Sample Category Title

Dovish Comments by Fed Governor Waller Grab Attention

Markets

The latest batch of US eco data and the absence of destabilizing headlines from the US president helped the S&P 500 (+0.54%) and Nasdaq (+0.75%) to new all-time closing highs. The dollar extended the July comeback with the trade-weighted dollar (DXY) ending the day 98.73 from 98.35. The greenback managed to record daily gains on all but one trading day so far this month, but we must add that the cumulative increase remains limited so far to only 1.7% which compares with a >10% loss in H1 2025. EUR/USD closed at 1.1596 from a start at 1.1641. First technical support only arrives around 1.1461/31 (mid-June low & 24% retracement on this year’s rally). Daily changes on the US yield curve were limited between +1.2 bps (2-yr) and -0.4 bps (30-yr). This hides intraday volatility around the release of solid (and consensus-beating) June US retail sales (+0.6% M/M headline; +0.5% M/M control group), lower-than-expected weekly jobless claims (221k from 228k) and a surge in July Philly Fed business outlook to the best level since February. New orders, shipments and employment all moved back into expansion territory, but price pressures increased as well (expected prices paid highest since January 2022). US Treasuries initially sold off on the data, but the move didn’t went far.

Dovish comments by Fed governor Waller grab attention this morning. They gently lift US Treasuries while weighing somewhat on the dollar. He repeats his call that it would make sense to lower the policy rate by 25 bps as soon as this month’s FOMC meeting. “With inflation near target and the upside risks to inflation limited, we should not wait until the labor market deteriorates before we cut the policy rate. The economy is still growing, but its momentum has slowed significantly and the risks to the FOMC’s employment mandate have increased.” Waller expects growth to remain soft for the rest of 2025. Together with Fed Bowman, Waller is the only one to back a July rate cut with the vast majority of the FOMC supporting Powell’s view to assess the summer inflation prints before drawing firm conclusions on the inflationary impact of Trump’s protectionist trade policy. SF Fed Daly nevertheless warned that you can’t wait forever (with making monetary policy less restrictive), because if you wait until inflation is 2% you risk injuring the economy in a way that was completely unnecessary. Daly still sees a path to two (25 bps) rate cuts this year. Recent Fed comments suggest that the September FOMC meeting might be a confrontational one between doves and hawks. Today’s US eco calendar contains housing data and July consumer confidence from the University of Michigan survey. Markets will be looking for more moderation in 1y (5% in June) and 5-10y (4%) inflation expectations. Overall, we expect this week’s trends on major markets to persist (friendly risk sentiment; breathing space for USD; truce in long term core bonds).

News & Views

National Japanese inflation excluding volatile fresh food prices, slowed in June to 0.1% M/M and 3.3% Y/Y from 0.5% M/M and 3.7% Y/Y in May. A measure excluding fresh food and energy prices, rose further by 0.4% M/M and 3.4% Y/Y from 3.3% in May. Both indices hold well above the Bank of Japan’s 2% target. A decline in energy/utility prices was behind the decline in core inflation. Services inflation accelerated to 0.3% M/M and 1.5% from (1.4%). Goods price inflation slowed to -0.1% M/M and 4.8% Y/Y (from 5.3%). A rise in underlying, cost-driven prices keeps the debate open on the timing of further BoJ policy normalization even as the potential negative impact of trade tensions recently put the central bank in a wait-and-see modus. Markets are very cautious in discounting further policy tightening (60% probability of 25 bps rate hike by year-end). The yen this morning underperforms but this probably mirrors investor caution going into this weekend’s Upper House elections. (USD/JPY 148.75).

Reuters reports that the Bank of England asked some lenders to test their resilience to potential US dollar shocks. The central bank was said to have requested that some lenders assess their dollar funding plans and the degree to which they depend on the US currency, including for short term needs. Amongst others, a bank reportedly was asked to run internal stress tests including scenarios where the USD swap market could dry up entirely. In the background the question swirls whether entities outside the US still can rely on Fed USD swap facilities in case of a shortage of US liquidity.

