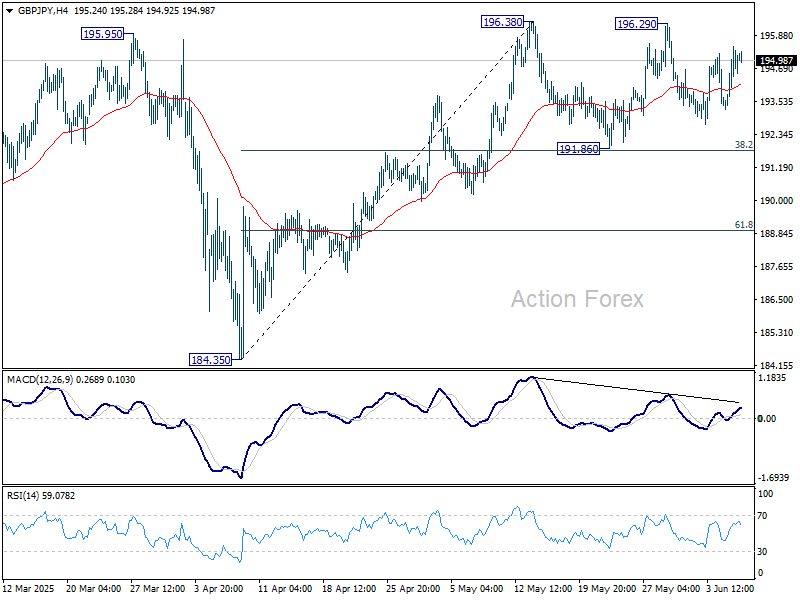

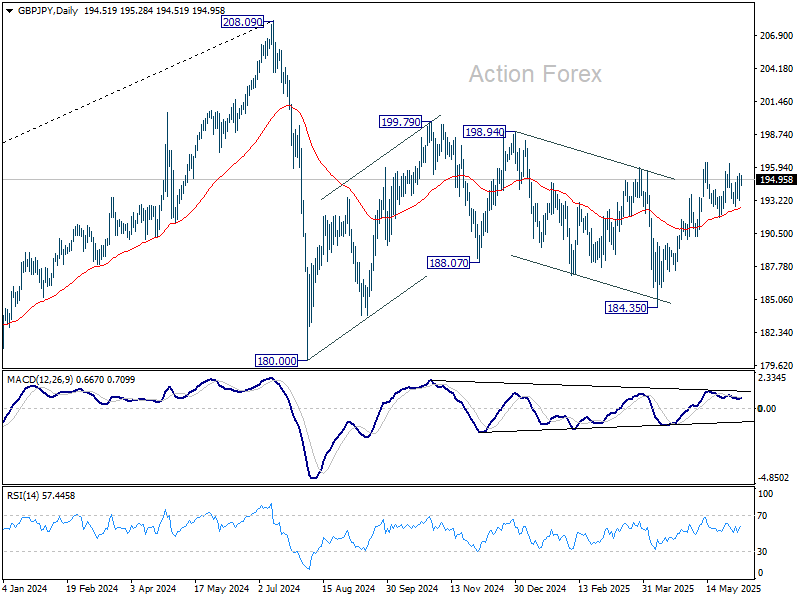

GBP/JPY Daily Outlook

Daily Pivots: (S1) 193.57; (P) 194.54; (R1) 195.80; More...

Intraday bias in GBP/JPY remains neutral as range trading continues. Further rise is in favor as long as 191.86 support holds. Firm break of 196.38 will resume whole rally from 184.35. However, firm break of 191.86 will indicate near term reversal and turn bias back to the downside.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

