Sample Category Title

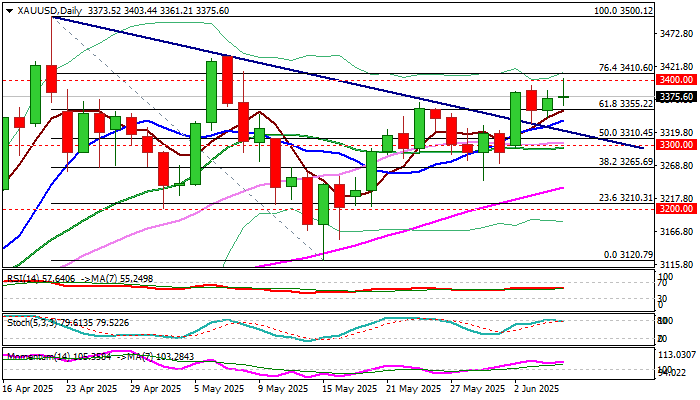

XAU/USD: Gold Hits One-Month High on Probe Through Strong $3.400 Resistance Zone

Gold cracked $3400 barrier in fresh acceleration that pushed the price to the highest in almost one month, dragged by today’s strong rise in silver price

Probe through significant barriers at $3400 zone (former recovery top / psychological / Fibo 76.4% of $3500/$3120 correction) is about to generate fresh bullish signal, which requires close above these barriers to be confirmed.

Technical picture remains bullish on daily chart, although overbought conditions are likely to provide more headwinds to fresh bulls.

Dips from new high ($3403) were so far shallow, with supports at $3384/80 zone (yesterday’s high / hourly lower platform / rising 10HMA) to hold dips and keep immediate bulls intact.

Sustained break of $3400 zone to signal continuation of recovery leg from $3120 towards $3437 (May 7 lower top) and key $3500 barrier in extension.

Pivotal supports lay at $3361/55 (Wednesday’s low / broken Fibo 61.8%) loss of which would weaken near-term structure and signal a false break higher.

Res: 3403; 3410; 3437; 3450.

Sup: 3380; 3365; 3355; 3343.

Export Slowdown Widens Canadian Trade Deficit in April

Canada's trade deficit widened from a revised $2.3 billion in March to $7.1 billion in April. This is the widest monthly trade deficit on record.

Merchandise exports cratered (-10.8% m/m) continuing their slide from February and March's much smaller declines. The drop in exports was broad-based, falling in 10 of 11 industries. Exports of passenger cars and light trucks (-22.9% m/m) heavily weighed on headline readings as buyers stockpiled in the months preceding auto tariffs. Sizeable decreases were also seen in exports of consumer goods (-15.4% m/m), energy products (-7.9% m/m), and industrial machinery and equipment (-22.5% m/m).

Merchandise imports were down by a more moderate 3.5% m/m in April. Once again, imports of motor vehicles and parts (-17.7% m/m) contributed most to the decline amid the implementation of tariffs. Industrial machinery, equipment, and parts (-9.5% m/m), consumer goods (-4.2% m/m) and electronics (-5.5% m/m) weighed on the total import reading.

In volume terms, merchandise exports were down by a hefty 9.1% m/m while imports moved lower by 2.9% m/m.

Canada's merchandise trade surplus with the United States shrunk to its smallest point since end-2020, currently at $3.6 billion as of April.

Key Implications

It was an abysmal month for Canadian trade but one that comes as no surprise. April marked the first month that Canada faced the full suite of American tariffs, most notably auto tariffs, which are imposing a massive headwind on auto trade. It is encouraging to see exports to non-U.S. markets ramp up over the past two months, but it hasn't been enough to offset the sizeable retraction in shipments south of the border.

A pull-forward in trade helped fuel healthy export gains in the first quarter, making a notable contribution to total Canadian GDP growth. While we only have one trade data point on the quarter, this story is due for a significant course-correction, with net trade pointing to a significant drag on second quarter growth. Risks to the near-term trade picture are also tilted to the downside. Canada recently paused many U.S. counter tariffs, which may buffer the impact on near-term imports, while exports are expected to dampen amid ongoing trade tensions.

