Sample Category Title

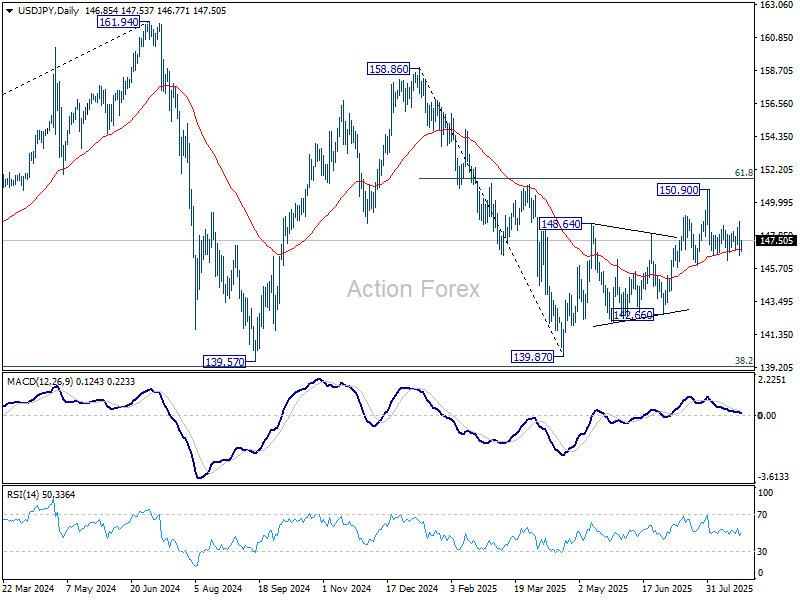

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.08; (P) 147.43; (R1) 148.28; More...

Range trading continues in USD/JPY and intraday bias stays neutral. On the downside, firm break of 146.20 will resume the fall from 150.90. Also, that would argue that rebound from 139.87 has completed as a corrective move to 150.90. Deeper fall should be seen to 142.667 support for confirmation. On the upside, above 148.76 will bring another rise to retest 150.90 instead.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). Decisive break of 61.8% retracement of 158.86 to 139.87 at 151.22 will argue that it has already completed with three waves at 139.87. Larger up trend might then be ready to resume through 161.94 high. In case the corrective pattern extends with another fall, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

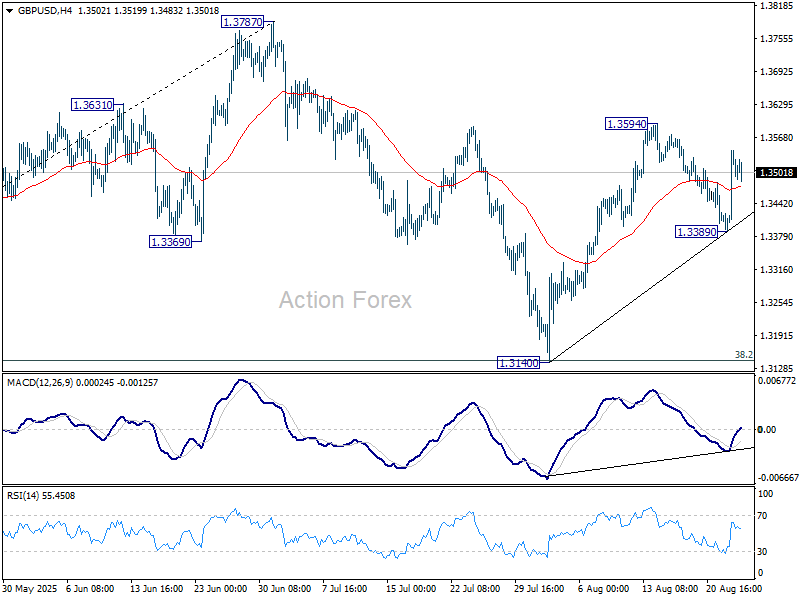

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3431; (P) 1.3487; (R1) 1.3584; More...

GBP/USD is still bounded in range of 1.3389/3594 and intraday bias stays neutral. Overall, price actions from 1.3787 high are seen as a corrective pattern. On the upside, break of 1.3594 will resume the rebound from 1.3140 to retest 1.3787 high. Firm break there will resume the larger up trend. For now, risk will stay on the upside as long as 1.3389 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3073) holds, even in case of deep pullback.

Global Markets Cool as Fed Boost Fades, Caution Dominates Late August Trade

Global market sentiment has cooled to start the week, with major European indexes trading mildly lower alongside softer U.S. futures. The lift from Fed Chair Jerome Powell’s dovish pivot appears to have run its course for now, leaving investors more hesitant during the final days of August.

While some profit-taking is likely, the prospect of a steep pullback looks limited given markets are firmly priced for a September Fed cut. At the same time, traders are wary of adding fresh exposure ahead of next week’s crucial U.S. jobs data, which could determine whether the Fed follows through on easing at its September 16–17 meeting.

Currency markets reflected the cautious tone, with overall activity sluggish. Aussie led gains, followed by Kiwi and Loonie, all of which face key domestic events this week including RBA minutes, Australia CPI, New Zealand business confidence, and Canada GDP.

On the weaker side, Yen underperformed, trailed by Euro and Swiss Franc. The Yen will be sensitive to Friday’s Tokyo CPI, while Switzerland releases GDP later in the week. Euro showed little reaction to today’s German Ifo survey. Sterling Dollar hold mid-pack positions.

In Europe, UK is on holiday. DAX is down -0.26%. CAC is down -0.73%. Germany 10-year yield is up 0.047 at 2.773. Earlier in Asia, Nikkei rose 0.41%. Hong Kong HSI rose 1.94%. China Shanghai SSE rose 1.51%. Singapore Strait Times rose 0.08%. Japan 10-year JGB yield rose 0.002 to 1.621.

German Ifo business climate edges higher to 89.0, recovery still weak

Germany’s Ifo business climate index rose modestly in August, climbing to 89.0 from 88.6 and beating expectations of 88.3. The improvement was driven by stronger expectations, with the sub-index rising to 91.6 from 90.7. Current assessment slipped from 86.5 to 86.4. Ifo said sentiment among companies has “brightened slightly,” but warned that the recovery “remains weak.”

Sector details painted a mixed picture. Manufacturing sentiment deteriorated further from -11.9 to -12.2, with firms less satisfied about current conditions and order intake still showing no signs of growth, though capital goods makers saw noticeable improvement.

Services dipped from 2.8 to 2.6 as expectations turned cautious despite a stronger current situation. Trade slumped from -20.3 to -21.4 on weaker performance. Construction slipped from -14.3 to -15.3, as firms were less satisfied with current conditions even as their outlook improved.

