Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8105; (P) 0.8130; (R1) 0.8148; More….

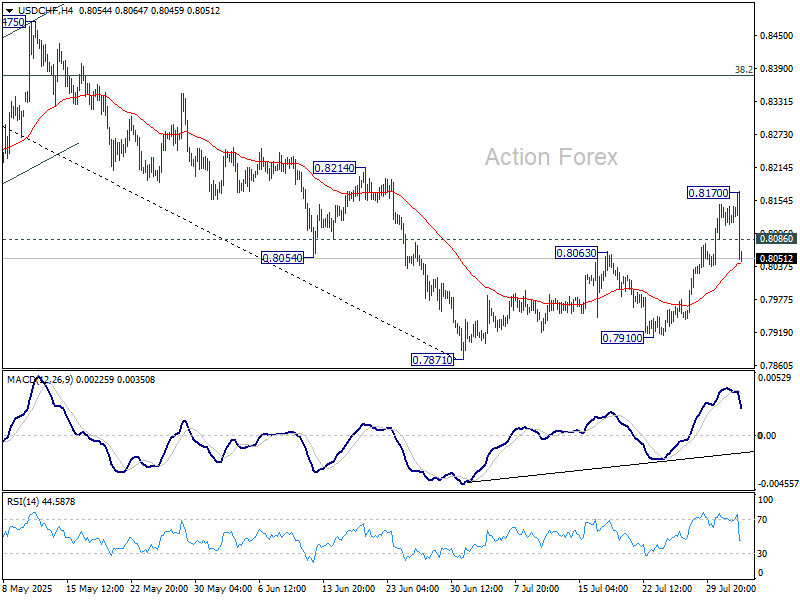

USD/CHF fell sharply after brief surge to 0.8170. Intraday bias is turned neutral first. On the downside, sustained break of 55 4H EMA (now at 0.8043) will argue that rebound from 0.7871 has completed as a three-wave correction. Deeper fall should then be seen back to 0.7871/7910 support zone. Nevertheless, break of 0.8170 will resume the rise to 38.2% retracement of 0.9200 to 0.7871 at 0.8379.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3167; (P) 1.3225; (R1) 1.3263; More...

