Sample Category Title

Sterling Surges on Brexit Optimism Again, Breaking Key Resistance Level

Sterling trades notably high against Dollar and Yen today on more optimism over Brexit. GBP/USD reaches as high as 1.3942 so far and looks set to take out 1.3835 key resistance decisively. That would carry long term bullish implications. But for now, Euro and Swiss Franc are trading as the strongest ones for today. There is no change in Dollar's fate for the moment as its rebound again lacks follow through momentum. The greenback is weighed down by talks of global diversifications away from Dollar assets, including China and others. And Euro is an important destination of the funds.

US initial jobless claims dropped -41k to 220k in the week ended January 13, well below expectation of 251k. That's also the lowest level in 45 years since 1973. Continuing claims rose 76k to 1.95m in the week ended January 6. Housing starts dropped to 1.19m annualized rate in December while building permits was unchanged at 1.30m. Philly Fed survey dropped to 22.2 in January.

Brexit bill passed in House of Commons

The latest leg in the Pound's rally is triggered by the approval of the Brexit bill in the House of Commons. The bill aims to incorporate European Law into British Law to ensure a smooth transition. The bill was approved by 324 to 295 votes. The bill will now be passed to the House of Lords. While debates there could be fierce, it's still highly likely for the bill to get enough support.

Improving prospect of a post-Brexit trade deal is expected to boost investments and hiring in UK. But at this point, it's generally believed that BoE is not ready to raise interest rates again. According to a Reuters poll, all 75 economists surveyed expect BoE to keep the bank rate unchanged at 0.50% at the meeting on February 8. The next move is generally expected to happen in Q4.

SPD to vote on coalition this Sunday

In Eurozone, all eyes will be on Germany this weekend. The Social Democrats (SPD) are expected to vote on coalition with Chancellor Angela Merkel's CDU/CSU this Sunday. For now, opinions among SPD members appear to be split, with two regional branches already said they do not back the grand coalition.

SPD leader Martin Schulz urged the members in a facebook live broadcast that "we live in a world of dictators who make the world's breath pause with their crazed ideas ... And we have the chance to make Europe a bit more social, peaceful and just." But there is political reality for SPD to consider. According to Forsa poll, support for SPD slipped to 18%, and that's something the party have to face.

Australia job growth extends record streak

Australian job growth remained strong with 34.7k expansion in December. That's more than double of market expectation of 15.2k. That's the 15th straight month of expansion, the longest streak since 1993. And the more encouraging part is that full time jobs rose by 322k since December 2016, making up the majority of the 393k growth. Unemployment rate rose to 5.5% but that's due to a jump in participation rate at 65.7%. For the moment, markets are only pricing in 50/50 chance of an RBA rate hike by August. Also from Australia, consumer inflation expectation rose 3.7% in January.

Elsewhere

China GDP grew 6.8% yoy in Q4, above expectation of 6.7% yoy. Retail sales rose 9.4% yoy in December, below expectation of 10.2% yoy. Industrial production rose 6.2% yoy, beat expectation of 6.1% yoy. Fixed assets investment rose 7.2% yoy, above expectation of 7.1% yoy.

