Sample Category Title

S&P 500: Rotation Has Put the Brakes on the Market

- A rotation is taking place in the US stocks.

- Seasonal factors and impressive earnings are supporting the S&P 500.

With geopolitical concerns receding and the likelihood of a Fed rate rise diminishing, the US equity market has returned to a familiar theme: rotation. Interest in artificial intelligence has not waned, but technology shares appear overbought. Furthermore, there are concerns about their ability to generate high returns commensurate with the capital invested. As a result, capital is being reallocated across sectors, leading to consolidation in the S&P 500.

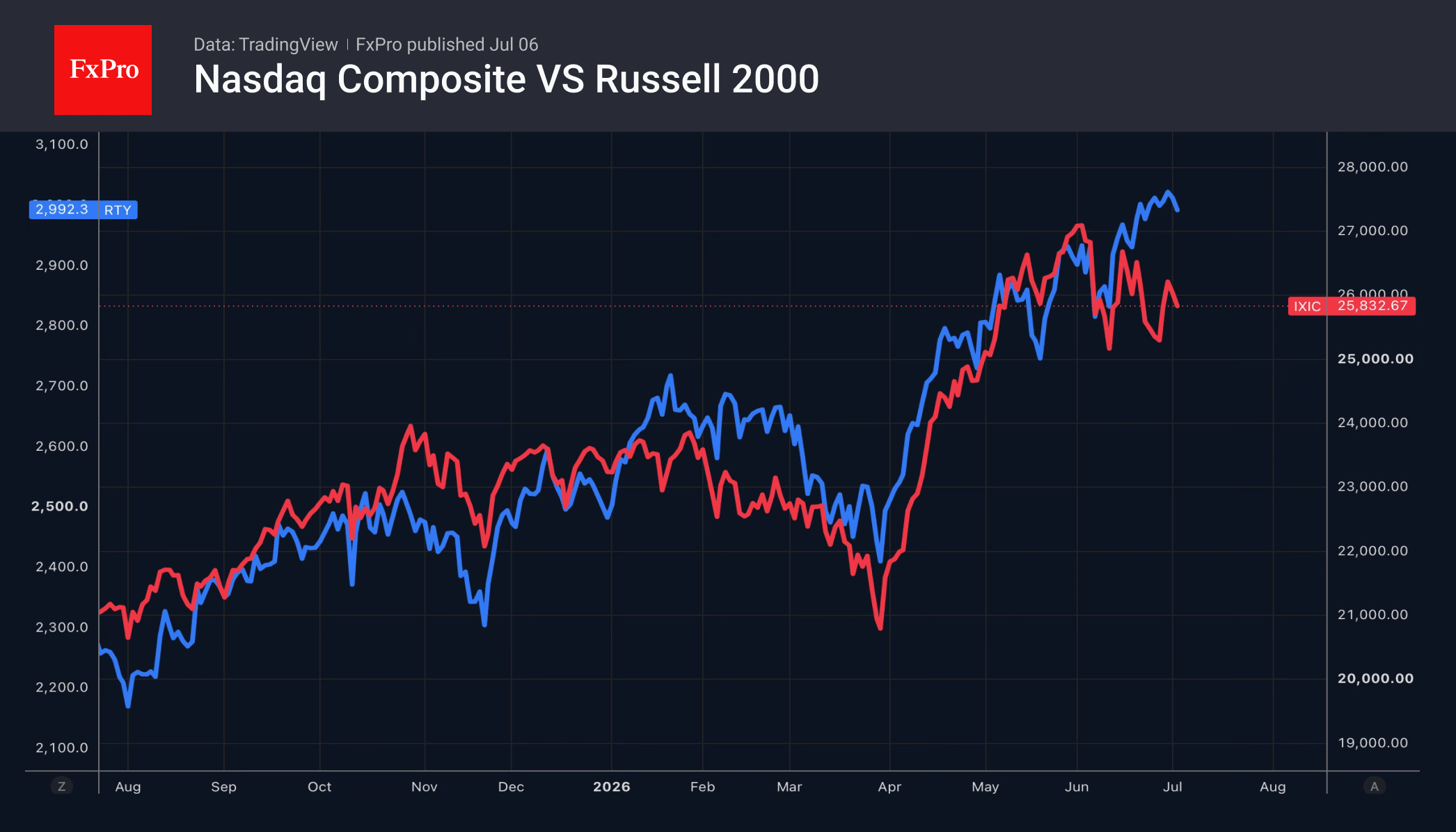

Investor interest in sectors sensitive to the US economy has lifted the Russell 2000 by 22% in the first half of the year. This marks the best performance by the small-cap index since 1991. Between January and June, it outperformed the Nasdaq Composite by 9 percentage points, for the first time since 2006. While the ‘Magnificent Seven’ dominated the market in 2023–2025 and chipmakers’ shares at the beginning of 2026, investors are now seeking new leaders.

The inability to identify them is driving capital outflows. According to Bank of America, citing EPFR Global, US-focused equity funds recorded outflows of $17.2 billion, the worst performance since March. By contrast, their Japanese counterparts recorded their largest inflow in seven weeks, totalling $1.9 billion.

