Sample Category Title

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6735; (P) 0.6744; (R1) 0.6755; More...

Intraday bias in AUD/USD remains on the upside as current rally continues to 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. For now, risk will stay on the upside as long as 0.6723 minor support holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

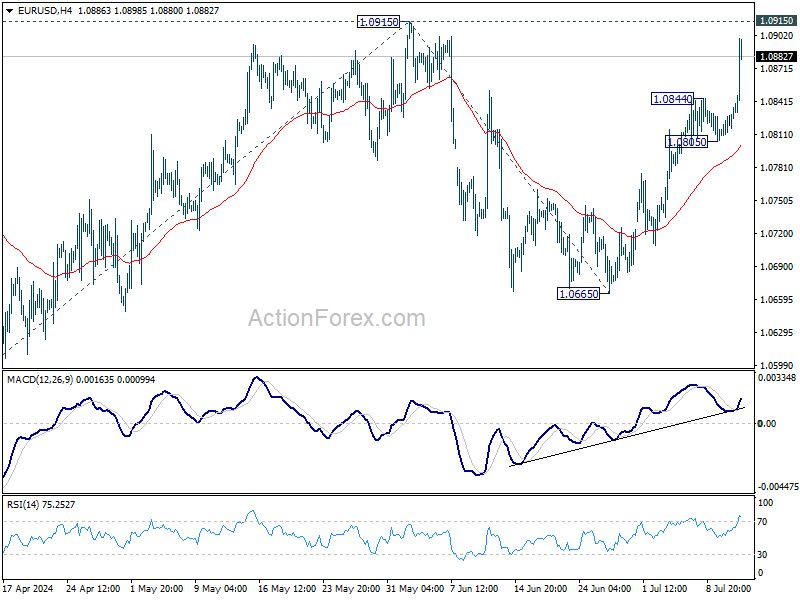

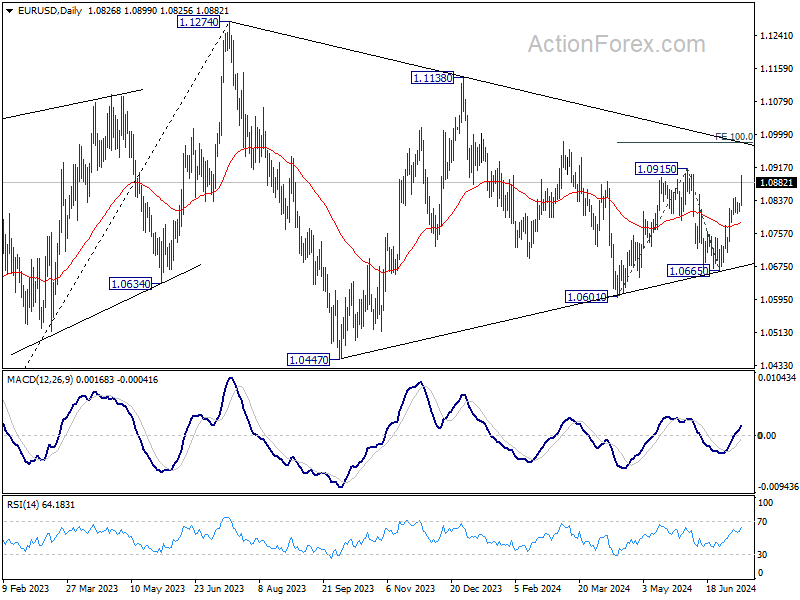

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0817; (P) 1.0824; (R1) 1.0838; More....

EUR/USD's rise from 1.0665 resumed by breaking through 1.0844 temporary top and intraday bias is back on the upside for 1.0915 resistance. Firm break there will resume whole rally from 1.0601 and target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. For now, risk will stay on the upside as long as 1.0805 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that could still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

