Sample Category Title

US: Retail Sales Continued to Rise in August

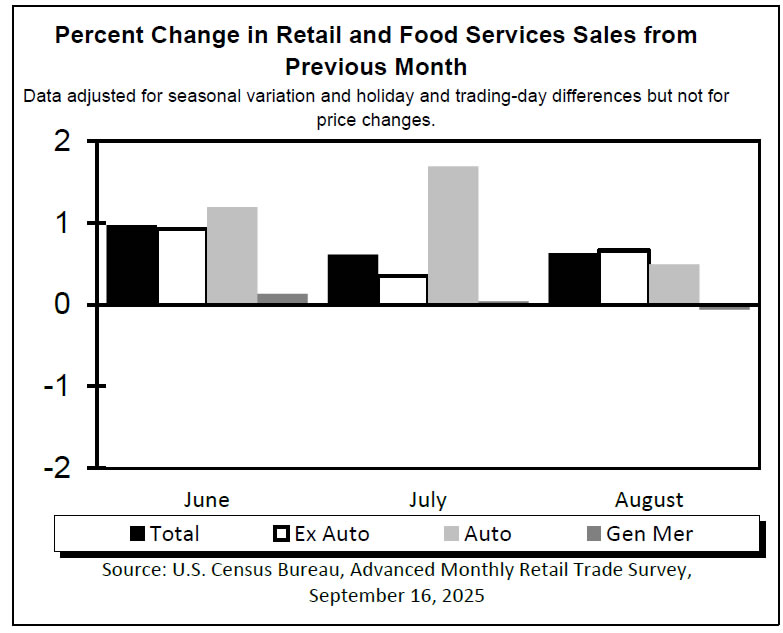

Building on their gain in July, retail and food services sales continued to grow in August, advancing by 0.6% month-on-month (m/m) and matching July's gain. Today's result was stronger than consesus expectations for a 0.2% gain.

Sales of autos & parts as well as sales at the gasoline stations both rose by 0.5% on the month. Sales at the building materials and garden equipment & supplies stores were little changed (+0.1% m/m).

Sales in the "control group", which excludes the three volatile components mentioned above (i.e., autos, gasoline and building supplies) were up by a healthy 0.7%. Online sales led the gains, with sales at non-store retailers rising by 2% on the month. Clothing stores had another good month, with sales rising by 1.0% - a sixth consecutive monthly increase. Sales of sporting goods & hobby items were also higher (+0.8%). Miscellaneous (-1.1%), general merchandise stores (-0.1%), health & personal care stores (-0.1%) and furniture (-0.3%) retailers were the categories where sales were lower.

Sales at bars and restaurants – the only service category in the report – rebounded by 0.7%, following a flat reading in the prior month.

Key Implications

There was not much to complain about in this report. Retail sales continued to rise at a decent clip for the third consecutive month, with above-consensus print for both core and headline numbers. Decent retail sales over the last few of months suggest that consumer spending growth is likely to come in around 2% (annualized) in the third quarter. This is still modest growth, particularly when compared with the 3.5% pace seen in the second half of last year, but better than our initial tracking.

Consumers may have breathed a sigh of relief that their worst inflation fears have not materialized, however, the impact of tariffs continues to show up in core goods prices. Up until recently, businesses have tried to absorb higher costs and shield consumers, but inflation data over the last few months have shown that some of the costs are now being passed on. We expect greater pass through of tariff-related price increases over the coming months. With the labor market downshifting and cost pressures heating up, consumer spending momentum is likely to remain modest through year-end.

