Sample Category Title

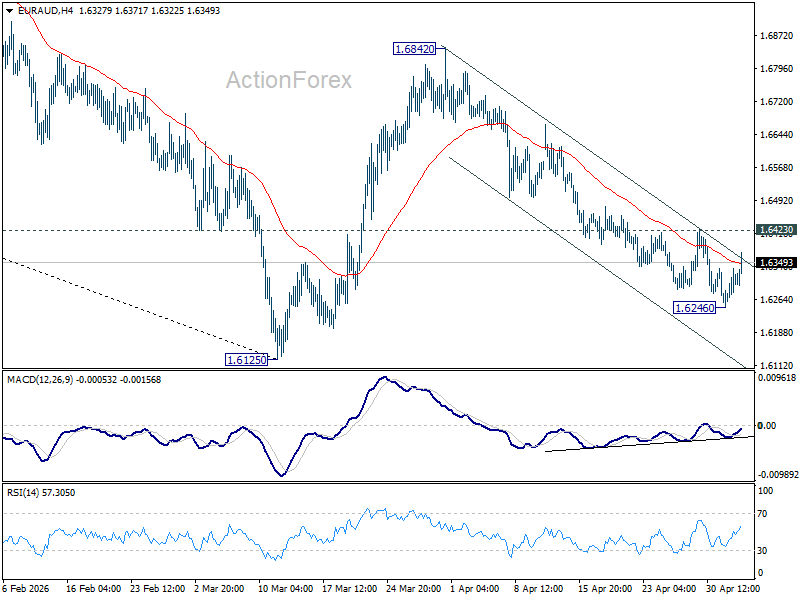

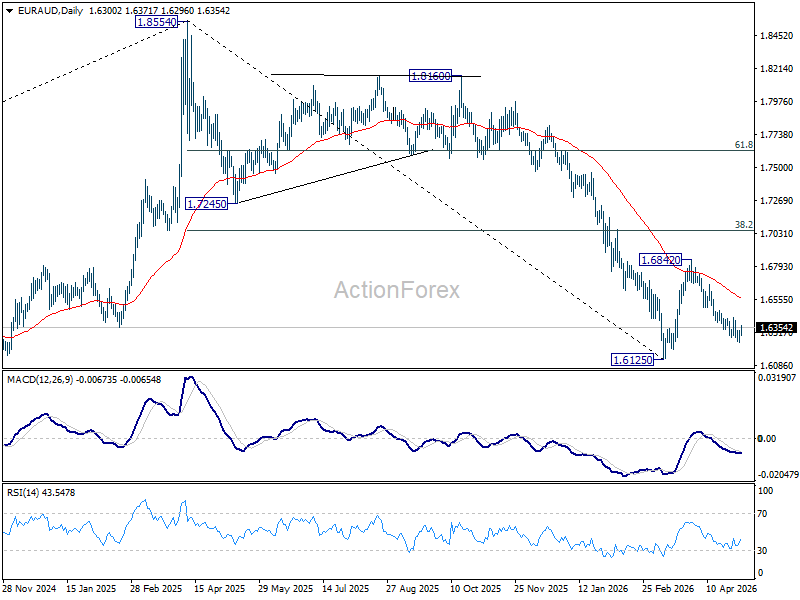

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6265; (P) 1.6301; (R1) 1.6348; More...

Intraday bias in EUR/AUD is turned neutral with current recovery. Further fall is expected as long as 1.6423 resistance holds. Below 1.6246 will bring retest of 1.6125 low. Decisive break there will resume whole fall from 1.8554. However, considering bullish convergence condition in 4H MACD, firm break of 1.6423 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.6560).

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7069) holds, even in case of strong rebound.

