Sample Category Title

ECB’s Schnabel: Falling Oil Prices Don’t Mean Inflation Battle Is Over

European Central Bank Executive Board member Isabel Schnabel cautioned that the recent decline in oil prices should not be interpreted as a return to pre-war inflation conditions, arguing that underlying price pressures remain elevated. "Does the decline in oil prices mean that we are back to the pre-war situation? I don't think so," she said on Monday, warning that the Middle East peace deal is still fragile and that markets continue to signal higher oil prices over longer horizons.

Schnabel noted that gas prices remain around 40% above pre-war levels, while refining margins are still elevated, with crack spreads "twice their pre-war levels." She also pointed to ongoing pipeline and supply chain pressures, adding that "core inflation remained strong." Together, these factors suggest that lower crude oil prices alone are insufficient to ease broader inflationary pressures facing the Eurozone economy.

She also highlighted emerging climate-related risks, saying that Europe's heatwave and the developing Super El Niño could push food prices higher, while declining rainwater levels threaten to disrupt transport and supply chains. The remarks reinforce the ECB's cautious stance on inflation and suggest policymakers are not yet ready to rule out further tightening, even as markets increasingly expect the central bank to leave interest rates unchanged at its July meeting.

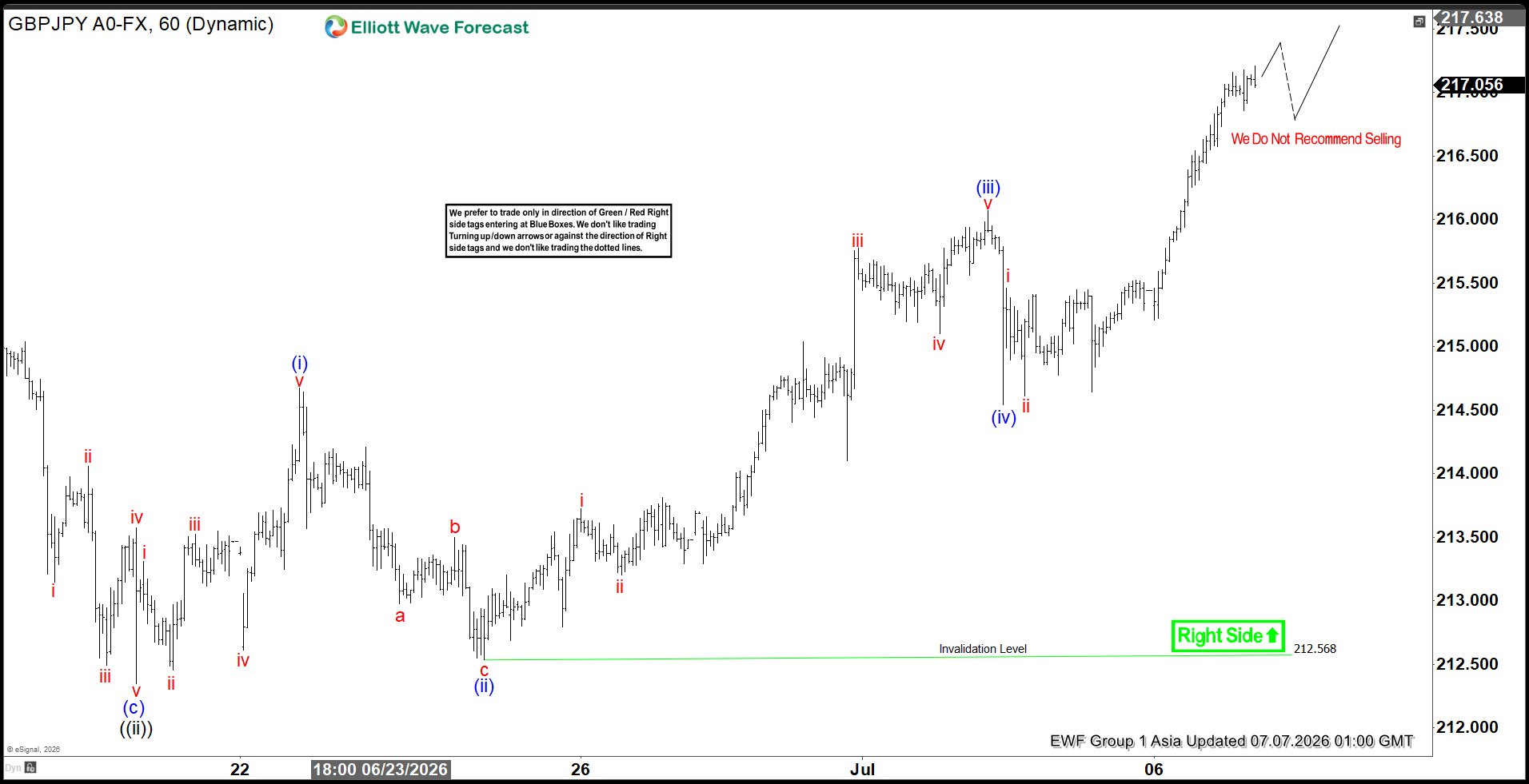

GBPJPY Elliott Wave Outlook: Break to New High Confirms Bullish Trend