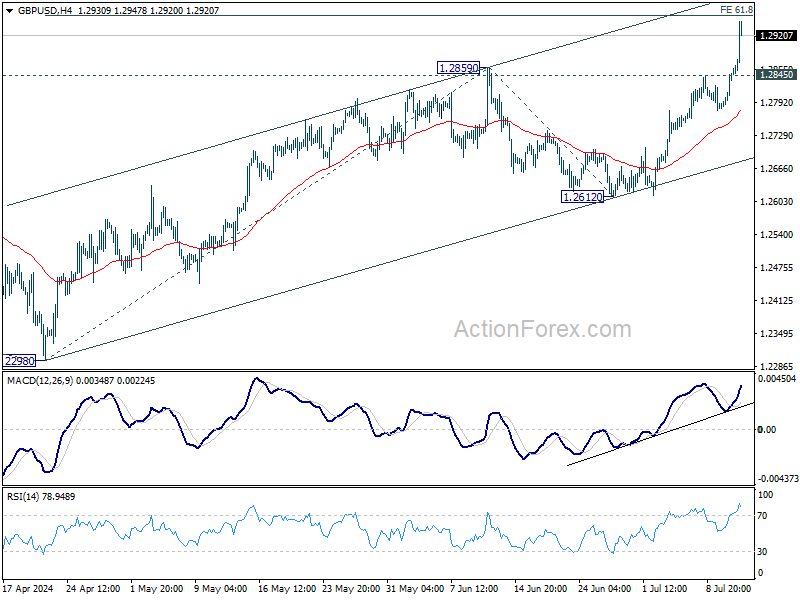

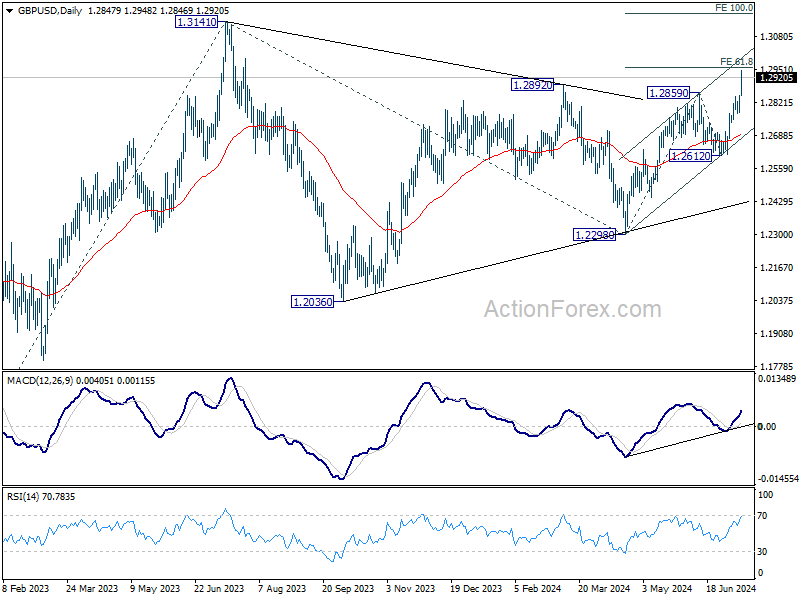

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2800; (P) 1.2825; (R1) 1.2872; More...

GBP/USD's rally continues today and intraday bias stays on the upside for 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959. Decisive break there would prompt upside acceleration through 1.3141 to 100% projection at 1.3173. On the downside, below 1.2845 resistance turned support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 (2023 high) from 1.2298 at 1.4022.

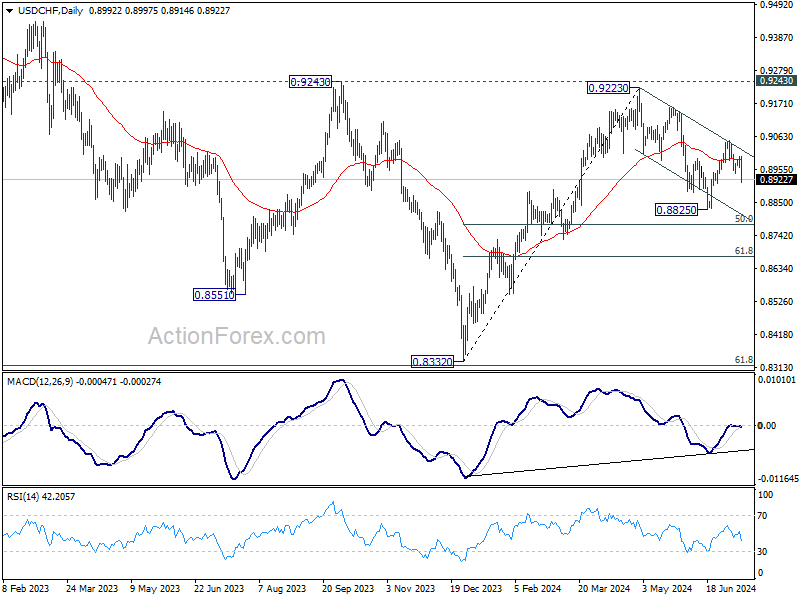

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8973; (P) 0.8987; (R1) 0.9011; More…