Sunset Market Commentary

Markets

With the upcoming Fed meeting looming – one which should see rates reduced for the first time since December – it would take something material to lure investors from the sidelines back into the market arena. US retail sales tried by coming in better than expected across the board. Headline sales rose 0.6% on a non-inflation adjusted monthly basis while the control group (used in GDP calculations) added 0.7%. Last month’s figures saw a slight upward adjustment as well. But the NY Fed’s services business activity indicator unexpectedly slumped to one of the weakest levels in recent years (-19.4 from 11.7) with weak details, including for the forward-looking gauge. It basically confirmed the message coming from the manufacturing series published yesterday. The mixed bag of data left no permanent marks on rates. The latter eventually turned south in early US dealings with changes varying between -2.7 (2-yr) and -0.2 bps (30-yr). German Bunds underperform, driven by the long end of the curve. The 30-yr rises 2.6 bps. The French spread overtook the Italian one yesterday and that remains the case today. It’s a symbolically important sign of the times. A nervous dollar loses some ground against G10 peers. The greenback on a trade-weighted basis hits a two-month low in the 97 area. EUR/USD rose to fall just short of the July high at 1.1829. The pair is currently trading around 1.1822 and seems eager for a leap higher. A nod from Fed chair Powell could be needed for a sustained break though. The 2-yr tenor hovers near important support at the 2024/2025 lows. In other Fed-related news, the US White House said it’ll appeal Monday’s court decision that affirmed Fed’s Cook can continue do her job with her lawsuit challenging Trump’s move to fire her pending. It seems that, at least for the September meeting, Cook will be able to cast her vote as member of the Board nonetheless. The UK labour market report came in largely as expected. Sterling shrugged and EUR/GBP followed EUR/USD higher. UK assets, including gilts, are now eying tomorrow’s CPI release and Thursday’s BoE annual decision on QT. It is near certain that the £100bn of the last three years will be reduced since it would mean topping up the £50bn passive rundown by the same amount. That could pressure an already jittery gilt market.

News & Views

The Hungarian Statistical office today published Full time employers’ average earnings data. Average gross earnings in July grew by 9.0% Y/Y down from 9.7% in June (-1.5% M/M). Private sector wages declined 1.7% M/M bringing the Y/Y measure to 8.7% from 9.7%. After a strong 3.7% M/M gain in June, public sector wages declined a modest 0.5% M/M still raising the Y/Y measure from 9.5% to 10%. Net earnings increased by 9.4% and real earnings were 4.9% higher compared to the same month last year. The overall outcome of the report was slightly softer than expected. Even so, it doesn’t profoundly change the outlook for MNB policy in the short term as wage growth is still expected to remain elevated. The MNB in its latest inflation report (June 2025) expected whole economy gross wage growth of 9.2% this year, accelerating back to 10.5% next year. Short-term HUF rates held stable today (2-y swap 6.15%). Money markets hardly see any chance the MNB already being able to further reduce the policy rate (6.5%) this year. The forint in the meantime is testing the strongest levels in more than a year (EUR/HUF 390 area).

Canadian CPI declined 0.1% M/M (NSA) raising the Y/Y measure from 1.7% to 1.9%, falling below consensus expectations (2.0% Y/Y). Gasoline prices falling to a lesser extent year over year in August (+1.4% M/M; -12.7% Y/Y) than in July (-16.1%) were an important driver behind the faster growth in headline inflation. Excluding gasoline, the CPI rose 2.4% in August, after increasing 2.5% in each of the previous three months. Moderating the acceleration in the all-items CPI were lower prices for travel tours and fresh fruit compared with July, statistics Cananda comments. Shelter prices rose a modest 0.1% M/M and 2.6% Y/Y (from 3.0%). Core inflation (trim measure) eased slightly to 3.0% from 3.1%. Even as core inflation still holds above the 2% target, softer activity data, including poor labour market data for July and August, are expected to push the Bank of Canada to restart its easing cycle and cut the policy rate tomorrow from 2.75% to 2.5%. The loonie gains modestly today against a broadly weaker US dollar (USD/CAD 1.375).

