Sample Category Title

XAU/USD Chart Analysis: Volatility at a Yearly Low

The daily chart of XAU/USD shows that the Average Directional Index (ADX) has reached its lowest level since the beginning of 2025, indicating a significant decline in gold price volatility.

Yesterday’s release of the US Producer Price Index (PPI) initially triggered a sharp spike in gold prices, but the gains were short-lived, with the price quickly reverting to previous levels. This price action aligns with a broader market narrative of equilibrium—where supply and demand are in relative balance, and the market appears to be efficiently pricing in key influencing factors, including geopolitical tensions and tariff-related developments.

However, this fragile balance may soon be disrupted.

Technical Analysis of XAU/USD

From a broader technical perspective, gold remains within a long-term ascending channel (highlighted in blue) in 2025. Key observations include:

→ Attempts to rebound from the lower boundary of the channel (marked with arrows) lack conviction. Bulls are not capitalising on these opportunities to reignite the uptrend, suggesting a potential exhaustion of buying interest.

→ A trendline drawn across the major highs of 2025 has proven to be a strong resistance level. All recent breakout attempts have failed at this barrier.

As a result, the XAU/USD chart is showing signs of forming a large-scale triangle pattern, with its axis centred around the $3,333 level. If bulls continue to falter in extending the multi-month rally, it could encourage bears to challenge the lower boundary of the ascending channel, increasing the risk of a downside breakout.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Pause in Dollar Rally: Weak Data and Powell Dismissal Rumours

Amid rising market volatility, the US dollar is losing ground: USD/JPY is correcting after a recent bullish impulse, while USD/CAD is retreating from the upper boundary of its medium-term sideways range. This corrective movement was triggered by disappointing US producer price index (PPI) data and speculation surrounding a potential dismissal of Federal Reserve Chair Jerome Powell—rumours later denied by Donald Trump.

Yesterday's US macroeconomic data underperformed expectations: the core PPI was flat month-on-month (forecast: +0.2%), while the annual reading slowed to 2.6% versus the expected 2.7%. The headline PPI also showed weakness, fuelling speculation that the Federal Reserve might accelerate its easing cycle if producer price pressures continue to weaken.

Market participants also reacted to a brief spike in volatility following unconfirmed reports that Powell could be removed from office. Although the rumour was quickly debunked, the episode has contributed to lingering unease in the dollar-denominated asset segment.

In the near term, traders’ attention is shifting towards today’s US labour market data, which could shape the dollar's direction for the remainder of the week.

USD/JPY

After updating its May highs, USD/JPY sharply pulled back and is currently trading near the 148.00 level. Technical analysis suggests the potential for a deeper correction, as a bearish engulfing pattern has formed on the daily timeframe. However, if recent highs are breached again, the pair may resume its rally towards the 150.00–151.00 range.

Key events likely to influence USD/JPY today:

- 15:30 (GMT+3): US Core Retail Sales

- 15:30 (GMT+3): US Initial Jobless Claims

- 15:30 (GMT+3): Philadelphia Fed Manufacturing Index

USD/CAD

USD/CAD has been consolidating in the 1.3550–1.3600 range for an extended period, despite heightened volatility and a mixed macroeconomic backdrop in recent weeks. Yesterday’s pullback from the 1.3750 level resulted in the formation of a bearish engulfing pattern, although the prevailing sideways trend suggests that the formation may lack sufficient momentum for a sustained downside move. The 1.3740–1.3760 zone remains a key resistance area; if price breaks and holds above this range, a test of the 1.3800 level could follow.

Key events that may impact USD/CAD pricing today:

- 15:30 (GMT+3): Canada Foreign Securities Purchases

- 19:45 (GMT+3): Speech by FOMC Member Mary Daly

- 20:00 (GMT+3): Atlanta Fed GDPNow Estimate

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD Under Pressure Amid Strong US Dollar Sentiment

The EUR/USD pair has dipped back into negative territory, trading at 1.1615 as the US dollar regains ground following yesterday’s losses.

Market sentiment was initially rattled by reports suggesting Federal Reserve Chair Jerome Powell could be dismissed. Although Donald Trump later described these rumours as “unlikely”, the speculation reignited concerns over the central bank’s independence.

