Sample Category Title

Loonie Plunges Ahead of Canadian Jobs Number

- Canada’s economy likely added fewer jobs in December

- Local dollar shows some weakness ahead of Friday’s data due at 13:30 GMT

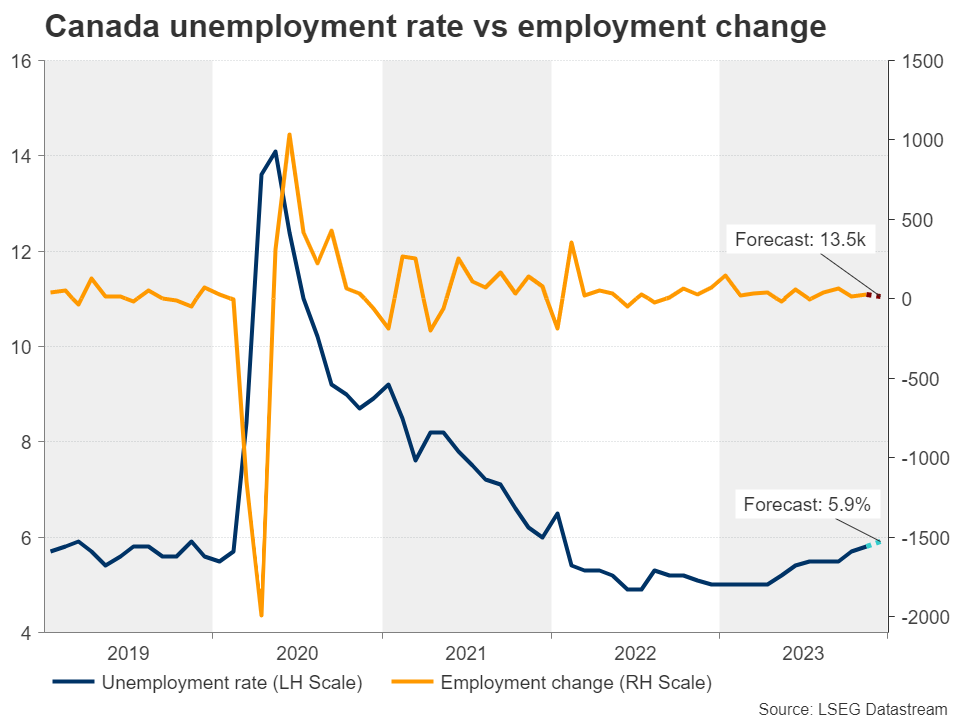

Unemployment rate to rise furhter

According to market forecasts, the unemployment rate in Canada increased to 5.8% in November 2023, higher than the 5.7% figure that was recorded in the previous month. The rate reached its highest point since January 2022, and it increased even further in December, reaching 5.9%. During the month of December, it is anticipated that the economy added only 13.5k new jobs. Despite this, wage growth is still growing at 5%, so investors will be keeping a close eye on that number and the most recent Ivey PMI indicator, which will be released on Friday as well.

Will the BoC raise rates in January?

As anticipated by the market, the Bank of Canada maintained its target for the overnight rate at 5% for the third consecutive meeting in December 2023. Consequently, the cost of borrowing money will remain at a level that was is the highest it has been in 22 years. Policymakers have noted the fact that there are additional indications that monetary policy is reducing price pressures and restraining spending. However, they continue to be concerned about the risks that could affect the outlook for inflation and are prepared to raise the policy rate even further if it becomes necessary. It is the goal of the central bank to see a further and sustainable decrease in core inflation, and it continues to concentrate on the equilibrium between demand and supply in the economy, inflation expectations, wage growth, and the pricing behaviour of corporations. The BoC also announced that it will continue to implement its policy of quantitative tightening.

BoC policy is unlikely to benefit the loonie

As rate cut bets for the Bank of Canada have also been ratcheted up recently, the Canadian dollar will be keeping a close eye on the domestic labor market. Compared to the other commodity-linked currencies, the Canadian dollar is expected to have gained approximately 2.5% against its US counterpart in 2023. This performance is a bit stronger than that of the Australian and New Zealand dollars, which are also commodity-linked currencies.

On the other hand, there is a possibility that the year 2024 will be much more difficult for the loonie if the BoC is forced to begin reducing interest rates due to the stagnation of economic development.