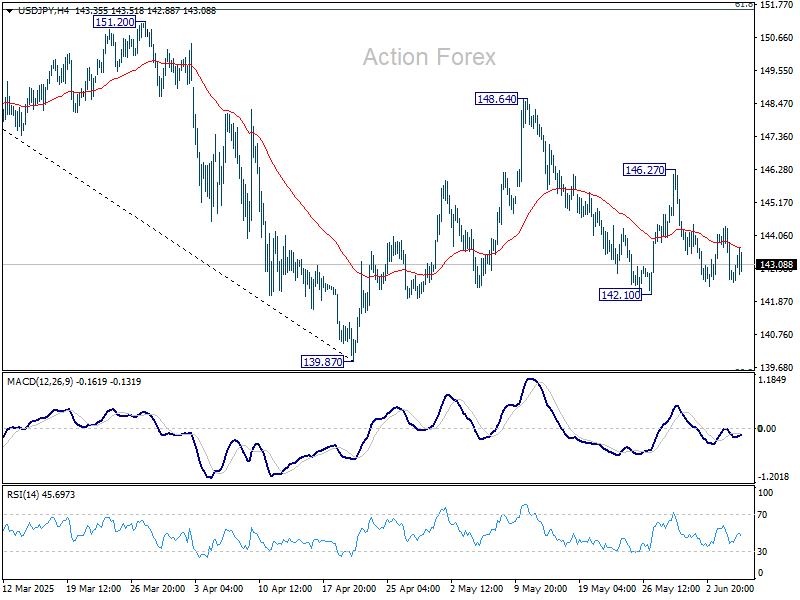

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.10; (P) 143.25; (R1) 143.88; More...

Range trading continues in USD/JPY and intraday bias remains neutral. On the upside, above 146.27 will target 148.64 resistance first. Firm break there will resume the rebound from 139.87. Nevertheless, break of 142.10 will bring deeper fall back to 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

