Sample Category Title

Aussie unemployment rate surges to 4.3% as full-time jobs slide

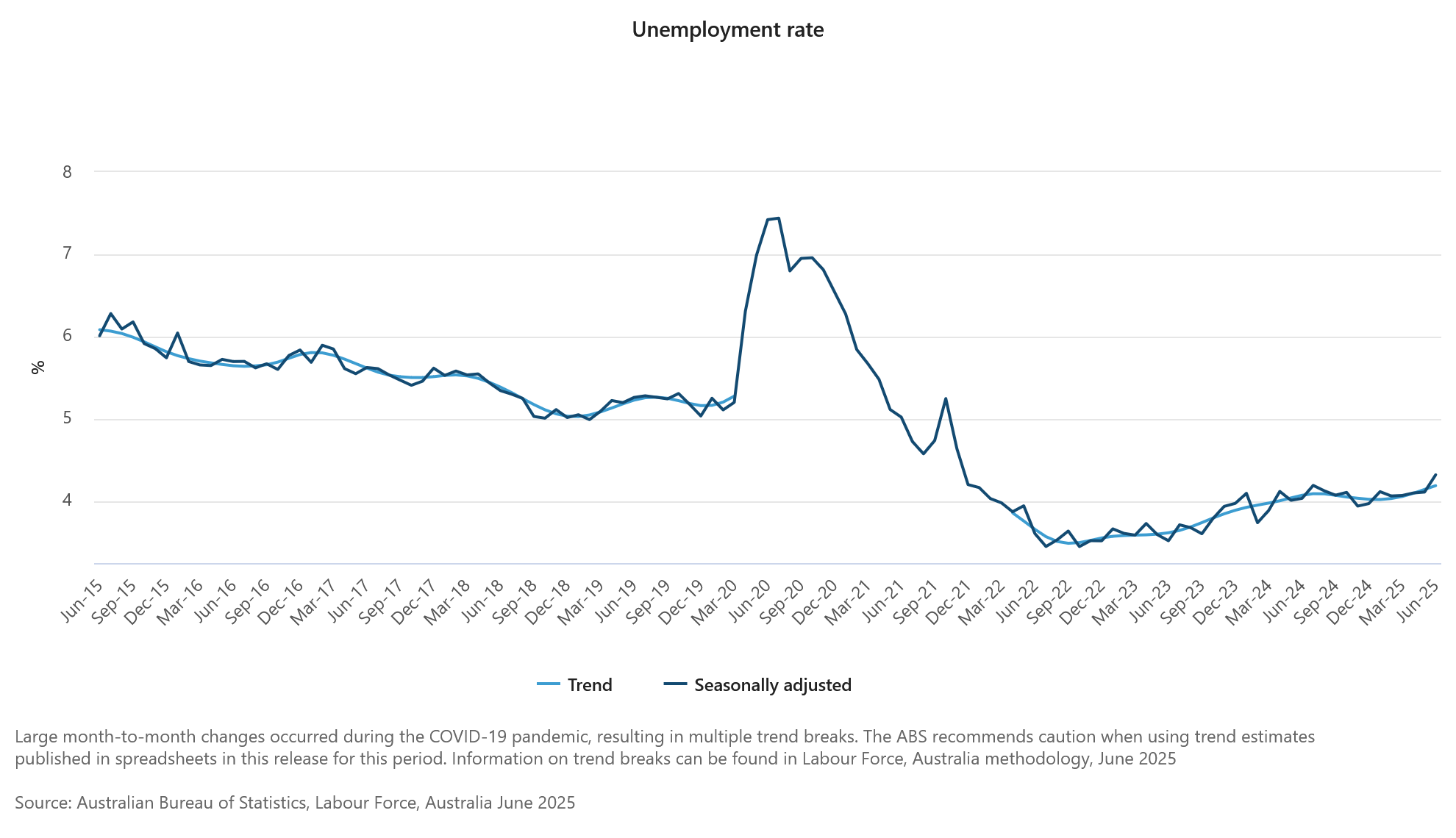

Australia’s June jobs report came in well short of expectations, with only a 2k increase in employment and a sharp divergence between full-time and part-time work. Full-time employment plunged by -38.2k while part-time roles rose 40.2k. Unemployment rate rose to 4.3%, defying forecasts for it to hold at 4.1%, while participation rate remained unchanged at 67.0%.