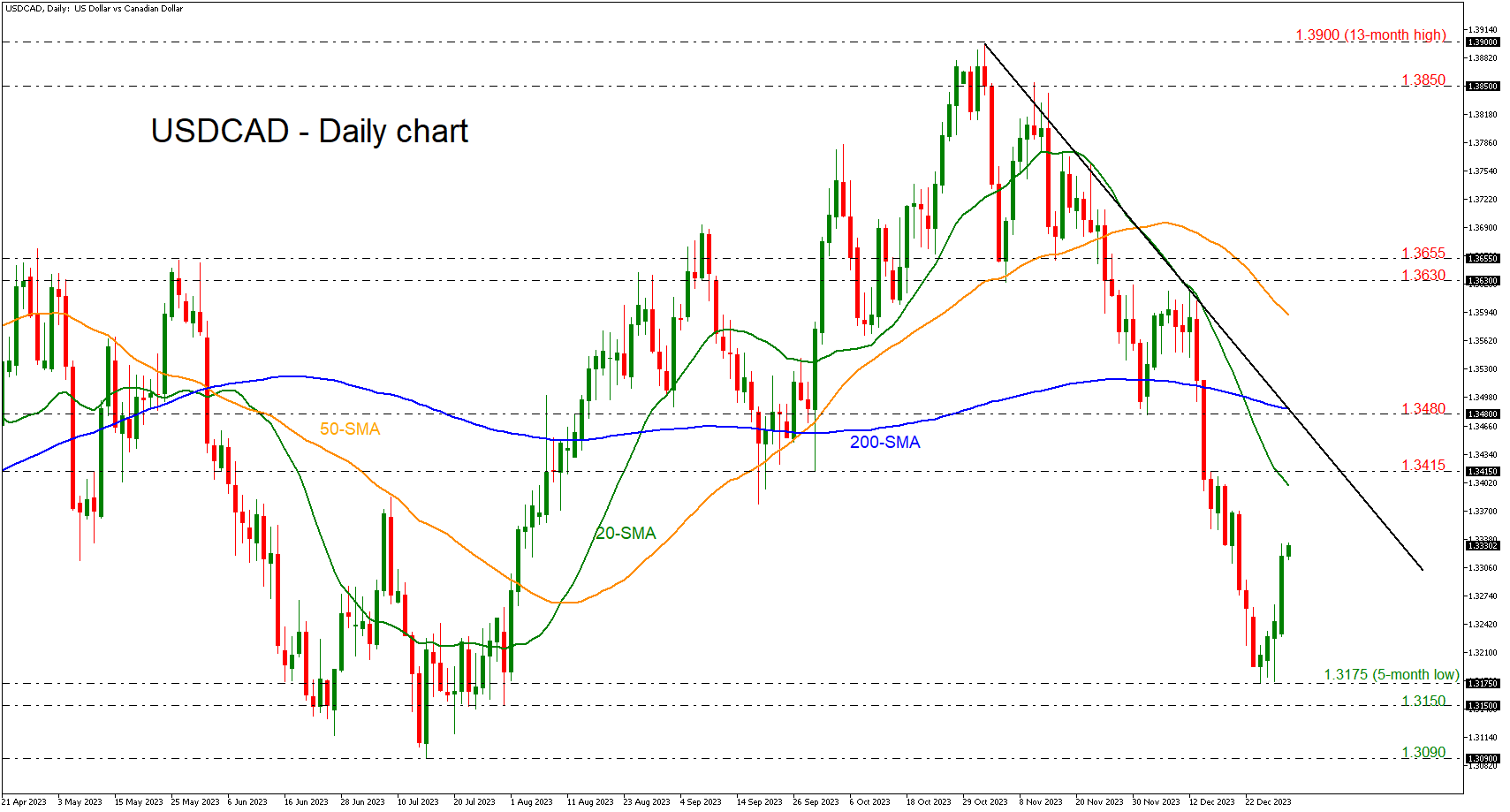

Dollar/loonie is surging after the significant bounce off the five-month low of 1.3175. A fresh move towards the 1.3415 resistance is possible in the near term, reaching the steep descending trend line if the US dollar can extend its bullish streak. However, should the pair reverse back down again, the five-month low of 1.3174 could provide initial support. More downside movements would turn the spotlight on the 1.3150 barrier and the 1.3090 bottom, taken from the low on July 14.