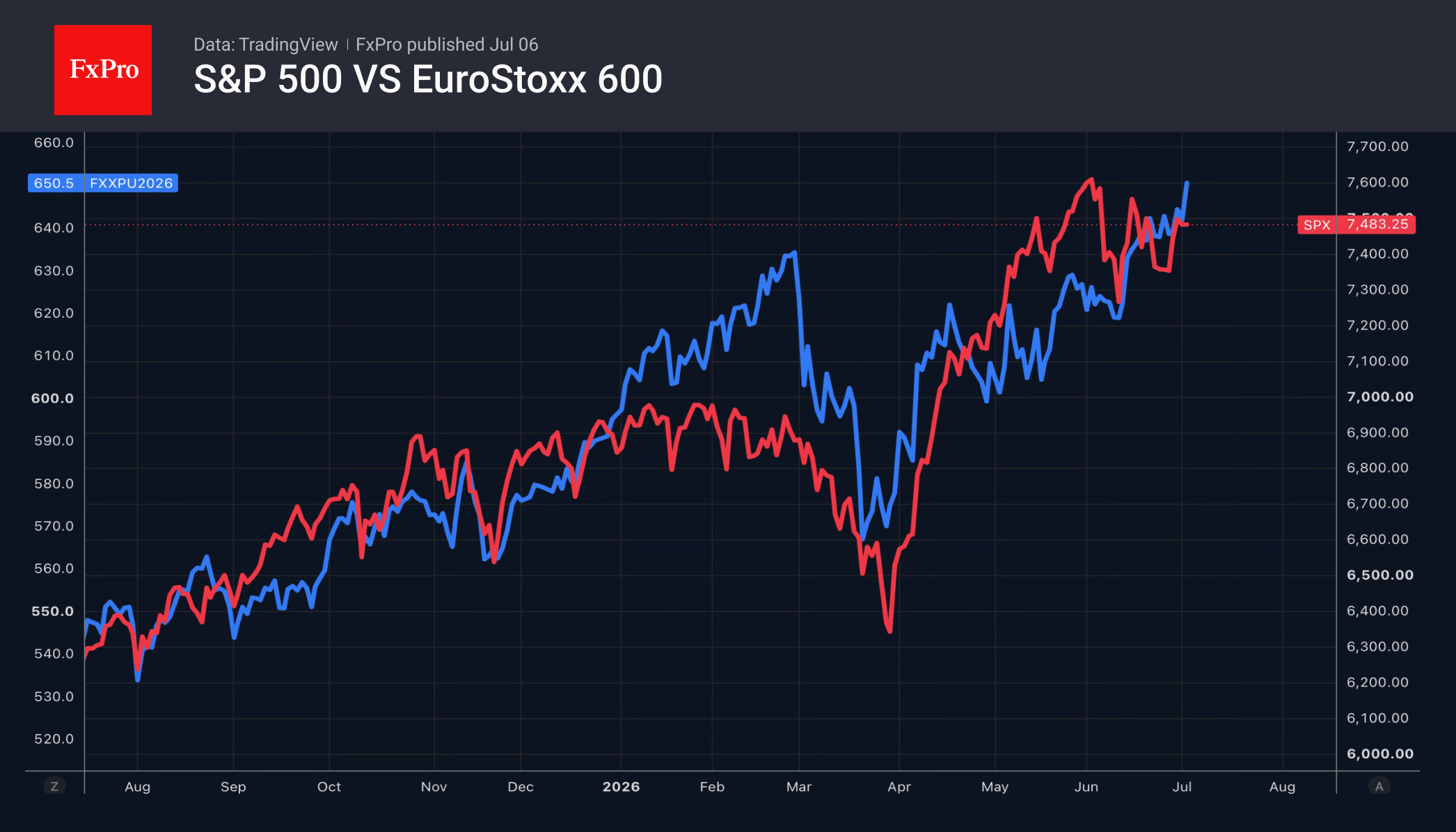

Europe is not left behind. The STOXX Europe 600 has closed in positive territory for four consecutive weeks and has set a new record. Technology, industrial, and utility companies are particularly popular. Falling oil prices are providing a tailwind, as are reduced prospects of monetary policy tightening by the ECB and the Fed, and the associated decline in global bond yields.

The S&P 500 is underperforming the STOXX Europe 600, but the US stock index has a seasonal advantage. Since 2014, it has never closed July in the red. The average gain at the end of the second month of summer has been 2.5%.

Investors remain encouraged by corporate results. In the first quarter, the net profit margin of S&P 500 companies rose by 14.8%. This marks the strongest performance since records began in 2009. The figure is expected to fall to 14.2% in April–June. However, compared with the same period in 2025, it will be up 3.4%. This is atypical for Wall Street. Over the last 40 quarters, it has lowered its forecasts by an average of 2.7 percentage points.

