Sample Category Title

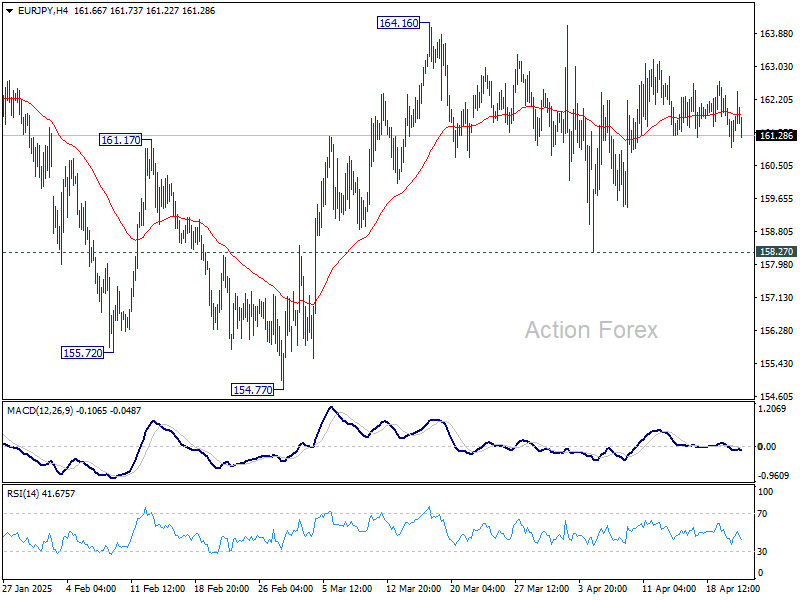

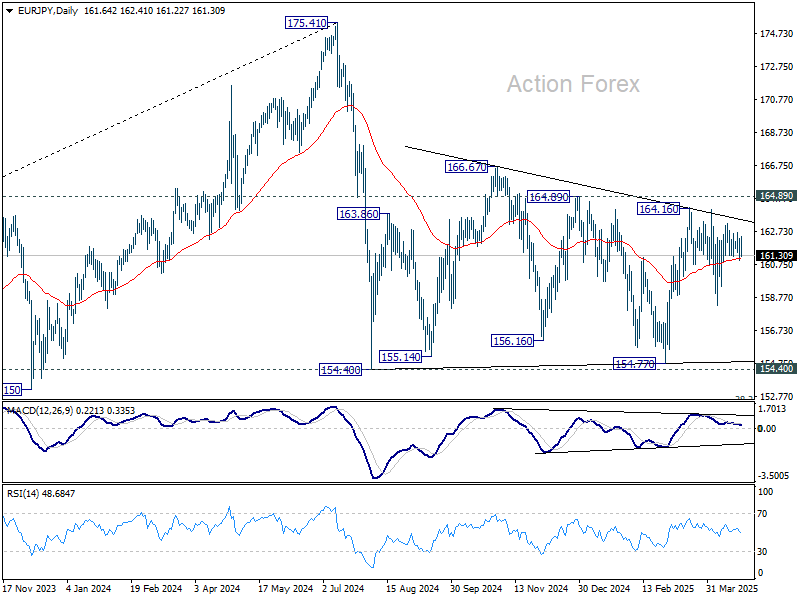

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.03; (P) 161.68; (R1) 162.36; More...

Intraday bias in EUR/JPY remains neutral for the moment, and more range trading could be seen. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

