Sample Category Title

EUR/USD Bounce Runs Into Trouble As Resistance Strikes Back

Key Highlights

- EUR/USD started a recovery wave and tested the 1.1675 resistance.

- An expanding triangle is forming with resistance at 1.1675 on the 4-hour chart.

- GBP/USD is still struggling to clear the 1.3550 resistance zone.

- Gold could start a fresh decline unless it closes above $4,600.

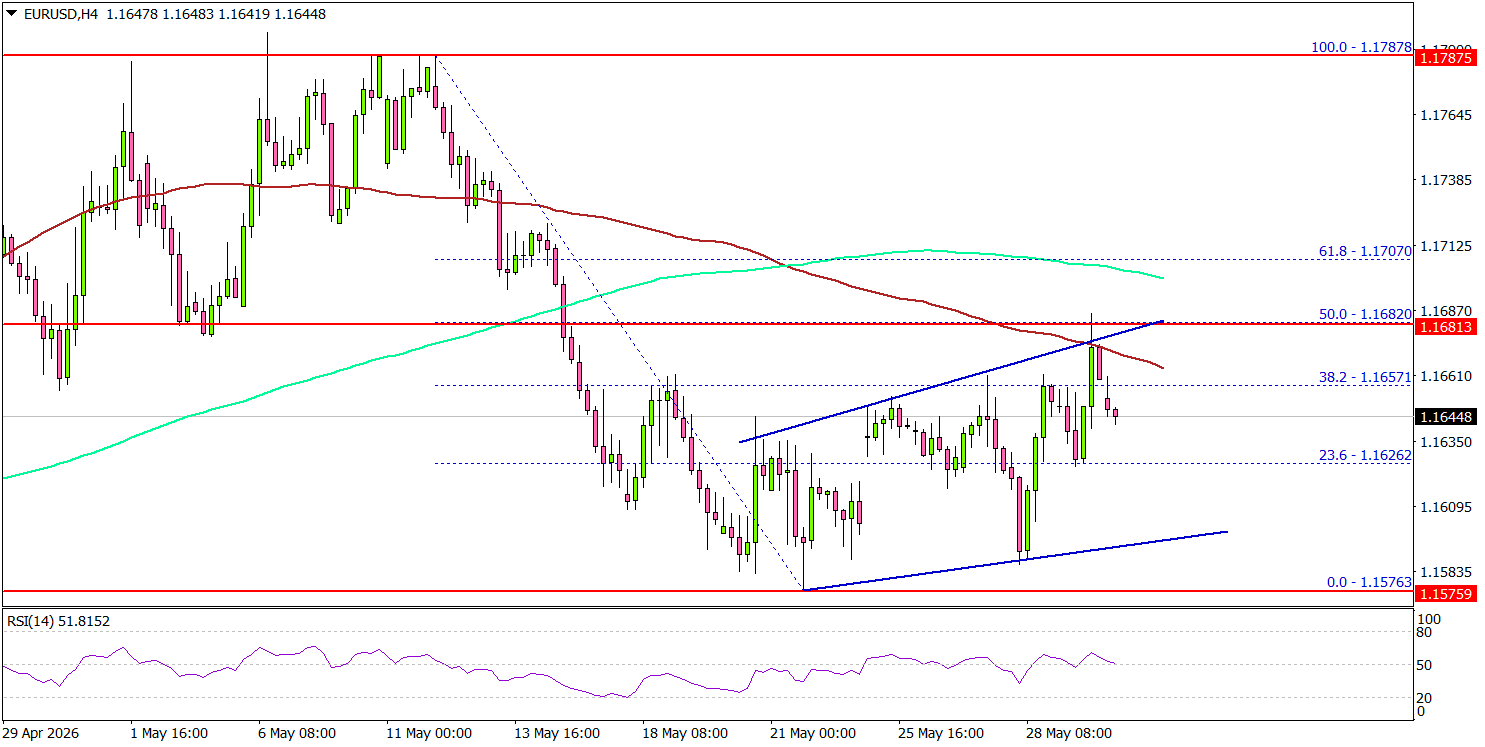

EUR/USD Technical Analysis

The Euro found support at 1.1575 against the US Dollar. EUR/USD started a recovery wave above 1.1600 and 1.1620, but it faces many hurdles.

Looking at the 4-hour chart, the pair climbed above the 38.2% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1576 low. However, the bears seem to be active near the key hurdle at 1.1675.