According to the ABS, the rise in joblessness was driven by a 34k increase in the number of unemployed Australians. ABS labor head Sean Crick added that full-time hours worked declined -1.3% in the month, suggesting further weakness ahead. Despite a marginal rise in total hours worked of 0.1% mom, the data add to signs that the labor market is losing momentum.

Japan auto exports to US plunge -26.7% yoy as carmakers cut prices

Japan logged a trade surplus of JPY 153B in June, with exports down -0.5% yoy and imports up 0.2% yoy. The most striking detail was a sharp -11.4% yoy drop in exports to the US, the steepest decline since February 2021. Imports from the US also fell, declining -2.0% yoy.

Automobile shipments to the US fell -26.7% by value, while auto parts (-15.5% yoy) and pharmaceuticals (-40.9% yoy) also saw double-digit drops. Still, a 3.4% yoy rise in car export volumes suggests Japanese automakers are slashing prices and absorbing costs to maintain market share.

On a seasonally adjusted basis, exports dipped -0.4% mom while imports fell -1.0%, leaving a JPY 235B trade deficit.

The report comes just weeks before a 25% reciprocal US tariff on Japanese goods takes effect on August 1. That is one percentage point higher than the 24% rate first announced on "Liberation Day" in April.

Fed’s Williams: Inflation to hit 3–3.5% as tariffs bite

New York Fed President John Williams warned that tariff effects are only beginning to show up in the data and could push inflation significantly higher in the months ahead. Speaking overnight, Williams said the full impact of US tariffs will take time to materialize, but expects them to add “about 1 percentage point” to inflation through the second half of this year and into early 2026. While he acknowledged current data shows only “modest” impact, he anticipates upward pressure will grow meaningfully.

Williams forecast inflation to average between 3% and 3.5% in 2025, before cooling to around 2.5% in 2026 and only returning to the Fed’s 2% target by 2027. For June specifically, he expects headline inflation at 2.5% and core at 2.75%. Alongside elevated price pressures, he also projects a slowing economy, with growth easing to around 1% this year and unemployment rising to 4.5% from the current 4.1%.

Against this backdrop, Williams endorsed holding rates at current levels. “Maintaining this modestly restrictive stance of monetary policy is entirely appropriate,” he said, suggesting the Fed is in no rush to cut despite cooling growth.

Fed’s Bostic: Price pressures are real

Atlanta Fed President Raphael Bostic warned that rising inflation linked to import tariffs may delay any rate cuts. Speaking to Fox Business, Bostic acknowledged the uncertainty created by Trump’s trade actions. He added that increasing price pressures is now visible across the Southeast. “The price pressures are real,” he said, citing business feedback and internal surveys.

Bostic suggested the June CPI report, which showed broad-based increases in prices—particularly for heavily imported goods—may mark an "inflection point". He highlighted that headline inflation moved further away from the Fed’s 2% target. “We've seen the highest increase in prices that we've seen all year,” he added. That backdrop, he argued, warrants caution.

When pressed about the possibility of no rate cut until 2026, Bostic didn’t rule it out. “Everything is on the table,” he said, stressing that the path of policy will depend entirely on how inflation evolves. “If prices continue to move steadily away from our target, then we’ll have to consider what policy response is appropriate.”

Fed Beige Book: Inflation to rise more rapidly by late summer

The Fed’s latest Beige Book reported a slight pickup in US economic activity from late May through early July, a modest improvement over the previous edition. Five districts saw slight or modest growth, while five were flat and two reported declines.

However, businesses remain wary, with uncertainty still elevated and the overall outlook described as “neutral to slightly pessimistic.” Only two districts expected any pickup in activity moving forward. Labor conditions remained cautious, with only a very slight increase in employment and modest wage growth.

Price pressures continued to build, described as moderate to modest across districts. Input costs tied to tariffs—particularly in manufacturing and construction—were widely cited, with most businesses facing “modest to pronounced” cost pressures.

A growing number of firms are beginning to pass these higher costs to consumers via price hikes or surcharges. Others, constrained by customer price sensitivity, have opted to absorb the increases, compressing margins. With broad expectations for continued cost pressure in the coming months, the Fed noted that "consumer prices will start to rise more rapidly by late summer".

