Sample Category Title

CADJPY Higher Timeframe Outlook – Expanding Trading Horizons

Traders are constantly seeking the next opportunity to elevate their results. A common challenge, however, is that many focus on the same popular products and patterns. So, how can one differentiate their approach?

One effective way is to explore less commonly traded Forex currency pairs.

While some might be concerned about liquidity issues with certain financial products, the Forex market is globally the most liquid.

Even the least traded major forex pairs offer ample liquidity and unique opportunities.

In today's example, let's take a look at CADJPY to spot ongoing trends and why this pair is interesting to trade.

CADJPY is a volatile minor pair that tends to move with different factors, including macroeconomic trends (generally, an appetite for risk means the pair goes higher, risk-off means the pair trades lower) and interest rate differentials—this factor has moved JPY pairs quite a lot in the past few years.

If you want to make these pairs your specialty, keep a close look at communications from both the Bank of Canada and Bank of Japan and track their own economic and inflation reports, which usually precede Central Bank rate decisions.

As a reminder, higher inflation (or inflation outlooks) tends to precede hawkish talks by Central Bank speakers, which then precede interest rate hikes.

The higher the interest rate of a currency, the more demand there is for it (as a rule of thumb, may vary) – One of the reasons why the Yen, which has maintained low rates throughout the past 20 years, has seen substantial depreciation.

About this, let's take a look at Monthly charts.

CADJPY Technical Analysis starting from Higher Timeframes

CADJPY Monthly Chart

CADJPY Monthly Chart, July 17, 2025 – Source: TradingView

The pair has seen some major trends in the past 20 years, starting from a huge descent in 2008 as global Interest Rates began a significant cutting cycle to stimulate the economy post Great Financial Crisis.

The already ultra-loose Japanese Interest Rate gave the yen some relative strength.

On the other hand, when Central Banks started to hike again post COVID, the pair jumped from 73.80 to highs of 118.80, and the top was found in the pair when the 2024 cut cycle from the Bank of Canada began.

Take a look at the interest rate differentials and the price movements of the pair on the chart.

CADJPY Weekly Chart

CADJPY Weekly Chart, July 17, 2025 – Source: TradingView

You can spot on the weekly chart how the expected bottom of interest rates in Canada have coincides with a bottom in CADJPY (followed by actual rise in rates) and the pair hadn't found a top until the 2Y Yield (attached below the CADJPY Chart) started to retract.

The Weekly chart also allows us to spot how rangebound the past year has been in the pair – the range extends from 104.00 Lows to 112.00 Highs.

A weekly bearish cross (Weekly MA 50 crossing the MA 200 from higher to lower) typically announces more selling momentum – However, these trends may take time to happen and may not materialize at all.

Markets are awaiting for any extra hawkishness from the Bank of Japan as Japanese inflation has been turning higher without much doing from the BoJ, hurting the yen and advantaging the CAD in the past few weeks.

CADJPY Daily Chart

CADJPY Daily Chart, July 17, 2025 – Source: TradingView

Now looking at the daily chart, we see more details on the rangebound action as Canada's cut cycle had been fully priced in and concluded (leading to the Mid-2024 correction).

Since, markets awaiting for a move from the Bank of Japan have led to a major range between the 112.00 to 114.00 Resistance Zone to the 102.00 to 104.00 Support Zone.

Since Mid-May however, the Yen has been relatively weak vs other majors and the CAD has gained back some strength, explaining the ongoing upward trendline, further supported by the 50-Day Moving Average – A key barometer to observe as we approach the high of the range.

Watch for any break below the MA 50 to confirm the range, and any new communication from the respective Central Banks (Particularly the Bank of Japan, tonight will see the release of their Inflation numbers)

Safe Trades!