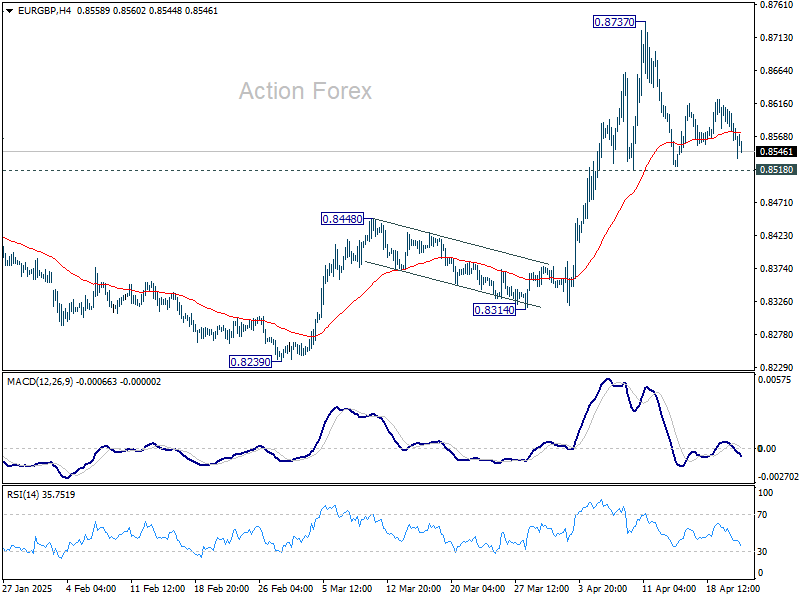

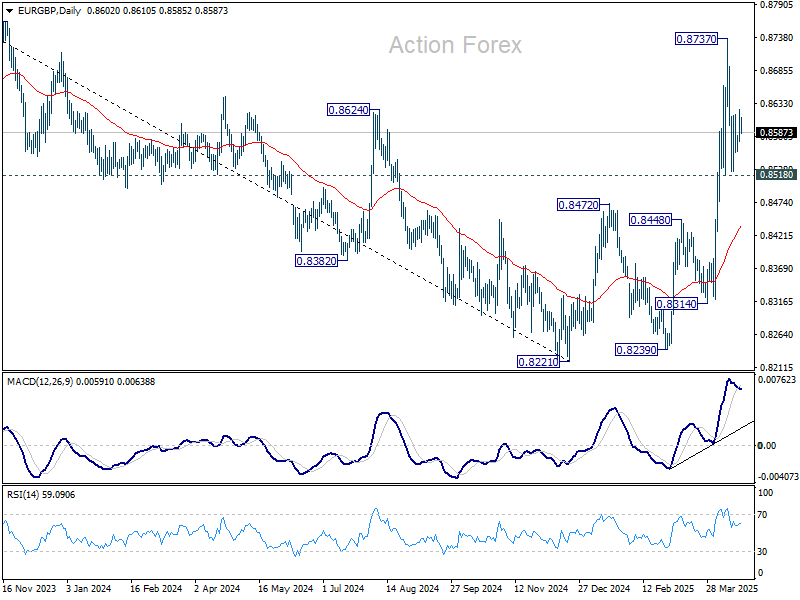

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8549; (P) 0.8582; (R1) 0.8599; More...

Intraday bias in EUR/GBP stays neutral at this point, and more consolidations could be seen below 0.8737 short term top. Further rise is expected as long as 0.8518 support holds. On the upside, break of 0.8737 will resume the larger rally from 0.8221. However, sustained break of 0.8518 will bring deeper fall back to 55 D EMA (now at 0.8438).