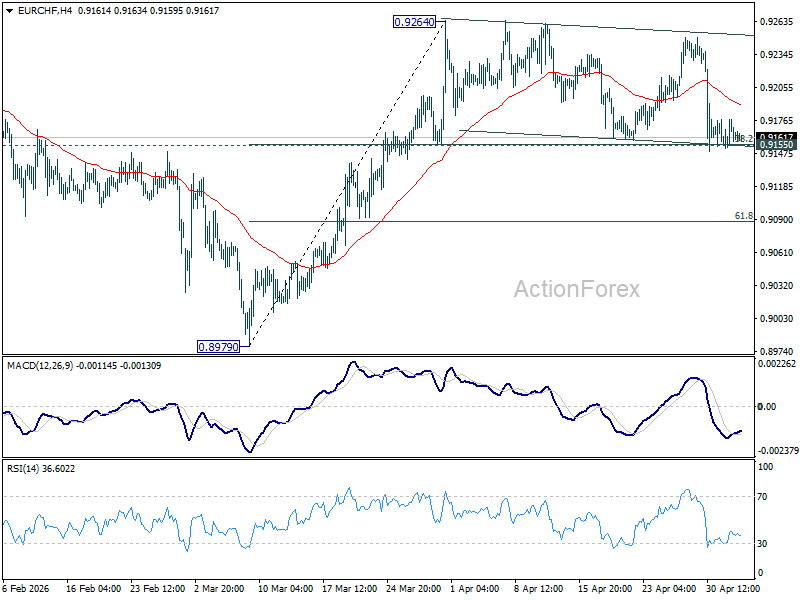

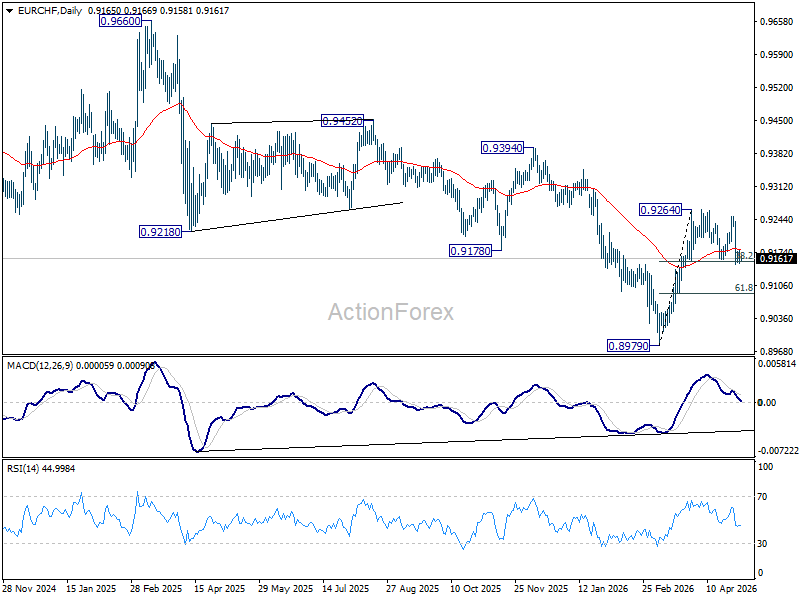

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9153; (P) 0.9167; (R1) 0.9178; More....

Range trading continues in EUR/CHF and intraday bias remains neutral. Rise from 0.8979 is expected to continue as long as 0.9155 cluster support (38.2% retracement of 0.8979 to 0.9264 at 0.9155) holds. On the upside, firm break of 0.9264 will target 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback to 61.8% retracement at 0.9088 and possibly below.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9268) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

Sunrise Market Commentary

Markets

Iran Foreign Minister Araghchi likened the US’s “Project Freedom” in the Persian Gulf to “Project Deadlock”. Since US President Trump announced plans to help commercial vessels through Hormuz, the number of reported military incidents went up reaching amongst the largest levels since the start of the cease-fire about a month ago. Brent crude went from opening levels near $106.5/b to currently $113. When asked about how long the situation would still last, President Trump returned to his answer of choice since the very beginning of the war: “two weeks, maybe three”. Yesterday’s events clearly raised the probability that the fragile cease-fire might snap. Defense Secretary Hegseth and Joint Chiefs of Staff Chairman Caine will hold a news conference later today.

Yesterday’s trading was skinned by public holidays in Japan, China and the UK. Markets nevertheless marched to the drums of the higher oil price. Risk sentiment took a hit with key European indices losing up to 2% for the EuroStoxx50. Main US benchmarks lost between -0.2% (Nasdaq) and -1.15% (Dow). Core bond yield curves extended the bear flattening process. EU swap rates added between 8.8 bps (2-yr) and 3.6 bps (30-yr). The EU 2y swap rate managed its highest closing level (2.94%) since July 2024 as money markets add to ECB tightening bets this year. With a 25 bps June rate hike almost fully discounted, that means adding to cumulative tightening bets for this year. Currently markets are swinging back a total of 3-4 moves. An avalanche of ECB speakers hit the wire with Governing Council member Kazimir bluntly saying that policy tightening in June is “all but inevitable”. ECB vice president de Guindos suggested that the war shock affected inflation more than growth with Bundesbank Nagel adding that a rate hike would come without marked improvement in price outlook. Recall that ECB President Lagarde suggested last week that “we’re certainly moving away” from the base scenario. ECB Simkus said it’s clear we’re talking about a possible hike in June. Other ECB members were less committed for now. US Treasuries yesterday followed the bear flattening with yields ending the day 7.5 bps (2-yr) to 5.6 bps (30-yr) higher. The former extends the trend that started after last week’s hawkish hold by the Fed. US money markets are back to erring on the side of a rate hike instead of a rate cut on a 12-month horizon. The US 30-yr yield closed at 5.02%, the highest the summer of 2025 as US risk premia start building again. Fitch over the weekend warned for US deficits just shy of 8% of GDP for this year and next. On FX markets, the dollar profited from the set-up with EUR/USD returning below 1.17. Today’s eco calendar contains US services ISM and JOLTS job openings but we don’t expect them to break the market reaction function to developments in the Middle East (higher oil, bear flattening, stronger USD, weak risk sentiment).