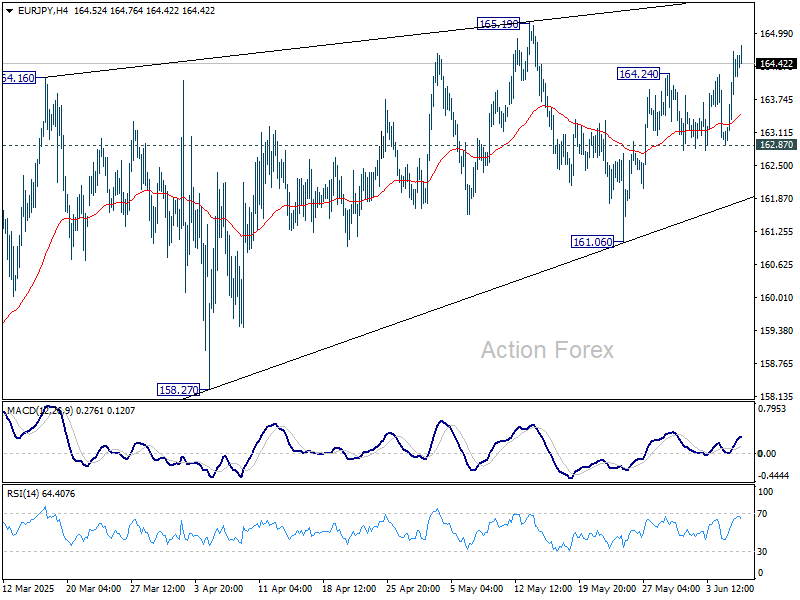

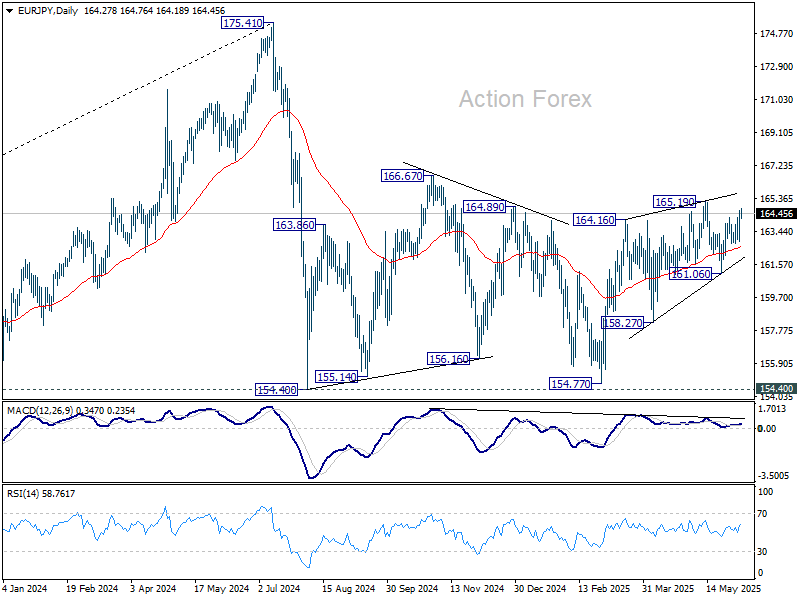

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.25; (P) 163.96; (R1) 165.04; More...

Intraday bias in EUR/JPY is back on the upside with break of 164.24. Firm break of 165.19 will resume whole rally from 154.77 and target 166.67 resistance next. For now further rise is expected as long as 162.87 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