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

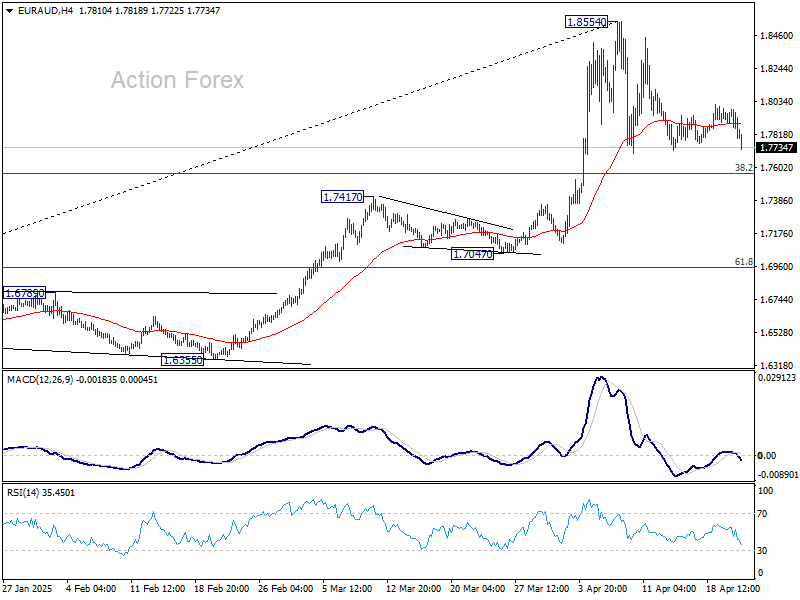

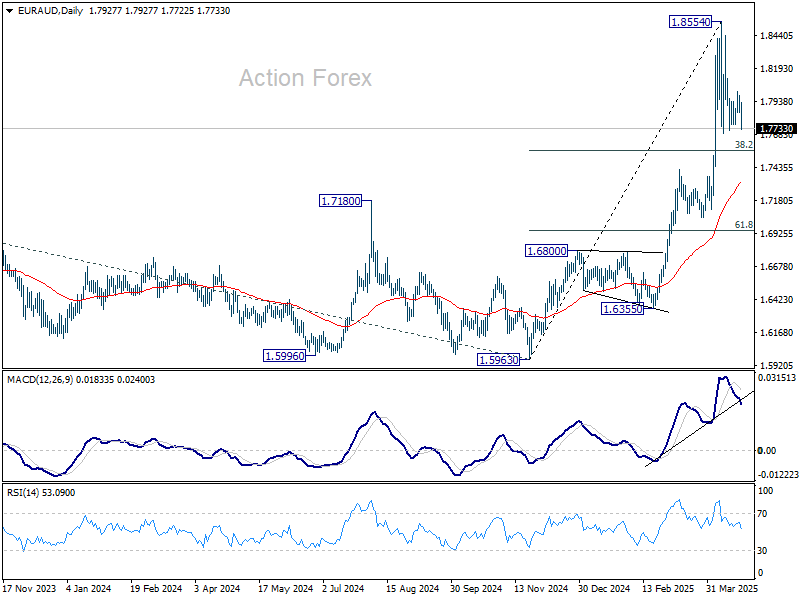

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7873; (P) 1.7928; (R1) 1.7997; More...

EUR/AUD is still extending the corrective pattern from 1.8554 short term top. Intraday bias remains neutral at this point. Downside of pull back should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend. However, firm break of 1.7750 will bring deeper fall to 55 D EMA (now at 1.7322).