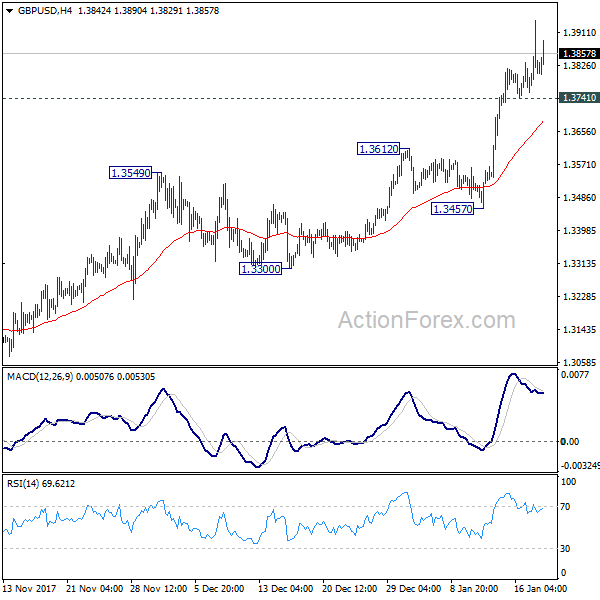

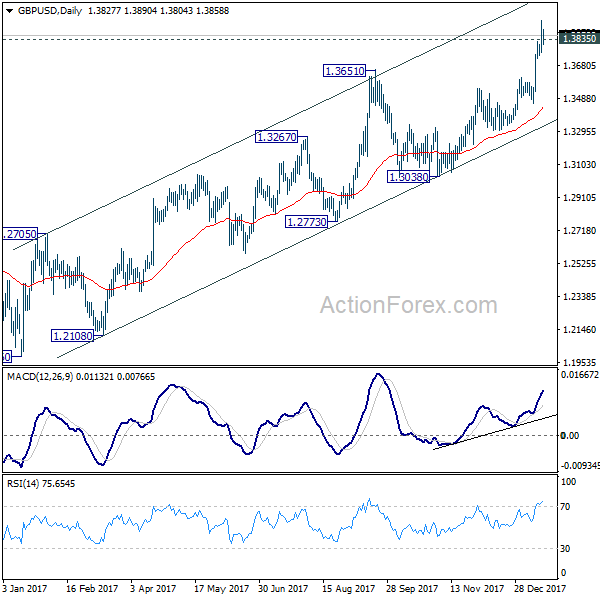

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3741; (P) 1.3841; (R1) 1.3927; More.....

GBP/USD's rally is trying to regain momentum above 1.3835 key resistance level. Intraday bias is mildly on the upside at this point. Sustained trading above 1.3835 will carry larger bullish implication and should target long term fibonacci level at 1.5466 next. On the downside, though, break of 1.3741 minor support will indicate rejection from 1.3835 and turn bias to the downside for 1.3457.

In the bigger picture, sustained break of 1.3835 key resistance level will indicate that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. In that case, further rise should be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Nonetheless, rejection from 1.3835 will maintain medium term bearishness and thus, the risk retesting 1.1946 ahead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | Consumer Inflation Expectation Jan | 3.70% | 3.70% | ||

| 00:01 | GBP | RICS House Price Balance Dec | 0.00% | -1.00% | 0.00% | |

| 00:30 | AUD | Employment Change Dec | 34.7K | 15.2K | 61.6K | 63.6K |

| 00:30 | AUD | Unemployment Rate Dec | 5.50% | 5.40% | 5.40% | |

| 04:30 | JPY | Industrial Production M/M Nov F | 0.50% | 0.60% | 0.60% | |

| 07:00 | CNY | GDP Y/Y Q4 | 6.80% | 6.70% | 6.80% | |

| 07:00 | CNY | Retail Sales Y/Y Dec | 9.40% | 10.20% | 10.20% | |

| 07:00 | CNY | Industrial Production Y/Y Dec | 6.20% | 6.10% | 6.10% | |

| 07:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Dec | 7.20% | 7.10% | 7.20% | |

| 13:30 | CAD | ADP Employment Dec | -7.1K | 59.2K | ||

| 13:30 | USD | Housing Starts Dec | 1.19M | 1.27M | 1.30M | |

| 13:30 | USD | Building Permits Dec | 1.30M | 1.29M | 1.30M | |

| 13:30 | USD | Philadelphia Fed Business Outlook Jan | 22.2 | 24 | 26.2 | |

| 13:30 | USD | Initial Jobless Claims (JAN 13) | 220K | 251K | 261K | |

| 15:30 | USD | Natural Gas Storage | -359B | |||

| 16:00 | USD | Crude Oil Inventories | -4.9M |

Dollar Weakens ahead of US House Data; European Stocks Strengthen

Here are the latest developments in global markets:

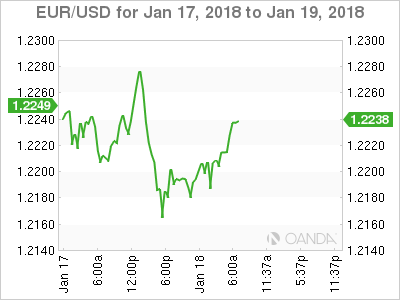

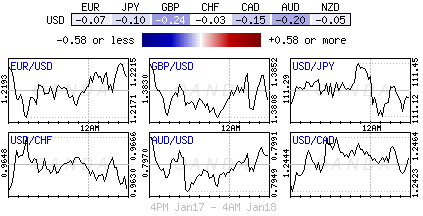

FOREX: The dollar index deviated below one-week highs reached earlier in the Asia session, edging down to 90.62 (+0.10%). Higher US Treasury yields and hopes on corporate tax repatriations contributed positively to the index's performance earlier. Dollar/yen was flat at 111.24 (-0.03%) and dollar/swissie tumbled to 0.9592 (-0.64%). Euro/dollar stretched its uptrend to 1.2236 (+0.42%) and pound/dollar rose to 1.3874 (+0.36%), potentially due to the positive sentiment related to Brexit developments. Aussie/dollar rebounded to $0.7988 (+0.25%) on the back of the dollar's weakness, while better-than-expected Australian jobs data also could have helped the pair.

STOCKS: Encouraging Chinese growth data provided moderate support to the European stocks after they sent the Hong Kong's Hang Seng index to record highs. The pan-European STOXX 600 opened higher but soon reversed earlier gains, trading flat at 1030 GMT (+0.06) due to losses in telecommunication services and utilities. The German Dax 30 jumped by 0.40% after Goldman Sachs upgraded the German chipmaker Infineon, while upbeat quarter sales stated by Carrefour sent the French CAC 40 higher. However, weakness in other sectors limited upside movements, with the index rising only by 0.17%. The British FTSE 100 fell by 0.38% as all index's components were on the backfoot except energy shares. US stock futures were in the green, pointing to a positive open.

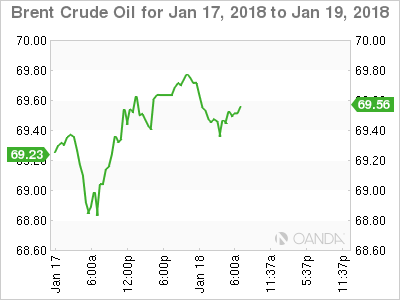

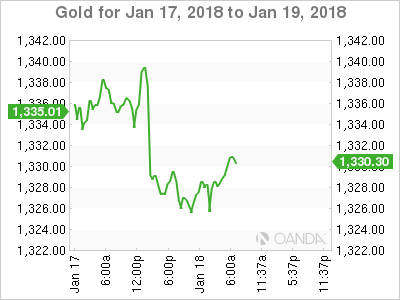

COMMODITIES: Oil prices were steady around three-year highs as threats of an attack on the Nigerian petroleum industry – Africa's largest oil exporter – weighed on the market. Particularly, the Militant group Niger Deltas Avengers warned of an attack on the Nigerian oil facilities in the next few days, hampering the region's supplies. WTI crude was last seen at $63.95 per barrel and Brent stood at $69.34. Gold inched up by 0.18% to $1,330 per ounce.

Day ahead: US reports on Housing data; EIA oil inventories pending

US housing data for the month of December will come into light on Friday with the potential to shake the dollar after the currency hit a three-year low on Thursday. At 1330 GMT, building permits are expected to climb by 1.290 million in the aforementioned month following an increase towards a two-year high at 1.303 million in November. On the other hand, the number of housing starts released at the same time are said to inch down from 1.297 million to 1.275 million, remaining around ten-month high levels.

In other data out of the US, weekly initial jobless claims and the January's Philadelphia Fed Manufacturing index due at 1330 GMT might show some weakness. According to forecasts, 250,000 people are expected to have applied for the first time for unemployment benefits in the week ending January 12 compared to 261,000 seen in the preceding week when the measure jumped to a three-month high. Regarding manufacturing business conditions in Philadelphia measured by the Federal Reserve of Philadelphia, the gauge is anticipated to fall by 2.9 points to +25.

In oil markets, investors will be waiting for the EIA weekly report, which tracks the change in US oil inventories, after yesterday's API data showed an unexpectedly sharp fall in US crude oil inventory levels. Analysts project that crude oil stocks have fallen by 3.536 million barrels in the week ending January 12, less than the decline of 4.948 million barrels seen in the week before. The report will be published at 1600 GMT.

