Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD was indecisive yesterday. The bias remains bearish in nearest term testing 1.0600 area. Immediate resistance remains at 1.0700. A clear break above that area could lead price to neutral zone in nearest term but only a clear break back above 1.0750 would interrupt the current short-term bearish bias following the appearance of a “shooting star” formation on daily chart last week. On the downside, a clear break and daily close below 1.0600 would expose 1.0500 this week. Overall I remain neutral.

GBPUSD

The GBPUSD had a bearish momentum yesterday bottomed at 1.2465. The bias is bearish in nearest term testing the lower line of the bullish channel as you can see on my H1 chart below located around 1.2450 area. A clear break below that area would expose 1.2400 – 1.2375 region. Immediate resistance is seen around 1.2515/30 area. A clear break back above that area could lead price to neutral zone in nearest term but would keep the short-term bullish bias remains alive and kicking testing 1.2615 region. Overall I remain neutral.

USDJPY

The USDJPY had a bearish momentum yesterday bottomed at 110.85 and hit 110.55 earlier today in Asian session. The bias is bearish in nearest term testing 110.10 key support. A clear break and daily close below that area would expose 108.50 region this week and establish a longer term bearish trend with 111.30 – 112.00 as key resistance. Immediate resistance is seen around 111.30. A clear break and daily close back above that area would keep the “hammer” bullish reversal scenario remains alive and kicking testing 112.00 or higher.

USDCHF

The USDCHF was indecisive yesterday. The bias remains bullish in nearest term testing 1.0060 but as you can see on my H4 chart below we have a CCI bearish divergence suggests a potential bearish pullback especially if price breaks below 0.9990 testing 0.9950 or lower. On the upside, a clear break and daily close above 1.0060 would expose 1.0120 or higher. Overall I remain neutral.

(RBA) Statement by Philip Lowe, Governor: Monetary Policy Decision

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

Conditions in the global economy have improved over recent months. Both global trade and industrial production have picked up. Labour markets have tightened in many countries. Above-trend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by higher spending on infrastructure and property construction. This composition of growth and the rapid increase in borrowing mean that the medium-term risks to Chinese growth remain. The improvement in the global economy has contributed to higher commodity prices, which are providing a significant boost to Australia's national income.

Headline inflation rates have moved higher in most countries, partly reflecting the higher commodity prices. Core inflation remains low. Long-term bond yields are higher than last year, although in a historical context they remain low. Interest rates have increased in the United States and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively.

The Australian economy is continuing its transition following the end of the mining investment boom. Recent data are consistent with ongoing moderate growth. Most measures of business confidence are at, or above, average and non-mining business investment has risen over the past year. At the same time, some indicators of conditions in the labour market have softened recently. In particular, the unemployment rate has moved a little higher and employment growth is modest. The various forward-looking indicators still point to continued growth in employment over the period ahead. Wage growth remains slow.

The outlook continues to be supported by the low level of interest rates. Lenders have recently announced increases in mortgage rates, particularly those paid by investors. Financial institutions remain in a good position to lend. The depreciation of the exchange rate since 2013 has also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment.

Inflation remains quite low. Headline inflation is expected to pick up over the course of 2017 to be above 2 per cent. The rise in underlying inflation is expected to be a bit more gradual with growth in labour costs remaining subdued.

Conditions in the housing market continue to vary considerably around the country. In some markets, conditions are strong and prices are rising briskly. In other markets, prices are declining. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Growth in rents is the slowest for two decades.

Growth in household borrowing, largely to purchase housing, continues to outpace growth in household income. By reinforcing strong lending standards, the recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness. Lenders need to ensure that the serviceability metrics that they use are appropriate for current conditions. A reduced reliance on interest-only housing loans in the Australian market would also be a positive development.

Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

Australian SPI200 Breakout And Retest

The Australian SPI200 index has finally broken through the resistance level that we watched go from a double top to a triple top over the last month or so.

SPI200 Daily:

As you can see clearly on the daily chart above, price has broken through the level and has pulled back to retest the broken support as resistance.

