Sample Category Title

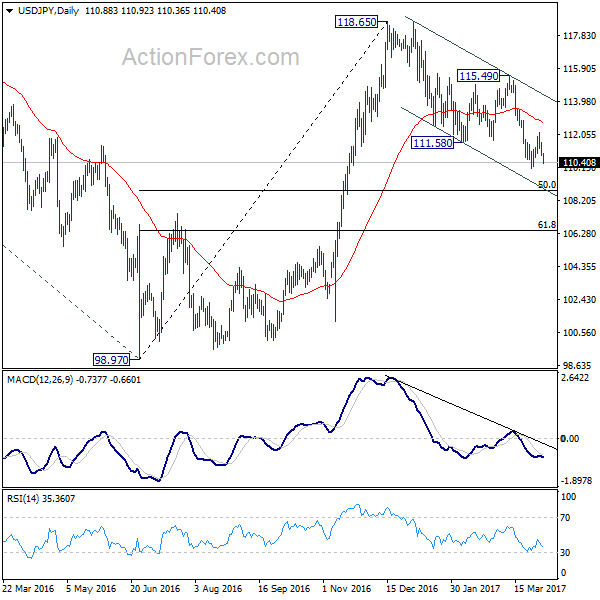

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.64; (P) 111.11; (R1) 111.37; More....

USD/JPY's fall and break of 110.99 minor support suggests that rebound from 110.10 is completed. More importantly, the corrective decline from 118.65 is still in progress. Intraday bias is turned back to the downside. Break of 110.10 will confirm fall resumption and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, break of 112.19 resistance is needed to confirm near term reversal. Otherwise, outlook will stay mildly bearish in case of recovery.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

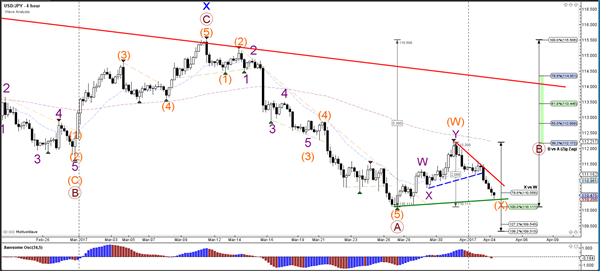

Daily Technical Analysis: USD/JPY Challenges Support Trend Line At 110

Currency pair USD/JPY

The USD/JPY broke below the support trend line (dotted blue) and is now testing the next support (green). A bounce and break above resistance (red) could indicate that wave X (orange) has been completed whereas a break below the 138.2% Fibonacci level invalidates wave X (orange).

The USD/JPY break above the 61.8% Fibonacci level invalidates wave 4 (pink). A final wave 5 (pink) after a wave 4 (pink) retracement could for instance bounce at the 100% Fib level of wave X vs W (orange) and 110 psychological round level.

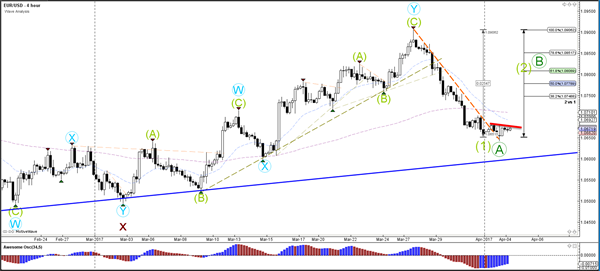

Currency pair EUR/USD

The EUR/USD is struggling to show strong bullish momentum above the resistance trend line (dotted orange). When looking at an hourly chart it seems more likely that a wave 2 or B retracement will occur soon.

The EUR/USD could still be in a wave ABC (orange) because it did not break below the 138.2% Fibonacci level of wave B vs A. A break below that level indicates a downtrend continuation whereas a break above resistance (red) could spark a wave C (orange).