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

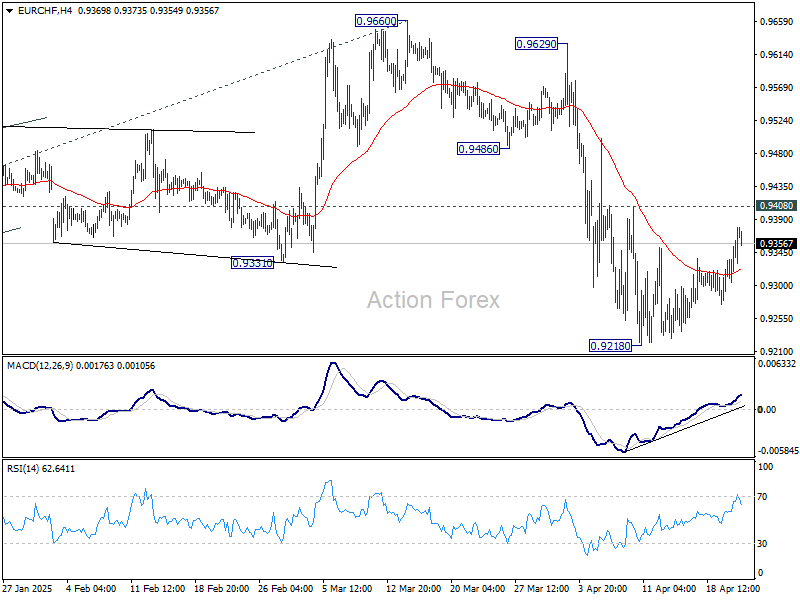

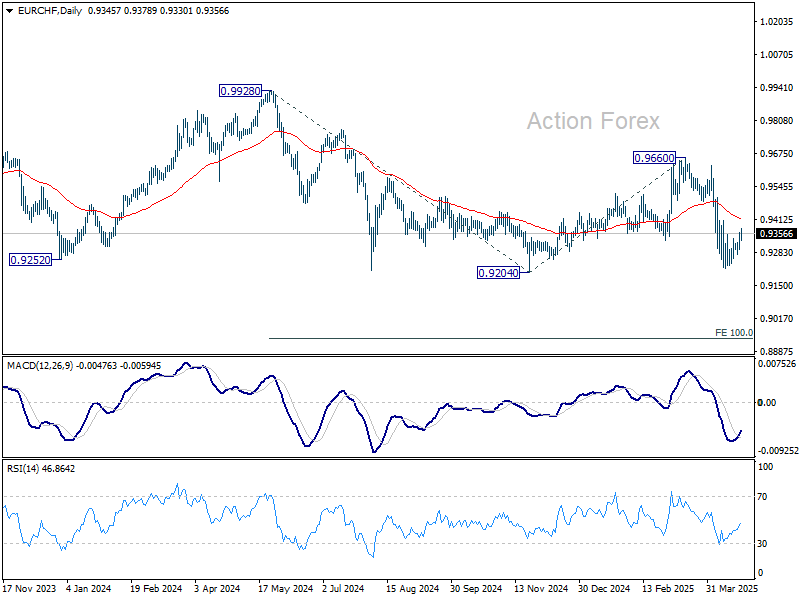

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9308; (P) 0.9335; (R1) 0.9381; More....

EUR/CHF's rebound from 0.9218 extended higher but stays below 0.9408 resistance. Intraday bias remains neutral and outlook stays bearish as long as 0.9408 resistance holds. On the downside, firm break of 0.9204 low will confirm larger down trend resumption.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. Next target is 100% projection of 0.9928 to 0.9204 from 0.9660 at 0.8936.

All Eyes on PMIs

In focus today

Today's key events will be the April flash PMIs from the euro area, US and the UK, which likely could give the first glimpse of the impact from tariff uncertainty.

In the euro area, we expect to see a decline in the manufacturing index to 48.2 from 48.6 due to less new orders from the US, while the services figure should remain broadly unchanged at 51.0. In principle, the PMI index should not be affected by sentiment effects, but the risk is that we see a negative impact anyway.

In the US, a similar pattern is likely to emerge, with the manufacturing sector weakening - as suggested by last week's gloomy Philly Fed index. The services PMI should hold up better, unless consumer uncertainty has begun to weigh on consumption, though March retail sales defied this.

Economic and market news

What happened overnight

In Japan, April PMIs were mixed, as the manufacturing leg continued to contract for the tenth straight month, printing 48.5, partly due to concerns over Trump's tariffs. Conversely, the service sector measure ticked up to 52.2, driven by customer demand that led to the strongest increase in sales in three months. Importantly, inflationary pressures remained high across both sectors, with overall input costs rising at the fastest rate in two years - and thus firms raising sales prices. The composite measure re-entered the expansionary territory, increasing to 51.1 from 48.9 in March.

What happened yesterday

In the US, the Richmond Fed Manufacturing index worsened to -13 in April (March: -4), with the shipments component dropping to -17 from -7. Coupled with last week's Philly Fed index, regional Fed manufacturing surveys are pointing towards a clear decline in April so far. Hence, it looks like the front-loading boost to new orders seen in Q1 is shifting towards an uncertainty-driven slowdown.

Politically, Trump altered course yesterday, backing off from his threat to fire Fed Chair Powell, stating: "I have no intention of firing him." This led prediction markets to price in a 13% chance that Powell will leave this year, down from 21% prior to the announcement. Trump's de-escalation also improved market sentiment, sending stocks higher, the USD gaining ground again, and gold prices declining. Before Trump's U-turn, Treasury Secretary Bessent had described the trade war with China as "unsustainable," which initially triggered the rebound in asset prices. Adding to the somewhat softer stance on China, Trump also expressed optimism about a potential trade deal, suggesting it would result in "substantially" lower tariffs on Chinese goods. However, he clarified that the final deal "won't be anywhere near" current tariff rates — though "it won't be zero," he added. Note that Bessent is set to speak later today on the state of the financial system.

In the euro area, consumer confidence declined to -16.7 in April from -14.5 in March, dropping to the lowest level since November 2023 - likely due to Trump's trade war and the sharp declines in equity markets. Notably, the lower confidence readings are yet to translate into hard data - both when looking at similar data from other economies (e.g., US March retail sales) and our own high-frequency data on card transactions in Denmark among Danske Bank private customers. Hence, the weakening in consumer confidence appears to be a Trump effect rather than a reflection of a concrete deterioration in household finances. That said, we do expect the trade war to negatively affect euro area growth over the coming year, though likely not to the extent consumers fear, given the backdrop of low unemployment, rising real incomes, and the ECB's monetary easing, which should help support consumption amid trade uncertainty.