TO THE PIP!

This is the sort of thing that keeps me coming back to technical analysis time and time again.

Just keep an eye on the economic calendar with today's RBA rate decision likely to be a little more lively than the most recent decisions thanks to the resurgence of Sydney/Melbourne house prices chatter.

Elliott Wave Trade Ideas Performance Update

The long position entered in EUR/GBP at 0.8620 finally met our upside upside at 0.8720 as the pair rebounded to 0.8735, however, euro ran into renewed selling interest there and the pair then tumbled from there to as low as 0.8485 late last week.

A short position was entered in USD/CAD at 1.3340, however, as the greenback continued finding decent demand just above previous support at 1.3278 (last week’s low) and has rebounded, we exited the position earlier today at 1.3359 with small loss.

The long positions entered in AUD/USD the week before at 0.7645 is still holding at the moment.

In short, 3 positions were entered with total profit of 81 points and the positions are listed below.

22 Mar: AUD/USD - Long at 0.7645,

23 Mar: EUR/GBP - Long at 0.8620, exited at 0.8720 (+ 100 points)

31 Mar: USD/CAD - Short at 1.3340, exited at 1.3359 (- 19 points)

| AUD EUR/JPY EUR/GBP CAD

Jan - 15 -275 - 35 -120

Feb + 140 -17 - 40 +11

Mar + 20 +115 +132 - 19

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Y-T-D + 145 - 177 + 57 + 38

Candlesticks and Ichimoku Trade Ideas Performance Update

We sold dollar against yen last week at 111.20 and although the pair retreated from 111.32, the greenback found renewed buying interest at 110.72 and rebounded again, we exited the position with small profit at 111.00 and price eventually rose to as high as 112.20 before dropping again.

We also sold dollar against euro and Swiss franc last week, a long position was entered in EUR/USD at 1.0800 and a short position was entered in USD/CHF at 0.9910, both positions ended with different levels of loss as the greenback reversed previous weakness.

No position was entered in cable last week.

In short, 3 positions were entered among all 4 currency pairs with total loss of 38 points and the position are listed below:

29 Mar : USD/JPY - Short at 111.20, exited at 111.00 (+ 20 points)

29 Mar : EUR/USD - Long at 1.0800, exited at 1.0765 (- 35 points)

29 Mar : USD/CHF - Short at 0.9910, exited at 0.9933 (- 23 points)

| JPY EUR CHF GBP

Jan + 167 - 85 - 10 + 50

Feb + 200 +150 +93 - 59

Mar -23 -70 -23 - 35

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Y-T-D + 344 - 10 +60 -44

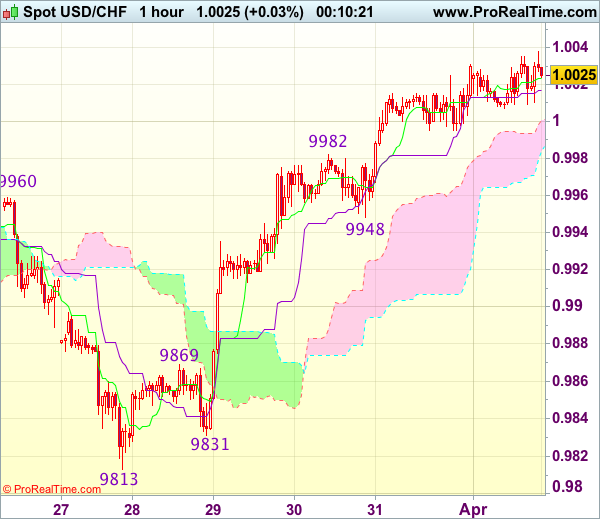

Trade Idea Wrap-up: USD/CHF – Buy at 0.9950

USD/CHF - 1.0025

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0024

Kijun-Sen level : 1.0017

Ichimoku cloud top : 1.0001

Ichimoku cloud bottom : 0.9984

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has continued trading with a firm undertone, suggesting recent rise from last week’s low at 0.9813 is still in progress and bullishness remains for this move to extend gain to previous support at 1.0060 (now resistance), however, loss of upward momentum should prevent sharp move beyond resistance at 1.0109, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as said support at 0.9948 should limit downside. Below 0.9931 (50% Fibonacci retracement of 0.9831-1.0031) would abort and signal top is formed instead, bring correction to 0.9905-10 (61.8% Fibonacci retracement) but reckon previous resistance at 0.9869 would hold from here.

