Sample Category Title

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9338; (P) 0.9347; (R1) 0.9356; More...

No change in EUR/CHF's outlook as consolidations continue above 0.9313. Intraday bias stays neutral and further decline is expected with 0.9394 resistance intact. On the downside, break of 0.9313 will resume the fall from 0.9452 to retest 0.9218 low. On the upside, break of 0.9394 will bring stronger rally towards 0.9452 resistance instead.

In the bigger picture, the down trend from 0.9204 (2018 high) might still be in progress considering that EUR/CHF is staying well inside the long term falling channel. However, with bullish convergence condition in W MACD, downside potential should be limited in case of another fall. Instead, firm break of 0.9660 resistance will be an important sign of medium term bullish trend reversal.

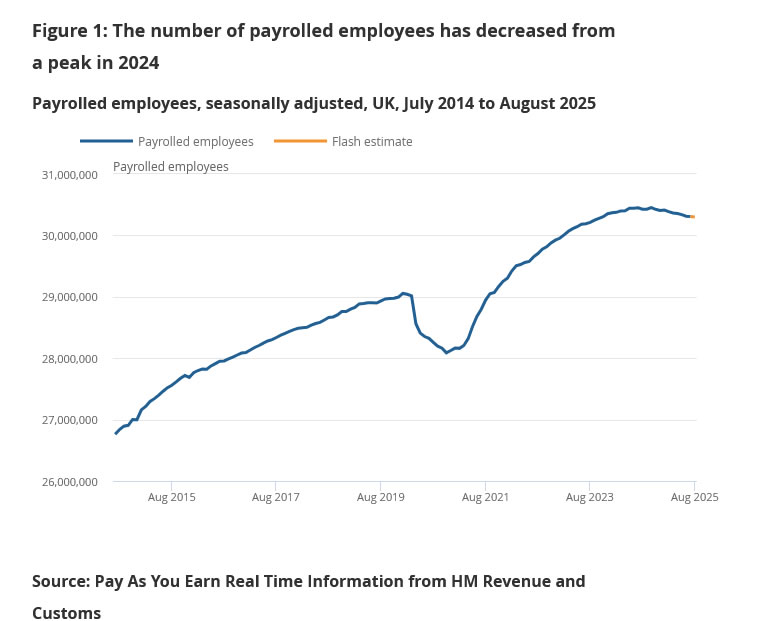

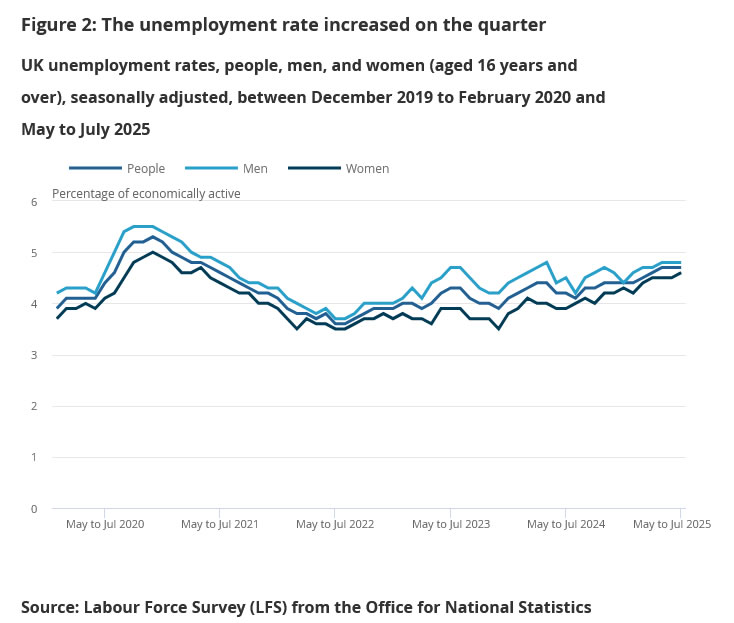

UK job losses continue, pay growth still strong

UK labor market data for August showed further signs of strain, with payrolled employment falling by -8k on the month, extending a steady decline since the peak in Q3 2024. Claimant count rose by 17.4k, less than expected 20.3k. Median monthly pay rose 6.6% yoy, up from July’s 6.0%, underlining persistent wage pressures.