The ECB's quarterly survey of professional forecasters showed slightly higher inflation expectations and lower growth expectation compared to the last release. Tariffs and defence spending were the main factors behind the revisions. However, the revisions were very small, indicating that analysts have not yet turned significantly negative on the euro area economy following Trump's trade war. The survey was conducted between April 1 and April 4, so it likely includes the "liberation day" tariffs but not the clear escalation between the US and China. Hence, we will likely see a further downward revision of the growth forecast in the next update, and we also expect lower inflation forecasts following the marked increase in EUR/USD since April 4.

Tariffs and the trade war remain in the limelight, as reflected by the IMF's downgrade of its 2025 global growth forecast, with notable cuts for the US and China. The downward revision is tied to escalating trade tensions amid sharp US tariff hikes. The IMF currently sees further escalation in tariffs and trade tensions as the major risk, alongside the risk of further tightening in financial conditions.

In Sweden, the LFS unemployment was much stronger than expected, with the seasonally adjusted measure decreasing to 8.1% in March from 8.9% in February. Although the series tends to be extremely volatile the details reveal a solid set of numbers, with employment for the full quarter exceeding our forecasts, while the labour force developed as expected. Hence, the worst is clearly behind us in the labour market - unless the recent tariff and stock market turbulence alters the trajectory ahead.

In geopolitics, both Russia and Ukraine showed some progress toward a peace deal. The Financial Times reported that Putin had offered to halt Russia's invasion at the current front lines, while Zelenskiy stated that Ukraine was ready for talks with Russia once a ceasefire was in place.

In commodities space, oil prices moved higher during yesterday's session, largely spurred by new US sanctions targeting Iranian oil exports and the sentiment improvement following Trump's softer tone on the Fed and Bessent's trade-war comments. Brent trades around 68 USD/bbl as of this morning.

Equities: Global equities moved higher yesterday in what largely appeared to be a reversal of Monday's price action. Equities were up, cyclicals outperformed defensives, and in the cross-asset space, we observed a similar dynamic with falling yields and a stronger dollar.

Although we had a fairly busy earnings calendar, neither the earnings nor the macro data released yesterday stood out in a particularly impressive manner. Once again, politics took centre stage. Notably, comments from US Treasury Secretary Scott Bessent seemed to calm markets and restore risk sentiment as he indicated de-escalation with China, describing the tariff standoff with Beijing as unsustainable. US equities yesterday: Dow +2.7%, S&P 500 +2.5%, Nasdaq +2.7% and Russell 2000 +2.7%. Looking at markets this morning, the positive tone continues with green prints across Asia and higher futures in both Europe and the US.

FI&FX: Markets showed some signs of relief after somewhat softer comments from Trump where he said he had no intention to fire J. Powell and gave some soft remarks with regards to the trade war with China. Today's PMI releases will be the first set of releases capturing 'liberation day' and are therefore expected to be on the weak side, which could be an important input for central banks.

FTSE Elliott Wave Update: Short-Term 5 Swing Pattern Favors Additional Gains

The FTSE index experienced a significant decline from its high on April 3, 2025, reaching a low of 7552.65. We identify this as the completion of wave II. This downturn followed a zigzag pattern, a common structure in Elliott Wave analysis. Starting from the April high, the decline unfolded in three phases: wave ((A)) dropped to 8481.1, wave ((B)) rebounded to 8742.75, and wave ((C)) fell further, structured as a five-wave impulse. Within wave ((C)), the sub-waves progressed as follows: wave (1) hit 8615.96, wave (2) recovered to 8717.03, wave (3) fell to 8023.45, wave (4) rose to 8123.27, and wave (5) concluded at 7547.69, finalizing wave ((C)) and wave II.

Since hitting this low, the FTSE has begun to recover. The ongoing rally from the wave II low is unfolding in a five-wave upward pattern, suggesting potential for further gains. So far, wave 1 of this rally peaked at 8021.77, and wave 2 pulled back to 7599.56. We anticipate wave 3 to push higher soon, followed by a wave 4 pullback, and then a final wave 5 to complete wave (1) of the broader upward move. In the short term, as long as the 7547.69 low holds, any dips are likely to attract buyers at key levels (often referred to as 3, 7, or 11 swings in Elliott Wave terms), supporting further upside.

