Sample Category Title

USD/JPY Daily Outlook

Daily Pivots: (S1) 142.10; (P) 143.25; (R1) 143.88; More...

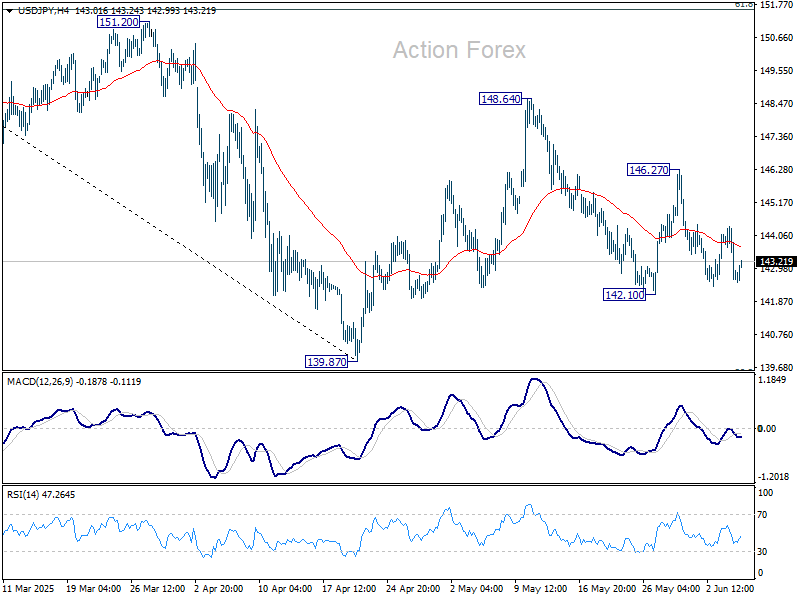

USD/JPY is still bounded in range trading and intraday bias remains neutral. On the upside, above 146.27 will target 148.64 resistance first. Firm break there will resume the rebound from 139.87. Nevertheless, break of 142.10 will bring deeper fall back to 139.87 low.