In the three months to July, unemployment rate held steady at 4.7%, in line with forecasts. Average earnings excluding bonuses eased slightly from 5.0% to 4.8%, while including bonuses ticked higher from 4.6% to 4.7%. Overall, the figures show employment losses are continuing, but wage growth remains firm enough to keep the BoE cautious on policy.

Big Tech Leads Rally as Fed Starts Two-Day Meeting

Another day, another record high for the S&P 500 on optimism that:

- Earnings grew around 13% last quarter and the profit outlook has been improving since the summer months, and

- The Federal Reserve (Fed) is about to start a fresh policy-easing cycle to counter the weakening U.S. jobs market – provided that inflation remains under control.

The combination of strong earnings growth and the prospect of lower rates is simply too good for investors to jump off a running bull. On the Fed and rate cuts, many expect a total of 100 bps over the next four meetings.

So if you think there’s a mismatch between the S&P 500’s outlook and the broader U.S. economy and Fed outlook – you’re not alone. That’s because the S&P 500 doesn’t represent the US economy. Roughly a third of the index is made up of Big Tech. Nvidia alone accounts for about 8% of the benchmark. These companies have deep pockets and support each others’ business. This ecosystem, combined with global demand for US tech, has kept the major US indices – the S&P 500 and Nasdaq in particular – in demand despite signs of economic weakness elsewhere. For the rest of the S&P 500, earnings growth last quarter was around 3–4%. You can see this divergence in the equal-weight S&P 500, which continues to lag the market-cap-weighted version.

The weak economic outlook and deteriorating jobs market are not necessarily a concern for US Big Tech, but the prospect of lower rates is clearly positive because it makes valuations look juicier – simple math. As such, the week kicked off at fresh record highs for the S&P 500, while the US 2-year yield – which captures Fed expectations – remained under pressure. Google jumped more than 4% and hit a $3 trillion valuation, fueled by the news (earlier this month) that the company doesn’t need to sell its Chrome browser. That, combined with AI momentum, is pushing Google higher with a slight delay. We’ve long argued that Meta and Google would be the next leg of the AI rally, given these data-rich companies are well placed to benefit from the technology. Nvidia, the icon of the global AI rally, opened lower but closed flat above its 50-DMA, despite reports that China is going after it for violating antitrust laws in a high-profile 2020 deal. The timing is noteworthy, as US and Chinese officials are simultaneously discussing trade terms, TikTok and US concerns about Chinese purchases of Russian oil. Meanwhile, there are also rumours that the trade truce with China could be extended, and that India could strike a trade agreement with the US as well. The good news: trade headlines no longer dent market sentiment as they once did.

So, does that mean everything is rosy? Well, the correction I was expecting over the summer hasn’t materialized, and underlying fundamentals have turned more positive in the meantime. US debt concerns have faded into the background, the trade war’s negative implications have been digested, the Trump administration’s interventions in private companies and the Fed have been absorbed. And now, the Fed appears convinced that cutting rates is indeed the right course.

Inside the Fed, Stephen Miran has been confirmed as a voting member just in time for this week’s Fed meeting, while Lisa Cook will likely participate despite Trump’s efforts to oust her. Beyond the policy rate decision, we’ll also get an update on the so-called dot plot, giving insight into Fed members’ expectations beyond this month. As I wrote earlier, many analysts think there could be four 25-bp cuts on the horizon in the coming months – a scenario that would likely give a fresh boost to equity markets. Small and mid-cap companies, as well as non-tech and non-U.S. names, are also enjoying the ride. A gauge of Asian equities hit a fresh all-time high this morning.