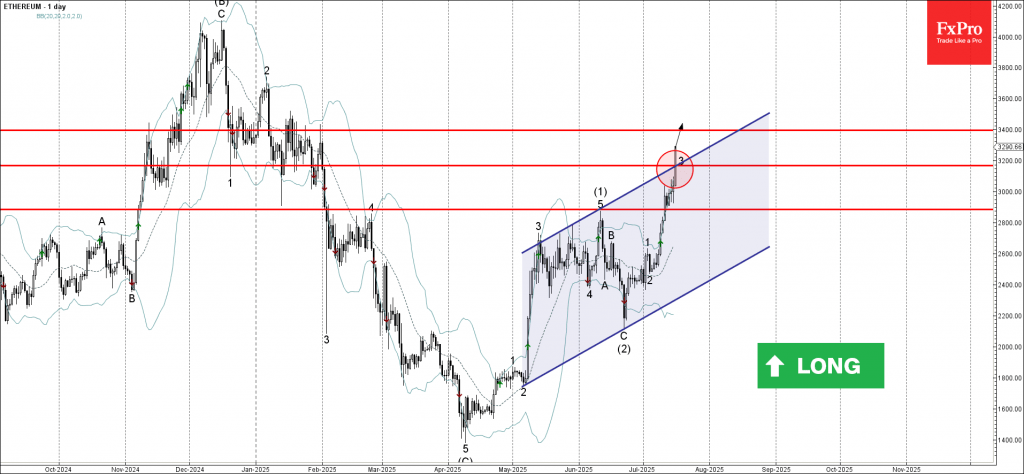

Ethereum Wave Analysis

Ethereum: ⬆️ Buy

- Ethereum broke resistance area

- Likely to rise to resistance level 3400.00

Ethereum cryptocurrency recently broke the resistance area located at the intersection of the resistance level 3200.00 and the resistance trendline of the daily up channel from May.

The breakout of this resistance area should accelerate both of the active impulse waves 3 and (3).

Given the clear daily uptrend, Ethereum cryptocurrency can be expected to rise to the next resistance level 3400.00 (which reversed Ethereum multiple times in January).

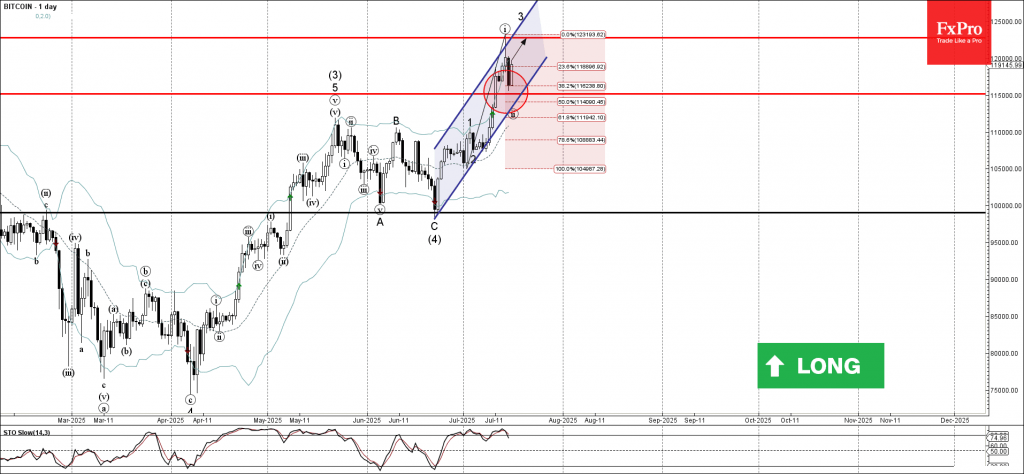

Bitcoin Wave Analysis

Bitcoin: ⬆️ Buy

- Bitcoin reversed from a support area

- Likely to rise to resistance level 122770.00

Bitcoin cryptocurrency recently reversed up from the support area located between the key support level 115000.00 and the support trendline of the daily up channel from June.

This support area was further strengthened by the 38.2% Fibonacci correction of the sharp upward impulse from July.