News & Views

The Reserve Bank of Australia this morning raised the policy rate by 25 bps to 4.35%. It was the third consecutive hike and was supported by a 8-1 majority (one vote for unchanged). The decision comes as inflation had already picked up materially in H2 2025 with information since the start of the year still reflecting capacity pressures. Higher fuel and commodity prices from the conflict in the Middle East now add to inflationary pressures as many firms are experiencing cost pressures and are looking to increase prices of goods and services. Even in a baseline scenario assuming that the conflict is resolved soon and fuel prices decline, the RBA sees inflation peaking higher than expected in February (4.8% end H1). Trimmed mean inflation is expected to peak at 3.8% with both measures expected to return to 2.5% by June 2028. The RBA still sees risks to inflation tilted to the upside. After three consecutive hikes, it is now well placed to respond to developments and the Board is focused on its mandate to deliver price stability and full employment. Money markets now discount one additional rate hike by end summer/autumn. The reaction to the decision is mild. The 3-y government bond yield eases 2.3 bps (to 4.64%). After filling offers north of AUD/USD 0.72 over the previous days, the Aussie dollar this morning eases slightly (0.715).

The US Treasury raised its estimate for borrowing in the current April-June quarter to $189bn. The amount is $79bn higher than in the estimate of February. The upward revision was mainly due to lower projected net cashflows, but this was partially mitigated by a higher cash balance at the start of the quarter. For the July–September 2026 quarter, Treasury expects to borrow $671bn in privately-held net marketable debt, assuming an end-of-September cash balance of $950bn. During the January–March 2026 quarter, Treasury borrowed $577bnin privately-held marketable debt and ended the quarter with a cash balance of $893bn compared with estimates of $574bn borrowing and an assumed an end-of-March cash balance of $850bn in the February projection. Additional details on the refinancing will be released tomorrow.

Narrative Flips from AI to Middle East

Yesterday, the US announced it would escort ships through the Strait of Hormuz — calling it a humanitarian operation (!) Iran warned it would retaliate, and reports suggest the US went ahead regardless. Iran then struck ships and key oil infrastructure in Fujairah, UAE — notably a terminal that allows exports bypassing the Strait. Unsurprisingly, oil prices spiked, with US crude nearing $110pb and Brent $115pb. This morning, uncertainty remains high, though prices have eased slightly.

The pattern is familiar: the $115–120pb range is acting as strong resistance — above this level, the market shifts from pricing supply constraints to pricing demand destruction. That brings rising inflation expectations, more hawkish central bank expectations and higher yields — all of which were triggered yesterday.

The US 2-year yield jumped near 4%, while the 30-year yield breached 5%. European 10-year benchmark yields also moved higher.

As a result, the dominant market narrative flipped from AI optimism to Middle East tensions. The US dollar index rebounded past its 200-DMA, while gold eased toward $4’500, pressured by the stronger dollar and rising yields, which increase the opportunity cost of holding non-yielding assets. I believe gold’s muted reaction also reflects the speculative positioning built up ahead of the crisis. That said, gold remains well supported in the current geopolitical backdrop, with central banks reportedly continuing to accumulate on dips.

Elsewhere, the Reserve Bank of Australia (RBA) delivered its third straight rate hike — in line with expectations — to rein in inflation. The AUDUSD nevertheless eased, pressured by a broadly stronger US dollar driven by geopolitical tensions and higher oil prices. The EURUSD is testing its 200-DMA to the downside, while USDJPY is consolidating just below its 100-DMA.

FX moves will likely remain driven by the US dollar in the near term. The higher the tensions, the higher oil prices, and the stronger the dollar. A stronger dollar raises imported inflation globally, reinforcing expectations for tighter monetary policy. That, in turn, weighs on risk appetite.