Looking back, some sectors have outperformed others under different rate-cutting scenarios. According to Ned Davis Research, the median gain after four or more cuts (following a six-month pause) was ~20% for health care, nearly 20% for consumer staples, 18% for energy and just 1.6% for tech – suggesting that heavy cutting cycles mostly happen in weak economic conditions, which favour defensives. By contrast, two or fewer cuts tend to support cyclicals such as industrials, energy and financials. We’ll see how many cuts the Fed puts on the menu in the coming months and how markets react.

Still, note that some, like JPMorgan’s chief strategist, warn that investors could lose appetite once the Fed actually starts cutting, if they believe the move is politically rather than economically motivated. That risk would rise if the Fed cut by 50 bps or signaled more cuts over the next 6–12 months than warranted. For now, though, dovish Fed expectations remain supportive of risk appetite. The US dollar is under pressure, gold and silver are pushing higher, and US crude is consolidating gains near the middle of the $62–65pb range, awaiting fresh direction.

ZEW Survey, US Retail Sales, and UK Labour Market in Focus

In focus today

In Germany, focus turns to the ZEW survey for August. Following great improvements in the first half of the year, the indicator took a hit last month with a decline in both the assessment of the current situation and expectations for growth. For today's data, consensus is looking for a further decline in both the assessment of the current situation and expectations to a four-month low.

In the afternoon, US retail sales and industrial production data is due for release. Retail sales will provide markets with the first hard data evidence of how consumer demand has evolved in August amid persistent tariff concerns. We expect to see cooling, but still relatively stable consumption growth.

The UK labour market report is released. The last report revealed a solid upward revision in payrolls data, which has raised the bar for further rate cuts. The labour market remains on a cooling trend, though, and despite the improvement in August, PMI indices suggest a continued weakness.

Economic and market news

What happened overnight

In the US, Lisa Cook is set to remain a Federal Reserve governor, following a ruling by a US appeals court. This means that Cook will be attending the FOMC meeting on Wednesday for which markets are pricing a 25bp cut. At the same time Stephen Miran, President Trump's pick for Federal Reserve governor was confirmed in a 48-47 vote in the Senate.

In the trade war, South Korea and the US have yet to finalize a trade deal as the two are caught in the details. In addition to the 25% tariff from the US, the Japanese deal signed last week adds to the pressure with Japanese auto manufacturers facing a 15% tariff vs. South Korean auto manufacturers facing a 25% tariff. While the USD 350bn investment fund in the US from South Korea is presumably at the centre of the difficulties, senior South Korean officials have said that the country is not in a position to make this investment due to the relatively small size FX market. The Koreans are concerned that a significant increase in dollar demand would depress the won.

What happened yesterday

In the US, President Trump sounded optimistic on US-China talks on Truth Social, while also announcing talks on Friday with Chinese President Xi. Recently, the US has again been threatening to ban TikTok if China does not drop demands for easier tariffs and tech restrictions. Trump also called for US companies to switch from quarterly reporting to semi-annual reporting, in an attempt to reduce compliance burdens and allow managers to focus on running their companies.

In the Ukraine war, tensions continue to build in Europe, as Poland neutralised another drone that was flying above the presidential palace. Russia's Zapad-2025 military drills in Belarus have also drawn attention. Surprisingly, two US military officers attended the drills - the first such visit in years. Poland has responded to the drills by deploying 40,000 troops to its border with Belarus.

Equities: Equities were marginally higher on Monday. Europe opened with substantial gains, but these faded once US markets opened. The S&P 500 eventually closed up 0.5%, while Stoxx 600 gained 0.4%. Once again, this was a Magnificent 7 market, with Alphabet and Tesla rising 4% despite little news. In Europe, it was more of a cyclical rotation, with consumer discretionary and banks leading the gains. In both regions, defensives sold off. The recent cyclical rebound marks a positive trend shift compared with the defensive rally seen in late August. Futures are little changed this morning.

FI and FX: A quiet start to the week with risk assets performing well, US and European rate curves bull flattening and the USD trading on the backfoot. Scandies picked up where they left off last week, this time with the SEK leading the way. Also, CAD and GBP had solid sessions, posting gains vs both EUR and the USD.