The FxPro Analyst Team

USD/JPY Bulls Return as Japan’s Intervention Window Closes

USD/JPY bulls are back. After last week's intervention scare briefly knocked the pair lower, Yen selling returned today as the most obvious window for Japanese action passed without official intervention. Dollar's rebound also helped, with markets now appearing to have fully absorbed the dovish surprise from June non-farm payrolls. But the sharper story is in Yen itself: the intervention premium that supported it late last week has quickly evaporated.

Last week's Yen rebound was driven by a shift in market psychology. Reports suggested Japan could abandon the usual cycle of warnings before intervention and instead move without notice, leaving traders exposed to a sudden strike. That threat mattered because it coincided with a window of thin liquidity: Friday's US holiday, followed by the typically quiet Monday Asian open. In such conditions, any official Yen buying would likely have had a larger market impact.

That was the reason traders blinked. The rally in Yen was not based on a narrowing Fed-BoJ rate gap or a material change in Japan's policy outlook. It was a positioning squeeze built around the fear that Tokyo might use holiday liquidity to punish Yen shorts. Once that window closed without intervention, the near-term risk premium dropped sharply, allowing USD/JPY to climb back above 162.

The pattern is familiar. Japan's earlier interventions around April-May took place during holiday or thin-liquidity periods, precisely when official buying could move prices more forcefully. That precedent made the Friday-to-Monday window particularly important. When nothing happened, traders effectively treated the immediate intervention scenario as expired rather than merely reduced.

The underlying trend therefore reasserted itself. US payrolls softened enough to cool expectations for aggressive Fed tightening, but not enough to shift the market toward rate cuts. Investors still expect one Fed hike this year, while BoJ policy remains far below US rates. That leaves carry trades intact and keeps pressure on Yen whenever intervention fears fade.

The nuance is that Tokyo's threat has not lost all credibility. USD/JPY near 162 and potentially toward 165 still carries intervention risk, especially if the move becomes disorderly. But intervention is now best viewed as lumpy and event-driven. It can interrupt the trend, especially around holidays, thin liquidity or psychologically sensitive levels, but it has not yet changed the structural direction.

In currency markets, Dollar is leading the day, followed by Sterling and Aussie. Yen is the clear laggard, followed by Kiwi and Swiss Franc, with Euro and Loonie trading in the middle. The price action suggests traders are no longer trading last week's intervention rumor. They are back to trading the wide policy gap, and that leaves USD/JPY's broader uptrend firmly in play.

Gold Finds Support at $4,000, but Only Softer Inflation Can Fuel the Next Rally

Gold's rebound from the $4,000 area has already begun to lose momentum as markets look beyond soft payrolls and refocus on the Fed's inflation concerns. With investors still pricing another rate hike this year, the July CPI report—not the recent jobs data—may determine whether Gold breaks higher or resumes its broader decline. We examine the macro backdrop, Fed expectations, and the technical levels that matter most. Read More.

NZD/USD Bears Await RBNZ Verdict After Relief Rally

NZD/USD enters one of its most important weeks of the year as the RBNZ faces a finely balanced decision between tackling inflation and supporting growth. With economists and major banks divided over whether the OCR will be raised, the policy statement could prove even more important than the rate decision itself. We examine the competing arguments, what they mean for the Kiwi, and why key technical levels suggest the recent rebound may only be temporary. Read More.

Eurozone Sentix Investor Confidence Surges to -3.1 as Germany's Recovery Gains Traction

Eurozone investor confidence strengthened for a third consecutive month in July as Germany's outlook improved and inflation concerns eased. The latest Sentix survey suggests the region's recovery is becoming more broad-based while reducing pressure on the ECB to tighten policy further. Read More.

Eurozone Producer Inflation Holds Firm as Core Factory Prices Continue to Rise

Eurozone producer inflation accelerated more than expected in May as strong gains in intermediate goods and a solid increase in prices excluding energy offset lower energy costs. The latest PPI report suggests underlying pipeline inflation remained firm even as headline monthly growth slowed. Read More.

Eurozone Retail Sales Rise 0.2% mom in May as Food Spending Leads Growth

Eurozone retail sales met expectations in May as stronger spending on food and non-food goods outweighed weaker fuel sales. While consumer demand remained resilient overall, performance varied widely across member states, highlighting an uneven recovery across the region. Read More.

