Sample Category Title

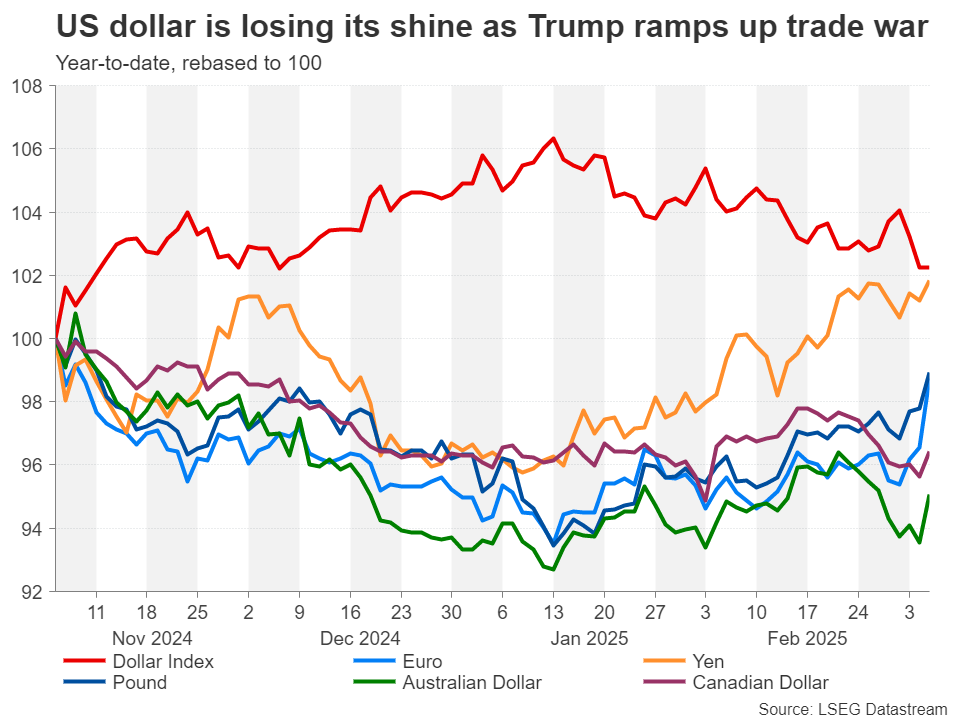

Dollar Loses Shine in Trade War as Investors Rethink Impact on US Economy

- Trade war gathers pace as Trump slaps tariffs on Canada, Mexico and China.

- But US dollar starts to wobble as cracks appear in US economy.

- Growing concerns about Trump’s policies also weigh on US outlook.

Not a bluff, as Trump proceeds with tariffs

US President Donald Trump went ahead this week with his pledge to implement 25% tariffs on goods entering America from its northern and southern borders, while adding another 10% to imports from China. Although the announcement wasn’t exactly out of the blue, investors had been hoping that a last-minute deal, at least with Canada and Mexico, would have averted the spike in tariffs with the United States’ biggest trading partners.

What is perhaps a more surprising development, however, is how the decision to proceed with the tariffs has changed investors’ perception about the implications of Trump’s trade war on the US economy.

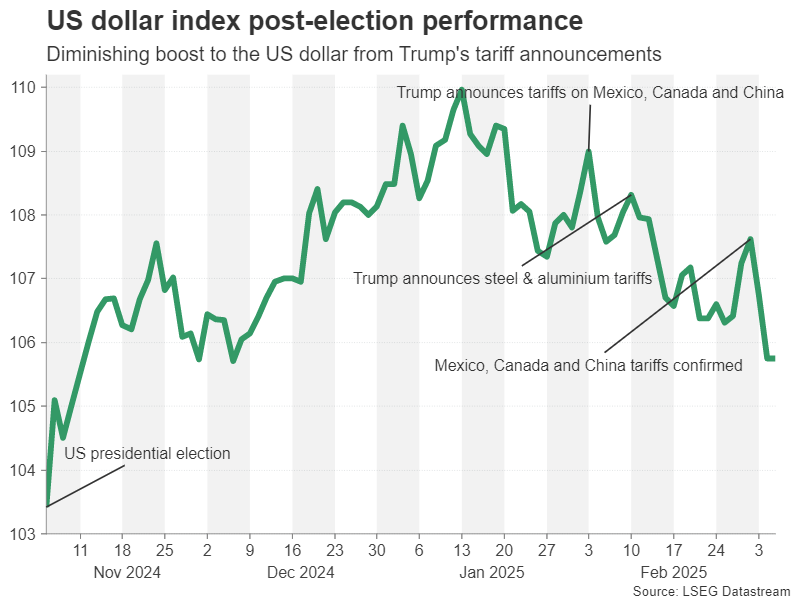

Dollar gives up post-election bounce

Following Trump’s resounding election victory in November, the US dollar rallied on the expectation that his pledge of higher tariffs would be inflationary, but that the impact on growth would be limited due to the boost from his promise of large tax cuts and deregulation. The former spurred a rally in the dollar, as investors pared back their rate cut bets for the Fed, while the latter kept risk appetite alive on Wall Street.

However, the optimism that America would be able to withstand Trade War II appears to have faded, partly because investors didn’t believe the White House would impose substantial tariffs on its allies, focusing mainly on China, and partly because the US economy is showing signs of cracks even before the full force of the tariffs has been felt.

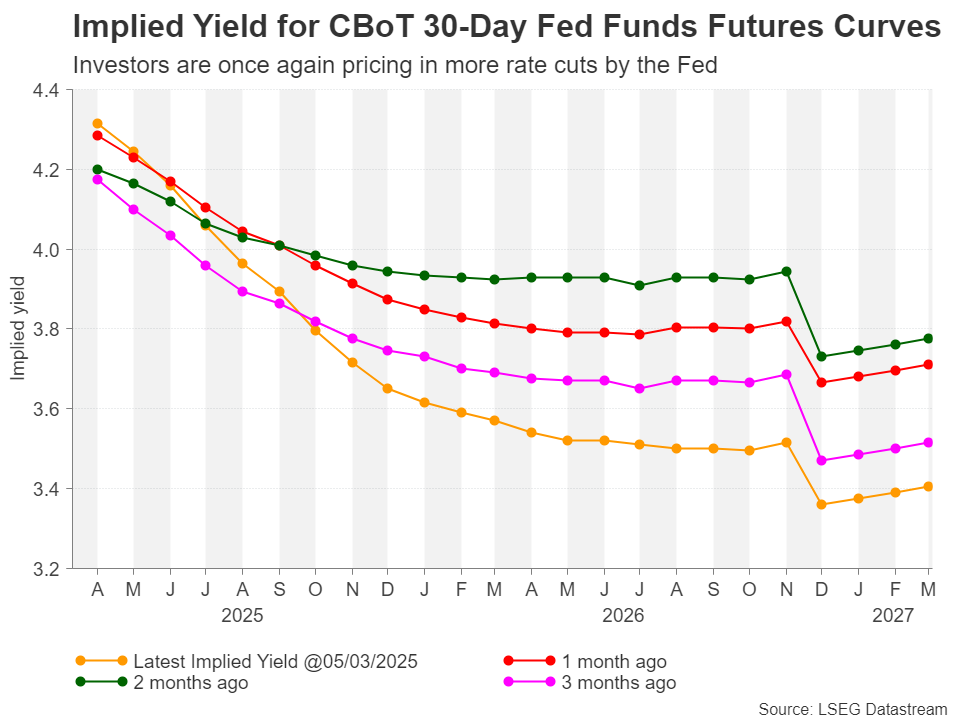

Fed rate cut bets ramped up as mood sours

Trump’s increasingly unpredictable nature has started to rattle markets, not just his stance on tariffs but also his positions on key foreign policy issues such as Ukraine. The destabilizing effect on world order of the current Trump administration is far greater than anything investors had seen during the President’s first term.