The markets will also keep their eyes on the US Congress, as lawmakers are expecting to vote on the government's funding bill, which expires on Friday and has been extended three times so far, avoiding any potential government shutdown.

In Canada, the ADP employment report is to be released at 1330 GMT, but the results might bring moderate fluctuations to the loonie.

Public appearances scheduled for today involve a speech by the Cleveland Fed President Loretta Mester, who will comment on monetary policy at the Council for Economic Education's Economist on the Economy at 2305 GMT. Earlier, ECB member, Benoit Coeure will be speaking at a conference in Frankfurt at 1430 GMT.

EURUSD: Bullish, Risk Builds Up On 1.2322 Level

EURUSD - The pair continues to retain its upside pressure as it looks to target the 1.2322 level . On the upside, resistance comes in at 1.2300 level with a cut through here opening the door for more upside towards the 1.2350 level. Further up, resistance lies at the 1.2400 level where a break will expose the 1.2450 level. Conversely, support lies at the 1.2200 level where a violation will aim at the 1.2150 level. A break of here will aim at the 1.2100 level. Below here will open the door for more weakness towards the 1.2050. Its daily RSI is bullish and pointing higher. All in all, EURUSD faces further upside move on bullish offensive.

USDJPY Intraday Bullish Above 111.22

The U.S dollar has broken higher against the Japanese yen, with the pair hitting 111.48 overnight, following a sharp reversal in the U.S dollar index and a return to risk-on trading sentiment in global equity markets. The USDJPY pair currently trades around the key 111.20 technical region, with buyers supporting any dips lower in intraday price-action. Going forward, the pair will need to break above the 111.48 resistance level to keep the current bullish momentum intact, with the 112.00 handle then likely to come into focus.

USDJPY buyers retain control of the pair while price-action trades above the 111.22 level, further upside towards the 111.74 and 112.00 levels remains possible.

Should the USDJPY pair start to trade much below the 111.22 level, a further slide towards the 110.80 region appears likely.

GBPUSD Further Bullish Above 1.3880 Level

The British pound has moved higher against the U.S dollar during the European trading session, with price-action moving towards the 1.3860 region. Despite an early dip lower, GBPUSD buyers managed to defend the 1.3800 level, keeping the recent bullish trading moment intact, after sterling's recent run to multi-year trading highs. Going forward, sellers will likely need confirmation a near-term top is in place at 1.3940, while medium-term buyers will continue to push price higher, until the 1.3800 downside level is clearly broken.

The GBPUSD pair will likely turn further bullish above the 1.3880 resistance area, with buyers moving price towards the 1.3910 and 1.3940 levels.

A loss of the 1.3800 level will likely create a sentiment shift in the GBPUSD pair, with sellers targeting the 1.3755 and 1.3657 levels.

Technical Outlook: USDTRY Drops After CBRT Kept Rates Unchanged

The USDTRY pair dipped after Turkish central bank left interest rates unchanged in its first meeting in 2018. The action was widely expected as Turkish President Erdogan opposes high interest rates to provide cheap credit to boost growth. CBRT kept overnight lending rate at 9.25% and borrowing rate at 7.25%, maintaining its unorthodox policy, despite double-digit inflation. Turkish lira advanced further after data release, as the dollar showed signs of weakness, following repeated strong recovery rejection at 3.8330/20 on Tue/Wed. Near-term price action is holding between daily Tenkan-se (3.7818) and daily Kijun-sen (3.8131) with near-term bias turning lower after bounce from daily cloud base stalled in the middle of the cloud. Further direction signals could be expected on sustained break of Tenkan-sen or Kijun-sen pivots. Break lower would risk retest of daily cloud base (3.7705) and could generate stronger bearish signal on break while sustained lift above daily Kijun-sen would revive bullish near-term bias.

Res: 3.8131, 3.8217, 3.8262, 3.8330

Sup: 3.7883, 3.7818, 3.7705, 3.7446

EURCHF Holds In Upward Sloping Channel, Some Losses Are Expected

EURCHF has eased in the previous two days after it hit a three-year high of 1.1830 earlier this week. Prices broke above the 1.1800 psychological level on January 12 and are trading above their moving averages in the daily chart. It is worth mentioning that the pair has been developing within an upward sloping channel since August 2017.