USD/CHF's decline from 0.9049 resumed by breaking through 0.8942 support and intraday bias remains is back on the downside for retesting 0.8825. Fall from 0.9223 should be in progress with near term channel intact. Break of 0.8825 will target 50% retracement of 0.8332 to 0.9223 at 0.8778 next. For now, risk will stay on the downside as long as 0.9000 resistance holds, in case of recovery.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

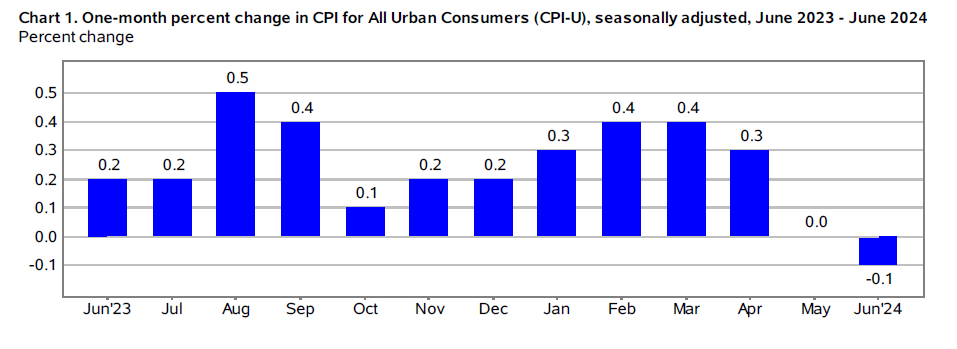

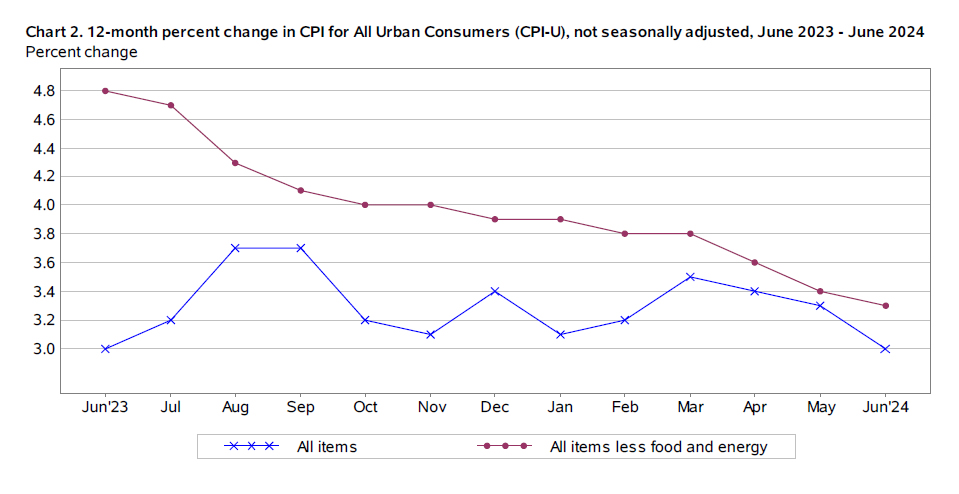

US: Inflationary Pressures Cool Faster than Expected in June, Bolstering Case for September Rate Cut

The Consumer Price Index (CPI) fell 0.1% month-on-month (m/m), below the consensus forecast calling for a modest 0.1% gain. On a twelve-month basis, CPI edged lower by 0.3 percentage points to 3.0%.

- Lower energy prices – largely attributed to a 3.7% decline in gasoline prices – helped to push down on the headline measure. Grocery store prices were up 0.2% on the month and are up a subdued 1.6% y/y.

Excluding food and energy, core prices rose a modest 0.1%, a deceleration from May's already soft 0.16% gain, and considerably below the hotter 0.37% monthly readings averaged through the first three months of the year. The twelve-month change on core slipped by a tenth of a percentage point to 3.3% – the smallest 12-month increase since April 2021.

Core services prices rose by a very subdued 0.1% – its weakest monthly gain since August 2021. This was the result of a notable deceleration in shelter costs – rising 0.2% after averaging monthly gains of 0.4% over the past twelve-month period – and an outright decline in the 'supercore' measure (-0.2%). Notable declines were seen across transportation – largely driven by a sharp 5% pullback in airfares – and recreational services.