This is adding to the general anxiety both in the markets and among businesses. Combined with the uncertainty created about future costs by Trump’s constant wavering on tariffs, business sentiment is taking a knock.

Investors have already started to price in steeper rate cuts by the Federal Reserve this year, betting that economic worries will outweigh inflation ones for policymakers. Ultimately, the Fed will only prioritize growth over inflation if the labour market deteriorates. That hasn’t happened yet and so the Fed has strongly signalled it intends to stay on pause for the time being.

The end of US exceptionalism?

Nevertheless, the dollar has come under intense selling pressure following the confirmation by Trump that the 25% levies on Canada and Mexico are definitely ‘on’. What was different this time was the fact that Trump seems unwilling to negotiate or compromise, as also demonstrated in the talks with Ukraine’s President Zelensky. If he applies the same ‘take it or leave it’ approach with all the countries that are set to be targeted by the reciprocal tariffs due to come into effect on April 2, there will be little chance of finding a middle ground.

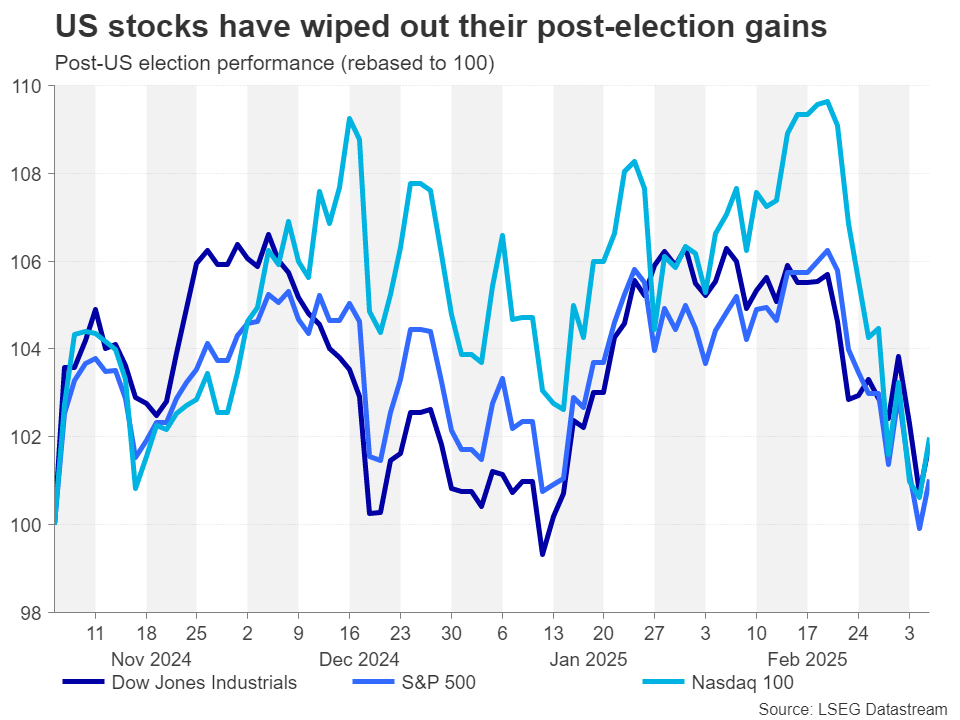

This potentially marks a turning point for American exceptionalism that was sustaining the strong dollar and Wall Street rally for such a long time. If what replaces it is US isolationism, the dollar could be facing a prolonged downtrend, while US equities could lose out to their international rivals. The S&P 500 has already erased its post-election rally and not even tech stocks are safe, as the Nasdaq is down the most year-to-date compared to both the Dow Jones and S&P 500. Of course, small caps have taken the biggest hit, with the Russell 2000 trading about 15% below its November all-time high.

Dollar rivals fight back

For the greenback, it doesn’t help that the yen is currently benefiting from a more hawkish Bank of Japan, while the euro got a shot in the arm by Germany’s decision to relax its self-imposed rule on borrowing. The pound is also holding its ground as the UK looks set to escape Trump’s tariffs, while the Australian and New Zealand dollars are being supported by China stepping up its stimulus measures to counter a more hostile Washington. Even the Canadian dollar has avoided a sharp selloff, as investors no longer see clear winners or losers in this trade war.

In the meantime, the traditional safe haven of gold has been attracting record inflows amid the heightened geopolitical risks and predictions about a US recession.

Will Trump back down?

For now, a full-blown recession in America seems unlikely, although it cannot be ruled out. Consumption appears to be waning and with mass government layoffs on the way thanks to Elon Musk’s DOGE, households may curtail their spending even more over the coming months. Reduced consumer spending and an increase in unemployment would likely trigger a strong response by the Fed.

However, it is possible that President Trump may yet do a U-turn on tariffs, especially if there’s a slump on Wall Street. The USMCA agreement, for example, is up for review in 2026. Trump may be laying the ground for tough talks with Mexico and Canada. In Europe, he has already won a major concession by forcing European nations to beef up their defence spending.

Uncertainty and stagflation cloud Dollar’s outlook

The problem, though, for the dollar and the US stock market is that even if Trump gets his way and the trade war de-escalates at some point in his presidency, the uncertainty generated by his style of leadership and radical policies is already wreaking havoc on business confidence and market sentiment.

This could all change once the Trump administration unveils its tax cut plans as well as announce measures to ease the regulatory burden. But hopes for a major boost are slowly dimming as it’s unclear whether the tax reductions and business-friendlier regulation will substantially offset the massive cuts to spending that are on Republicans’ agenda.

What is even less certain, however, is whether any slowdown in the economy will significantly dampen inflationary pressures to allow the Fed to cut rates as aggressively as the markets are currently pricing in. Any disappointment on this front could pave the way for a potential bounce back in the US dollar, although the scope for a rebound in a stagflationary environment is probably quite modest.