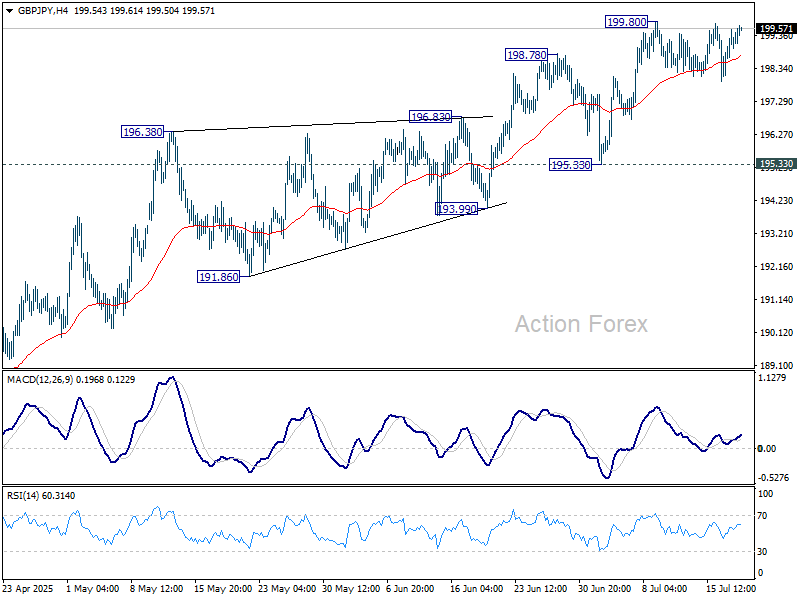

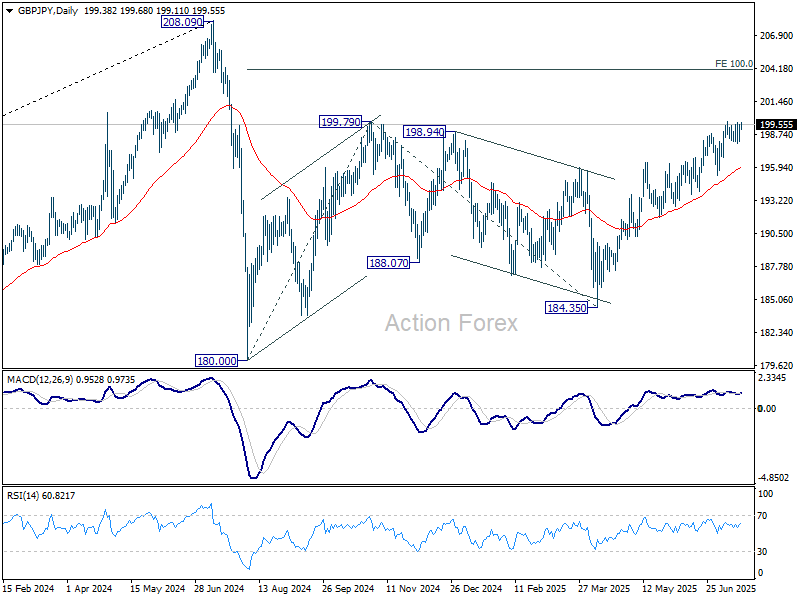

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.57; (P) 199.06; (R1) 199.90; More...

GBP/JPY is staying in consolidations below 199.80 and intraday bias remains neutral. While deeper retreat cannot be ruled out, further rise is expected as long as 195.33 support holds. On the upside, break of 199.80 will resume the rally from 184.35 and target 100% projection of 180.00 to 199.79 from 184.35 at 204.14.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

