Sample Category Title

EUR/AUD Weekly Outlook

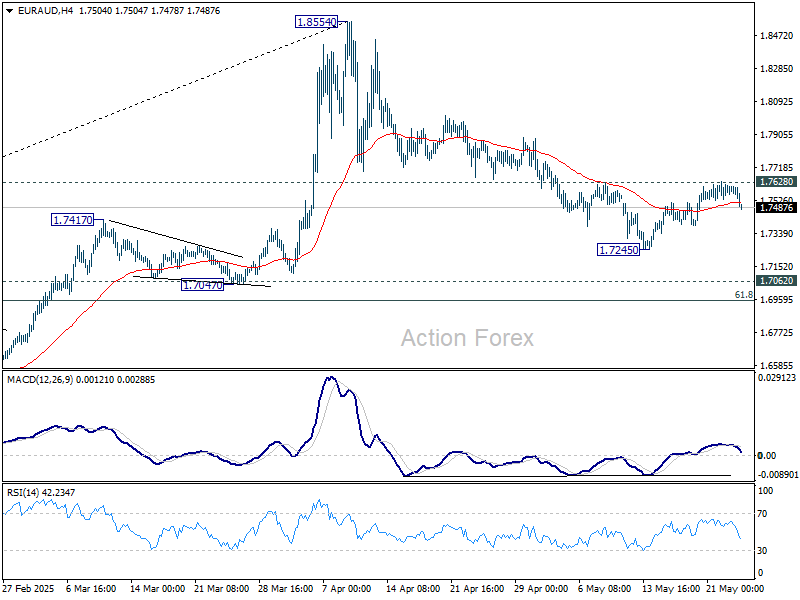

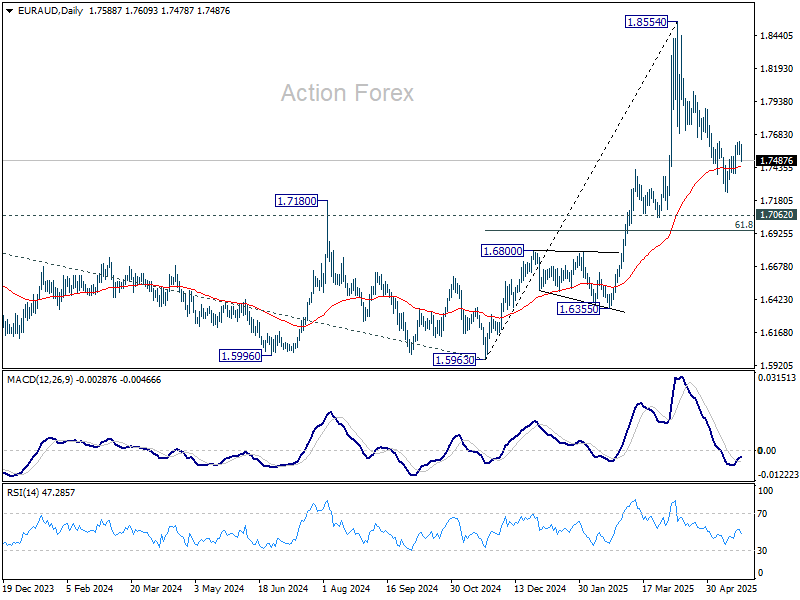

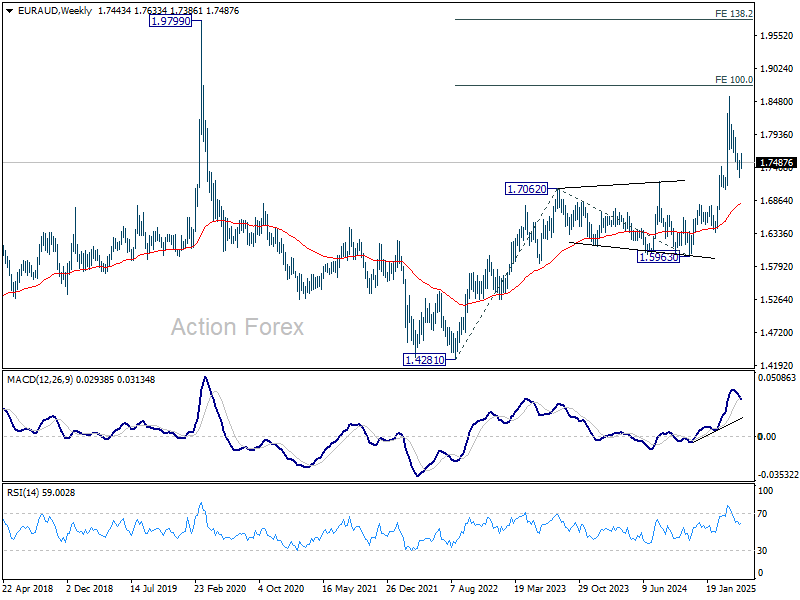

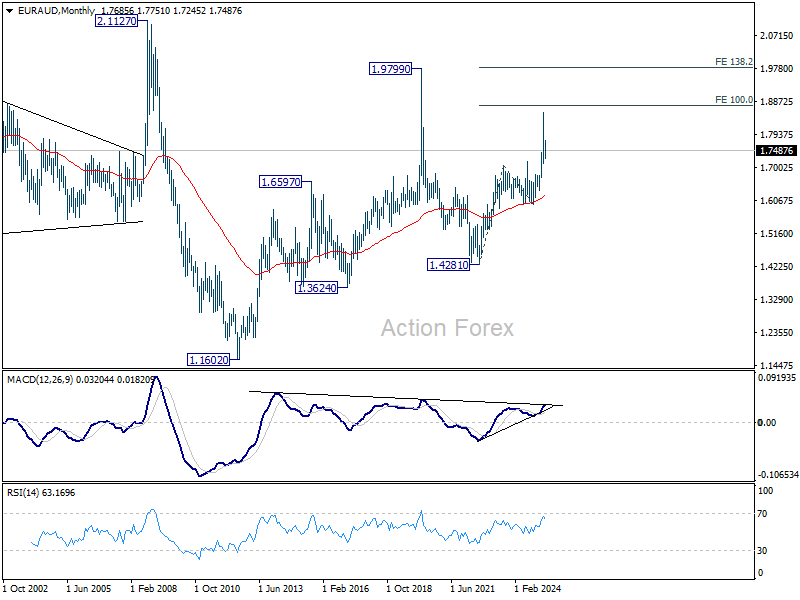

EUR/AUD's recovery from 1.7245 extended higher last week but failed to break through 1.7628 resistance. Initial bias remains neutral this week first. On the upside, firm break of 1.7628 resistance will suggest that fall from 1.8554 as completed as a correction, and retain larger bullishness. Intraday bias will be back on the upside for stronger rebound. However, below 1.7245 will resume the fall to 61.8% retracement of 1.5963 to 1.8554 at 1.6953.

In the bigger picture, as long as 1.7062 resistance turned support (2023 high) holds, up trend from 1.4281 (2022 low) should still be in progress. Break of 1.8554 will target 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. However, sustained break of 1.7062 will confirm medium term topping and bring deeper fall back to 1.5963 support.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6240) holds, this second leg could still extend higher. However, firm break of the above mention 1.8744 projection level with strong momentum will argue that it's indeed resuming the up trend from 1.1602 (2012 low).

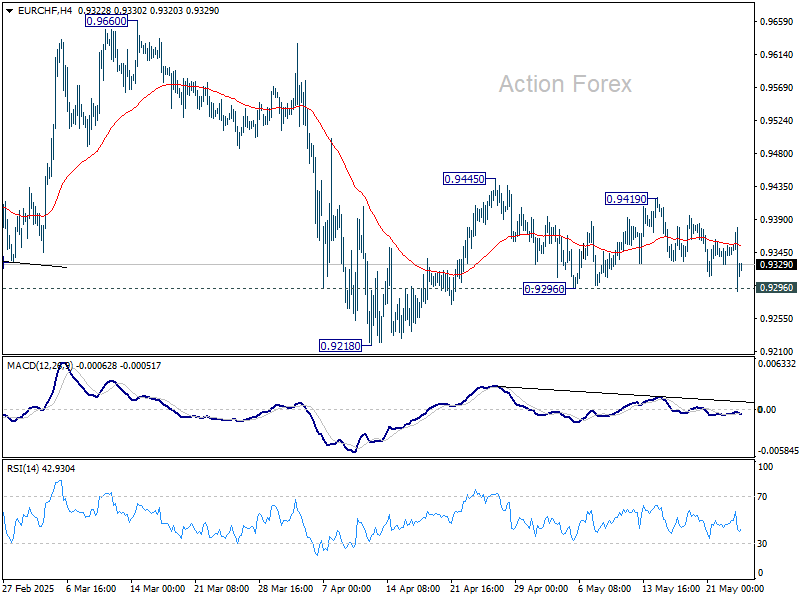

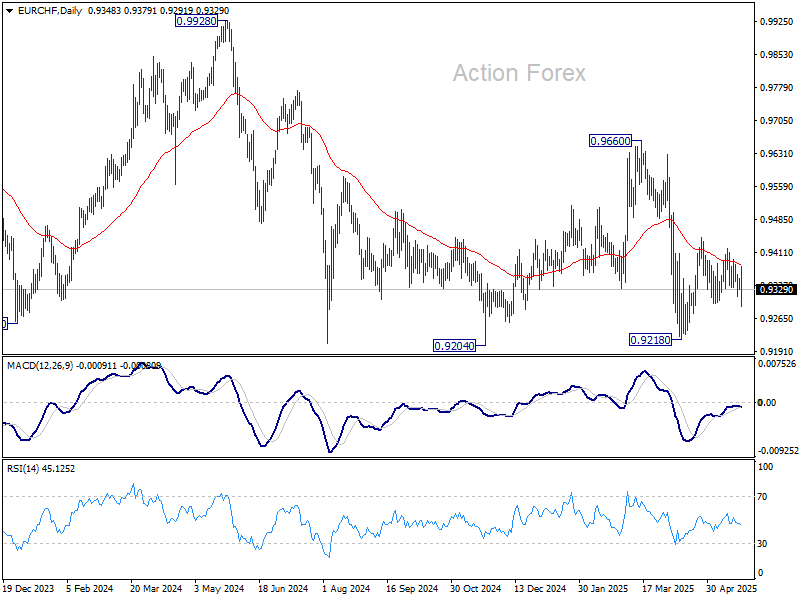

EUR/CHF Weekly Outlook

EUR/CHF weakened slightly last week it's so far still supported by 0.9296 support. Initial bias remains neutral this week and more range trading could still be seen. Price actions from 0.9218 are seen as either a corrective move or the third leg of the pattern from 0.9204. On the upside, break of 0.9419 will resume the rise from 0.9218 through 0.9445 resistance. However, break of 0.9296 support will bring retest of 0.9218 low.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9548) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

In the long term picture, overall long term down trend is still in force in EUR/CHF. Outlook will continue to stay bearish as long as 55 M EMA (now at 0.9919) holds.