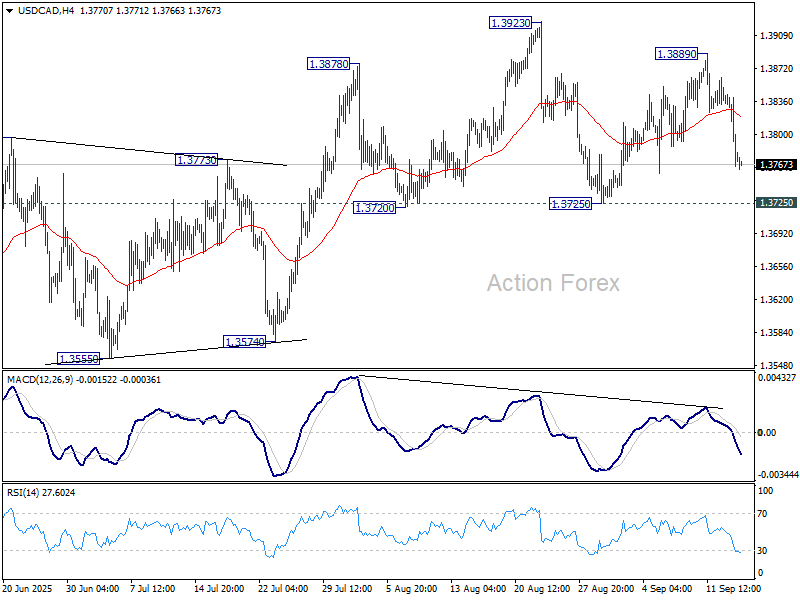

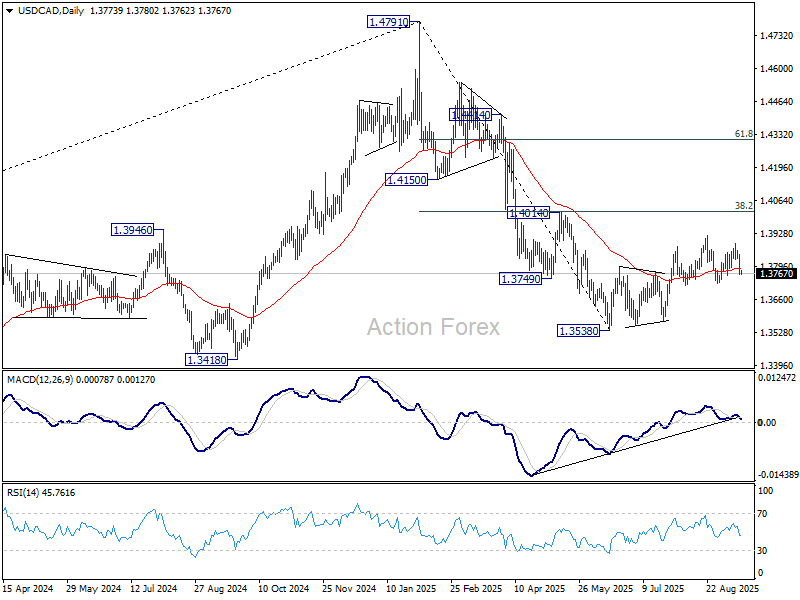

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3748; (P) 1.3797; (R1) 1.3828; More...

USD/CAD drops notably today but stays above 1.3725 support. Intraday bias remains neutral at this point. On the downside, firm break of 1.3725 support will complete a head and shoulder top (ls: 1.3878, h: 1.3923, rs: 1.3889). That would indicate that corrective rebound from 1.3538 has already completed, and turn near term outlook bearish. Deeper fall should then be seen to 1.3574 support. On the upside, however, break of 1.3923 will resume the rebound towards 1.4014 cluster resistance.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4014 cluster resistance (38.2% retracement of 1.4791 to 1.3538 at 1.4017) holds. Next target is 61.8% retracement of 1.2005 (2021 low) to 1.4791 at 1.3069.