The GBPJPY pair has decisively broken to a new high, thereby confirming the prevailing bullish trend. This development underscores the presence of a bullish sequence that favors continued upside momentum. In the short term, the rally from the May 1, 2026 low is unfolding as a clear five‑wave advance. From that low, wave ((i)) concluded at 215.6, followed by a corrective pullback in wave ((ii)) that ended at 212.3. The market has since resumed higher, with wave ((iii)) progressing as another five‑wave structure, reinforcing the strength of the upward cycle.

Within wave ((iii)), the internal subdivision is evident. Wave (i) terminated at 214.67, while the subsequent pullback in wave (ii) found support at 212.26. The pair then advanced in wave (iii) towards 216.06, before a modest retracement in wave (iv) ended at 214.54. The resumption higher in wave (v) has been underway, aiming to complete wave ((iii)) and solidify the bullish sequence. Once wave ((iii)) concludes, expectations call for a corrective phase in wave ((iv)), which should adjust the cycle from the June 19, 2026 low. This correction is anticipated to be temporary, paving the way for renewed strength in the next upward leg.

Near term, the critical pivot at 212.56 remains intact. As long as this level holds, dips are expected to attract buyers, either in a three‑swing or seven‑swing corrective sequence, thereby supporting further upside potential. The overall structure continues to favor higher prices, with corrections viewed as opportunities within the broader bullish trend.

GBPJPY 60-Minute Elliott Wave Chart

GBPJPY Elliott Wave Video:

https://www.youtube.com/watch?v=jN3aRpQtfd4

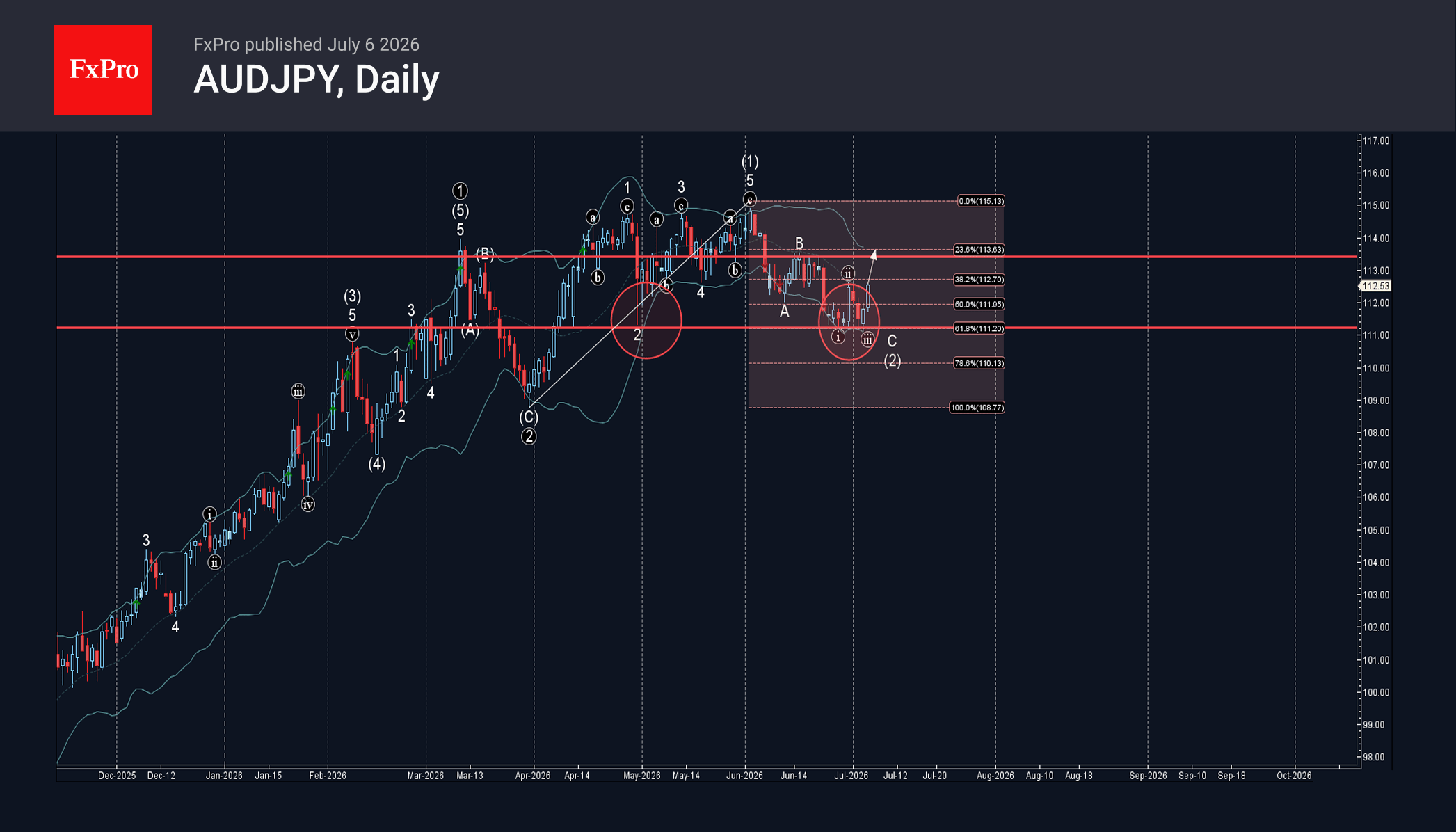

AUDJPY Wave Analysis

AUDJPY: ⬆️ Buy

– AUDJPY reversed from support zone

– Likely to rise to next resistance level 113.40

AUDJPY currency pair recently reversed from the support zone between the key support level 111.25 (which stopped wave 2 in April), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse (1) from March.

The upward reversal from this support zone stopped the previous minor impulse wave C – that belongs to the ABC correction (2) from the start of June.

Given the clear daily uptrend, AUDJPY currency pair can be expected to rise to the next resistance level 113.40 (top of wave B).