Given the clear daily uptrend and the strongly bullish sentiment seen across cryptocurrency markets today, Bitcoin cryptocurrency can be expected to rise to the next resistance level 122770.00 (top of the previous impulse wave i).

Better Than Expected PPI and More Turmoil in the Middle East

Some of yesterday's move in the Dollar Index has been undone by some heavy USD selling after Israel attacked Syria amid some rising tensions between Druze-Militias and the Syrian Government Forces.

It seems that a ceasefire has currently been reached, calmying the tensions – This is however a story to follow for the upcoming days.

US Producer Price Index data had been released just before the intensification of the Middle East turmoil and had previously led to some more USD buying – The report was pretty positive as PPI came out unchanged vs a revised + 0.3% release from last month and a 0.2% rise expected.

FED Chair Jerome Powell is also speaking right now for those interested.

A bizarre reaction from the US Dollar at the attacks

Dollar Index 30m Chart – July 16, 2025 – Source: TradingView

Observe the consecutive reactions after the PPI release and the Middle East Headlines –The US Dollar finishes the session down 0.35% after hitting new highs of 98.90 (right now 98.29)

After marking its top, the huge selling candle touched 97.71, down at one point 1.15% before reverting higher.

Other markets cared much less about the headlines, particularly US Indices which have all risen today even after some heavy flash selling – The Dow actually felt the most relief, up 0.53% on the session