FTSE 60 Minute Elliott Wave Chart

FTSE Video

https://www.youtube.com/watch?v=HgiZ3dlaIcY

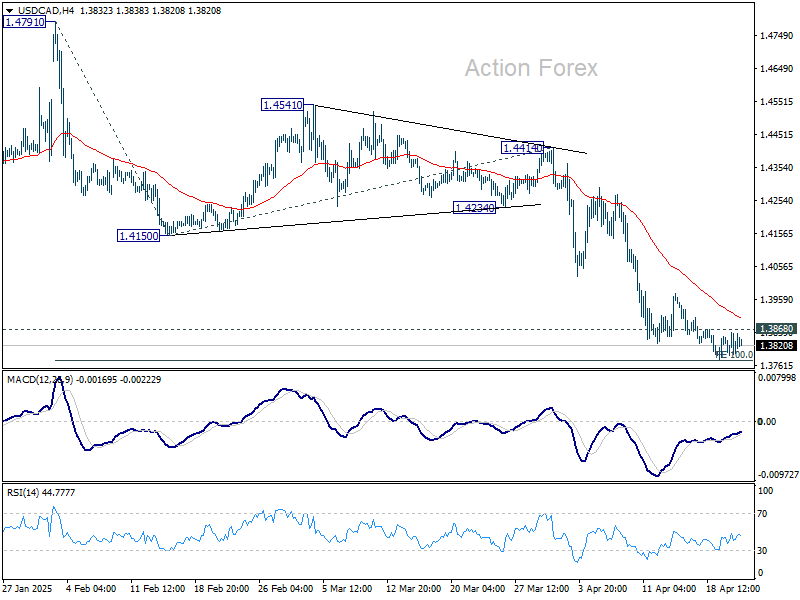

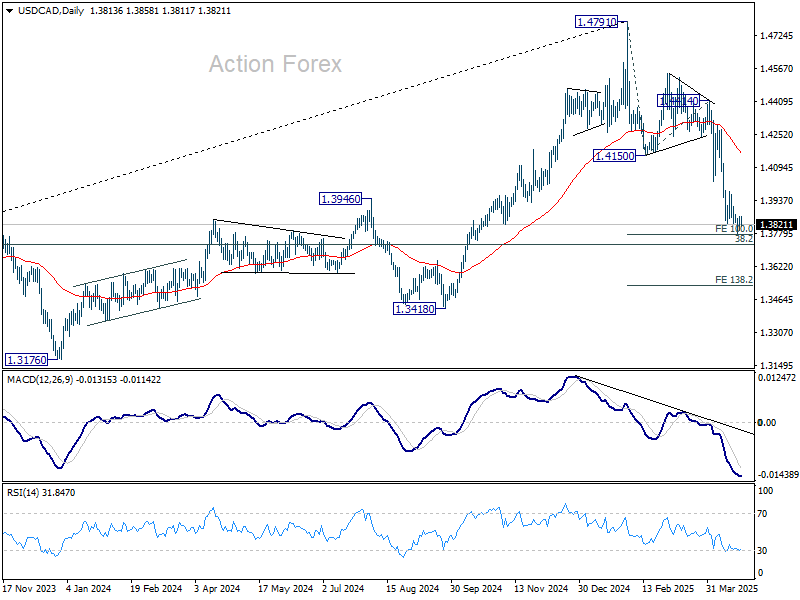

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3785; (P) 1.3823; (R1) 1.3854; More...

Further decline is in favor in USD/CAD with 1.3868 minor resistance intact. Firm break of 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773 will extend the decline from 1.4791 to 138.2% projection at 1.3528. On the upside, above 1.3868 minor resistance will turn intraday bias back to the upside for stronger recovery.

In the bigger picture, the break of 1.3976 resistance turned support (2022 high) and 55 W EMA (now at 1.3982) indicates that a medium term top is already in place at 1.4791. Fall from there would either be a correction to rise from 1.2005, or trend reversal. In either case, firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