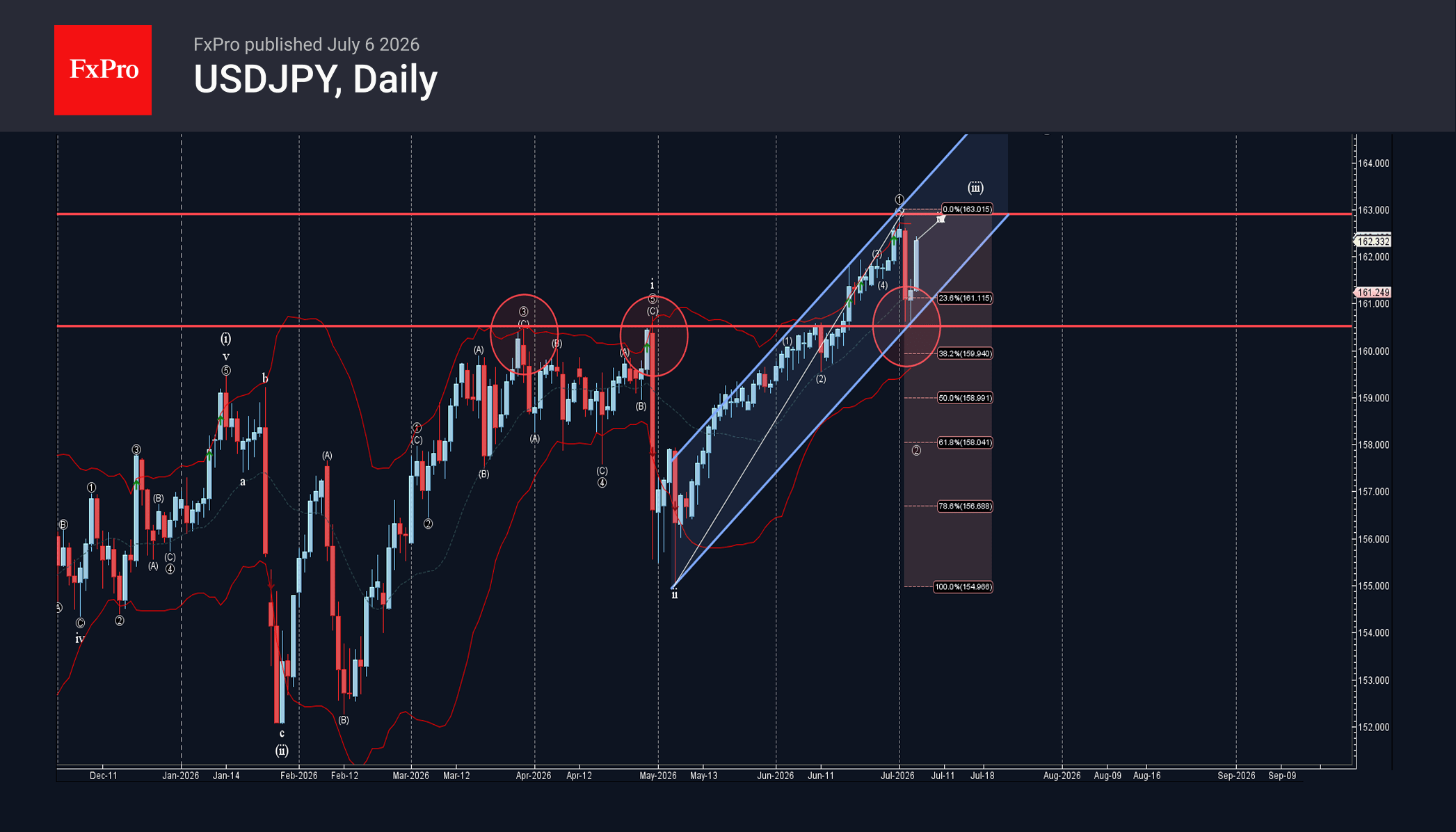

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

– USDJPY reversed from pivotal support level 160.50

– Likely to rise to resistance level 163.00

USDJPY currency pair recently reversed from the support area zone between the pivotal support level 160.50 (former monthly high from March and April), 38.2% Fibonacci correction of the upward impulse from March and the support trendline of the daily up channel from May.

The upward reversal from this support area will most likely form the daily Japanese candlesticks reversal pattern Morning Star.

Given the strong daily uptrend and strong US dollar inflows, USDJPY currency pair can be expected to rise to the next resistance level 163.00.