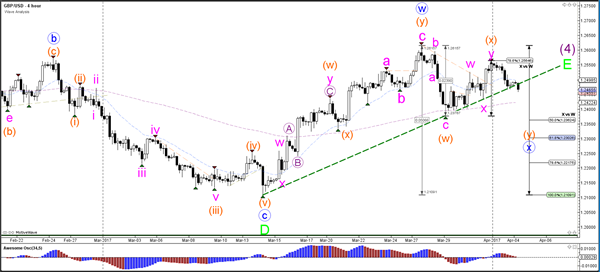

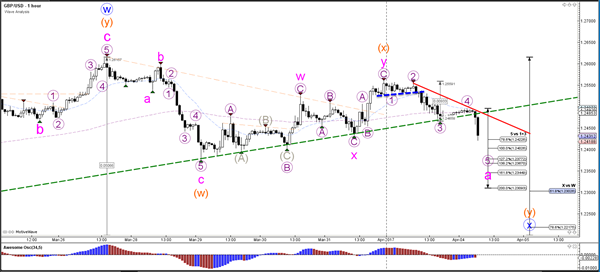

Currency pair GBP/USD

The GBP/USD failed to break above the previous top or 78.6% Fibonacci resistance level and is now breaking below the support trend line (dotted green) which changes the expected wave structure. The failure of the bullish price movement makes it a wave X (orange). Price could now be retracing to the Fibonacci levels of wave X vs W (blue).

The GBP/USD bearish breakout below the support level of the mini triangle (dotted blue) made an ABC (purple) zigzag within wave Y (pink) of wave X (orange) more likely than a 12345. The wave 4 (purple) developed as a bear flag and broke earlier today. A larger ABC zigzag (pink) could occur before completing wave X (blue).

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3314; (P) 1.3356; (R1) 1.3425; More....

USD/CAD rebounded strongly after defending 1.3263 support but it's held below 1.3413 resistance so far. Intraday bias remains neutral for the moment. Fall from 1.3534 is seen as a correction, no change in this view. On the upside, break of 1.3413 will argue that such correction is completed and turn bias back to the upside for 1.3534 and above. On the downside, below 1.3263 will bring deeper fall. But we'd expect strong support from 1.3211 cluster level (61.8% retracement of 1.3008 to 1.3534 at 1.3209) to contain downside and bring rebound.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

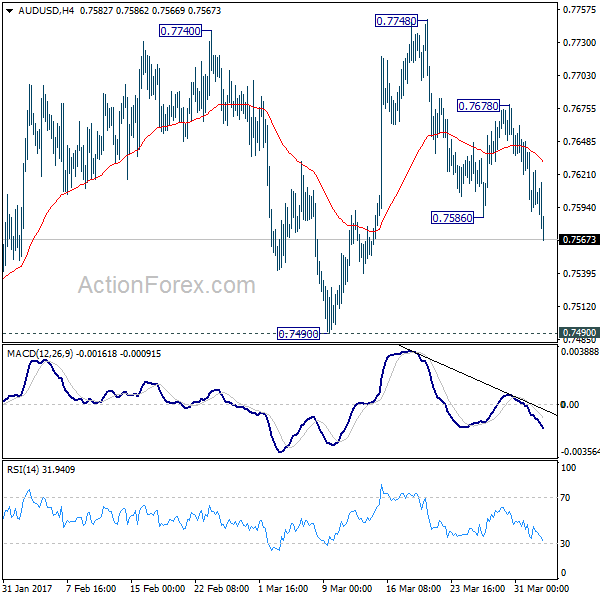

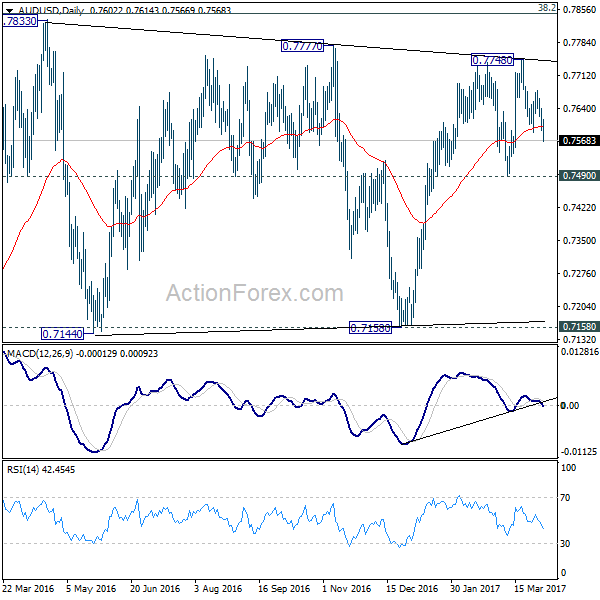

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7583; (P) 0.7612; (R1) 0.7632; More...