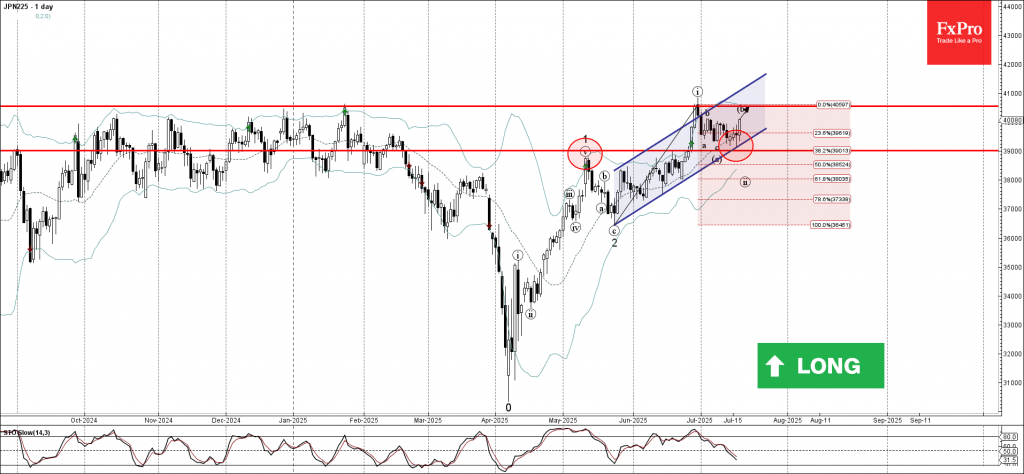

Nikkei 225 Wave Analysis

Nikkei 225: ⬆️ Buy

- Nikkei 225 rever

- stance level 40550.00

Nikkei 225 index recently reversed up with the daily Doji from the support area located between the key support level 39000.00 (former resistance from May) and the support trendline of the daily up channel from May.

This support area was further strengthened by the 38.2% Fibonacci correction of the sharp upward impulse i from May.

Given the strong daily uptrend and the improved sentiment across global equity markets, Nikkei 225 index can be expected to rise to the next resistance level 40550.00 (former multi-month high from January).

Fed’s Kugler sees more tariff inflation coming, favors holding steady for some time

Fed Governor Adriana Kugler said she favors keeping interest rates unchanged "for some time," citing a resilient labor market and rising inflation pressures from tariffs.

In a speech today, she noted that both headline and core inflation "have shown no progress in the last six months". Instead, this week's CPI and PPI report showed core goods prices are now driving inflation higher, "partially reflecting the pass-through of increased tariffs". Kugler said she expects inflation to accelerate further through the second half of 2025 as "larger effects of tariffs are still coming".

While acknowledging some moderation in broader economic activity, Kugler emphasized that the labor market remains stable and near full employment. She also flagged geopolitical risks as a potential wildcard for inflation in the months ahead.

EURUSD at a Tipping Point

The most traded Forex pair hasn't disappointed traders in terms of trends and volatility throughout 2025.

Going from 1.02 to 1.18 highs in 7 months, there had been some decisive momentum to participate with as this strong buying took the Euro to highs unseen since 2021.

The geopolitical mishandles from the Trump Administration earlier this year had led to European leaders putting back the Euro unification back on the table. After some major deals were announced from Germany and other Euro Nations, the Euro started its ascent. to up 15% on the year at one point.

This theme got accompanied with general lack of confidence from the Trump Administration which led to some major US Dollar selling and financial flows rewiring.

But, it seems today that markets are taking profits on these trends, leading to some intermediate tops in the Pair currently – Let's take a look at EURUSD Technicals to spot if there is any elements to help us see if the flows have really shifted or not.