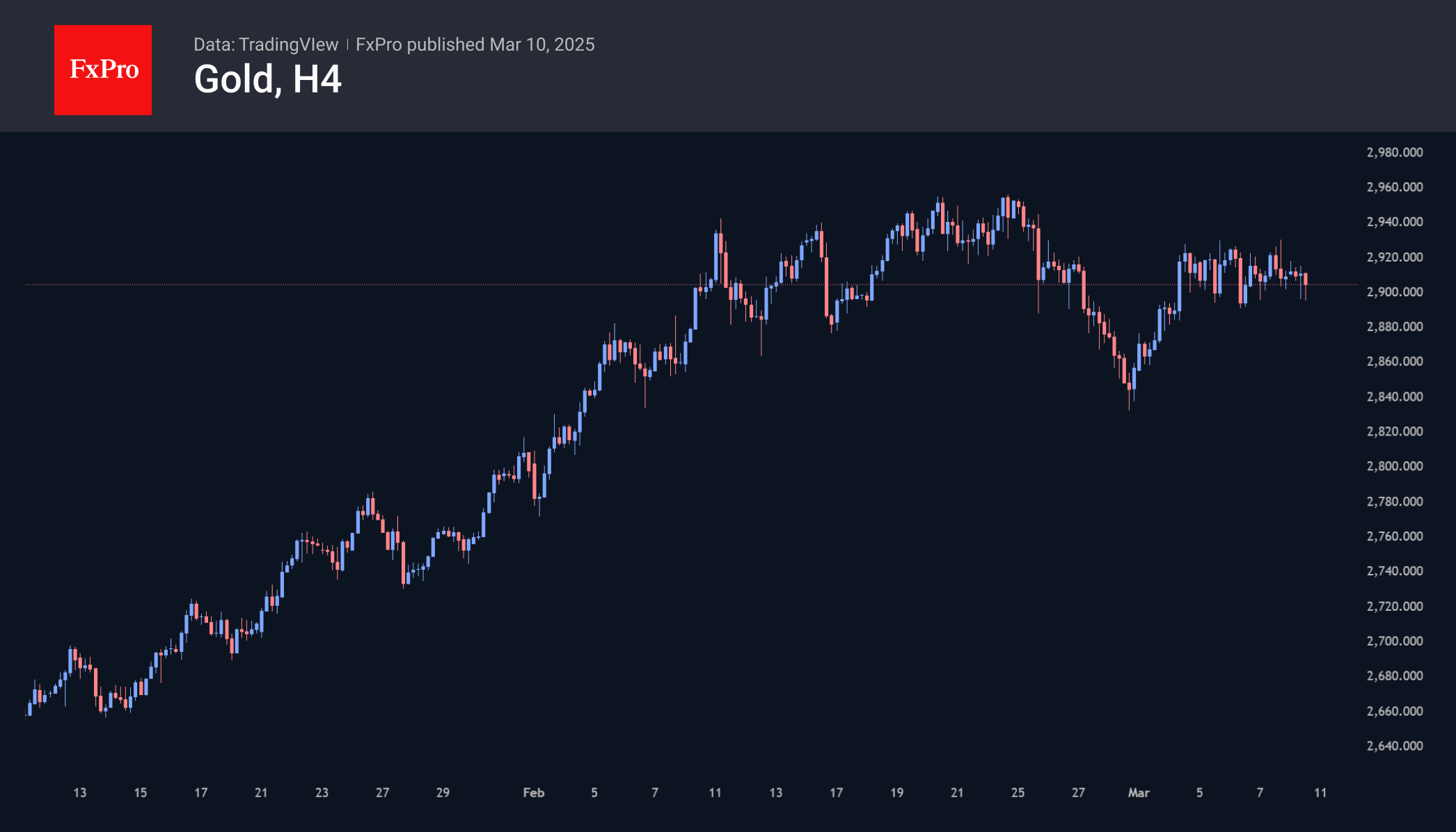

Gold Traders Weighting the Next Move

Since early March, the gold price has reversed to the upside, regularly exceeding the $2900 mark during the week. The cautious trading tone of the US indices works on the side of the bears, while the weakness of the dollar infuses confidence in the bulls.

On the tech analysis side, the dip at the end of last month now looks like a corrective pullback from the rally from the beginning of the year. If this is the case, overcoming the highs above $2950 opens the way to $3180. Gold bulls should still look at the sentiment around US equities. Further declines could switch the market into global deleveraging mode, and gold will initially have a tough time.