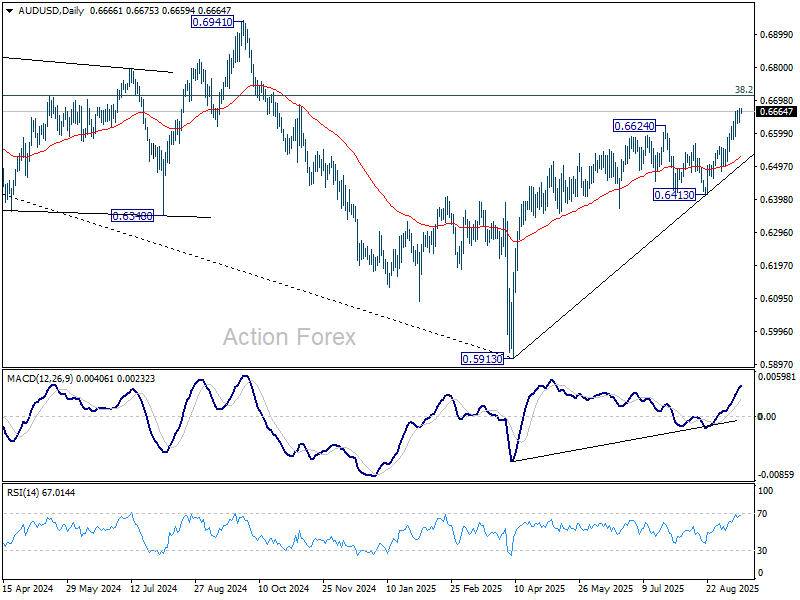

AUD/USD Daily Report

Daily Pivots: (S1) 0.6648; (P) 0.6661; (R1) 0.6684; More...

Intraday bias in AUD/USD remains mildly on the upside. Current rally from 0.5913 should target 0.6713 fibonacci level. Firm break there will carry larger bullish implications. On the downside, below 0.6630 minor support will turn bias neutral and bring consolidations first, before staging another rise.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, sustained break of 0.6713 will be a strong sign of bullish trend reversal, and path the way to 0.6941 structural resistance for confirmation.

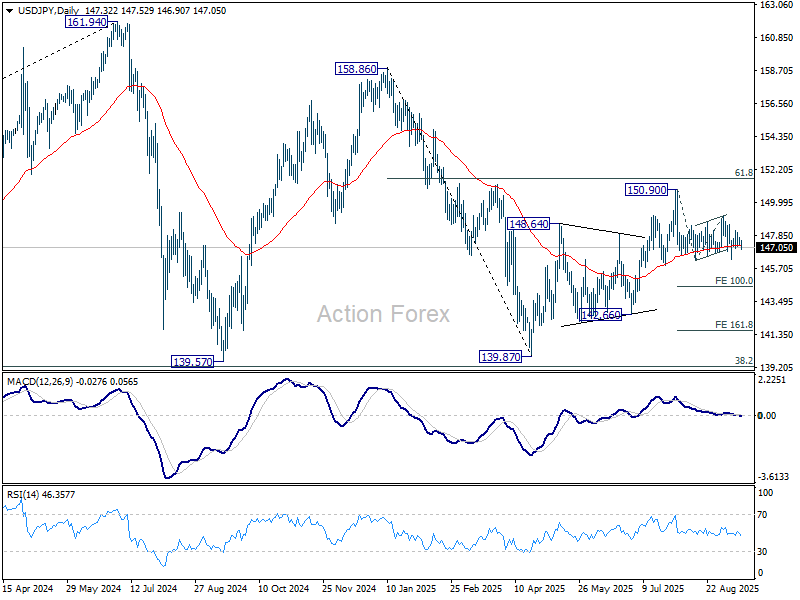

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.15; (P) 147.48; (R1) 147.73; More...