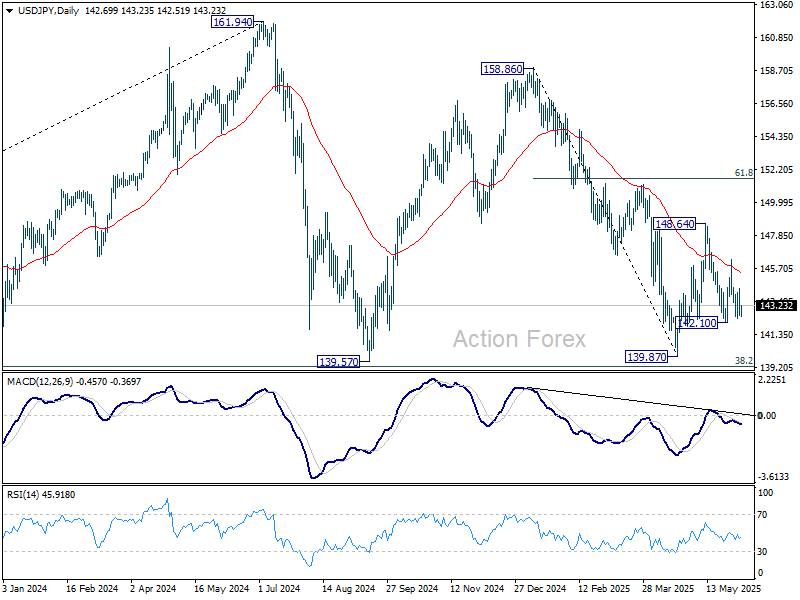

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

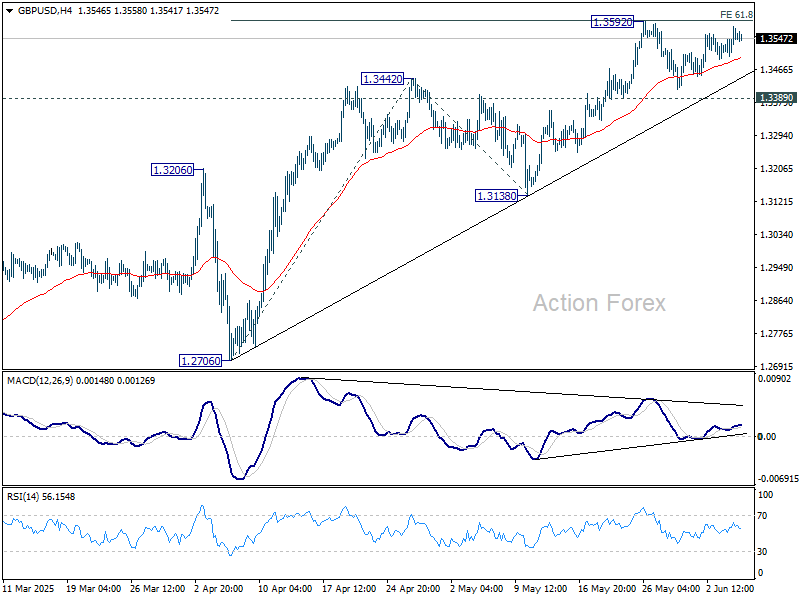

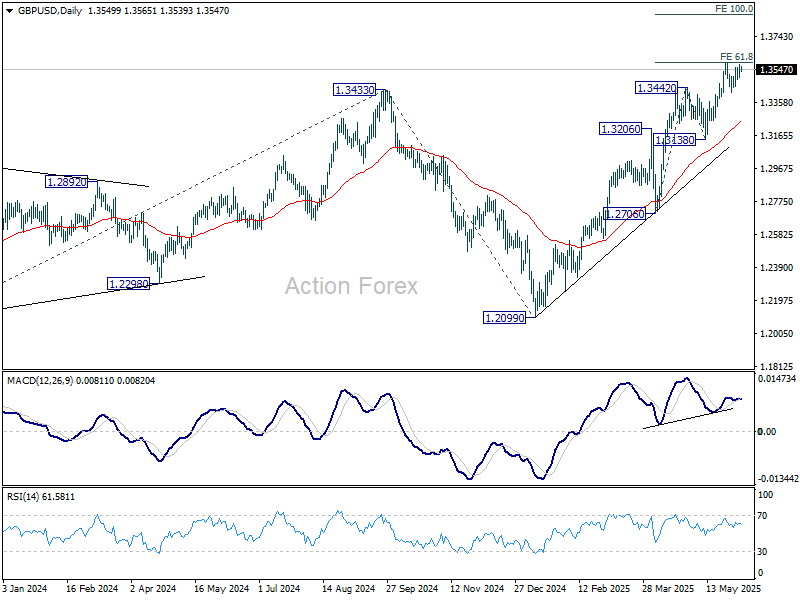

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3511; (P) 1.3545; (R1) 1.3590; More...

Intraday bias in GBP/USD remains neutral as it's still bounded in range below 1.3592. With 1.3389 support intact, further rise is expected. On the upside, firm break of 1.3592 will resume larger up trend to 100% projection of 1.2706 to 1.3442 from 1.3138 at 1.3874. However, decisive break of 1.3389 will turn bias back to the downside for 1.3138 support instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2866) holds, even in case of deep pullback.