EURUSD Multi-Timeframe analysis going from the Daily to 1H Charts

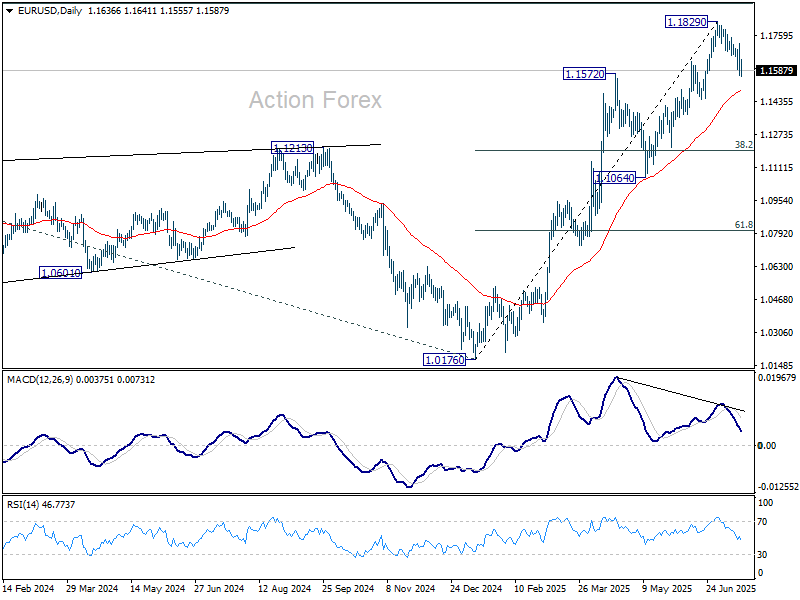

EURUSD Daily

EUR/USD Daily Chart, July 17, 2025 – Source: TradingView

The Israel-Iranwar consolidation in the pair had led to a major relief rebound towards the 1.1830 2025 Highs in a strong fashion – from 1.1450 to the highs in 7 consecutive bull candles (Tight bull channel).

However, since July 1st, all currencies have found some of their strength against the US Dollar taken back and the Euro hasn't been an exception.

Almost all daily candles have been red since that day and prices are close to back to pre-end-of-war levels – Momentum just fell below the mid-line, indicating some seller strength which will have to decisively breach below. the 50-Day Moving average to regain more control.

Higher timeframe levels to keep an eye on:

Resistance Levels:

- Current Pivot Zone 1.16 to 1.1650

- 2020 Resistance around the 1.18 Zone (2025 Highs)

- Sep 2021 Highs – Main Resistance 1.20 Zone

Support Levels:

- 1.15 Support Zone (Confluence with 50-Day MA)

- 1.12 to 1.13 Main Support Zone

- 1.10660 Last major pivot to the upside

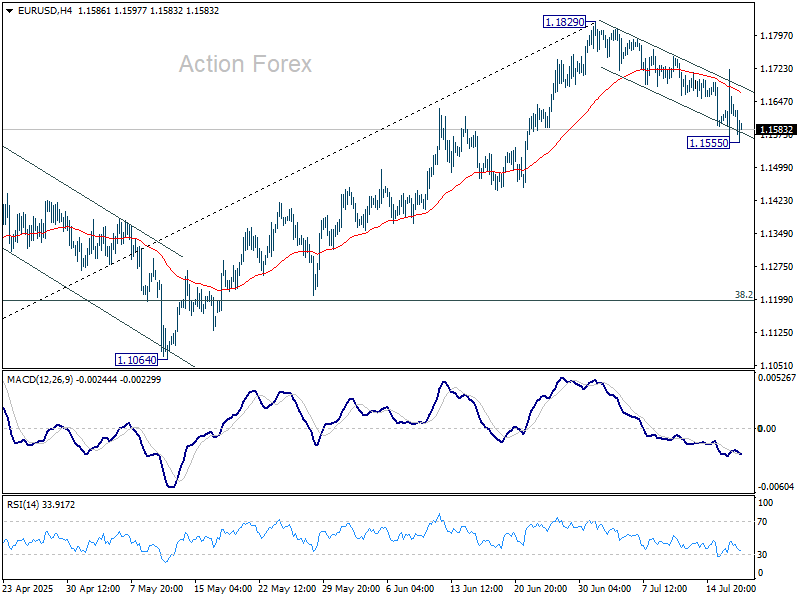

EURUSD 4H

EUR/USD 4H Chart, July 17, 2025 – Source: TradingView

Looking closer allows to observe the current ongoing descending downwards channel were prices have trended down with some regularity but the move is currently stalling as markets approach oversold levels.

Prices are currently evolving between the 50 and 200 4H Moving Averages as buyers held the 1.16 Support Zone (smaller timeframe support) to bid the Pair during the past day Syria War headlines.

Monitor closely any decisive break below the 200 MA that is currently holding prices – We are currently trading just below that indicator but we would require a stronger move to assume more bearishness.