On the macroeconomic front, weaker-than-expected US producer inflation data added to the case for potential Fed rate cuts later this year. June’s price index remained flat, contrary to forecasts of a modest rise.

Traders now await retail sales figures, which could provide further insight into the strength of US domestic demand.

Meanwhile, trade tensions persist as Trump reaffirmed plans to maintain 25% tariffs on Japanese imports while hinting at a potential new trade deal with India. Earlier in the week, he also signalled progress in negotiations with Indonesia. These developments suggest the White House is balancing its hardline trade stance with efforts to engage Asian partners.

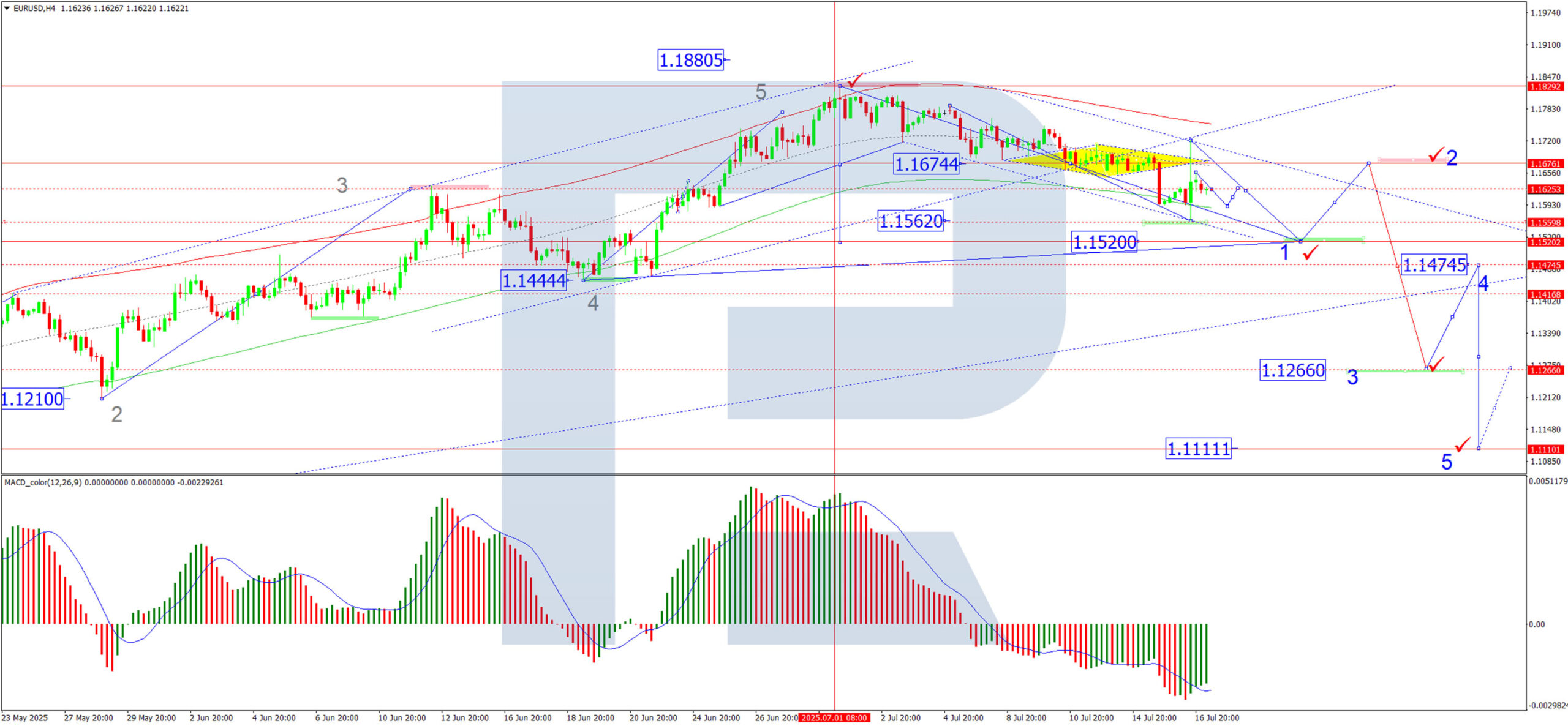

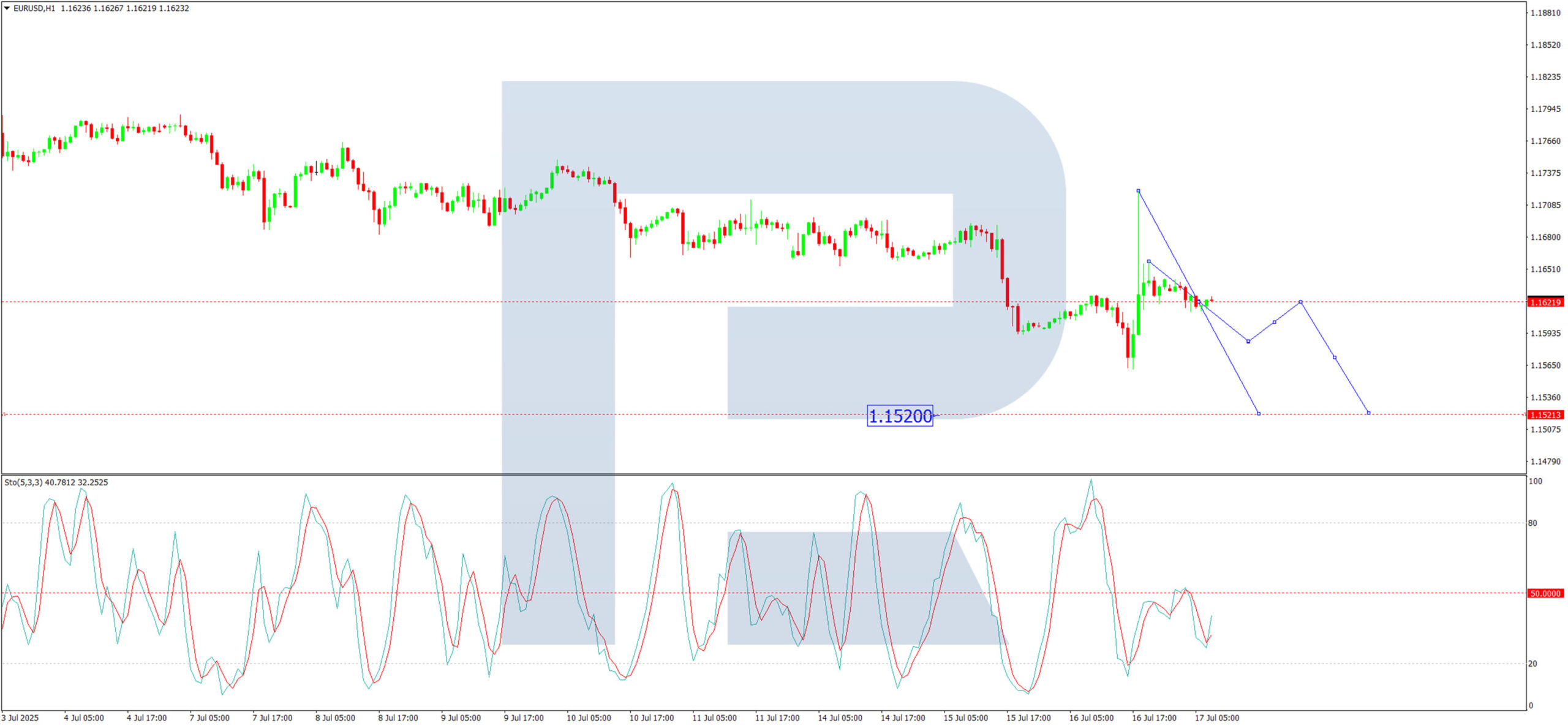

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, the EUR/USD pair has formed a consolidation range following the breakdown from the growth channel at 1.1675 and has subsequently completed a downward move towards the local target of 1.1562. A correction back to the 1.1720 level has also taken place. At present, a new wave of decline is developing towards 1.1520. Technically, this scenario is confirmed by the MACD indicator, as its signal line is below zero and pointing firmly downward.