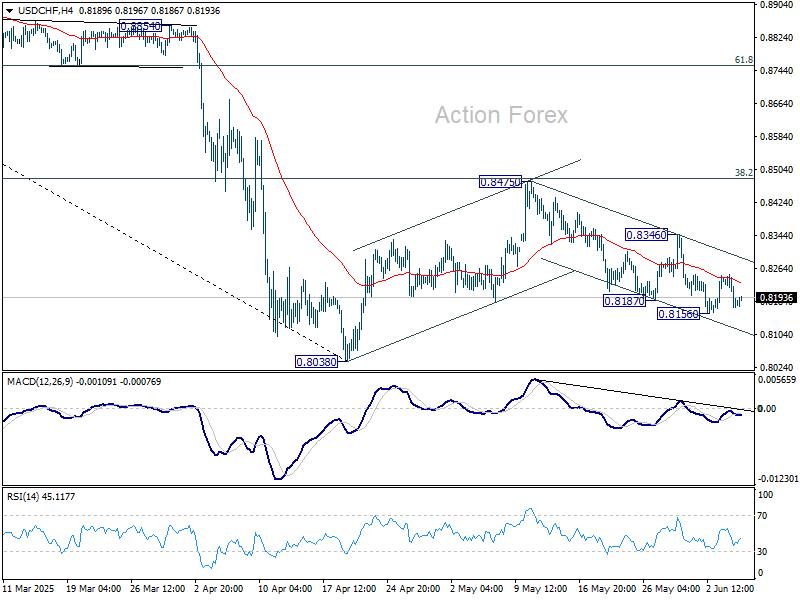

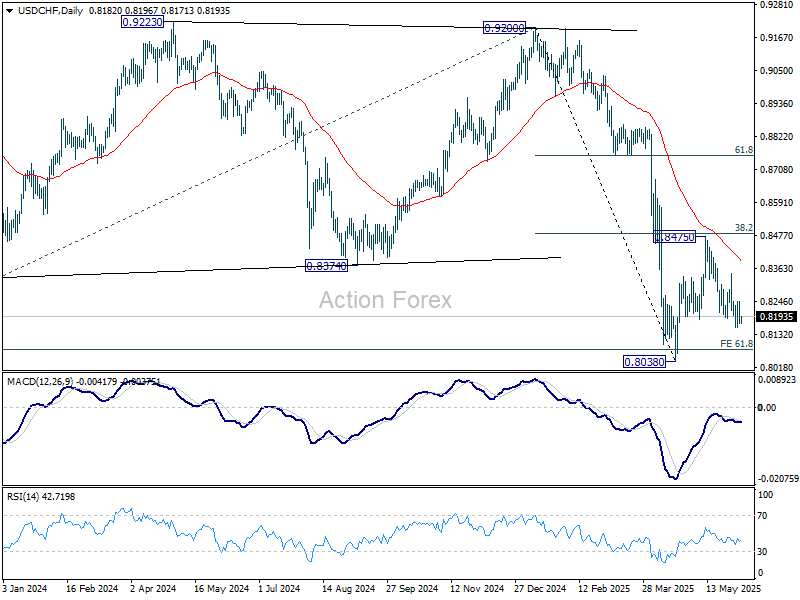

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8153; (P) 0.8202; (R1) 0.8233; More….

Range trading continues in USD/CHF and intraday bias stays neutral. Fall from 0.8475 could extend lower, and break of 0.8156 will target 0.8038 low. But strong support should be seen from there to bring rebound, at least on first attempt. On the upside, break of 0.8346 resistance will extend the corrective pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

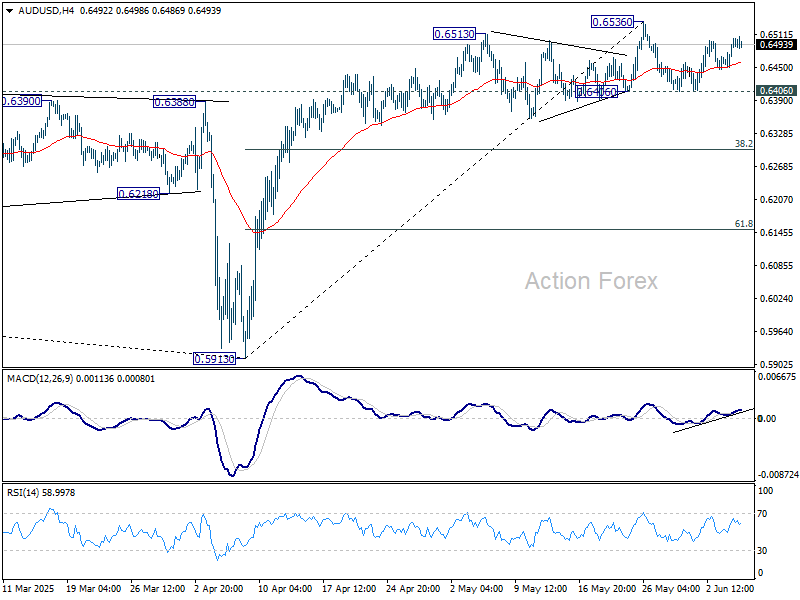

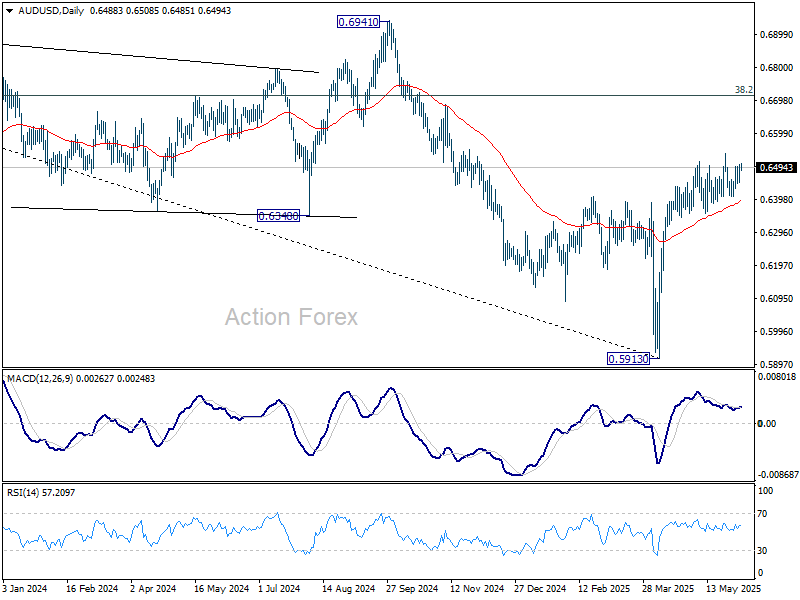

AUD/USD Daily Report

Daily Pivots: (S1) 0.6460; (P) 0.6483; (R1) 0.6514; More...

Range trading continues in AUD/USD and intraday bias remains neutral. With 0.6406 support intact, further rally is expected. On the upside, firm break of 0.6536 will resume the rally from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, decisive break of 0.6406 will confirm short term topping, and turn bias back to the downside for 38.2% retracement of 0.5913 to 0.6536 at 0.6298.