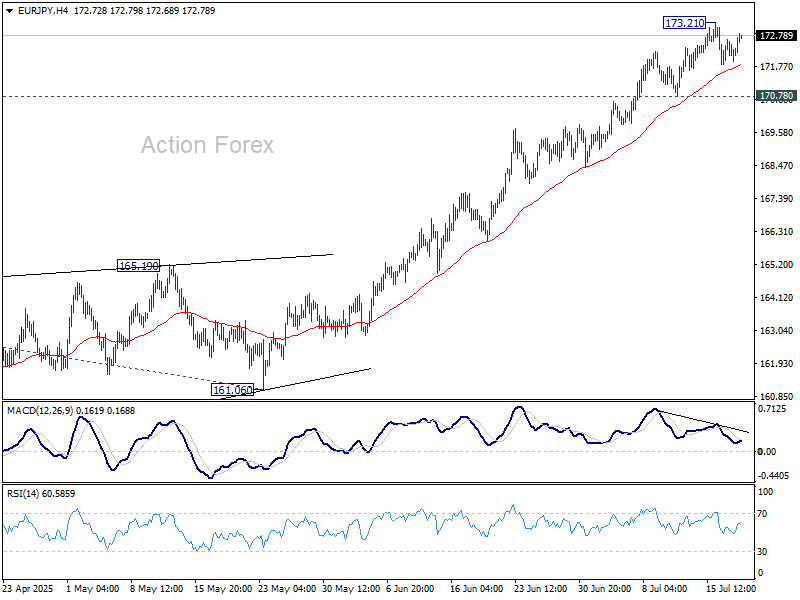

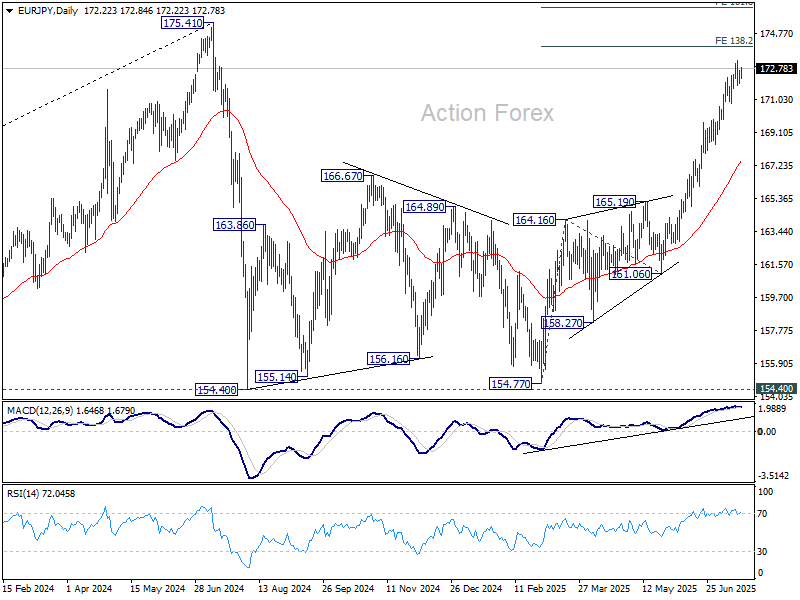

EUR/JPY Daily Outlook

Daily Pivots: (S1) 171.93; (P) 172.30; (R1) 172.75; More...

EUR/JPY's consolidations from 173.21 is in progress and intraday bias remains neutral. Further rally is expected as long as 170.78 support holds. Above 173.21 will resume the rise from 154.77 to 138.2% projection of 154.77 to 164.16 from 161.06 at 174.03.

In the bigger picture, price actions from 175.41 (2024 high) are seen as correction to up trend from 114.42 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. Meanwhile, decisive break of 175.41 will confirm long term up trend resumption.

