Sample Category Title

Euro Under Pressure as Services PMIs Slip

The euro fell close to 1% on Wednesday but has recovered. In the European session, EUR/USD is trading at 1.1430, down 0.09% on the day.

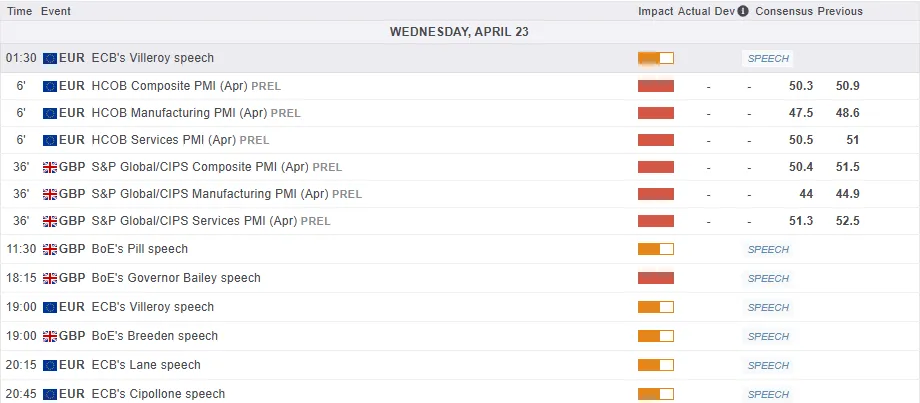

Euro, German PMIs contract in April

Euro and German Services PMIs disappointed in April, as they were lower than expected and fell into contraction territory. This marked the first decline in business activity in Germany and the eurozone since November 2024.

The Euro Services PMI eased to 48.8, down from 50.9 in March and shy of the market estimate of 50.2. Business confidence was sharply lower. Germany's Services PMI fell from 51.0 to 49.7, below the market estimate of 50.5. Concerns about tariffs and uncertainty over economic conditions resulted in a decrease in new orders and weaker business sentiment.

The manufacturing sector remained in contraction. Eurozone Manufacturing PMI rose to 48.7 from 48.6, above the market estimate of 47.5. The German Manufacturing PMI eased to 48.0, down from 48.3 in March but above the market estimate of 47.6.

The weak PMI numbers point to weakness in the German and eurozone economies due to the escalation in trade tensions. The ECB has lowered interest rates seven times in the current easing cycle, and the current key rate is down to 2.25%, its lowest since Dec. 2022. The markets are looking at up to three more rate cuts this year from the ECB. The central bank wants to support the fragile recovery by continuing to trim rates but must keep an eye on the upside risk to inflation due to the tariffs.

It is a light data calendar in the US this week, and the first key events of the week, Services and Manufacturing PMIs, will be released later today. The markets are braced for a weak showing - services is expected to ease from 54.4 to 52.8 and manufacturing to 49.4 from 50.2.

EUR/USD Technical

- EUR/USD tested support at 1.1377 and 1.1332 earlier

- There is resistance at 1.1462 and 1.1507

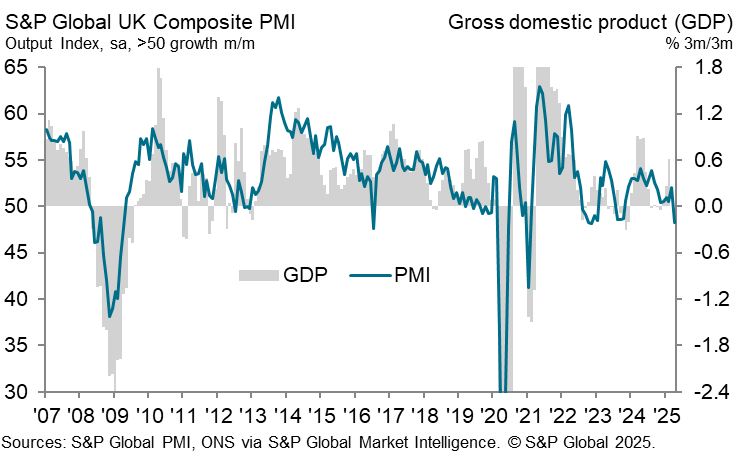

UK PMI composite plunges to 48.2, recession fears, pressures BoE to cut rates

The UK private sector contracted sharply in April, with the flash PMI Composite falling from 51.5 to 48.2, the lowest reading in 29 months. PMI Manufacturing dropped from 45.3 to 44.0, a 20-month low. PMI Services slipped from 52.5 to 48.9, the weakest in 27 months.