Core goods prices fell by a modest 0.1%, thanks to a further pullback in both new (-0.2%) and used (-1.5%) vehicle prices.

Key Implications

This is exactly what the FOMC is looking for. Not only did the supercore measure slip into deflationary territory, but the long-awaited adjustment lower on shelter prices also appears to be underway, while core goods prices also continued to edge lower. Encouragingly, the three-month annualized rate of change on core inflation fell sharply to 2.1% – the softest reading since March 2021.

Speaking at his semiannual Congressional testimony earlier this week, Chair Powell described the May inflation report as 'very good', which would make this morning's report excellent. Should the next two inflation readings remain on the softer side, a September rate cut looks to be very much in play.

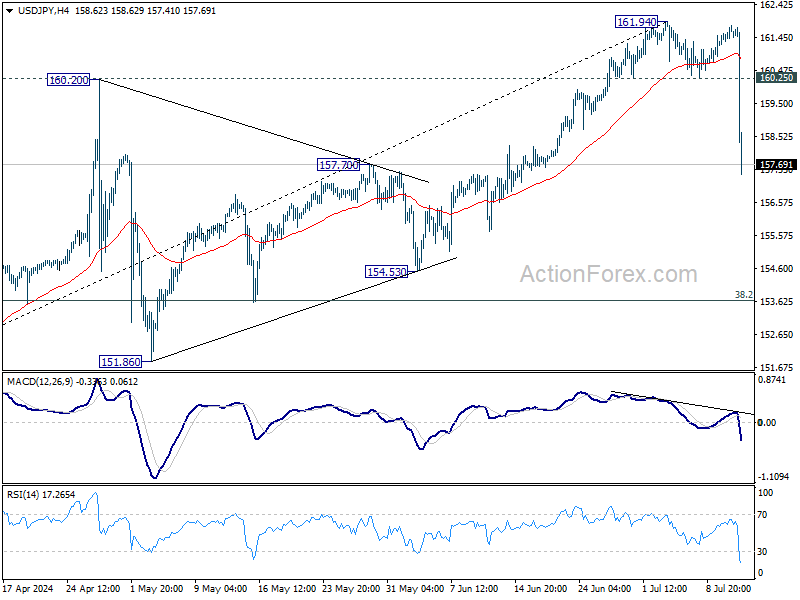

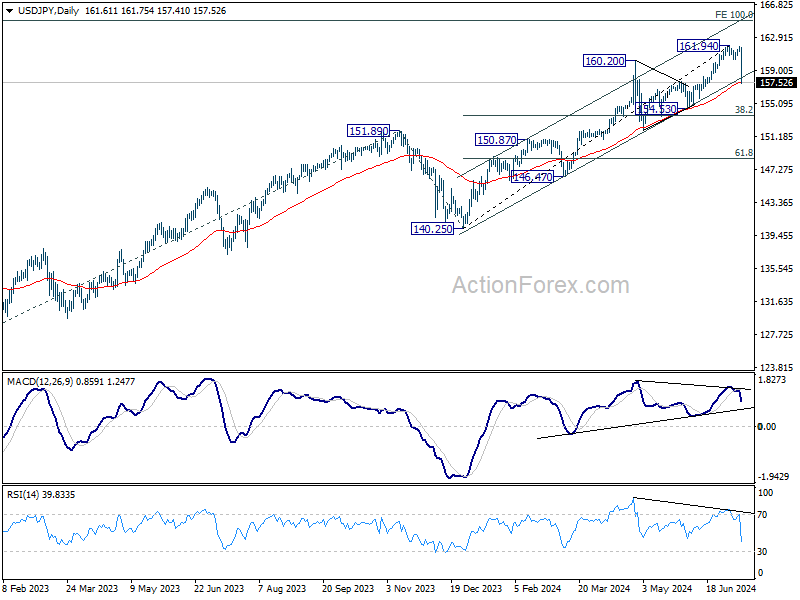

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 161.38; (P) 161.59; (R1) 161.93; More...

USD/JPY declines sharply in early US session and breaks 160.25 support decisively. Considering bearish divergence condition in D MACD, fall from 161.49 might already be correcting the whole five-wave rally from 140.25. Intraday bias is back on the downside. Sustained break of 55 D EMA (now at 157.62) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65. Meanwhile, rise will now stay on the downside as long as 160.25 support turned resistance holds, in case of recovery.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94. However, sustained break of 154.53 will raise the chance of larger scale correction and target 140.25/151.89 support zone.