Short-term momentum indicators are holding in the positive area. The RSI indicator is flattening above the 50 level, whilst the MACD oscillator stands above its trigger line with weak momentum, indicating further consolidation.

Should prices reverse lower, immediate support should come at 1.1680, which is slightly below the 23.6% Fibonacci retracement level at 1.1690 of the last upward movement with the low at 1.1255 and the high at 1.1830. A drop below this area would take the pair closer to the 38.2% Fibonacci mark of 1.1610.

To the upside, there is a resistance level at 1.1980 if the price breaks above this week’s high of 1.1830 and extends its gains beyond the upward sloping channel.

U.S Dollar Looking For A Toe Hole

Thursday January 18: Five things the markets are talking about

Europe's single currency and regional equities remain on firmer footing as Asian data lends the global growth story more momentum. U.S Treasury prices trade steady after yesterday's drop, while gold prices are little changed.

The EUR (€1.2233) has somewhat dismissed the European Central Bank (ECB) attempts to talk the currency down this week, while the ‘big' dollar continues its efforts to hold onto yesterday's advance. The U.S 10-year Treasury yields remain steady atop +2.60% amid speculation Congress will avert a government shutdown.

Today's agenda: Data stateside is expected to show that U.S housing starts probably slipped last month for the first time in three-months as frigid winter weather impeded work (08:30 am EDT). Elsewhere, central banks in Indonesia, Turkey and South Africa are all expected to keep policy unchanged.

1. Stocks record new records

In Japan, the Nikkei ended lower after hitting a new 26-year high overnight. The Nikkei dropped -0.4% as investors turned cautious. Both real estate stocks and financial firms underperformed.

Down-under, Aussie shares slid to a fresh five-week low, pressured by noted profit taking in heavyweight miners BHP Billiton and Rio Tinto. Faltering a second day running amid broad local weakness, the S&P/ASX 200 fell -0.5%. In S. Korea, the KOSPI traded effectively flat.

In Hong Kong, Hong Kong stocks rallied overnight to fresh new highs, led by telecommunications and financial firms. The China Enterprises index extended gains after data showed China's Q4 economic growth beats expectations. At close of trade, the Hang Seng index was up +0.43%, while the Hang Seng China Enterprises index rose +1.76%.

Note: China's economy grew +6.8% in Q4, helped by a rebound in the industrial sector, a resilient property market and strong export growth.

In China, banking and infrastructure firms power China stocks to a two-year high. The Shanghai Composite index was up +0.91%, while the blue-chip CSI300 index was up +0.58%.

In Europe, regional indices trade mixed with notable strength in DAX following on from a strong close yesterday stateside – the Dow settled above the psychological +26K for the first time.

U.S stock futures are expected to open in the ‘red' (-0.1%).

Indices: Stoxx600 +0.1% at 398.5, FTSE -0.3 at 7702, DAX +0.4% at 13235, CAC-40 +0.2% at 5504, IBEX-35 -0.1% at 10463, FTSE MIB +0.3% at 23575, SMI flat at 9439, S&P 500 Futures -0.1%.

2. Oil holds near three-year highs, supported by threat of Nigeria attack

Oil prices are holding steady ahead of the U.S open, supported by falling inventories of crude and threats of an attack on Nigeria's petroleum industry, despite a reported rise in U.S fuel supplies weighed.

Crude is within sight of its three year highs, supported by supply cuts led by the OPEC and on concerns that unrest in producer nations such as Nigeria could further curb output.

Note: Militant group Niger Delta Avengers (NDA) has threatened to attack Nigeria's oil sector in the next few days, potentially hampering supplies in Africa's largest exporter.

Brent crude futures have slipped -7c to +$69.31 barrel. On Monday it hit +$70.37, the highest since December 2014. U.S crude is up +2c at +$63.99 and reached it's highest price in three-years on Tuesday.

Note: Yesterday's API supply report presented a mixed picture, with inventories of gas and diesel rising and crude stocks falling.

Expect investors to take directional clues from today's U.S government's weekly supply data (10:30 am).