In the meantime, there is a somewhat high probability to retest the high of the range that revisits the 50 MA at the same time around 1.1678 but prices will first have to cross the 1.1620 to 1.1650 Pivot Zone.

EURUSD 1H

EUR/USD 1H Chart, July 17, 2025 – Source: TradingView

The ongoing session has begun with a double bottom right at the bottom of the 1.16 Support Zone (1.1560).

Anyways, buyers will still have to breach back into the downwards channel (which has been broken out overnight – coincides with the 1.16 psychological Level) to avoid a further bearish continuation.

Take a look at reactions at the low of the channel, the 1H MA 50 and the 1.1650 Pivot Zone if prices do get there.

Safe Trades!

US Retail Sales Shine, Dollar-Yen Jumps, Japan Inflation Expected to Ease

The Japanese yen continues to have a busy week, with strong movement in both directions. In the North American session, USD/JPY is trading at 148.53, up 0.45% on the day. On Wednesday, USD/JPY strengthened to 149.18, its highest level since March.

US retail sales surprise with 0.6% gain

US retail sales have been in the doldrums of late, posting declines in April and May as consumers reacted with a thumbs-down to President Trump's tariffs, which took effect in April and made imported goods more expensive.

The markets had anticipated a marginal gain of just 0.1% m/m in June but retail sales came in at an impressive 0.6%, bouncing back from -0.9% in May. Most sub-categories recording stronger activity in June.

The US tariffs appear to have had a significant impact on retail sales, as consumers continue to time their purchases to minimize the effect of tariffs.

Consumers increased spending ahead of the tariffs and cut back once the tariffs went into effect. With a truce in place between the US and China which has slashed tariff rates, consumers opened their wallets and purchased more on big-ticket items such as motor vehicles, which jumped 1.2% in June.

With Trump threatening new rounds of tariffs against allies such as Canada and Japan on August 1 if no agreements are reached, it will be interesting to see if consumer spending reverses direction next month.

Japan's inflation rate expected to ease

This week, the US and UK posted higher inflation numbers for June, but Japan is not expected to follow suit. Headline inflation is projected to drop to 3.3% y/y from 3.7% in May and core CPI, which is closely watched by the Bank of Japan, is expected to drop to 3.3% from 3.5%. If inflation is higher than expected, it will raise expectations for a rate hike from the BoJ in the fourth quarter.

USDJPY Technical

- There is resistance at 148.00 and 149.08

- 146.80 and 145.72 are providing suppport

USDJPY Technical 1-Day, July 17, 2025

Sunset Market Commentary

Markets

(Equity) markets of late showed remarkable resilience to multiple sources of (potential) risk. Those risks were supposed to remain risks that in the end won’t materialize. This attitude in some way again dominated trading this morning. President Trump signaling that multiple (150) countries would get a letter advocating tariffs of about 10-15%, can be seen as an indication that the trade war could be settled at a sub-optimal, but manageable, level. This is also the hoped for conclusion for the outcome of pending negotiations with other majors (EU, Japan en even China). Trump added a new layer of uncertainty as he steps up efforts to dismiss Fed Chair Powell. After a spike in risk aversion yesterday, this issue for now is also shelved. Market expectations on Fed policy show remarkable stability. Any indication on tariff-related inflation is still countered by easing services inflation, making the Fed’s by default wait-and-see stance the most logical option. There even was no additional headline news on the debt sustainability issue. This ‘’volatility narrative” allows (US) stocks to hold near record levels (S&P 500 unchanged). European indices also continue to perform well given recent euro strength (Eurostoxx 50 +1.0%). In this context, today’s US data (Philly Fed survey, jobless claims, retail sales) likely would only be of short-term relevance even in case of an outcome out of line with consensus. This was exactly what happened. All three series were better than expected. Headline retail sales rose 0.6% M/M (0.1% expected), control group sales 0.5% M/M. Jobless claims dropped further to 221k (from 227k). The Philly Fed business outlook jumped to 15.9 from (-4.0 and -1.0 expected). In line with other price data this week, headline import prices (0.1%M/M; -0.2% Y/Y) were softer than expected even as the likes of consumer goods (0.4% M/M) showed tentative signs of rising. US yields initially gained modestly after the release, but currently are trading modestly lower (<3 bps). Idem for German yields. For now, the combination of solid US data, yields discounting the Fed not rushing into easing and the debate on the replacement of Powell moving to the background, supports the recent technical rebound of the dollar. DXY trades at 98.75 (from 98.35). EUR/USD declines modestly (1.1590). USD/JPY also rebounds after yesterday’s setback, but at 148.6 still trades below this week’s peak levels. The UK labour market data showed a further decline in payrolled employment in June (-41k). The unemployment rate ticked higher to 4.7%. Weekly earnings eased but stay elevated (5% from 5.4%). UK yields are gaining modestly (up to 3 bps). The report doesn’t change the trajectory of gradual further BoE easing (August/Nov) with markets currently positioned in a cautious wait-and-see bias 25 bps Nov not yet fully discounted). Sterling eases modestly against a broadly stronger dollar (Cable 1.3395). Against the euro, sterling extends its technical comeback of the 0.87 barrier.