Fed Sep Cut Now Realistic after US CPI; Japan Intervenes to Boost Yen?

Dollar tumbled sharply in early US session following lower-than-expected consumer inflation readings. Headline CPI showed its first month-over-month decline since early 2023, while core CPI annual rate unexpectedly slowed to its lowest level since April 2021. Now, a September Fed rate cut is becoming a realistic possibility. Fed fund futures are quick to react and are pricing in near 90% chance of that. Indeed, Fed policymakers might start to rethink whether there would be one rate cut or two rate cuts this year.

Simultaneously, Yen surged across the board following US CPI data. The scale of Yen's rally against other currencies suggests that Japan might be capitalizing on the current Dollar weakness to intervene and reverse some of Yen's extended depreciations. Japan has been clear about its readiness to intervene at any time of the day. Also, it has record of acting in the markets strategically, and today's US CPI data gives it a golden opportunity to act. Now, focus is on whether Yen's rebound would spiral further higher with other market participants joining in.

Elsewhere in the currency markets, Sterling is currently the second strongest performer. The pound initially led the pack with a rally on stronger-than-expected UK GDP data but has been overshadowed by the ultra-strong Yen. Dollar is the weakest, followed by Canadian Dollar. Other major currencies are finding their positions amid the current high volatility.

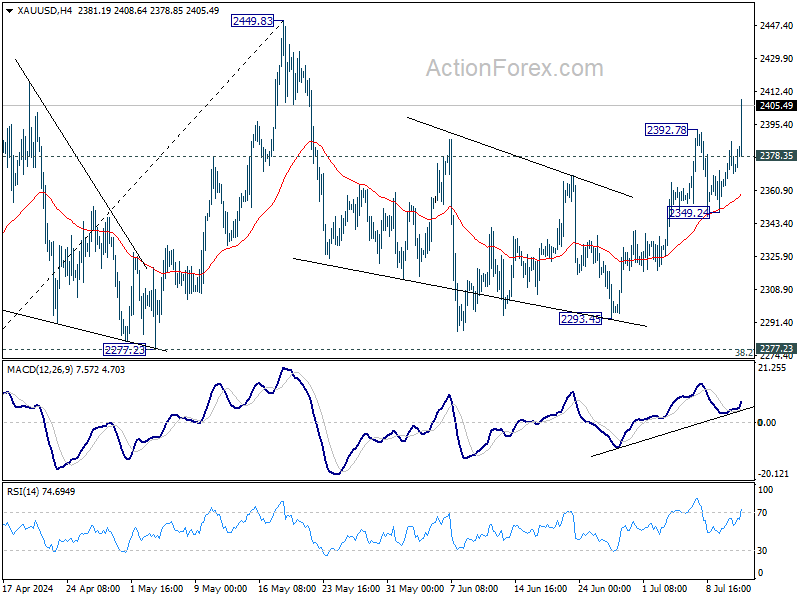

Technically, Gold rally from 2293.45 resumed by breaking through 2392.78 resistance. Current development affirms that case that correction from 2449.83 has completed. Further rise is expected as long as 2378.35 minor support holds. Decisive break of 2449.83 will confirm larger up trend resumption.

In Europe, at the time of writings, FTSE is up 0.36%. DAX is up 0.72%. CAC is up 0.86%. UK 10-year yield is down -0.037 at 4.097. Germany 10-year yield down -0.046 at 2.490. Earlier in Asian, Nikkei rose 0.94%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 1.06%. Singapore Strait Times rose 0.44%. Japan 10-year JGB yield fell -0.0039 to 1.084.

US core CPI slows to 3.3%, lowest since Apr 2021

In June, US CPI fell -0.1% mom, versus expectation of 0.1% mom rise. Core CPI (all items less food and energy) rose 0.1% mom, below expectation of 0.2% mom rise. Energy index fell -2.0% mom while food index rose 0.2% mom.

For the 12-month period, headline CPI slowed from 3.3% yoy to 3.0%yoy, below expectation of 3.1% yoy. Core CPI slowed from 3.4% yoy to 3.3% yoy, below expectation of being unchanged at 3.4% yoy. Core CPI was also the lowest since April 2021. Energy index was up 1.0% yoy while food index was up 2.2% yoy.