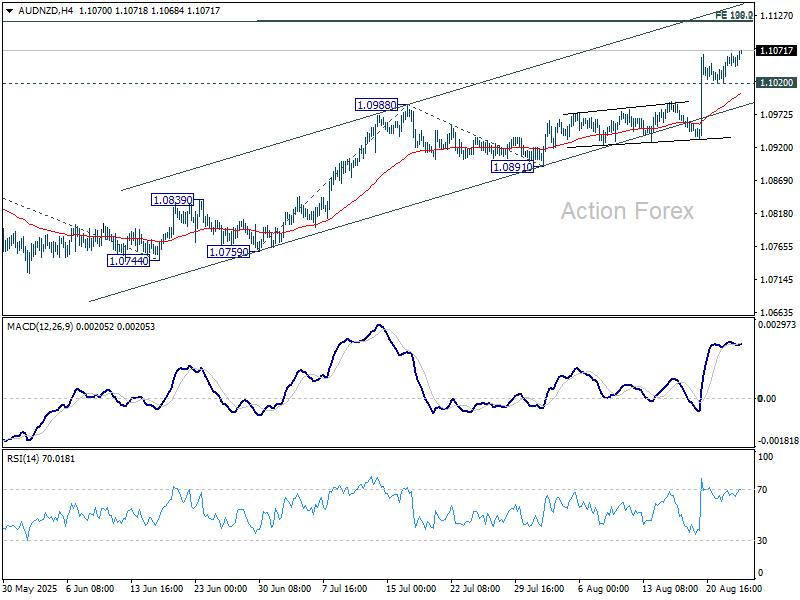

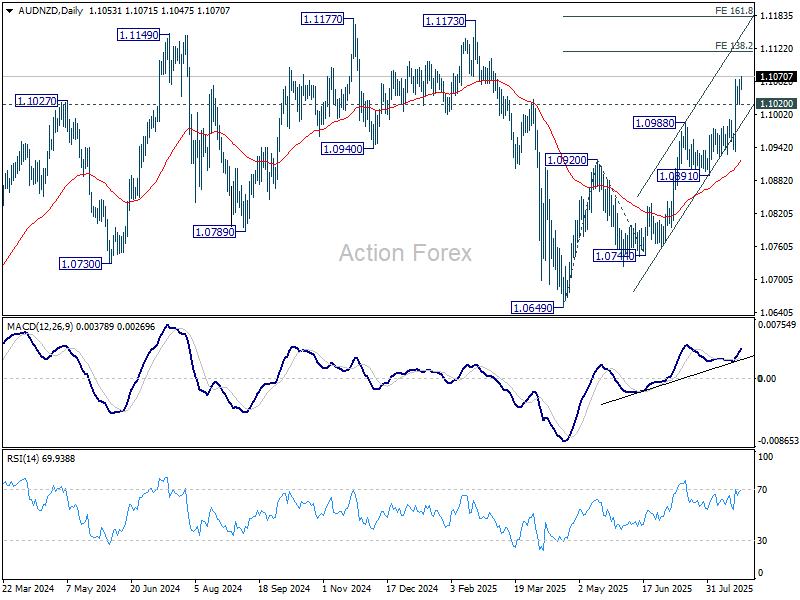

AUD/NZD rally intact, busy week with RBA minutes, Aussie CPI and NZ confidence

AUD/NZD could see sharp moves this week as markets digest a run of significant releases from both economies. RBA minutes on Tuesday, Australia’s monthly July CPI on Wednesday, and New Zealand’s ANZ business confidence survey on Thursday are possible movers.

In New Zealand, Q2 retail sales offered an upside surprise today. Headline volumes rose 0.5% qoq, beating expectations of 0.2%, while ex-auto sales jumped 0.7% qoq, defying forecasts of contraction. However, the Kiwi failed to capitalize, remaining pressured after last week’s dovish RBNZ decision. Markets have since shifted toward expecting two more rate cuts before the easing cycle ends.

RBNZ Governor Christian Hawkesby reinforced that view by stressing that both remaining policy meetings this year are “live.” This leaves scope for either two consecutive cuts in 2025, or one this year and one early next year, depending on how upcoming economic data evolves.

Meanwhile, the RBA appears more deliberate. After cutting 25bps earlier this month, the new projections signaled that one additional cut this year and two in 2026 remain the likely path under current assumptions. November is seen as the more appropriate window for action, allowing time to absorb Q3 CPI data. This week’s minutes and July’s monthly CPI release will be important checks on whether that outlook holds.

Technically, AUD/NZD’s near-term rally remains intact, supported by firm momentum on D MACD. As long as 1.1020 holds, further gains are likely, with scope toward the 138.2% projection of 1.0649 to 1.0920 from 1.0744 at 1.1119.

However, there is no clear sign of medium term range breakout yet. Hence, AUD/NZD would likely lose momentum above 1.119. Upside should be capped by 161.8% projection at 1.1182, which is slightly above key resistance of 1.1177 (2024 high).

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3431; (P) 1.3487; (R1) 1.3584; More...

GBP/USD is still bounded in range of 1.3389/3594 and intraday bias stays neutral. Overall, price actions from 1.3787 high are seen as a corrective pattern. On the upside, break of 1.3594 will resume the rebound from 1.3140 to retest 1.3787 high. Firm break there will resume the larger up trend. For now, risk will stay on the upside as long as 1.3389 support holds, in case of retreat.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3073) holds, even in case of deep pullback.