News & Views

The UK and Germany today signed a “Friendship and Bilateral Cooperation Treaty” in London. Both reaffirm their commitment to deepening cooperation to ensure a prosperous, secure, and sustainable future. They recognize the evolving geopolitical landscape, particularly the threat posed by Russia’s aggression in Europe, and emphasize the importance of defending democracy, human rights, and the rule of law. They aim to strengthen their partnership in areas such as security and defense, climate action, economic collaboration, technological innovation and respect for governance structures. They also highlight the importance of the UK-EU relationship and the legal frameworks that support it, and reaffirm their commitment to the Transatlantic Alliance. Separately, they drew up a list as part of an implementation plan to deliver on 17 priority projects (to be reviewed every two years). Ukraine recovery and reconstruction tops the list together with the Trinity House defense agreement.

EU Climate Commissioner Hoekstra told Bloomberg that the €400bn crisis tool presented by the EC in yesterday’s €2tn 2028-2034 budget proposal would be funded using joint borrowing. The crisis tool would provide loans to countries to react faster to adverse events, according to sources. Hoekstra added that the mechanism would be subject to strict controls such as unanimity among the 27 EU states..

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1561; (P) 1.1642; (R1) 1.1721; More...

Intraday bias in EUR/USD remains neutral first. Risk Risk will stay mildly on the downside as long as 1.1829 resistance holds. Fall from there is correcting the rise from 1.1829 or whole rally from 1.0176. Below 1.1555 will target 55 D EMA (now at 1.1478). Sustained break there will target 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

