Sample Category Title

Japanese Yen Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.45% against the JPY and closed at 110.87.

In the Asian session, at GMT0300, the pair is trading at 110.64, with the USD trading 0.21% lower against the JPY from yesterday's close.

Overnight data indicated that Japan's monetary base rose 20.3% YoY in March, after recording a rise of 21.4% in the prior month.

The pair is expected to find support at 110.20, and a fall through could take it to the next support level of 109.76. The pair is expected to find its first resistance at 111.33, and a rise through could take it to the next resistance level of 112.02.

March, scheduled to release in the early hours of tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

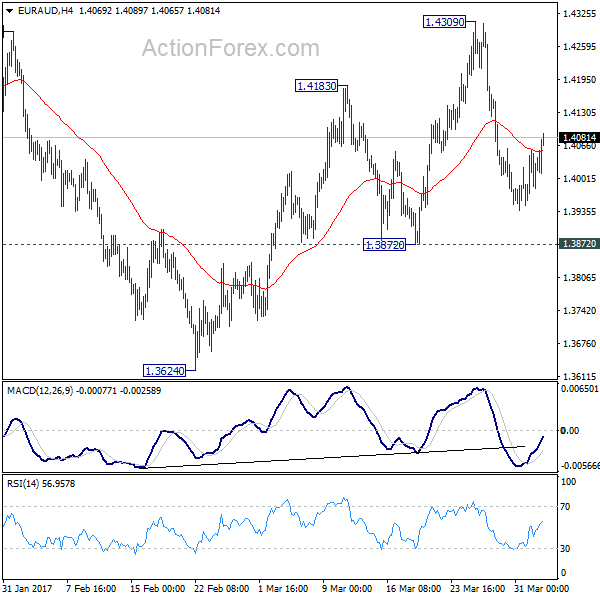

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.3969; (P) 1.4012; (R1) 1.4072; More...

EUR/AUD remains bounded in range of 1.3872/4309 and intraday bias remains neutral. We're holding on to the case of trend reversal after defending key support level at 1.3671. Another rise is expected as long as 1.3872 minor support holds. Break of 1.4309 will extend the rebound from 1.3624 to 1.4721 key resistance level next. Break should confirm larger trend reversal. However, firm break of 1.3872 support will dampen our bullish view. In such case, intraday bias will be turned back to the downside for 1.3624 low instead.

In the bigger picture, price actions from 1.6587 medium term top are viewed as a corrective pattern. Such correction could be completed after testing 1.3671 support. Break of 1.4721 cluster resistance (38.2% retracement of 1.6587 to 1.3624 at 1.4756) should confirm this case and target 61.8% retracement at 1.5455 and above. Overall, we'd expect the up trend from 1.1602 to resume later. However, sustained break of 1.3671 will invalidate our bullish view and would turn extend the fall from 1.6587 towards 1.1602 long term bottom.

Swiss Real Retail Sales Rebounded For The First Time In 3 Months In February

For the 24 hours to 23:00 GMT, the USD slightly rose against the CHF and closed at 1.0018.

On the data front, Switzerland’s real retail sales rebounded 0.6% on an annual basis in February, rising for the first time in three-months. In the previous month, real retail sales had recorded a revised drop of 1.2%. Further, the nation’s SVME–PMI advanced to a level of 58.6 in March, higher than market expectations of an increase to a level of 58.0. The PMI had registered a level of 57.8 in the prior month.

In the Asian session, at GMT0300, the pair is trading at 1.0020, with the USD trading marginally higher from yesterday’s close.

The pair is expected to find support at 1.0004, and a fall through could take it to the next support level of 0.9989. The pair is expected to find its first resistance at 1.0036, and a rise through could take it to the next resistance level of 1.0053.