Sunset Market COmmentary

Markets

Interest rate markets tried to build on last week’s ‘U-turn’ after the accelerated decline in yields triggered by the December Fed policy announcement. Corporates and sovereigns are eager to use lower funding costs to frontload at least part of their 2024 financing needs, with new bond issuance taking a solid start. Still, a sustained countermove on the recent bond rally not only needs supply but also an economic narrative. US yields maintain some upside momentum going in the release of the manufacturing ISM and the JOLTS job openings (see below), rising between 4 bps (2-y) and 5.5 bps (30-y). Richmond Fed president Barkin sees a soft landing scenario as ‘increasingly conceivable, but in no way inevitable’. Most Fed officials are expecting rate cuts in 2024, but he stressed the Fed is keeping a close eye both on the economic performance and inflation continuing its decent. With respect to the latter, the recent plunge in yields could stimulate too much demand and keep inflation elevated. He even kept the option for further rate hikes on the table. Understandably, his remarkets were ‘invisible’ on the interest rate charts. German yields in the meantime reversed an early rise to trade marginally lower across the curve. French and German CPI data to be published tomorrow ahead of the flash EMU estimate on Friday are expected to face a less easy comparison base compared to previous months, potentially lifting the Y/Y (headline) measure. However, given recent market momentum, European investors stay cautious to front-run on such an outcome. A more gradual rise/pause in the core yield rebound compared to yesterday doesn’t help risk sentiment. The EuroStoxx 50 is ceding 1.5%, turning its back to the multi-year top reached last week. US equities opened about 0.5% lower (S&P). The dollar extends its comeback. DXY is testing the 102.5 area, compared to a correction low near 100.62 last week. EUR/USD is drifting further south in the 1.09 big figure. First resistance at 1.0875 (38% retracement of the rebound since early October) is coming on the radar. With the BOJ still in wait-and-see modus, USD/JPY revisits the 143 area. Sterling holds ‘strong’ (EUR/GBP 0.865).

At the time of finishing this report US JOLTS job openings eased further from 8852k to 8790k. The headline manufacturing ISM rose slightly more than expected to 47.4 from 46.7, but the prices paid subindex dropped from 49.9 to 45.2 while new orders unexpectedly eased to 47.1. Yields declined a couple of bps after the release.

News & Views

The Swiss manufacturing industry can’t buck the global trend and remains in dire straits. The PMI ticked from 42.1 to 43 in December, but is stuck deep into contraction territory since early 2023. Details showed a new deceleration in output (43.6 from 46.6) with companies running down inventories (45.5 from 49) and hardly having any backlog of orders (39.8 from 38.1). The quantity and stock of purchases slowed at a slower pace though, suggesting that 2024 might see a new start in the inventory cycle. Companies still shed jobs, though at a much smaller pace (49.2 from 46). The data didn’t impact Swiss markets, but a quick look at the FX chart shows that the strong Swiss currency is also one of the factors holding back the manufacturing industry. The November/December global bond rally played in the advantage of the Swiss franc with EUR/CHF touching an all-time low just above 0.9250 around year-end when we exclude volatility around the end of the release of the EUR/CHF 1.20 peg early 2015.

Turkish inflation accelerated to 2.93% M/M in December with the Y/Y-comparison broadly unchanged at 64.77%. Clothing and footwear and transportation were the only two categories reporting a M/M-decline. Underlying core inflation readings also increased by 2.3% to 3% M/M with Y/Y-figures depending on the specific measure around 61% to 70%. Today’s data were close to expectations and in line with the central bank’s outlook. The Turkish government’s end of December decision to hike the minimum wage by 49% this year poses additional upside risks to the Turkish inflation outlook, leaving the Turkish central bank with no options but to stick with its hawkish stance. In an orthodox turn after May’s elections, the CBRT raised its policy rate from 8.5% to 42.5%, but the pace of hiking is slowing (+250 bps in December). A (final) January hike (to 45%?) is still in the cards. The Turkish lira continues its gradual depreciation process facing deep negative real yields. EUR/TRY is close to the all-time high just below 33.

US ISM manufacturing rises to 47.4, 14th month of contraction

US ISM Manufacturing PMI rose from 46.7 to 47.4 in December, above expectation of 47.1. That's still the 14th month of contraction reading.

Looking at some details, new orders, fell from 48.3 to 47.1, the 16th month of contraction. Production rose from 48.5 to 50.3. Employment rose from 45.8 to 48.1. Prices fell sharply from 49.9 to 45.2.

December PMI reading of 47.4 corresponds to an estimated decrease of -0.5% in the real GDP on an annualized basis.

British Pound Starts New Year’s With a Tumble

The British pound is steady on Wednesday after sharp losses a day earlier. In the European session, GBP/USD is trading at 1.2632, up 0.11%.