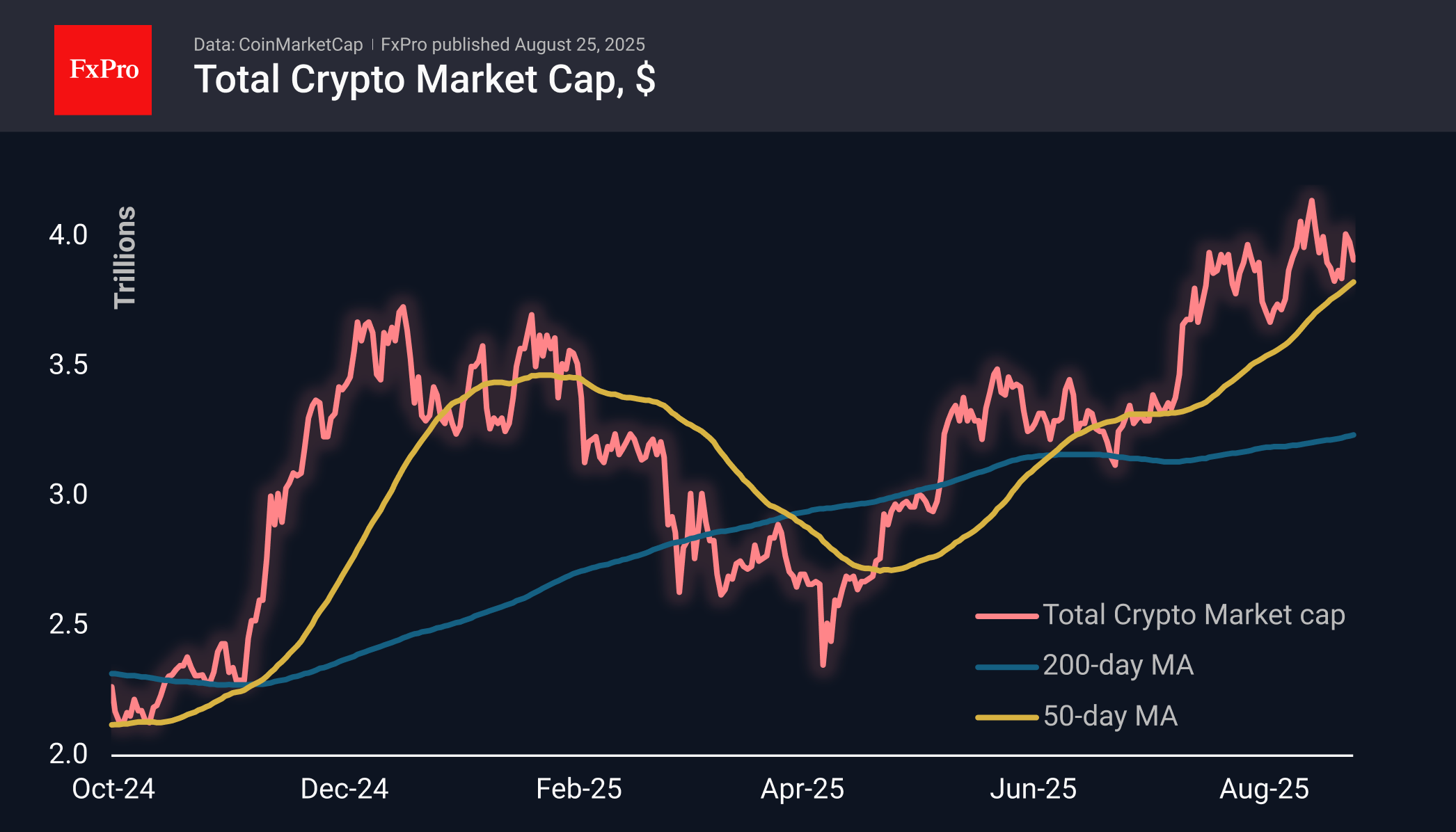

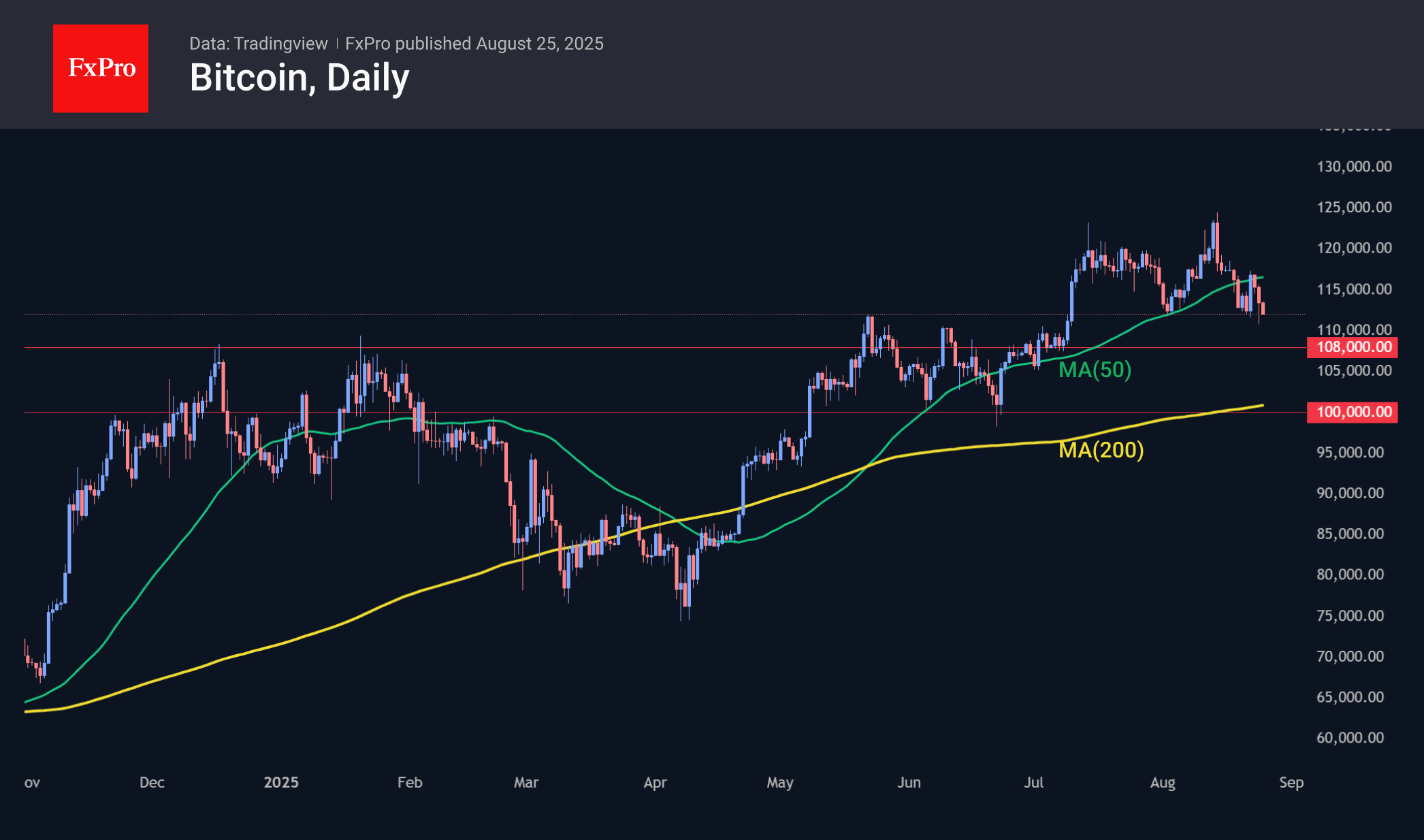

Bitcoin Drags Crypto Down

Market Overview

The crypto market capitalisation fell to $3.91 trillion, down 2% in the past day and 3.5% from last week’s peak, as Bitcoin came under pressure following Friday’s surge. The dynamics on Sunday were noteworthy, when the sell-off of the first cryptocurrency coincided with Ethereum setting historic highs. Solana is also doing well, adding 11% in 7 days, stronger than Ethereum’s 9% growth and against BTC’s 3% decline and the near-zero dynamics of the total cryptocurrency market capitalisation.