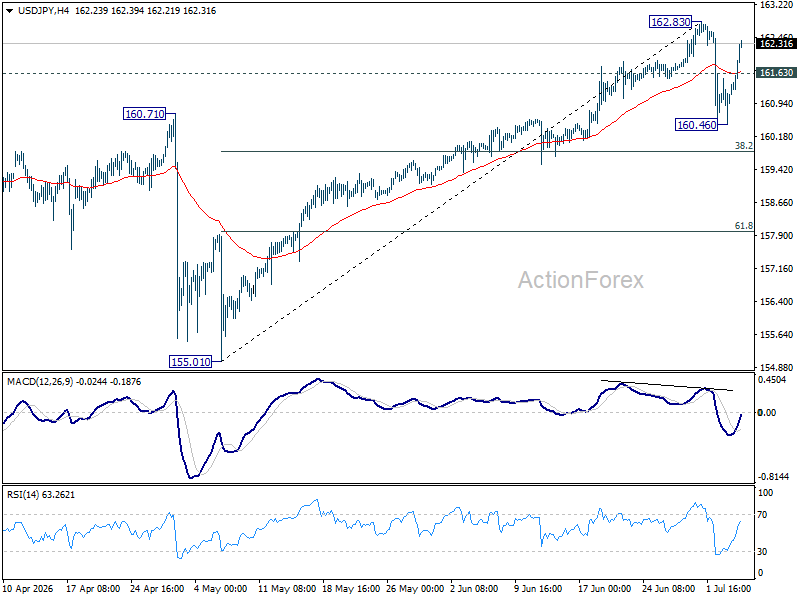

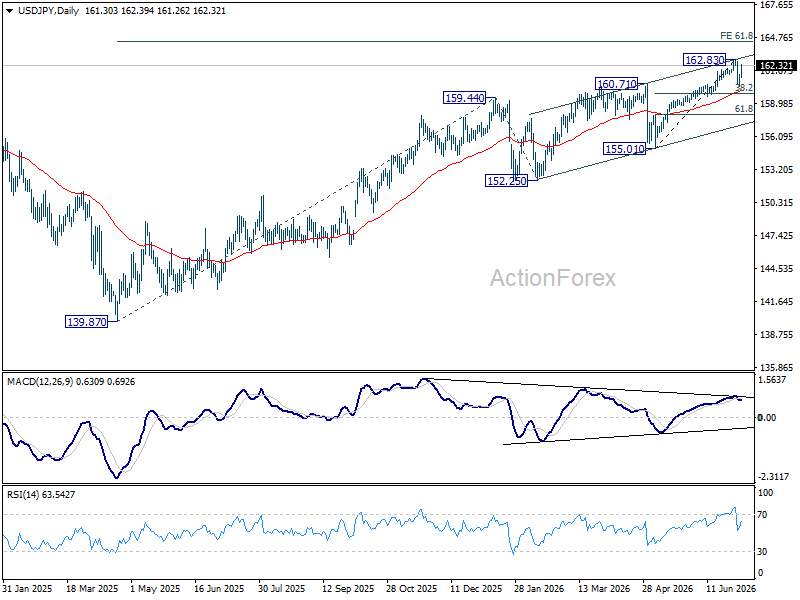

USD/JPY Daily Outlook

Intraday bias in USD/JPY is turned neutral first with current strong rebound. Consolidations could extend below 162.83. But in case of another fall, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

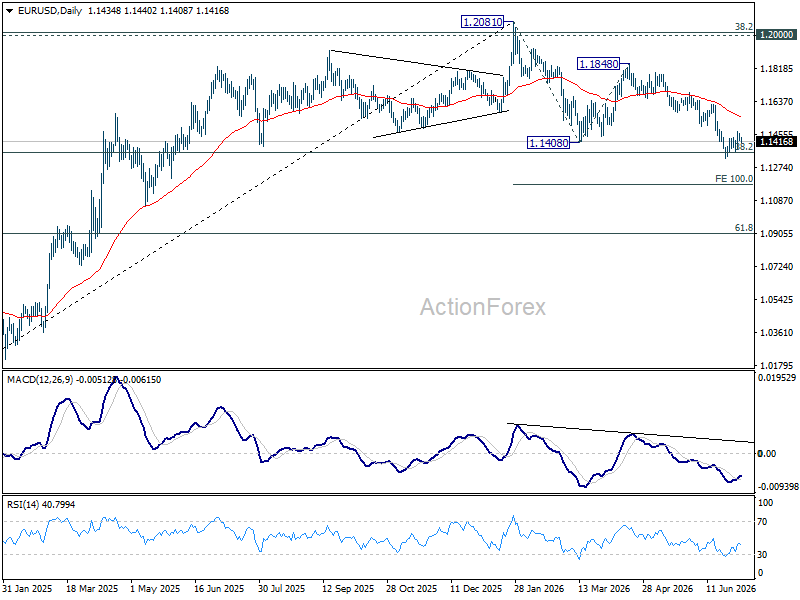

EUR/USD Daily Outlook

Intraday bias in EUR/USD remains neutral and more consolidations could be seen above 1.1323. With 1.1499 support turned resistance intact, further decline is expected. On the downside, break of 1.1323 will resume the fall from 1.2081 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. However, decisive break of 1.1499 will turn bias back to the upside for 55 D EMA (now at 1.1559) and above.

In the bigger picture, focus is back on 38.2% retracement of 1.0176 to 1.2081 at 1.1353. Decisive break there will revive the case of medium term bearish trend reversal after rejection by 1.2 key cluster resistance level. Further fall should be seen to 61.8% retracement at 1.0904. Nevertheless, strong rebound from 1.1353, followed by break of 1.1621 resistance, will retain medium term bullishness.

USD/JPY Daily Outlook

Intraday bias in USD/JPY is turned neutral first with current strong rebound. Consolidations could extend below 162.83. But in case of another fall, downside should be contained by 38.2% retracement of 155.01 to 162.83 at 159.84. On the upside, firm break of 162.83 will resume larger up trend.