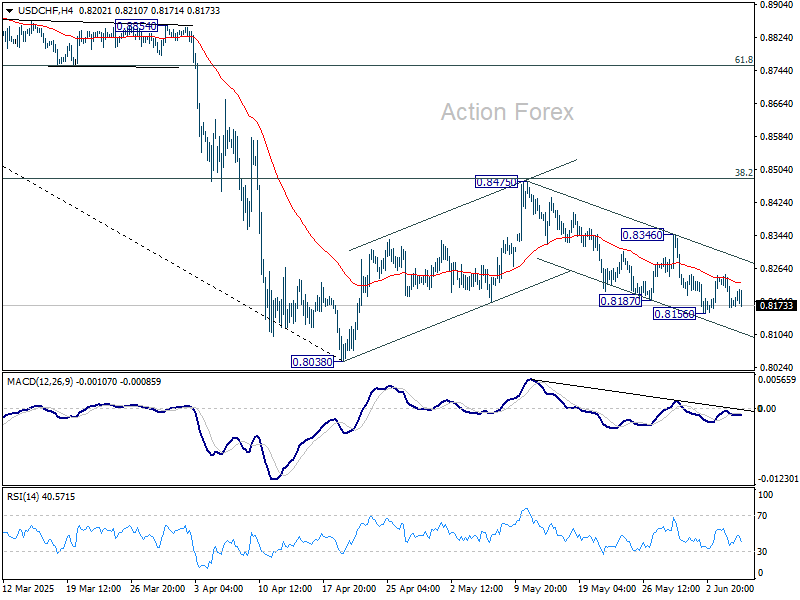

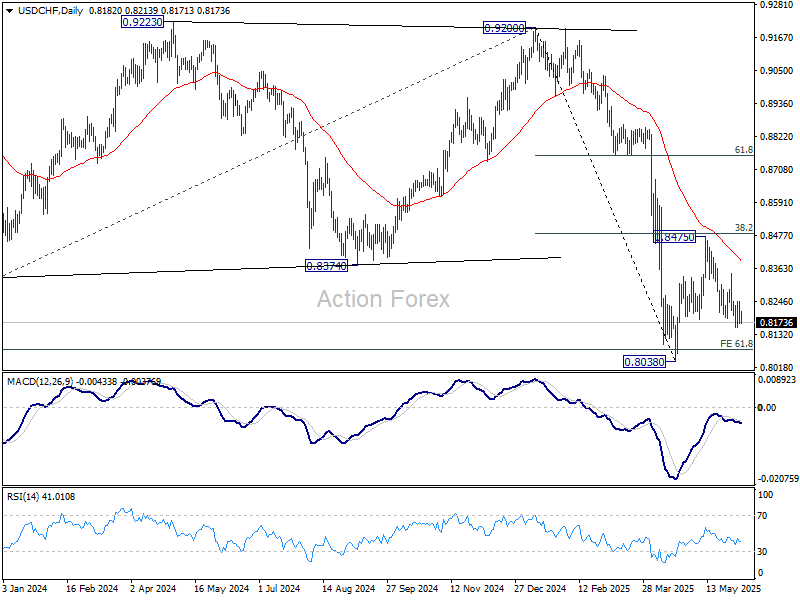

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8153; (P) 0.8202; (R1) 0.8233; More….

Intraday bias in USD/CHF remains neutral as it's staying in established range. Fall from 0.8475 could extend lower, and break of 0.8156 will target 0.8038 low. But strong support should be seen from there to bring rebound, at least on first attempt. On the upside, break of 0.8346 resistance will extend the corrective pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