In the bigger picture, AUD/USD is still struggling to sustain above 55 W EMA (now at 0.6441) cleanly, and outlook is mixed. Sustained trading above 55 W EMA will indicate that rise from 0.5913 is at least correcting the down trend from 0.8006 (2021 high), with risk of trend reversal. Further rise should be seen to 38.2% retracement of 0.8006 to 0.5913 at 0.6713. However, rejection by 55 W EMA will revive medium term bearishness for another fail through 0.5913 at a later stage.

Markets and Fed Governors Still Navigating Implications of ‘Stagflationary Dichotomy’ for Policy

Markets

Markets and Fed governors are still in the process of navigating the implications of the ‘stagflationary dichotomy’ for policy going forward. Fed’s Kashkari in an interview held the line that, at least for now, the Fed has the time to assess the impact on inflation that hasn’t returned to target yet, even as uncertainty via several channels (e.g. investment) might weigh on activity at some point in the future. Markets yesterday switched attention to growth rather than to inflation risks. ADP growth slowed sharply (37k vs 114k expected), followed by a disappointing services ISM. The headline index dropped below the 50 mark (49.9) and poor new orders (46.4) suggest more trouble ahead. At the same time, a better reading for employment (50.7) and a further rise in the prices paid subseries (68.7) were ignored. US yields dropped 8.5 bps (2-y) to 10.4 bps (30-y). Aside from softening Fed rate cut expectations, the strong performance at the long end of the curve also caught the eye. For now, investors don’t feel the need to further push the deficit theme. Shorts at the long end of the curve apparently took some chips off the table. The real reality check will come with tomorrow’s US payrolls. German yields this time fully disconnected from the US with investors in wait-and-see modus ahead of today’s ECB meeting. Yields change less than 2 bps across the curve. The dollar suffered from the combined ADP/ISM miss, but the damage could have been bigger. No technically important barriers were challenged (DXY close 98.78; EUR/USD 1.1417). US equities simply maintained recent gains, even as the stalemate in trade negotiations between the US and most of its main trading partners persists.

This morning, the focus in Asian markets was on a Japanese 30-y bond auction. Bonds rally after the sale even as the bid-cover ratio was far from convincing. As in the US yesterday, this suggests that the pressure at the long end of the curves(s) might be easing, at least temporarily. US markets probably face an ‘interludium ahead of tomorrow’s payrolls, with only the trade balance data and jobless claims scheduled for release. Question is whether the ECB policy decision will bring some more inspiring insights for European investors. Anything different from a 25 bps cut to 2.0% would be a huge surprise. The market focus will be on the now ECB staff projections and the press conference from ECB’s Lagarde. Staff projections will probably confirm that the ECB will meet its inflation target over the policy horizon. Interesting to see the assessment on growth, as recent hard data mostly were better than expected. With the ECB now ‘deep’ in neutral territory, we expect chair Lagarde to switch to a highly data/tariffs depended bias with little directional guidance. With still more than one additional 25 bps cut discounted, we expect the downside in European yields be rather well protected.

News & Views

The Bank of Canada kept its policy rate for second consecutive meeting unchanged at 2.75% yesterday. Growth was slightly stronger than the BoC had forecast in Q1. The pull-forward of exports to the United States and inventory accumulation boosted activity, with final domestic demand roughly flat. The economy is expected to be considerably weaker in Q2 as these effects reverse. The labour market has softened, particularly in trade-intensive sectors, and unemployment has risen to 6.9%. The BoC’s preferred measures of core inflation moved up while the elimination of the federal consumer carbon tax reduced headline inflation by 0.6 ppt (1.7% in April instead of 2.3%). Household inflation expectations are rising over tariff treats with many businesses saying they’ll pass on higher costs. The BoC holds a wait-and-see approach as it balances the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs. The Canadian dollar extended gains against the USD as some expected a rate cut or at least a softer signal from the BoC. USD/CAD closed at its lowest level since October (1.3678). Canadian money markets discount another 25 bps rate cut after Summer.

The US Congressional Budget Office (CBO) calculated that US President Trump’s big beautiful bill would increase budget deficits by $2.4tn over the next 10 year compared with doing nothing. The bill would lower tax revenues by $3.75tn while cutting spending by around $1.3tn. In a separate report, the CBO said that the tariffs in place as of May 13 would reduce budget deficits by $2.8tn over a decade if they remain, or more than the deficit increase from the bill. They didn’t take into account macro-economic effects with import duties expected to lift inflation by an average of 0.4% this year and next while reducing growth by 0.6% by 2035. Those estimates are obviously subject to significant uncertainty.

The World May be Wobbling, But Markets March On

Here’s a fun fact: the iShares MSCI All World Index just hit a fresh all-time high yesterday, only a few hours after the OECD cut the global growth forecast, citing global trade uncertainties, tighter monetary conditions, and weakened consumer and business sentiment.

Add to that the rising worries around some major economies’ ability to finance their ballooning debt and the recent spike in long-maturity sovereign bond yields, and you've got a pretty murky picture.