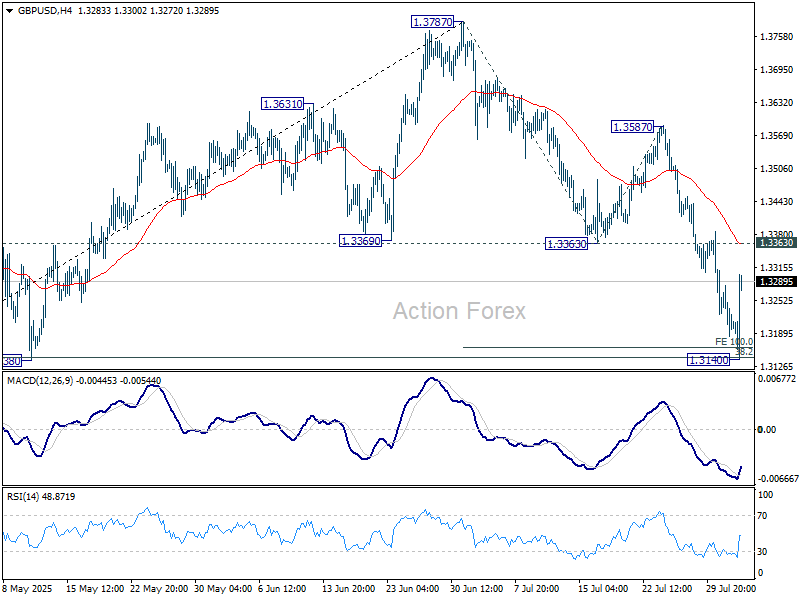

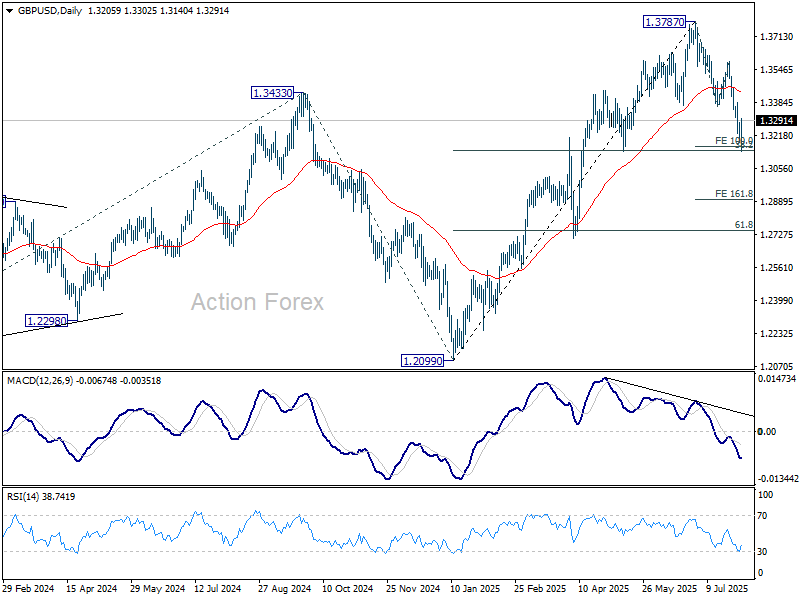

GBP/USD rebounded strongly after hitting 100% projection of 1.3787 to 1.3363 from 1.3587 at 1.3163. Intraday bias is turned neutral first. On the upside, sustained break of 1.3363 resistance turned support will argue that correction from 1.3787 has already completed with three waves down to 1.3140. Further rally should be seen to 1.3587 resistance next. On the downside, firm break of 1.3163 will target 161.8% projection 1.2901 next.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3045) holds, even in case of deep pullback.