Bitcoin is trading at $112K, having fallen at one point to $110K, a new low since early July. Friday’s surge seems to have attracted new sellers, pushing the coin below its 50-day average. So far, it looks like liquidity is being transferred from BTC to ETH or other altcoins, such as SOL. However, we cannot rule out the possibility that all processes are starting in Bitcoin, and a similar shift to selling on growth is just around the corner in altcoins.

News Background

The weekly inflow into spot Bitcoin ETFs in the US has been interrupted after two weeks of inflows. According to SoSoValue, the net outflow from spot BTC ETFs amounted to $1.17 billion last week, the highest since the end of February. Cumulative inflows since the approval of Bitcoin ETFs in January 2024 have decreased to $53.80 billion.

A 14-week streak of net inflows into spot Ethereum ETFs in the US was also replaced by an outflow of $578.9 million, the highest in recorded history. Total net inflows since the launch of ETFs in July 2024 have fallen to $12.09 billion.

According to Lookonchain, a Bitcoin whale became active on Friday, selling more than 100 BTC that had been ‘dormant’ for seven years and investing the proceeds in Ethereum on the spot and futures markets. The crypto community viewed the whale’s actions as a positive signal for Ether.

Finally, the SEC recently approved the possibility of redeeming spot ETFs on BTC and ETH in kind, which will allow institutions to buy shares directly for cryptocurrency rather than converting them into cash.

The number of companies buying BTC daily is declining. According to investment fund Capriole, some metrics signal growing risks of a sell-off, which could be either a temporary downturn or a sign of market saturation.

The latest recalculation increased the difficulty of mining Bitcoin to a record 129.7T. The indicator rose by only 0.2% but updated its historical maximum. According to Glassnode, the average hash rate for seven days is 945 EH/s.

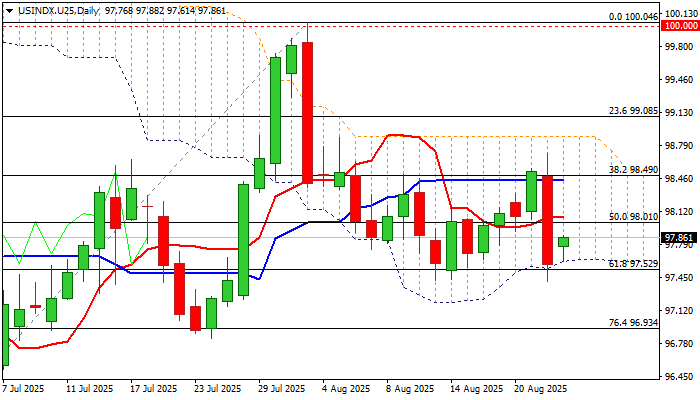

USD Index: Bears Pause for Consolidation Before Renewed Attack at Key Supports

The dollar index takes a breather after nearly 1% drop on Friday, inspired by unexpectedly dovish Fed Chair Powell’s remarks in his speech in Jackson Hole symposium of central bankers.

The dollar has registered the biggest daily drop since Aug 1, deflated by signals that the Fed may start to ease its currently restrictive monetary policy, as chief Powell focused on strong weakening in the labor sector and described elevated inflation as short-lasting phenomenon.

Although Powell did not provide any details and did not commit any action by the central bank in the near future, the signal he sent was very negative for the dollar.

Sharp fall found firm ground at $97.53 (strong technical support provided by daily Ichimoku cloud base / Fibo 61.8% of $95.97/$100.04 upleg), with consolidation likely to be limited (ideally to be capped by barriers at 98.06/98.42 (daily Tenkan-sen / Fibo 38.2% retracement of $100.04/$97.41 descend) to keep bears in play.

Violation of triggers at $97.50/40 zone (cloud base / Fibo / higher base on daily chart) would signal bearish continuation and expose July 24 higher low at $96.82) which guards key support at $95.97 (2025 low).

Daily studies remain predominantly bearish, with a number of factors keeping the dollar under pressure and contributing to negative short-term outlook.

Res: 98.06; 98.42; 98.69; 98.88.

Sup: 97.53; 97.41; 96.82; 95.97.

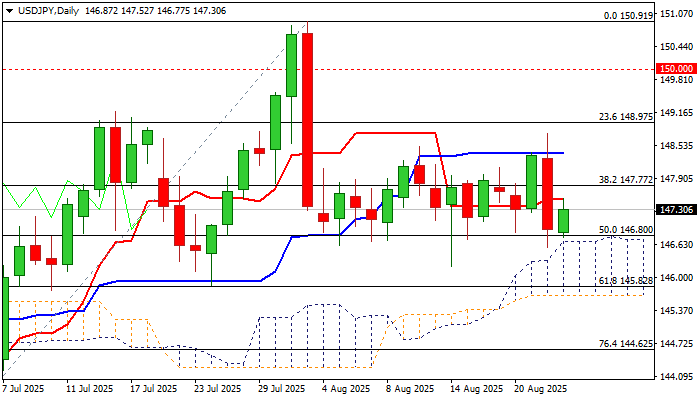

USD/JPY Outlook: Regains Traction After Friday’s Fall

USDJPY edged up in early Monday, recovering a part of Friday’s around 1% drop, sparked by dovish comments from Fed Chair Powell.

Friday’s fall was contained by rising 55DMA (146.60) which tracks the pair’s ascend since early July, as well as by the top of ascending daily Ichimoku cloud (spanned between 146.70 and 145.64).

The price returned to the range (146.21/148.77), where it is held for the fourth consecutive week, but the downside is expected to remain vulnerable (despite strong supports) as long as the price stays on the lower side of the range and while capped by daily Tenkan-sen (147.50).

Technical picture on daily chart is mixed (daily Tenkan/Kijun-sen in bearish setup / 14-d momentum broke into negative territory vs rising daily cloud / 55DMA), with markets awaiting stronger direction signals.

Focus will be on release of US PCE (due on Friday) which will provide more details about inflation, and next week’s releases of US labor reports, both expected to contribute to Fed’s decision on September’s policy meeting.

Expect initial bullish signal on firm break of daily Tenkan-sen, with rise through daily Kijun-sen (148.38) to bring bulls fully in play and bring psychological 150 barrier in focus.

Conversely, violation of cloud top / 55DMA would weaken near-term structure and generate initial signal of bearish continuation of larger downtrend from 150.91 (Aug 1 peak).

Res: 147.50; 147.80; 148.38; 148.77.

Sup: 146.70; 146.21; 145.82; 145.64.

EURUSD : Calling the Rally After Elliott Wave Double Three Pattern

Hello fellow traders. In this technical article we’re going to look at the Elliott Wave charts of EURUSD forex pair published in members area of the website. The pair has recently given us Double Three pull back and found buyers again precisely at the equal legs area as we expected. In the following text, we’ll explain the Elliott Wave count.