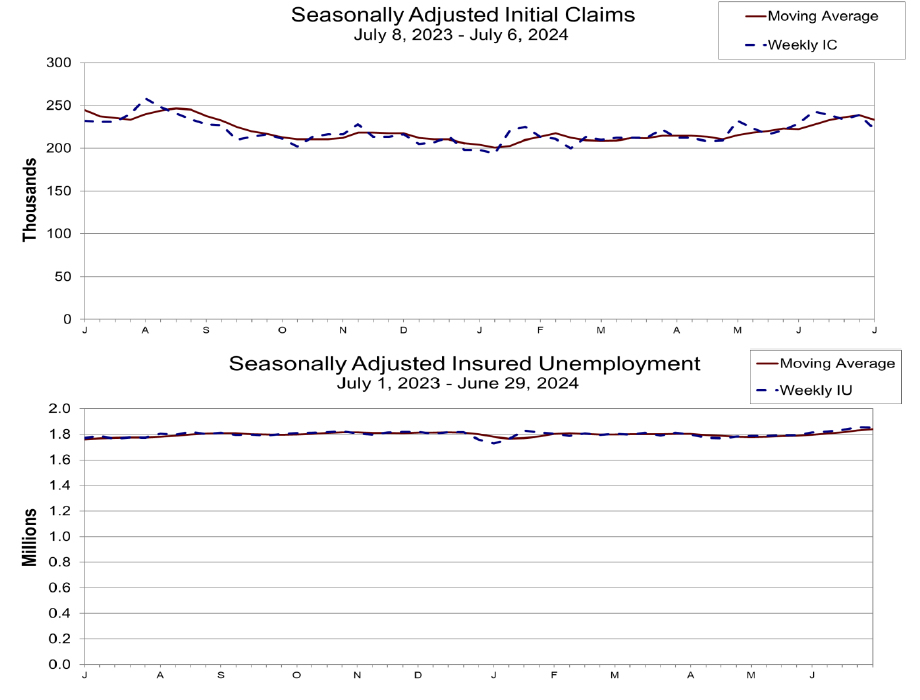

US initial jobless claims falls to 222k vs exp 239k

US initial jobless claims fell -17k to 222k in the week ending July 6, below expectation of 239k. Four-week moving average of initial claims fell -4k to 233.5k.

Continuing claims fell -4k to 1852k in the week ending June 29. Four-week moving average of continuing claims rose 10k to 1840k, highest since December 4, 2021.

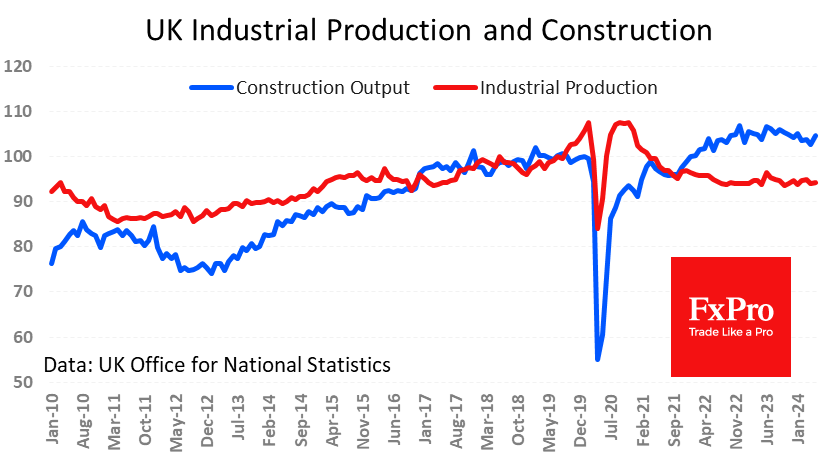

UK GDP grows 0.4% mom in May, driven by services

UK GDP grew by 0.4% mom in May, surpassing expectations of 0.2% mom increase. The primary driver of this growth was a 0.3% mom rise in services output, which significantly contributed to the overall monthly GDP increase. Additionally, production output grew by 0.2% mom , while construction output saw a substantial jump of 1.9% mom.

On a broader scale, real GDP is estimated to have grown by 0.9% in the three months leading up to May compared to the previous three months ending in February. This growth was predominantly driven by a 1.1% increase in services output. However, production remained stagnant with no growth, and construction output declined by -0.7%.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 161.38; (P) 161.59; (R1) 161.93; More...