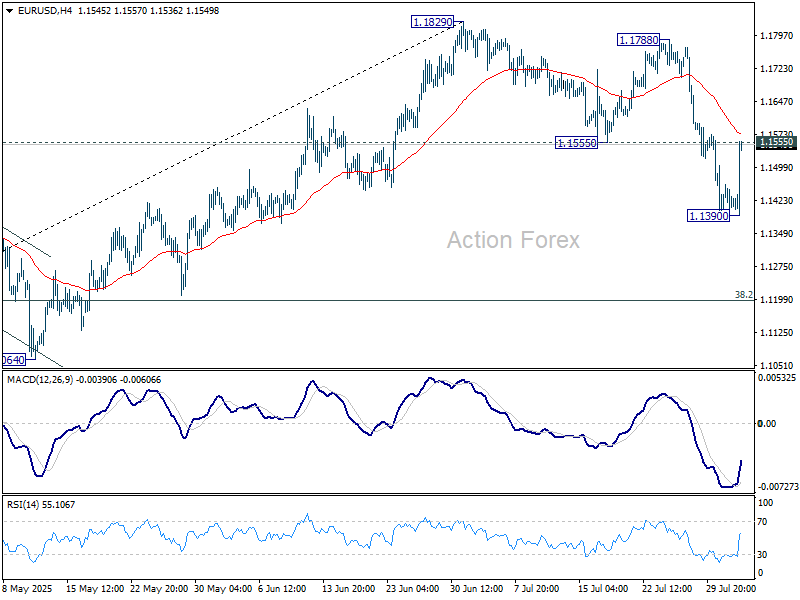

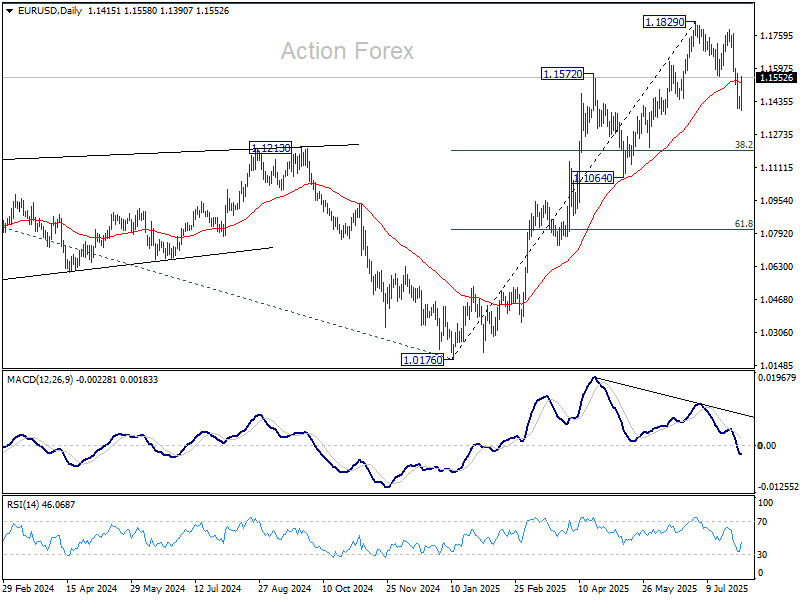

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1391; (P) 1.1426; (R1) 1.1449; More...

Intraday bias in EURUSD is turned neutral first with current strong rebound. Immediate focus is now on 1.1555 support turned resistance. Sustained break there will argue that near term corrective pattern from 1.1829 has already completed with three waves down to 1.1390. Further rise should then be seen to 1.1788/1829 resistance zone. On the downside, though, break of 1.1390 will extend the correction to 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Dollar Tumbles on Jobs Miss, Fed Dissenters Add Fuel

Dollar fell sharply Friday after a dismal July jobs report cast doubt on the resilience of the labor market. While the headline job growth missed expectations, the bigger blow came from a stunning downward revision to June’s figure. The data raised alarm bells that the U.S. labor market may be losing momentum far quicker than previously thought.

Adding to the pressure was a coordinated release by Fed Governors Waller and Bowman, both of whom dissented at this week’s FOMC meeting in favor of a rate cut. Their remarks, published just before the payrolls release, emphasized the risks of delayed action in the face of labor market weakness. Waller argued for a proactive path, while Bowman called the July cut a necessary step toward neutralizing policy. While perhaps coincidental, the synchronized release raised eyebrows and intensified market concerns.

The combined impact of soft jobs data and dovish Fed messaging sent the Dollar lower across the board. Though the greenback still clings to the top spot among major currencies for the week, its lead is looking fragile. If selling persists into the weekend, Dollar could lose its weekly crown. Loonie holds second place, followed by Yen. On the other end, Euro remains the weakest, trailed by Kiwi and Swiss Franc. Sterling and Aussie are middle-of-the-pack. But with volatility likely to persist, rankings could shift before the week closes.

Meanwhile, equity markets in Europe and US are trading lower, showing a sharper reaction than Asia to US President Donald Trump’s newly announced tariff regime. The latest executive order establishes “reciprocal” duties ranging from 10% to 41%, with a 40% penalty on goods transshipped to dodge tariffs. All unlisted countries face a blanket 10% duty. The new rules will take effect August 7.

Canada is among the hardest hit with a 35% tariff, although items covered under the USMCA are exempt. Prime Minister Mark Carney expressed disappointment and rejected Trump’s justification that tariffs were linked to drug trafficking. Switzerland faces a steep 39% duty despite what its government called “constructive” talks with Washington. The Swiss federal council expressed “regret” and signaled it would evaluate its options while continuing diplomatic engagement.

By contrast, Australia escaped with just a 10% rate. Trade Minister Don Farrell called the outcome “a vindication” of Australia’s calm diplomatic strategy. New Zealand wasn’t as fortunate—its rate was raised to 15%, prompting Trade Minister Todd McClay to warn that exporters may begin to feel meaningful strain at that level.

In Europe, at the time of writing, FTSE is down -0.58%. DAX is down -1.88%. CAC is down -2.15%. UK 10-year yield is down -0.024 at 4.549. Germany 10-year yield is down -0.014 at 2.682. Earlier in Asia, Nikkei fell -0.66%. Hong Kong HSI fell -1.07%. China Shanghai SSE fell -0.37%. Singapore Strait Times fell -0.48%. Japan 10-year JGB yield fell -0.003 to 1.553.