According to S&P Global’s Chris Williamson, the downturn marks the steepest fall in output in nearly two and a half years, with data now pointing to a potential quarterly GDP decline of -0.3%.

Also, business sentiment has sunk to its lowest level since late 2021, and even beneath the post-Brexit vote lows. The slump in exports, tied to weak global demand and escalating trade tensions, is adding to domestic burdens. Rising staffing costs—partly due to changes in National Insurance and minimum wage rules—have further squeezed margins.

The sharp contraction and collapsing sentiment pose "red flags" for policymakers and could tip BoE toward cutting rates at its upcoming May meeting.

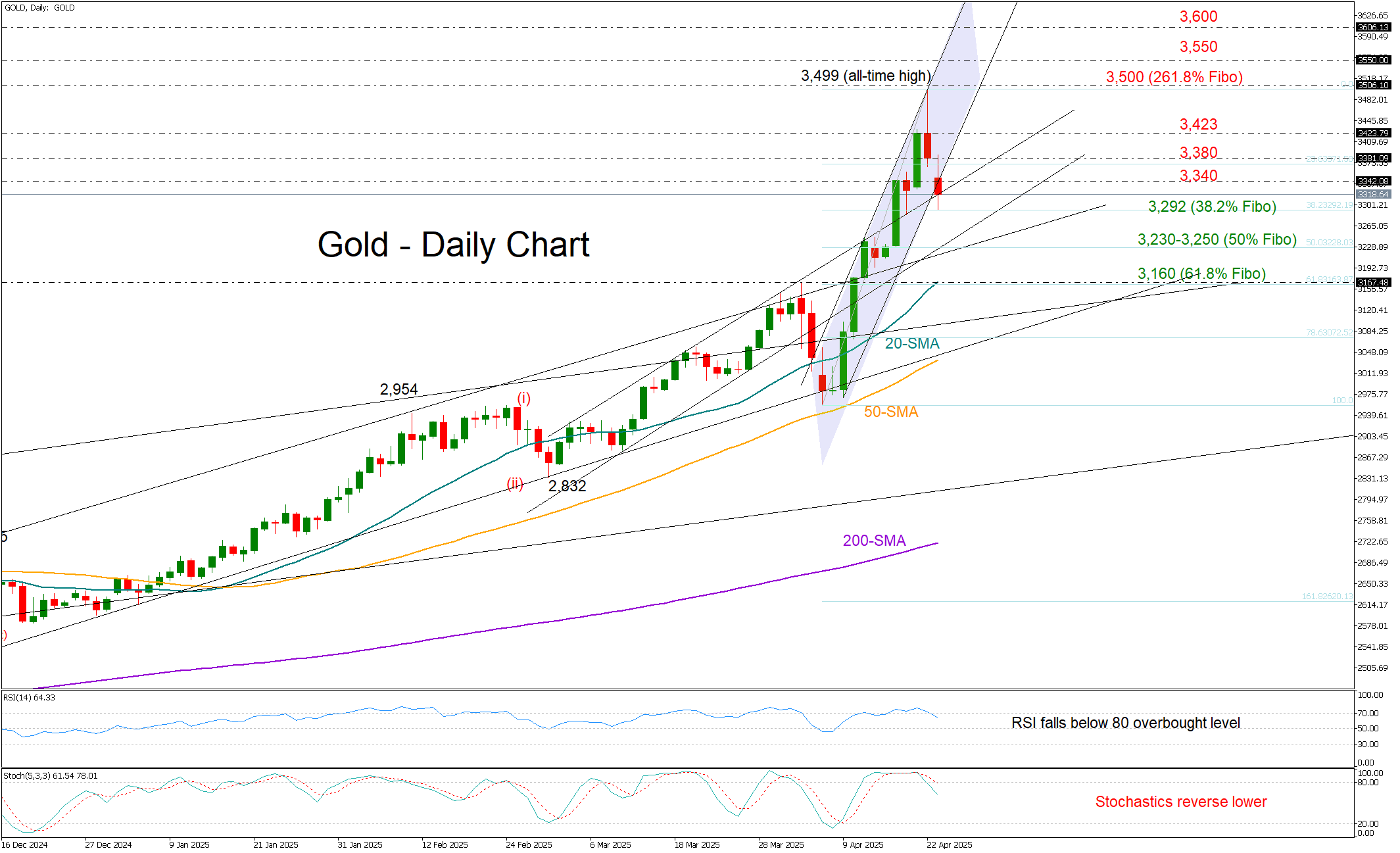

Gold Takes a Breather After Another Milestone

- Gold pulls back after sharp rally to all-time high.

- Bearish candlestick pattern emerges; overbought signals confirmed.

- Sellers eye a close below 3,290 to target lower levels.

Gold opened Wednesday’s session with a downside gap, extending its retreat from the record high of 3,499.

The formation of a bearish shooting star on the weekly chart increases the probability of a downside reversal. This view is reinforced by overbought signals coming from both the RSI and the stochastic oscillator on the daily timeframe.

However, a confirmation of the bearish bias would likely come with a drop below the 3,340 support area, and more importantly, a break beneath the 38.2% Fibonacci retracement level of the recent rally at 3,292 – a level that provided a footing under the price earlier today. If the bears take control below this zone, the next key support could come around the trendline area of 3,230-3,250, where the 50% Fibonacci mark resides. Further weakness could potentially lead the price toward the 61.8% Fibonacci mark at 3,160 and the 20-day simple moving average (SMA). A drop below that could expose the price to the 3,100 region.

On the flip side, if the precious metal pivots above 3,340, it may initially retest resistance around the 3,380 zone ahead of the 3,423 barrier. A sustained break above the 3,500 psychological level could reignite bullish momentum, setting the stage for a rally toward 3,550 and potentially 3,600. A continuation higher may even put the 3,800 region in focus.