Sunset Market Commentary

Markets

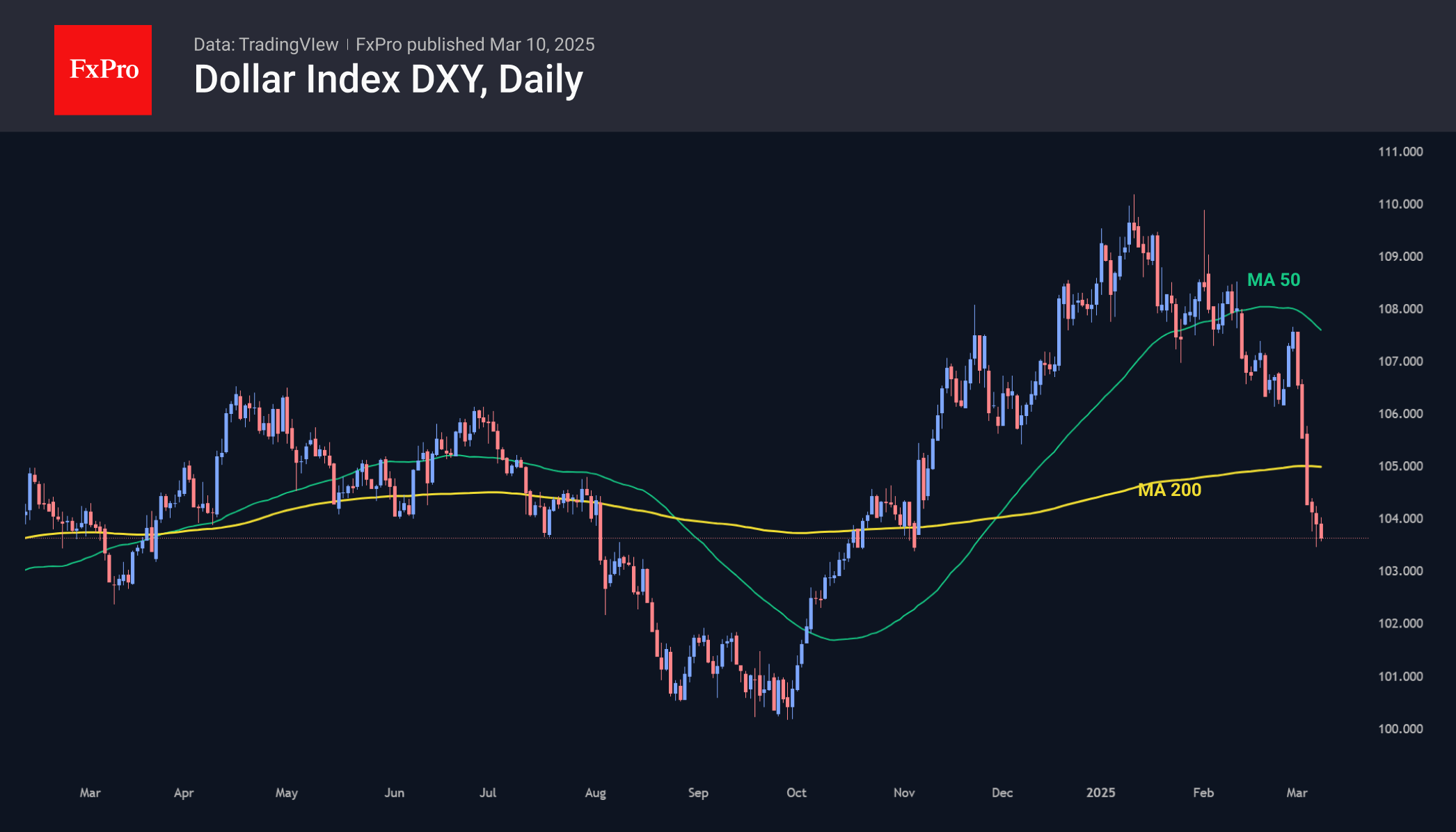

Odds this morning were for markets to take a slow start to the new trading week after last week’s sharp (divergent) repositioning on both sides of the Atlantic. Fed Chair Powell on Friday in a ‘last-minute’ assessment before the black-out period in the run-up to the March 19 Fed meeting, kept a wait-and-see-approach. Powell still sees the US economy as holding fairly robust and doesn’t get carried away by a limited number of (perceived) weaker than expected data. Maybe there was room for US yields to look for a bottom after markets raised Fed rate cut bets to a cumulative 75 bps this year from just one 25 bps step about one month ago. Still, with little in the way of hard US eco or political news, US markets today still are governed by the forces of gravity with yields, US equities and even the dollar printing in red. Recessionary fears don’t subside. US yields again are declining up to 10 bps (5-y) with the belly outperforming the wings. Recent lows (3.84% 2-y; 4.10% 10-y) are surviving, but stay within reach. Markets clearly aren’t convinced that the US economy is only going through a transition period as president Trump indicated in a Fox interview this weekend. US equities also are again ceding up to 3.0%+ (Nasdaq). The US tech index is (at risk of) falling below the 17817 level (23% retracement 2022/2024 upleg), a genuine technical warning. German yields are slightly off last week’s peak levels after the country made a U-turn to an outright defensive-driven fiscal stimulus. The German Green Party, which doesn’t take part in the CDU/CSU-SPD talks to form a government but is necessary to approve the constitutional amendment of the debt brake, today indicated that it rejects the spending package from the ‘upcoming’ coalition. The Greens want a ‘real’ reform of the debt break. The new collation partners and the Greens are said to hold talks later today. Maybe, the ‘risk’ is for the additional priorities of the Green party to be included in the ‘debt-brake package’. German bunds clearly underperform US Treasuries with yields easing between 4.0 bps (5-y) and 1.0 bps (30-y). The Eurostoxx 50 is ‘only’ losing about 1.5 %. As was the case of late, the dollar clearly isn’t able to reclaim its (previous) safe haven status. DXY declines marginally (103.82). EUR/USD is holding last week’s gain (1.0835). The yen continues its outperformance with USD/JPY drifting below the 147 big figure. Brent oil still struggles near $70 p/b.

News & Views

The German seasonally-adjusted trade surplus declined from €20.7bn in December to €16bn in January. German exports fell by 2.5% M/M to €129.2bn (-0.1% Y/Y) with imports rising by 1.2% M/M to €113.1bn (+8.7% Y/Y). Exports of goods to countries outside of the EU amounted to €59.4bn, most of which was sent to the US (-4.2% M/M to €13bn). Imports from the US rose by 6.5% M/M to €8bn. Most imports from outside the EU came from China (-2.8% M/M to €12.9bn vs €6.7bn exports to China). Other data series showed German industrial production rising by 2% M/M in January, to be down 1.6% Y/Y. The strong start to the year erased a weak ending with the less volatile 3M/3M comparison showing the production in the period from November 2024 to January 2025 was at the level of the previous three months (0.0%). Significant production growth in the automotive sector together with increases in the food industry and in machine maintenance and assembly outweighed lower production in the manufacture of fabricated metal products. Core industrial production, excluding energy and construction was up 2.6% M/M with intermediate goods production rising by 3.3%. The production data need to be combined with a staggering 7% drop in January factory orders, published last week and a 2.5% M/M decrease in the truck toll mileage index for February (to 93.2, the second lowest level since the pandemic). It’s a combination of frontrunning tariffs and pre-election uncertainty. Last week’s events suggests that the German industrial sector could be ready for a debt-funded revival.

Norwegian inflation outpaced expectations in February, rising by 1.4% M/M (vs 0.5% expected) to 3.6% Y/Y (vs 2.6% and from 2.3%). Underlying core inflation beat consensus by a wide margin as well, accelerating to 1% M/M and 3.4% Y/Y. Elevated price pressure is a setback for the Norges Bank who prepared markets for a first policy rate cut later this month. Norwegian money market believe that a pullback is possible, discounting only 50% probability to such action with only 1 full rate cut discounted by the end of the year compared with Norges Bank guidance of three such moves. The Norwegian krone roars back today with EUR/NOK dropping from 11.80 to 11.67 and on its way to test the strong EUR/NOK 11.52/60 support zone.

Surging Yen Hits 5-Month High, Wage Data Mixed

The Japanese yen has started the week with strong gains. In the European session, USD/JPY is trading at 147.07, down 0.766 on the day. Earlier, the yen strengthened to 146.72, its best level since Oct. 4, 2024.

Japan’s real wages fall 1.8% in January

Japan’s wage data for January was mixed. Base pay for Japanese workers jumped by 3.1% y/y but more importantly, inflation-adjusted real wages declined by 1.8%. This follows two consecutive months of gains and signals that inflation has outpaced growth.

The wage report was released just days before the end of annual wage negotiations at Japan’s largest companies. The largest labor union in Japan is demanding large wage hike of 6% and the Bank of Japan wants to see a strong rise in wages in order to keep inflation sustainable at the 2% level.

The BoJ has urged companies and workers to reach a deal that significantly raises wages. The central back meets next week and is widely expected to keep interest rates unchanged. Still, the Bank has signaled it plans to continue raising rates during the year.

US nonfarm payrolls edge higher

In the US, nonfarm payrolls rose to 151 thousand in February, up from a downwardly revised 125 thousand in January but shy of the market estimate of 160 thousand. The unemployment rate rose to 4.1% from 4%. Wage growth eased to 0.3% m/m from a revised 0.4% in January, in line with expectations. Annualized, wages ticked higher to 4%, up from a revised 3.9% in January but below the market estimate of 4.1%.

The employment report was decent but the threat of US tariffs continues to cloud the economic outlook. If trade tensions escalate, the Federal Reserve may have to adjust its rate path, depending on how tariffs affect inflation and growth.

USD/JPY Technical

- USD/JPY has pushed below support at 147.26 and is testing support t 147.26. Next is support at 1.46.48