With no economic releases in Switzerland today, investor sentiment will be governed by global macroeconomic factors.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

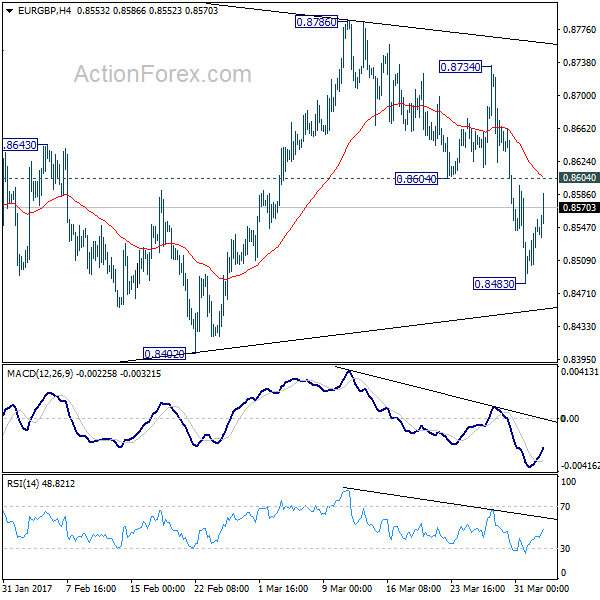

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8505; (P) 0.8531; (R1) 0.8571; More...

EUR/GBP recovered after forming a temporary low at 0.8430, ahead of 0.8402 support. Intraday bias is turned neutral first. There is no change in the view that price actions from 0.8303 are a consolidation pattern. And, it's the second leg of the correction from 0.9304. Below 0.8430 will target 0.8402. Break of 0.8402 will resume the fall from 0.9304 to 0.8116/20 cluster support, where the correction should end. Above 0.8604 minor resistance will bring another recovery before fall from 0.9304 resumes.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Such decline is likely ready to resume and should make a new low below 0.8303. At this point, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Break of 0.9304 will pave the way to 0.9799 (2008 high). However, sustained break of 0.8116 could bring deeper decline to next key support level at 0.7564 before the correction completes.

Canadian RBC Manufacturing PMI Jumped To Its Highest Level Since October 2013 In March

For the 24 hours to 23:00 GMT, the USD rose 0.47% against the CAD and closed at 1.3383.

Macroeconomic data showed that Canada's RBC manufacturing PMI advanced to a level of 55.5 in March, expanding at its fastest rate since October 2013, compared to a level of 54.7 recorded in the previous month.

Separately, the Bank of Canada (BoC), in its latest business outlook survey, indicated that the balance of opinion on future sales dropped to 21.0% from 26.0% in the previous quarter.

In the Asian session, at GMT0300, the pair is trading at 1.3383, with the USD trading flat against the CAD from yesterday's close.

The pair is expected to find support at 1.3328, and a fall through could take it to the next support level of 1.3272. The pair is expected to find its first resistance at 1.3419, and a rise through could take it to the next resistance level of 1.3454.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0674; (P) 1.0684; (R1) 1.0695; More...

As noted before, EUR/CHF's rebound form 1.0629 should have completed at 1.0823. Intraday bias stays mildly on the downside for 1.0620/29 key support zone. Decisive break there will resume the larger fall from 1.1198. On the upside, above 1.0709 minor resistance will turn intraday bias neutral. But outlook will be cautiously bearish as long as 1.0761 resistance holds.

In the bigger picture, the decline from 1.1198 is seen as a corrective move. Current development suggests that it's not completed yet. sustained trading below 38.2% retracement of 0.9771 to 1.1198 at 1.0653 will target 50% retracement at 1.0485. In any case, break of 1.0823 resistance is needed to be the first indication of reversal. Otherwise, deeper fall is still expected even in case of recovery.