UK Services PMI expected to accelerate

UK Services PMI will be released on Thursday. The services sector, which is responsible for most of the economy’s growth, hit a rough patch late last year and posted three straight declines. The PMI managed to claw back into expansion territory in November with a reading of 50.9. The consensus for December is 52.7, which would indicate modest growth.

The UK manufacturing sector remains mired in a depression. December’s Manufacturing PMI eased to 46.2, below the consensus of 46.4 and shy of the November reading of 47.2, which was a seven-month high. Manufacturing production has now declined for ten straight months. The December decline was driven by weaker demand abroad for UK goods and less optimism from manufacturers about business conditions. The weak UK economy and high borrowing costs continue to dampen manufacturing activity.

The Federal Reserve releases the FOMC meeting of the December meeting later today. The meeting was highly significant as the Fed surprised the markets by failing to push back against rate-cut fever. The Fed signalled that it expected to trim rates three times in 2024, a major pivot from the well-worn script of ‘higher for longer’. Still, some Fed members have cautioned the markets from expecting imminent rate cuts and the timing of any rate cuts is unclear. Investors will be looking to the minutes for further details about the Fed’s surprise pivot. The markets are bubbling with confidence that the Fed will slash rates this year and have priced in six rate cuts starting in March.

GBP/USD Technical

- There is resistance at 1.2753 and 1.2807

- GBP/USD pushed below support lines at 1.2678 and 1.2624 earlier. Below, there is support at 1.2549

Fed’s Barkin: Soft landing within reach, but not assured

Richmond Fed Thomas Barkin, in his prepared remarks for a speech, acknowledged that soft landing is "increasingly conceivable. But he also cautioned that such an outcome is "in no way inevitable."

Barkin outlined four key risks that could potentially derail the US economy from its desired path. Firstly, he expressed concern that the economy might "run out of fuel", implying a slowdown in economic momentum. Secondly, he pointed to the possibility of "unexpected turbulence".

Thirdly, the risk that inflation might stabilize at a level above Fed's 2% target. Finally, Barkin mentioned the risk of a delayed "landing", suggesting that the economy could continue to perform better than expected, which might prolong the process of policy normalization.

Addressing the approach to monetary policy, Barkin emphasized the importance of incoming data in shaping the Fed's decisions. He stated, "Is inflation continuing its descent and is the broader economy continuing to fly smoothly? Conviction on both questions will determine the pace and timing of any changes in rates. There's no autopilot. The data that come in this year will matter."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.13; (P) 141.67; (R1) 142.54; More...