- 148.51 and 148.98 are the next resistance lines

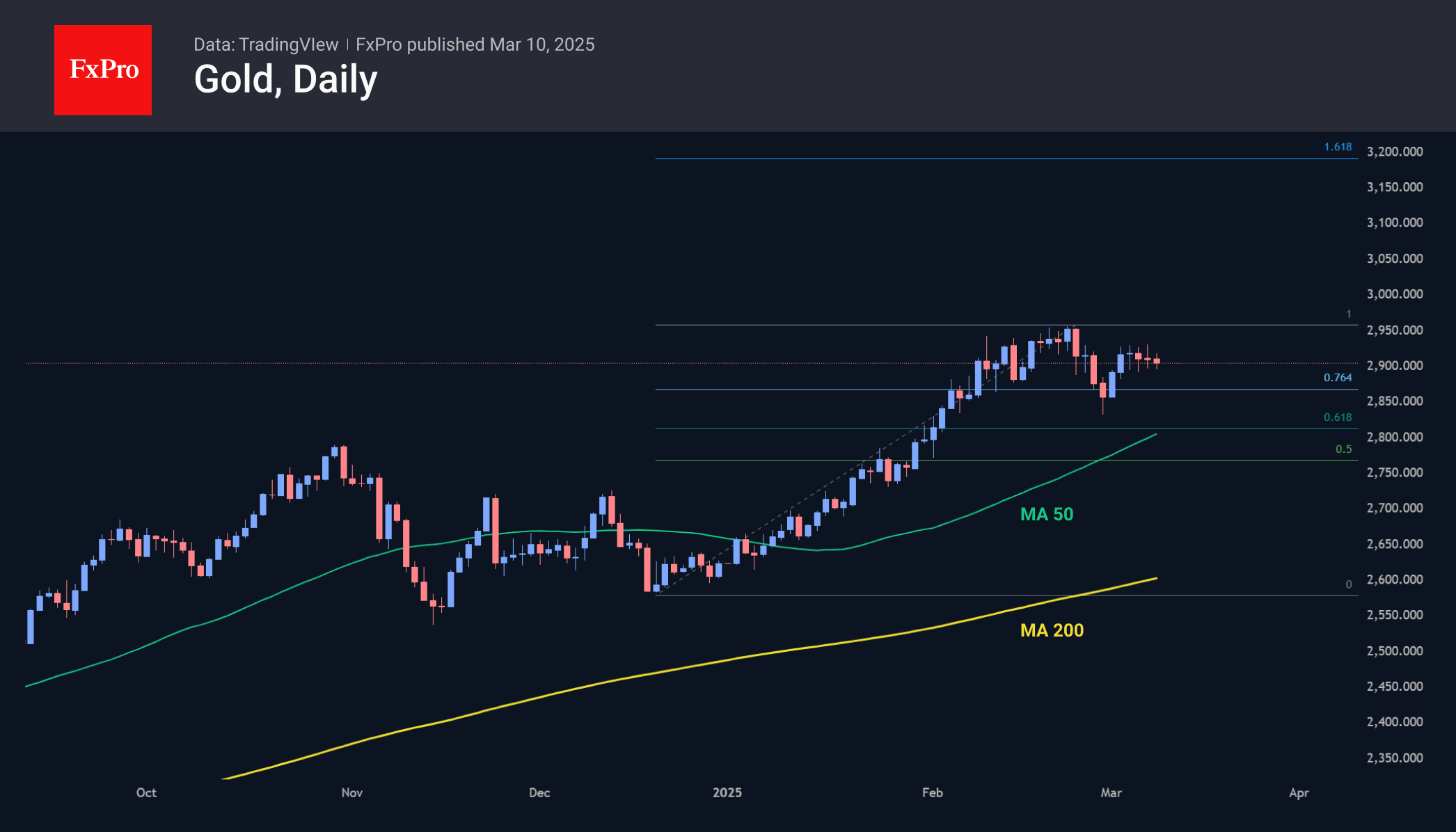

Dollar’s Plunge Accelerated on Easier FOMC Prospects

The dollar plunged rapidly last week, losing over 3.5% and pulling back to levels below 104.0, nearly erasing gains since Trump’s election victory.

The US dollar has been actively declining since early February and intensified the decline at the start of this month. An attempt to climb above the 50-day average at the end of February was met with intensified selling, and this week, the price has already pulled back below the 200-day.

A popular explanation is that the dollar is suffering because of Trump’s tariffs. It is correct to call the dollar’s decline a reassessment of expectations for the US Fed key rate.

The odds of two or more key rate cuts before the end of the year exceed 90% vs. 48% two weeks earlier.

A big EU defence spending plan and a dramatic shift in budget planning approaches in Germany lead to lower expectations for a key rate cut.

This news has caused the single currency to rally against most of its peers, most notably in the pairing with the dollar, where we have seen a 4.5% rally since the start of the week.

Higher-than-expected inflation in Japan is also setting the stage for a key rate hike, perhaps as early as March 19th. In other words, the gap in monetary policy is closing rapidly on both sides.