In the bigger picture, rise from 139.87 (2025 low) is seen as another rising leg of the long term up trend. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. For now, outlook will remain bullish as long as 155.01 support holds, even in case of deep pullback.

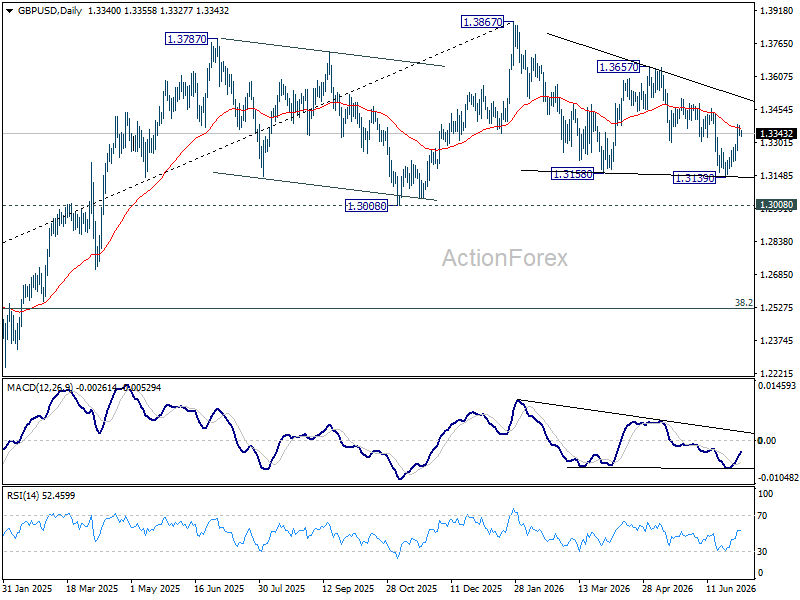

GBP/USD Daily Outlook

Intraday bias in GBP/USD is turned neutral first with current retreat. Risk will stay on the upside as long as 55 4H EMA (now at 1.3288) holds. Above 1.3384 temporary top will target r 1.3459 resistance. Firm break there will argue that whole correction from 1.3867 has completed, and target 1.3657 resistance for confirmation. However, sustained break of 55 4H EMA will bring deeper fall to retest 1.3139 low instead.

In the bigger picture, price actions from 1.3867 are a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