Even Elon Musk is growing frustrated with Trump’s ‘Big Beautiful Tax Bill’, reportedly saying he realized that the carnage at DOGE — and the hit to his reputation — were simply not worth it. In today’s context, the U.S. deficit is expected to grow by another $2.5 trillion over the next decade. But we’ll likely reach the $40 trillion mark well before that, probably around 2030.

Yet investors couldn’t care less. Dips in equity markets are still seen as opportunities to buy cheaper. And while the data is fun to watch (and sometimes useful to dilute Trump headlines), it remains secondary to the blind bullishness. That’s the takeaway from the post–April 2nd rally: the world may be wobbling, but markets march on.

On the trade and data front, the news is less than ideal. The latest headlines suggest that US–EU negotiations could be getting back on track, but with few details. Meanwhile, US–China talks are going nowhere, with Xi unwilling to talk unless Trump makes concessions.

Trump is visibly frustrated with China’s resilience but China holds a powerful card: rare earth metals. They supply around 90% of global rare earth elements, essential for carmakers and tech producers. These metals aren’t rare like gold or platinum — they’re found in many places, but not in concentrated form. You need to mine and refine them, and China excels at doing that cheaply.

That’s why we all depend on China for these 17 elements, and it’s said that it would take the US 5–10 years to build the necessary refining capacity. China knows it. A restriction in rare earth exports could have serious economic consequences. But Xi isn’t sitting down without real concessions — on tech, on tariffs, you name it. Even the UK, temporarily exempt from the 50% steel and aluminium tariffs, is back at the table, warning that uncertainty isn’t going anywhere.

Markets, for now, are ignoring it. But for how long?

Because yesterday’s ISM services data showed a surprise contraction, and the ADP jobs report was weak, just 37,000 new private jobs last month. Over the past four months, three readings came in under 100K, and one under 50K. Historically, a string of sub-50K prints often signals recession is knocking.

But weak data just boosts rate-cut hopes. Markets now expect two Federal Reserve (Fed) rate cuts by year-end, the first likely in September. The US 2-year yield fell below 3.90%, limiting equity downside — the S&P 500 closed flat.

That’s the magic, right? Good data = optimism on growth. Bad data = optimism on rate cuts.

The only problem is: the Fed says it won’t cut until it sees tariffs affect inflation. That part... goes unheard.

Interestingly, the US dollar is one of the few assets reflecting trade pessimism, and its weakness helps stabilize European inflation. The flash CPI for May suggests eurozone headline inflation dipped below the European Central Bank’s (ECB) 2% target.

That gives the ECB breathing room to cut rates with confidence today — a 25bp cut is expected, marking the seventh consecutive meeting with a cut, and the eighth since early last year. Combined with fiscal stimulus plans, the easing bolsters the European growth story — and the euro. The single currency still needs a strong catalyst to break above the 1.1450/1.15 resistance. But it feels like a matter of time.

Across the Pacific, the Bank of Canada (BoC) paused its rate cuts, but that didn’t stop USDCAD shorts from pushing the pair below a key long-term Fibonacci level — the 38.2% retracement of the 2021–2025 rally. The USDCAD is now consolidating in the long-term bearish zone, with prospects of further downside toward 1.30–1.33.

And that’s despite oil prices coming under pressure. WTI crude remains above its 50-DMA, but is losing momentum. Even escalating tensions between Russia and Ukraine, and a 4 million barrel drop in US weekly inventories, couldn’t drive prices higher. The failure to rally past $64/barrel suggests the recent uptrend may have peaked, and a new wave of weakness may be on the horizon.