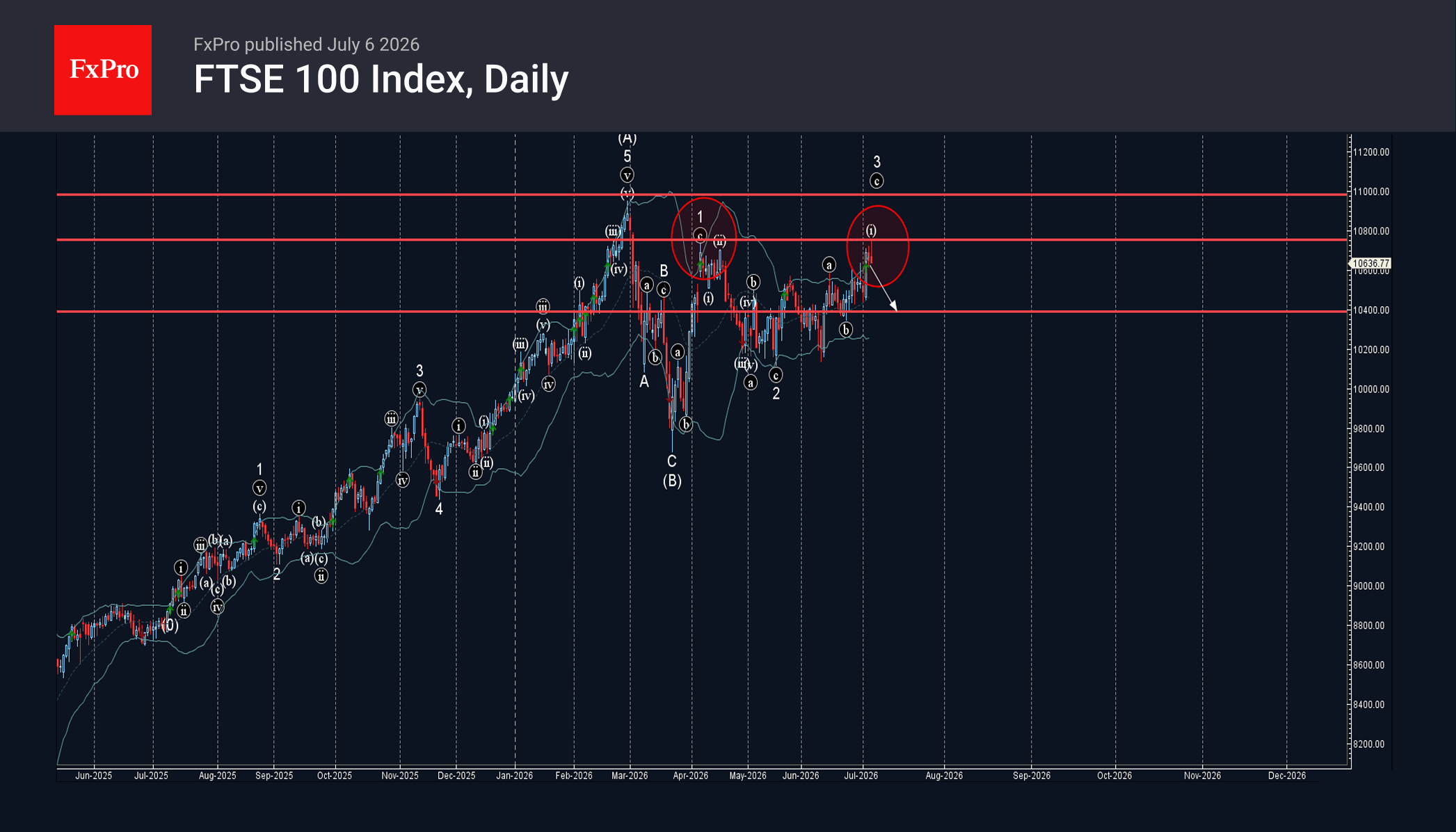

FTSE 100 Index Wave Analysis

FTSE 100: ⬇️ Sell

– FTSE 100 reversed from key resistance level 10750.00

– Likely to fall to support level 10400.00

FTSE 100 recently reversed from the resistance area zone between the key resistance level 10750.00 (which stopped wave 1at the start of April) and the upper daily Bollinger Band.

The downward reversal from this resistance area stopped the previous sharp upward impulse wave 3 from the middle of May.

Given the strength of the resistance level 10750.00, FTSE 100 can be expected to fall to the next support level 10400.00.

Eco Data 7/7/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Labor Cash Earnings Y/Y May | 3.20% | 3.40% | 3.50% | 3.60% |

| 23:30 | JPY | Overall Household Spending Y/Y May | -0.40% | -2.20% | -0.50% | |

| 05:00 | JPY | Leading Economic Index May P | 116.8 | 116.9 | 116.1 | |

| 06:00 | EUR | Germany Industrial Production M/M May | 0.90% | 0.40% | 0.40% | 0.20% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jun | 759B | 711B | ||