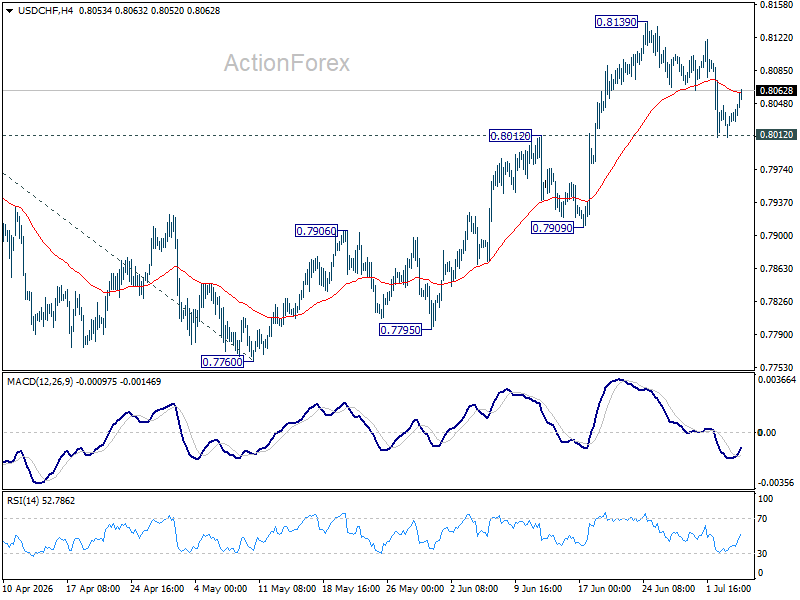

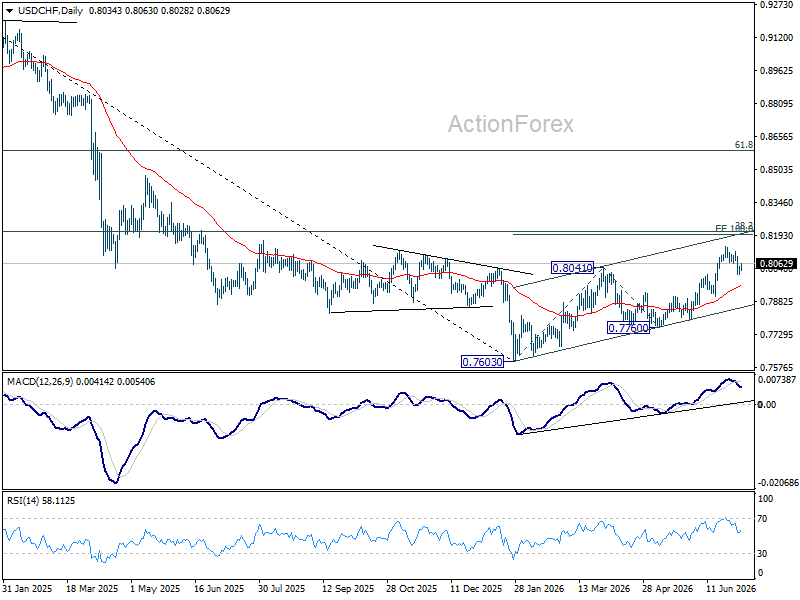

USD/CHF Daily Outlook

USD/CHF recovered after drawing support from 0.8012. Intraday bias remains neutral and another rise is still mildly in favor. Above 0.8139 will extend the rally from 0.7760 to 100% projection 0.7603 to 0.8041 from 0.7600 at 0.8198 next. However, sustained break of 0.8012 will bring deeper fall to 55 D EMA (now at 0.7952) and below.

In the bigger picture, while a medium term bottom was formed at 0.7603, it's still early to call for bullish trend reversal. As long as 38.2% retracement of 0.9200 (2025 high) to 0.7603 at 0.8213 holds, the larger down trend could still continue through 0.7603 at a later stage. However, firm break of 0.7603 will argue that the trend has reversed and turn focus to 0.8332 support turned resistance (2023 low) for confirmation.

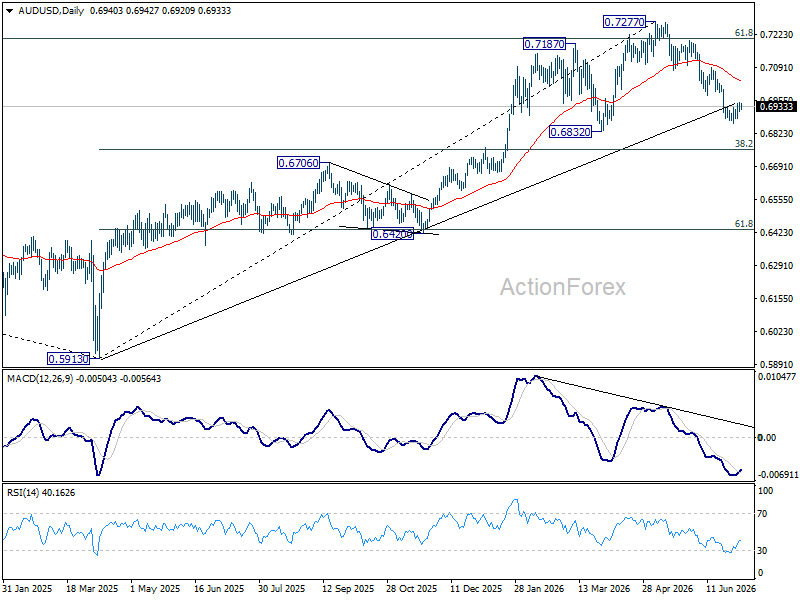

AUD/USD Daily Report

Intraday bias in AUD/USD remains neutral and more consolidations could be seen above 0.6864. Further fall is expected as long as 0.6977 support turned resistance holds. Below 0.6864 will target 0.6832 support. Firm break there will target 0.6756 fibonacci level. However, sustained break of 0.6977 will bring stronger rebound to 0.7087 resistance instead.

In the bigger picture, considering bearish divergence condition in D MACD, a medium term top could be formed at 0.7277 after failing to sustain above 61.8% retracement of 0.8006 (2021 high) to 0.5913 (2024 low) at 0.7206. Deeper fall could be seen to 38.2% retracement of 0.5913 to 0.7277 at 0.6756 as a correction. But strong support should be seen there to bring rebound. Consolidations would continue below 0.7277 for a while.