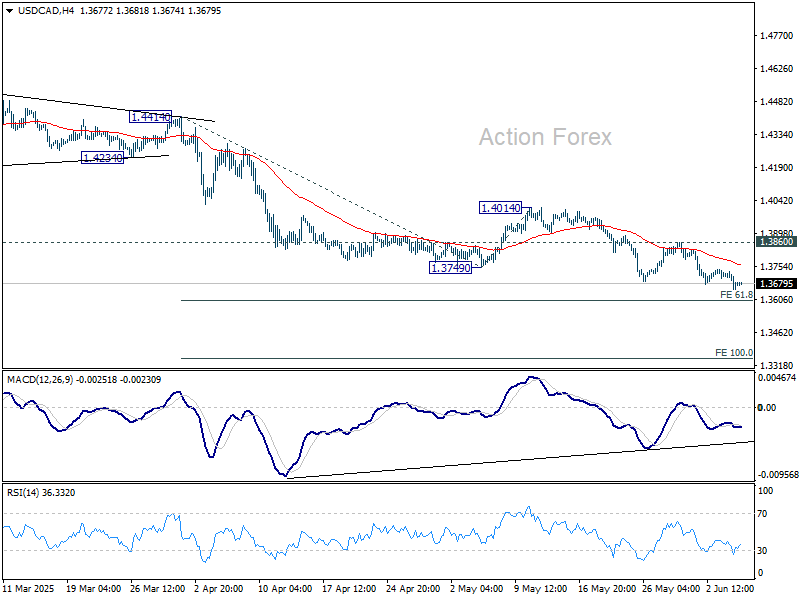

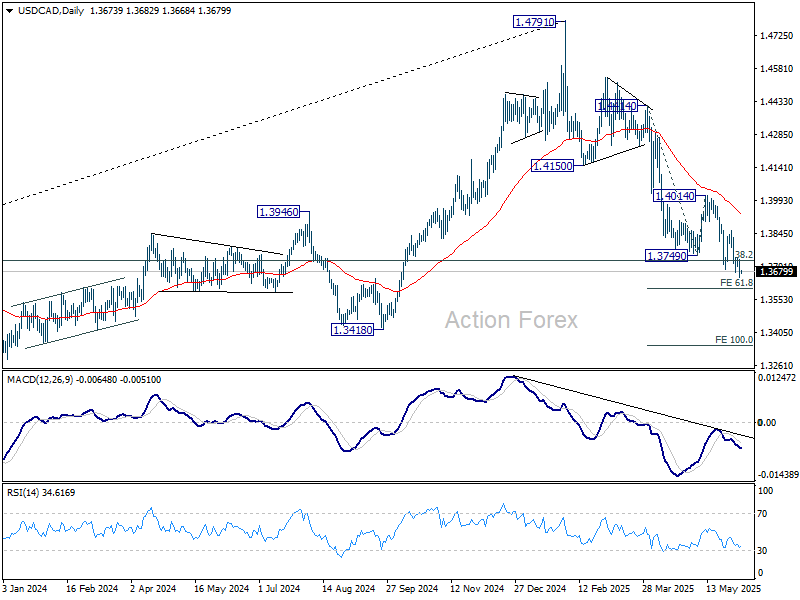

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3645; (P) 1.3688; (R1) 1.3724; More...

USD/CAD's decline from 1.4791 is still in progress and intraday bias stays on the downside. Next target is 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. Firm break there will pave the way to 100% projection at 1.3349. On the upside, outlook will stay bearish as long as 1.3860 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

Markets Unshaken by Weak US Data, Await Guidance from ECB

The US markets remain remarkably steady overnight despite a string of soft US economic releases overnight. Disappointing job and services data failed to trigger any meaningful selloff in equities, while Dollar edged slightly lower. Market pricing for Fed policy remains broadly unchanged, with a 96% chance of a hold at the upcoming meeting and a 70% probability for no change in July. Still, Friday’s non-farm payrolls report looms as a potential catalyst for repricing should the labor market disappoint more sharply than expected.

On the trade front, tensions are simmering as the US formally doubled its tariffs on imported steel and aluminum. Canada is now openly preparing retaliatory measures should ongoing negotiations with Washington break down. Prime Minister Mark Carney told lawmakers that Canada is engaged in “intensive negotiations” but is also preparing reprisal tariffs in parallel.

Meanwhile, EU-US trade talks appear to be moving in a more constructive direction. After a meeting in Paris, EU negotiator Maros Sefcovic and US Trade Representative Jamieson Greer described the discussions as productive and advancing “at pace.” Sefcovic noted the talks are now “very concrete,” and Greer echoed that sentiment, signaling genuine willingness from both sides to achieve a reciprocal agreement.

Attention now turns to ECB’s policy decision later today. A 25 bps rate cut is fully priced in, with the real focus on whether President Lagarde signals a pause for July. Given the subdued market response to recent central bank events and the current range-bound conditions, it remains to be seen whether today’s meeting will break the stalemate .

In weekly performance terms, Dollar is currently the worst performer, followed by Swiss Franc and Loonie. At the other end of the spectrum, Kiwi leads gains, with the Aussie and Sterling also modestly firmer. Euro and Ten are trading in the middle of the pack. Yet, almost all major pairs and crosses remain trapped within last week’s ranges.

In Asia, at the time of writing, Nikkei is down -0.53%. Hong Kong HSI is up 0.60%. China Shanghai SSE is up 0.08%. Singapore Strait Times is up 0.10%. Japan 10-year JGB yield is down -0.039 at 1.466. Overnight, DOW fell -0.22%. S&P 500 rose 0.01%. NASDAQ rose 0.32%. 10-year yield fell -0.095 to 4.365.

Looking ahead, German factory orders, UK PMI construction and Eurozone PPI will be released in European session, but the main event is defintely ECB rate decision and press conference. Later in the data, Canada will release trade balance and Ivey PMI. US will release jobless claims and trade balance.

ECB to cut, focus on Lagarde’s signal for a July pause

ECB is set to lower its deposit rate by 25 bps to 2.00% today, marking the eighth cut of this easing cycle and bringing policy deep into neutral territory. With inflation falling back below the 2% target in May, the case for further easing is clear in the near term. However, the main focus will be on President Christine Lagarde's forward guidance, particularly whether she signals a July pause in rate cuts, and the ECB’s updated economic projections.