AUD/USD drops to as low as 0.7567 so far today. Break of 0.7586 support indicates resumption of whole decline from 0.7748. Intraday bias is back on the downside for 0.7490 key near term support next. As noted before, firm break of 0.7490 will confirm completion of rise from 0.7158. In such case, near term outlook will be turned bearish for 0.7158 support. On the upside, however, above 0.7678 minor resistance will turn bias back to the upside. And in this case, rise from 0.7159 could extend towards long term retracement level at 0.7849 before completion.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8165) and above.

Australian Dollar Lower as RBA Shows Concern on Employments, US Yield Down on Fed Dudley Comments

Australian dollar weakens after the Reserve bank of Australia held cash rate unchanged at 1.50% as widely expected and maintained a neutral stance. RBA reiterated in the statement that "taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time." The statement itself is largely unchanged from the prior one.

Nonetheless, RBA sounded more concerned on employment as it noted that "some indicators of conditions in the labour market have softened recently." Meanwhile, RBA also said that "by reinforcing strong lending standards, the recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness. " And the central bank welcomed the "reduced reliance" on interest-housing loans as a positive development.

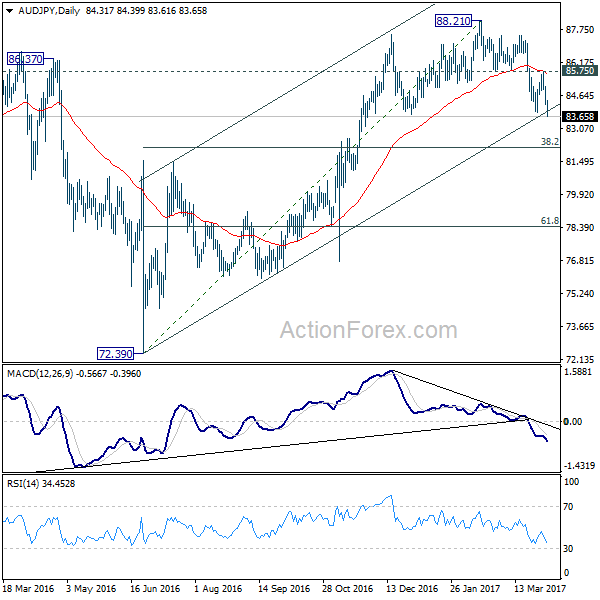

AUD/USD and AUD/JPY resumes near term fall

Technically, AUD/USD's break of 0.7586 today indicates that fall from 0.7748 has resumed for 0.7490 key near term support. Decisive break there will confirm short term trend reversal. AUD/JPY also dives through last week's low at 83.81. And it confirms resumption of whole decline from 88.21. Prior rejection from 55 day EMA is seen as a sign of near term bearishness. As mentioned in our weekly report, we'd expect AUD/JPY to target 38.2% retracement of 72.39 to 88.21 at 82.16.

Yen jumps after Russia terrorist attack...

Elsewhere, Yen surges broadly on risk aversion as terrorist attack at St Petersburg, Russia weighed on sentiment,According to three state-owned Russian media, at least eleven people were killed in the St Petersburg metro explosion. President Vladimir Putin suggested it would be considered as a terrorist attack "first of all". As noted in his statement released after the incident, "the causes of this event have not been determined yet, so it's too early to talk about [possible causes]… The investigation will show. Certainly, we will consider all variants, common, criminal, first of all, of a terrorist nature".

... and falling US treasury yields

Comments from New York Fed President William Dudley weighed down US treasury yields. At an interview with Bloomberg TV, Dudley indicated that the Fed is not in a rush to raise the policy rate. As he noted, "a couple more hikes this year seems reasonable… It wouldn't surprise me if sometime later this year or sometime in 2018, should the economy perform in line with our expectations, that we'll start to gradually let securities mature rather than reinvesting them,…we might actually decide at the same time to take a little pause in terms of raising short-term interest rates". 10 year yield dropped through last week's low at 2.348 to as low as 2.332 before closing at 2.350.

On the data front...