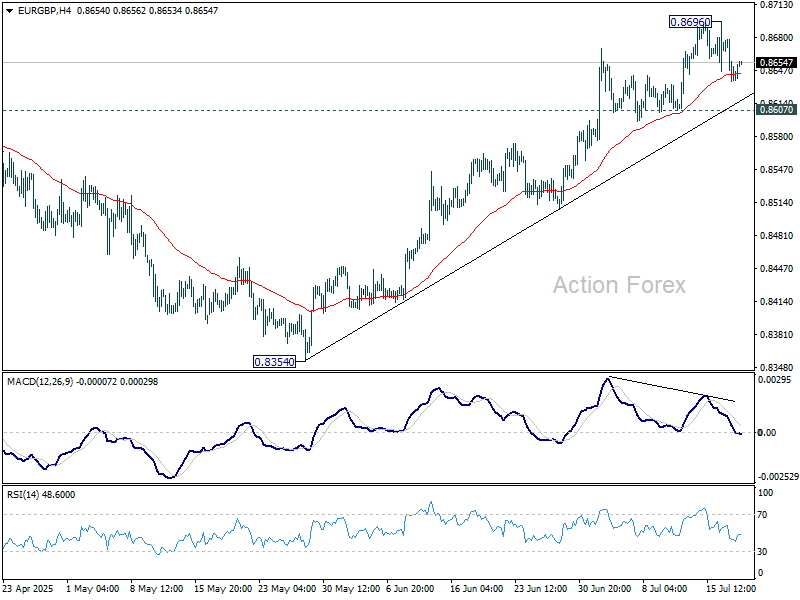

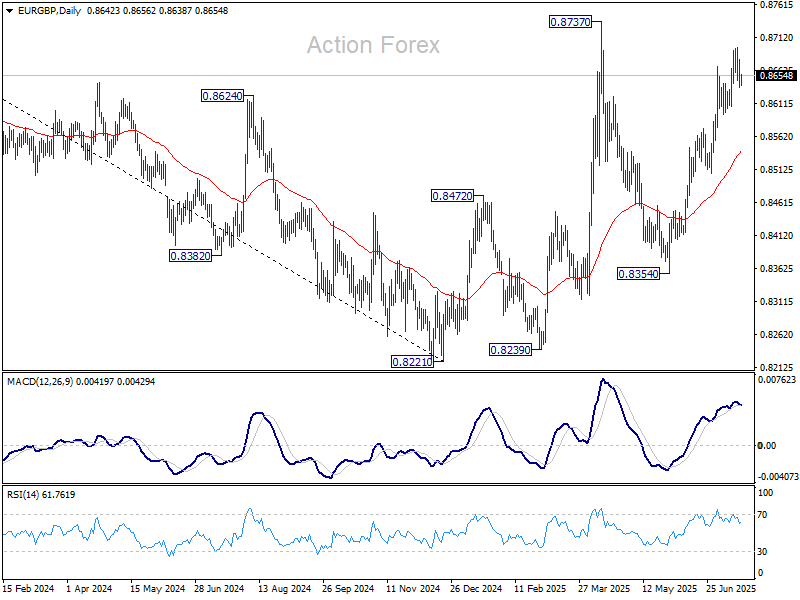

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8626; (P) 0.8654; (R1) 0.8672; More...

EUR/GBP is staying in consolidations below 0.8695 and intraday bias remains neutral. Further rise is expected as long as 0.8607 support holds. Above 0.8695 will target 0.8737 high. Decisive break there will resume the whole rise from 0.8221 low, and target 0.8867 fibonacci level. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 0.8607 will argue that rebound from 0.8354 has completed, and turn bias back to the downside for 55 D EMA (now at 0.8541).

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it's reversing the down trend from 0.9267 (2022 high). But even if it's a correction, firm break of 0.8737 will still pave the way to 61.8% retracement of 0.9267 to 0.8221 at 0.8867.