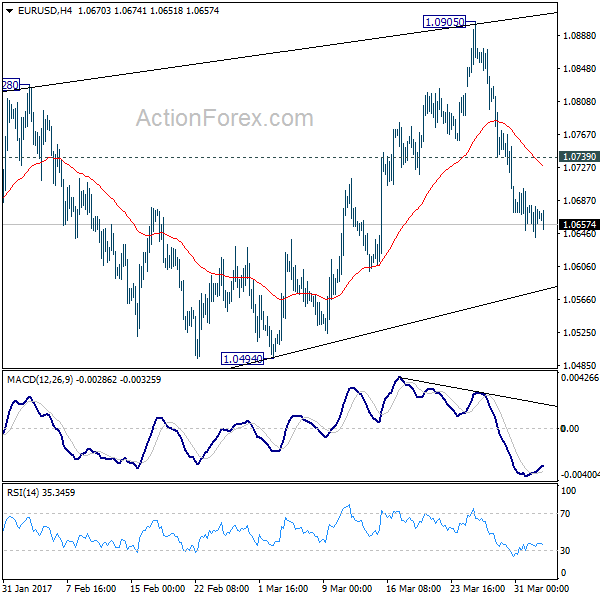

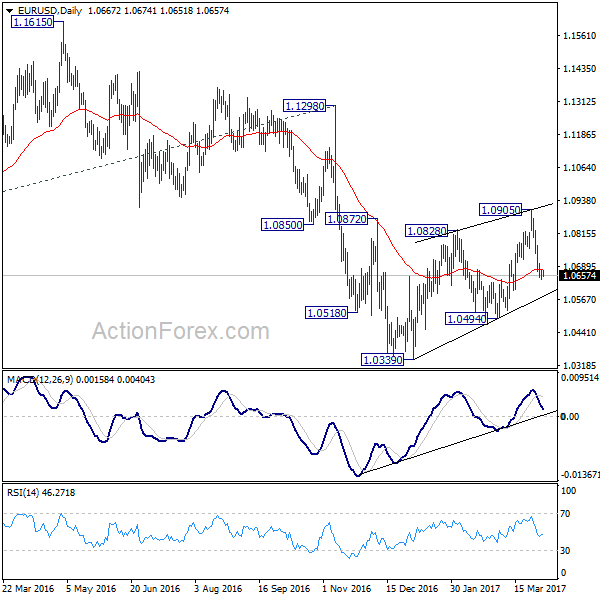

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0647; (P) 1.0664 (R1) 1.0686; More....

EUR/USD lost some downside momentum with 4 hour MACD crossed above signal line. But deeper decline is still expected with 1.0739 minor resistance intact. Our view is unchanged that corrective rise from 1.0339 is completed at 1.0905. And more importantly, larger down trend is probably resuming. Break of 1.0494 should confirm this bearish case and target 1.0339 low. Further break of 1.0339 will target parity next. On the upside, above 1.0739 minor resistance will delay the bearish case and turn focus back to 1.0905 resistance instead.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