The case for caution is clear. The Eurozone faces a highly uncertain backdrop with multiple crosscurrents. Trade war remain front and center, with US President Donald Trump’s tariff agenda weighing heavily on confidence and investment. Retaliatory moves from the EU could compound the hit to activity. At the same time, the surprised surge in Euro risks exerting additional downward pressure on inflation. Amid this uncertainty, ECB is expected to lower both its 2025 growth and inflation forecasts, acknowledging the softening outlook.

At the same time, medium-term fundamentals could provide some support. The EU’s major rearmament plans and Germany’s fiscal pivot to expansion are likely to bolster investment and domestic demand over time. That said, these structural measures will take time to feed through.

A July pause would allow policymakers to evaluate how these domestic tailwinds and external headwinds ultimately shape the outlook, particularly as geopolitical and policy unpredictability continues to cloud the picture.

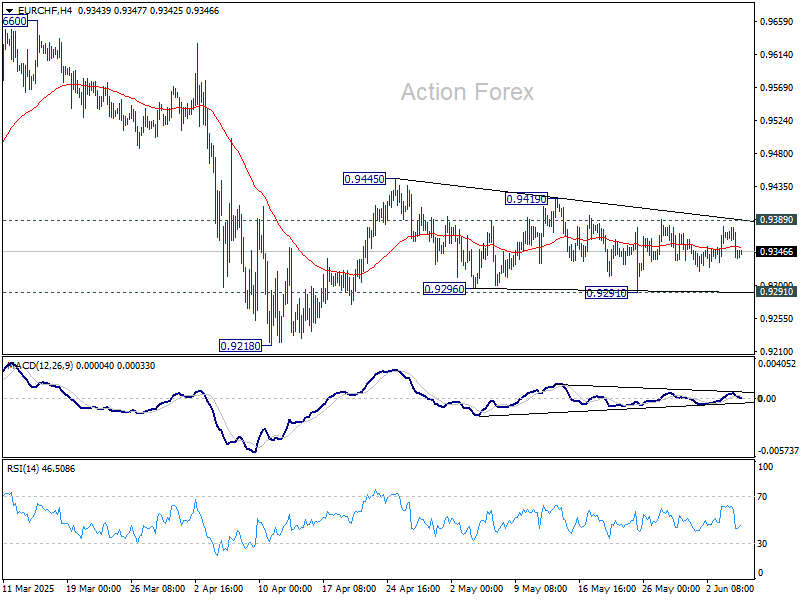

Technically, EUR/CHF's near term price actions from 0.9445 are more likely than not a triangle consolidation pattern. That is, rise from 0.9218 is in favor to resume, even as a corrective move. Break of 0.9389 minor resistance will be a bullish sign and further break of 0.9419 should sent EUR/CHF through 0.9445 resistance.

Japan’s real wages fall -1.8% yoy in April, down for the fourth month

Real wages in Japan fell by -1.8% yoy in April, marking the fourth consecutive month of decline as persistent inflation continued to erode household purchasing power.

While nominal wages rose 2.3% yoy, slightly below the expected 2.6%, gains were outpaced by a still-elevated consumer inflation rate of 4.1%, driven by rising food and energy costs. The inflation metric used by the labor ministry has remained near 4% for five straight months, keeping real income in negative territory.

On the positive side, base salaries rose 2.2% yoy, the fastest increase in four months and well above March’s 1.4% yoy gain. This also marked the 42nd consecutive month of growth in regular pay. Overtime pay rebounded with a modest 0.8% yoy rise, while special payments grew 4.1% yoy.