All in all, gold’s recent pullback could extend in the short term, but sellers may wait for a decisive break below 3,292 before stepping in more aggressively.

President Trump, Bessent Temper Rhetoric Which Fuels Optimism, Risk Assets Rise

Stock prices rose, and the dollar gained slightly as the Trump administration eased tensions that had recently unsettled financial markets.

President Trump's comments last night boosted sentiment and once again proved that his outbursts should at times be taken with a pinch of salt. Any concerns about Federal Reserve independence appear to have been put to bed as President Trump confirmed he has no plans to remove Fed Chair Jerome Powell but that he would prefer a rate cut sooner rather than later.

Signs of progress in some trade talks also helped improve market sentiment with Trump and Treasury Secretary Scott Bessent saying that a standoff with China will ease. \there were also reports of positive developments in trade talks with Japan and India which further aided market optimism.

The above has seen risk assets wipe out early week gains with Gold trading lower than its weekly open, down around $3300/oz handle.

US index futures rose, wiping out Monday's losses and also gapping up overnight. A continuation of the improved risk appetite we are seeing could lead to further gains ahead in today's session.

The improved sentiment has also led to European stock indices recovering with the DAX finally breaking above key areas of resistance and eyeing further gains at the start of the European session.

SAP shares surged 9.3% after the German company exceeded analysts' expectations for first-quarter adjusted operating profit. The European technology sector rose 3.3%, making it the best-performing industry group.

The dollar gained over 1% against the yen, hitting 143.21 early on but later settled at 141.85. It also rose 0.4% against the Swiss franc to 0.8222, after climbing more than 1% earlier. Meanwhile, the euro dropped 0.2% to $1.1393, and the British pound fell 0.15% to $1.3313.