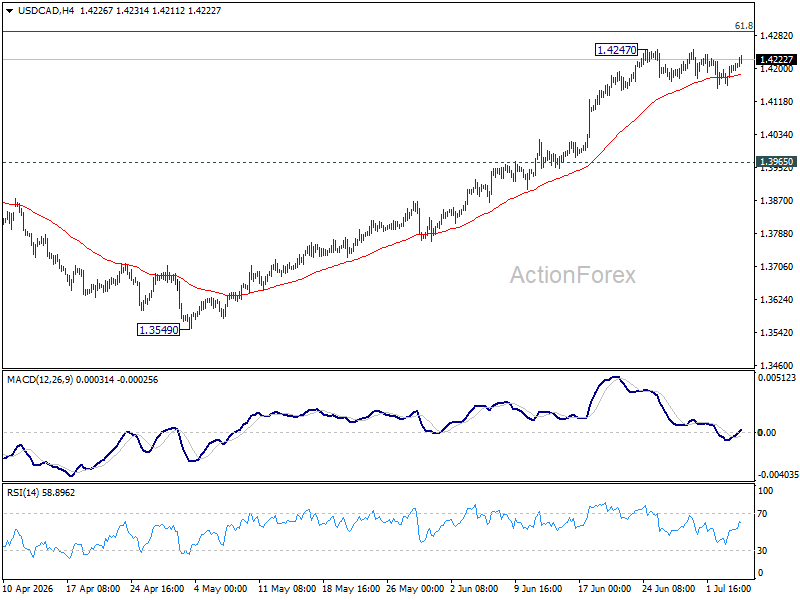

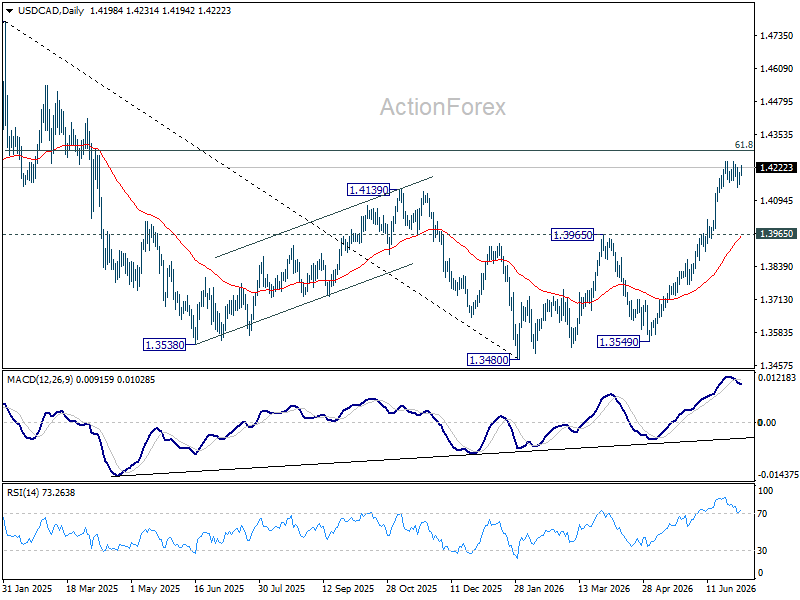

USD/CAD Daily Outlook

Intraday bias in USD/CAD remains neutral as consolidations continues below 1.4247. Deeper pullback cannot be ruled out. But downside should be contained above 1.3965 resistance turned support. Above 1.4247 will resume the rally from 1.3480 to 61.8% retracement of 1.4791 to 1.3480 at 1.4290. Firm break there will pave the way back to 1.4791 high.

In the bigger picture, current development suggests that fall from 1.4791 has completed as a three wave correction to 1.3480. It's still early to judge if rise from there a corrective bounce, or resumption of the larger up trend from 1.2005 (2021 low). But in either case, retest of 1.4791 high should be seen next.