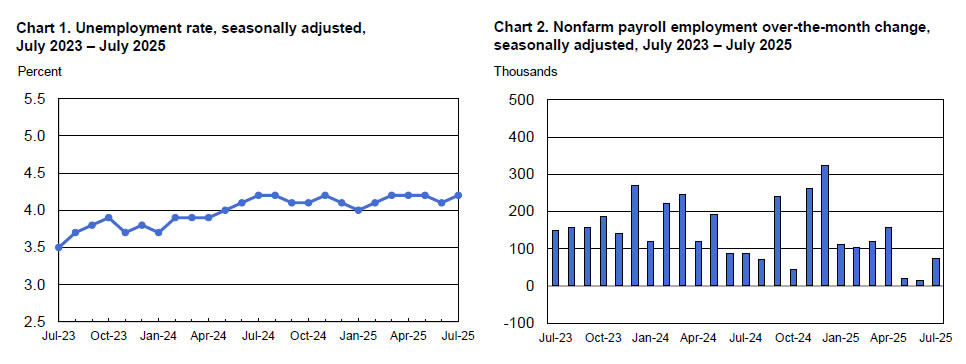

US NFP misses with 73k growth and sharp downward revision

U.S. non-farm payrolls rose just 73k in July, well short of the expected 102k. Unusually large revisions made the picture worse—June’s job growth was slashed from 147k to a mere 14k. Unemployment rate edged up from 4.1% to 4.2% as expected, while average hourly earnings rose 0.3% month-over-month, keeping the annual pace at 3.9%.

While not a disaster, the report showed a clear loss of momentum in hiring, pushing a September rate cut by the Fed back into focus. The sharp downward revision to June data adds weight to concerns that labor market strength is fading more quickly than anticipated.

EUR/USD bounces notably after the release as Dollar is sold off broadly. Immediate focus is now on 1.1555 support turned resistance. Sustained break there will argue that corrective pattern from 1.1829 has completed with three waves down to 1.1390. Further rally would then be seen back to 1.1788/1829 resistance zone.

Fed's Waller and Bowman urge proactive rate cut amid labor market risks

Fed Governors Christopher Waller and Michelle Bowman issued rare public statements today defending their dissenting votes in favor of a rate cut at this week’s FOMC meeting. Both argued that a more proactive approach was needed to support the economy amid slowing growth and labor market softening.

Waller reiterated points he made in a July 17 speech, emphasizing that maintaining the current policy rate risks falling behind the curve. He argued that if tariffs don’t materially worsen inflation, rate reductions should continue at a moderate pace. In contrast, if inflation or employment picks up sharply, the Fed can always pause. “I see no reason we should hold and risk a sudden decline in the labor market,” he stated.

Bowman echoed similar concerns, saying the decision to begin gradually reducing rates was a hedge against further labor market weakness. She stressed that recent inflation increases tied to tariffs are likely transitory, and holding policy too tight could harm the Fed’s employment mandate. “A proactive approach... would avoid an unnecessary erosion in labor market conditions,” she said.

Eurozone CPI steady at 2% in July, reinforces case for ECB pause through rest of 2025

Eurozone inflation held firmer than expected in July, with headline CPI steady at 2.0% yoy, defying expectations for a slight dip to 1.9% yoy. Core CPI was unchanged at 2.3% yoy as forecast. Today’s inflation release reinforces the growing expectation that ECB already completed the easing cycle, as the bar for additional easing is increasingly high.

The underlying components show little sign of disinflation picking up momentum. Non-energy industrial goods inflation rose to 0.8% from 0.5%. While energy inflation remained deeply negative at -2.5%, that decline is slowing. Food inflation ticked up slightly from 3.1% to 3.3%. Services inflation eased only modestly from 3.3% to 3.1%.