Summary 5/26 – 5/30

Monday, May 26, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar F | 107.7 | 107.7 |

| 06:30 | CHF | Employment Level Q1 | 5.534M | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | 0.00% | -0.10% |

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | 3.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 05:00 | JPY | Leading Economic Index Mar F | |

| Forecast: 107.7 | Previous: 107.7 | ||

| 06:30 | CHF | Employment Level Q1 | |

| Forecast: | Previous: 5.534M | ||

| 23:01 | GBP | BRC Shop Price Index Y/Y May | |

| Forecast: 0.00% | Previous: -0.10% | ||

| 23:50 | JPY | Corporate Service Price Index Y/Y Apr | |

| Forecast: | Previous: 3.10% | ||

Tuesday, May 27, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Apr | 5.55B | 6.35B |

| 06:00 | EUR | Germany GfK Consumer Sentiment Jun | -19.7 | -20.6 |

| 09:00 | EUR | Eurozone Economic Sentiment May | 94 | 93.6 |

| 09:00 | EUR | Eurozone Industrial Confidence May | -11 | -11.2 |

| 09:00 | EUR | Eurozone Services Sentiment May | 1.4 | |

| 09:00 | EUR | Eurozone Consumer Confidence May F | -15.2 | -15.2 |

| 12:30 | USD | Durable Goods Orders Apr | -8.00% | 7.50% |

| 12:30 | USD | Durable Goods Orders ex Transport Apr | 0.00% | -0.40% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | 4.50% | 4.50% |

| 13:00 | USD | Housing Price Index M/M Mar | 0.20% | 0.10% |

| 14:00 | USD | Consumer Confidence May | 87.1 | 86 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | CHF | Trade Balance (CHF) Apr | |

| Forecast: 5.55B | Previous: 6.35B | ||

| 06:00 | EUR | Germany GfK Consumer Sentiment Jun | |

| Forecast: -19.7 | Previous: -20.6 | ||

| 09:00 | EUR | Eurozone Economic Sentiment May | |

| Forecast: 94 | Previous: 93.6 | ||

| 09:00 | EUR | Eurozone Industrial Confidence May | |

| Forecast: -11 | Previous: -11.2 | ||

| 09:00 | EUR | Eurozone Services Sentiment May | |

| Forecast: | Previous: 1.4 | ||

| 09:00 | EUR | Eurozone Consumer Confidence May F | |

| Forecast: -15.2 | Previous: -15.2 | ||

| 12:30 | USD | Durable Goods Orders Apr | |

| Forecast: -8.00% | Previous: 7.50% | ||

| 12:30 | USD | Durable Goods Orders ex Transport Apr | |

| Forecast: 0.00% | Previous: -0.40% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Mar | |

| Forecast: 4.50% | Previous: 4.50% | ||

| 13:00 | USD | Housing Price Index M/M Mar | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 14:00 | USD | Consumer Confidence May | |

| Forecast: 87.1 | Previous: 86 | ||

Wednesday, May 28, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Apr | 2.30% | 2.40% |

| 02:00 | NZD | RBNZ Interest Rate Decision | 3.25% | 3.50% |

| 03:00 | NZD | RBNZ Press Conference | ||

| 06:45 | EUR | France Consumer Spending M/M Apr | -1% | |

| 06:45 | EUR | France GDP Q/Q Q1 F | 0.10% | 0.10% |

| 07:55 | EUR | Germany Unemployment Change Apr | 10K | 4K |

| 07:55 | EUR | Germany Unemployment Rate Apr | 6.30% | 6.30% |

| 08:00 | CHF | UBS Economic Expectations May | -51.6 | |

| 18:00 | USD | FOMC Minutes |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Monthly CPI Y/Y Apr | |

| Forecast: 2.30% | Previous: 2.40% | ||

| 02:00 | NZD | RBNZ Interest Rate Decision | |

| Forecast: 3.25% | Previous: 3.50% | ||

| 03:00 | NZD | RBNZ Press Conference | |

| Forecast: | Previous: | ||

| 06:45 | EUR | France Consumer Spending M/M Apr | |

| Forecast: | Previous: -1% | ||

| 06:45 | EUR | France GDP Q/Q Q1 F | |

| Forecast: 0.10% | Previous: 0.10% | ||

| 07:55 | EUR | Germany Unemployment Change Apr | |

| Forecast: 10K | Previous: 4K | ||

| 07:55 | EUR | Germany Unemployment Rate Apr | |

| Forecast: 6.30% | Previous: 6.30% | ||

| 08:00 | CHF | UBS Economic Expectations May | |

| Forecast: | Previous: -51.6 | ||

| 18:00 | USD | FOMC Minutes | |

| Forecast: | Previous: | ||

Thursday, May 29, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence May | ||

| 01:30 | AUD | Private Capital Expenditure Q1 | 0.50% | -0.20% |

| 05:00 | JPY | Consumer Confidence May | 31.8 | 31.2 |

| 12:30 | CAD | Current Account (CAD) Q1 | -3.6B | -5.0B |

| 12:30 | USD | Initial Jobless Claims (May 23) | 230K | 227K |

| 12:30 | USD | GDP Annualized Q1 P | -0.30% | -0.30% |

| 12:30 | USD | GDP Price Index Q1 P | 3.70% | 3.70% |

| 14:00 | USD | Pending Home Sales M/M Apr | -1.00% | 6.10% |

| 14:30 | USD | Natural Gas Storage | 120B | |

| 15:00 | USD | Crude Oil Inventories | 1.3M | |

| 22:45 | NZD | Building Permits M/M Apr | 9.60% | |

| 23:30 | JPY | Tokyo CPI Y/Y May | 3.50% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 3.50% | 3.40% |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y May | 2% | |

| 23:30 | JPY | Unemployment Rate Apr | 2.50% | 2.50% |

| 23:50 | JPY | Industrial Production M/M Apr P | -1.40% | 0.20% |

| 23:50 | JPY | Retail Trade Y/Y Apr | 2.90% | 3.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence May | |

| Forecast: | Previous: | ||

| 01:30 | AUD | Private Capital Expenditure Q1 | |

| Forecast: 0.50% | Previous: -0.20% | ||

| 05:00 | JPY | Consumer Confidence May | |

| Forecast: 31.8 | Previous: 31.2 | ||

| 12:30 | CAD | Current Account (CAD) Q1 | |

| Forecast: -3.6B | Previous: -5.0B | ||

| 12:30 | USD | Initial Jobless Claims (May 23) | |

| Forecast: 230K | Previous: 227K | ||

| 12:30 | USD | GDP Annualized Q1 P | |

| Forecast: -0.30% | Previous: -0.30% | ||

| 12:30 | USD | GDP Price Index Q1 P | |

| Forecast: 3.70% | Previous: 3.70% | ||

| 14:00 | USD | Pending Home Sales M/M Apr | |

| Forecast: -1.00% | Previous: 6.10% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 120B | ||

| 15:00 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 1.3M | ||

| 22:45 | NZD | Building Permits M/M Apr | |

| Forecast: | Previous: 9.60% | ||

| 23:30 | JPY | Tokyo CPI Y/Y May | |

| Forecast: | Previous: 3.50% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y May | |

| Forecast: 3.50% | Previous: 3.40% | ||

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y May | |

| Forecast: | Previous: 2% | ||

| 23:30 | JPY | Unemployment Rate Apr | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 23:50 | JPY | Industrial Production M/M Apr P | |

| Forecast: -1.40% | Previous: 0.20% | ||

| 23:50 | JPY | Retail Trade Y/Y Apr | |

| Forecast: 2.90% | Previous: 3.10% | ||

Friday, May 30, 2025

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Apr | 0.30% | 0.30% |

| 01:30 | AUD | Private Sector Credit M/M Apr | 0.50% | 0.50% |

| 01:30 | AUD | Building Permits M/M Apr | 3.10% | -8.80% |

| 05:00 | JPY | Housing Starts Y/Y Apr | -18.30% | 39.10% |

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.30% | -0.20% |

| 07:00 | CHF | KOF Economic Barometer May | 98.3 | 97.1 |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 3.70% | 3.60% |

| 12:00 | EUR | Germany CPI M/M May P | 0.10% | 0.40% |

| 12:00 | EUR | Germany CPI Y/Y May P | 2.10% | |

| 12:30 | CAD | GDP M/M Mar | 0.20% | -0.20% |

| 12:30 | USD | Personal Income M/M Apr | 0.30% | 0.50% |

| 12:30 | USD | Personal Spending M/M Apr | 0.20% | 0.70% |

| 12:30 | USD | PCE Price Index M/M Apr | 0% | |

| 12:30 | USD | PCE Price Index Y/Y Apr | 2.30% | |

| 12:30 | USD | Core PCE Price Index M/M Apr | 0.10% | 0% |

| 12:30 | USD | Core PCE Price Index Y/Y Apr | 2.60% | |

| 12:30 | USD | Wholesale Inventories Apr P | 0.40% | 0.50% |

| 12:30 | USD | Goods Trade Balance (USD) Apr P | -141.8B | -162.0B |

| 13:45 | USD | Chicago PMI May | 45.1 | 44.6 |

| 14:00 | USD | UoM Consumer Sentiment May F | 50.8 | 50.8 |

| 14:00 | USD | UoM 1-year Inflation Expectations May | 7.30% | 7.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M Apr | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 01:30 | AUD | Private Sector Credit M/M Apr | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 01:30 | AUD | Building Permits M/M Apr | |