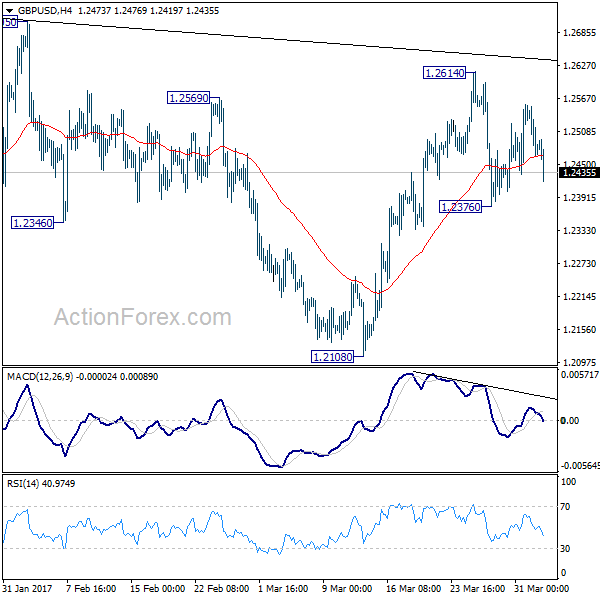

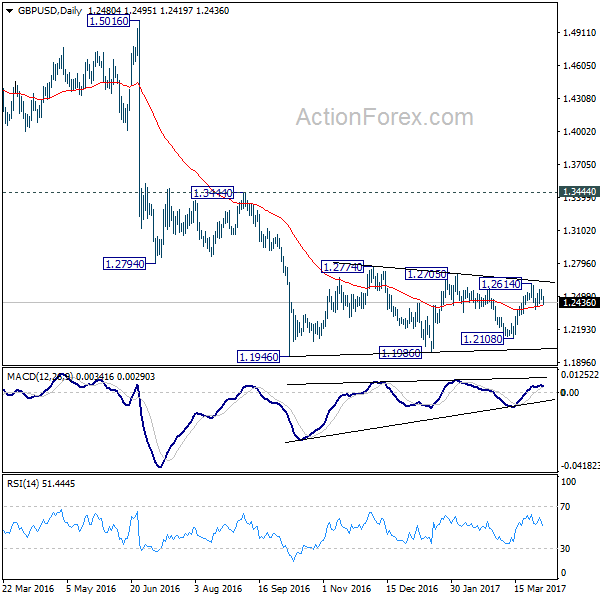

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2448; (P) 1.2501; (R1) 1.2538; More...

GBP/USD is still bounded in range of 1.2376/2614 and intraday bias stays neutral for the moment. Overall, price actions from 1.1946 are viewed as a consolidation pattern pattern. On the downside, break of 1.2376 will turn bias to the downside for 1.2108 support. Decisive break there will be an early sign of larger down trend resumption. On the upside, break of 1.2614 will extend the rise from 1.2108. But upside should be limited by 1.2705/2774 resistance zone to bring larger down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

RBA Torn Between High Housing Prices And Subdued Inflation

RBA left the cash rate unchanged at 1.5% in April, continuing to struggle between soaring property prices and subdued inflation. Policymakers appeared more optimistic over the global economic outlook than the domestic one. The central bank remained concerned over the rising property prices and warned of the situation that household borrowing growth was outpacing growth in income. We expect RBA to leave its monetary stance unchanged throughout the year.

Economy to show moderate growth

The central bank noted domestic economy continued to show 'moderate growth' in the 'transition following the end of the mining investment boom'. Policymakers acknowledged rising non-mining business investment over the past year and pickup in business confidence. Meanwhile, they also acknowledged some deterioration in the employment market, noting the rise in unemployment rate, modest growth in payrolls as slow wage growth. RBA continued to warn of low inflation.

Inflation remains quite low

As noted in the statement, inflation 'remains quite low'. While the headline reading should 'pick up over the course of 2017 to be above 2%, underlying inflation would rise more gradually with 'growth in labour costs remaining subdued'. Recall that the country's unemployment rate rose to 5.9%, the highest in 13 months, in February, up from 5.7% a month ago. The number of payrolls slipped -0.1K, the first drop in 5 months, while the number of unemployed increased +26K. Headline CPI moderated to +0.5% q/q in 4Q16, from +0.7% in the prior quarter. Core inflation steadied at +0.4% q/q for the quarter.

RBA concerned on house prices

The persistently-high housing prices remained a concern. As suggested in the statement, 'conditions in the housing market continue to vary considerably around the country'. While 'conditions are strong and prices are rising briskly' in some markets, prices are 'declining' in others. It also addressed the situation in the eastern capital cities, noting that 'a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Growth in rents is the slowest for two decades'. Yet, the above message was only a repeat of previous meeting statements.

Household borrowing outpaced income growth

What's new was the warning that household borrowing growth was outpacing growth in income. Policymakers judged that 'the recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness'. They added that 'lenders need to ensure that the serviceability metrics that they use are appropriate for current conditions. A reduced reliance on interest-only housing loans in the Australian market would also be a positive development'.

USD/CHF Daily Outlook

Daily Pivots: (S1) 1.0002; (P) 1.0019; (R1) 1.0032; More.....

USD/CHF lost some upside momentum after hitting 110.36 as seen in 4 hour MACD. But still, further rally is in favor with 0.9948 minor support intact. As noted before, corrective decline fall from 1.0342 should have finished with three waves down to 0.9812 already. Sustained trading above 55 day EMA (now at 1.0023) will affirm this bullish case. Break of 1.0169 resistance will confirm and target a test on 1.0342 high. On the downside, however, below 0.9948 minor support will turn bias back to the downside for 0.9812 instead.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.