Swaps now price in less than 50% chance of another rate cut this year. Comments from officials in recent weeks have leaned cautious, citing inflation stabilization at and waning downside risks tied to the global trade environment. The recent breakthrough in US-EU trade negotiations has also removed a key external headwind.

Besides, major banks are shifting their forecasts in line with this view. Deutsche Bank, Goldman Sachs, and BNP Paribas have all walked back expectations for more cuts in 2025.

European data wrap: PMI points to manufacturing recovery across Europe

China Caixin PMI manufacturing contracts again as export demand falters

China’s Caixin Manufacturing PMI dropped from 50.4 to 49.5 in July, signaling renewed contraction in factory activity and marking the second sub-50 reading in the past three months.

S&P Global’s Jingyi Pan noted that manufacturing production declined for only the second time since October 2023, as firms pulled back operations amid cautious demand outlook heading into H2 2025.

Weaker foreign demand was again a key drag, with export orders remaining sluggish amid global trade tensions. Domestic sales saw some resilience thanks to business development efforts, but overall growth was described as “only fractional.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1391; (P) 1.1426; (R1) 1.1449; More...

Intraday bias in EURUSD is turned neutral first with current strong rebound. Immediate focus is now on 1.1555 support turned resistance. Sustained break there will argue that near term corrective pattern from 1.1829 has already completed with three waves down to 1.1390. Further rise should then be seen to 1.1788/1829 resistance zone. On the downside, though, break of 1.1390 will extend the correction to 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

Fed’s Waller and Bowman urge proactive rate cut amid labor market risks

Fed Governors Christopher Waller and Michelle Bowman issued rare public statements today defending their dissenting votes in favor of a rate cut at this week’s FOMC meeting. Both argued that a more proactive approach was needed to support the economy amid slowing growth and labor market softening.

Waller reiterated points he made in a July 17 speech, emphasizing that maintaining the current policy rate risks falling behind the curve. He argued that if tariffs don’t materially worsen inflation, rate reductions should continue at a moderate pace. In contrast, if inflation or employment picks up sharply, the Fed can always pause. “I see no reason we should hold and risk a sudden decline in the labor market,” he stated.

Bowman echoed similar concerns, saying the decision to begin gradually reducing rates was a hedge against further labor market weakness. She stressed that recent inflation increases tied to tariffs are likely transitory, and holding policy too tight could harm the Fed’s employment mandate. “A proactive approach... would avoid an unnecessary erosion in labor market conditions,” she said.

US NFP misses with 73k growth and sharp downward revision, EUR/USD bounces

U.S. non-farm payrolls rose just 73k in July, well short of the expected 102k. Unusually large revisions made the picture worse—June’s job growth was slashed from 147k to a mere 14k. Unemployment rate edged up from 4.1% to 4.2% as expected, while average hourly earnings rose 0.3% month-over-month, keeping the annual pace at 3.9%.

While not a disaster, the report showed a clear loss of momentum in hiring, pushing a September rate cut by the Fed back into focus. The sharp downward revision to June data adds weight to concerns that labor market strength is fading more quickly than anticipated.

EUR/USD bounces notably after the release as Dollar is sold off broadly. Immediate focus is now on 1.1555 support turned resistance. Sustained break there will argue that corrective pattern from 1.1829 has completed with three waves down to 1.1390. Further rally would then be seen back to 1.1788/1829 resistance zone.

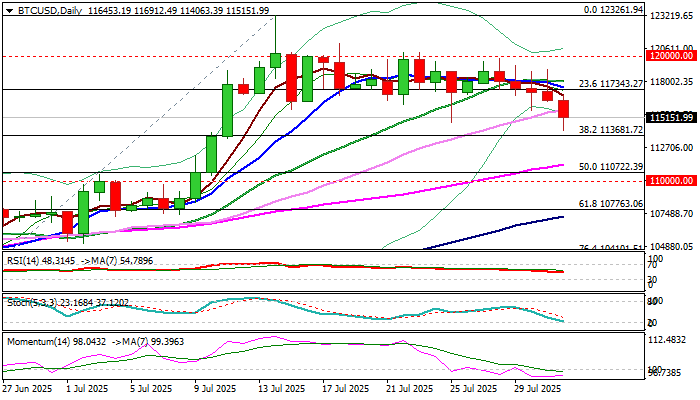

BTCUSD: Break of Two-Week Range Floor is Negative Signal But Key Support Still Holds

BTCUSD fell to three-week low at 114K zone on Friday morning after the latest orders from President Trump to impose trade tariffs on a number of countries, soured the sentiment.