| Forecast: 3.10% | Previous: -8.80% | ||

| 05:00 | JPY | Housing Starts Y/Y Apr | |

| Forecast: -18.30% | Previous: 39.10% | ||

| 06:00 | EUR | Germany Retail Sales M/M Apr | |

| Forecast: 0.30% | Previous: -0.20% | ||

| 07:00 | CHF | KOF Economic Barometer May | |

| Forecast: 98.3 | Previous: 97.1 | ||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | |

| Forecast: 3.70% | Previous: 3.60% | ||

| 12:00 | EUR | Germany CPI M/M May P | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 12:00 | EUR | Germany CPI Y/Y May P | |

| Forecast: | Previous: 2.10% | ||

| 12:30 | CAD | GDP M/M Mar | |

| Forecast: 0.20% | Previous: -0.20% | ||

| 12:30 | USD | Personal Income M/M Apr | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 12:30 | USD | Personal Spending M/M Apr | |

| Forecast: 0.20% | Previous: 0.70% | ||

| 12:30 | USD | PCE Price Index M/M Apr | |

| Forecast: | Previous: 0% | ||

| 12:30 | USD | PCE Price Index Y/Y Apr | |

| Forecast: | Previous: 2.30% | ||

| 12:30 | USD | Core PCE Price Index M/M Apr | |

| Forecast: 0.10% | Previous: 0% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Apr | |

| Forecast: | Previous: 2.60% | ||

| 12:30 | USD | Wholesale Inventories Apr P | |

| Forecast: 0.40% | Previous: 0.50% | ||

| 12:30 | USD | Goods Trade Balance (USD) Apr P | |

| Forecast: -141.8B | Previous: -162.0B | ||

| 13:45 | USD | Chicago PMI May | |

| Forecast: 45.1 | Previous: 44.6 | ||

| 14:00 | USD | UoM Consumer Sentiment May F | |

| Forecast: 50.8 | Previous: 50.8 | ||

| 14:00 | USD | UoM 1-year Inflation Expectations May | |

| Forecast: 7.30% | Previous: 7.30% | ||

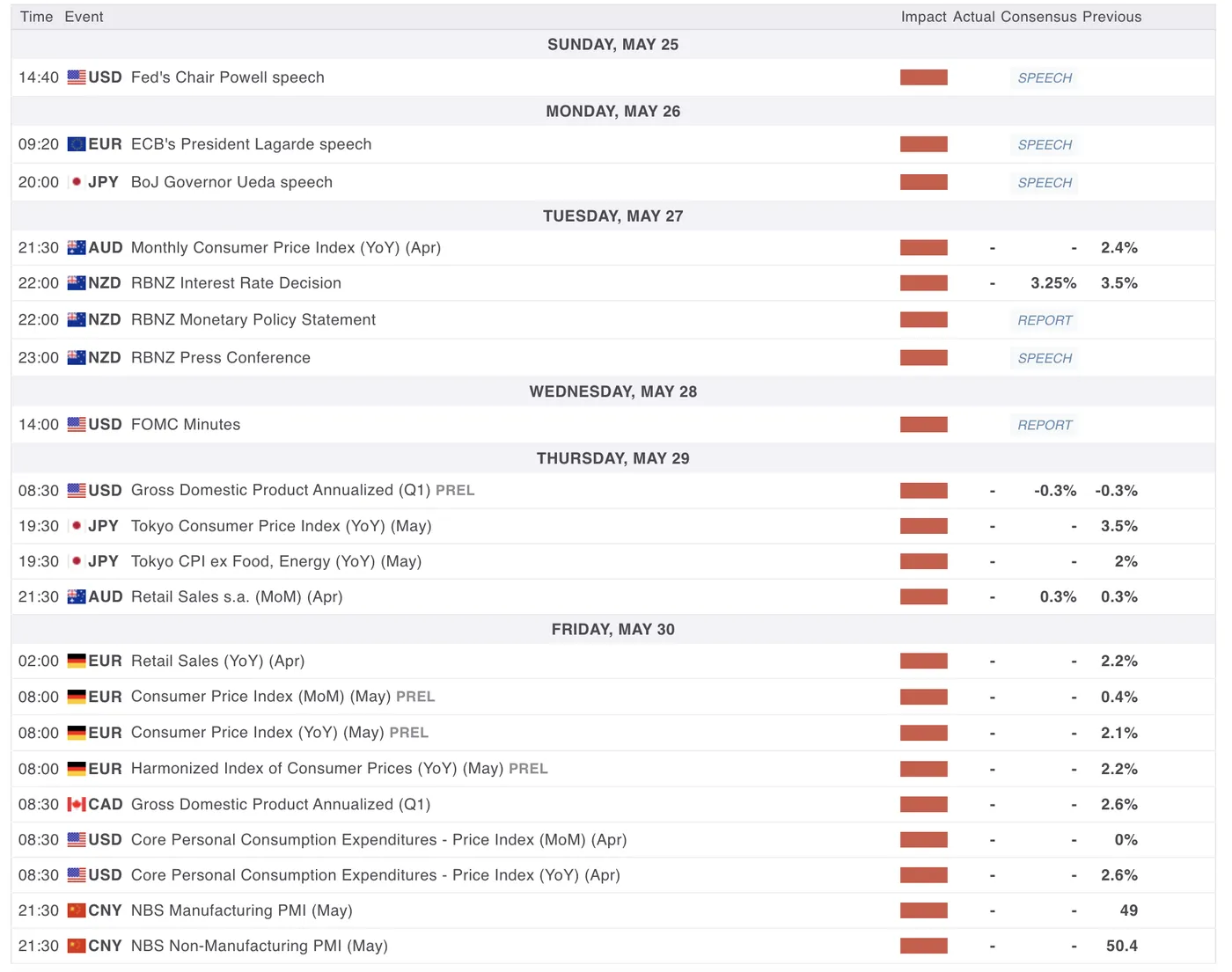

RBNZ Decision, Japan CPI, Fed Minutes, and US Core PCE – Markets Weekly Preview

Week in Review: Bitcoin all-time highs, Weaker Dollar in another volatile week

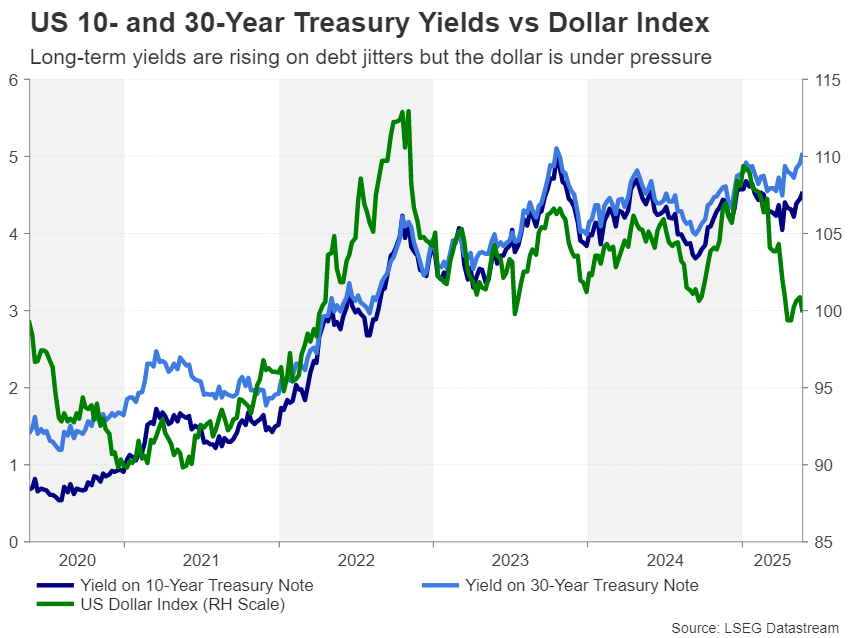

The US Dollar was once again on the main stage this week as we have observed initial market reactions after last Friday's US Credit Rating Downgrade by Moody's Agency.

The Dollar Index (DXY) went back below the 100.00 level, Longer-end yields in US Treasury Bonds went back above 5% and this Dollar weakness fueled rallies in Gold and Bitcoin, the latter breaking fresh all-time highs with a weekly high at $112,030.

Indices in North-America took a beating from the US Credit Downgrade with both the S&P and Nasdaq down more than 2.5%.

This also dragged European indices which were playful in the beginning of the week after a EU-UK Trade Deal was achieved.

The entente was the most impactful trade deal since Brexit separated the two entities in 2020. IBEX and DAX both made new highs but got rejected particularly after Trump's most recent tariff comments, more on this further in the article.

Bitcoin and Gold were the winners of the week, enjoying from a lower US Dollar. Both are up 4.85% as the weekly candle closes. Markets will now eye to a confirmation of new all-time highs in Bitcoin, and a retest of the last highs in the Bullion at $3,500. You can take a look at key levels for Gold here.

Currencies also all enjoyed from a fall in the Greenback, with the DXY down 1.7% on the week.

The winner was the Japan yen closely followed by the Swissie, as markets were diversifying their Safe-Havens into other currencies.

The Euro, Pound, and even the Canadian Dollar finished up more than 1.5% against the USD. The Australian Dollar was the laggard in the race against the Greenback, with AUDUSD “only” up 1.17%.

The Week Ahead: New Zealand Rate Decision and US Core PCE and FED Minutes

The upcoming week is packed with central bank speeches, kicking off over the weekend. Federal Reserve Chair Jerome Powell leads the lineup with remarks scheduled for Sunday at 2:40 P.M. ET. He’ll be followed on Monday by ECB President Christine Lagarde and Bank of Japan Governor Kazuo Ueda, setting the tone for the week.