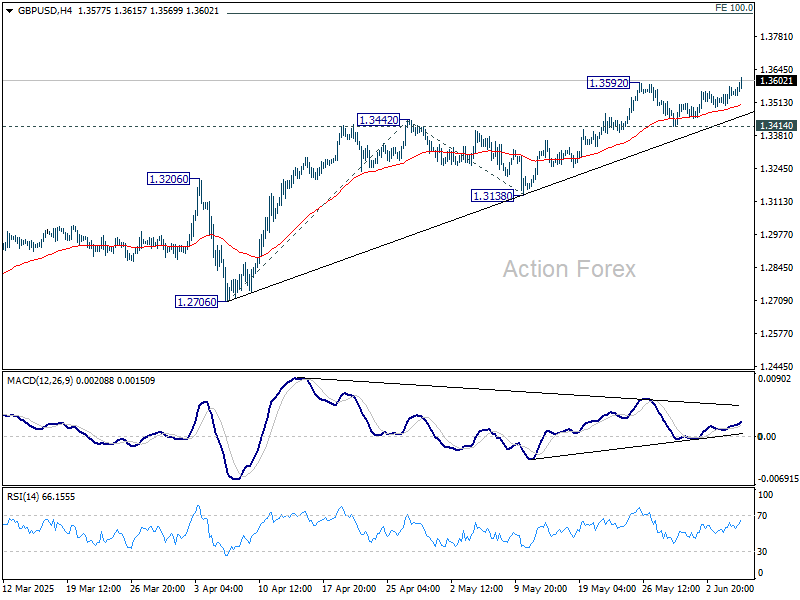

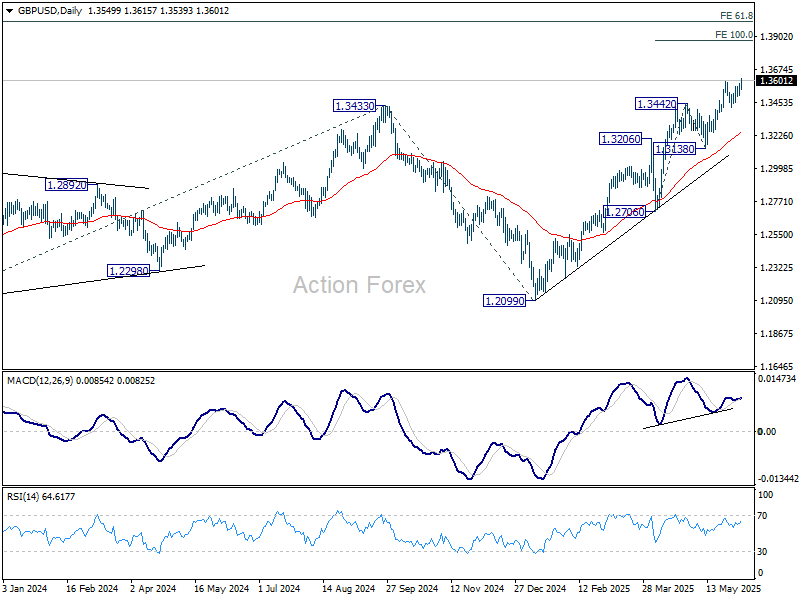

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3511; (P) 1.3545; (R1) 1.3590; More...

GBP/USD's rally resumed by breaking through 1.3592 resistance today. Intraday bias is back on the upside. Next target is 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. For now, near term outlook will stay bullish as long as 1.3414 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2866) holds, even in case of deep pullback.