The latest dip that broke below two-week consolidation range generated fresh negative signal that weakened near term structure and shifted focus to the downside.

Daily studies show negative momentum and 10/20DMA’s in bearish setup that fuels negative outlook, as fresh bears pressure pivotal support at 113681 (Fibo 38.2% of 98182/123261 upleg).

Sustained break here is needed to confirm negative signals and open way for deeper pullback towards 112K zone (former record high), 110700 (50% retracement) and 110K (psychological).

However, ability to hold above 113681 Fibo level would ease downside pressure, but bounce above 10DMA (117500, around the mid-point of recent range) will be required to sideline bears and probably bring in focus key barrier at 120K.

Res: 116900; 117500; 118920; 120000

Sup: 114063; 113680; 112000; 111340

European data wrap: PMI points to manufacturing recovery across Europe

Eurozone inflation came in firmer than expected in July, with headline CPI holding at 2.0% yoy, defying forecasts for a slight dip. Core CPI was steady at 2.3%, as anticipated. The data supports the view that the ECB may already be done cutting rates this year, with markets increasingly convinced that further easing will require a significant downside surprise.

More on ECB CPI steady at 2% in July, reinforces case for ECB pause through rest of 2025.

At the same time, Eurozone PMI Manufacturing was finalized at 49.8, up from June’s 49.5 and marking a 36-month high. While still technically in contraction, momentum is clearly improving. According to Hamburg Commercial Bank, smaller economies like Spain and the Netherlands are leading the way, while recessionary signals are fading in larger countries like Germany and France. The new US–EU trade agreement is also expected to ease business uncertainty moving forward.

In the UK, Manufacturing PMI was finalized at 48.0 in July, a six-month high. Output neared stabilization, and future expectations rose to their strongest level since February. While the sector remains in mild contraction, the tone has shifted toward cautious optimism.

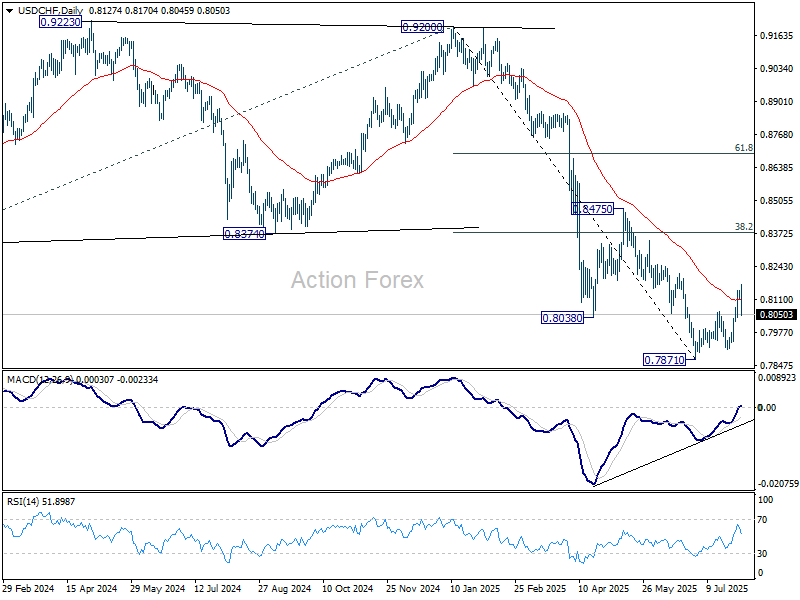

USD/CHF Technical: Swiss Franc’s Medium-Term Bearish Trend in Progress

The Swiss franc has continued to face downside pressure against the US dollar as it extends its losses in place since last Wednesday, 23 July. In today’s Asia, it shed -0.3% at this time of writing, making it the worst-performing major currency against the greenback.