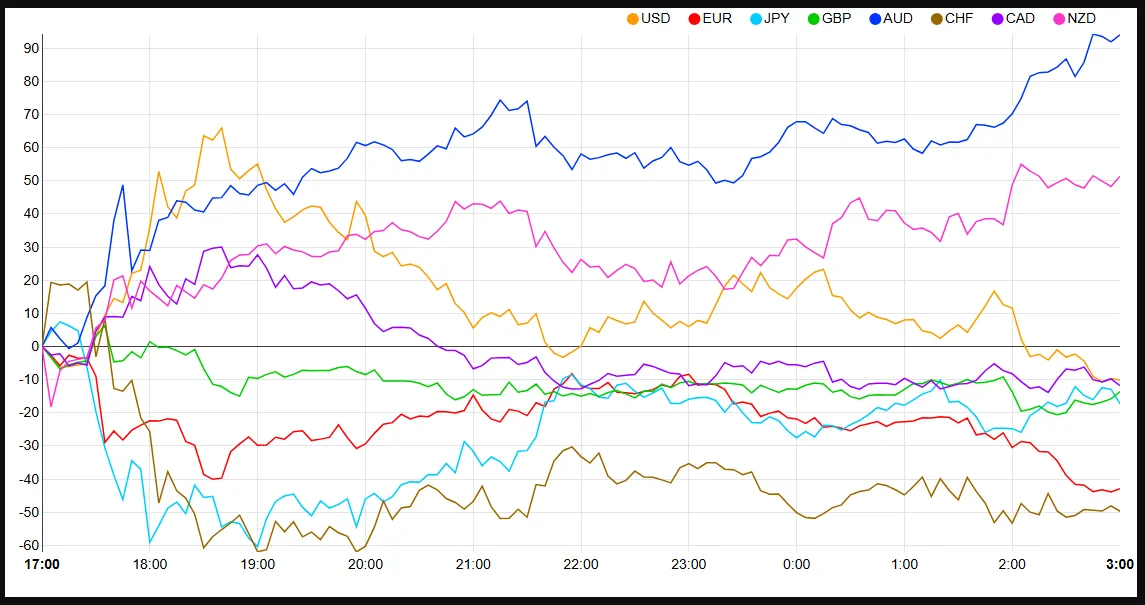

Currency Strength Chart, Strongest - Weakest: AUD, NZD, USD, CAD, GBP, JPY, EUR, CHF

Source: FinancialJuice

Economic data releases

From a data standpoint, it’s a packed session for Europe as key economic reports from the Eurozone and the UK are set to be released. Significant deviations from expectations could trigger notable market volatility.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - DAX

From a technical standpoint, the DAX has broken above a key resistance level thanks to the improved risk sentiment in play.

The index now trades above the 20 and 100-day MAs with the potential death cross now looking unlikely if the bullish momentum persists.

The DAX is now eyeing resistance at a key level around 22405 with the the 200-day MA resting just below at 22278 and could prove a stubborn hurdle.

If the index is able to maintain the bullish momentum and break above the 22405 handle then focus shifts to 22800 and 23200 as key areas of resistance.

Any move lower now, and support rests at 21602, 21433 before the 20800 and 20400 handles come into focus.

DAX Chart, April 23, 2025

Source: TradingView.com (click to enlarge)

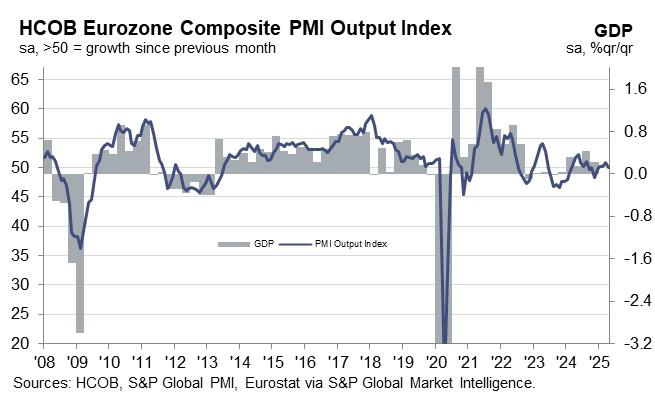

Eurozone PMI Composite slips to 50.1, services contract but manufacturing unfazed by tariffs