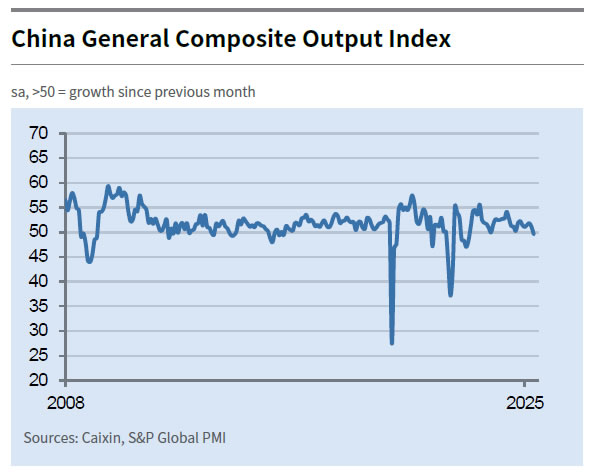

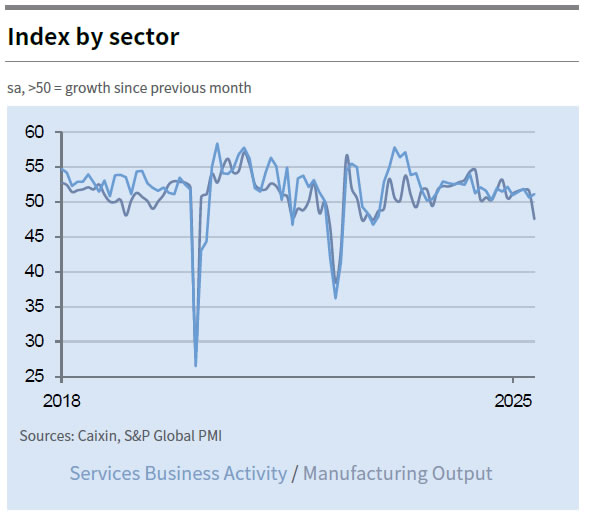

China’s Caixin PMI composite falls to 49.6, contracts for first time since 2022

China’s Caixin PMI Services rose modestly from 50.7 to 51.1 in May, aligning with expectations. However, the gain in services was not enough to offset the drag from manufacturing, as PMI Composite slipped into contraction at 49.6, its first reading below 50 since December 2022.

Wang Zhe of Caixin Insight Group noted that the manufacturing slump was weighing heavily on the overall market, with new export orders remaining "sluggish" across both goods and services. Although input costs rose slightly, firms were unable to pass these on to customers, with selling prices continuing to fall and compressing profit margins.

Caixin flagged "unfavorable factors remain relatively prevalent", with growing external trade uncertainty and "noticeable weakening" in macro indicators at the start of Q2. The "significantly intensified"downward pressure raises the urgency for further targeted policy support.

Fed's Beige Book: General tone slightly pessimistic and uncertain

Fed's Beige Book report paints a picture of slowing US economy marked by pervasive caution and subdued sentiment.

Economic activity was reported to have “declined slightly” overall, with half of the twelve Districts seeing slight to moderate declines, while three reported no change and three noted slight growth. The general tone remains “slightly pessimistic and uncertain,” echoing the previous report, as elevated policy and economic uncertainty continues to weigh on both business and household decision-making.

Consumer spending trends were mixed, with most Districts reporting little change or modest declines. However, in some cases, spending picked up on goods expected to be affected by tariffs—suggesting front-loading behavior amid trade concerns. Employment levels were largely stable, while price pressures persisted, rising at a moderate pace.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3645; (P) 1.3688; (R1) 1.3724; More...

USD/CAD's decline from 1.4791 is still in progress and intraday bias stays on the downside. Next target is 61.8% projection of 1.4414 to 1.3749 from 1.4014 at 1.3603. Firm break there will pave the way to 100% projection at 1.3349. On the upside, outlook will stay bearish as long as 1.3860 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 resistance holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

ECB to cut, focus on Lagarde’s signal for a July pause

ECB is set to lower its deposit rate by 25 bps to 2.00% today, marking the eighth cut of this easing cycle and bringing policy deep into neutral territory. With inflation falling back below the 2% target in May, the case for further easing is clear in the near term. However, the main focus will be on President Christine Lagarde's forward guidance, particularly whether she signals a July pause in rate cuts, and the ECB’s updated economic projections.

The case for caution is clear. The Eurozone faces a highly uncertain backdrop with multiple crosscurrents. Trade war remain front and center, with US President Donald Trump’s tariff agenda weighing heavily on confidence and investment. Retaliatory moves from the EU could compound the hit to activity. At the same time, the surprised surge in Euro risks exerting additional downward pressure on inflation. Amid this uncertainty, ECB is expected to lower both its 2025 growth and inflation forecasts, acknowledging the softening outlook.

At the same time, medium-term fundamentals could provide some support. The EU’s major rearmament plans and Germany’s fiscal pivot to expansion are likely to bolster investment and domestic demand over time. That said, these structural measures will take time to feed through.

A July pause would allow policymakers to evaluate how these domestic tailwinds and external headwinds ultimately shape the outlook, particularly as geopolitical and policy unpredictability continues to cloud the picture.

Technically, EUR/CHF's near term price actions from 0.9445 are more likely than not a triangle consolidation pattern. That is, rise from 0.9218 is in favor to resume, even as a corrective move. Break of 0.9389 minor resistance will be a bullish sign and further break of 0.9419 should sent EUR/CHF through 0.9445 resistance.

China’s Caixin PMI composite falls to 49.6, contracts for first time since 2022

China’s Caixin PMI Services rose modestly from 50.7 to 51.1 in May, aligning with expectations. However, the gain in services was not enough to offset the drag from manufacturing, as PMI Composite slipped into contraction at 49.6, its first reading below 50 since December 2022.

Wang Zhe of Caixin Insight Group noted that the manufacturing slump was weighing heavily on the overall market, with new export orders remaining "sluggish" across both goods and services. Although input costs rose slightly, firms were unable to pass these on to customers, with selling prices continuing to fall and compressing profit margins.

Caixin flagged "unfavorable factors remain relatively prevalent", with growing external trade uncertainty and "noticeable weakening" in macro indicators at the start of Q2. The "significantly intensified"downward pressure raises the urgency for further targeted policy support.