As such, major US and European indices retreated. The Stoxx 600 was also hit by a notable selloff in European carmakers on reports that Trump would impose a 25% tariff, arguing Europeans are not complying with trade agreements. Europeans deny. The situation remains legally and politically unclear, anyway.

But forget about the tariffs for a second. The broader issue is structural: European carmakers will struggle to replace US demand, as the US continues to restrict Chinese EV penetration. Outside these regions, markets are increasingly open to Chinese EVs, which are cheaper and often more advanced. Meanwhile, higher fuel prices accelerate the global EV transition.

To me, European carmakers will remain under pressure with or without US market access — without it, the unravelling would simply be faster.

On oil, renewed tensions and damage to infrastructure should keep upward pressure in place. A spike above $120pb is possible, but unlikely to be sustained — at those levels, demand destruction typically kicks in and caps further gains.

Voilà, that’s it for the big picture.

The recent spike in oil prices is weighing on European futures this morning, while Nasdaq futures are in positive territory.

After the bell yesterday, Palantir Technologies reported an 85% jump in Q1 sales year-on-year, driven by strong US military demand. Alas, solid results and guidance were not enough — the stock fell in after-hours trading.

Today, AMD heads into earnings with expectations for ~30%+ year-on-year growth, driven by AI and data centre demand. But the bar is high: after a rally of more than 85% since late March, the key question is whether AMD can deliver a convincing beat, particularly against Nvidia’s dominance and ongoing supply constraints.

Nvidia, for its part, is starting to face growing competition — from AMD, as well as custom chips developed by hyperscalers like Amazon and Google.

So far, none have matched Nvidia’s full-stack ecosystem — especially its CUDA software moat — which keeps it firmly in the driver’s seat. But a shift is underway between training and inference. Training large models remains compute-heavy and tightly tied to Nvidia’s ecosystem. Inference, however, is about cost, efficiency and scale — and that’s where competition intensifies, with solutions like Google’s TPUs and Amazon’s Inferentia chips.

Anyway, let’s see how AMD’s earnings resonate — and whether they can help offset the geopolitical noise.

US-Iran Tensions Rise, RBA Hikes Rates to Counter Inflation

In focus today

Today will be quiet in terms of data releases, with only US data releases on the calendar. In the afternoon, the April ISM Services Index and March JOLTs job openings will be released. Especially, the latter is a key indicator of labour demand for the Fed. It will be interesting to see how March figures compare to February, when JOLTS job openings fell to 6.882m, with the job openings-to-unemployment ratio dropping to 0.9, signalling weaker wage growth ahead.

Economic and market news

What happened overnight

In Australia, the Reserve Bank of Australia (RBA) hiked rates by 25bp, bringing the policy rate to 4.35%. This marks the third increase in 2026, as the RBA responds to sustained inflationary pressures. While higher energy prices driven by Middle East tensions are a key factor, stronger-than-expected domestic demand and capacity constraints are also contributing. Inflation remains elevated, with second-round effects emerging, reinforcing the RBA's commitment to restoring price stability.

Tensions in the US-Iran conflict intensified as Iran launched missile and drone attacks on the UAE, igniting a fire at a petroleum industrial site and prompting the UAE to intercept multiple projectiles. In response, the US reported sinking six Iranian boats in the Strait of Hormuz. Amidst these developments, US forces reportedly cleared paths for two vessels through the strait, with Mærsk confirming its US-flagged Alliance Fairfax transited under military protection. Tehran condemned the move as a violation of the ceasefire. Energy markets remain volatile, with Brent crude prices at 113 USD/bbl, reflecting persistent supply concerns. Mounting tensions are testing the fragile ceasefire, with risks to inflation becoming more pronounced.

What happened yesterday

In the euro area, the ECB's quarterly Survey of Professional Forecasters (SPF) revealed higher inflation expectations, but lower growth projections compared to the previous survey. Inflation is projected at 2.7% y/y for 2026 and 2.1% y/y for 2027, while GDP growth for 2026 has been revised down to 1.0% y/y from 1.2% y/y. With minimal changes to long-term inflation expectations, the report offers limited support for rate hikes and leans slightly dovish. Inflation forecasts may have a downward bias, as the survey was conducted during the two-week ceasefire announcement. Forecasts assumed USD oil prices of 94 in Q2, 85 in Q3, and 80 in Q4, while Brent oil prices fell sharply during the survey period, dropping from 120 USD/bbl on 31 March to 90 USD/bbl by 8 April.