H1 Chart:

On the H1 chart, the EUR/USD pair has executed a downward impulse to 1.1610, followed by a correction to 1.1658. Today, a tight consolidation range is expected to form around 1.1620. If the pair breaks lower from this range, a move towards 1.1585 becomes likely, with the potential for further downside continuation to 1.1520. Technically, this scenario is confirmed by the Stochastic oscillator: its signal line lies below 50 and is heading sharply lower towards 20.

Conclusion

The EUR/USD remains under pressure amid dollar strength, with technical indicators supporting further downside potential. Market focus now shifts to upcoming US retail sales data and evolving trade dynamics.

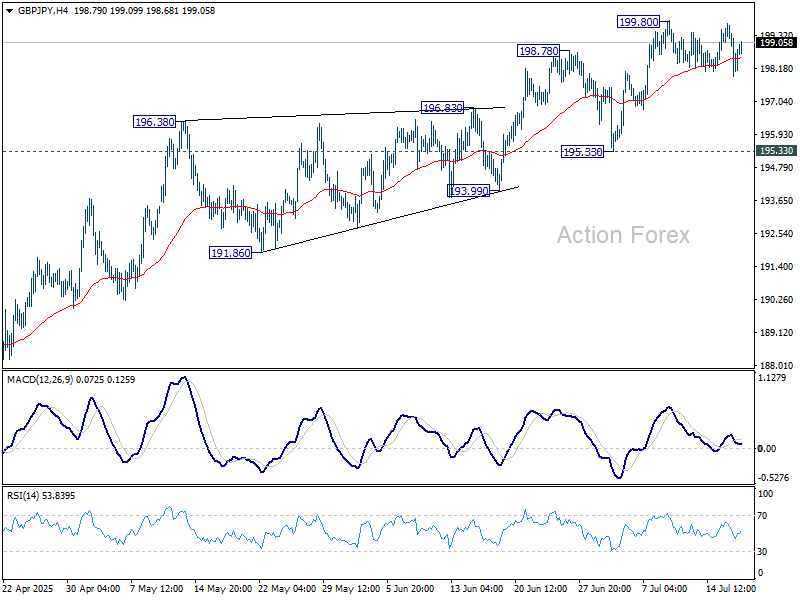

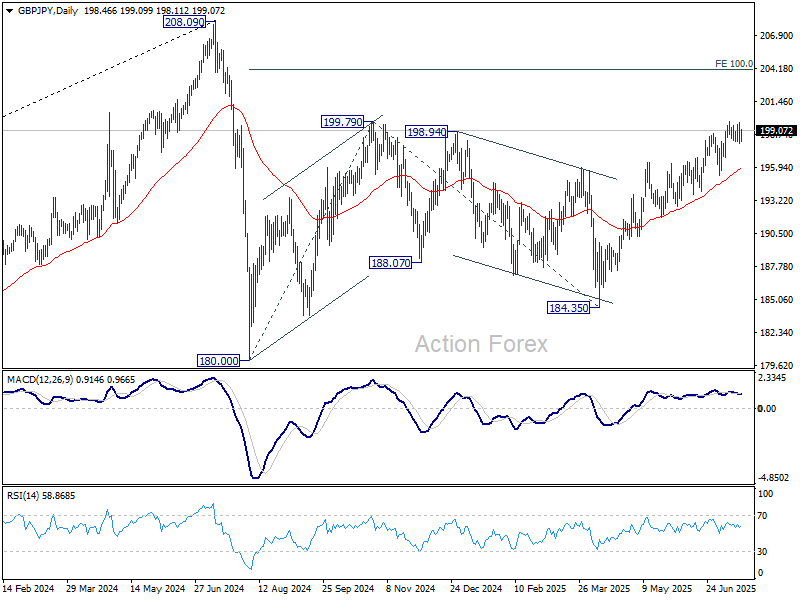

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.69; (P) 198.71; (R1) 199.49; More...