There is also an expanding triangle forming with resistance at 1.1675. It coincides with the 50% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1576 low.

The pair is now trading below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). To continue higher, it must settle above 1.1675.

The next major resistance could be 1.1700. A close above 1.1700 could open doors for gains above 1.1750. In the stated case, the bulls could aim for a move to 1.1800.

On the downside, the pair could find bids near 1.1620. The first major support might be 1.1600. A close below 1.1600 might initiate a drop to 1.1550. Any more losses might open the doors for a drop toward the 1.1420 zone.

Looking at GBP/USD, the pair is attempting to recover some losses, but it faces a major hurdle near the 1.3550 region.

Upcoming Key Economic Events:

- US ISM Non-Manufacturing Index for May 2026 – Forecast 52.6, versus 52.7 previous

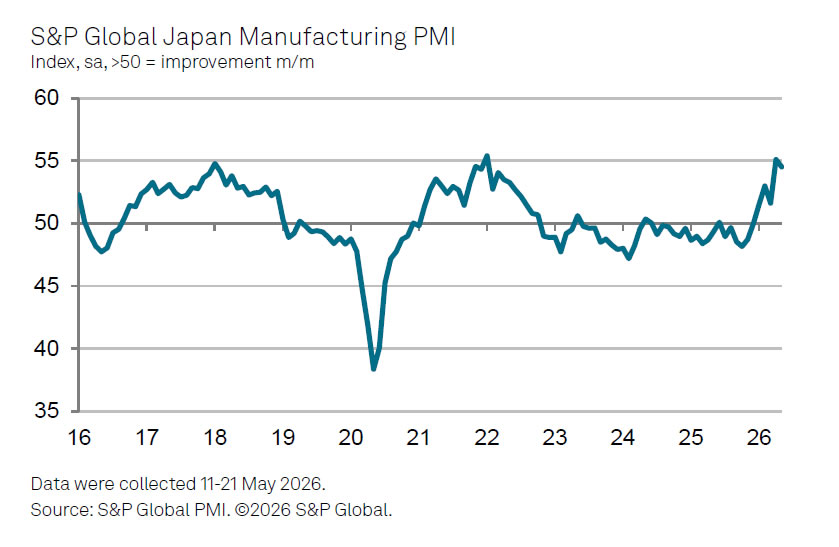

Japan Manufacturing PMI Finalized at 54.1, Strong Growth Despite Rising Cost Pressures

Japan's manufacturing sector delivered another strong performance in May, with PMI Manufacturing finalized at 54.4, slightly down from April's 55.1. The latest reading signaled a fifth straight month of improving business conditions as both output and new orders expanded at historically strong rates. The data suggest Japanese manufacturers continue to benefit from resilient demand, particularly in technology-related industries linked to ongoing investment in AI and electronics.

Yet the survey also revealed that some of the recent strength may be temporary. Firms reported increasing inventories across supply chains as manufacturers and customers sought to guard against potential disruptions and rising costs stemming from the Middle East conflict. This precautionary stockpiling helped lift production but may also have brought forward some demand that would otherwise have occurred later in the year.

The survey painted a more cautious picture beneath the headline strength. Input costs and selling prices surged, with both inflation gauges reaching levels rarely observed since data collection began more than two decades ago. Meanwhile, confidence about future output improved only slightly from April's recent low. While manufacturers remain optimistic that technology investment will continue to support activity, elevated costs and sluggish global demand are emerging as key risks to Japan's manufacturing outlook.

| Indicator | Previous | Latest |

|---|---|---|

| PMI Manufacturing | 55.1 | 54.4 |

| Manufacturing Conditions | Improving | Improving |

| Output | Expansion | Strong Expansion |

| New Orders | Expansion | Strong Expansion |

| Inventory Building | Elevated | Elevated |

| Input Prices | High | Near Record High |

| Output Prices | High | Near Record High |

| Future Output Sentiment | Recent Low | Slightly Improved |

China PMIs Signal Slower Growth as Export Demand Weakens

China's latest PMI surveys suggest the economy navigated the second quarter with a growing split between domestic and external demand. Manufacturing activity slowed in May while services improved, indicating that consumer spending at home is helping offset mounting pressure from weaker overseas markets. The data reinforce signs from April activity indicators that growth momentum has cooled despite earlier resilience in exports.

NBS PMI Manufacturing fell from 50.3 to 50.0, the weakest reading in three months. While production remained solid at 51.2, new orders slipped from expansion into contraction at 49.9. The sharpest deterioration came from foreign demand, with new export orders falling from 50.3 to 48.6.