In Denmark, the central bank did not intervene in the FX market in April, even as EUR/DKK reached a new historic high of 7.4735. Its steady approach toward the recent upward trend in EUR/DKK suggests that it may allow the currency pair to rise further if upward pressure resumes. Additionally, the lack of intervention in FX markets indicates that the likelihood of a unilateral rate hike in Denmark this year remains low, in our view.

In Sweden, manufacturing PMI increased to 57.2 in April. Input prices surged to 81.3, its highest level since 2022. Despite this increase, the report revealed declines in new orders and production. Delivery times lengthened, which typically boosts PMI as longer delivery times often signal strong demand. However, it is likely that the current increase in delivery times is primarily due to supply chain disruptions rather than heightened demand.

Equities: Equities were lower yesterday. S&P 500 -0.4% and Stoxx 600 -1% in a volatile session, characterized by Iran headlines. This was a de-risking session in equities, with almost all sectors lower but tech and energy. Defensive stocks outperformed, including health care and tech while industrials, materials and consumer discretionary sold off ~-1%. It is interesting to see tech outperforming even in a defensive session like yesterday, especially as yield were materially higher. This mix would easily have made the tech the worst performing sector three months ago. Instead, software stocks even bounced 2% yesterday, outperforming the market by a meaningful 3pp. This says something about the strength of the latest tech stock rotation. As our readers will know, we see it continuing.

FI and FX: Escalation between the US and Iran sent bond yields higher and USD stronger. Global bond yields rose again as tensions remain high in the Middle East after an escalation of the conflict in the Strait of Hormuz sent oil prices higher. 30Y Treasuries are now trading above 5% and the short-term risk is that yields will grind higher unless some form of deal is reached between Iran and the US. The dollar grinded lower versus the euro, while JPY remains stable given the possibility for currency intervention.

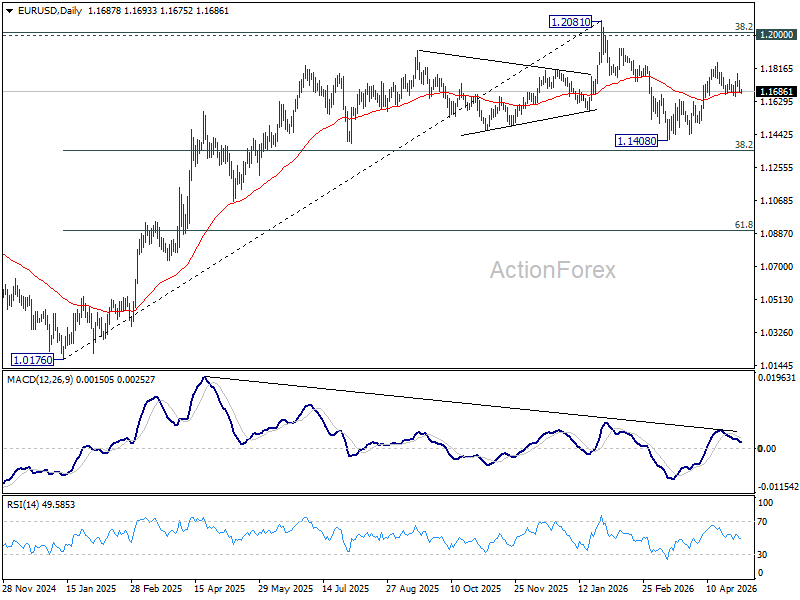

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1664; (P) 1.1707; (R1) 1.1732; More….

Intraday bias in EUR/USD remains neutral and outlook is unchanged. Rise from 1.1408 is expected to continue as long as 1.1642 support holds. Firm break of 1.1848 will target 1.2081 high next. However, firm break of 1.1662 support will indicate the the rebound from 1.1408 has completed, and bring deeper decline back towards this low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1537). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