Asia Pacific Markets Outlook

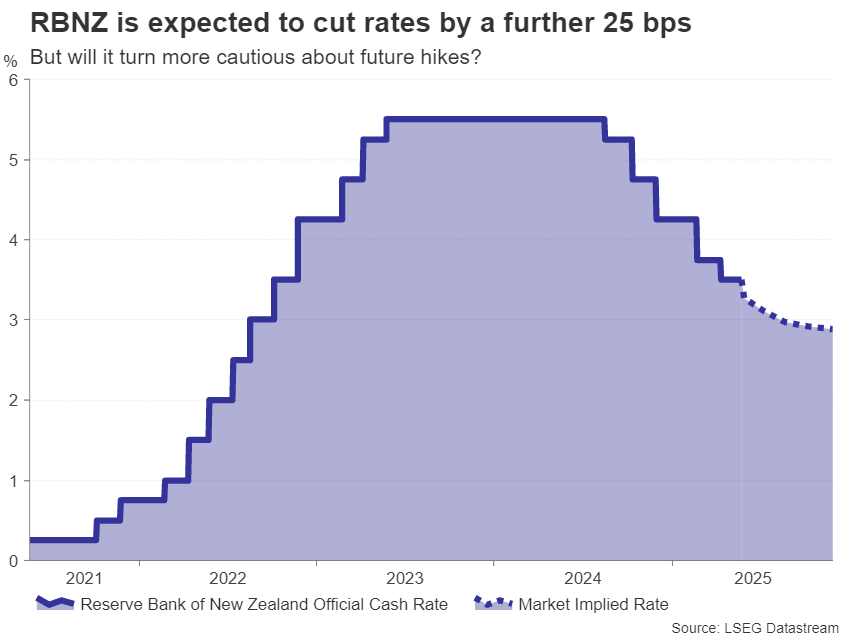

The Reserve Bank of New Zealand is expected to cut its Official Cash Rate from 3.50% to 3.25% on Wednesday May 28. A new Quarterly business survey was recently published by the RBNZ which sent mixed signals ahead as Inflation expectations from businesses are seen to be growing. You can access the RBNZ Report here.

The Key for the meeting will be to track any neutral or hawkish tone which would be hinting at a slower pace of cuts in the case where Inflation Expectations get out of hand.

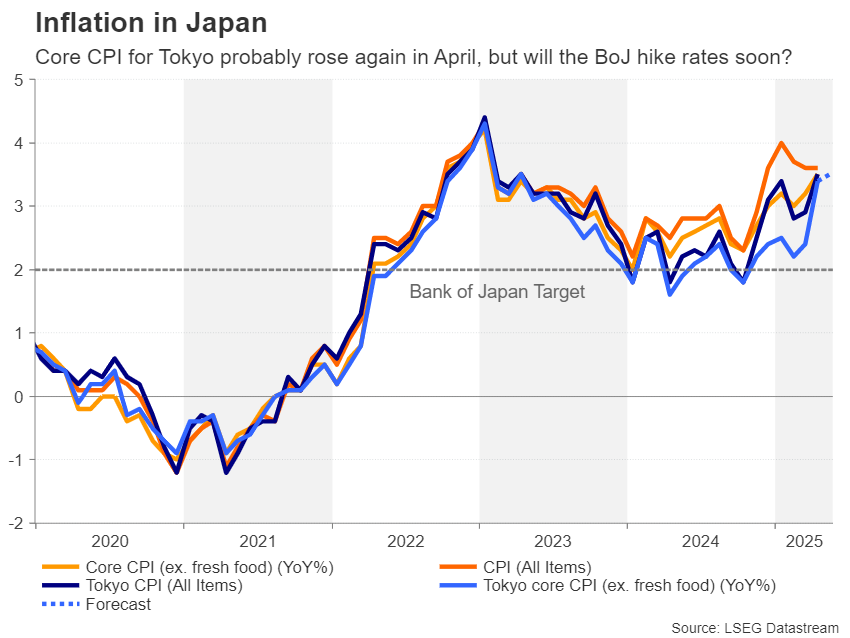

Japan will the release of CPI Data on Thursday May 29 which will be key for all markets, as all eyes have been on a Bank of Japan move. A beat on CPI may hint at future raises in the BoJ Policy Rate, which will greatly influence Carry Trades, potentially shaking markets around the world as it did in July 2024.

Last month CPI came in at 3.5%. We will also see the release of the Japanese unemployment rate and Retail Trade data, and how both were affected by frantic US Policies.

The most recent change from the Bank of Japan was a hike to 0.50% from 0.25%, though the Central Bank has been communicating concerns about future changes due to Tariff uncertainty. The Policy Rate in Japan was negative from February 2016 until March 2024, which a change that took markets by surprise.

Europe, US and UK Market Outlook

Data releases will be limited in Europe with mostly ECB Speakers, markets will nonetheless expect releases for Consumer Confidence from Germany, with the last release at -20.6 and the same data for Europe expected at -15.2. These data points will release on Tuesday May 27.

It will be essential to see if European businesses enjoyed a more sympathetic approach by President Trump about tariffs, though his most recent comments affected the European Indices, sending the DAX down 2.7%.

FED Minutes will be released on Wednesday, and we will have a better idea of what the Federal Reserve is expecting going into future meetings.

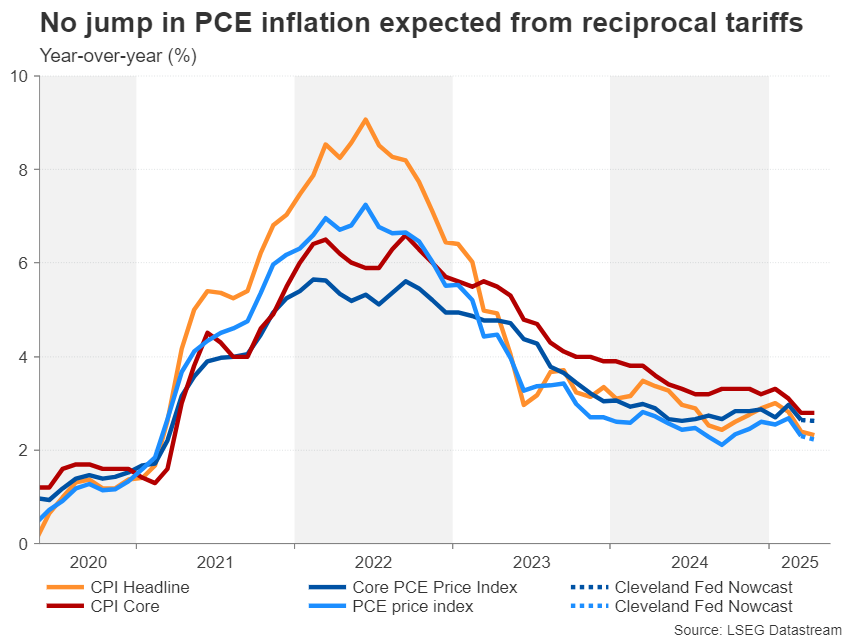

Minutes are not the most market-moving event in the calendar, but they give more emphasis to what precise data the FED is targeting. FED Chair Powell's favorite measure until now was the Core PCE.

Talking about Core PCE, we will see the data release next Friday. The past released indicated a 2.6% Y/Y change, though the upcoming release will incorporate the most recent US PMI data and further news of the tariff's influence on core prices.

No data releases are expected from the UK, with only speeches from Bank of England Pill and Lombardelli.

Most impactful Economic Calendar releases for Next Week

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Safe Trades for the week ahead!

The Weekly Bottom Line: Economic Data Support CAD Rally

Canadian Highlights

- The Canadian dollar firmed against the USD, gaining over 1.0% and is currently sitting at 72.7 cents U.S. in this holiday shortened week.

- April data for Canada’s economy were generally healthy, suggesting Q1’s solid momentum continued into the second quarter.

- Outlays on cars and parts helped to support strong retail spending in March, though tariff front-running was likely a factor, suggesting some giveback in the months ahead.

U.S. Highlights

- The U.S. House of Representatives passed its version of the reconciliation bill, which includes major tax cuts and expands the U.S. deficit over the next ten years.

- U.S. government bond yields moved up this week, likely due to a combination of the market response to higher deficits and expectations of higher inflation.

- Expectations for U.S. interest rates have moved higher this week, as data start to show signs of price pressures.

Canada – Economic Data Support CAD Rally

A bit of a muddy picture for markets this week, with renewed tariff threats from south of the border arresting this week’s sell-off in government bonds. However, with new tariff threats and some evidence of inflationary pressures heating up, the Canadian dollar firmed against the USD, gaining over 1.0% and currently sitting at 72.7 cents U.S. Looking beyond the headlines to close out the week, the April data for Canada’s economy were surprisingly healthy, pointing to continued momentum heading into the second quarter.