Intraday bias in GBP/JPY remains neutral as consolidations continue below 199.870. While deeper retreat cannot be ruled out, further rise is expected as long as 195.33 support holds. On the upside, break of 199.80 will resume the rally from 184.35 and target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

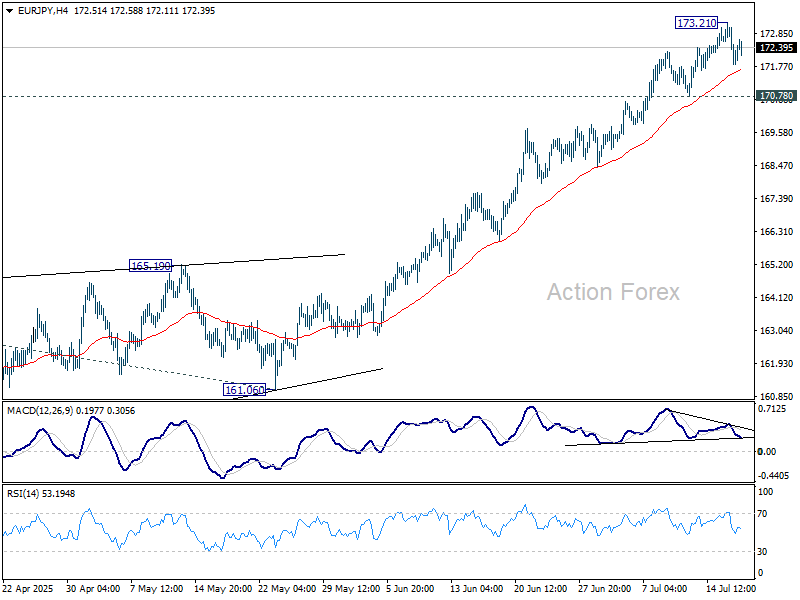

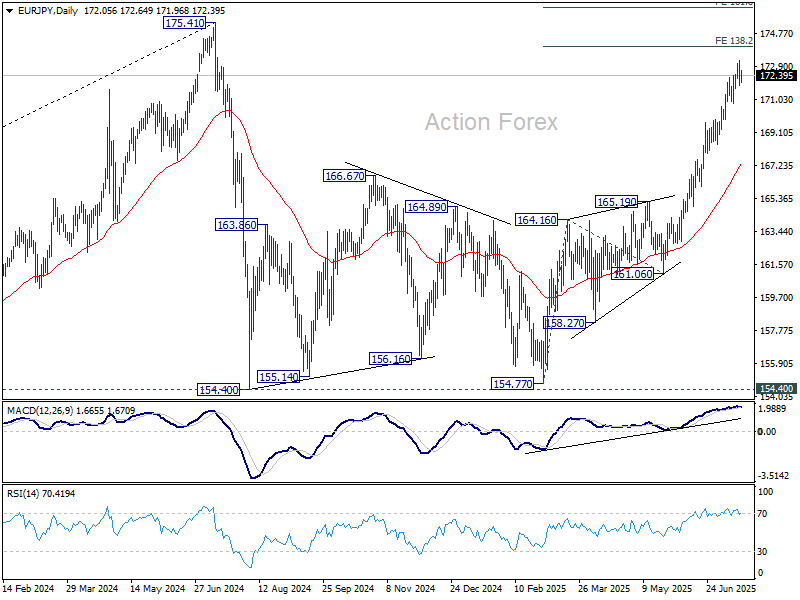

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.58; (P) 172.41; (R1) 172.98; More...

A temporary top is formed at 173.21 with current retreat and intraday bias in EUR/JPY is turned neutral first. Some consolidations would be seen but further rally is expected as long as 170.78 support holds. Above 173.21 will resume the rise from 154.77 to 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03.

In the bigger picture, price actions from 175.41 (2024 high) are seen as correction to up trend from 114.42 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. Meanwhile, decisive break of 175.41 will confirm long term up trend resumption.