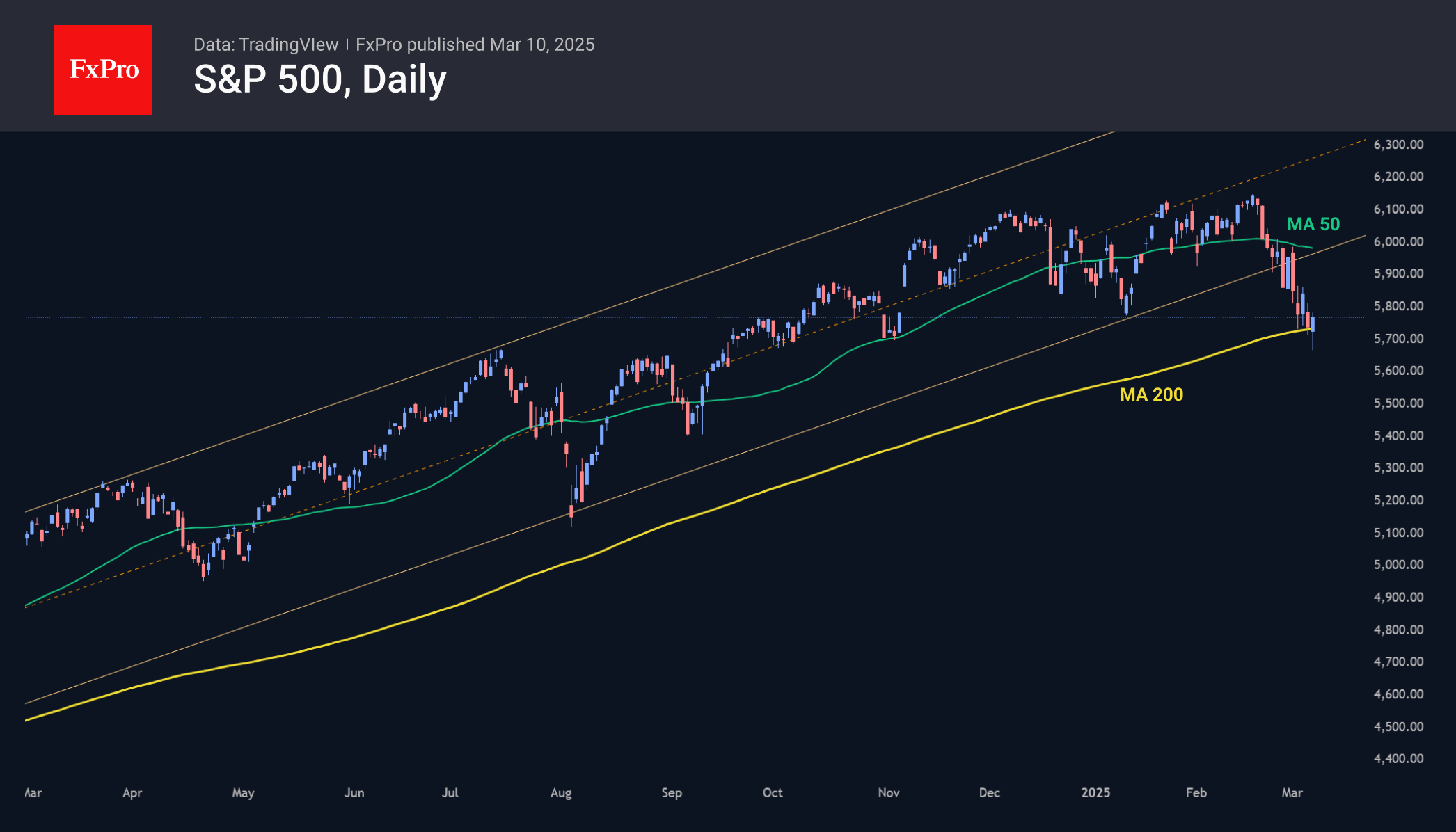

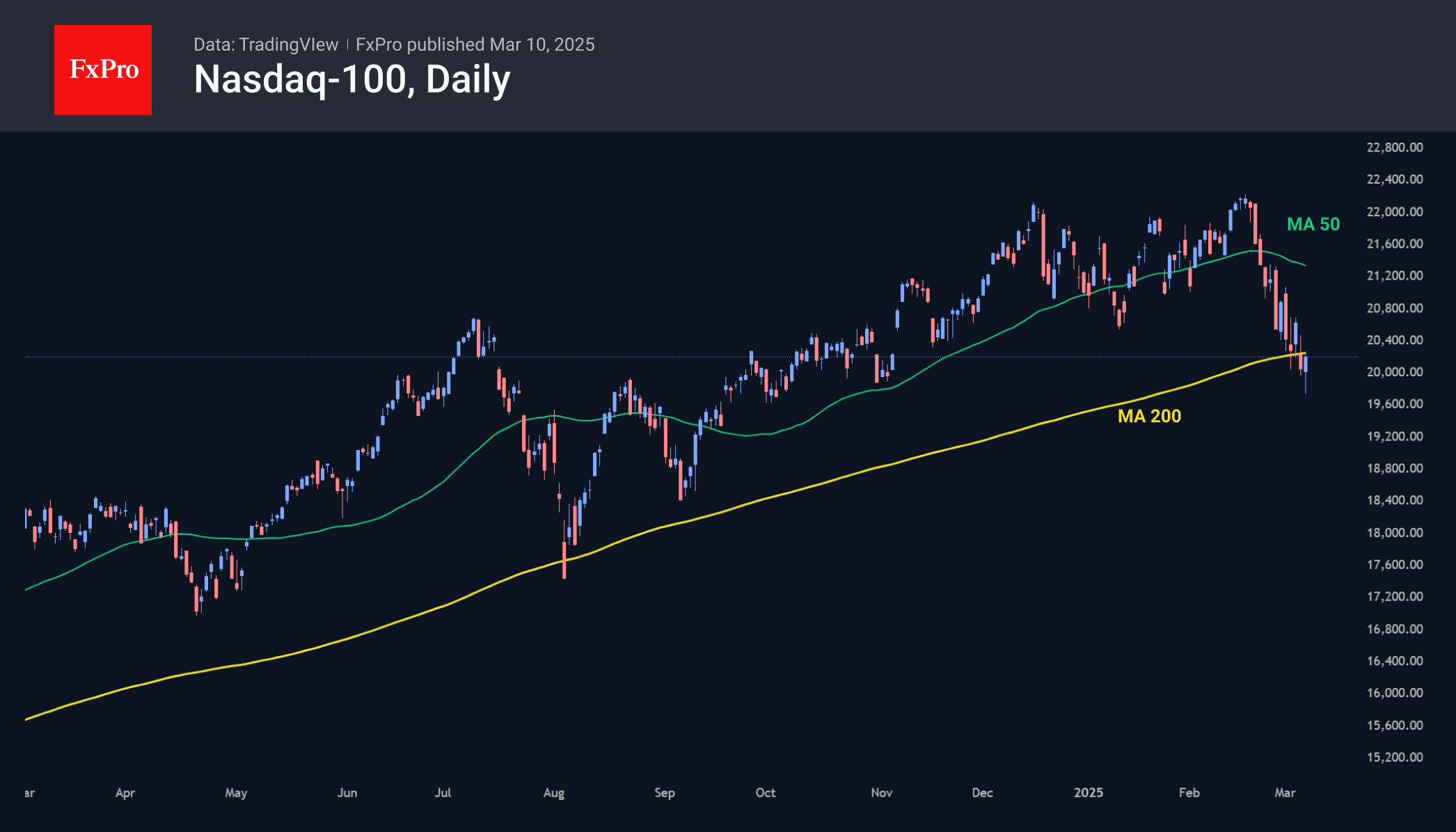

US Indices Desperately Cling to the 200-day MA

US indices declined in unison with the dollar, although they usually go in the opposite direction. But not all is terrible.

The S&P500 and Nasdaq100 indices were getting support on declines towards the 200-day moving average. That’s a long-term trend signal line for many of the big players. A failure below it could mean a regime change for stocks from ‘buying dips’ to ‘selling highs.’

The S&P500 has already broken a year-and-a-half upward trend and settled dangerously at levels just above 5700, testing buyers’ resolve almost daily. A failure of this support would activate an accelerated downside scenario into the 5200-5300 area.

For the Nasdaq100, which is now near 20000, a sustained move lower may not have meaningful headwinds until 18000. The beginning of recovery from this area will allow us to talk about the start of a new impulse with the potential to renew historical highs, as the accumulated oversold is whetting investors’ appetite.

It is a completely different story in Europe, where the German DAX40 continued to rewrite historical highs at its peak, showing an 18% increase since the beginning of the year. The new government’s plans to spend money on stimulus, setting aside self-imposed constraints in the form of budget deficits and debt-to-GDP ratios, sparked a sell-off in bonds. But this sell-off is in anticipation of a larger supply of government debt, not because of fears about Germany’s solvency. We are seeing a flow of money into euros and equities, not a flight from the region like during the Greek crisis.