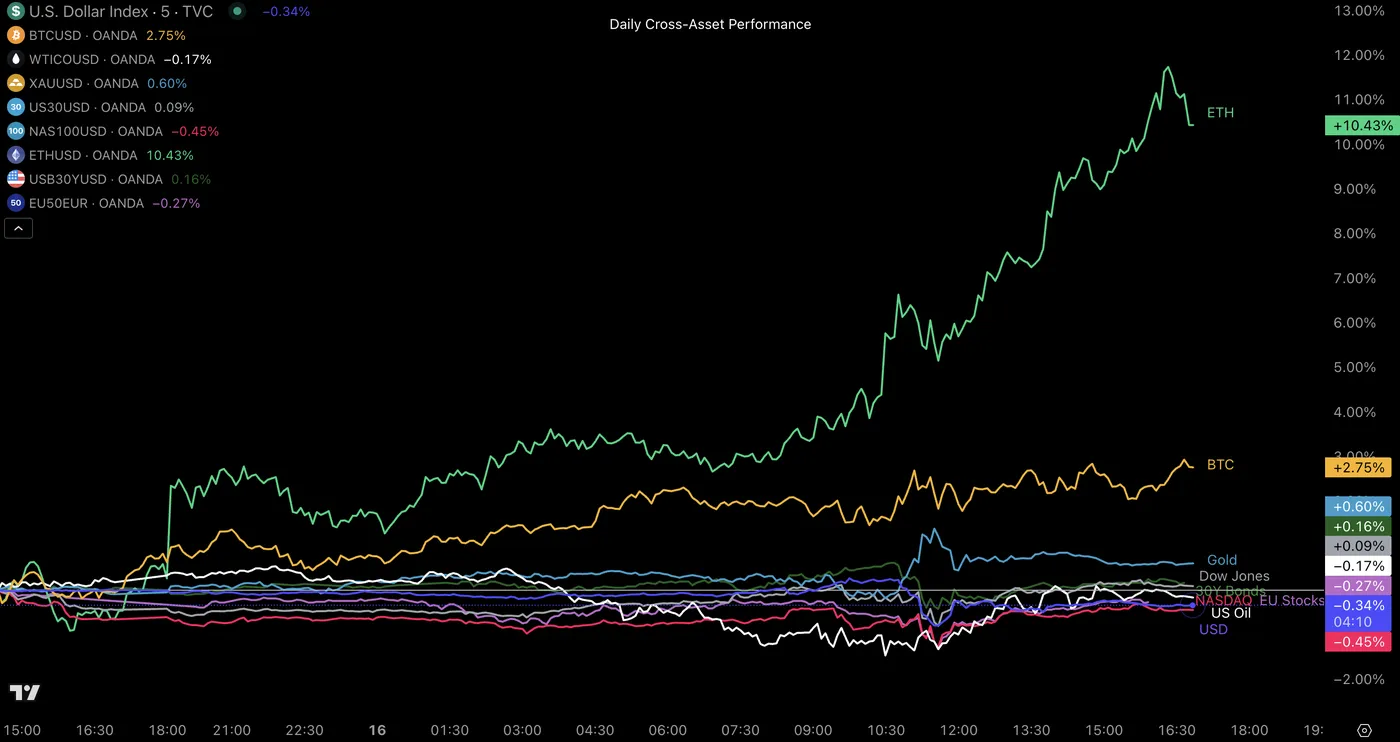

Daily Cross-Asset performance

Cross-Asset Daily Performance, July 16, 2025 – Source: TradingView

The story repeats, and Ethereum is again the best performer of the day, up close to 12% at one point – It's closing the session still up around 11%, touching highs of $3,425.

You can check our latest Ethereum in-depth analysis here.

Apart from that Equities rose after a volatile session due to the factors mentioned in the intro and the USD is actually the worst performer of the session.

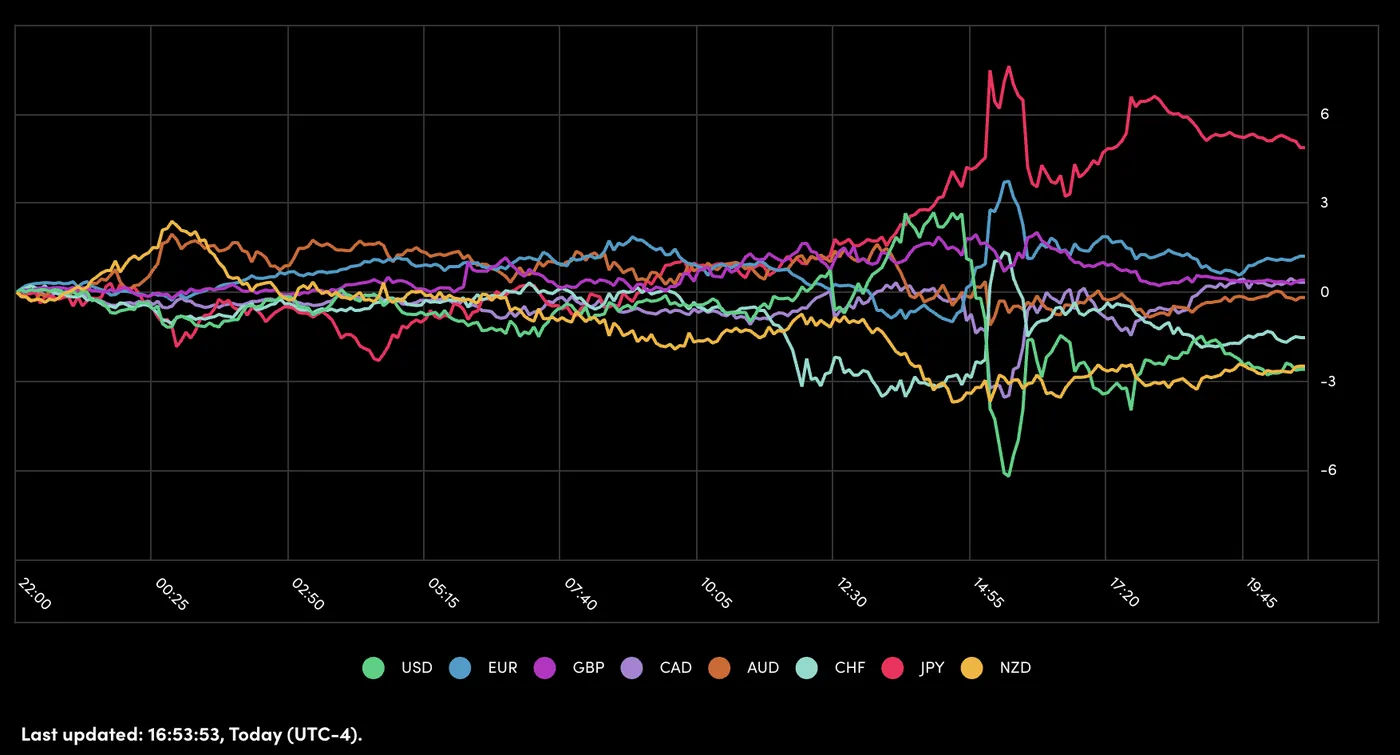

A picture of today's performance for major currencies

Currency Performance, July 16 – Source: OANDA Labs

The Yen is the winner of the session seeing some major risk-off flows towards it after the Middle East attacks as markets went towards the most "value" risk-off currency, particularly as Technical tops (in USDJPY) were right around.