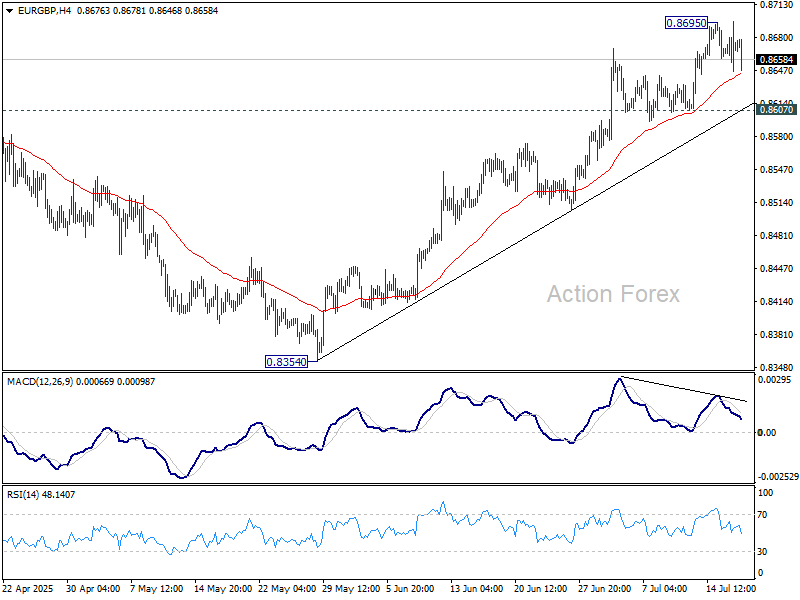

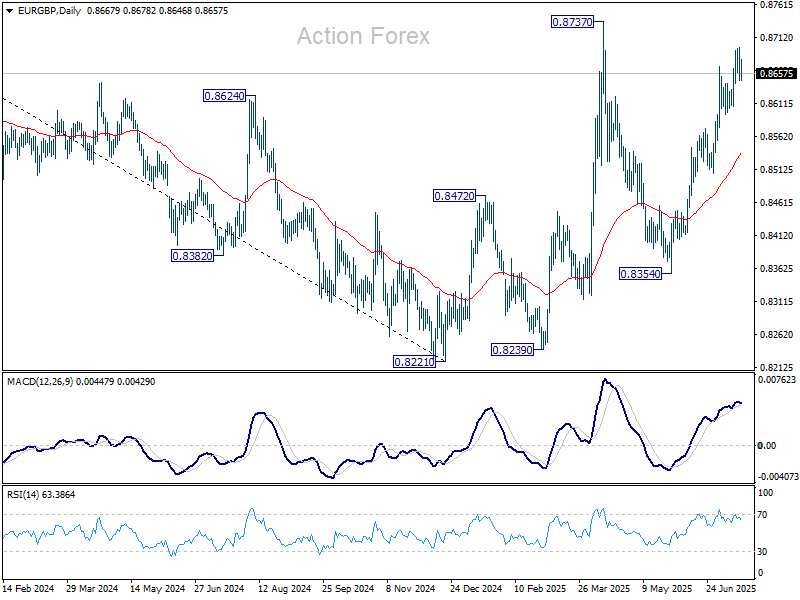

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8649; (P) 0.8674; (R1) 0.8700; More...

Intraday bias in EUR/GBP remains neutral for consolidations below 0.8695. Further rise is expected as long as 0.8607 support holds. Above 0.8695 will target 0.8737 high. Decisive break there will resume the whole rise from 0.8221 low, and target 0.8867 fibonacci level. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 0.8607 will argue that rebound from 0.8354 has completed, and turn bias back to the downside for 55 D EMA (now at 0.8537).

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867.