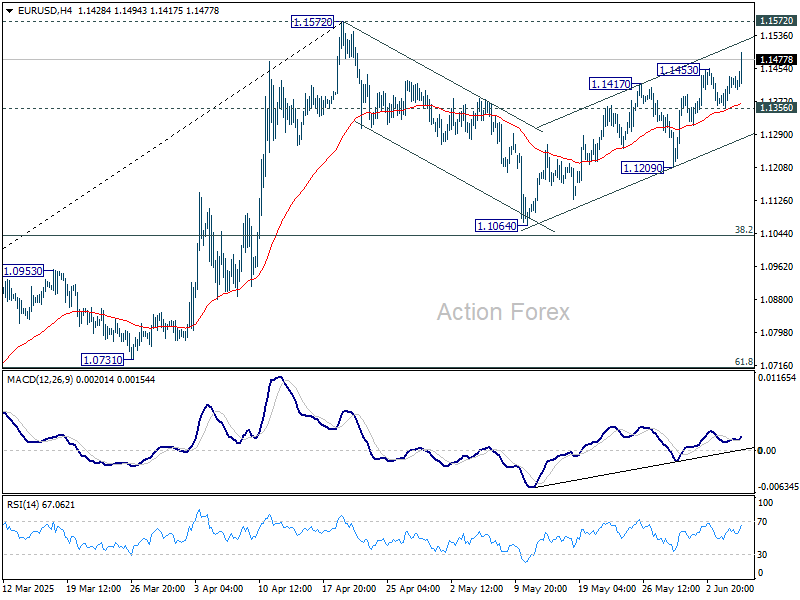

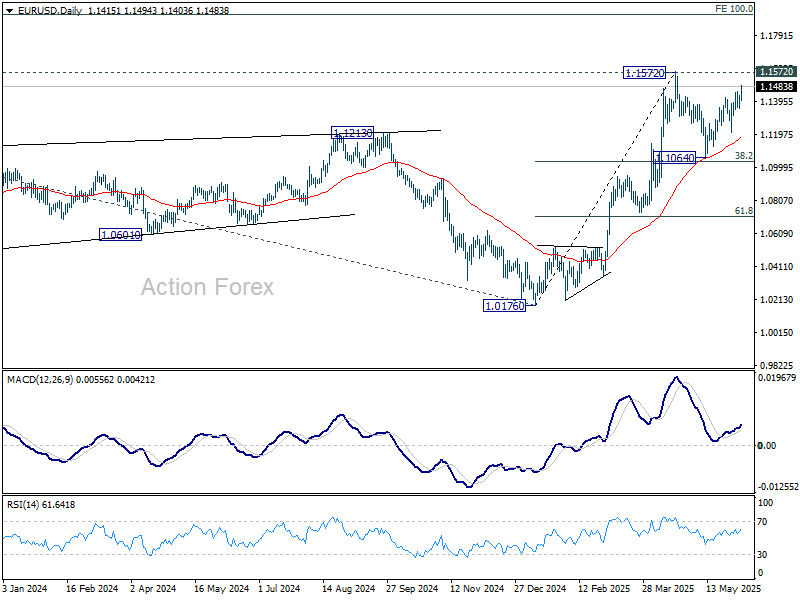

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1371; (P) 1.1403; (R1) 1.1449; More...

EUR/USD's rebound from 1.1064 resumed by breaking through 1.1453 today. Intraday bias is back on the upside for 1.1572 high. Strong resistance could be seen there to limit upside, at least on first attempt. On the downside, On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 has started the third leg, and target 1.1209 support. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

Euro Firms as ECB Lagarde Stays Confident; Silver Surges on Shift from US Assets

Euro surged against Dollar after ECB President Christine Lagarde struck a relatively confident tone in her post-meeting press conference. She downplayed immediate trade war fallout, stating that U.S. tariffs would likely impact growth more in 2026, by which time EU fiscal expansion—particularly military spending—would help cushion the blow.

Also, Lagarde emphasized that the ECB is well positioned to respond to prevailing uncertainties. There was no explicit signal of a pause in the easing cycle, but the emphasis on a "meeting-by-meeting" approach suggests the ECB will tread carefully going forward.

Meanwhile, US futures ticked up after Chinese state media reported that President Trump and President Xi had held a phone call, providing a modicum of relief amid heightened trade tensions. The news sparked a mild rally in US equity futures and lent support to risk-sensitive currencies like the Australian and Canadian Dollars.

However, Dollar itself faced renewed pressure following a surprising jump in initial jobless claims. The data added to a string of disappointing US labor signals this week—weak ADP job growth and declines in ISM employment components—raising the risk of a downside surprise in Friday’s NFP report.

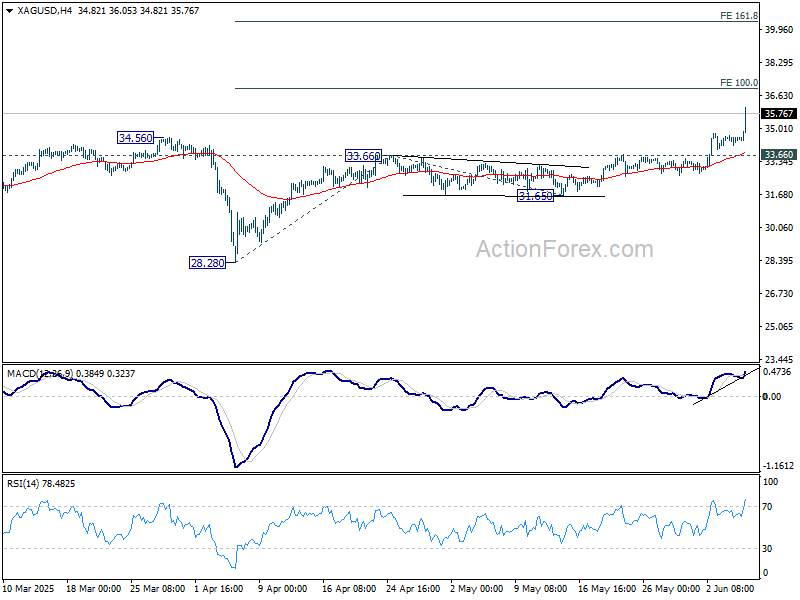

Elsewhere, Silver extended its rally and surged to its highest level in 13 years. The move reflects growing investor demand for tangible, supply-constrained assets amid structural uncertainties around US fiscal and trade policies.