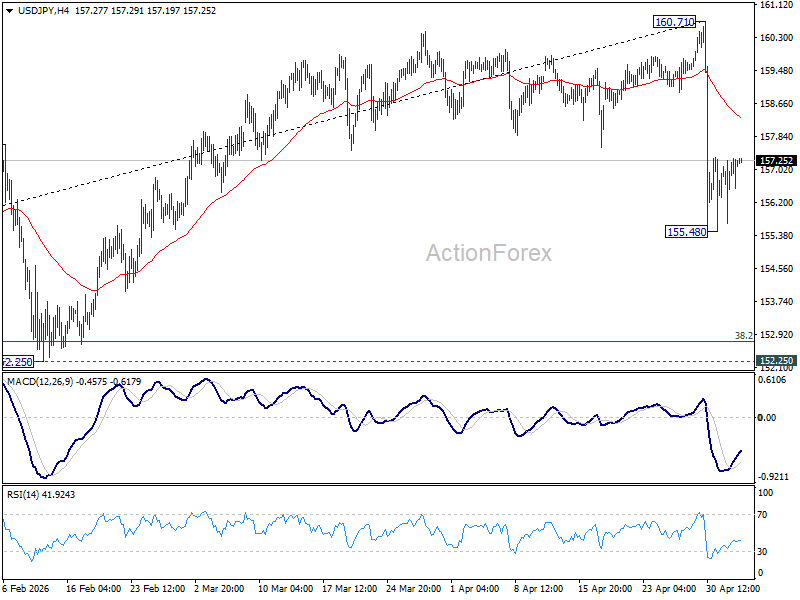

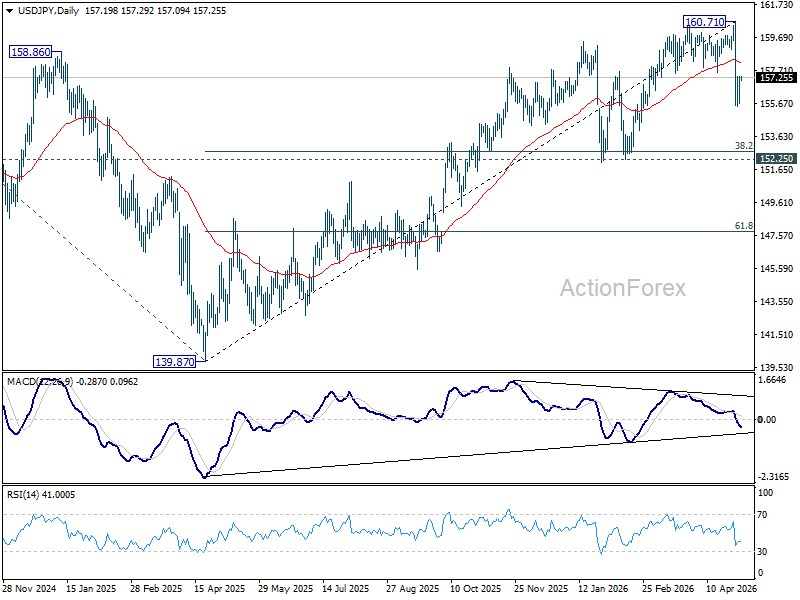

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.22; (P) 156.76; (R1) 157.79; More...

USD/JPY is staying in consolidations above 155.48 and intraday bias remains neutral. Risk will stay on the downside as long as 55 4H EMA (now at 158.29) holds. Below 155.48 will extend the fall from 160.71 and target 152.25 cluster support (38.2% retracement of 139.87 to 160.71 at 152.74).

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.03) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