Australia trade surplus widened to AUD 3.57b in February. Japan monetary base rose 20.3% yoy in March. UK will release construction PMI in European session while Eurozone will release retail sales. Canada will released trade balance. US will release trade balance and factory orders.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7583; (P) 0.7612; (R1) 0.7632; More...

AUD/USD drops to as low as 0.7567 so far today. Break of 0.7586 support indicates resumption of whole decline from 0.7748. Intraday bias is back on the downside for 0.7490 key near term support next. As noted before, firm break of 0.7490 will confirm completion of rise from 0.7158. In such case, near term outlook will be turned bearish for 0.7158 support. On the upside, however, above 0.7678 minor resistance will turn bias back to the upside. And in this case, rise from 0.7159 could extend towards long term retracement level at 0.7849 before completion.

In the bigger picture, we're still treating price actions from 0.6826 low as a correction. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8165) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Mar | 20.30% | 23.20% | 21.40% | |

| 1:30 | AUD | Trade Balance (AUD) Feb | 3.57B | 1.75B | 1.30B | 1.50B |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 8:30 | GBP | Construction PMI Mar | 52.5 | 52.5 | ||

| 9:00 | EUR | Eurozone Retail Sales M/M Feb | 0.50% | -0.10% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | 0.7B | 0.8B | ||

| 12:30 | USD | Trade Balance Feb | -46.0B | -48.5B | ||

| 14:00 | USD | Factory Orders Feb | 0.90% | 1.20% | ||

| 14:00 | USD | ISM Manufacturing Mar | 57.1 | 57.7 | ||

| 14:00 | USD | ISM Prices Paid Mar | 66 | 68 | ||

| 14:00 | USD | Construction Spending M/M Feb | 1.00% | -1.00% |

Elliott Wave View: EURJPY More downside

Short term Elliott Wave view in EURJPY suggests that cycle from 3/12 peak (122.89) is unfolding as a double three Elliott wave structure where Minor wave W ended at 119.28 and Minor wave X ended at 120.45. Minor wave Y is in progress and the internal is unfolding also as a double three Elliott wave structure where Minute wave ((w)) can be complete already at 117.8 and wave ((x)) bounce should correct cycle from 3/28 peak (120.445) before pair turns lower. As pair is showing a 5 swing bearish sequence from 3/12 peak as well as from 12/14/2016 peak, more downside is expected in the pair. We don’t like buying the proposed bounce and expect sellers to appear once wave ((x)) bounce is complete in 3, 7, or 11 swing provided that pivot at 3/28 high is intact in the first degree.

1 Hour EURJPY Elliott Wave Chart

Dollar Yen Reversal Back On The Cards This Week

Key Points:

- The pair should be readying to reverse in the coming sessions.

- Falling wedge and double bottom structures remain in play.

- MACD crossover suggestive of a change in medium-term trend.

The Dollar Yen had an interesting session yesterday, moving rather notably against the broader market trend as the USD picked up some momentum. Whilst much of this movement is explainable by weaker bond yields and a leaky stock market, this fundamental bias is likely to be countered in the coming session as the market repositions to better reflect the developing technical bias.

First and foremost, there are two key structures in play that are now suggestive of an impending reversal and subsequent uptrend for the USDJPY. Firstly, the long-term falling wedge remains intact and its downside constraint will be providing some solid support around the current price. However, this doesn’t necessarily indicate that we are likely to have the rather strong uptrend forecasted below. Luckily, the well-defined double bottom structure present on the chart does infer such a rally is on the way which should see buying pressure mount shortly.

On their own, the two chart patterns may not be enough to spark the requisite shift in momentum to see the pair push higher and, ultimately, break through the 38.2% Fibonacci level. Fortunately, we have a number of other instruments that are supportive of just such a breakout. For one, the parabolic SAR retains a bullish bias and the stochastics are hovering around oversold. Moreover, the MACD oscillator is on the cusp of having a signal line crossover which could spell a change in the medium-term trend for the USDJPY.

Despite the cumulative evidence suggestive of this forecast, there remains one key hurdle that the pair needs to overcome. Specifically, that 38.2% Fibonacci level around the 112.10 mark will prove to be a major cap on upside potential given that it coincides with both the neckline of the double bottom and the 100 day EMA. However, due to the rigidity of this zone of resistance, if the venerable pair can manage to break free, the resulting uptick in buying pressure could be fairly spectacular and this could, in turn, see a sharp rally to upside constraint of the wedge.