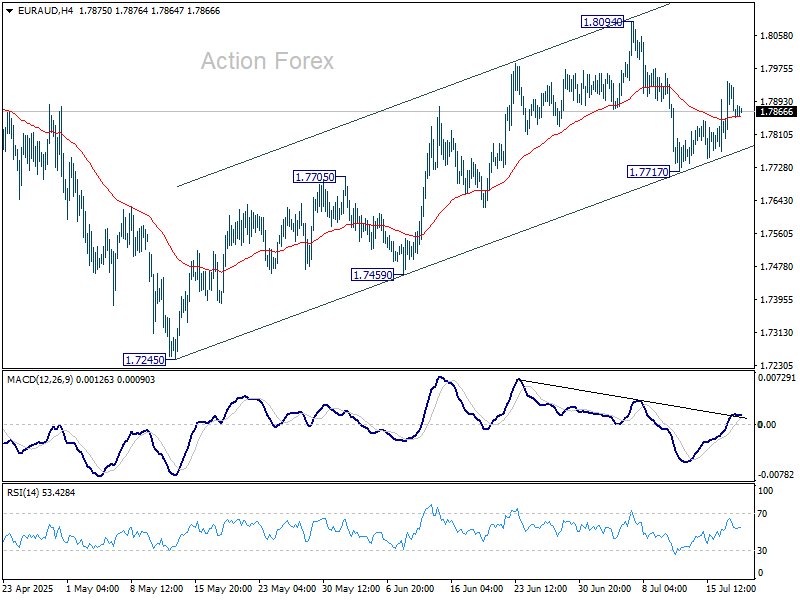

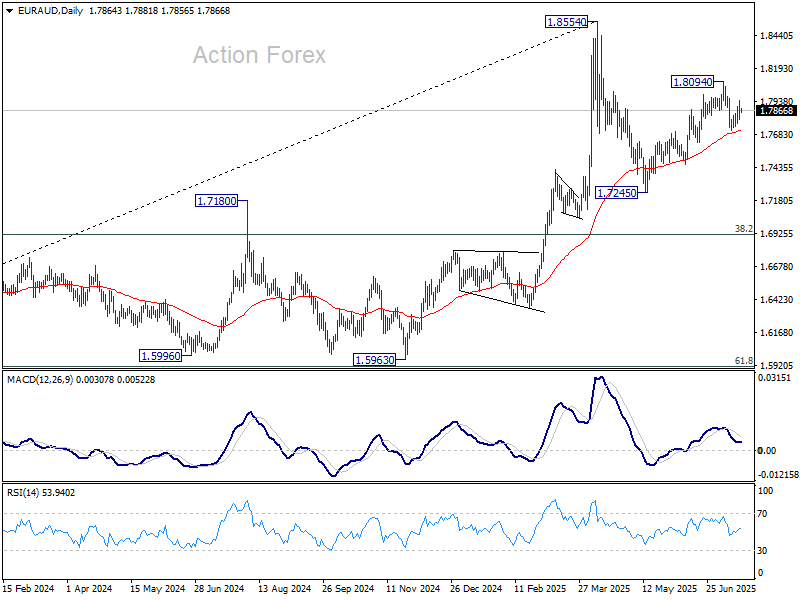

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7812; (P) 1.7880; (R1) 1.7944; More...

Intraday bias in EUR/AUD remains mildly on the upside for 1.8094. Firm break there will resume the rise from 1.7245 to retest 1.8554 high. Nevertheless, break of 1.7717 support will revive the case that rise from 1.7245 has completed, and turn bias back to the downside for 1.7459 support instead.

In the bigger picture, price actions from 1.8554 medium term are seen as a corrective pattern. While deeper pullback might be seen, downside should be contained by 38.2% retracement of 1.4281 (2022 low) to 1.8554 at 1.6922 to bring rebound. Up trend from 1.4281 is expected to resume at a later stage.

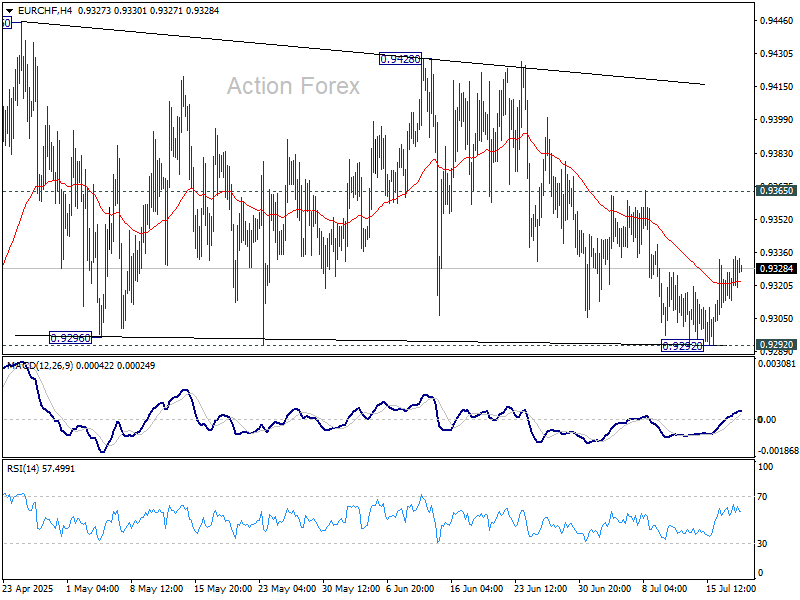

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9317; (P) 0.9327; (R1) 0.9338; More....