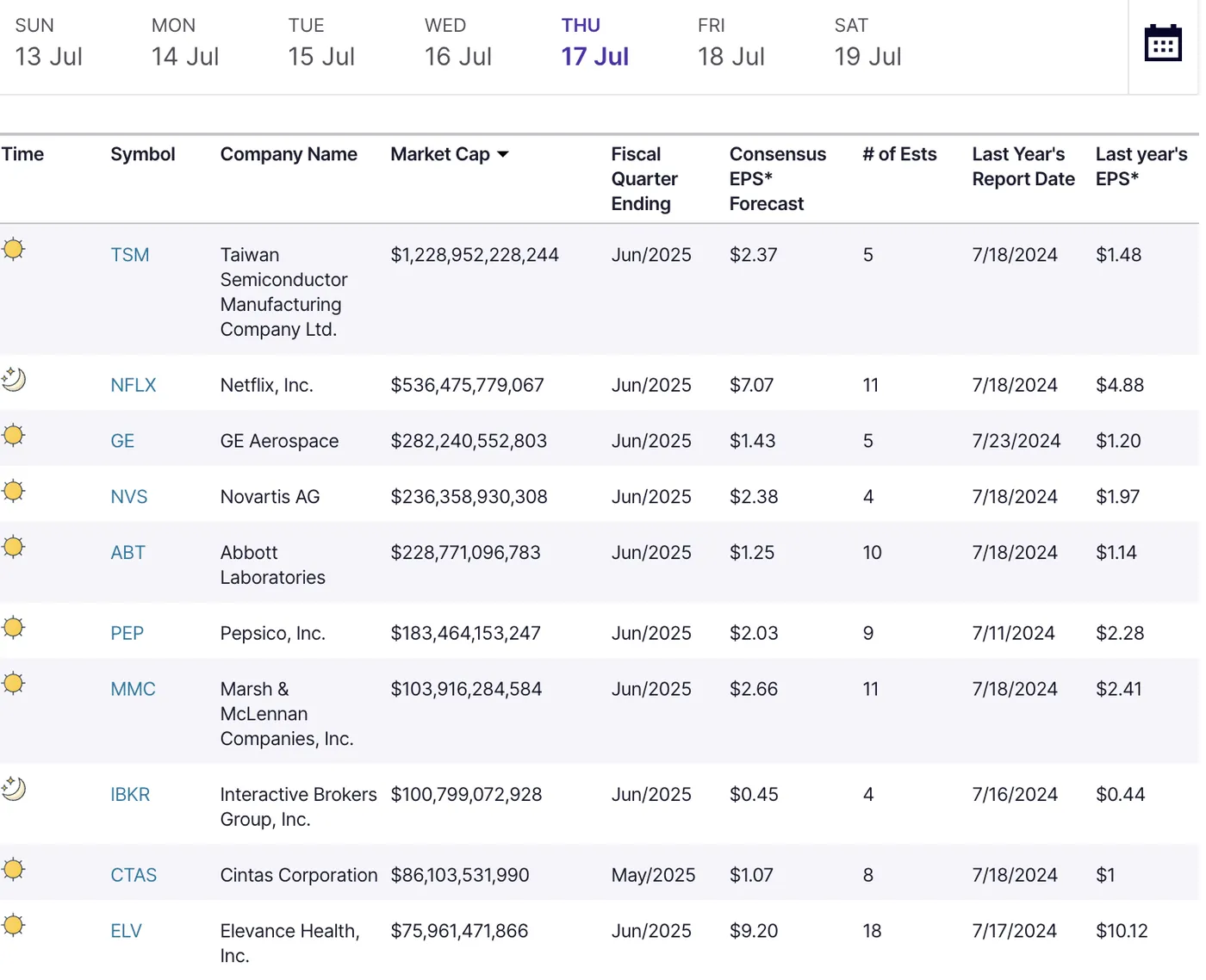

Earnings Season: Who is releasing their numbers tomorrow?