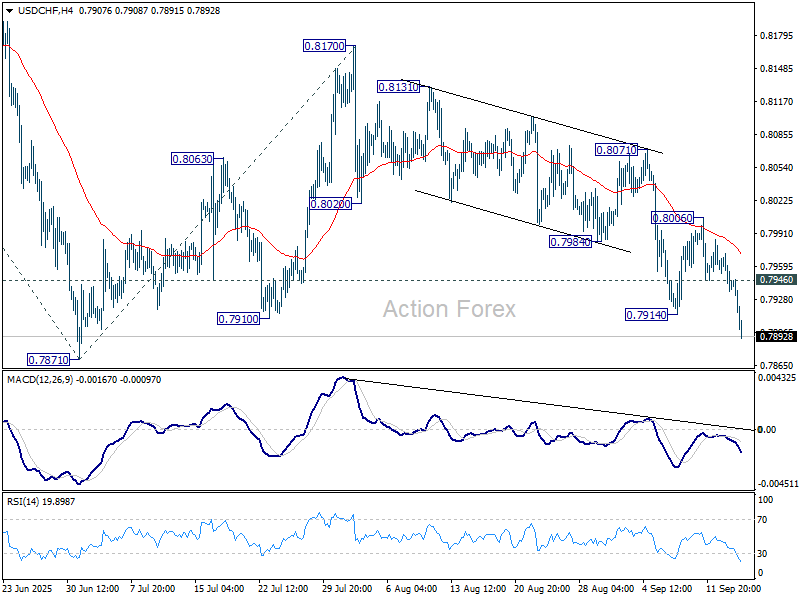

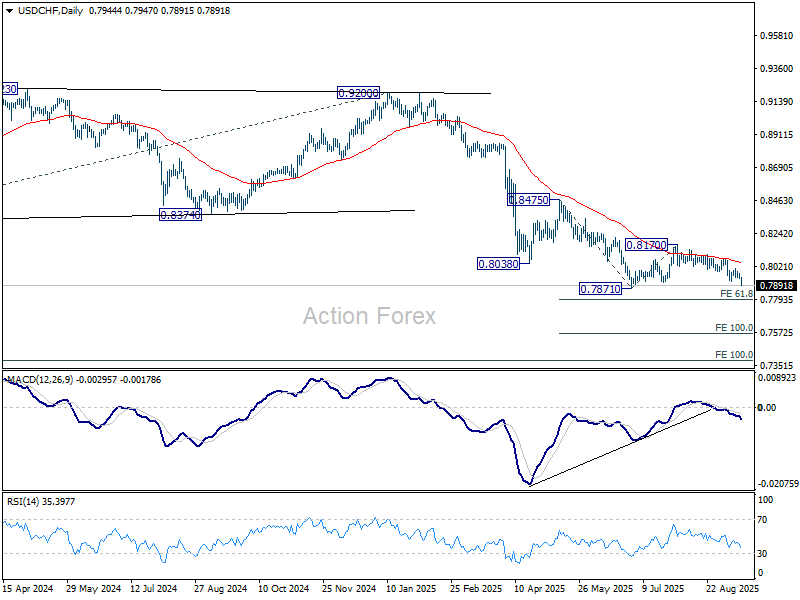

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7931; (P) 0.7953; (R1) 0.7968; More….

Intraday bias in USD/CHF is back on the downside with break of 0.7914 support. Further fall should be seen to retest 0.7871 low. Decisive break there will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797. On the upside, above 0.7946 minor resistance will turn intraday bias neutral again.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

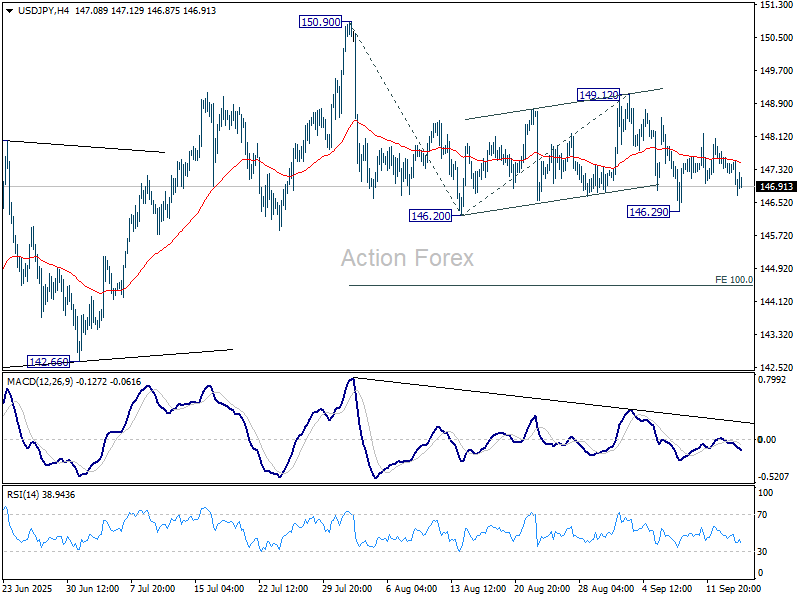

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 147.15; (P) 147.48; (R1) 147.73; More...