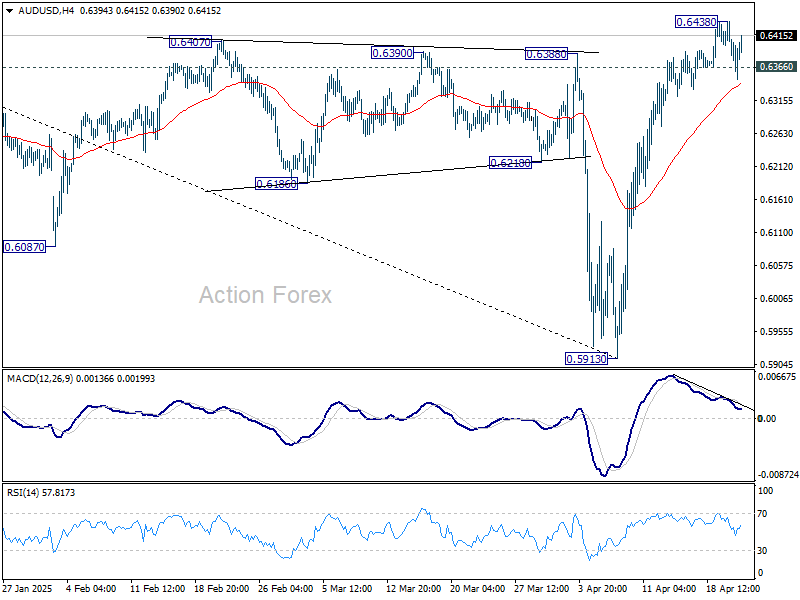

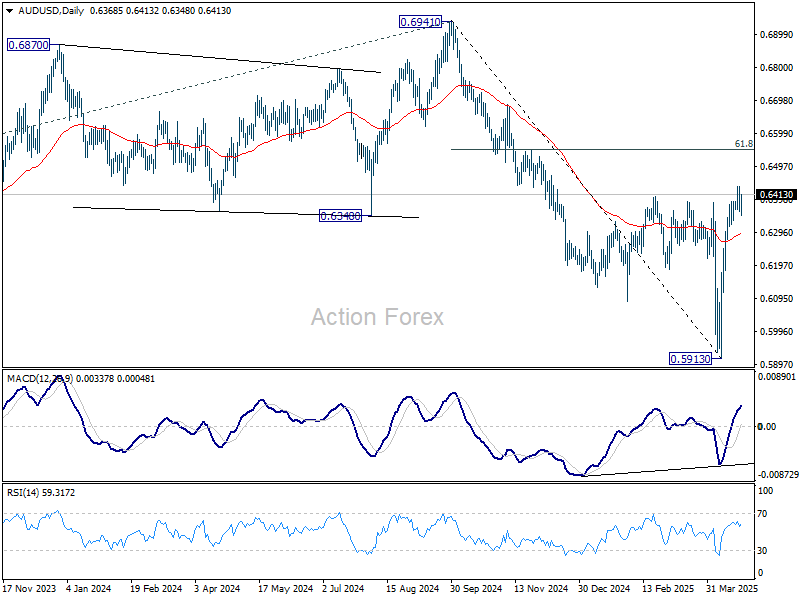

AUD/USD Daily Report

Daily Pivots: (S1) 0.6338; (P) 0.6389; (R1) 0.6416; More...

Intraday bias in AUD/USD is turned neutral first with breach of 0.6366 minor support. Some consolidations would be seen but further rally is expected as long as 55 D EMA (now at 0.6296) holds. Above 0.6438 temporary top will resume the rebound from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, sustained trading below 55 D EMA will argue that the rebound has completed and turn bias back to the downside.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA (now at 0.6443) will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