Eurozone economy showed signs of stagnation in April as its Composite PMI slipped to 50.1, down from 50.9 in March—a four-month low. The decline was driven primarily by a downturn in the services sector, which contracted for the first time in five months, with the PMI falling from 51.0 to 49.7. In contrast, manufacturing showed unexpected resilience, with PMI ticking up slightly from 48.6 to 48.7, reaching a 27-month high.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that manufacturers appear "not too fazed" by the recent imposition of broad US tariffs, including 10% general duties and 25% on autos.

He pointed to falling energy prices, driven in part by US recession fears, and planned increases in defence spending as factors supporting the manufacturing sector. However, the decline in services activity has dragged down overall output, pushing the Eurozone economy into what de la Rubia called "stagnation territory."

ECB may find some comfort in the latest inflation signals. While input costs in services remained elevated, the pace of selling price increases eased. In the goods sector, input prices fell, breaking a four-month trend of rising costs, while output prices saw only a modest rise.

At the country level, both Germany and France mirrored the regional trend, with manufacturing output gaining but services activity declining.

Pound Hits Fresh High Against US Dollar Before Correcting: What’s Driving GBP/USD?

GBP/USD reached a seven-month peak at 1.3423 — its highest level since 26 September 2024 — before entering a corrective phase.

Key Drivers Behind GBP/USD Movements

Market concerns over US President Donald Trump’s criticism of Federal Reserve Chair Jerome Powell have eased. Trump has since clarified that Powell will not be dismissed, though he expressed frustration over the Fed’s reluctance to cut interest rates sooner.

The US Dollar’s rebound against the Pound followed the release of UK inflation data and a slightly weaker outlook for the labour market. Although the figures were published last week, the market has only now fully digested their implications.

In March, the UK Consumer Price Index (CPI) slowed to a three-month low. Meanwhile, the employment sector appears vulnerable ahead of another planned rise in employer taxes, due by the end of April.

Current market expectations suggest the Bank of England (BoE) will cut interest rates by 25 basis points (bps) in May, with an additional 85 bps of easing anticipated by year-end.

While US tariff policies are unlikely to directly impact UK inflation, their broader effect may contribute to lower rather than higher price pressures.

Technical Analysis: GBP/USD

H4 Chart Overview

- The pair formed a consolidation range near 1.3066 before breaking upwards in a wave structure towards 1.3420.

- A corrective pullback to 1.3200 is now underway.

- The next phase may see a resumption of upward momentum towards 1.3310, potentially establishing a new consolidation range around this level.

- The MACD indicator supports this outlook, with its signal line exiting the histogram area and pointing sharply downward, suggesting near-term bearish momentum.

H1 Chart Overview

- GBP/USD broke below 1.3310, hitting a local downside target at 1.3233.

- Today, the pair retested 1.3310 from below, and further downside movement towards 1.3200 is now in focus.

- The Stochastic oscillator aligns with this view, as its signal line remains below 80 and is trending downward towards 20, indicating weakening bullish momentum.

Conclusion

The GBP/USD rally has paused as traders assess mixed UK economic data and shifting Fed policy expectations. While near-term corrections are likely, the broader trend could see renewed upside if key support levels hold. Technical indicators suggest further consolidation before the next decisive move.

EUR/USD Dips From Highs, USD/JPY Eyes Fresh Increase

EUR/USD declined from the 1.1570 resistance and traded below 1.1470. USD/JPY is rising and might gain pace above the 142.45 resistance.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline after a strong surge above the 1.1500 zone.

- There was a break below a key bullish trend line with support at 1.1440 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 141.00 and 141.65 levels.

- There was a break above a connecting bearish trend line with resistance at 141.20 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair rallied above the 1.1500 resistance zone before the bears appeared. The Euro started a fresh decline and traded below the 1.1500 support zone against the US Dollar.