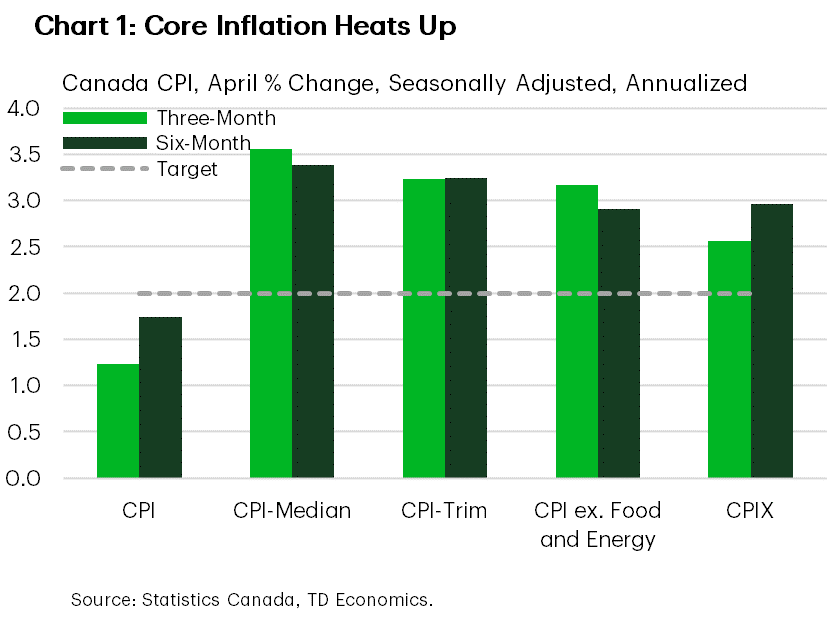

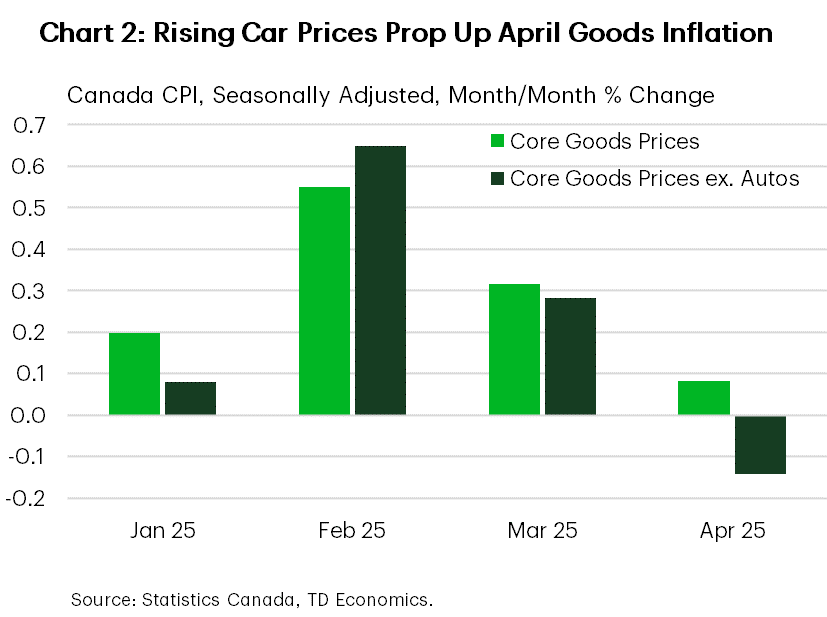

Headline inflation for April came in on the softer side, with the consumer price index falling well below the Bank of Canada’s (BoC) inflation target. However, this was largely due to the repeal of the consumer carbon tax, which helped to push energy prices meaningfully lower last month. Meanwhile, measures of core inflation showed signs of heating up. Both of the BoC’s preferred core measures shot north of 3.0% when measured on a year-on-year basis, while traditional core price trackers (CPIX and CPI excluding food and energy) rose to 2.6% y/y. Importantly, the rise is being driven by near-term momentum in inflation, as both three- and six-month annualized rates of change accelerated last month (Chart 1). Amid still high economic uncertainty, and a labour market that has been slowing significantly in recent months, the uptick in price pressures is an unwelcome development for policymakers. Financial markets appear to be putting more weight on the inflation data, as evidence by the probability of a June rate cut falling to just 30% (from 70% ahead of the inflation release). Making the decision on any further cuts to the policy rate in an environment where inflation is accelerating may force them to carefully weigh the trade-offs between further stoking inflation and supporting an economy that, in some respects, looks to be losing momentum.

Luckily for rate setters at the BoC, today’s retail sales data supported the notion that the price gains in past months could be the result of an economy with a bit more verve than the softening labour market suggested. Retail spending rose 0.8% from February to March (0.9% after stripping out price effects), powered by spending on motor vehicles and parts. Tariff front-running is likely part of the story for the strong print, but the flash estimate for April’s spending is showing another healthy gain, and this is even though vehicle sales were soft in April.

Moving forward, one key to monitor is for strength in spending outside of the automotive sector. Vehicle prices were a key driver of consumer goods price gains last month (Chart 2) and outside of cars and gasoline, real spending only advanced 0.1% in March. If the momentum in the sector is solely being driven by tariff front-running, then we’re likely to see a sharp reversal in spending activity in the coming months. From our lens, the economy is not out of the woods yet, and policymakers will have space to deliver two more cuts in 2025, providing the economy a bit more of a tailwind amid still-elevated economic uncertainty.

U.S. – One Big, Beautiful Deficit

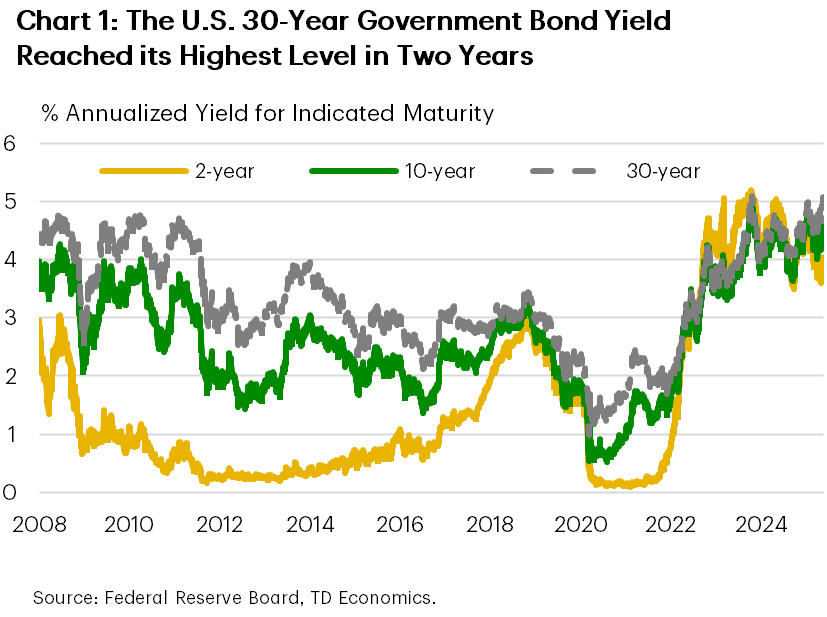

If we’ve got our eyes trained on one thing this week, it is the House of Representatives reconciliation bill, which has been officially dubbed the “One Big Beautiful Bill Act”. The bill still must go through the Senate and so nothing is set in stone, but early estimates show the bill in its current state could add over $3 trillion to the U.S. deficit over the next ten years. The main culprit behind the expanded deficits are the promised tax cuts, including the extension of President Trump’s 2017 Tax Cuts & Jobs Act in addition to several new tax breaks for households. These are paired with some spending cuts, but not enough to cover the tax cuts and added interest payments. The bond market has already started to show some reservations to the prospects of higher deficits, with term-yields pushing notably higher this week (Chart 1). The 2-year and 10-year government bond yields have also been backing up in the past few weeks, reflecting some increased premium on government bonds and higher rate expectations for the Federal Reserve. These moves precede today’s threat from President Trump of even higher tariffs on the EU.

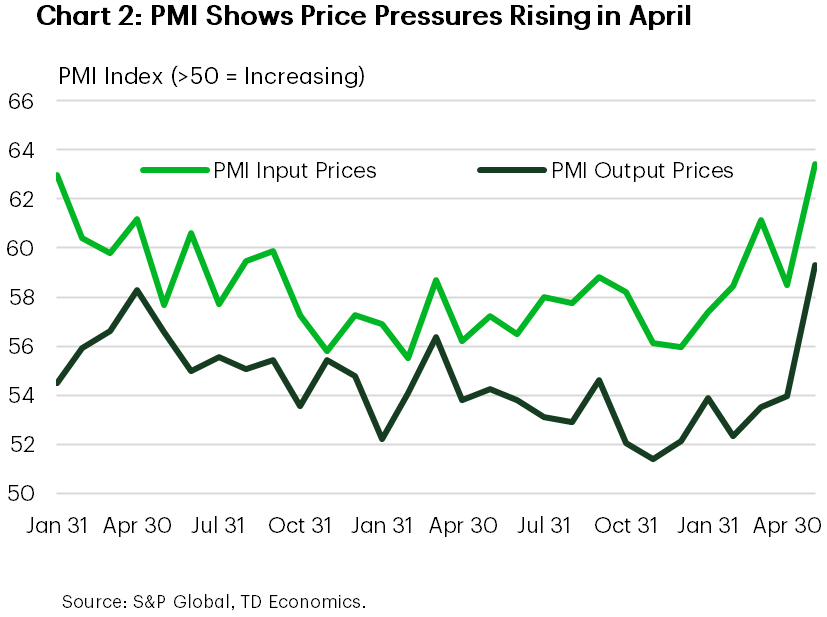

Government bond yields aren’t the only thing heating up. We are also seeing early signs of a build-up in price pressures in recent survey data, including yesterday’s release of the Purchasing Manager Index (PMI) for April. These PMIs are surveys of industry that provide a timely indicator of business activity during the survey period and can also shed light on how prices fared. The April PMIs, shown in Chart 2, showed a large concurrent rise in input and output prices. We had expected that higher tariffs would have an impact on firms costs and their prices to consumers. Several large U.S. companies have been indicating that they will be increasing their prices, anecdotally confirming what the data is pointing to – that the U.S. is heading to a world of higher interest rates and prices.

The rise in government bond yields will be filtering through to the rest of the economy, and this will have an impact on consumers. We noted in our commentary yesterday that existing home sales took a hit in April and March. The housing market, already on weak footing, now has to contend with mortgage rates that have risen back above 7%, on the back of a higher U.S. Treasury yields. For those held back by current rates, interest rate relief may not be coming quickly for U.S. households. St. Louis Fed President Musalem, who is a voting member on the FOMC, said that monetary policy is in a good place, mirroring sentiment expressed in the last set of minutes that FOMC members are in a wait-and-see mode about inflation before cutting rates further.

We look ahead to next week to see how the budget talks continue to unfold. The ball is now in the Senate’s court and since the bill was controversial among Republican House members, we do not take the Senate’s acquiescence to its current form as a given. Their stated goal is to have the bill passed by July 4, which gives Congressional Republicans and the White House time to iron out disagreements. On the data side, most important is the April personal spending and price data, which come at the end of next week and will be an early indicator of what impact April’s tariff increases had.