Intraday bias in EUR/CHF stays neutral at this point. On the upside, break of 0.9365 resistance will suggest that fall from 0.9428 has completed. Further rally should be seen to retest 0.9428/45 resistance zone. Firm break there will resume the rebound from 0.9218. On the downside, firm break of 0.9292 support will bring retest of 0.9218 low instead.

In the bigger picture, while downside momentum has been diminishing as seen in W MACD, there is no sign of bottoming yet. EUR/CHF is still staying below 55 W EMA (now at 0.9437) and well inside long term falling channel. Outlook will stay bearish as long as 0.9660 resistance holds. Break of 0.9204 (2024 low) will confirm resumption of down trend from 1.2004 (2018 high).

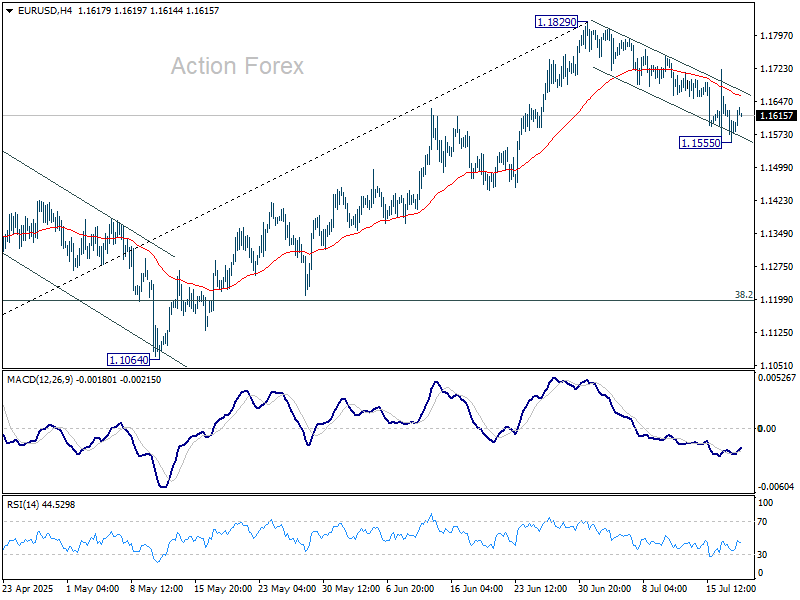

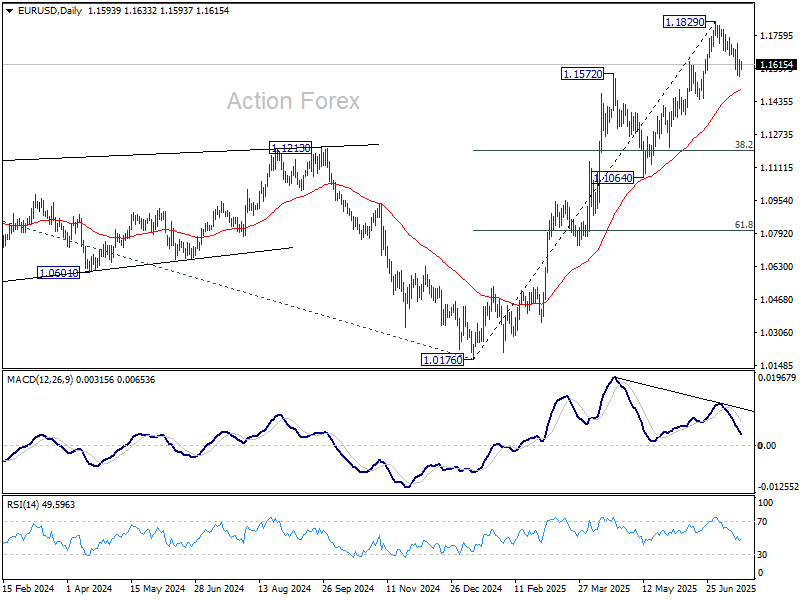

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1555; (P) 1.1600; (R1) 1.1642; More...