Earnings Calendar for July 17th – Source: Nasdaq.com

Expect earnings from the TSM (Taiwan Semiconductor Manufacturing Company), Netflix, Abbott and Pepsico.

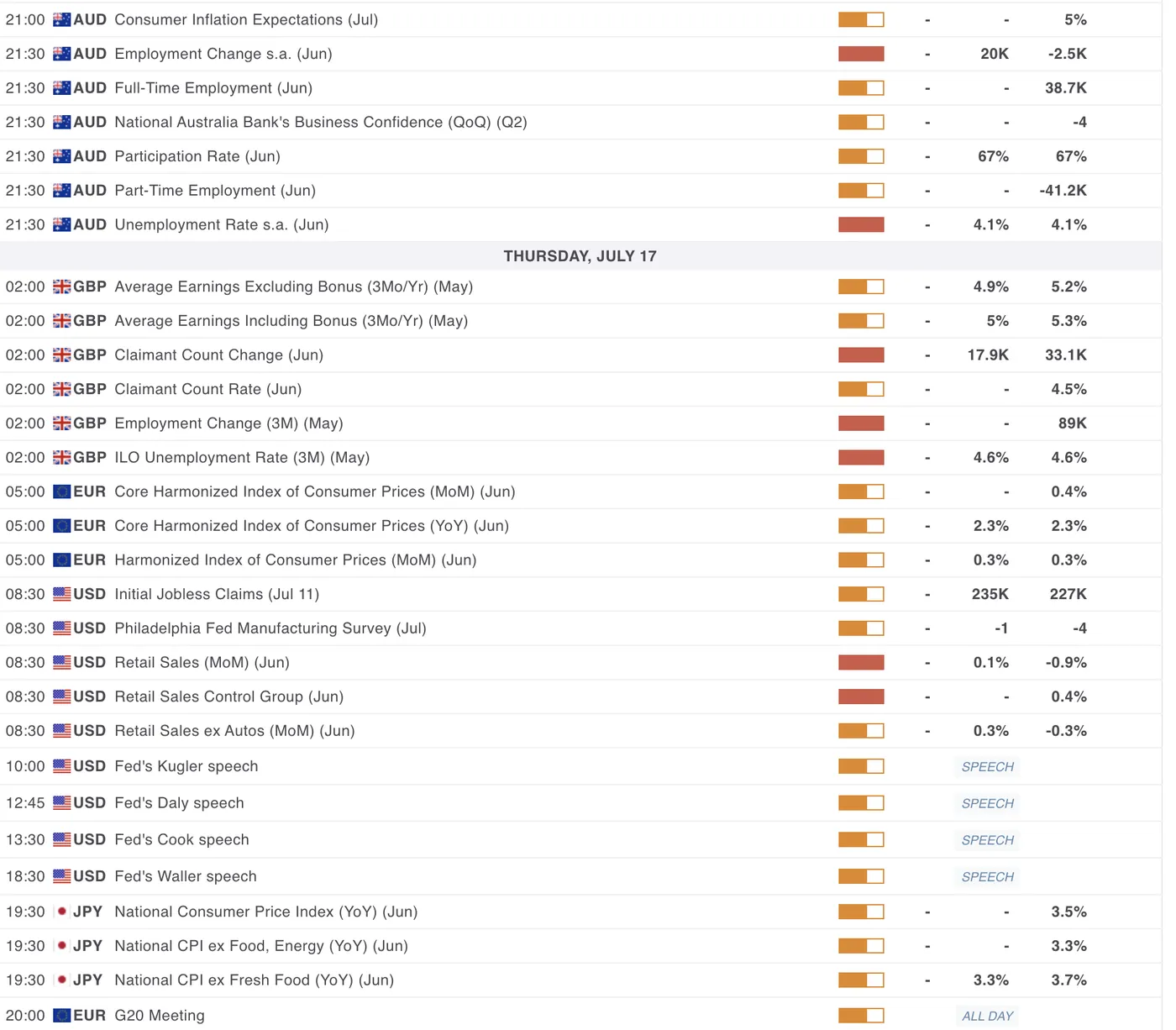

A look at Economic Data releasing in the overnight and upcoming Session

For all Market moving events, check the MarketPulse Economic Calendar

The overnight session is not finished for AUD Traders as some data is expcted at 21:00 ET (Inflation Expectations) and even bigger data right after at 21:30 ET in Australian Employment.