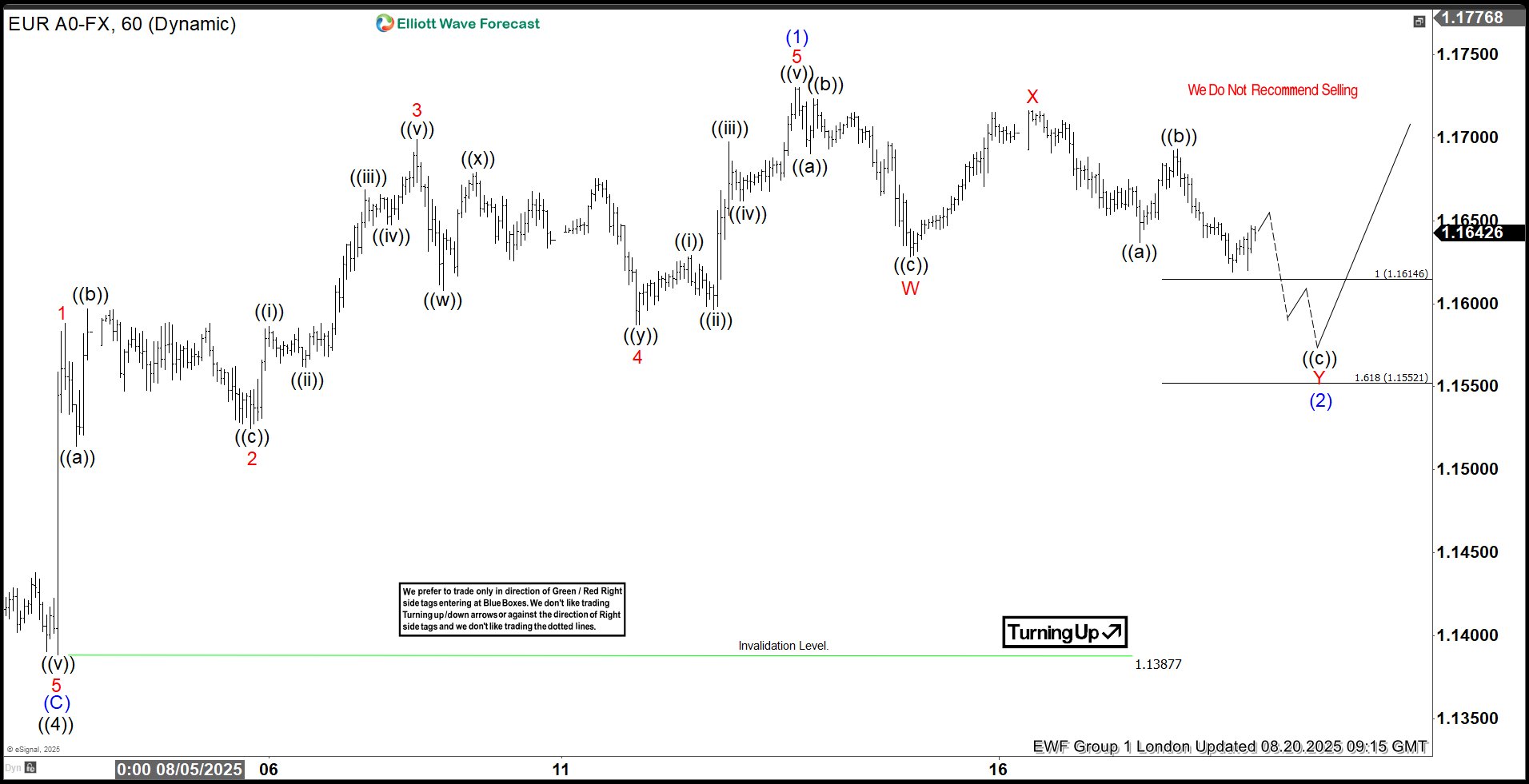

EURUSD Elliott Wave 1 Hour Chart 08.20.2025

EURUSD is currently developing an intraday three-wave pullback from recent highs. Our members know how to identify potential reversal zones using the Equal Legs technique — in this case, the ideal support area comes in at 1.16146-1.15521. The pair can see more downside in near term. As long as price holds within this region, we expect buyers to step in and rally to resume.