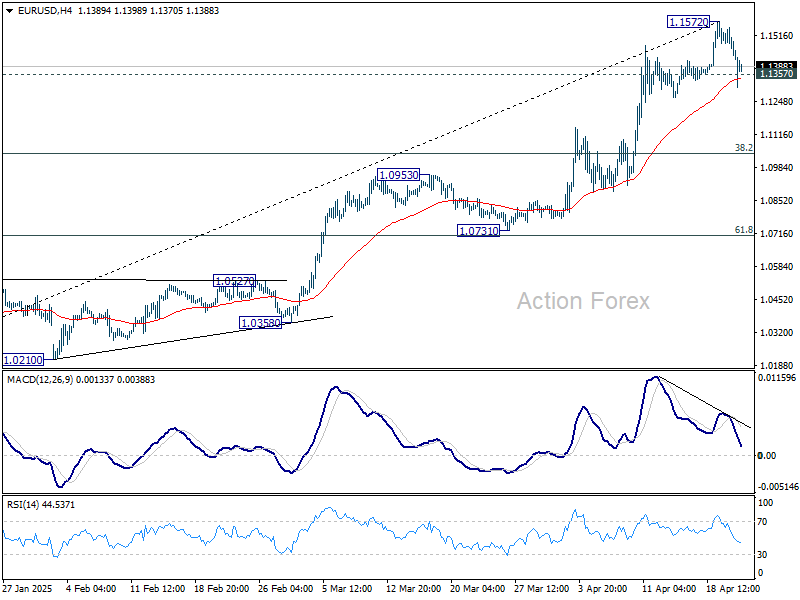

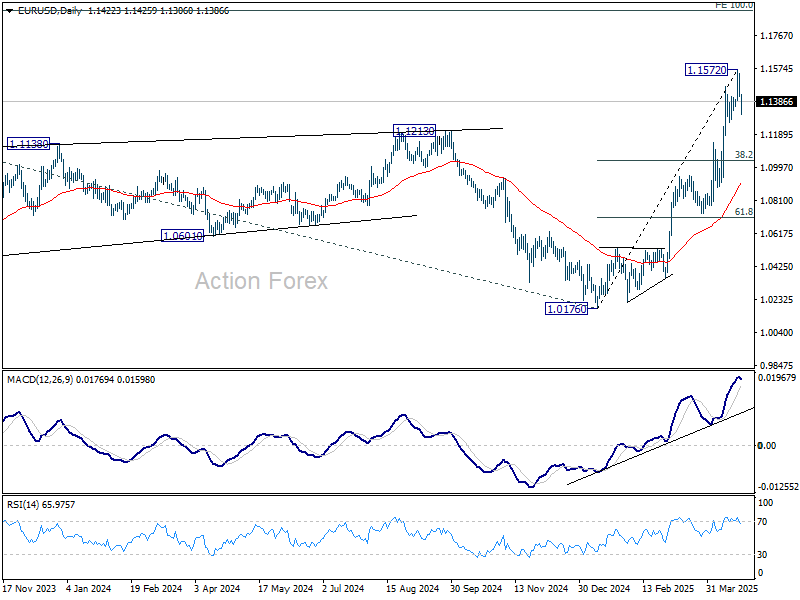

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1377; (P) 1.1462; (R1) 1.1507; More...

EUR/USD's breach of 11357 minor support suggests short term topping at 1.1572, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for deeper pullback. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1572 will resume larger up trend.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

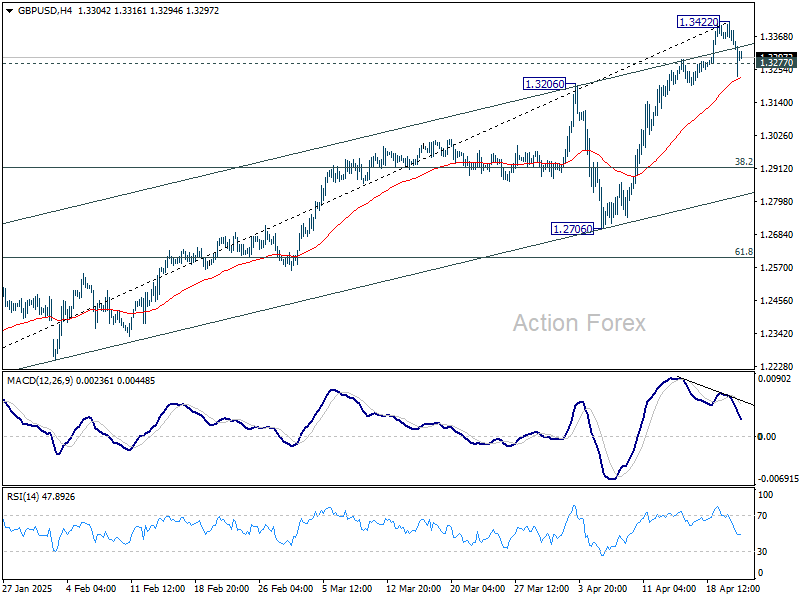

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3298; (P) 1.3360; (R1) 1.3395; More...

GBP/USD's breach of 1.3277 minor support suggests short term topping at 1.3422, on bearish divergence condition in 4H MACD, ahead of 1.3433 high. Intraday bias is turned to the downside for deeper pullback. But downside should be contained by 38.2% retracement of 1.2099 to 1.3422 at 1.2917. On the upside, firm break of 1.3433 will resume larger up trend.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.