USD/JPY declines sharply in early US session and breaks 160.25 support decisively. Considering bearish divergence condition in D MACD, fall from 161.49 might already be correcting the whole five-wave rally from 140.25. Intraday bias is back on the downside. Sustained break of 55 D EMA (now at 157.62) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65. Meanwhile, rise will now stay on the downside as long as 160.25 support turned resistance holds, in case of recovery.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94. However, sustained break of 154.53 will raise the chance of larger scale correction and target 140.25/151.89 support zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS Housing Price Balance Jun | -17% | -14% | -17% | |

| 23:50 | JPY | Machinery Orders M/M May | -3.20% | 1.00% | -2.90% | |

| 01:00 | AUD | Consumer Inflation Expectations Jul | 4.30% | 4.40% | ||

| 06:00 | EUR | Germany CPI M/M Jun F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 2.20% | 2.20% | 2.20% | |

| 06:00 | GBP | GDP M/M May | 0.40% | 0.20% | 0.00% | |

| 06:00 | GBP | Industrial Production M/M May | 0.20% | 0.30% | -0.90% | |

| 06:00 | GBP | Industrial Production Y/Y May | 0.40% | 0.60% | -0.40% | -0.70% |

| 06:00 | GBP | Manufacturing Production M/M May | 0.40% | 0.30% | -1.40% | -1.60% |

| 06:00 | GBP | Manufacturing Production Y/Y May | 0.60% | 1.20% | 0.40% | -0.40% |

| 06:00 | GBP | Goods Trade Balance (GBP) May | -17.9B | -16.1B | -19.6B | -19.4B |

| 12:30 | USD | Initial Jobless Claims (Jul 5) | 222K | 239K | 238K | 239K |

| 12:30 | USD | CPI M/M Jun | -0.10% | 0.10% | 0.00% | |

| 12:30 | USD | CPI Y/Y Jun | 3.00% | 3.10% | 3.30% | |

| 12:30 | USD | CPI Core M/M Jun | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Jun | 3.30% | 3.40% | 3.40% | |

| 14:30 | USD | Natural Gas Storage | 56B | 32B |

US initial jobless claims falls to 222k vs exp 239k

US initial jobless claims fell -17k to 222k in the week ending July 6, below expectation of 239k. Four-week moving average of initial claims fell -4k to 233.5k.

Continuing claims fell -4k to 1852k in the week ending June 29. Four-week moving average of continuing claims rose 10k to 1840k, highest since December 4, 2021.

US core CPI slows to 3.3%, lowest since Apr 2021

In June, US CPI fell -0.1% mom, versus expectation of 0.1% mom rise. Core CPI (all items less food and energy) rose 0.1% mom, below expectation of 0.2% mom rise. Energy index fell -2.0% mom while food index rose 0.2% mom.

For the 12-month period, headline CPI slowed from 3.3% yoy to 3.0%yoy, below expectation of 3.1% yoy. Core CPI slowed from 3.4% yoy to 3.3% yoy, below expectation of being unchanged at 3.4% yoy. Core CPI was also the lowest since April 2021. Energy index was up 1.0% yoy while food index was up 2.2% yoy.

Pound on the Offensive

Positive news for the Pound, beyond the fact that England will play in the Euro-24 final. The monthly estimate showed that the economy grew by 0.4% in May (twice as much as expected) and that growth in the last three months accelerated to 1% year-on-year. That’s the fastest pace since early 2023, although it’s about half of what it was before the pandemic hit.

The services sector continued to drive growth, adding 1.1% over three months. Meanwhile, the construction sector added 1.9% in May (vs 0.5% expected), shifting from -2.1% y/y to +0.8% over the month. Construction and services are non-tradable sectors, and the current situation points to very healthy domestic demand.

It’s a different story for industry and trade. Industrial production rose by 0.2% in May, a slight rebound after a 0.9% drop in the previous month. The year-over-year gain is 0.4%, extending the index’s stagnation to almost two years after two years of decline.