Intraday bias in USD/JPY remains neutral a,d with 149.12 resistance intact, further fall is in favor. On the downside, firm break of 146.29 support will solidify the case that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 100% projection of 150.90 to 146.20 from 149.12 at 144.42.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

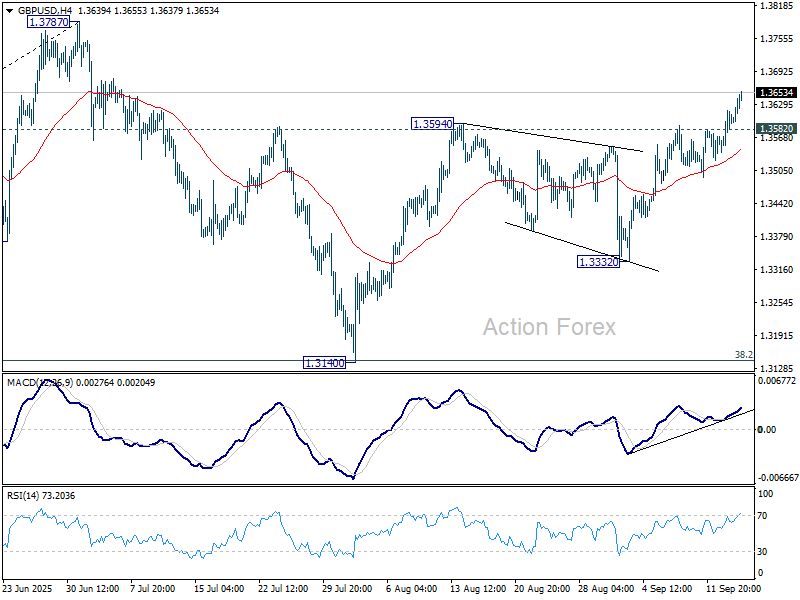

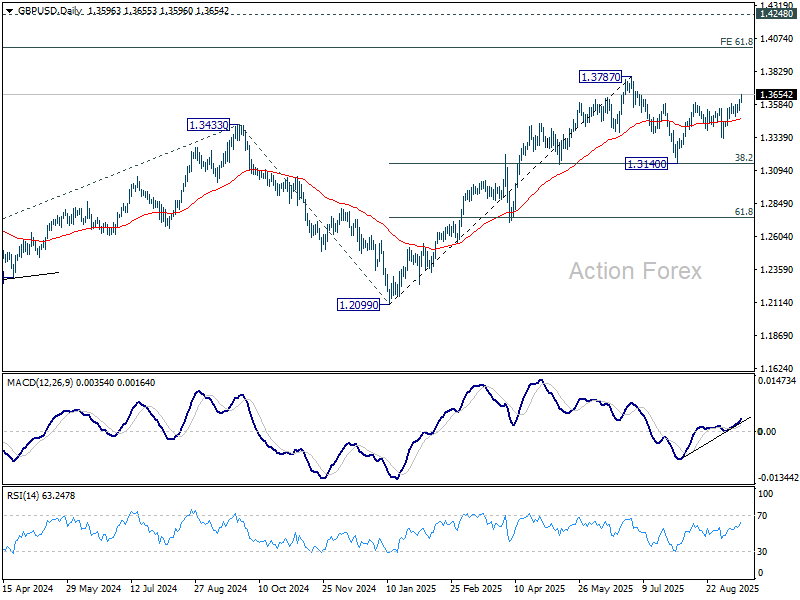

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3588; (R1) 1.3629; More...

GBP/USD's rally from 1.3140 is still in progress and intraday bias remains on the upside for retesting 1.3787 high. Decisive break there will resume larger up trend to 1.4004 projection level. On the downside, below 1.3582 minor support will turn intraday bias neutral first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

Inflation Ticks Higher But Falls Short of Expectations Opening Door for Bank of Canada

Headline CPI inflation for August came in at 1.9% year-on-year (y/y), below expectations for a 2.0% y/y print. August's reading was up from 1.7% in July.

Gasoline prices provided a smaller drag to the headline, down 12.7% y/y from -16.1% last month. On a monthly basis, prices rose 1.5% as higher refiner margins offset lower crude prices.

Prices for cellular services also fell at a slower pace (-1.2%) compared with July (-6.6%) as fewer back-to-school sales were available. Providing an offset was a steeper contraction in travel services (-3.8% y/y in August), with lower demand for destinations in the U.S. being cited by Statistics Canada as a contributor.