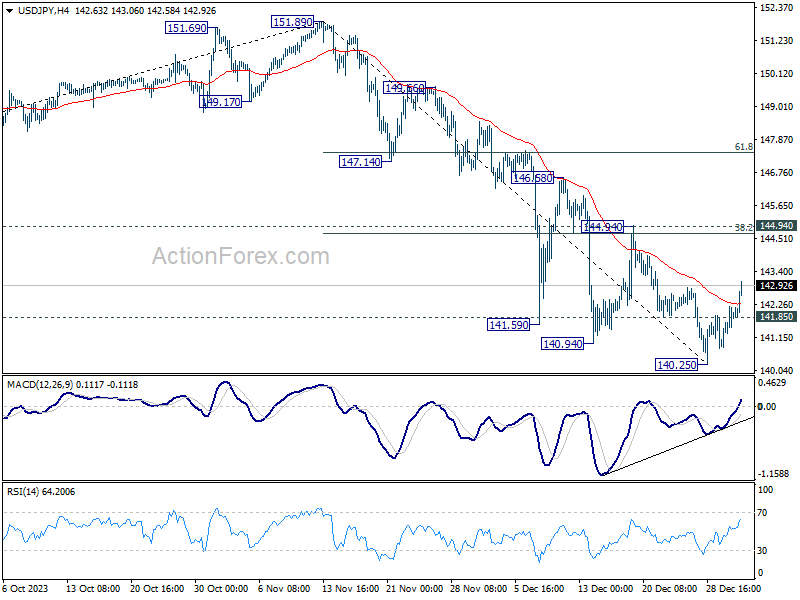

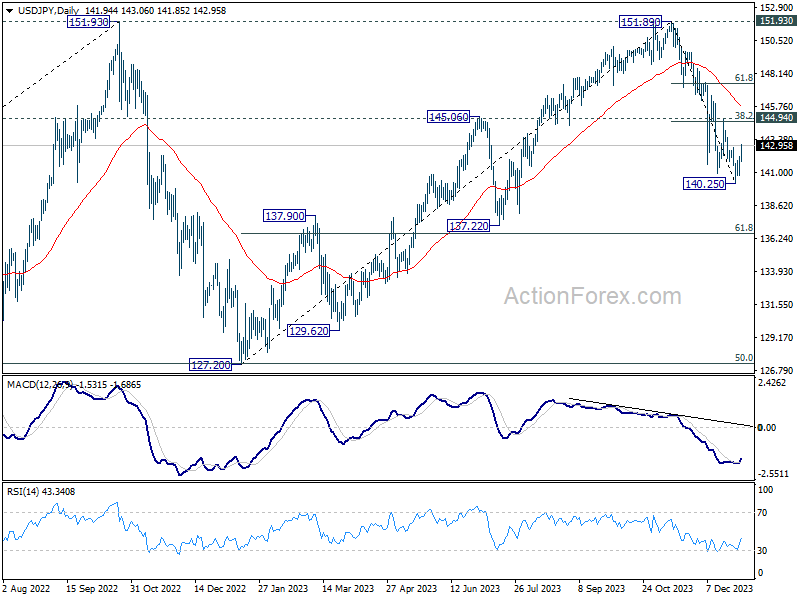

USD/JPY's break of 142.84 minor resistance indicates short term bottoming at 140.25, on bullish divergence condition in 4H MACD. Intraday bias is back on the upside for stronger rebound to 38.2% retracement of 151.89 to 140.25 at 144.69. On the downside, below 141.85 minor support will bring retest of 140.25 low instead.

In the bigger picture, fall from 151.89 is seen as the third leg of the corrective pattern from 151.93 (2022 high). Deeper decline would be seen to 61.8% retracement of 127.20 to 151.89 at 136.63, sustained break there will pave the way to 127.20 support (2022 low). This will now remain the favored as long as 144.94 resistance holds.

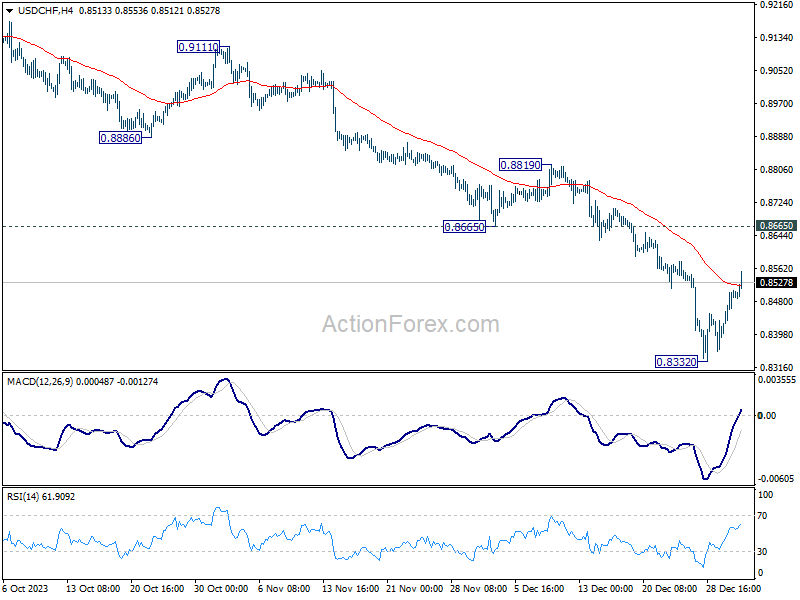

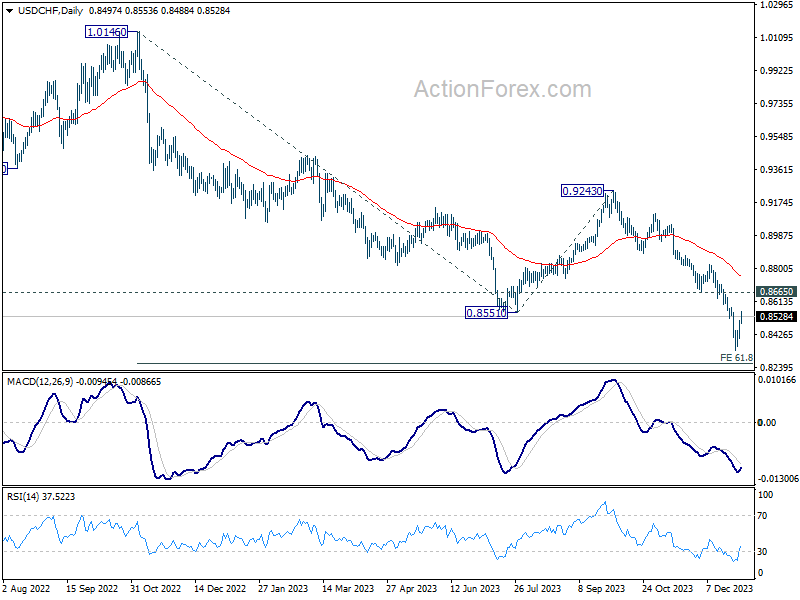

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8308; (P) 0.8585; (R1) 0.8779; More....