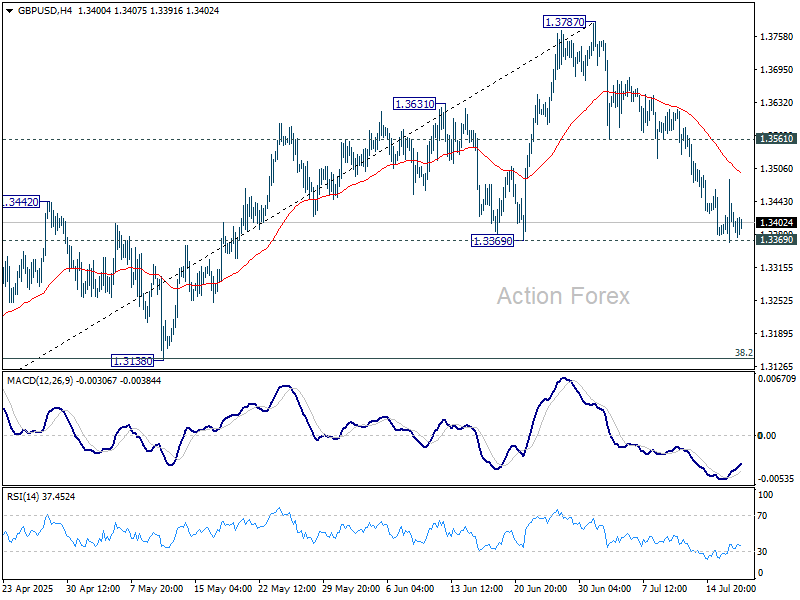

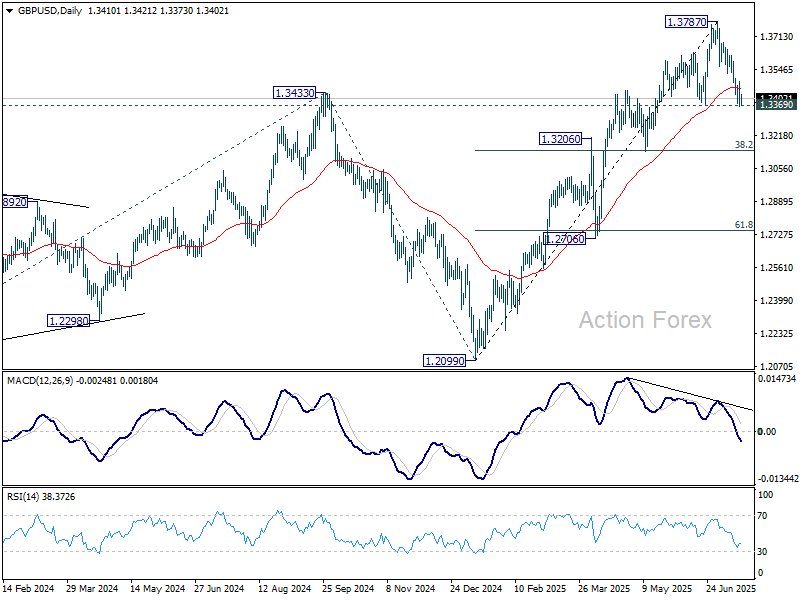

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3361; (P) 1.3424; (R1) 1.3482; More...

Intraday bias in GBP/USD remains neutral and focus stays on on 1.3369 support. Decisive break there will suggests that it's already correcting the rise from 1.2099. Deeper fall should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Nevertheless, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

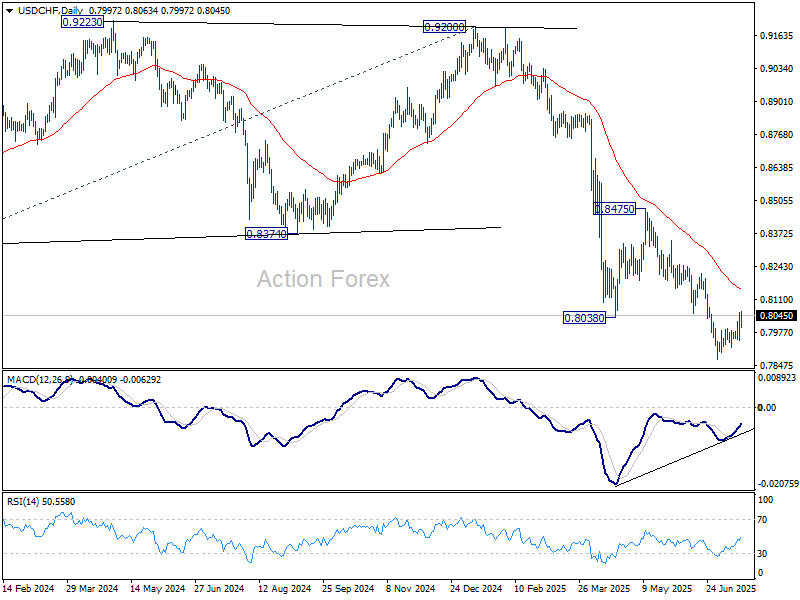

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7950; (P) 0.8006; (R1) 0.8065; More….

No change in USD/CHF's outlook. Intraday bias stays neutral with focus on 0.8054 support turned resistance. Decisive break there will suggest that it's at least correcting the fall from 0.8475. Further rise should then be seen to 55 D EMA (now at 0.8151). Nevertheless, rejection by 0.8054 will retain near term bearishness. Below 0.7946 minor support will bring retest of 0.7871 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.