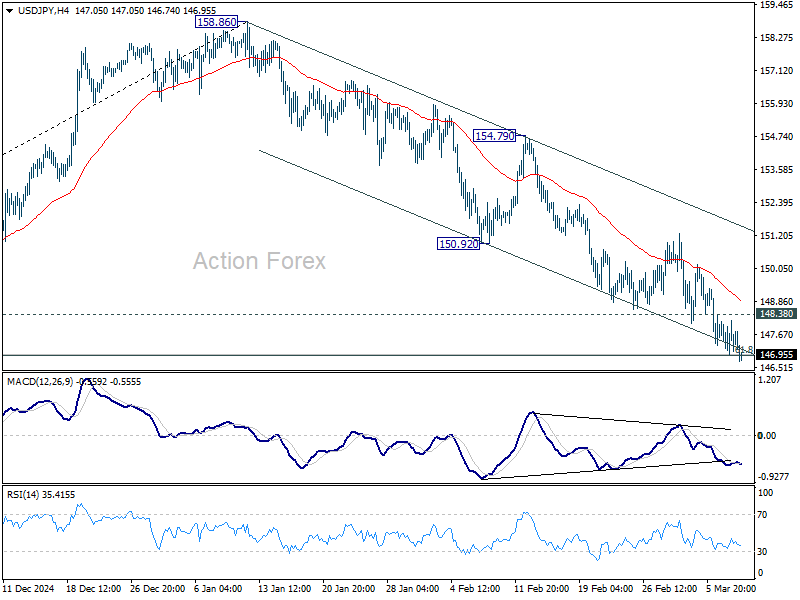

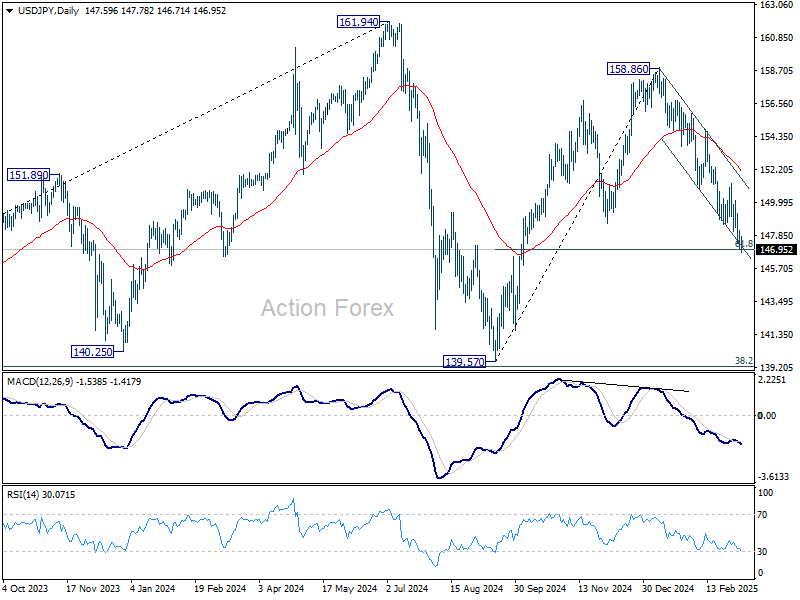

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.26; (P) 147.73; (R1) 148.51; More...

No change in USD/JPY's outlook and intraday bias stays on the downside. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way to 139.57 support. On the upside, 148.38 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

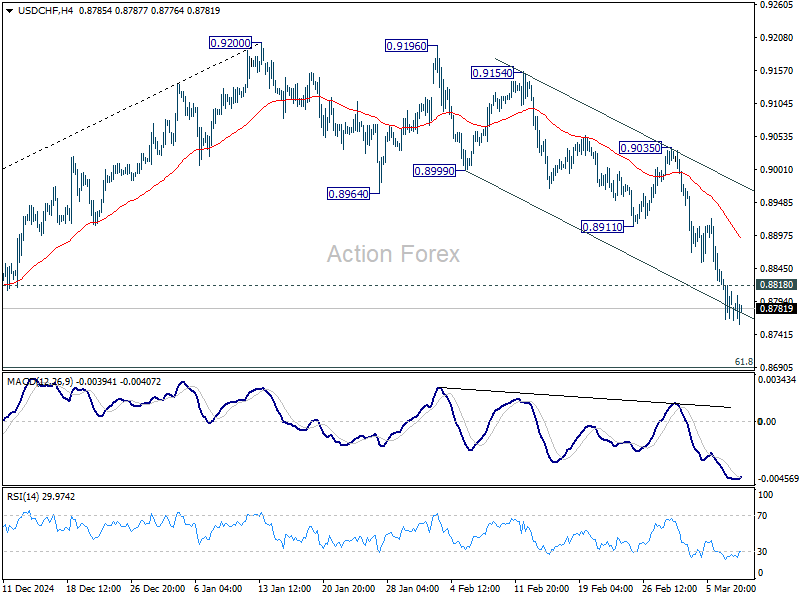

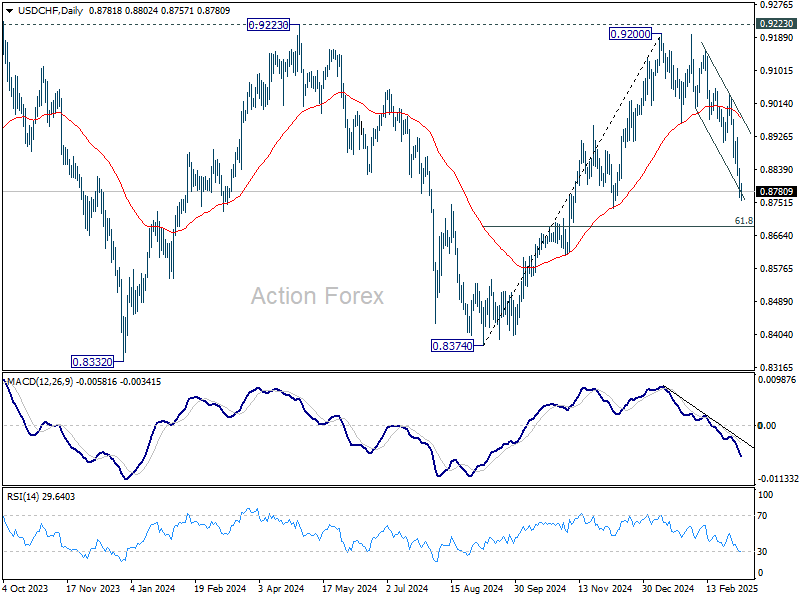

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8759; (P) 0.8809; (R1) 0.8850; More…

USD/CHF's decline from 0.9200 is still in progress and intraday bias stays on the downside. Next target is 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support. On the upside, above 0.8818 minor resistance will turn intraday bias neutral and bring consolidations, before staging another fall.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

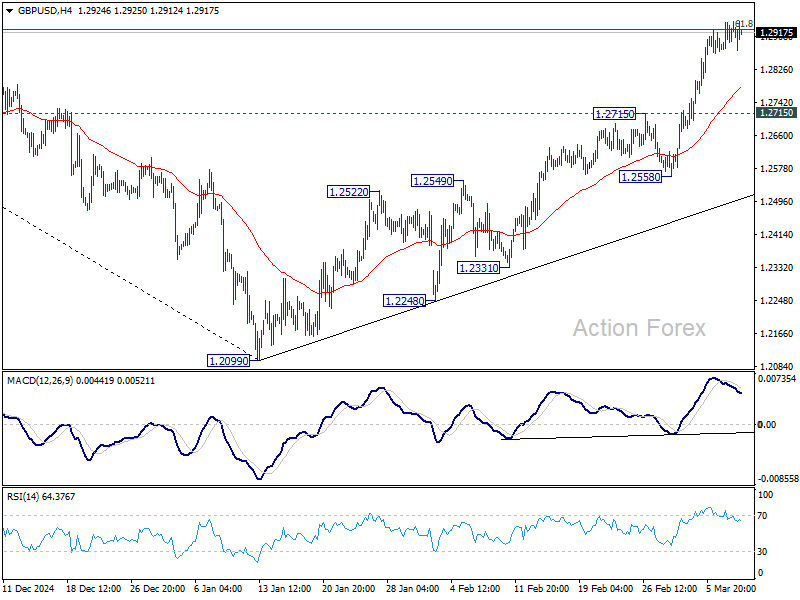

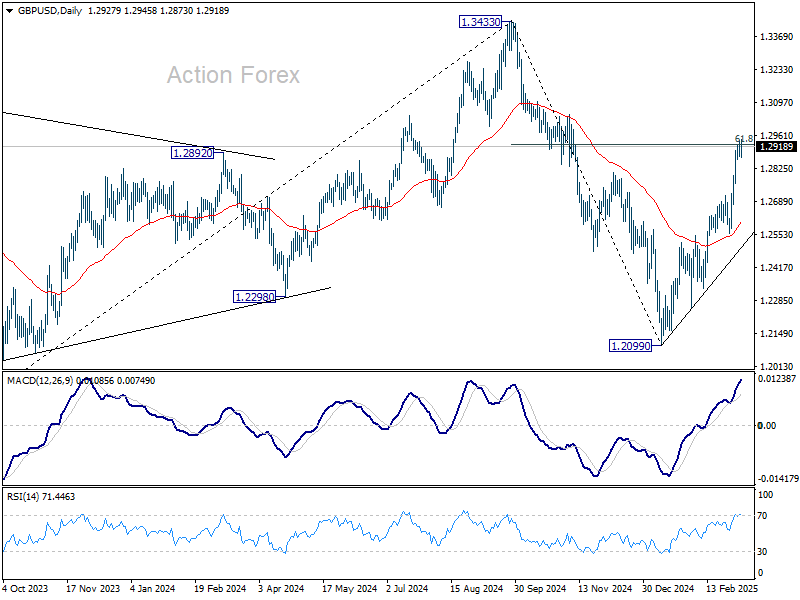

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2879; (P) 1.2912; (R1) 1.2953; More...