Swiss franc under pressure as US hikes tariffs to 39%, SNB may turn more dovish

The current onslaught of the Swiss franc has been further reinforced by a higher-than-expected US tariff rate of 39% on Swiss products versus the earlier 31% levy announced in April. The latest 39% tariff slapped on Switzerland by the US White House administration is one of the steepest levies globally, which is likely to trigger a significant adverse economic effect on the export-dependent Swiss economy.

After cutting the interest rate to zero in June, the Swiss central bank (SNB) may be forced to adopt a more dovish monetary policy stance to alleviate the negative impact of the higher tariff rates on Swiss exports. The next SNB monetary policy meeting will be on 25 September 2025.

Let’s now focus our attention on a short to medium-term technical trading set-up on the USD/CHF.

Fig 1: USD/CHF medium-term trend as of 1 Aug 2025 (Source: TradingView)

Preferred trend bias (1-3 weeks)

Bullish bias for USD/CHF with key medium-term pivotal support at 0.8060 for the next medium-term resistances to come in at 0.8215/8250 and 0.8350/8380 (also a Fibonacci retracement/extension cluster).

Key elements

- Yesterday’s price action has staged a bullish breakout above the upper boundary of a former medium-term descending channel from the 3 February 2025 swing high, and the 50-day moving average. These observations suggest that the medium-term downtrend of the USD/CHF from 13 January 2025 high to 1 July 2025 has ended.

- The 4-hour RSI momentum indicator has reached its overbought region (above 70 level) but has not flashed out any bearish divergence condition which indicates that short to medium-term upside momentum remains intact.

- The yield premium between the 2-year US Treasury note over the 2-year Swiss government bond has continued to inch upward steadily since 10 July 2025, which is likely to support further potential up moves on the USD/CHF.

Alternative trend bias (1 to 3 weeks)

A break below 0.8060 invalidates the bullish scenario for the USD/CHF to resume its bearish movement to revisit 0.7990 (also the 20-day moving average), and below it exposes the critical 1 July swing low of 0.7870.

USD/CAD Rises to 2-Month High

Today, the USD/CAD exchange rate briefly exceeded the 1.3870 mark – the highest level seen this summer. In less than ten days, the US dollar has strengthened by over 2% against the Canadian dollar.

Why Is USD/CAD Rising?

Given that both the Federal Reserve and the Bank of Canada left interest rates unchanged on Wednesday (as expected), the primary driver behind the pair’s recent rally appears to be US President Donald Trump's decision to impose tariffs on several countries – including Canada:

→ Despite efforts by Prime Minister of Canada Mark Carney to reach an agreement with Trump, no deal was achieved;

→ Canadian goods exported to the US will now be subject to a 35% tariff;

→ The tariffs take effect from 1 August;

→ Goods compliant with the United States-Mexico-Canada Agreement (USMCA) are exempt.

Media analysts note that the tariffs are likely to increase pressure on the Canadian economy, as approximately 75% of the country's exports are destined for the United States.

USD/CAD Technical Analysis

At the end of July, the price formed a steep ascending channel (A-B), with bullish momentum confirmed by a decisive breakout above the 1.3790 resistance level, as illustrated by the arrow:

→ the pullback before the breakout was relatively shallow;

→ the bullish breakout was marked by a long bullish candlestick with a close near the session high;

→ following the breakout, the price confidently consolidated above 1.3790.

Provided that the fundamental backdrop does not undergo a major shift, bulls might attempt to maintain control in the market. However, the likelihood of a correction is also increasing, as the RSI indicator has entered extreme overbought territory.

Should USD/CAD show signs of a correction after its steep ascent, support might be found at:

→ line C, drawn parallel to the A-B channel at a distance of its width;

→ the previously mentioned 1.3790 level, which now acts as a support following the breakout.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.