Weekly Economic & Financial Commentary: Moody’s Downgrade Spotlights Fiscal Reality

Summary

United States: The Old versus the New

- The challenges facing the housing market have yet to meaningfully abate. Our expectation for mortgage rates to soften slightly alongside Federal Reserve rate cuts could help improve affordability, but the prospects for such a move in the near term have dimmed.

- Next week: Durable Goods (Tue.), Consumer Confidence (Tue.), Personal Income and Spending (Fri.)

International: International Data Show Mixed Growth and Lingering Inflation

- This week brought a range of data and events from foreign economies. On the policy front, the Reserve Bank of Australia delivered a widely expected rate cut. Sentiment surveys from the Eurozone and the United Kingdom underwhelmed, providing further evidence of an uncertain outlook. On the price front, the U.K.'s and Japan’s overall inflation increased, while Canadian inflation eased on the back of the carbon tax removal. In China, industrial production and retail sales figures were mixed.

- Next week: Brazil GDP (Fri.), Canada GDP (Fri.), China PMIs (Sat.)

Interest Rate Watch: Moody's Downgrade Spotlights Fiscal Reality

- Late in the afternoon on Friday, May 16, Moody's downgraded the sovereign credit rating of the United States to AA+, one notch below the top rating of AAA. This decision by Moody's, in conjunction with the House-passed budget reconciliation bill this week, has brought U.S. fiscal policy back into the spotlight for financial markets.

Topic of the Week: Will Tariffs Spur a Resurgence of U.S. Manufacturing Jobs?

- The goals of the administration's trade regime changes are varied, but a resurgence of American manufacturing jobs is certainly a priority. Could higher trade barriers spur a rebound in U.S. manufacturing employment?

Preview of RBNZ: Forward into the Mist

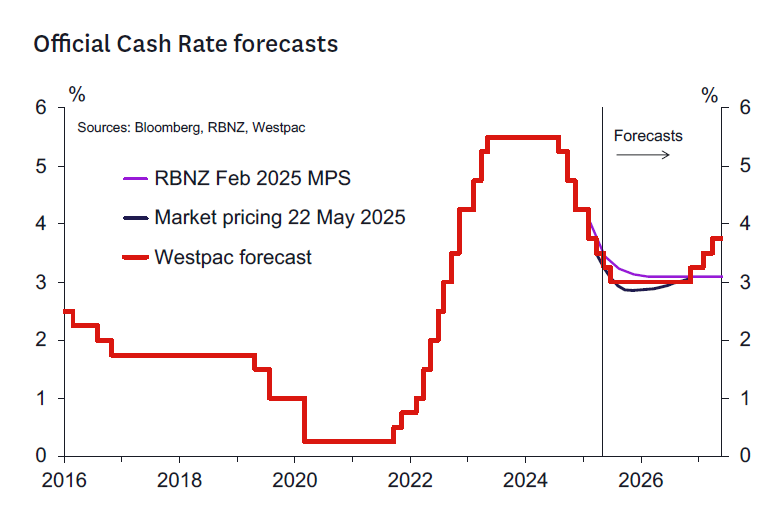

- We expect the RBNZ to cut the OCR by 25bp to 3.25%.

- We see the RBNZ’s OCR profile being revised down by around 20bp to around 2.9% by the end of 2025.

- Beyond this meeting a data dependent easing bias seems likely.

- The RBNZ may be open to a pause in July depending on events.

- We expect downside and upside scenarios to be canvassed. The downside scenario will likely imply more policy adjustment than the upside scenario.

- We expect to see evidence of increased debate among MPC members the amount of weight placed on high near-term inflation and rising expectations versus lower medium- term forecasts.

RBNZ decision and communication.

We expect the RBNZ to cut the OCR by 25bp to 3.25% and signal a data dependent easing bias looking ahead. We see the RBNZ’s OCR profile being revised down by around 20bp to around 2.9% by the end of 2025. A broadly flat profile beyond 2025 seems likely. The very shortterm assumption for Q3 2025 is likely to leave the RBNZ the option to cut the OCR in either of July or August. Arithmetically, a 3.1% OCR projection for Q3 would split the difference between the two meetings and signal the intention to assess the next move carefully with reference to emerging data and global developments.

We don’t see either an unchanged OCR or a 50bp cut as likely outcomes and put around 5% probabilities on each (although there is debate among the team on whether one is slightly more likely than the other).

The RBNZ will likely assess the economy as still being on a recovering trend. However, it will probably view the recovery in domestic activity as somewhat weaker than hoped (consumer spending/consumption and investment), but stronger than expected in externally focused sectors (tourism, primary sector, services exports). The labour market outlook will remain the same – we suspect they won’t need to revise down their peak unemployment rate given it was already at a low level of 5.2% in the February Monetary Policy Statement. The starting point for the output gap will be revised modestly upwards (less slack in the economy) but the more muted short-term outlook may mean little net change if evaluated over all of 2025.

The RBNZ may modestly upgrade their short-term inflation outlook given the Q1 CPI and subsequent Selected Price Indices. Previously, the RBNZ expected the CPI to peak around 2.7% in 2025 – that might push up to 2.8 or 2.9% at the peak. This uncomfortable short term inflation outlook will likely temper at least somewhat the dovish implications of the slightly weaker domestic growth outlook. Rising inflation expectations, and still robust pricing intentions on some measures, will likely rate a mention on the hawkish side of the ledger.

The RBNZ is very likely to make a decent sized downgrade in their trading partner GDP outlook – perhaps in the order of 0.5% over 2025. This will depress GDP and the output gap over the medium term – although the final impact on the interest rate projections will depend somewhat on their assumptions on the impact of the terms of trade. The RBNZ will upgrade the starting point for the terms of trade (export prices have been stronger and import prices weaker than expected) which will offset downgrades made to future export price assumptions.

The RBNZ will likely emphasize the uncertainty and downside risks associated with global economic developments. We expect the RBNZ to present an alternative scenario based on an outlook where the world steps back to global tariffs closer to those presented by the US authorities on “Liberation Day” with some escalation on some bilateral tariff rates (although not to the full extent reached in the aftermath of April 8). We expect this scenario to assume at least a degree of retaliation – although not to the extremes assumed by the Reserve Bank of Australia in their Statement on Monetary Policy this week.

This downside scenario may also feature heightened uncertainty over a longer period. The implication would be downward adjustments to investment and consumption and a higher unemployment rate. The presented scenario may not include an implied OCR profile but might focus on the implications for key variables such as GDP growth, the unemployment rate and CPI inflation. It’s hard to be definitive on the size of the scenario shock, but it will likely leave the implication that in a downside scenario the OCR could move down towards 2-2.5%.

An upside scenario may also be presented that could feature a faster resolution of uncertainty on the global trade outlook and hence a stronger short term growth profile. The scenario might imply some reduction in the 10% tariff the US has imposed on New Zealand exports. This scenario would imply little additional need to ease policy further.

The RBNZ’s commentary will likely emphasize that it is navigating difficult waters between an uncomfortably high short term inflation outlook and downside medium term growth and inflation risks. We expect them to signal a data dependent easing bias that leaves open the option to pause in future meetings. The Summary Record of Meeting is likely to reflect a potentially vigorous debate on the weight the MPC should put on the uncomfortably high near-term inflation outlook versus hopes for lower inflation in 2026 and beyond. Some members are likely to argue for a much slower and more data dependent pace of easing going forward.

In many respects, the August Statement may be a more natural time to take the next step lower in the OCR if required. By then the trading partner outlook may be clearer (noting 8 July is the US authorities’ self-imposed deadline to conclude trade negotiations - just a day before the July MPR). Also, the RBNZ will have key CPI data (21 July) and labour market reports (6 August). We don’t expect the outcome of this week’s Budget to feature prominently in the MPCs discussions. The MPC will likely remain comfortable that government consumption as a proportion of GDP will continue to decline and hence not hinder the goal of moving inflation back closer to 2%. Some alternative scenarios for the outcome of this meeting include:

- Hawkish scenario – a 25bp cut with a clear intent to pause in July. The RBNZ would note an intent to review things again in August and with the possibility of one final cut to 3% if required.

- Dovish scenario - a 25bp cut with a presumption of a further cut to 3% by August and a further cut to 2.75% later in 2025. The possibilities of a move lower still in the OCR towards 2-2.5% might also be discussed as a risk scenario. The RBNZ would be putting more weight on the downside growth and inflation scenario and less regard for the short-term inflation picture.

Key developments since the February Monetary Policy Statement.

Aside from the US tariff announcement, the main data developments since the RBNZ’s February policy statement have been:

GDP: Activity rose by 0.7% in the December 2024 quarter, ahead of the RBNZ’s estimate of 0.3%. Given their usual approach, the RBNZ will likely now assess that the negative output gap is narrower than the 1.7% of GDP that had been estimated for Q4.

Business confidence: Indicators have been mixed, but consistent with an improving but still sub-trend growth outlook. The NZIER survey for the March quarter showed firms becoming more optimistic in the outlook for the months ahead, but the assessment of current conditions remained subdued. The monthly ANZ survey has seen confidence hold up at high levels, though responses in the second half of April – after the ‘Liberation Day’ announcement – were notably softer. However, this represents a small sample and coincides with when the commentary and market reaction to the tariffs was at its most negative. The indicator of firms’ activity compared to a year earlier lifted into positive territory in April.

Other activity indicators: High-frequency economic data have been mixed. The BusinessNZ manufacturing PMI has risen and held above the 50 mark since the start of the year, but the comparable index for services has softened again in the last few months. Retail card spending has slowed again after a strong end to 2024. Residential building consents have been broadly steady in recent months. Westpac’s GDP Nowcast suggests still sub-par GDP growth in Q1 and Q2 while the new RBNZ Nowcast remains consistent with the RBNZ’s February short term GDP growth profile.