The Bank of Canada's (BoC) CPI-trim measure dipped to 3.0% y/y (3.1% in July), while the CPI-median index was unchanged at 3.1% y/y. The CPI excluding food and energy ticked down to 2.4% y/y from 2.5% the month prior and the CPI excluding the eight most volatile components and indirect taxes (CPIX) was unchanged at 2.6% y/y. On a seasonally adjusted monthly basis the CPIX (+0.19% from 0.06%), CPI ex. food and energy (0.13% from 0.07%) and CPI Median (0.23% from 0.14%) all accelerated in August. The CPI trim was the outlier, moderating slightly to 0.19% m/m from 0.23% m/m in July.

Key Implications

Momentum in the right direction from inflation this month, as the expected lift from energy prices had a smaller impact than expected. Moreover, even though three of the core indexes moved higher on the month, the trend towards cooler prints remains favourable.

Looking forward, the Bank of Canada should have room to cut at its meeting tomorrow. The economy continues to show signs of waning momentum as the unemployment rate ticks higher and job losses accumulate. Moreover, the termination of many retaliatory tariffs will help provide some offset to price pressures. We maintain the view that the BoC will have room to deliver two cuts this year to support growth and keep inflation in the target range.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1728; (P) 1.1751; (R1) 1.1786; More...

Intraday bias in EUR/USD remains on the upside with immediate focus on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next. On the downside, below 1.1757 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916, and further to 1.2 psychological level. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.

Dollar Struggles Despite Strong US Retail Sales, EUR/USD Eyes Key 1.1829 Resistance

Dollar remained under pressure today even after U.S. retail sales came in stronger than expected. While the data trimmed expectations of back-to-back Fed cuts in October slightly, with odds dipping yet still holding near 78%, it did little to support the greenback. Markets appear more focused on front-running a dovish outcome from tomorrow’s FOMC decision as the two-day meeting gets underway.

Attention in FX markets is firmly on whether EUR/USD can decisively break through the 1.1829 resistance. Sustained move higher would reinforce the prevailing bearish tone for Dollar and could open room for further gains in European majors.

Overall in the forex markets, Swiss Franc led the pack today. Geopolitical concerns deepened after Romania reported a violation of its airspace by Russian drones, heightening risks of conflict spillover into NATO territory. US President Donald Trump sharpened his stance, directly calling Russia the aggressor in Ukraine—a shift that signals harder U.S. positioning toward Moscow.

Commodity-linked currencies lagged despite the broader risk-on mood. Aussie and Kiwi held steady but underperformed their European peers. The softer inflation print from Canada reinforced expectations of a BoC rate cut tomorrow, but Loonie’s resilience highlights that much of the easing story was already priced in.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is down -0.66%. CAC is down -0.12%. UK 10-year yield is up 0.03 at 4.665. Germany 10-year yield is up 0.026 at 2.719. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI fell -0.03%. China Shanghai SSE rose 0.04%. Singapore Strait Times fell -0.02%. Japan 10-year JGB yield rose 0.002 to 1.604.

US retail sales rise 0.6% mom in August, beat forecasts with broad gains

U.S. retail sales surprised to the upside in August, rising 0.6% mom to USD 732.0B, well ahead of expectations for a 0.2% mom increase. Core categories also posted robust results, with sales excluding autos up 0.7% mom to USD 592.3B and sales excluding gasoline up 0.6% mom to USD 680.3B. Sales excluding both autos and gasoline gained 0.7% mom to USD 540.1B, pointing to broad-based consumer strength.

The latest figures confirm resilience in household spending despite high borrowing costs and moderating labor market conditions. Over the June–August period, total retail sales rose 4.5% yoy, extending steady growth and highlighting the consumer’s role as a key driver of U.S. activity.

Canada CPI edges higher to 1.9% in August, core measures ease

Canada’s headline CPI rose to 1.9% yoy in August, up from 1.7% yoy in July but slightly below market expectations of 2.0% yoy. The increase was largely due to a smaller year-on-year drop in gasoline prices, which fell -12.7% yoy in August compared with -16.1% yoy in July. Excluding gasoline, inflation rose 2.4% yoy, moderating slightly from the consistent 2.5% yoy pace of recent months.

Underlying price pressures showed further signs of cooling. CPI median measure held steady at 3.1% yoy, while the CPI trimmed eased from 3.1% yoy to 3.0% yoy, both matching expectations. CPI common measure slowed to 2.5% yoy, undershooting forecasts of 2.6% and marking a softening in broad-based inflation.

German ZEW sentiment improves, outlook brighter for exports despite weak base

Germany’s ZEW Economic Sentiment index rose more than expected in September, climbing from 34.7 to 37.3 against forecasts of 25.0. The improvement highlights growing optimism among financial market experts, particularly toward export-oriented sectors. However, Current Situation index deteriorated further from -68.6 to -76.4, missing expectations of -65.0.