The UK will also see its own Employment Data overnight at 2:00 A.M. ET – Check out the MarketPulse Calendar (select UK if needed) to spot the expectations for the key data for the GBP.

The North-American Session should be dynamic between the Retail Sales and might also be shaken by an army of FED Speakers .

It's always good to check out what the FED has to say around this time of the cycle as despite just providing more ideas on Cuts and Hikes, you can also observe how they envision the impact of tariffs (They're fairly good economists I would say).

And for JPY Traders, don't forget the Monthly CPI report which may add just more volatility to USDJPY and other Yen focused pairs – Any major beat should trigger some anticipated reactions from the Bank of Japan.

Safe Trades!

Dollar dives as Trump reportedly set to fire Fed Powell imminently

Quick update: Trump was swift in denying the news. “We’re not planning on doing it,” he said. “It’s highly unlikely.”

Dollar reversed earlier gains and fell sharply after reports emerged that US President Donald Trump is preparing to fire Fed Chair Jerome Powell "very soon". The move would spark a dramatic clash over the independence of the central bank, with immediate market implications.

Trump reportedly asked a group of House Republicans on Tuesday whether he should fire Powell, drawing vocal approval. Rep. Anna Paulina Luna later posted on X that she was “99% sure firing is imminent.”

Dollar had traded firmer earlier in the day but quickly reversed course as markets digested the political shockwave. Investors are now pricing in elevated institutional risk and potential disruption to monetary policy continuity. While Powell was originally appointed by Trump in 2017, the president has since turned sharply critical of the Fed’s slow approach to rate cuts during his second administration.

Any dismissal of Powell would almost certainly trigger a legal showdown. The Supreme Court recently signaled that Trump cannot automatically extend his authority to remove the Fed chair, given the central bank’s unique semi-private governance structure. Still, the mere threat of such a move is enough to inject fresh volatility into markets already wary of political interference.

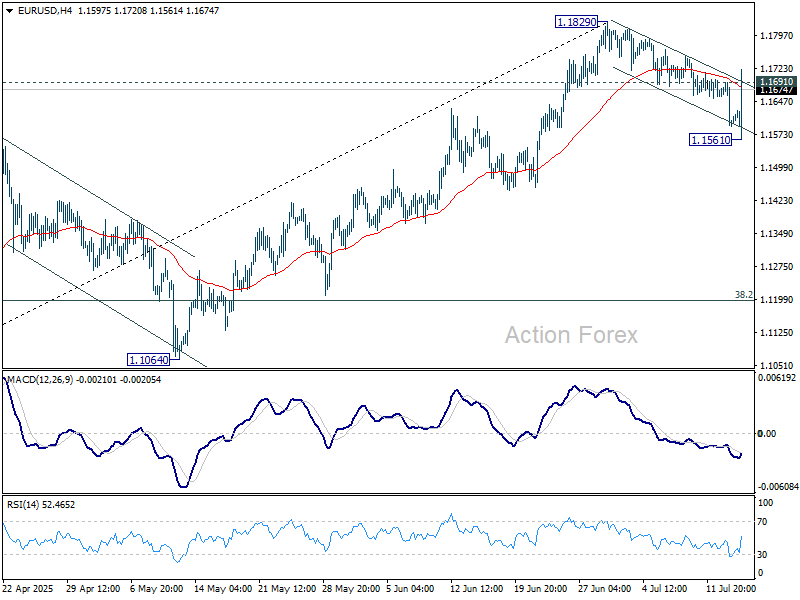

Techncially, EUR/USD's strong rebound and break of 1.1691 minor resistance suggests that a temporary low was formed at 1.1561. For now, it's still early to decide if the whole corrective pattern from 1.1829 has completed. Nevertheless, firm break of 1.1829 will confirm larger rally resumption. Meanwhile, break of 1.1561 will extend the correction.