| 12:30 | CAD | Trade Balance (CAD) May | 4.2B | 2.8B | 2.7B | 3.4B |

| 12:30 | USD | Trade Balance (USD) May | -77.6B | -78.8B | -55.9B | -54.6B |

| 14:00 | CAD | Ivey PMI Jun | 56.2 | 59.1 | 58.2 |

| 23:30 | JPY |

| Labor Cash Earnings Y/Y May | |

| Actual | 3.20% |

| Consensus | 3.40% |

| Previous | 3.50% |

| Revised | 3.60% |

| 23:30 | JPY |

| Overall Household Spending Y/Y May | |

| Actual | -0.40% |

| Consensus | -2.20% |

| Previous | -0.50% |

| 05:00 | JPY |

| Leading Economic Index May P | |

| Actual | 116.8 |

| Consensus | 116.9 |

| Previous | 116.1 |

| 06:00 | EUR |

| Germany Industrial Production M/M May | |

| Actual | 0.90% |

| Consensus | 0.40% |

| Previous | 0.40% |

| Revised | 0.20% |

| 07:00 | CHF |

| Foreign Currency Reserves (CHF) Jun | |

| Actual | 759B |

| Consensus | |

| Previous | 711B |

| 12:30 | CAD |

| Trade Balance (CAD) May | |

| Actual | 4.2B |

| Consensus | 2.8B |

| Previous | 2.7B |

| Revised | 3.4B |

| 12:30 | USD |

| Trade Balance (USD) May | |

| Actual | -77.6B |

| Consensus | -78.8B |

| Previous | -55.9B |

| Revised | -54.6B |

| 14:00 | CAD |

| Ivey PMI Jun | |

| Actual | 56.2 |

| Consensus | 59.1 |

| Previous | 58.2 |

NZD/CHF Analysis: Which Currency Breaks the Consolidation First?

NZD/CHF remains locked in a tight range as traders await the next monetary policy catalyst.

The Reserve Bank of New Zealand heads into Wednesday's meeting on shaky ground. After May's 3-3 split was resolved by a casting vote, the committee still lifted its rate path sharply, eyeing a 3.28% terminal rate by 2029. But the oil slide following the US-Iran truce has cut hike odds from over 80% to around 66-70%, splitting major banks between a hold and a further move.

Meanwhile, the Swiss National Bank holds firm at 0% for a fourth straight meeting. Switzerland's challenge mirrors New Zealand's in reverse: subdued inflation rather than overheating, leaving little room—or need—for tightening. The franc's strength stems more from so-called safe-haven flows than rate differentials.

The result: NZDCHF caught between short-term RBNZ uncertainty and near-static Swiss policy, with direction hinging on Wednesday's decision.

Technical Analysis of NZD/CHF

NZD/CHF remains locked in a broader consolidation on higher timeframes, trapped between resistance at 0.4660-0.4690 and support at 0.4540-0.4560. Price is now compressing into a tighter triangle just below the 100-period EMA, which continues to cap upside as dynamic resistance.

Bullish Scenario

Fundamentally, a hawkish RBNZ surprise on Wednesday—hiking despite the oil-driven pullback in tightening expectations—would give the kiwi a strong tailwind. Technically, buyers first need to break the descending trendline capping price since late May, already rejected on several attempts. Once cleared, the decisive test becomes the 0.4660-0.4690 resistance zone. A genuine breakout would likely require both a strong NZD fundamental catalyst and confirming technical momentum.

Bearish Scenario

Conversely, a dovish hold—as several major banks now expect—could reignite downside pressure. Technically, sellers first need to break the ascending trendline price has leaned on in recent sessions, then push through the more significant 0.4540-0.4560 support. Notably, the 100-period EMA continues to act as reliable dynamic resistance, keeping price capped beneath it and reinforcing the bearish structure until proven otherwise.

Two central banks, two opposite stories: RBNZ still weighing when to tighten, SNB content to sit still. Wednesday's decision could finally break this narrowing range — will the kiwi's rate case win out, or does the franc's quiet resilience hold firm?