For the Eurozone, ZEW sentiment index also improved, rising from 25.1 to 26.1, ahead of consensus at 20.3. Current Situation measure edged higher by 2.4 points to -28.8.

ZEW President Achim Wambach noted that while the sentiment indicator has stabilized, “the economic situation has worsened” and significant risks remain. He cited uncertainty over U.S. tariff policy and Germany’s upcoming “autumn of reforms.” Outlooks have improved for autos, chemicals, pharmaceuticals, and metals, but sentiment for these sectors remains in negative territory, showing recovery prospects are fragile.

Eurozone industrial output rises 0.3% mom, energy drag offsets goods gains

Eurozone industrial production rose 0.3% mom in July, missing expectations of a 0.5% mom gain. Output was supported by intermediate goods (+0.5%), capital goods (+1.3%), and consumer goods, with durable and non-durable production up 1.1% and 1.5% respectively. However, a sharp -2.9% decline in energy output capped overall growth.

Across the wider EU, industrial production increased 0.2% mom on the month. Croatia led gains with a 2.6% rise, followed by Hungary and Slovenia at 2.1% each, while steep drops were recorded in Estonia (-5.5%), Malta (-4.7%), and Sweden (-3.9%).

UK job losses continue, pay growth still strong

UK labor market data for August showed further signs of strain, with payrolled employment falling by -8k on the month, extending a steady decline since the peak in Q3 2024. Claimant count rose by 17.4k, less than expected 20.3k. Median monthly pay rose 6.6% yoy, up from July’s 6.0%, underlining persistent wage pressures.

In the three months to July, unemployment rate held steady at 4.7%, in line with forecasts. Average earnings excluding bonuses eased slightly from 5.0% to 4.8%, while including bonuses ticked higher from 4.6% to 4.7%. Overall, the figures show employment losses are continuing, but wage growth remains firm enough to keep the BoE cautious on policy.

RBA’s Hunter: Inflation near target, monitoring consumer strength

RBA Assistant Governor Sarah Hunter said today the central bank is “close to getting inflation to target,” with risks around the outlook now appearing "balanced". She emphasized that monetary policy works with a delay and must remain forward looking.

Hunter also noted that household spending has “picked up a bit,” with consumption showing signs of improvement and the broader position “beginning to turn over.” She added the RBA is “very closely monitoring” the underlying strength of consumer demand as it seeks to keep the economy near full employment.

July’s CPI outcome was partly affected by timing of rebates, she explained, while core inflation appears broadly in line with forecasts.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1728; (P) 1.1751; (R1) 1.1786; More...

Intraday bias in EUR/USD remains on the upside with immediate focus on 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next. On the downside, below 1.1757 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916, and further to 1.2 psychological level. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.

US retail sales rise 0.6% mom in August, beat forecasts with broad gains

U.S. retail sales surprised to the upside in August, rising 0.6% mom to USD 732.0B, well ahead of expectations for a 0.2% mom increase. Core categories also posted robust results, with sales excluding autos up 0.7% mom to USD 592.3B and sales excluding gasoline up 0.6% mom to USD 680.3B. Sales excluding both autos and gasoline gained 0.7% mom to USD 540.1B, pointing to broad-based consumer strength.

The latest figures confirm resilience in household spending despite high borrowing costs and moderating labor market conditions. Over the June–August period, total retail sales rose 4.5% yoy, extending steady growth and highlighting the consumer’s role as a key driver of U.S. activity.

{kind=link}

Canada CPI edges higher to 1.9% in August, core measures ease

Canada’s headline CPI rose to 1.9% yoy in August, up from 1.7% yoy in July but slightly below market expectations of 2.0% yoy. The increase was largely due to a smaller year-on-year drop in gasoline prices, which fell -12.7% yoy in August compared with -16.1% yoy in July. Excluding gasoline, inflation rose 2.4% yoy, moderating slightly from the consistent 2.5% yoy pace of recent months.

Underlying price pressures showed further signs of cooling. CPI median measure held steady at 3.1% yoy, while the CPI trimmed eased from 3.1% yoy to 3.0% yoy, both matching expectations. CPI common measure slowed to 2.5% yoy, undershooting forecasts of 2.6% and marking a softening in broad-based inflation.