For decades, persistent US current account deficits were offset by capital inflows into Treasuries and equities. That dynamic is now being reassessed, as sovereign wealth funds and large institutional investors rebalance away from the US due to rising geopolitical risk, trade protectionism, and concerns over long-term debt sustainability. This structural shift has driven renewed interest in precious and industrial metals.

Technically, next near term target for Silver is 100% projection of 28.28 to 33.66 from 31.65 at 37.03. Decisive break there will pave the way to 161.8% projection at 40.35. For now, outlook will remain bullish as long as 33.66 resistance turned support holds, in case of retreat.

In Europe, at the time of writing, FTSE is up 0.22%. DAX is up 0.52%. CAC is up 0.24%. UK 10-year yield is up 0.01 at 4.621. Germany 10-year yield is up 0.031 at 2.558. Earlier in Asia, Nikkei fell -0.51%. Hong Kong HSI rose 1.07%. China Shanghai SSE rose 0.23%. Singapore Strait Times rose 0.35%. Japan 10-year JGB yield fell -0.044 to 1.461.

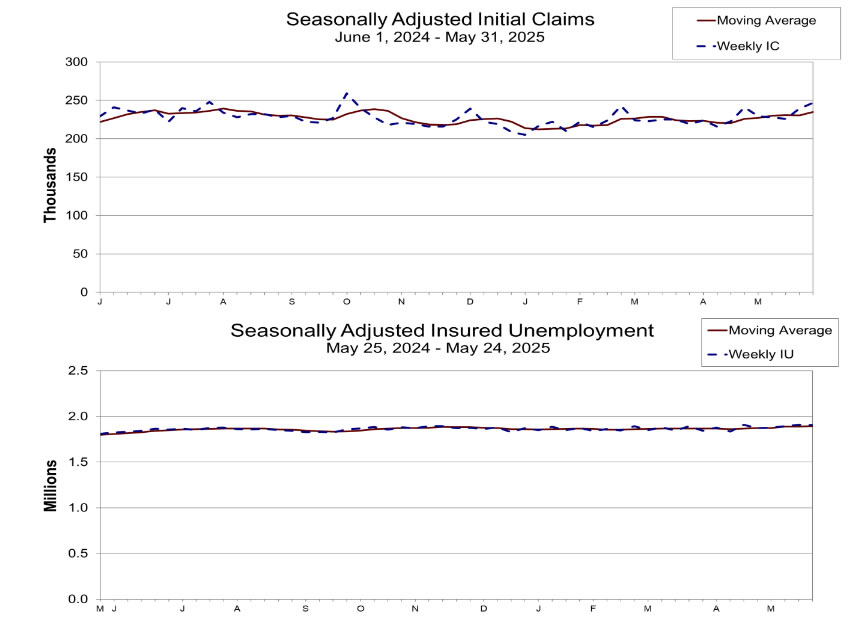

US initial jobless claims jump to 247k vs exp 235k

US initial jobless claims rose 8k to 247k in the week ending May 30, above expectation of 235k. Four-week moving average of initial claims rose 4.5k to 235k. Continuing claims fell -3k to 1904k in the week ending May 24. Four-week moving average of continuing claims rose 8k to 1895k, highest since November 27, 2021.

ECB cuts 25bps, downgrades inflation forecasts

ECB lowered deposit rate by 25bps to 2.00% as widely expected. The central bank cited “exceptional uncertainty,” and its commitment to a data-dependent, meeting-by-meeting approach, refraining from offering forward guidance on the future path of interest rates.

In the updated economic projections, ECB now expects headline inflation to average 2.0% in 2025 and 1.6% in 2026—down 0.3 percentage points from March's forecast. Headline inflation would then return to target at 2.0% in 2027. The revision was largely due to lower energy prices and a stronger Euro.

Core inflation is expected to ease to 2.4% in 2025 and 1.9% in both 2026 and 2027, broadly unchanged from previous forecasts.