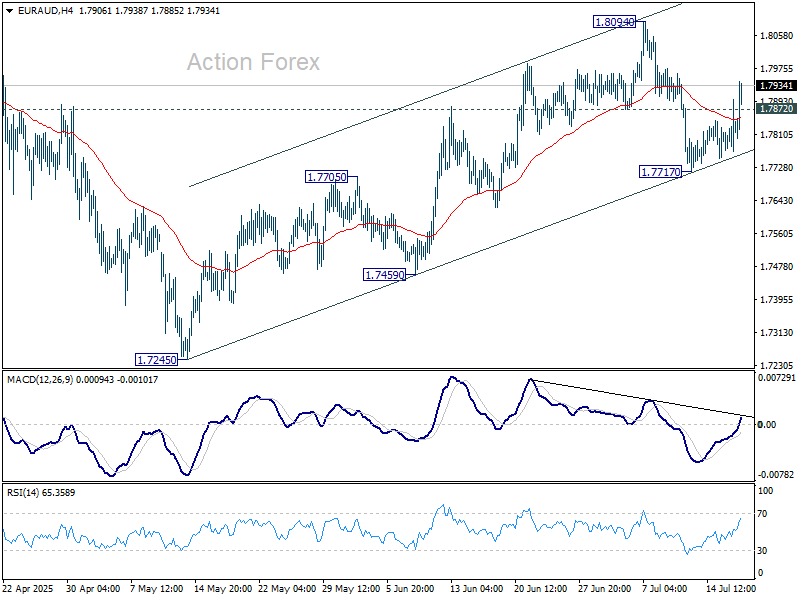

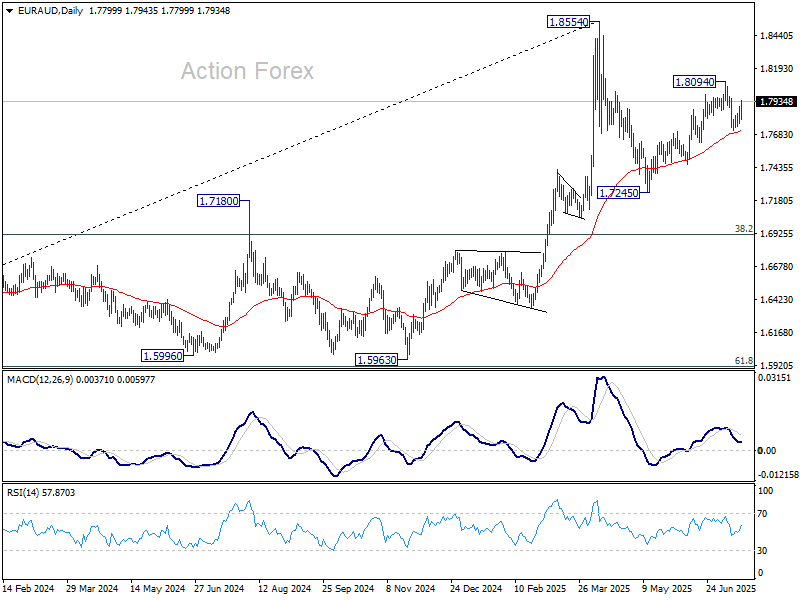

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7769; (P) 1.7834; (R1) 1.7896; More...

EUR/AUD's break of 1.7872 resistance argues that pullback from 1.8094 has completed already. Strong support from 55 D EMA (now at 1.7706) suggests that rise from 1.7245 is still in progress. Intraday bias is back on the upside for 1.8094 first. Firm break there will target 1.8554 high next.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