Overall, there is a rather robust technical case for a reversal for the USDJPY which could see some serious gains claimed over the coming weeks. Indeed, if the US fundamentals begin to show a greater degree of consensus, we could see that 113.50 handle challenged significantly sooner than currently projected. Although, it’s worth mentioning, the JPY’s safe haven status has been dragging the pair lower more generally as of late and this shouldn’t be entirely ignored moving forward.

Euro Receives Reprieve But Watch For Further Falls In The Week Ahead

Key Points:

- Price action holding up due to poor U.S. bond yields and a leaky equity market.

- Draghi's pending speech will be one of the key events ahead.

- Watch for a further breakdown as sentiment swings back to the greenback.

The Euro had a torrid week after the markets seemingly unwound their hawkish view of the ECB's policy path. In addition, the EU CPI figures also proved highly disappointing, coming in well below forecasts at a meagre 1.5% y/y. Subsequently, the past week has seen a sharp reversal, away from challenging the 1.10 handle, and we have again returned to a bearish trend direction. However, there are some interesting events coming in the week ahead so let's review what is potentially on the horizon for the embattled pair.

Last week proved disastrous for the Euro as the air seemingly leaked out of the hawkish trial balloon that the ECB had floated. The market had previously taken a relatively positive view of the ECB's potential policy path on hikes following some odd comments from the central bank on near term rate hikes. However, the ECB was quick to walk those comments back last week and the balloon deflated with astonishing speed sending the Euro Dollar collapsing back below the 1.07 handle. In addition, the Eurozone CPI figures also provided a negative result at 1.5% y/y which was sharply below the economic forecast. Subsequently, the pair never really had a chance to recover and ended the week sharply lower around the 1.0656 mark.

Looking ahead, the pair is likely to focus sharply on ECB Chair Mario Draghi's pending speech, along with the always volatile U.S. Non-Farm Payroll figures. In particular, Draghi's statement is likely to provide the market with some further clarity on the ECB's near term policy path. Given the current level of uncertainty, it's unlikely that the Euro has yet reached a stable equilibrium so expect plenty of volatility following the event. In addition, the U.S. NFP figures are also due out and could further complicate the pair's near term trend. Most market analysts have estimated a 180k print but, as always, we could potentially see a fairly wide range from the metric. Subsequently, the Dollar is likely to be in-play as well which provides for a relatively volatile week for the pair.

However, early indications are suggesting that there are some negative capital flows away from the U.S. Dollar occurring. In particular, falling bond yields and a leaking equity market has seen capital flowing into safe havens overnight which has stalled the decline of the Euro Dollar, at least in the short term.

From a technical perspective, the Euro's recent rise took it right to the 1.0905 resistance zone before a rejection saw the move reverse and a sharp pullback subsequently ensued. This development argues that the rally is now over and a new corrective phase is in progress with a downside target around the 1.0494 support level. In addition, the RSI Oscillator is continuing to trend lower, within neutral territory, suggesting that there is still plenty of room to move on the downside. Subsequently, our initial bias for the week ahead is bearish with targets well under the 1.05 handle.Support is currently in place for the pair at 1.0620, 1.0495, and 1.0364. Resistance exists on the upside at 1.0677, 1.0783, and 1.0828.

Ultimately, the Euro is likely to remain under pressure over the next few days as the inevitable sentiment swing back towards the greenback is all but assured. Subsequently, near term support is unlikely to hold for the pair and we could potentially see the pair back below the 1.06 handle in the coming sessions.

Daily Technical Outlook And Review: EUR/USD, GBP/USD, USD/JPY, AUD/USD, USD/CHF, AUD/JPY, XAU/USD

EUR/USD

While the outlook remains bearish, there is positive Stochastic divergence on the hourly charts, suggesting the currency pair could have a small bounce before the downtrend continues.

Look for the area around 1.0720 as first stronger technical resistance. To the downside, 1.06 is key. A break below that level would signal that a move towards 1.05 could follow quickly.