Gold prices trade a tad lower as the as dollar gains on stronger U.S. data. The ‘yellow' metal has hit its lowest in nearly a week, as the dollar edged higher from three-year lows on stronger-than-expected U.S. economic data. Spot gold is down -0.1% at +$1,326.11 per ounce.

3. Sovereign bond yields climb

The U.S 10-year Treasury yield has hit its highest print since March 2017 at +2.60% in overnight trading. This rally higher has managed to drag along its European counterparts sovereign yield curves.

Note: The yield on the two-year U.S note, which is considered to be especially sensitive to expectations for interest-rate increases from the Fed, settled last week above +2% for the first time in a decade.

Investors will now get a look at data on U.S housing starts and jobless claims (08:30 am EDT), as well as comments from multiple Federal Reserve officials for further directional yield clues.

In Germany, the 10-year Bund yield is trading atop of its six-month high at +0.52%, while in the U.K, the 10-year Gilt yield has advanced +2 bps to +1.33%.

4. Dollar looking for a toe hole

The U.S dollar is a tad weaker versus G10 currency pairs despite higher Treasury yields – U.S 10-year yields have moved above the psychological +2.60% level to print a new 11-month high.

The EUR/USD (€1.2212) is hovering just above key support levels in a quiet European session as investors' assesse the ECB's recent rhetoric. The ‘single' unit is off its recent three-year high print as market participants contemplated whether ECB's Draghi would push back against EUR's strength during his press conference next week following the ECB's policy meeting.

Note: Several Governing Council members of the ECB are set to speak today.

Elsewhere, the sterling has rallied less than +0.05% to £1.3834, hitting the strongest in 19-months. The U.K's House of Commons has approved the E.U Withdrawal Bill in its third reading (as expected) with vote at 324 to 295. The Bill will now be reviewed by the House of Lords, which could ask for more changes.

USD/JPY (¥111.28) is hovering above key support as some at BoJ officials are said to be seeking future normalization talks.

In South Africa, a sounder political backdrop has seen the rand surge – ZAR has climbed +0.4% to $12.2493, the strongest in more than two-years.

5. China's 2017 GDP growth accelerates for first time in seven years

Data overnight indicated that China's economy expanded by +6.9% in 2017, growing at a faster annual pace for the first time since 2010.

The country's economy grew by +6.8% y/y in Q4 2017, beating a +6.7% consensus increase forecast.

Digging deeper, the GDP growth was largely helped by strong investment momentum, especially in infrastructure and real estate, and partly by improved trade performance.

Nevertheless, China's domestic demand is expected to be the biggest factor that drags down economic growth this year while external demand may increase.

Note: Investment in infrastructure projects and the property sector – which helped fuel 2017 activity, is expected to experience a sharp slowdown in 2018.

Technical Outlook: WTI Oil – Rising 10 SMA Contains For Now, EIA Crude Stocks Report Eyed

WTI oil ticked higher on Thursday, supported by stronger than expected draw in crude stocks (API report on Tuesday showed draw of 5.12 million barrels vs 3.6 million barrels draw forecasted) and threats of attack at oil infrastructure in Nigeria. The price stayed at the back foot in past two days, following pullback from new three-year high at $64.87, but dips were contained by rising 10SMA at $63.30 zone. Recovery attempts however, were so far limited and keeping the downside vulnerable. Extended consolidation could be likely near-term scenario before the price establishes in fresh direction. Downticks should be held by rising 10 SMA (currently at $63.50) and above past two day lows at $63.30 zone to keep immediate focus at the upside. Expectations for today's EIA crude stocks report show draw of 3.4 million barrels, which could be supportive on release at forecasted level or stronger than expected draw in oil inventories. Conversely, weaker than expected crude stocks could soften near-term structure for break below $63.50/30 pivots and signal deeper pullback.

Res: 64.32, 64.87, 65.00, 65.88

Sup: 63.83, 63.50, 63.30, 63.05

AUD/USD Riding Higher

AUD/USD's upside pressures are growing. Hourly resistance is now given at 0.8025 (17/01/2018 high). Support stands at 0.7849 (12/01/2018 low). The road is wide open for further upside.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view