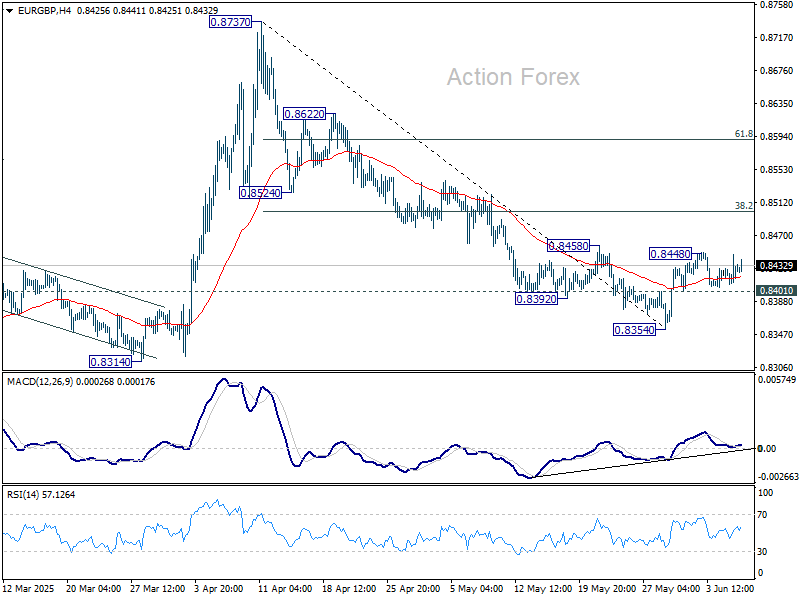

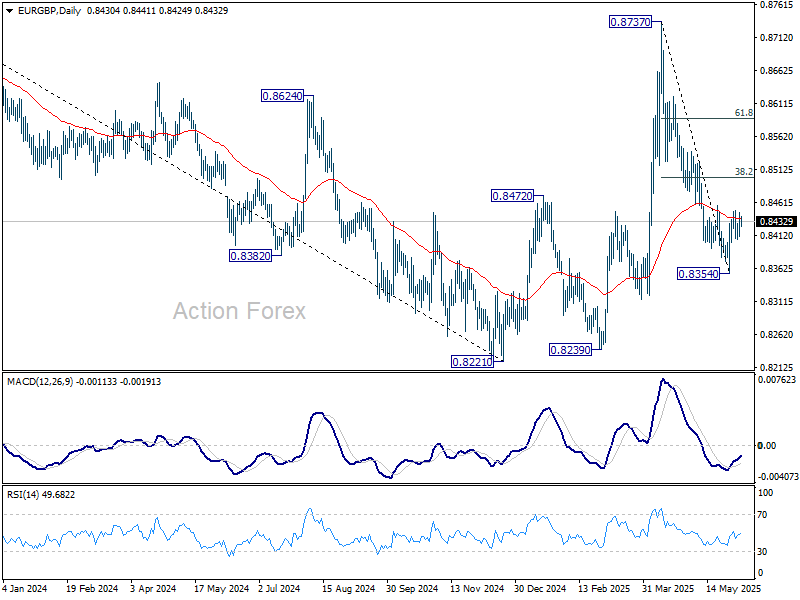

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8414; (P) 0.8431; (R1) 0.8451; More...

No change in EUR/GBP's outlook and intraday bias remains neutral. On the upside, above 0.8448 will resume the rebound to 38.2% retracement of 0.8737 to 0.8354 at 0.8500. On the downside, however, break of 0.8401 minor support will bring retest of 0.8354 low.

In the bigger picture, price actions from 0.8221 medium term bottom are merely forming a corrective pattern. There is no clear momentum to break through 0.8201 key support (2022 low) yet. Hence, range trading is expected between 0.8221/8737 for now.