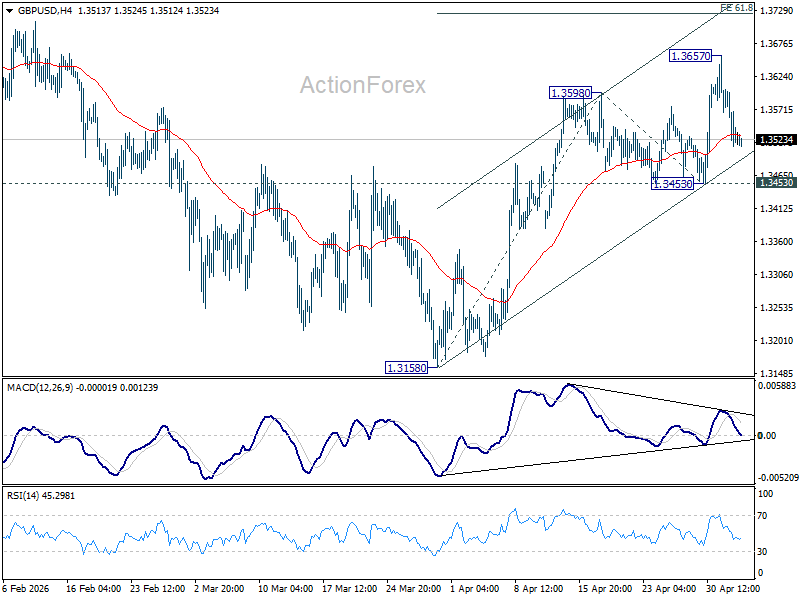

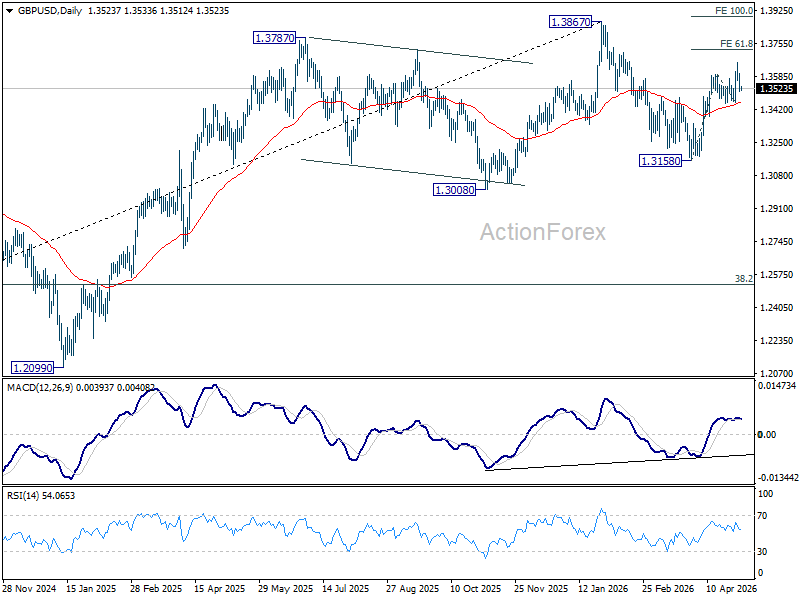

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3542; (P) 1.3601; (R1) 1.3634; More...

Intraday bias in GBP/USD remains neutral and further rise is still expected as long as 1.3453 holds. Above 1.3657 will target 61.8% projection of 1.3158 to 1.3598 from 1.3453 at 1.3725 first. Firm break there will target a retest on 1.3867 high. However, break of 1.3453 will turn bias back to the downside for 1.3158 support instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high).

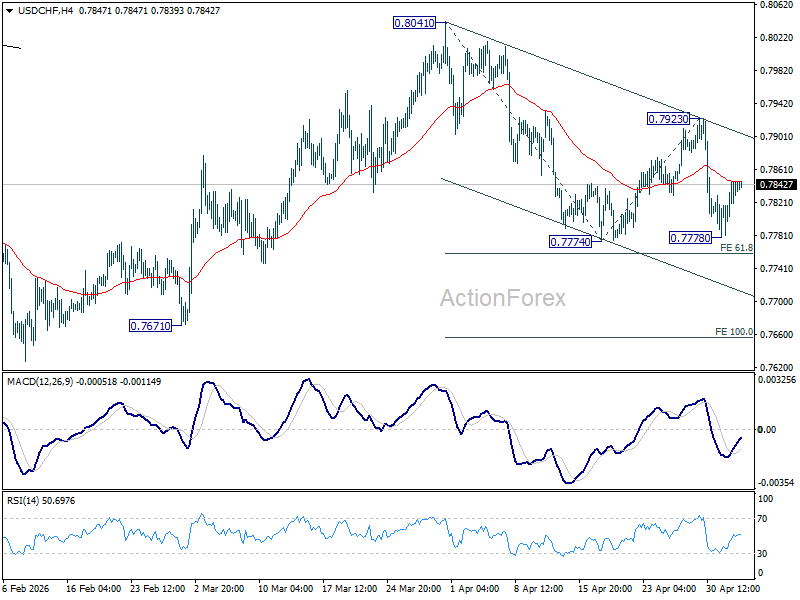

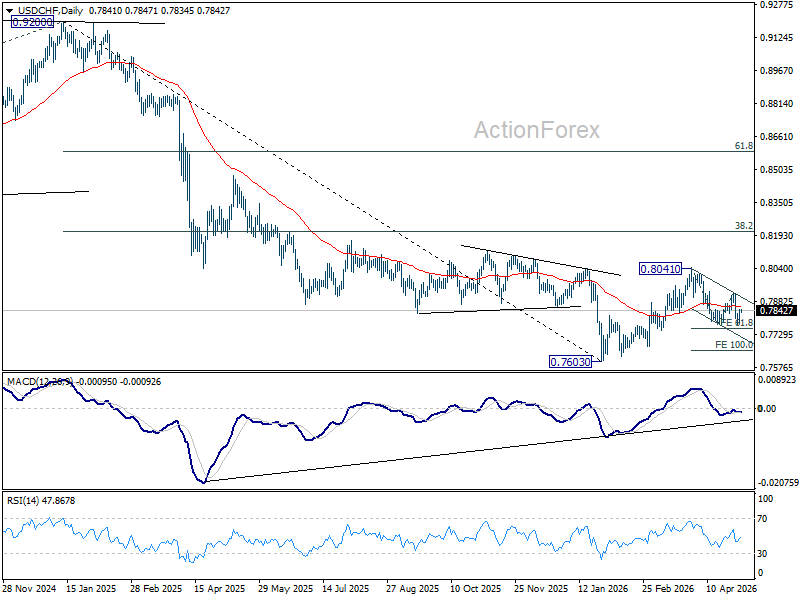

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7808; (P) 0.7829; (R1) 0.7861; More….