Consumer goods producers experienced particularly pronounced weakness, underscoring the challenges facing Chinese exporters as global demand softens.

In contrast, NBS PMI Non-Manufacturing rose from 49.4 to 50.1, helped by strong travel spending during the May Day holiday period, while the services component climbed to a nine-month high of 50.3.

The private RatingDog PMI Manufacturing survey echoed the official findings. The index eased from 52.2 to 51.8 as growth in production and new orders moderated. Firms benefited from slightly easing inflation pressures, but export demand weakened noticeably. New export orders contracted for the first time in five months, providing an early signal that higher energy prices and slower global demand are beginning to affect overseas sales.

| Indicator | Previous | Latest |

|---|---|---|

| NBS PMI Manufacturing | 50.3 | 50.0 |

| Production Sub-Index | 51.2 | |

| New Orders Sub-Index | 49.9 | |

| New Export Orders | 50.3 | 48.6 |

| NBS PMI Non-Manufacturing | 49.4 | 50.1 |

| NBS Services Activity | N/A | 50.3 |

| RatingDog PMI Manufacturing | 52.2 | 51.8 |

| Production (RatingDog) | Expansion | Expansion |

| New Orders (RatingDog) | Expansion | Expansion |

| New Export Orders (RatingDog) | Expansion | Contraction |

| Inflation Pressures | Elevated | Eased |

U.S.-Iran Talks, BoJ Intervention Risk, and Jobs Data in Focus

The shorter trading week, due to U.K. and U.S. holidays, had no major economic releases, but the data that did come out was mixed. U.S. GDP was weaker than expected, while durable goods orders were stronger than forecast.

Recent market trends continued. U.S. and Japanese equities moved higher, while USD/JPY tested higher levels as the Bank of Japan stayed on the sidelines and did not intervene. Optimism around reports that the U.S. and Iran were moving toward a 60-day ceasefire extension, along with a possible reopening of traffic through the Strait of Hormuz, helped push oil prices lower and supported risk appetite through much of the week.

U.S.-Iran deal optimism also contributed to a fall in longer-term U.S. interest rates. However, Fed officials remained cautious on inflation. Fed Governor Lisa Cook said she was prepared to raise rates if inflation continued moving in the wrong direction, reminding markets that rate-cut hopes may still be premature.

Markets This Week

U.S. Stocks

The Dow posted another week of gains, and the outlook remains positive for now. There is always a risk of surprise news, but while the current uptrend remains in place, buying near the 10-day moving average remains the preferred strategy. Resistance levels are at 51,200, 51,500 and 52,000. Support is seen at 50,000, 49,500, 49,000, 48,500 and 48,000.

Japanese Stocks

Japanese equities remain popular with investors around the world, with the Nikkei rising 4% last week and now up more than 25% this year. The strong uptrend remains in place, so buying on weakness remains the preferred strategy for both short-term and long-term traders. Resistance is seen at 67,000, 68,000, 69,000 and 70,000, while support is at 64,000, 62,000, 61,000, 60,000 and 59,000.

USD/JPY

Despite the risk of Bank of Japan intervention, traders continued to focus on the large interest rate gap between the U.S. and Japan. Comments from a Fed official about the possibility of rate hikes if inflation stays high also encouraged buying. However, the Bank of Japan still remains likely to support the yen if USD/JPY moves above 160. A selling opportunity could appear if the pair falls below the 10-day moving average and breaks the recent uptrend from the past few weeks. Resistance is at 160.00, 160.50, 162.00 and 165.00, while support is seen at 158.00, 157.00, 156.00, 155.50 and 155.00.

Gold

Gold volatility increased as the market fell below the May lows, encouraging technical selling in the middle of the week. However, a fall in long-term U.S. interest rates, as crude oil moved lower toward the end of the week, helped gold recover and finish the week close to unchanged. The quick rebound was positive, and with long-term U.S. rates falling, gold is more likely to trade sideways to higher this week. Resistance is at $4,600, $4,665, $4,750 and $4,900, while support is at $4,500, $4,450, and $4,350.

Crude Oil

WTI crude oil fell significantly as reports that Washington and Tehran had tentatively agreed to extend a ceasefire reduced fears of supply disruption. The market remained volatile because the deal was not final and still needed approval from President Trump. However, the downward trend is becoming stronger, so selling into strength may be the preferred strategy in the current environment, as long as the Iran situation does not worsen. Resistance is at $95, $100, $105, $110 and $120, while support is at $90, $80, $75, $70, and $67.50.