Inflation: March quarter prices were a little firmer than the RBNZ expected, with annual inflation rising from 2.2% to 2.5% compared to their February forecast of 2.4%. A technical change to the measurement of tertiary education fees may have accounted for the upside surprise. The selected monthly prices up to April are showing mixed trends, with re-emerging upward pressure in food prices but slowing growth in rents. Increased vehicle licensing fees will likely lift their short term forecasts a tad.

Inflation expectations: The pricing intentions gauge in the ANZ’s business survey has increased in recent months and continues to sit at levels that historically have not been consistent with inflation remaining inside the target range. The RBNZ’s quarterly surveys shows that inflation expectations have increased at both the shortterm and long-term horizons.

Labour market: The unemployment rate held steady at 5.1% in the March quarter, against the RBNZ’s forecast of a slight rise to 5.2%. The level of employment rose by 0.1%. Wage growth was softer than the RBNZ expected, with the Labour Cost Index slowing from 3.3% yr to 2.9%yr. Job advertisements are yet to show a lift from the cyclical lows reached last year.

Housing market: Both house sales and mortgage approvals point to increasing levels of housing activity since the second half of last year, trending higher as mortgage rates have been progressively lowered. Mortgage approvals remain strong. House prices have risen gradually in the last six months, broadly in line with the RBNZ’s expectations.

Commodity prices: Export commodity prices have continued to improve in recent months, especially in meat and dairy. Oil prices are noticeably lower than the RBNZ’s February projections. The overall terms of trade (measured on a National Accounts basis) is running ahead of what the RBNZ assumed in February.

Exchange rate: The trade-weighted exchange rate index (TWI) is currently around 69, about 2% higher than what the RBNZ assumed in the February MPS (and the RBNZ will likely flatline its May forecast at this level). Higher export commodity prices provide some justification for the stronger currency.

Kelly’s take.

The easing at this meeting seems reasonable given the weaker global outlook that has eventuated since April (and certainly February). However, I think the MPC should be increasingly mindful of the amount of easing already delivered, and the lags to when the peak impact of that easing will take hold.

Uncertainty is high right now due to the trade outlook. But underneath that uncertainty there are factors that should underwrite economic recovery over time, and which could frustrate a timely return of inflation to 2%. Uncertainty is a transitory factor while the interest rates and terms of trade levels will be more enduring when the uncertainty resolves. I think there are encouraging signs that deals will be done on trade that resolves the uncertainty soon enough.

While there could be adverse outcomes that require a lot more easing, they remain just a possibility at this stage. Our terms of trade have strengthened in the last month or so as trade policy uncertainty has surged. Policy is well placed to respond if negative scenarios unfold. With inflation nudging 3% there’s no strong case for taking insurance by easing pre-emptively right now. Taking the time to assess the impact of the easing already delivered and the likelihood of future damage to the economy coming from a tougher global trade environment may be more prudent between now and August.

Week Ahead – Fed Minutes, PCE Inflation and RBNZ Eyed as Trade War Cools Off

- Attention turns to Fed minutes and PCE inflation; can they lift the Dollar?

- RBNZ to likely cut again despite inflation pickup.

- Australian and Tokyo CPI, Canadian GDP, OPEC meeting on the agenda too.

- US yields and Treasury auctions also in focus as budget bill passes House.

US Dollar feels the strain of debt jitters

The trade war has taken a backseat over the past week amid an absence of fresh tariff headlines, bringing to the forefront the long-running concerns about the ballooning US national debt. America’s debt problem has been brought into the limelight as Congress is struggling to find common ground on tax and spending reductions. Market anxiety about what the new budget bill will entail has been made worse by Moody’s downgrade of America’s prized triple A rating.

The concerns are primarily about Congress passing a bill that could possibly add $4 trillion to the mounting debt, with long-dated Treasury yields surging in recent days. Even equity traders are nervous, while the US dollar has retraced 60% of its April-May rebound.

Having just scraped through the House of Representatives, the legislation will now head to the Senate where a vote is not expected before early June. Any headlines suggesting that Senate Republicans will try and push for deeper spending cuts than the House might offer some relief to the Treasury bond market, pushing yields lower, and steady the dollar.

The main risk is that worries about the growing deficit could rattle bond markets in a week where the US Treasury will auction 2-, 5- and 7-year notes.

Will core PCE ease further?

Another important driver over the coming week will be the PCE inflation and consumption numbers for April on Friday, which will be vital as they will be the first since President Trump’s ‘Liberation Day’. The core PCE price index – the Fed’s preferred inflation gauge – declined sharply in March, falling from 3.0% to 2.6% y/y. It’s estimated to have stayed unchanged in April according to the Cleveland Fed’s Nowcast model, but headline PCE is forecast to have fallen slightly to 2.2%.

Personal consumption will be monitored too for signs that the heightened uncertainty surrounding tariffs dampened household spending. After rising by a solid 0.7% m/m in March, personal consumption is expected to have increased by just 0.2% in April.

Ahead of that key report, durable goods orders will be watched on Tuesday, along with the consumer confidence index, followed by the second estimate of Q1 GDP growth and pending home sales on Thursday, rounded up by the Chicago PMI on Friday.

Investors will also be scrutinizing the FOMC minutes of the Fed’s May policy meeting for any clues about the timing of the next rate cut. The minutes are unlikely to offer any new clues as most policymakers have already expressed their views since the last meeting, maintaining their wait-and-see stance. Nevertheless, if the tone of the minutes is slightly more hawkish than anticipated, this could weigh on Wall Street but lift the dollar somewhat.

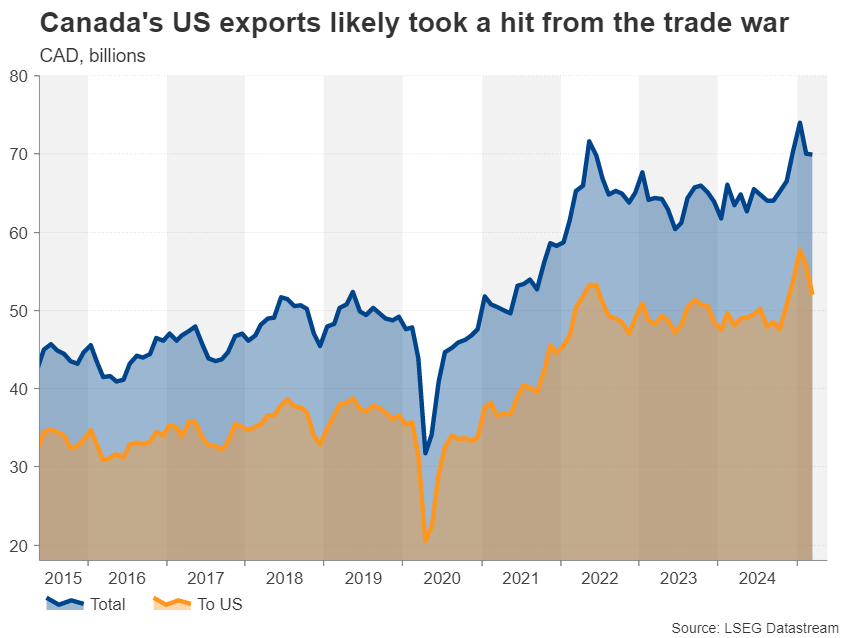

Canadian GDP to show hit from trade war

Across the border, Trump’s tariff war is certainly being felt in Canada where two thirds of the country’s exports are destined for the US. Frontloading by businesses might have provided some boost to exports in February before the new tariff levels for Canada and Mexico came into effect in March when they likely slumped. There’s been some indication that exports to countries other than the US surged in March, but this was probably not enough to offset the loss in US markets.

The overall impact on the Canadian economy in the first three months of the year should become clearer on Friday when the GDP report is released. After expanding by 0.6% q/q in Q4, the economy likely grew by a more tepid 0.2% q/q in Q1.

A bigger-than-expected slowdown could weigh on the Canadian dollar, as it would bolster bets of the Bank of Canada cutting interest rates at its June meeting, the probability of which currently stands at 30%.

RBNZ to cut for sixth time

There is a bit more certainty, however, with the Reserve Bank of New Zealand’s next policy decision. Investors are 90% confident the RBNZ will trim its cash rate by 25 basis points on Wednesday for the sixth consecutive meeting since last August. The remaining 10% odds are for rates to be kept on hold at 3.5% amid an uptick in both actual CPI and inflation expectations.

Nevertheless, with the labour market remaining weak and trade frictions casting a shadow over the global economy, the RBNZ will probably press on with another reduction but take a more cautious approach going forward.

As such, in the event of a hawkish cut, the New Zealand dollar might resume its rebound against the greenback that’s been on pause since late Aprill.

Over in Australia, the Reserve Bank of Australia’s rate-cutting cycle is only just getting started but some doubts remain about the pace of easing as inflation there is also proving to be stickier than anticipated.

The CPI numbers for April due on Wednesday should reveal whether inflation continued to ease in April or if it it’s turning higher again. Quarterly data on capital expenditure out on Thursday will also be watched.

Will Tokyo CPI edge higher?

Despite the ongoing trade war and a GDP contraction in Q1, inflation in Japan remains elevated well above the Bank of Japan’s 2% target. Even so, with the recent spike in Japanese government bond yields and trade talks between the US and Japan stalling, the BoJ is careful not to hike interest rates again until the clouds hovering over the outlook have cleared.

Yet, BoJ policymakers have also signalled that they are still committed to normalizing policy. Hence, the longer inflation stays above 2%, the more likely the BoJ will feel compelled to raise rates by a further 25 bps.

The CPI figures for the Tokyo region that are due on Friday will provide an update on price pressures in the Japanese capital as trade tensions spread uncertainty for local exporters. Other releases on Friday will include preliminary industrial production readings for April, the unemployment rate and retail sales. Before all that, the services PPI on Tuesday might attract some attention.

The combination of a weaker dollar and renewed risk aversion in the markets has been a boon for the yen, and those gains could be extended if the data boost rate hike bets.

Quiet start to week as OPEC considers new quotas

In the Eurozone, it will somewhat of an uneventful week, with only Tuesday’s economic sentiment indicator and Friday’s preliminary CPI prints out of Germany having the potential to stir the euro.