There was a break below a key bullish trend line with support at 1.1440. The pair declined below 1.1410 and tested the 1.1310 zone. A low was formed near 1.1308 and the pair started a consolidation phase. There was a minor recovery wave above the 1.1370 level.

The pair climbed above the 23.6% Fib retracement level of the downward move from the 1.1573 swing high to the 1.1308 low. EUR/USD is now trading below 1.1440 and the 50-hour simple moving average.

On the upside, the pair is now facing resistance near the 1.1410 level. The next key resistance is at 1.1440 and the 50% Fib retracement level of the downward move from the 1.1573 swing high to the 1.1308 low.

The main resistance is near the 1.1470 level. A clear move above the 1.1470 level could send the pair toward the 1.1570 resistance. An upside break above 1.1570 could set the pace for another increase. In the stated case, the pair might rise toward 1.1650.

If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.1335. The next key support is at 1.1310. If there is a downside break below 1.1310, the pair could drop toward 1.1265. The next support is near 1.1220, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh upward move from the 140.00 zone. The US Dollar gained bullish momentum above 141.65 against the Japanese Yen.

There was a break above a connecting bearish trend line with resistance at 141.20. It even cleared the 50-hour simple moving average and 142.45. The pair climbed above 143.00 and traded as high as 143.21 before there was a downside correction.

The pair dipped below the 23.6% Fib retracement level of the upward move from the 139.88 swing low to the 143.21 high. The current price action above the 141.65 level is positive.

Immediate resistance on the USD/JPY chart is near 142.45. The first major resistance is near 143.20. If there is a close above the 143.20 level and the RSI moves above 75, the pair could rise toward 144.50.

The next major resistance is near 145.00, above which the pair could test 148.00 in the coming days. On the downside, the first major support is 141.65 and the 50% Fib retracement level of the upward move from the 139.88 swing low to the 143.21 high.

The next major support is visible near the 141.00 level. If there is a close below 141.00, the pair could decline steadily. In the stated case, the pair might drop toward the 139.90 support zone. The next stop for the bears may perhaps be near the 137.50 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

US-China De-Escalation Optimism Sparked a Relief Risk Appetite Revival

Risk appetite returned in the overnight US session yesterday, 22 April, sparked by US Treasury Secretary Bessent's remarks that he sees a de-escalatory path forward regarding the U.S. trade standoff with China in a closed-door investor summit.

All the major US stock indices erased Monday’s losses with the S&P 500, Nasdaq 100, Dow Jones Industrial Average, and Russell 2000 gaining more than 2% yesterday, but remained below their respective 20-day moving averages.

Yesterday’s revival in risk appetite has also been led by a recovery in the US dollar, especially against the haven currencies, where the USD/CHF and USD/JPY gained by 1.2% and 0.5% respectively.

In today’s Asian opening session, the S&P 500 and Nasdaq 100 E-mini futures extended their intraday gains to 1.6% and 1.8% respectively at this time of writing, reinforced by the news report stating that US President Trump backed down from his earlier threat to remove Fed Chair Powell from office, and mentioned the 145% tariffs on Chinese imports will eventually “come down substantially”

Major Asian benchmark stock indices were jolted up by such “US-China de-escalation” optimism. Japan’s Nikkei 225 staged a rally of 2%, and Hong Kong’s Hang Seng Index surged by 2.4% at this time of writing.

Lack of safe haven demand triggered a sharp bearish reversal in gold (XAU/USD), which fell 1.3% to close yesterday’s US session at $3,381, its worst single-day performance since 7 April. This decline came after gold hit a fresh intraday all-time high of $3,500. Despite the pullback, it remains above its 20-day moving average, which continues to provide support around the $3,170 level.

In its latest updated World Economic Outlook report, the IMF cut economic growth forecasts for most countries due to US trade tariffs and rising trade tensions. The global economic growth forecast for 2025 was slashed to 2.8% from 3.3% projected in January.