Intraday bias in USD/CHF remains neutral and more consolidations could be seen above 0.7778. Risk will remain on the downside as long as 0.7923 resistance holds. Firm break of 61.8% projection of 0.8041 to 0.7774 from 0.7923 at 0.7758 will extend the fall from 0.8041 to 100% projection at 0.7656. However, firm break of 0.7923 will turn bias back to the upside for stronger rebound.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8042) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

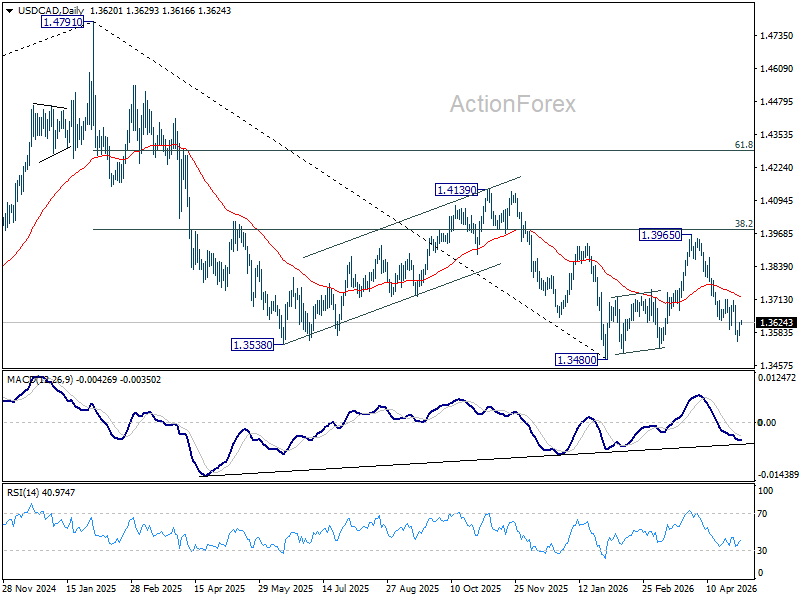

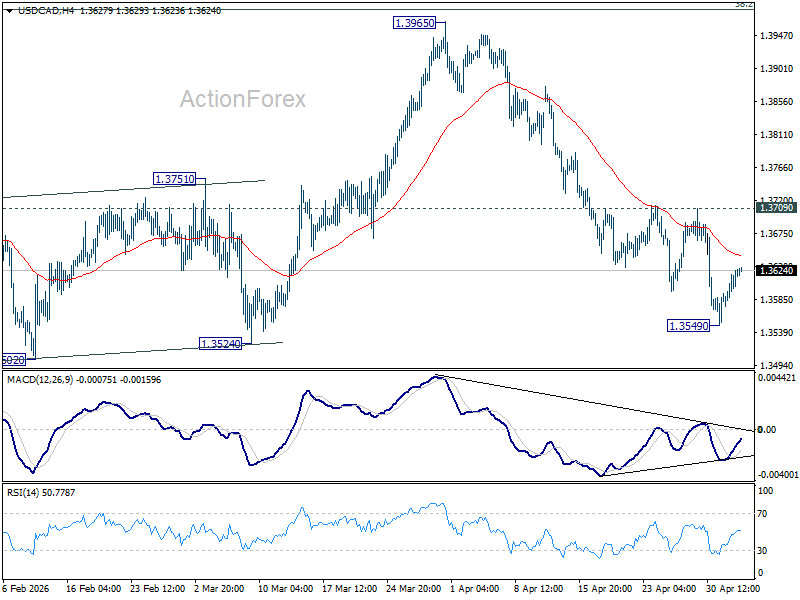

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3594; (P) 1.3611; (R1) 1.3643; More...

Intraday bias in USD/CAD is turned neutral with current recovery, and some consolidations would be seen above 1.3549. Further decline is expected as long as 1.3709 resistance holds. Below 1.3549 will resume the fall from 1.3965 to retest 1.3480 low. Decisive break there will resume whole down trend from 1.4791. However, firm break of 1.3709 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.