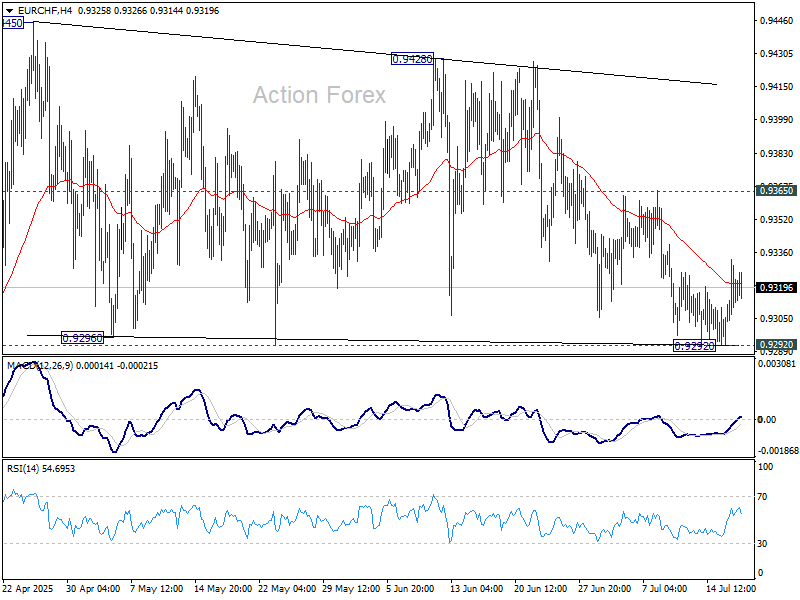

EUR/CHF Daily Outlook

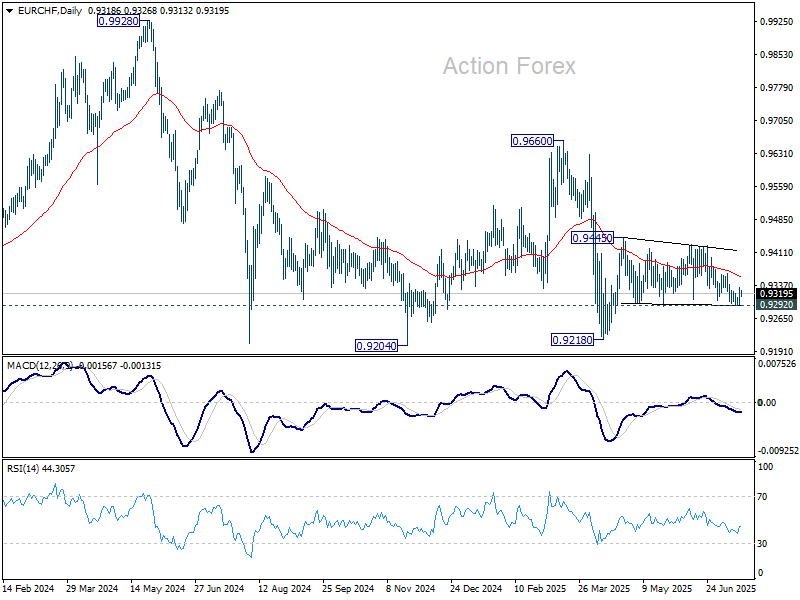

Daily Pivots: (S1) 0.9298; (P) 0.9317; (R1) 0.9342; More....

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, break of 0.9365 resistance will suggest that fall from 0.9428 has completed. Further rally should be seen to retest 0.9428/45 resistance zone. Firm break there will resume the rebound from 0.9218. On the downside, firm break of 0.9292 support will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9437) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1561; (P) 1.1642; (R1) 1.1721; More...

A temporary low is formed at 1.1561 and intraday bias is turned neutral. Risk will stay mildly on the downside as long as 1.1829 resistance holds. Fall from there correcting the rise from 1.1829 or whole rally from 1.0176. Below 1.1561 will target 55 D EMA (now at 1.1478). Sustained break there will target 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

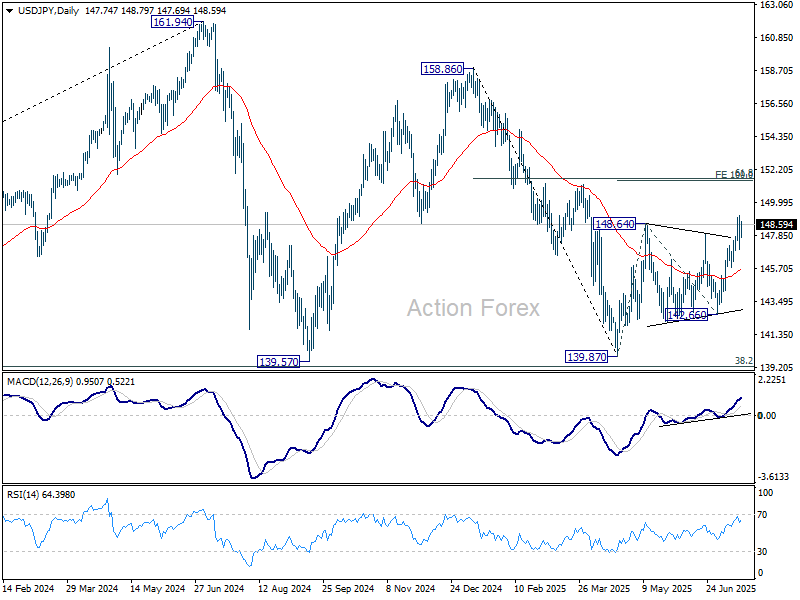

USD/JPY Daily Outlook

Daily Pivots: (S1) 146.80; (P) 148.00; (R1) 149.08; More...

Intraday bias in USD/JPY is turned neutral first with a temporary top formed at 149.17. Some consolidations would be seen but downside should be contained by 55 D EMA (now at 145.56). Break of 149.17 will resume the whole rise from 139.87 to 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.