Intraday bias in GBP/USD remains neutral for the moment. Some consolidations could be seen first, but downside should be contained by 1.2715 resistance turned support to bring another rally. On the upside, sustained break of 61.8% retracement of 1.3433 to 1.2099 at 1.2923 will pave the way back to 1.3433 high.

In the bigger picture, fall from 1.3433 (2024 high) should have completed at 1.2099 as a corrective move. Up trend from 1.3051 (2022 low) is still in progress but it's too early to say that it's resuming. Corrective pattern from 1.3433 could extend with one more down leg. But after all, eventual upside breakout is expected at a later stage.

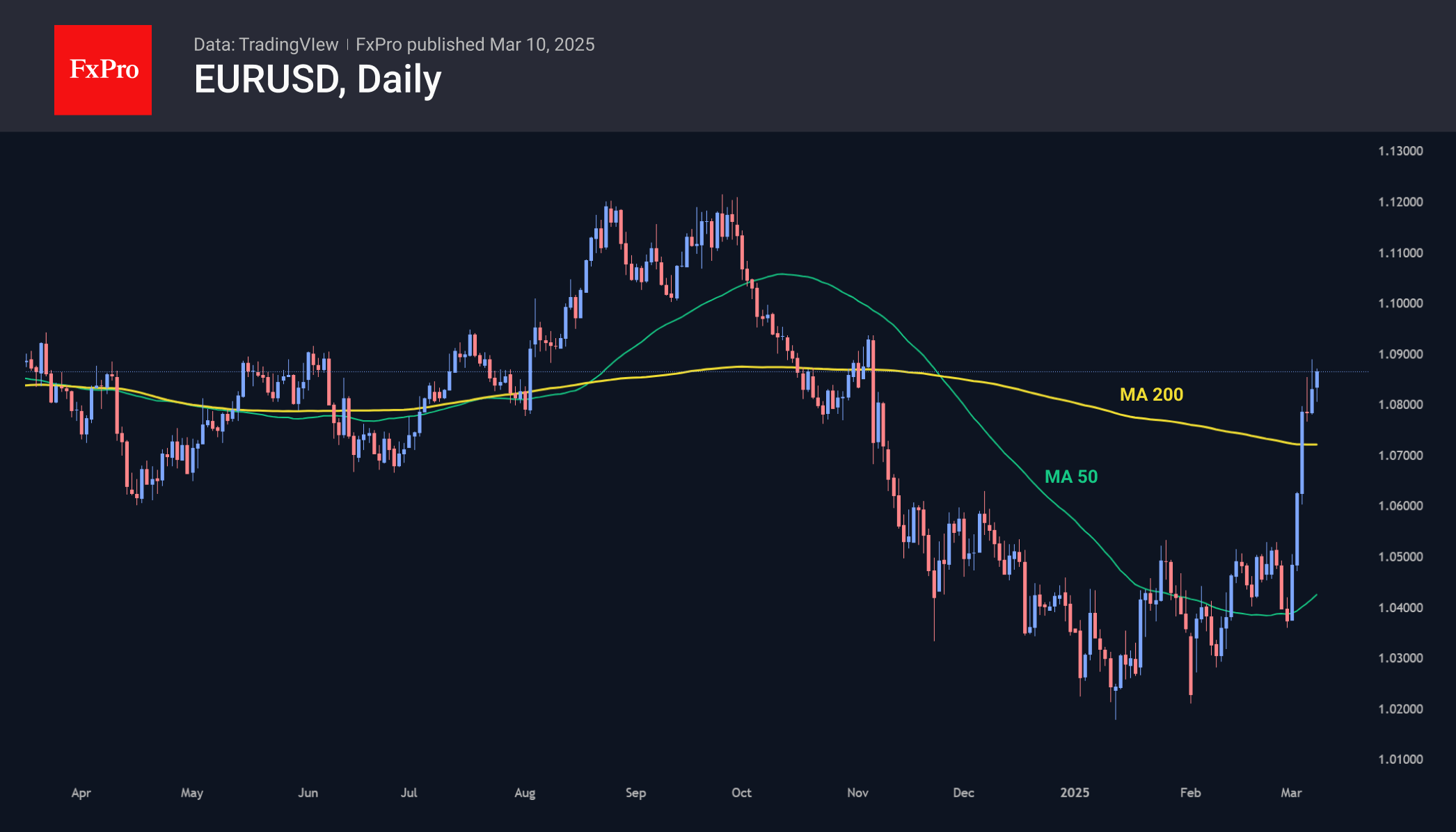

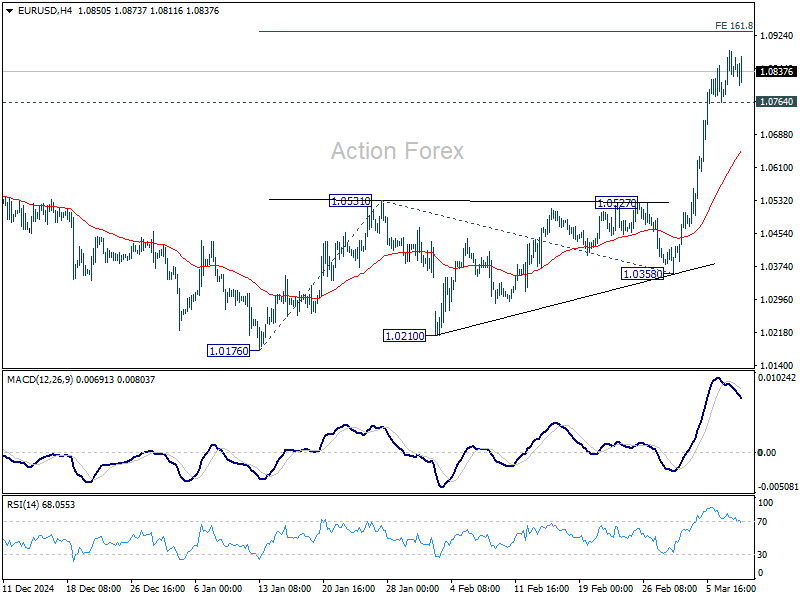

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0780; (P) 1.0834; (R1) 1.0888; More...

While further rise could be seen in EUR/USD, loss of momentum as seen in 4H MACD could limit upside to bring retreat. On the downside, break of 1.0764 minor support will with bias neutral for consolidations first, before staging another rally. Nevertheless, firm break of 1.0932 will pave the way back to 1.1274 key resistance next.

In the bigger picture, the strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.