Economic data releases

Fig 1: Key data for today’s Asian mid-session (Source: MarketPulse)

Chart of the day – Japan 225 cleared above 20-day moving average

Fig 2: Japan 225 CFD Index minor trend as of 23 Apr 2025 (Source: Trading View)

The price actions of the Japan 225 CFD Index (a proxy of the Nikkei 225 futures) have staged a bullish gap-up above its 20-day moving average with a positive momentum reading in its hourly RSI momentum indicator, which suggests that it may extend its mean reversion corrective rebound in place since its 7 April swing low of 30,343.

Watch the 34,315 key medium-term pivotal support for the next immediate resistances to come in at 35,730 and 36,450 (also the 50-day moving average).

On the flip side, a break below 34,315 invalidates the bullish tone to revive the bears to expose the next intermediate supports at 33,680 and 32,425 in the first step.

Trump’s Comments Give Impression of Intended De-escalation Effort

Markets

Yesterday during the day, markets gradually entered calmer waters as the impact of the rift between President Trump and the Fed gradually unwound. US equities more than reversed Monday’s decline with major indices closing between 2.51% (S&P 500) and 2.71% (Nasdaq) higher. US Treasuries also entered calmer waters. Despite recent pressure from the White House, most Fed members (in a balanced way) still joined Chair Powell’s thesis that policy is currently well positioned for changes in the economy and that if the combination of a olid labour market and higher inflation risks/expectations persists, the Fed will keep rates on hold at least of a while (e.g. Fed Kugler). US yields in a corrective flattening move changed between + 5.7 bps (2-y) and -2.5 bps (30-y). However, the major market-relevant events still came after the close of US markets. President Trump’s media messages aren’t contained by the regular trading hours. In comments to reporters, he stated that he has no intention of firing Powell. He only would like him to be ‘early or on time as opposed to being late’ with respect to cutting interest rates. At the same time, the US President also struck a relatively ‘soft’ tone on trade negotiations with China as he indicated that tariffs might drop substantially in case of a deal. The comments of course were only a ‘temporary photo’ of the mindset at the White House. Even so, it gave the impression of some kind of an intended de-escalation effort. US equities rallied further post-market. The US yield curve this morning bull flattens (30-y -7.5 bps) and the dollar regains some further ground after yesterday’s intraday comeback (USD DXY 99.2, EUR/USD 1.138). On European markets, yields yesterday still declined a few bps (Germany -2.5 bps 2-y; -3.7 bps 30-y). Several ECB members, including Chair Lagarde, indicated that the ECB is close to reaching its price stability objective, but that all options are open for the June policy meeting as uncertainty remains elevated. Despite this balanced comments post last week’s ECB meeting, markets continue to anticipate further ‘aggressive’ ECB easing later this year (near 1.50% by year end). We assume this trend has gone (more than) far enough.

Asian markets this morning mostly show gains between 1 à 2% after the de-escalation in the US yesterday evening. Aside from new ‘guidance’ from the US administration, markets today will keep a close eye at the April PMI’s. Overall sentiment in EMU (composite PMI) is expected to backtrack from the positive momentum in March (50.2 from 50.9). The survey already covers the period after Trump’s tariff announcement on liberation day (April 2). Especially for Europe, we keep a close eye at the expected impact on prices. If slower growth coincides with rather modest price growth, it might further fuel the market debate on an additional ECB rate cut in June even as we consider it too early to draw conclusions. In the US, the composite index also is expected to ease from 53.5 to 52.0. Over there, a stagflationary narrative is likely, but an outright negative signal from the labour market might put additional pressure on the Fed to reconsider the balance with respect to its dual mandate. The dollar recently suffered from a US-driven risk-off, but we don’t expect a sustained comeback, even in case of a (temporary) improvement in risk sentiment.

News & Views

Czech National Bank deputy governor Frait yesterday signaled room for one more rate cut in the second half of the year, from 3.75% now to 3.5% even though investors expect it to be slightly lower in part due to global financial market turbulence. Money markets discount a 25 bps at the next, May 7, policy meeting and a 3% policy rate by year-end. Ahead of that meeting, the CNB still gets Q1 GDP data (Apr 30) and one additional CPI report (May 6). Frait wants to be very careful with further monetary easing with the labour market being one of the reasons. It is still tight and wages, especially in market services, are growing relatively quickly. Rising property prices and fiscal dynamics are other domestic inflation risks.