GBP/USD

Price is consolidating within a triangle pattern on the hourly chart. After the rejection at 1.2550 resistance yesterday, it has a slight downside bias for the day. Watch the trendline support on the H1 chart.

A break below could then pave the way for a test of at least 1.2435 – an important intraday level. Strong support is then seen in the area between 1.2340-75, which would be a buy opportunity with a favourable risk-reward.

USD/JPY

The downtrend is intact and yesterday's price action confirmed that once again. The currency pair broke below support at 110.80 and fell to 110.47 in Asia. A test of 110.00 seems likely in the near-term. That level is key.

A break below would very likely trigger momentum selling and push USD/JPY towards the next major support level around 108.00. To the topside, watch the 110.85 and 111.13 level for sell opportunities.

AUD/USD

The Aussie is showing resilience. The currency pair bounced off 0.7587 support, and while it is struggling to rally, there is a lack of downside momentum as well. Nevertheless, it looks increasingly likely that the support level will crack in the near-term. This would then signal a move towards 0.75. Intraday, keep an eye on the trendline resistance on the hourly chart and the 0.7640 & 0.7680 resistance levels.

USD/CHF

USDCHF is showing negative Stochastic divergence on the hourly charts. A correction seems likely before the uptrend continues. Traders should keep an eye on support at 0.9960 for buying opportunities.

To the topside, immediate resistance is seen at 1.0060, followed by stronger resistance at 1.01.

AUD/JPY

Price is approaching a very significant support level at 83.75. A clear break below it would signal that a decline towards 81.50 could follow. Medium-term, the currency pair remains in an uptrend.

A break below 83.75 would change the outlook however and confirm the top at 88.

XAU/USD

Support at 1240 held once again and Gold was able to recover to 1257 in Asia. Another test of 1263 resistance is very likely. If Gold is able to break and close the trading day above that level, an extension of the rally to at least 1292 is highly likely.

Intraday, keep an eye on 1250 and 1244 for support.

European Open Briefing: Yen Rose Against Most Other Currencies

Global Markets:

- Asian stock markets: Nikkei down 0.70 %, ASX 200 lost 0.20 %, Hang Seng and Shanghai Composite closed for holiday

- Commodities: Gold at $1258 (+0.32 %), Silver at $18.32 (+0.60 %), WTI Oil at $50.30 (+0.05 %), Brent Oil at $53.15 (+0.05 %)

- Rates: US 10-year yield at 2.33, UK 10-year yield at 1.06, German 10-year yield at 0.28

News & Data:

- Australian Trade Balance (AUD) Feb: 3.574B (exp 1.800B; prev 1.302B)

- Australian Exports (MoM) Feb: 1.0% (prev -3.0%)

- Australian Imports (MoM) Feb: -5.0% (prev 4.0%)

- Australian ANZ Roy Morgan Weekly Consumer Confidence Index 2-Apr: 111.1 (prev 113.8)

- New Zealand NZIER Business Confidence Q1: 17.0% (prev 28.0%)

- South Korean CPI (YoY) Mar: 2.2% (exp 2.0%; prev 1.9%)

- South Korean CPI (MoM) Mar: 0.0% (exp -0.2%; prev 0.3%)

- Asia stocks skittish as investors seek safe havens before Trump-Xi meeting – RTRS

Markets Update:

There was a risk-off sentiment in Asia with stock markets down on the day, and the Japanese Yen the best performing currency overnight. Traders in Asia are waiting for the upcoming meeting between US President Trump and the Chinese President Xi Jinping. Trump has criticized China many times before, accusing them of currency manipulation and 'stealing US jobs'. Therefore, the market is interested to see how the meeting will go and if it will calm the situation between the two countries.

In FX, the Yen rose against most other currencies. USD/JPY came under pressure again, and could soon test 110.00. A break below would be quite bearish and signal a move towards 108. Other than that, price action in most currency pairs was quiet. Several key markets in Asia were closed for a holiday today, so volumes were lower than usual.

Upcoming Events:

- 09:30 GMT – UK Construction PMI

- 10:00 GMT – Euro Zone Retail Sales

- 10:15 GMT – RBA Governor Lowe speaks

- 13:30 GMT – Canadian Trade Balance

- 14:30 GMT – ECB President Draghi speaks

- 15:00 GMT – US Factory Orders