USD/CHF's recovery from 0.8332 is extending. But still, with 0.8665 support turned resistance, current price actions are seen as corrective, and outlook stays bearish. On the downside, break of 0.8332 will resume larger fall from 0.9243 to 0.8257 projection level.

In the bigger picture, break of 0.8551 support indicates resumption of whole decline from 1.0146 (2022 high). Next target is 61.8% retracement of 1.0146 to 0.8551 from 0.9243 at 0.8257. Sustained break there could prompt downside acceleration to 100% projection at 0.7648. This will now remain the favored case as long as 0.8819 resistance holds.

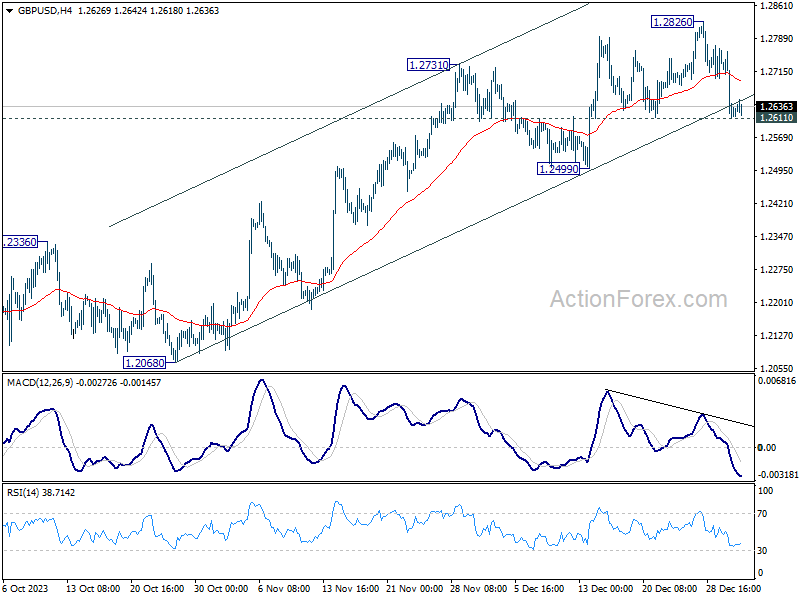

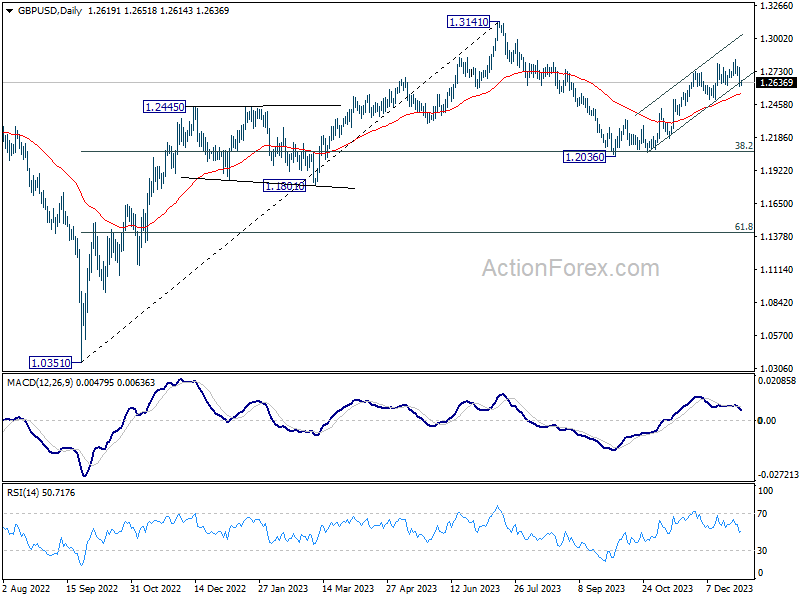

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2567; (P) 1.2663; (R1) 1.2716; More...