Bitcoin

Bitcoin selling continued last week as investor interest kept falling. The technical picture also remained bearish, with the 10-day moving average pointing lower and the market breaking below support at $75,000. The downtrend is worth following for now, so selling into strength remains the preferred strategy as long as prices stay below the 10-day moving average. Resistance is at $75,000, $80,000, $85,000, and $90,000, while support is at $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: Japan Capital Spending, E.U. HCOB Eurozone Manufacturing PMI and Unemployment Rate, U.K. S&P Global Manufacturing PMI, U.S. S&P Global Manufacturing PMI and ISM Manufacturing PMI

- Tuesday: Australia Current Account and Building Approvals, E.U. CPI, U.S. JOLTS Job Openings

- Wednesday: Japan S&P Global Services PMI, Australia GDP, E.U. HCOB Eurozone Services PMI, U.K. S&P Global Composite PMI, U.S. ADP Nonfarm Employment Change, S&P Global Services PMI, Factory Orders and Beige Book

- Thursday: Australia Trade Balance, U.K. S&P Global Construction PMI

- Friday: Japan Household Spending, E.U. GDP, U.S. Nonfarm Payrolls

Markets have been quiet recently, but volatility could rise soon. The main focus remains on U.S.-Iran negotiations and whether oil supply could increase. USD/JPY will also stay important, as further yen weakness could raise the risk of Bank of Japan intervention. Traders will also be watching the key U.S. employment data released on Friday.

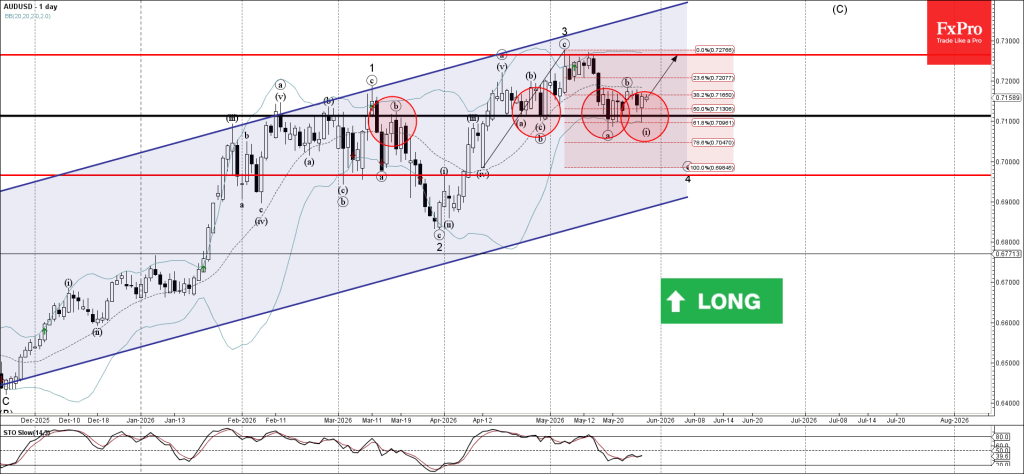

AUDUSD Wave Analysis

AUDUSD: ⬆️ Buy

- AUDUSD reversed from support area

- Likely to rise to resistance level 0.7265

AUDUSD currency pair recently reversed from the support area between the key support level 0.7100 (which has been reversing the price from the end of April), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from April.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Piercing Line.

Given the clear daily uptrend and the bearish US dollar sentiment seen today across the FX markets, AUDUSD currency pair can be expected to rise to the next resistance level 0.7265 (top of the previous impulse wave 3).