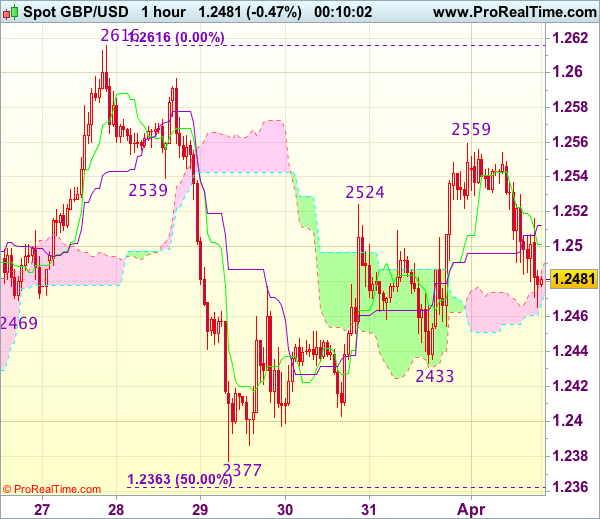

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2482

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2501

Kijun-Sen level : 1.2512

Ichimoku cloud top : 1.2486

Ichimoku cloud bottom : 1.2468

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable has retreated after meeting resistance at 1.2559 on Friday on active cross-trading in sterling and consolidation with mild downside is seen for weakness to 1.2450-55, break of support at 1.2433 is needed to signal top has been formed at 1.2559, bring further fall towards 1.2400-05. Looking ahead, only a drop below 1.2400-05 would signal the rebound from 1.2377 has ended, bring retest of 1.2377 first.

In view of this, would not chase this fall here and would be prudent to stand aside for now. Above 1.2515-20 would bring another bounce towards 1.2559 but break there is needed to signal the erratic rise from 1.2377 (last week’s low) is still in progress and may extend gain towards 1.2570-75, however, as broad outlook remains consolidative, reckon upside would be limited to 1.2595-00 and price should falter below last week’s high at 1.2616.

WTI Crude Oil Hugging $50 at Start of Week

West Texas crude has started the trading week quietly, as the pair trades just above the symbolic $50 in the North American session. On the release front, there is just one major release on the schedule. ISM Manufacturing PMI dropped to 57.2, matching the forecast.

It was a month to forget for crude, as prices sagged 6.0 percent. Weak oil prices is not the scenario that OPEC scripted, as its landmark deal to cut production was supposed to send crude above $60 a barrel and beyond. Instead, prices have fallen since the deal took effect on January 1. OPEC members have kept to the deal, as compliance levels have been exemplary. Still, the world remains awash in oil, as increasing US production has offset the OPEC cuts. US Crude Inventories continue to show surpluses, most of which have been higher than the forecast. Last week, US crude inventories have reached an all-time high of 534.0 million barrels, so oil prices may have trouble staying above the $50 level.

Donald Trump's young presidency has been rocky, with Trump's controversial statements and actions making headlines almost daily. The battles with the media continue, an economic policy remains a mystery, and Trump suffered a major setback as he couldn't even muster a vote over his healthcare bill. Despite these hiccups, the US economy hasn't missed a beat in 2017. The CB consumer confidence report soared to 125.6 in March, and strong consumer confidence levels should translate into increased consumer spending. GDP for the fourth quarter was revised to 2.1%, up from 1.9% in the previous GDP report. This points to strong growth for the economy,

The discussions around the monetary policy tables are not whether the Fed will raise rates, but rather how many times will the Fed press the rate trigger in 2017. The Fed has forecast two more hikes this year, but the markets are looking for three hikes, and the US dollar took a hit last week as the markets were disappointed with the Fed's dovish rate statement. The Fed will release the minutes of its March meeting on Wednesday, and the markets will be looking for clues as to the timing of a possible rate hike.