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

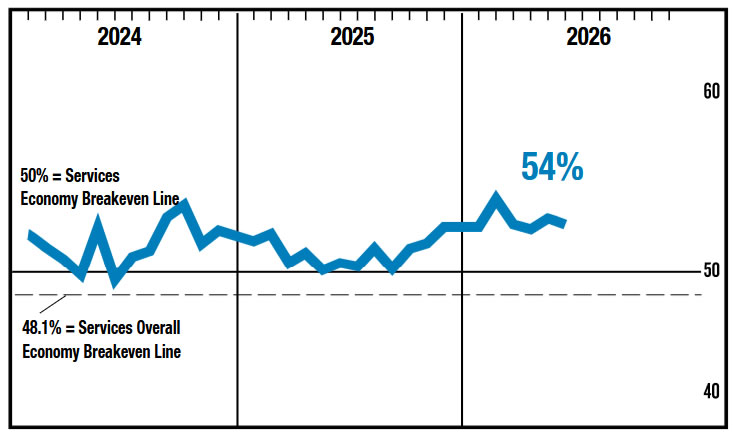

ISM Services in June Shows Softer Demand, but Improved Hiring and Still-Elevated Price Pressures

- The ISM Services index slipped 0.5 points from 54.5 in May to 54.0 in June, remaining in expansionary territory for a 24th consecutive month.

- Demand moderated but stayed healthy, with the new orders index falling 2.2 points to 55.1 after May’s sharp rebound.

- Current output cooled from a firm pace, as business activity declined 2.3 points to 55.4 while remaining solidly above the 50 threshold.

- Labor market conditions improved, with employment rising 3.3 points to 51.2 and returning to expansion for the first time in four months.

- Price pressures eased but remained elevated, with the prices paid index falling 3.6 points to 67.7—its first reading below 70 since February, but still above 60 for a 19th straight month.

- The largest move came from inventories, which fell 11.3 points to 51.2 after May’s record-high reading, while supplier deliveries eased slightly to 54.4 and backlogs rose 3.6 points to 54.9.

Key Implications

- The June report points to a modest cooling in services momentum. The headline index, business activity and new orders all eased from May’s stronger readings but remained comfortably in expansionary territory. The sharp pullback in inventories was the standout move, suggesting May’s stock building surge was not sustained, but the rise in backlogs indicates that demand is still firm enough to keep pressure on capacity. Importantly, employment moved back into expansion, reducing some of the prior concern that firms were relying on productivity gains rather than hiring to meet demand.

- Price conditions improved at the margin but remain a key concern. The prices index fell below 70 for the first time since February, helped by mixed reports on fuel-related costs, but it remains well above the 50 threshold and has been above 60 for 19 consecutive months. Taken together, the report shows services demand still expanding, hiring improving and cost pressures easing gradually - a mix the Fed is likely to view as consistent with patience rather than a clear green light to move.

US ISM Services Slips in June as Price Pressures Ease and Employment Rebounds

US ISM Services PMI edged down from 54.5 to 54.0 in June, missing expectations of 54.2 but remaining comfortably above the 50 threshold that separates expansion from contraction. The report pointed to continued growth in the services sector, although activity and demand moderated slightly from the previous month.

Business Activity/Production eased from 57.7 to 55.4, while New Orders slipped from 57.3 to 55.1, suggesting growth remained solid but lost some momentum. A notable bright spot came from the labor market, with the Employment Index rising sharply from 47.9 to 51.2, returning to expansion for the first time in four months. ISM noted that a Services PMI reading of 54.0 is historically consistent with annualized real GDP growth of about 1.9%.

Inflation pressures also showed signs of easing. The Prices Index fell from 71.3 to 67.7, dropping below 70 for the first time since February, although it has remained above 60 for 19 consecutive months. ISM said some respondents reported lower gasoline and diesel costs, but petroleum-related products continued to face price increases as earlier oil shocks worked through supply chains. Those pressures are expected to ease later this year if recent progress in restoring oil flows through the Strait of Hormuz continues.

| Indicator | Previous | Latest | Expectation |

|---|---|---|---|

| ISM Services PMI | 54.5 | 54.0 | 54.2 |

Key Components

| Component | Previous | Latest | Comments |

|---|---|---|---|

| Business Activity / Production | 57.7 | 55.4 | Growth moderated but remained above its 12-month average of 55.1 |

| New Orders | 57.3 | 55.1 | Demand eased but continued to expand |

| Employment | 47.9 | 51.2 | Returned to expansion for the first time in four months |

| Prices | 71.3 | 67.7 | Lowest since February; still above 60 for the 19th consecutive month |