Outlook in USD/JPY is unchanged and intraday bias stays neutral. More consolidations could be seen first. Further fall is in favor as long as 149.12 resistance holds. Firm break of 146.29 will solidify the case that whole rebound from 139.87 has completed with three waves up to 150.90. Deeper decline should then be seen to 100% projection of 150.90 to 146.20 from 149.12 at 144.42.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

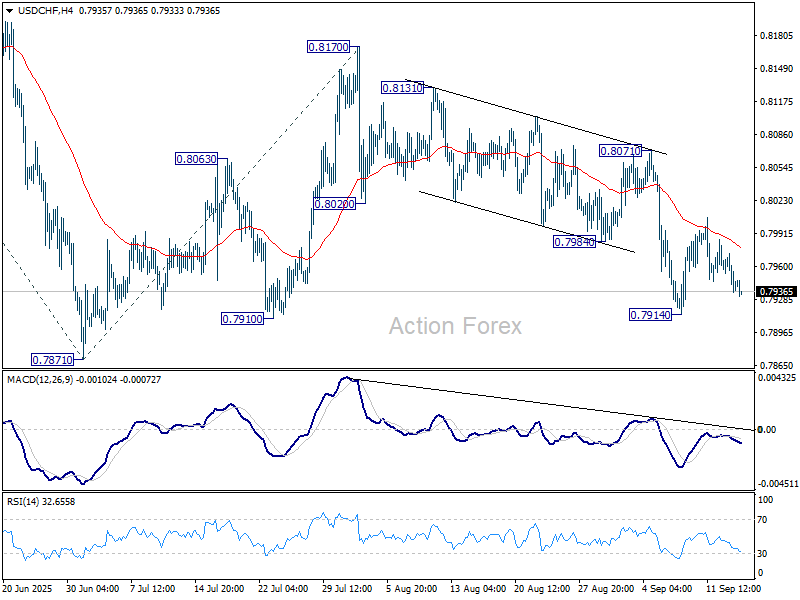

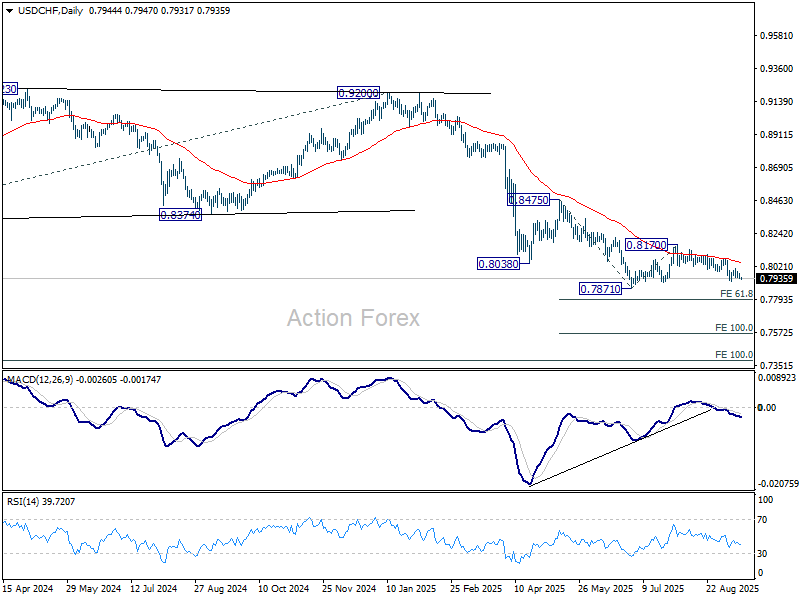

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7931; (P) 0.7953; (R1) 0.7968; More….

Intraday bias in USD/CHF stays neutral and more consolidations could be seen above 0.7914 support. But further rally is expected as long as 0.8071 resistance holds. Below 0.7914 will bring retest of 0.7871 low. Decisive break there will resume larger down trend to 61.8% projection of 0.8475 to 0.7871 from 0.8170 at 0.7797.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds.