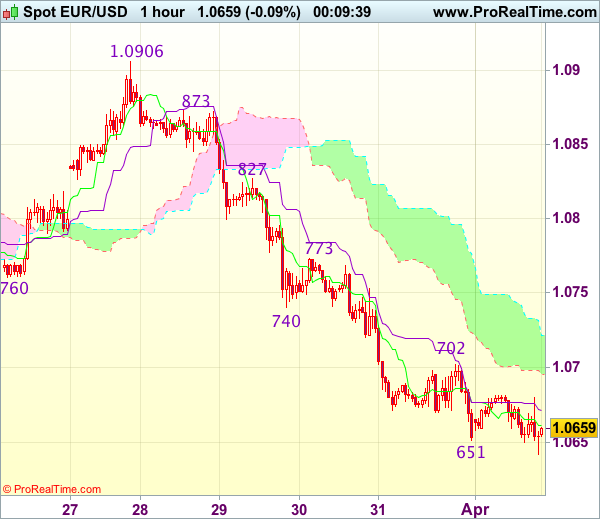

Trade Idea Wrap-up: EUR/USD – Sell at 1.0740

EUR/USD - 1.0658

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0661

Kijun-Sen level : 1.0672

Ichimoku cloud top : 1.0722

Ichimoku cloud bottom : 1.0695

Original strategy :

Sell at 1.0740, Target: 1.0625, Stop: 1.0775

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0740, Target: 1.0625, Stop: 1.0775

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after last week’s selloff, suggesting the decline from 1.0906 top is still in progress and bearishness remains for this fall to extend further weakness to 1.0620-25, then test of previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 first, otherwise, risk from there is seen for a rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0735-40 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

BoC Survey Joins List of Indicators Pointing to Stronger Canadian Economy

Highlights:

- The future sales measure inched lower but remained above its long-run average the long-run average. The 'indicators of future sales' measure rose to a 5-year high.

- Hiring intentions rose for a third consecutive quarter and business machinery and equipment investment intentions jumped to their highest level since Q3 2010 (and matched the second-highest level on record)

- Capacity pressures tightened modestly although indicators of labour shortages eased.

- 94% of respondents expected inflation in the 1% to 3% Bank of Canada target range. That is up from 89% in Q4/16 and with the increase reflecting more respondents expecting growth in the top 2%-3% half of the range.

- Credit conditions eased modestly both from the borrower's perspective and the lender's perspective (from the concurrently released Senior Loan Officer Survey)

Our Take:

The data from the Q1 BOS remains consistent with earlier indicators (GDP growth, for example, is on track to outpace U.S. growth for a third consecutive quarter in Q1/17) pointing to a firming in the Canadian economic backdrop. Expectations for future sales growth moderated but held above long-run average levels and hiring intentions improved for a third consecutive quarter (consistent with strong labour market improvement to-date in 2017). Perhaps most encouragingly, business investment intentions surged to their highest level since Q3 2010, and matched the second-highest reading on record, despite reports of significant uncertainty around the outlook tied to potential trade disruptions and changes to U.S. taxation that could hurt Canadian competitiveness. The business investment intentions in the BOS survey are in sharp contrast to a pull-back in private business investment intentions in a closely-watched annual CAPEX intentions survey from Statistics Canada. The indicator of labour market shortages did tick lower but overall capacity pressures tightened slightly. Bank of Canada Governor Poloz remained adamant last week that, notwithstanding a run of good economic data, the economy continues to run well-below its long-run production capacity. Today's BOS report will not necessarily change the Bank's view ahead of next week's policy decision; however, the longer the run of stronger economic data persists, the harder that position will be to defend.