EURUSD Elliott Wave 1 Hour Chart 08.20.2025

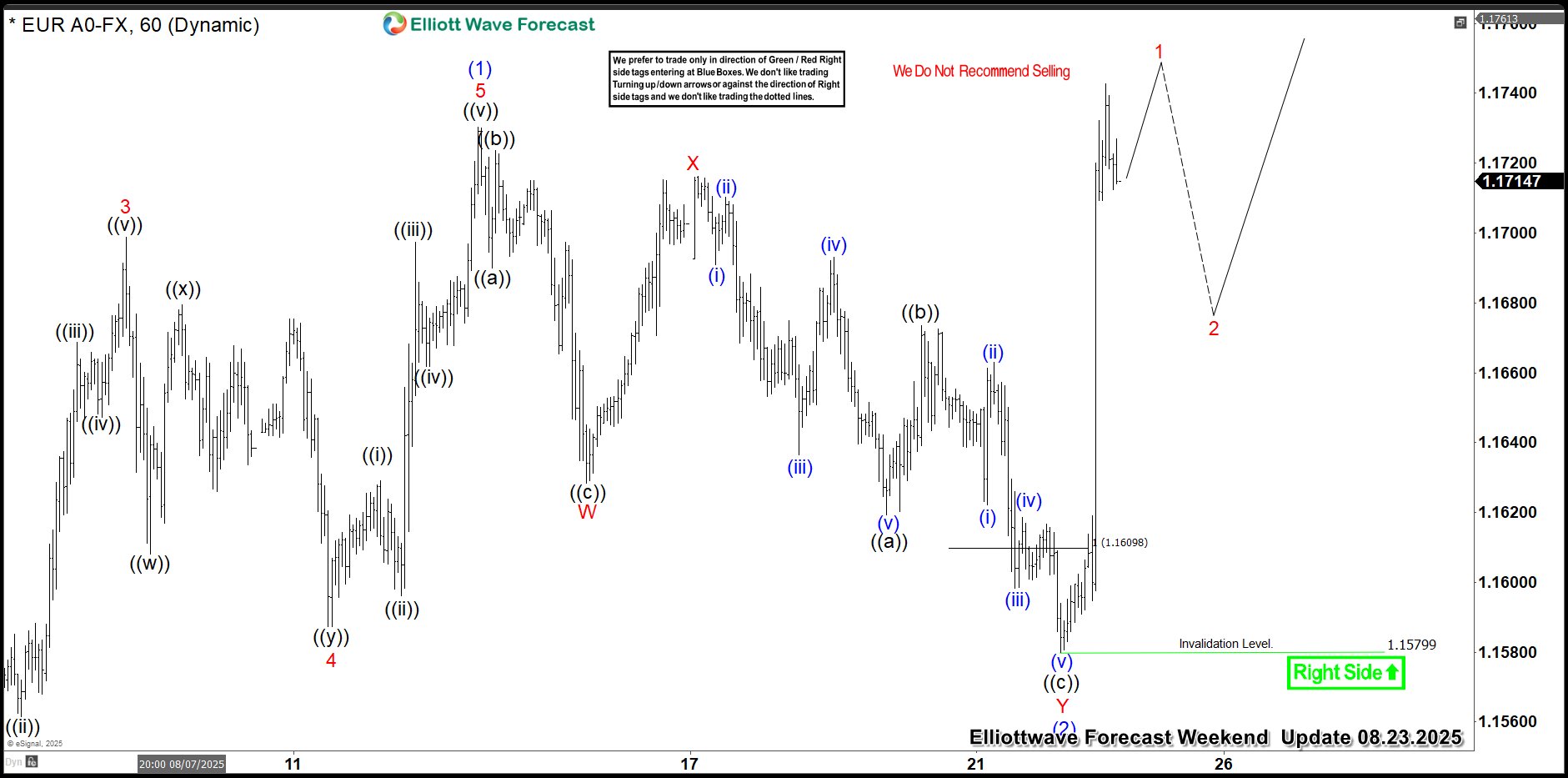

The pair has reached our target area and found buyers as expected. EURUSD made strong rally from the buyers zone and completed pull back at the 1.15799 low. We do not recommend selling the pair at this stage and favor the long side. 1.15799 is the key low for proposed short term view. While above that low, next leg up can be in progress.

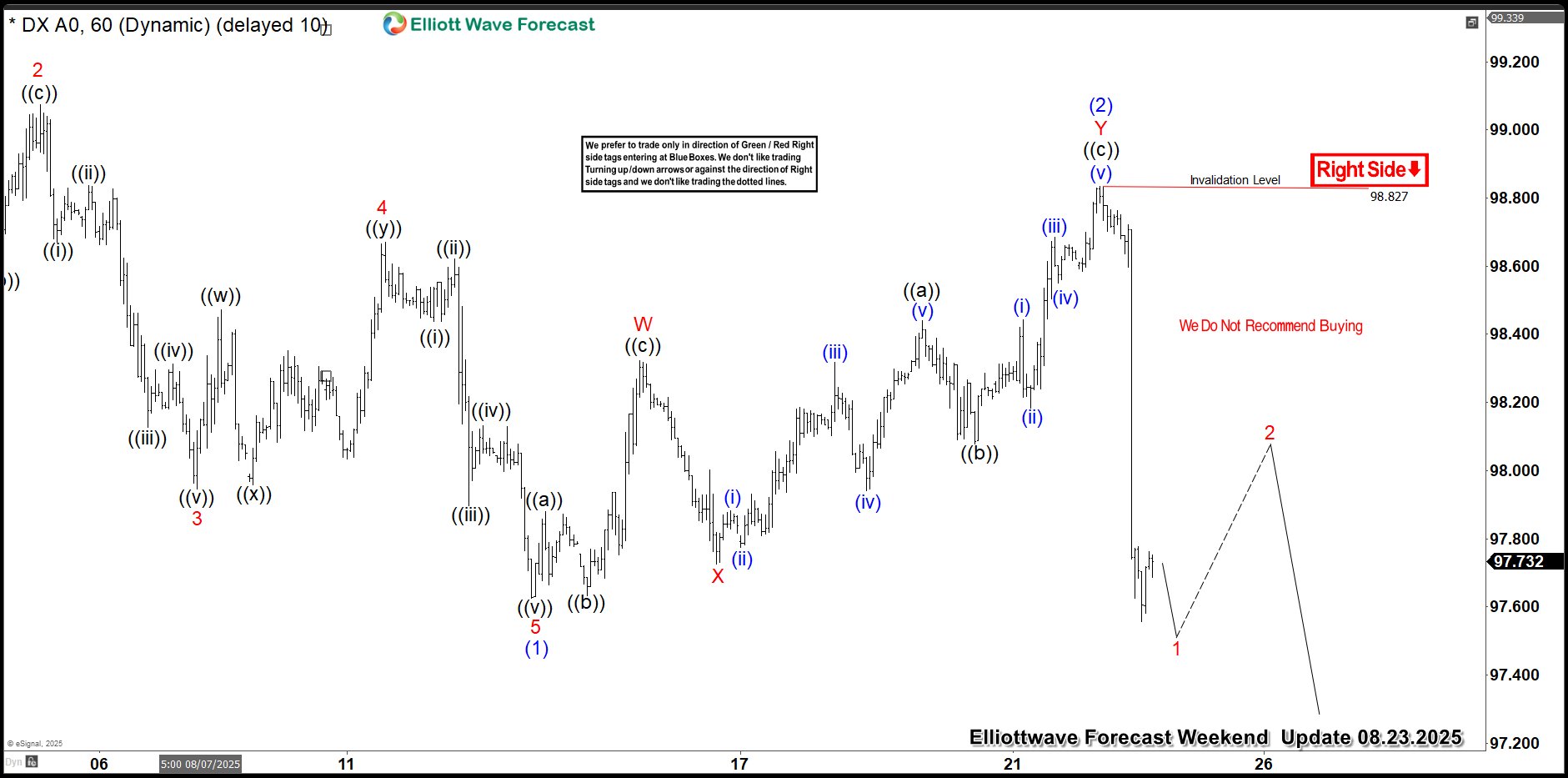

Dollar Index (DXY) : Forecasting the Decline From the Equal Legs Zone

In this technical article we’re going to look at the Elliott Wave charts of Dollar index DXY published in members area of the website. US Dollar has recently given us Double Three pull back and found buyers again precisely at the equal legs area as we expected. In this discussion, we’ll break down the Elliott Wave pattern and forecast.