Intraday bias in GBP/USD stays neutral first with 1.2611 support intact. On the upside, break of 1.2826 will resume whole rally from 1.2036. However, break of 1.2611 will indicate short term topping, and turn bias back to the downside for 1.2499 support.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to rise from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg that's in progress. Upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0901; (P) 1.0978; (R1) 1.1019; More...

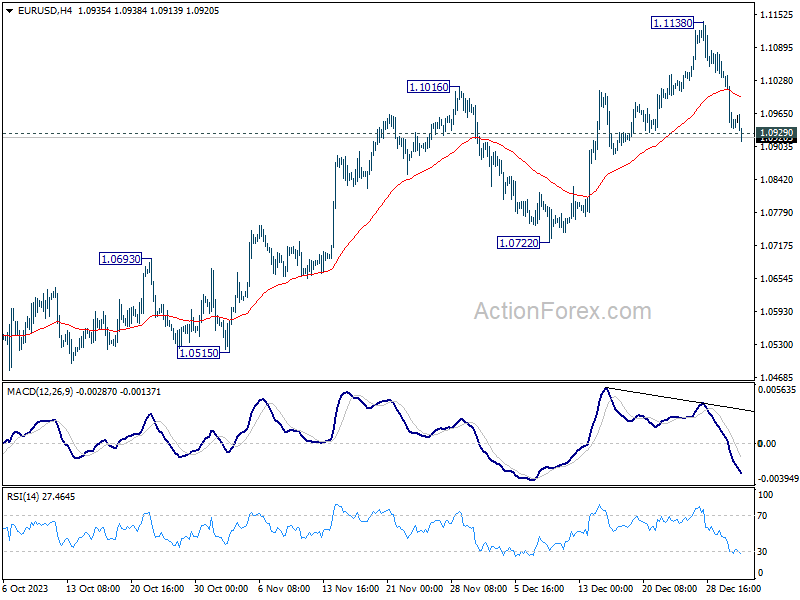

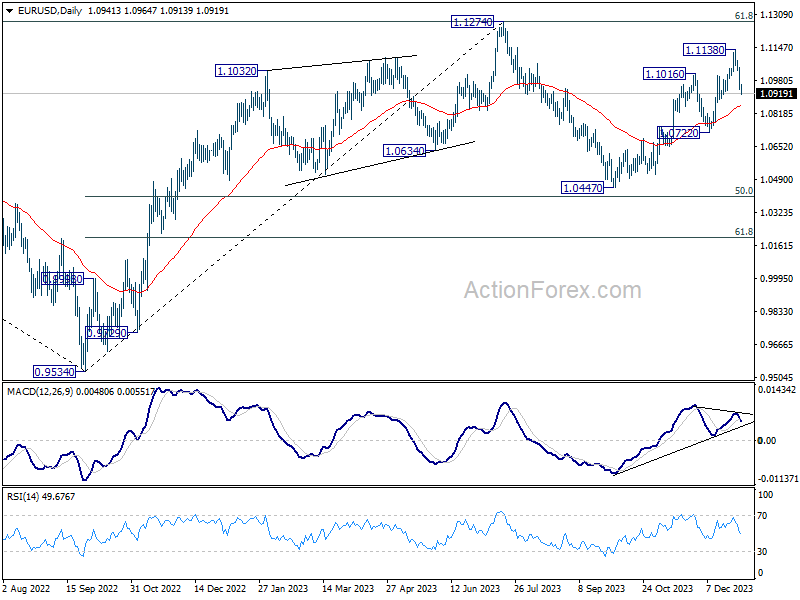

EUR/USD's break of 1.0929 minor support confirms short term topping at 1.1138, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 1.0772 support. Sustained break there will argue that whole rise from 1.0447 has completed, and break deeper fall back to this support. For now, risk will stay mildly on the downside as long as 55 4H EMA (now at 1.0998) holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Dollar Strengthens Amidst Global Tech Selloff and Treasury Yield Recovery

Dollar is having a renewed attempt to extend its near-term rebound, buoyed by mild risk-off sentiment prevalent in Europe and US premarkets. This resurgence in the greenback's strength coincides with ongoing selloff in technology stocks, which has now extended to major Asian markets, with key indexes in South Korea and Taiwan closing down. Additionally, Dollar is finding support from a recovery in the benchmark 10-year treasury yield, which appears to be on track to test the 4% psychological level.