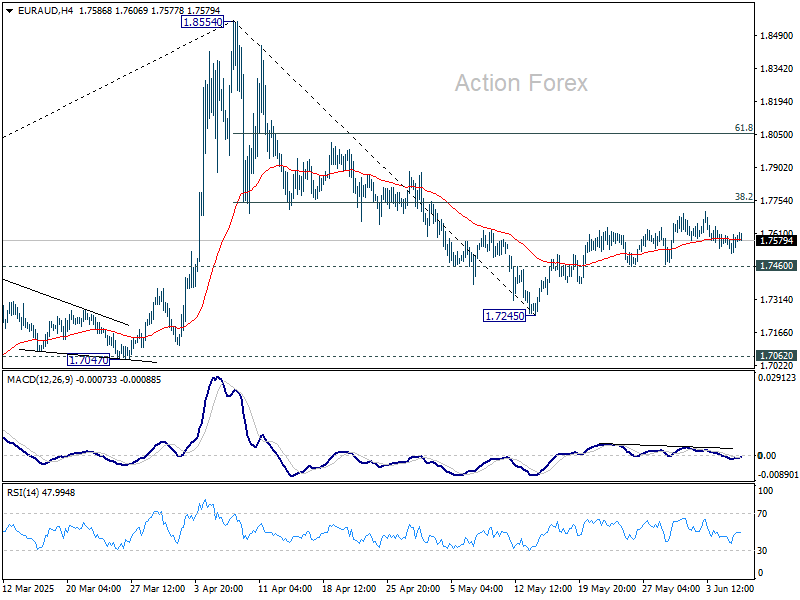

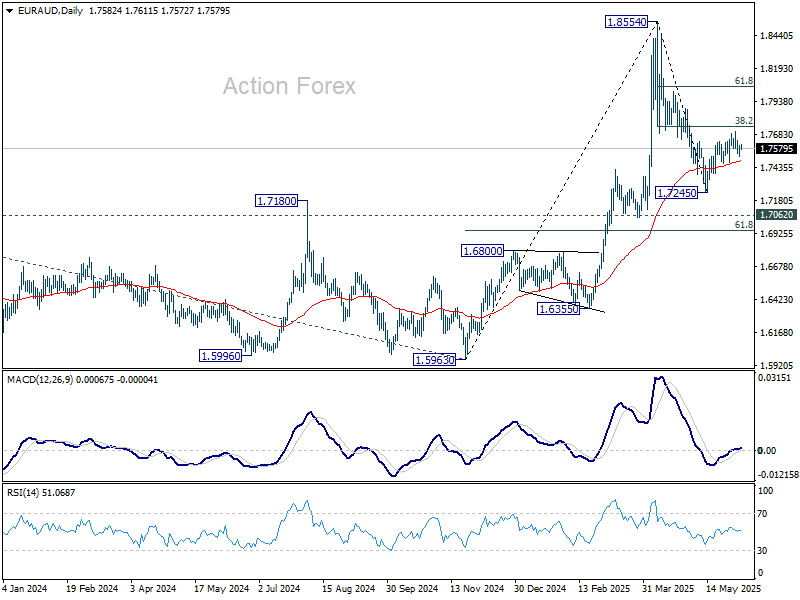

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7543; (P) 1.7574; (R1) 1.7624; More...

No change in EUR/AUD's outlook and intraday bias stays neutral. On the upside, firm break of 38.2% retracement of 1.8554 to 1.7245 at 1.7745 will solidify the case that fall from 1.8554 has completed as a correction. Next target is 61.8% retracement at 1.8054. On the downside, however, break of 1.7460 support will bring retest of 1.7245 instead.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 is expected after the whole corrective pattern from there completes. However, sustained break of 1.7062 will bring deeper fall back to 1.5963 support.

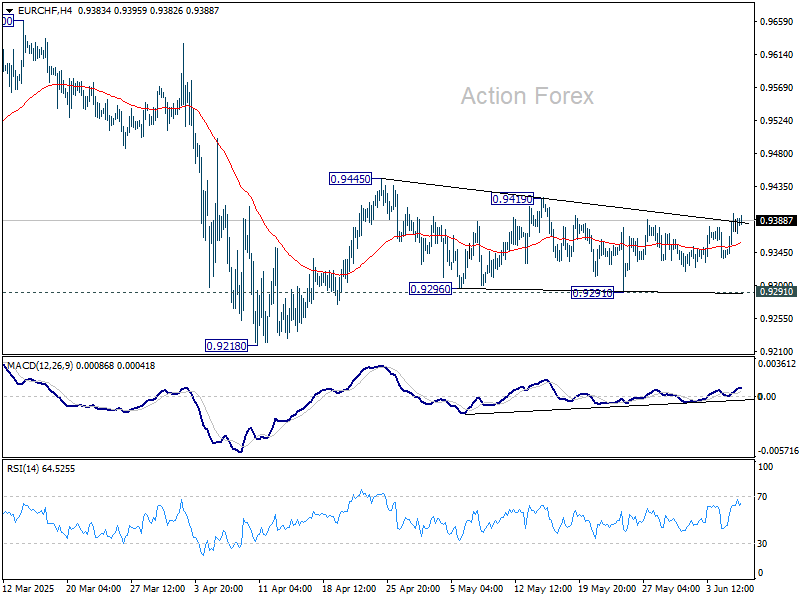

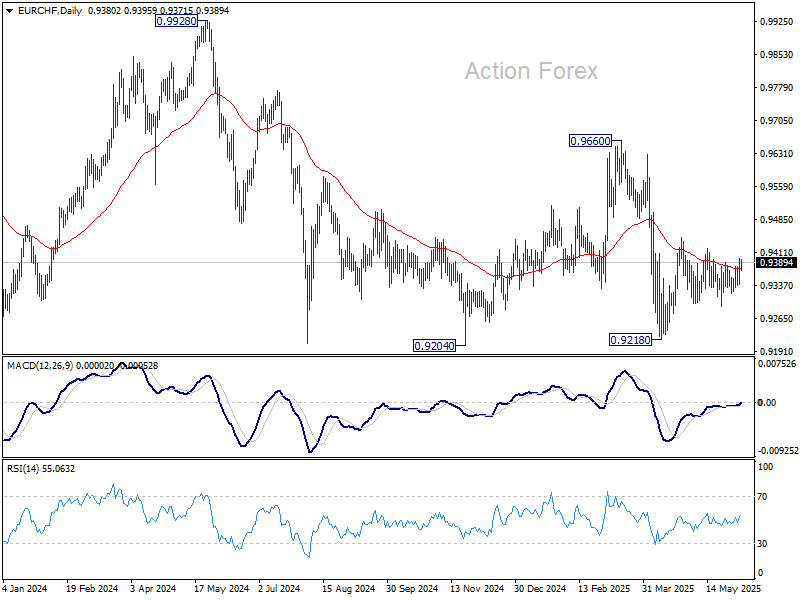

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9347; (P) 0.9374; (R1) 0.9408; More....