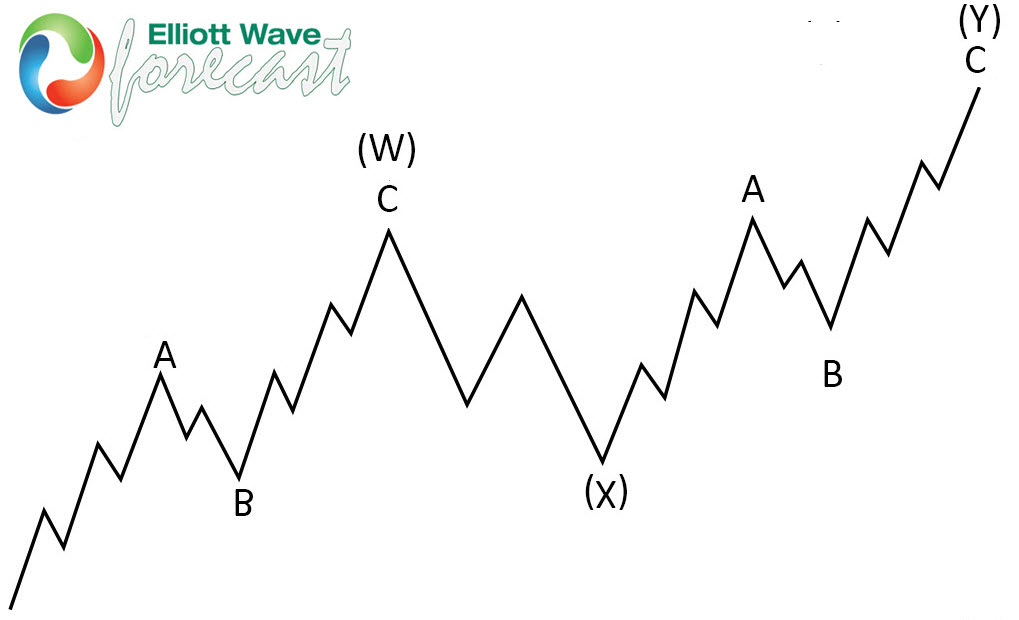

Elliott Wave Double Three Pattern

Double three is the common pattern in the market , also known as 7 swing structure. It’s a reliable pattern which is giving us good trading entries with clearly defined invalidation levels.

The picture below presents what Elliott Wave Double Three pattern looks like. It has (W),(X),(Y) labeling and 3,3,3 inner structure, which means all of these 3 legs are corrective sequences. Each (W) and (Y) are made of 3 swings , they’re having A,B,C structure in lower degree, or alternatively they can have W,X,Y labeling.

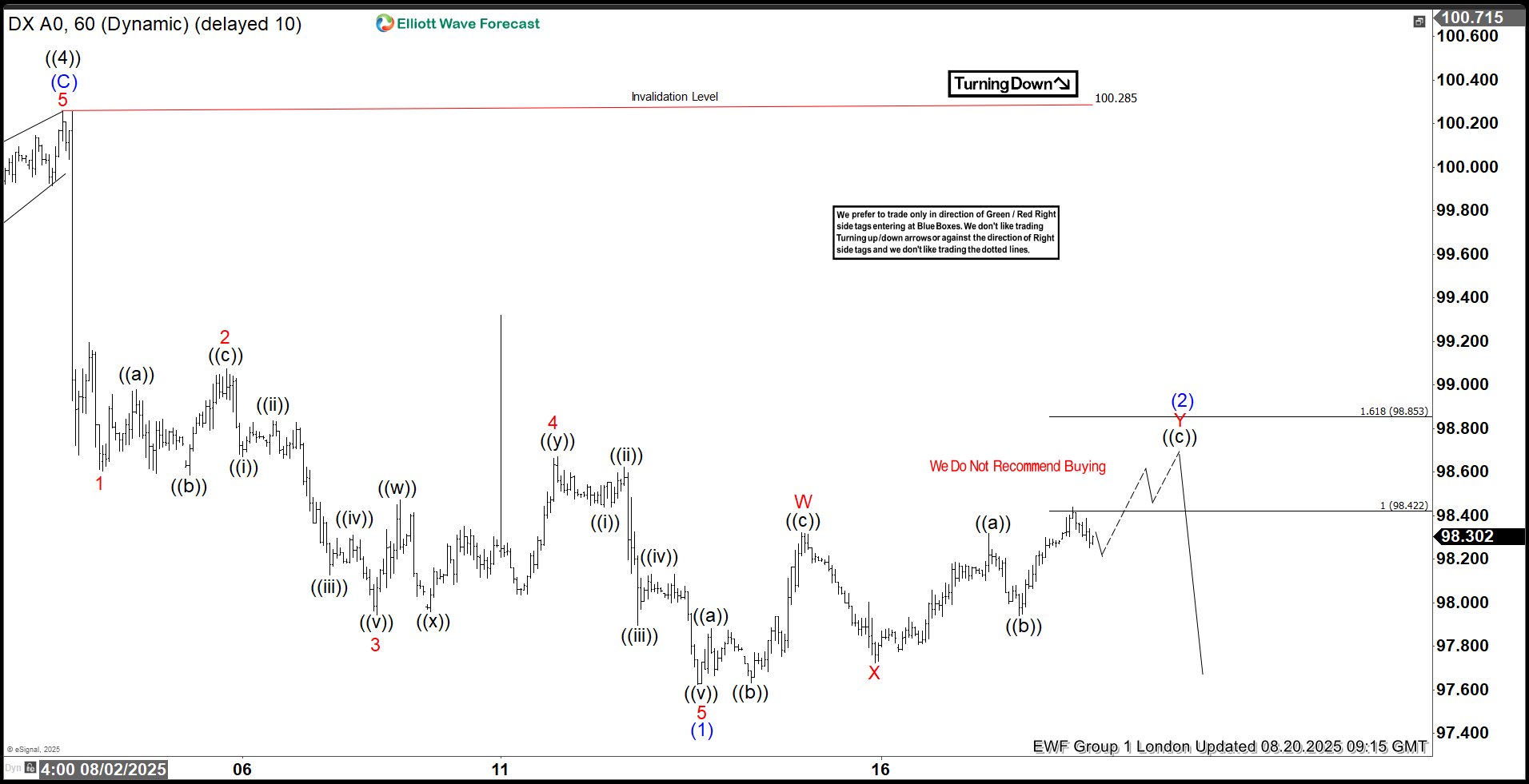

DXY Elliott Wave 1 Hour Chart 08.20.2025

DXY is forming a Double Three pattern. Our members know that we identify potential reversal zones using the Equal Legs technique — in this case, the sellers’ area lies at 98.422–98.853. The dollar may see further upside in the near term within this zone. As long as the price stays within this region, we expect sellers to take control and push it down toward new lows. We recommended that members avoid buying the Dollar at this stage, while favoring the short side.

DXY Elliott Wave 1 Hour Chart 08.20.2025

A few days later, we can see the result. The Dollar found sellers at the marked Equal Legs zone, as expected. DXY made a sharp drop from the sellers’ zone. The recovery peaked at 98.827. As long as it remains below that high, the next leg down may be in progress.