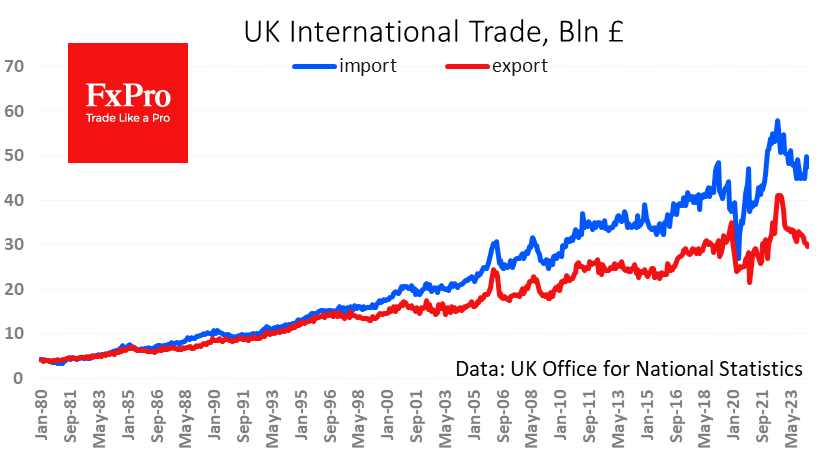

There is also disappointment in the performance of foreign trade, with the value of exports falling to its lowest level since January 2022 at £29.6 billion, the level the UK saw five to six years ago. Imports fell over the month but remain high by historical standards at 47.5B, which is 10% above the average five to six years ago.

So, the current monetary regime moderately restricts services and construction but suppresses industrial production and exports. Inflation is the Bank of England’s priority, so the continued expansion of the services and construction sectors, which together account for around 90% of GDP, may force the central bank to tighten monetary policy in the coming quarters.

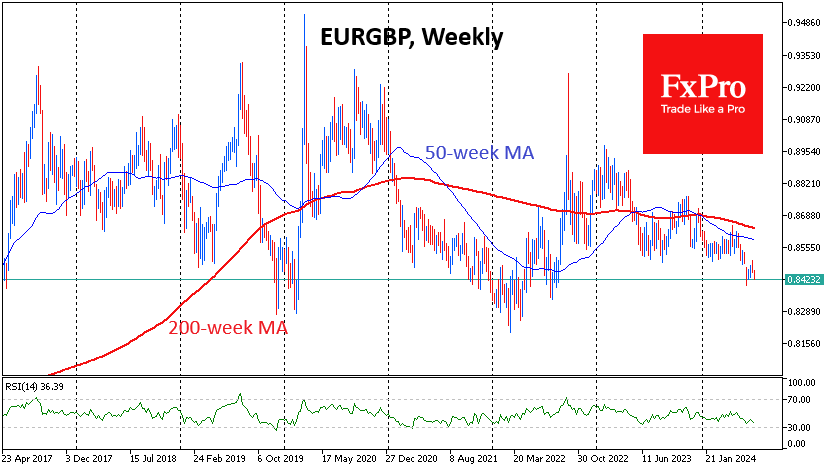

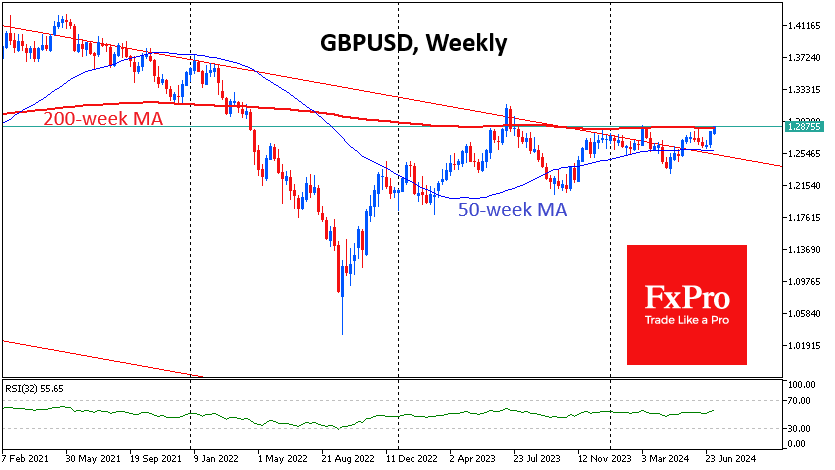

This news is a driver for the pound as it tests 12-month highs and a key long-term trend line, the 200-week moving average against the dollar. A potential break above this resistance could open the way to the next leg of the 1.35-1.40 range.

Just as much attention is being paid to the EURGBP, which is making its second plunge to 2-year lows in a month and looks vulnerable to further Euro retreats ahead of the Pound. The pair is now trading near 0.8420 with the potential to test 0.8300, the lower boundary of the important 8-year range.