Barring any fresh trade tirades by Trump or geopolitical flare ups, global markets are also expected to start the week on a muted note as both US and UK markets will be shut on Monday for a Bank Holiday.

Meanwhile, OPEC and non-OPEC countries will hold a Joint Ministerial Monitoring Committee meeting on Wednesday to discuss new production quotas, but a decision may not be made until the regular monthly meeting the following Sunday.

There is speculation that the alliance will announce a further output increase for July, but there’s some doubts as to the size of the hike, specifically if it will match the 411,000 barrels agreed for May and June.

Oil futures could come under pressure if OPEC+ leaders maintain that pace for a third month.

Trade Woes Slow Canadian GDP

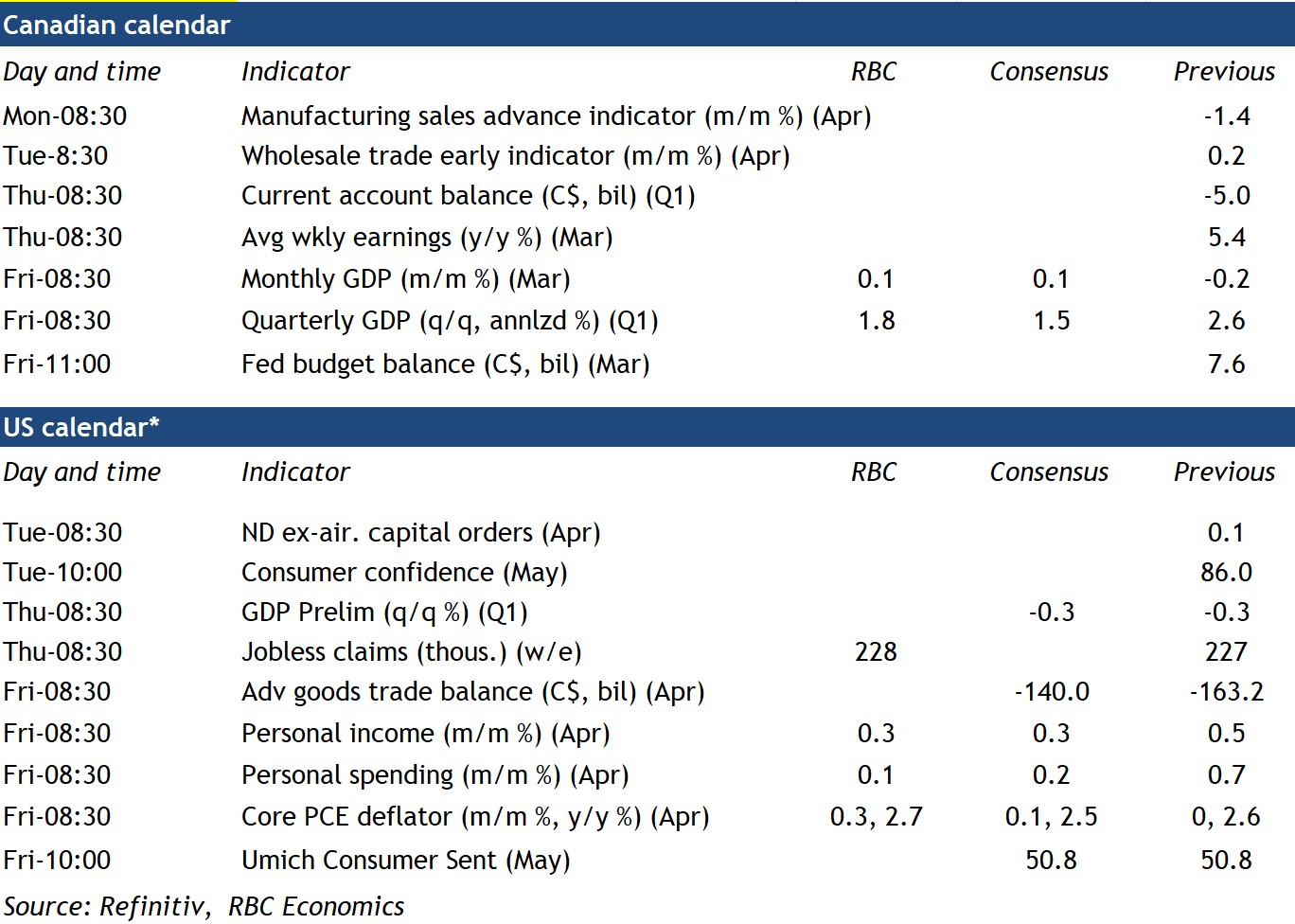

We expect gross domestic product data on Thursday will show the Canadian economy grew by 1.8% annualized in Q1.

The catch is that most of the increase came early in the quarter from a 0.4% rise in January. GDP contracted 0.2% in February from January as the federal GST tax holiday ended, severe weather disrupted transportation activity, and weakened sentiment from international trade uncertainty began to weigh on the economy. A recovery in the transportation sector and a bounce back in oil production in March likely led to a 0.1% increase in GDP—consistent with Statistics Canada’s advance estimate.

For expenditures, we expect to see an increase in household consumption in Q1 that was partially offset by a contraction in residential investment as home resales cooled. Business investment likely inched higher, but is expected to soften in the coming quarters as businesses freeze spending plans amid disruptive trade policies.

April’s manufacturing sales on Monday, wholesale sales on Tuesday, and the preliminary April GDP estimate will be closely watched for signs of softening in the economy extending into Q2. Housing markets remain soft, and trade uncertainty will likely continue to dampen business investment. Employment would have declined in April without temporary federal election hiring. Manufacturing has already posted its largest one month of job losses (-30,600) since the pandemic.

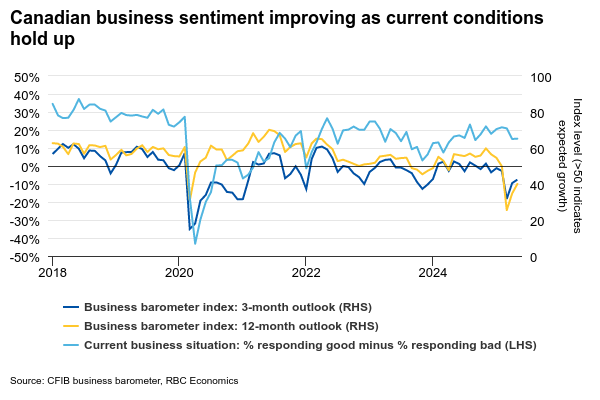

There are still spots of resilience in the economy. Our RBC cardholder tracking shows consumer spending has remained resilient despite plunging confidence, aligning with StatsCan's advance estimate of retail sales rising 0.5% in April following a 0.8% March gain. And while businesses still report significant worries about the future outlook, the assessment of current conditions was firmer in data from the Canadian Federation of Independent Business this week.

Canada’s still facing the lowest tariff rate among all U.S. trade partners after being exempted from reciprocal tariffs in April. Job opening data in early May from Indeed.com shows signs of stabilization in labour markets. Overall, we expect Canadian GDP growth to slow significantly this year, but not contract as strength in domestic demand continues to offset external weakness from trade turbulence.

Week ahead data watch

Weekly Focus – US Budget Bill Not So ‘Beautiful’ If You Ask the Bond Market

The US House managed to pass the budget bill with a slim majority of just one vote on Thursday. Cuts to spending on medicare and food stamps flipped the last votes in favour of the bill, which also includes an extension of the 2017 tax cuts, and adds further tax cuts. US President Donald Trump calls it his 'one, big, beautiful bill' and while bond markets agree it is big they do not see it as 'beautiful'. The budget bill has added further steam to the rise in long bond yields following last week's downgrade by Moody's. US 30-year bond yields pushed to a new high of 5.15% on Thursday, close to the highest yield in 18 years and around 80bp above a 30-year Greek government bond yield. The anxiety over rising yields spilled into weaker US equity markets as well as a lower USD. The bill now goes to the Senate where it will take some time to pass and any changes must go back to the House for approval again, which means it could still take some time before it is all done and ready to be signed by Trump. On the data front US PMIs surprised to the upside but a sharp uptick in the inventory component suggests it is related to front loading of imports and production. This week we moved our call for the next Fed cut to September, but we still see gradual rate cuts after that until rates are around neutral at 3.25%.

Turning to Europe, PMIs for May were a mixed bag with PMI manufacturing rising from 49.0 to 49.4 while PMI service dropped yet again from 50.1 to 48.9, the lowest in more than a year. With the service sector being the biggest part of the economy, the declining activity is a concern. On Monday, the EU Commission lowered their inflation forecast for 2026 to 1.7% from 1.9%. Since the ECB uses a similar model as the Commission it would suggest we see a comparable revision at their upcoming June meeting. Markets now price a 95% probability of a rate cut at the meeting and one further cut by year-end. We expect two further cuts after June as downward pressure on inflation continues due to falling wage pressure, lower oil prices and China exporting deflation.

Chinese data for April was soft but spending may have been affected by the massive escalation of the trade war at the time. Activity is set to increase over the next three months as exports surge in the 90-day truce period and stimulus support demand. Oil prices moved lower again this week to USD64 per barrel from USD67 a week ago as OPEC+ members are weighing a third output increase in July after raising it in both May and June.

Not much happened on the trade talks agenda. After a successful meeting between US and China 10 days ago, frictions have returned. China stated that a US guideline on banning Huawei AI chips globally undermined the consensus reached at the talks. We still see a bumpy road ahead in US-China trade talks and a long way to a real deal (see also recording of our webinar on US-China trade that we held on Wednesday). US is negotiating with a long list of other countries but apart from UK, we still wait for new deals. EU sent a new proposal to the US ahead of talks on Thursday this week.

Next week is quiet on the news front. Main releases are US consumer confidence, euro inflation expectations from ECB, US consumer spending and any news on trade talks. The following week we get more action again with ECB meeting on 5 June and US non-farm payrolls on 6 June. Chinese PMIs and US ISM manufacturing is also due.