No change in EUR/CHF's outlook and intraday bias stays neutral. Rise from 0.9218 might continue, either as a correction to fall from 0.9660, or the third leg of the pattern from 0.9204. On the upside, above 0.9419 will target 0.9445 resistance and above. Nevertheless, on the downside, firm break of 0.9291 will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9527) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

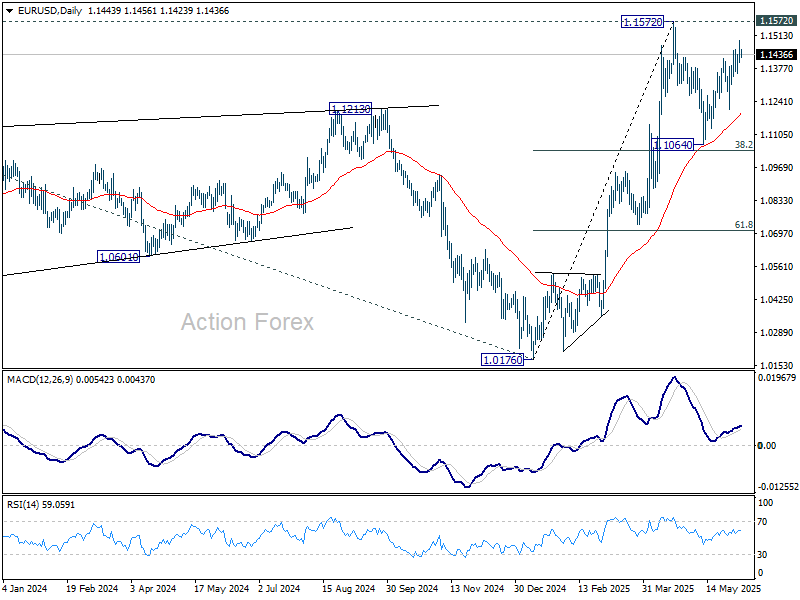

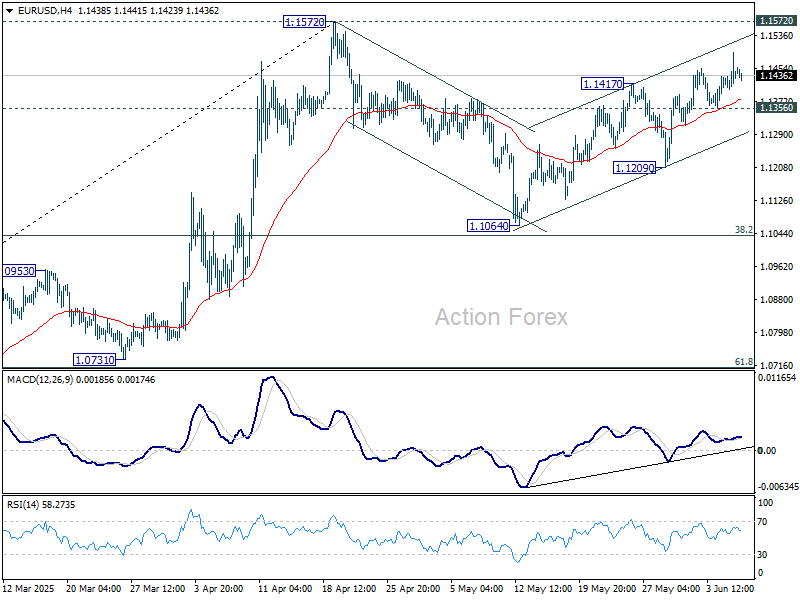

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1401; (P) 1.1448; (R1) 1.1491; More...

EUR/USD's rebound from 1.1064 is in progress and intraday bias stays mildly on the upside. Strong resistance could be seen from 1.1572 to limit upside, at least on first attempt. On the downside, On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 has started the third leg, and target 1.1209 support. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.