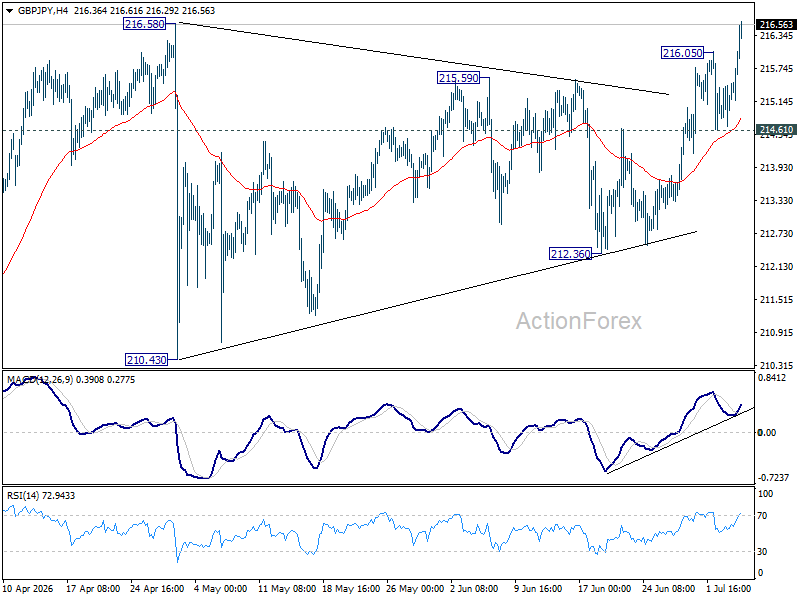

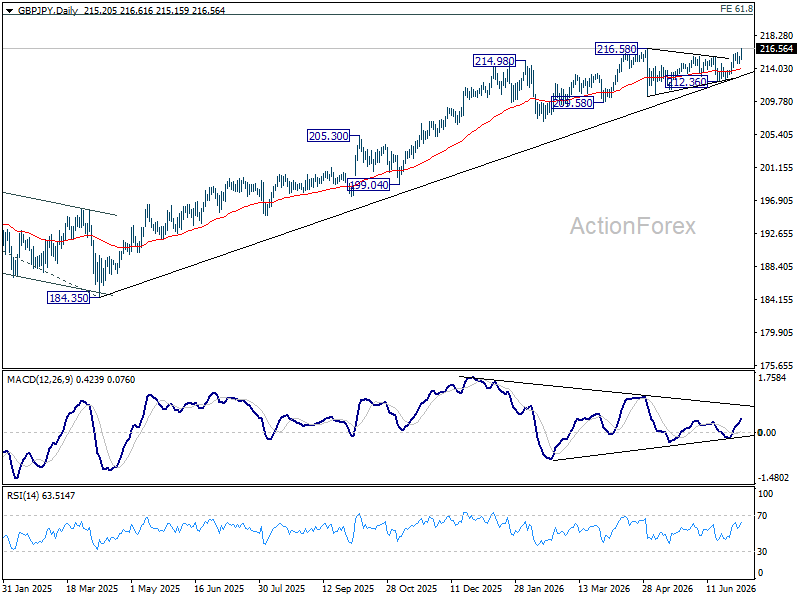

GBP/JPY Daily Outlook

GBP/JPY's strong rally today and breach of 216.58 suggests that larger up trend is resuming. Intraday bias is back on the upside. Sustained trading above 216..58 will target 220.90 fibonacci projection. For now, risk will stay on the upside as long as 214.61 support holds, in case of retreat.

In the bigger picture, there is no clear sign of trend reversal yet. The long term up trend could still extend to 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90 on resumption. However, sustained break of 55 W EMA (now at 207.89) will argue that it's already in medium term down trend for 184.35 support.

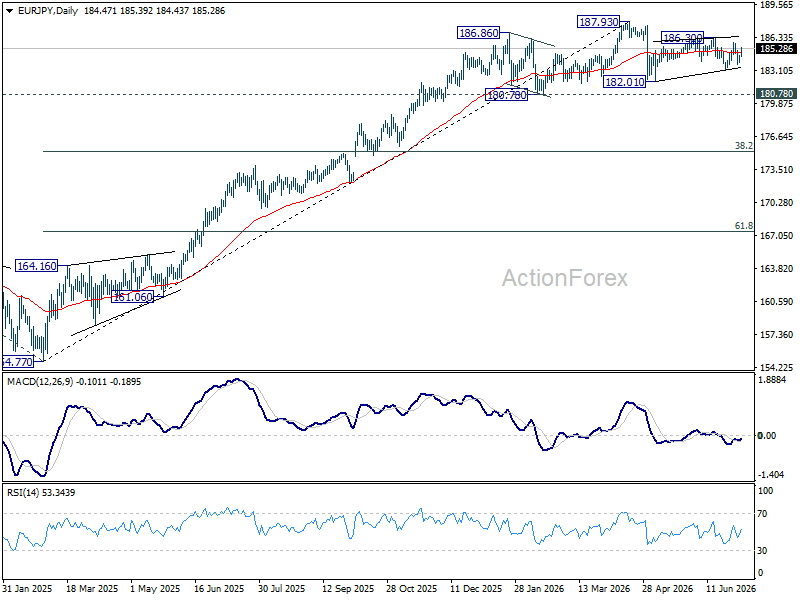

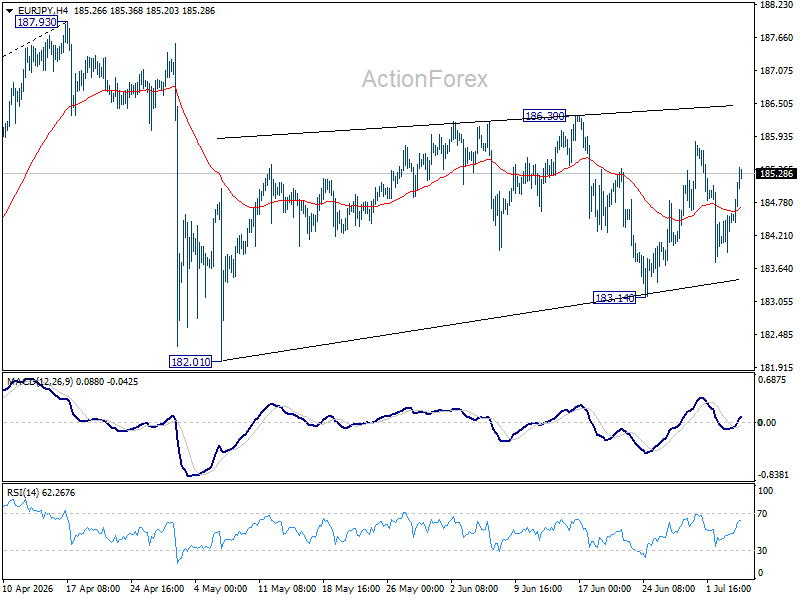

EUR/JPY Daily Outlook

EUR/JPY rebounded strongly today but stays in range of 183.14/186.30. Intraday bias remains neutral for the moment. On the upside, break of 186.30 will resume the rebound from 182.01 to retest 187.93 high. On the downside, break of 183.14 will target 182.10 support next.

In the bigger picture, there is no sign of reversal yet. Uptrend from 114.42 (2020 low) is still expected to resume at a later stage to 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88. However, sustained break of 55 W EMA (now at 179.76) will argue that it's already in a medium term down trend to 175.41 resistance turned support and below.