Intraday bias in EUR/USD remains neutral at this point. Risk will stay mildly on the downside as long as 1.1829 resistance holds. Fall from there is correcting the rise from 1.1829 or whole rally from 1.0176. Below 1.1555 will target 55 D EMA (now at 1.1493). Sustained break there will target 38.2% retracement of 1.0176 to 1.1829 at 1.1198.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will remain the favored case as long as 1.1604 support holds.

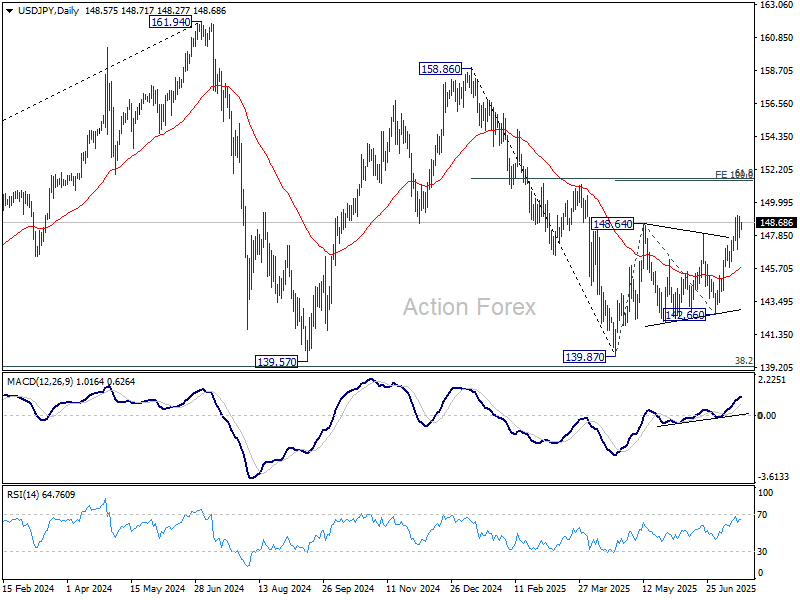

USD/JPY Daily Outlook

Daily Pivots: (S1) 147.86; (P) 148.48; (R1) 149.22; More...

Intraday bias in USD/JPY remains neutral for the moment. More consolidations could be seen below 149.17. Downside should be contained by 55 D EMA (now at 145.77). Break of 149.17 will resume the whole rise from 139.87 to 100% projection of 139.87 to 148.64 from 142.66 at 151.43. That is close to 61.8% retracement of 158.86 to 139.87 at 151.22.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3379; (P) 1.3411; (R1) 1.3447; More...

Intraday bias in GBP/USD remains neutral for the momentum. Focus stays on on 1.3369 support. Decisive break there will suggests that fall from 1.3787 is already correcting the rise from 1.2099. Deeper fall should then be seen to 1.3138 cluster support (38.2% retracement of 1.2099 to 1.3787 at 1.3142). Nevertheless, strong rebound from current level will retain near term bullishness. Break of 1.3561 support turned resistance will bring retest of 1.3787 high first.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.3019) holds, even in case of deep pullback.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8011; (P) 0.8037; (R1) 0.8071; More….

Intraday bias in USD/CHF remains neutral at this point. Focus stays on 0.8054 support turned resistance. Decisive break there will suggest that rise from 0.7871 at least correcting the fall from 0.8475. Further rise should then be seen to 55 D EMA (now at 0.8146). Nevertheless, rejection by 0.8054 will retain near term bearishness. Below 0.7946 minor support will bring retest of 0.7871 low.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.