Rumours suggest that French President Macron is considering to call snap parliamentary elections as early as this autumn or alongside municipal elections next year (March). Macron is reportedly consulting with his inner circle and weighing the potential benefits and risks of such a move. The aim would be to regain a legislative majority, banking on his boost in popularity thanks to greater international prominence. The gamble to regain political stability through elections could backfire though in more political instability if results disappoint. Macron’s presidential term ends in April 2027 ahead next parliamentary elections (June 2029).

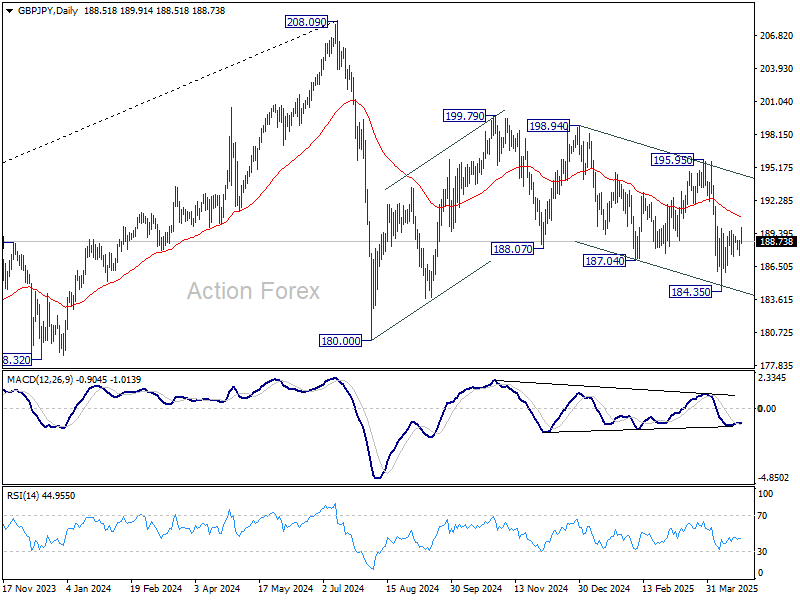

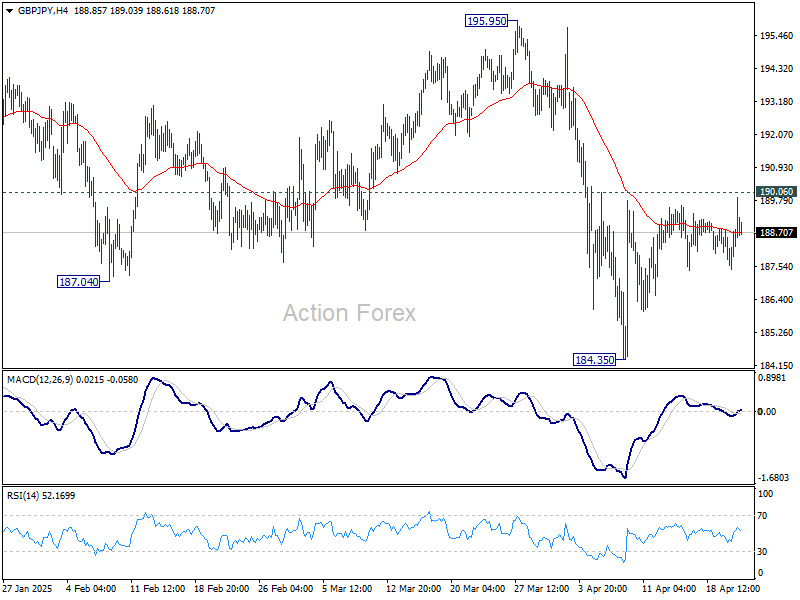

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.88; (P) 188.38; (R1) 189.29; More...

Intraday bias in GBP/JPY stays neutral and outlook is unchanged. Risk will remain on the downside as long as 190.06 resistance holds. Below 184.35 will target 180.00 low. Nevertheless, break of 190.06 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.