Sunset Market Commentary

Markets

US investors returned after enjoying a long weekend in observance of Independence Day. However, it hardly brought new impetus to the trading dynamics. With very little in the way of important EMU data, EU (and UK) yields held very tight ranges, changing less than 1.5 bp across the curve. US bonds still see minor follow-through gains after Thursday's softer than expected US payrolls. With Brent oil currently holding in the $71–72 p/b area, quite some inflation improvement may be discounted. The theme of fiscal sustainability continues to linger. Long-term Japanese government bond yields again touched multi-year peak levels for the 10-y and 20-y (4.1 bps and 3.8 bps respectively). After an unconvincing 10-y auction last week, a next reality check comes as soon as tomorrow, with a 30-y JGB auction. Moves in intra-EMU government bond spreads (vs swap) still develop orderly. Still, spreads vs swaps (10-y) of the likes of Italy (72 bps), France (73 bps), Belgium (51 bps) or Spain (43 bps) are off the levels before the start of the conflict between the US and Iran. On other markets, several tech/AI-related indices again traded volatile this morning (Kospi, e.g.), but some calm returned. The EuroStoxx 50 touched an all-time record, but currently cedes 0.4%. US equities also again try to overcome doubts on tech/AI. The Nasdaq gains 0.85% at the open, but price action last week shows that intraday trends can change quickly.

On FX markets, the dollar gains modestly despite a limited loss in interest rate support. DXY regains the 101 mark. EUR/USD eases from 1.144 to 1.142. For now it's not clear yet whether (and to what extent) sustainability of public finances might affect the likes of the euro, the dollar and/or sterling. Fiscal intentions of the Burnham government still have to be concretized, but sterling continues to perform quite well. After last week's break below EUR/GBP 0.86, sterling today again gains a few ticks against the euro, nearing the 0.855 area. Japanese authorities didn't use Friday's 'USD correction' post-payrolls or lower market liquidity to force out some JPY shorts. Today at least it looks that this window of opportunity is closing with USD/JPY rebounding near 162.3 compared to a 160.49 low on Friday and a multi-year top of 162.84 earlier last week. The combination of a 30-y auction, the yen testing multi-year lows and Japanese authorities playing some kind of poker with markets on the intervention strategy, might cause quite a hefty mix tomorrow morning. After finishing this report, the US services ISM still will be released, but probably a big surprise is needed to trigger a sustained market reaction.

News & Views

The European Stability Mechanism, lender of last resort for euro area countries, released its inaugural annual Euro Area Stability Watch report today. It warns the bloc won't be immune to the shocks that lie ahead. The ESM sees three important pockets of vulnerability. The first one is eroding fiscal space, in part driven by increased defence spending needs. The second is a structural exposure to energy supply disruptions stemming from geopolitical tensions. Lastly, the ESM says European investors are exposed to a potential repricing of US Treasuries and equities. It added that EA sovereign markets meanwhile are becoming increasingly reliant on price-sensitive investors (e.g. hedge funds). The ESM came up with an adverse scenario (relative to the European Commission's baseline), defined as two shocks materializing simultaneously: prolonged geopolitical tensions which raise energy prices and keep uncertainty high, and a sharp repricing of US assets. That would push the euro area economy into a recession with negative y/y growth through 2027 Q4, raise inflation to almost 5% by end 2026 and put public debt on a further upward path. The ESM urges countries to quickly rebuild fiscal buffers, spend efficiently and advance structural reforms so they come prepared when the next shock hits.

Belgium's budget monitoring committee in a preliminary estimate offered to the government said an additional €7.9bn fiscal effort is needed by end-2029 to be compliant with the European deficit rules (expenditure-based), several Belgian news outlets reported. The Middle East conflict, which resulted in higher inflation and lower economic growth, and a higher interest rate burden has thrown government finances further off track. The €7.9bn is significantly more than the €4.9bn the committee expected in its March report and topped the approximately €7bn the government had been bracing for internally. An unchanged policy would lift the budget deficit by the end of De Wever I in 2029 to 5.8% and further to 6.3% in a five-year horizon. The debt ratio would climb from 108% this year to 117% in 2029 and 122.8% in 2031.