On growth, ECB projects real GDP to expand by 0.9% in 2025, 1.1% in 2026, and 1.3% in 2027. While the 2025 GDP forecast remains unchanged due to a strong first quarter, ECB acknowledged that the remainder of the year looks weaker, in part due to trade-related uncertainty.

Weak global demand and potential retaliation to US tariffs could continue to drag on exports and business investment. However, rising public investment, particularly in defense and infrastructure, is expected to lend some support to growth in the medium term.

Eurozone PPI slumps -2.2% mom on energy prices

Eurozone PPI dropped sharply by -2.2% mom in April, steeper than the expected -1.8% mom. decline. Annual PPI rose just 0.7% yoy, below forecasts of 1.2% yoy. PPI ex-energy was up 0.1% mom, 1.1% yoy

The drag on Eurozone PPI was driven primarily by a -7.7% mom fall in energy prices. Prices for intermediate goods also declined slightly by -0.1% mom, while capital goods prices held flat. In contrast, consumer goods offered some offset, with durable and non-durable segments rising 0.1% mom and 0.3% mom respectively.

The broader EU showed a similar picture, with PPI falling -2.1% mom and rising just 0.6% yoy. Country-level data revealed significant monthly drops in industrial prices in France (-4.3%), Ireland (-4.0%), and Bulgaria (-4.9%). Only a handful of smaller economies like Cyprus and Malta posted slight increases.

Japan’s real wages fall -1.8% yoy in April, down for the fourth month

Real wages in Japan fell by -1.8% yoy in April, marking the fourth consecutive month of decline as persistent inflation continued to erode household purchasing power.

While nominal wages rose 2.3% yoy, slightly below the expected 2.6%, gains were outpaced by a still-elevated consumer inflation rate of 4.1%, driven by rising food and energy costs. The inflation metric used by the labor ministry has remained near 4% for five straight months, keeping real income in negative territory.

On the positive side, base salaries rose 2.2% yoy, the fastest increase in four months and well above March’s 1.4% yoy gain. This also marked the 42nd consecutive month of growth in regular pay. Overtime pay rebounded with a modest 0.8% yoy rise, while special payments grew 4.1% yoy.

China’s Caixin PMI composite falls to 49.6, contracts for first time since 2022

China’s Caixin PMI Services rose modestly from 50.7 to 51.1 in May, aligning with expectations. However, the gain in services was not enough to offset the drag from manufacturing, as PMI Composite slipped into contraction at 49.6, its first reading below 50 since December 2022.

Wang Zhe of Caixin Insight Group noted that the manufacturing slump was weighing heavily on the overall market, with new export orders remaining "sluggish" across both goods and services. Although input costs rose slightly, firms were unable to pass these on to customers, with selling prices continuing to fall and compressing profit margins.

Caixin flagged "unfavorable factors remain relatively prevalent", with growing external trade uncertainty and "noticeable weakening" in macro indicators at the start of Q2. The "significantly intensified"downward pressure raises the urgency for further targeted policy support.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1371; (P) 1.1403; (R1) 1.1449; More...

EUR/USD's rebound from 1.1064 resumed by breaking through 1.1453 today. Intraday bias is back on the upside for 1.1572 high. Strong resistance could be seen there to limit upside, at least on first attempt. On the downside, On the downside, break of 1.1356 support will indicate that the corrective pattern from 1.1572 has started the third leg, and target 1.1209 support. Nevertheless, decisive break of 1.1572 will confirm larger up trend resumption.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0856) holds.

US initial jobless claims jump to 247k vs exp 235k

US initial jobless claims rose 8k to 247k in the week ending May 30, above expectation of 235k. Four-week moving average of initial claims rose 4.5k to 235k.

Continuing claims fell -3k to 1904k in the week ending May 24. Four-week moving average of continuing claims rose 8k to 1895k, highest since November 27, 2021.

ECB cuts 25bps, downgrades inflation forecasts

ECB lowered deposit rate by 25bps to 2.00% as widely expected. The central bank cited “exceptional uncertainty,” and its commitment to a data-dependent, meeting-by-meeting approach, refraining from offering forward guidance on the future path of interest rates.