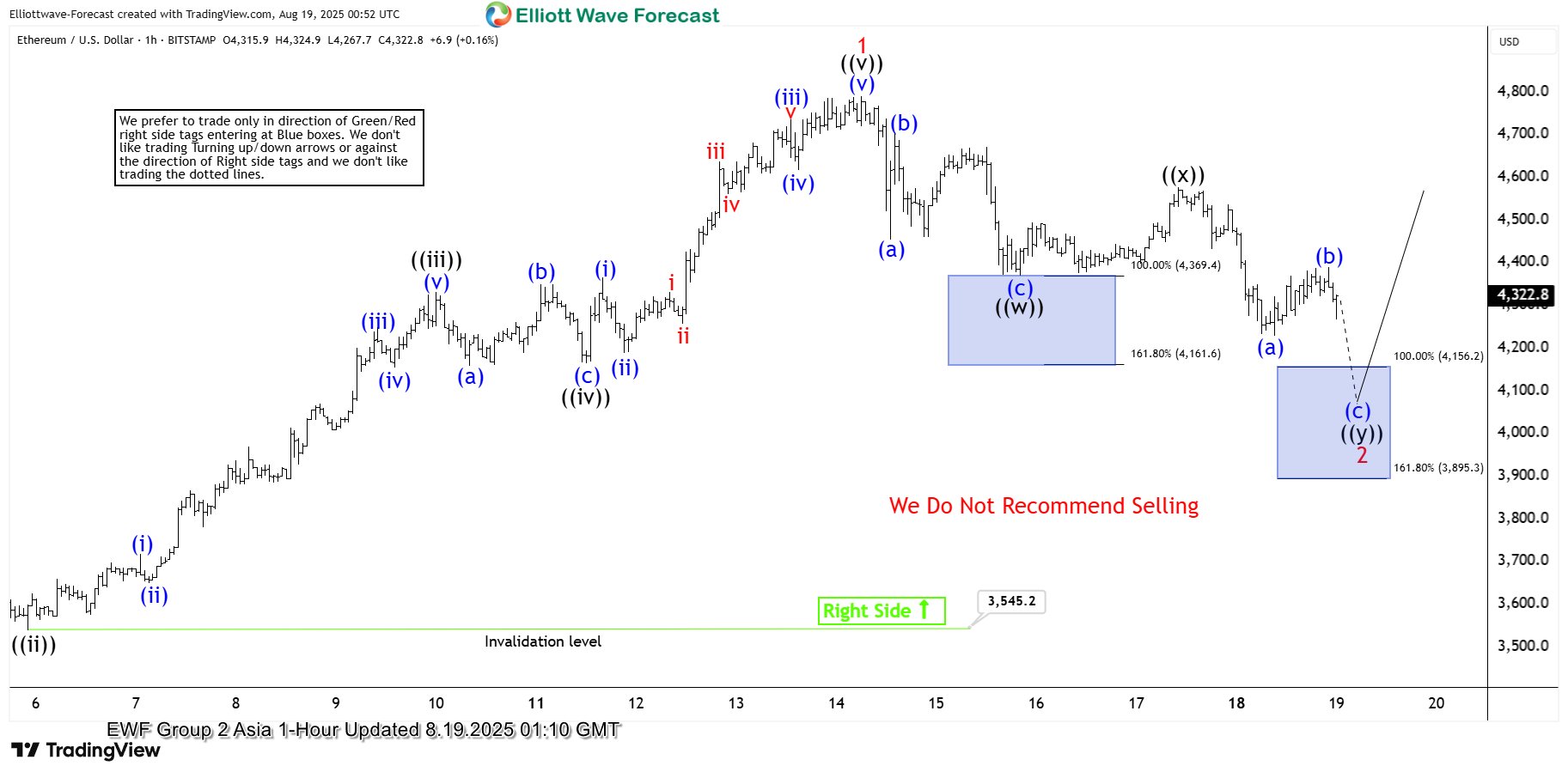

Ethereum Bounces: ETHUSD Reacts Strongly from Key Support Zone

In this technical blog, we will look at the past performance of the 1-hour Elliott Wave Charts of Ethereum ticker symbol: ETHUSD. We presented to members at the elliottwave-forecast. In which, the rally from the 09 April 2025 low unfolded as an impulse structure. Showing a higher high sequence favored more upside extension to take place. Therefore, we advised members not to sell the crypto & buy the dips in 3, 7, or 11 swings at the blue box areas. We will explain the structure & forecast below:

Ethereum 1-Hour Elliott Wave Chart From 8.19.2025

Here’s the 1-hour Elliott wave chart from the 8.19.2025 Asia update. In which, the cycle from the 8.03.2025 low ended in wave 1 at $4788.7 high. Down from there, the ETHUSD made a pullback in wave 2 to correct that cycle. The internals of that pullback unfolded as Elliott wave double three structure where wave ((w)) ended at $4370.9 low. Wave ((x)) bounce ended at $4578.1 high and wave ((y)) managed to reach the blue box area at $4156.2- $3895.3. From there, buyers were expected to appear looking for the next leg higher or for a 3 wave bounce minimum.

Ethereum Latest 1-Hour Elliott Wave Chart From 8.25.2025

This is the latest 1-hour Elliott wave Chart from the 8.25.2025 London update. In which the ETHUSD is showing a reaction higher taking place, right after ending the double correction within the blue box area. Allowed members to create a risk-free position shortly after taking the long position at the blue box area. Since then the pair has already made a new high above previous wave 1 confirming the next extension higher targeting $5501.5- $5840.7 area higher.

New Zealand Dollar Flies After Powell Speech, NZ Retail Sales Beat Forecast

The New Zealand dollar has steadied on Monday. In the European session, NZD/USD is trading at 0.562, down 0.07% on the day. On Friday, the New Zealand dollar shot up 0.82%, its best one-day performance since June.

US dollar sinks after Powell's signals a rate cut

The US dollar was hammered on Friday, posting sharp losses against all the major currencies, including the New Zealand dollar. This followed Federal Reserve Chair Powell's dovish speech at a meeting of central bankers' in Jackson Hole.

Powell did not explicitly say that the Fed would cut rates next month and noted that inflation remained a risk due to tariffs. He expressed concern about the labor market, saying that "downside risks to employment are rising" and such risks could materialize quickly.

The markets focused on Powell's warning about the employment outlook and bumped up expectations that the Fed will cut rates at the September 17 meeting. As well, a second cut before the end of the year is a strong possibility.

The Fed has been in a prolonged wait-and-see stance, holding rates since December 2024. With inflation largely under control and the labor market showing wider cracks, the Fed is likely to respond with a rate cut or two before the end of the year.

New Zealand retail sales rise to 0.5%

New Zealand's retail sales for the second quarter rose by 0.5% q/q, down from 0.8% in Q1 but above the market estimate of 0.2%. Annually, retail sales jumped 2.3%, up sharply from 0.7% in Q1. The positive release indicates that consumers are spending in response to lower interest rates. The Reserve Bank of New Zealand has aggressively chopped rates and has hinted that the easing cycle will continue.

NZD/USD Technical

- NZD/USD is testing support at 0.5860, followed by 0.5854 and 0.5843

- 0.5871 and 05877 are the next resistance lines

NZDUSD 1-Day Chart, Aug. 25, 2025