In terms of currency performance, Japanese Yen is currently the weakest for the day, followed by Australian Dollar and Swiss Franc. Euro and Canadian Dollar are mixed while British Pound is demonstrating some resilience. The direction of the next move for these currencies is highly contingent on the forthcoming release of FOMC minutes. Market participants are keenly awaiting insights into Fed's discussions on the planned rate cuts for this year, including specifics on the timing of the initial cut.

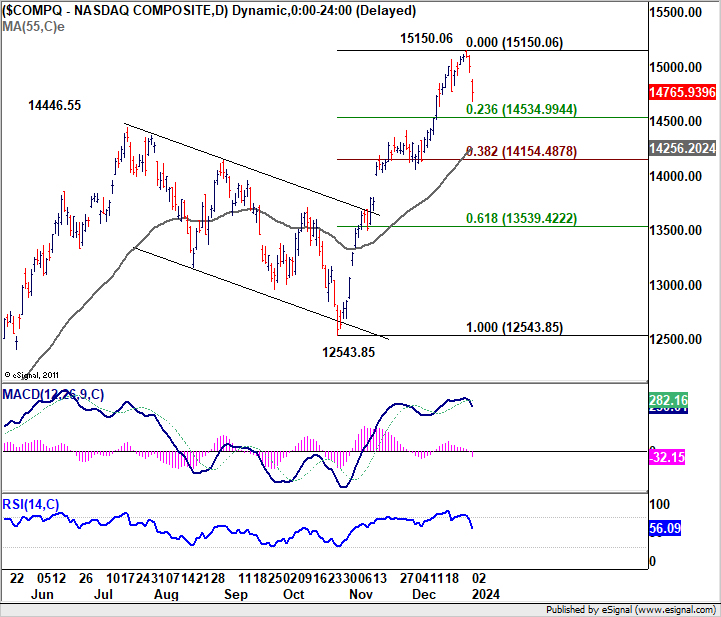

On the technical front, a short term top is likely in place at 15150.06 in NASDAQ, with this week's deep retreat. For now, as long as 23.6% retracement of 12543.85 to 15150.06 at 14534.99 holds, consolidations from 15150.06 should be relatively brief, and larger rally should resume sooner rather than later. However, firm break of 14534.99 will indicate that lengthier correction is underway, and risk deeper fall to 55 D EMA (now at 14256.20). That would provide additional support to Dollar for extending its near term rebound.

In Europe, at the time of writing, FTSE is down -0.69%. DAX is down -1.06%. CAC is down -1.49%. Germany 10-year yield is down -0.0133 at 2.055. UK 10-year yield is up 0.011 at 3.656. Earlier in Asia, Hong Kong HSI fell -0.85%. China Shanghai SSE rose 0.17%. Singapore Strait Times fell -0.94%. Japan was still on holiday.

Germany's unemployment rises 5k, still holding up well

In December, Germany's unemployment count rose by 5k to 2.703m, a figure notably lower than the anticipated increase of 20k. This increment brings the total number of unemployed in Germany to 183k higher compared to the same period a year ago. Additionally, unemployment rate inched up from revised 5.8% to 5.9%, aligning with expectations.

Andrea Nahles, chair of Federal Employment Agency, acknowledged that economic challenges of 2023 have indeed impacted the labor market, but she also emphasized the market's relative resilience in the face of these stressors.

She noted, "If we look back at 2023, we can see that the weak economy has left its mark on the labor market — however, considering the extent of the stress and uncertainty, the labor market is still holding up well."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0901; (P) 1.0978; (R1) 1.1019; More...

EUR/USD's break of 1.0929 minor support confirms short term topping at 1.1138, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 1.0772 support. Sustained break there will argue that whole rise from 1.0447 has completed, and break deeper fall back to this support. For now, risk will stay mildly on the downside as long as 55 4H EMA (now at 1.0998) holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is seen as the second leg. While further rally could cannot be ruled out, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 1.0722 support will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | CHF | Manufacturing PMI Dec | 43 | 43 | 42.1 | |

| 08:55 | EUR | Germany Unemployment Change Dec | 5K | 20K | 22K | |

| 08:55 | EUR | Germany Unemployment Rate Dec | 5.90% | 5.90% | 5.90% | 5.80% |

| 15:00 | USD | ISM Manufacturing PMI Dec | 47.1 | 46.7 | ||

| 15:00 | USD | ISM Manufacturing Prices Paid Dec | 50 | 49.9 | ||

| 15:00 | USD | ISM Manufacturing Employment Index Dec | 45.8 | |||

| 19:00 | USD | FOMC Minutes |