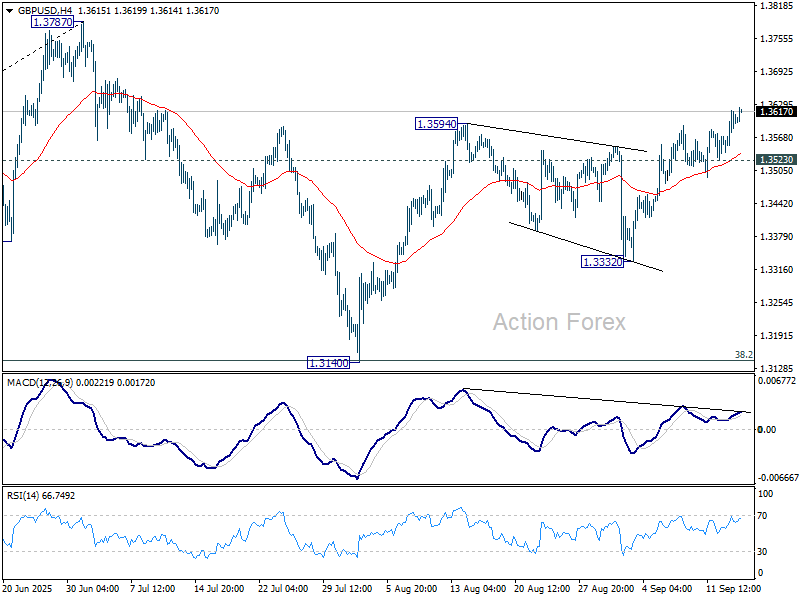

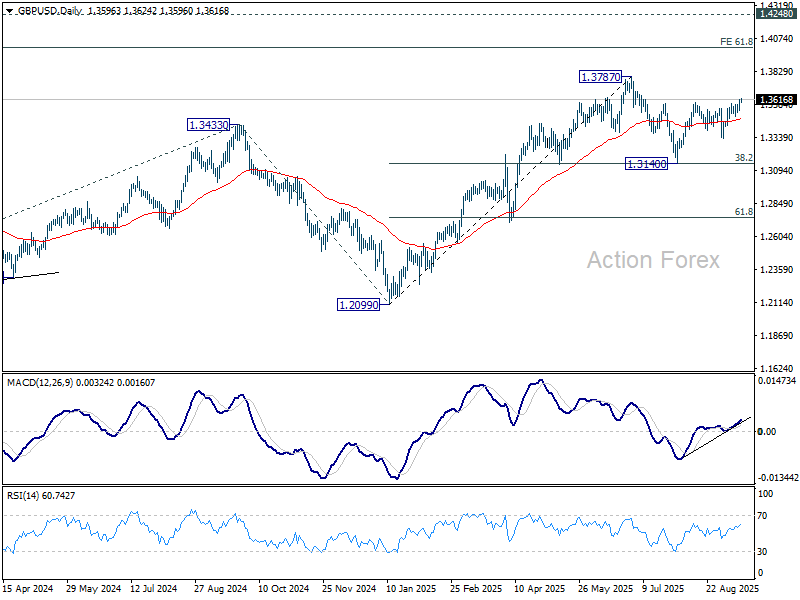

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3555; (P) 1.3588; (R1) 1.3629; More...

Intraday bias in GBP/USD remains on the upside for the moment. Rise from 1.3140 should continue to retest 1.3787 high. Decisive break there will resume larger up trend to 1.4004 projection level. On the downside, below 1.3523 support will turn intraday bias neutral again first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3151) holds, even in case of deep pullback.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1728; (P) 1.1751; (R1) 1.1786; More...

Intraday bias in EUR/USD is back on the upside with breach of 1.1779 resistance. Rise from 1.1390 should extend to retest 1.1829 high. Firm break there will resume larger up trend to 1.1916 projection level next. On the downside, below 1.1715 minor support will turn intraday bias neutral again first.

In the bigger picture, rise from 0.9534 (2022 low) long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 55 W EMA (now at 1.1215) holds.