In the updated economic projections, ECB now expects headline inflation to average 2.0% in 2025 and 1.6% in 2026—down 0.3 percentage points from March's forecast. Headline inflation would then return to target at 2.0% in 2027. The revision was largely due to lower energy prices and a stronger Euro.

Core inflation is expected to ease to 2.4% in 2025 and 1.9% in both 2026 and 2027, broadly unchanged from previous forecasts.

On growth, ECB projects real GDP to expand by 0.9% in 2025, 1.1% in 2026, and 1.3% in 2027. While the 2025 GDP forecast remains unchanged due to a strong first quarter, ECB acknowledged that the remainder of the year looks weaker, in part due to trade-related uncertainty.

Weak global demand and potential retaliation to US tariffs could continue to drag on exports and business investment. However, rising public investment, particularly in defense and infrastructure, is expected to lend some support to growth in the medium term.

(ECB) Monetary policy decisions

5 June 2025

The Governing Council today decided to lower the three key ECB interest rates by 25 basis points. In particular, the decision to lower the deposit facility rate – the rate through which the Governing Council steers the monetary policy stance – is based on its updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission.

Inflation is currently at around the Governing Council’s 2% medium-term target. In the baseline of the new Eurosystem staff projections, headline inflation is set to average 2.0% in 2025, 1.6% in 2026 and 2.0% in 2027. The downward revisions compared with the March projections, by 0.3 percentage points for both 2025 and 2026, mainly reflect lower assumptions for energy prices and a stronger euro. Staff expect inflation excluding energy and food to average 2.4% in 2025 and 1.9% in 2026 and 2027, broadly unchanged since March.

Staff see real GDP growth averaging 0.9% in 2025, 1.1% in 2026 and 1.3% in 2027. The unrevised growth projection for 2025 reflects a stronger than expected first quarter combined with weaker prospects for the remainder of the year. While the uncertainty surrounding trade policies is expected to weigh on business investment and exports, especially in the short term, rising government investment in defence and infrastructure will increasingly support growth over the medium term. Higher real incomes and a robust labour market will allow households to spend more. Together with more favourable financing conditions, this should make the economy more resilient to global shocks.

In the context of high uncertainty, staff also assessed some of the mechanisms by which different trade policies could affect growth and inflation under some alternative illustrative scenarios. These scenarios will be published with the staff projections on the ECB’s website. Under this scenario analysis, a further escalation of trade tensions over the coming months would result in growth and inflation being below the baseline projections. By contrast, if trade tensions were resolved with a benign outcome, growth and, to a lesser extent, inflation would be higher than in the baseline projections.

Most measures of underlying inflation suggest that inflation will settle at around the Governing Council’s 2% medium-term target on a sustained basis. Wage growth is still elevated but continues to moderate visibly, and profits are partially buffering its impact on inflation. The concerns that increased uncertainty and a volatile market response to the trade tensions in April would have a tightening impact on financing conditions have eased.

The Governing Council is determined to ensure that inflation stabilises sustainably at its 2% medium-term target. Especially in current conditions of exceptional uncertainty, it will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. The Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Key ECB interest rates

The Governing Council today decided to lower the three key ECB interest rates by 25 basis points. Accordingly, the interest rates on the deposit facility, the main refinancing operations and the marginal lending facility will be decreased to 2.00%, 2.15% and 2.40% respectively, with effect from 11 June 2025.

Asset purchase programme (APP) and pandemic emergency purchase programme (PEPP)

The APP and PEPP portfolios are declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

***

The Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation stabilises sustainably at its 2% target over the medium term and to preserve the smooth functioning of monetary policy transmission. Moreover, the Transmission Protection Instrument is available to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across all euro area countries, thus allowing the Governing Council to more effectively deliver on its price stability mandate.

The President of the ECB will comment on the considerations underlying these decisions at a press conference starting at 14:45 CET today.