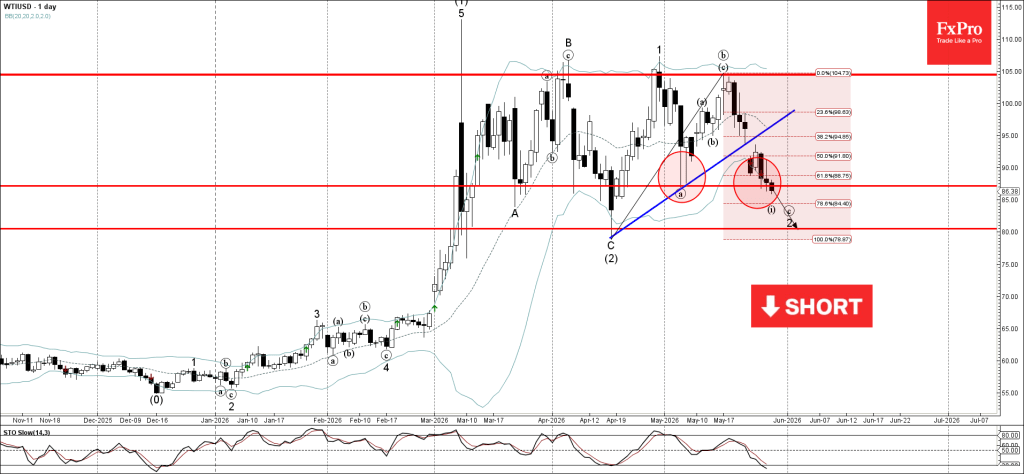

WTI Crude Oil Wave Analysis

WTI crude oil: ⬇️ Sell

- WTI crude broke support area

- Likely to fall to support level 80.00

WTI crude oil recently broke the support area between the support level 87.15 (low of the previous correction a) and the support trendline from the middle of April.

The breakout of this support area accelerated the active impulse wave c – which belongs to the ABC correction from the end of April.

WTI crude oil can be expected to fall to the next round support level 80.00 (low of the previous medium-term ABC correction (2) from April and the forecast price for the completion of the active wave c).

Eco Data 6/1/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 0.00% | 4.10% | 6.50% | |

| 00:30 | JPY | Manufacturing PMI May | 54.5 | 54.5 | 54.5 | |

| 01:00 | AUD | TD-MI Inflation Gauge M/M May | -0.30% | 0.60% | ||

| 01:45 | CNY | RatingDog Manufacturing PMI May | 51.8 | 51.4 | 52.2 | |

| 06:00 | EUR | Germany Retail Sales M/M Apr | -0.30% | -0.40% | -2.00% | -0.30% |

| 06:30 | CHF | Real Retail Sales Y/Y Apr | 1.60% | 0.20% | 0.50% | |

| 07:00 | CHF | GDP Q/Q Q1 | 0.70% | 0.50% | 0.10% | 0.20% |

| 07:30 | CHF | Manufacturing PMI May | 57.3 | 54 | 54.5 | |

| 07:50 | EUR | France Manufacturing PMI May F | 49.7 | 48.9 | 48.9 | |

| 07:55 | EUR | Germany Manufacturing PMI May F | 50.1 | 49.9 | 49.9 | |

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 51.6 | 51.4 | 51.4 | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Apr | 2.70% | 3.30% | 3.20% | |

| 08:30 | GBP | Manufacturing PMI May F | 53.9 | 53.7 | 53.7 | |

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.30% | 6.20% | 6.20% | 6.30% |

| 13:30 | CAD | Manufacturing PMI May | 52.9 | 53.3 | ||

| 13:45 | USD | Manufacturing PMI May F | 55.1 | 55.3 | 55.3 | |

| 14:00 | USD | ISM Manufacturing PMI May | 54.0 | 52.6 | 52.7 | |

| 14:00 | USD | ISM Manufacturing Prices Paid May | 82.1 | 85.3 | 84.6 | |

| 14:00 | USD | ISM Manufacturing Employment Index May | 48.6 | 46.4 | ||

| 14:00 | USD | Construction Spending M/M Apr | 0.40% | 0.30% | 0.60% | 0.20% |

| 23:50 | JPY |

| Capital Spending Q1 | |

| Actual | 0.00% |

| Consensus | 4.10% |

| Previous | 6.50% |

| 00:30 | JPY |

| Manufacturing PMI May | |

| Actual | 54.5 |

| Consensus | 54.5 |

| Previous | 54.5 |

| 01:00 | AUD |

| TD-MI Inflation Gauge M/M May | |

| Actual | -0.30% |

| Consensus | |

| Previous | 0.60% |

| 01:45 | CNY |

| RatingDog Manufacturing PMI May | |

| Actual | 51.8 |

| Consensus | 51.4 |

| Previous | 52.2 |

| 06:00 | EUR |

| Germany Retail Sales M/M Apr | |

| Actual | -0.30% |

| Consensus | -0.40% |

| Previous | -2.00% |

| Revised | -0.30% |

| 06:30 | CHF |

| Real Retail Sales Y/Y Apr | |

| Actual | 1.60% |

| Consensus | 0.20% |

| Previous | 0.50% |

| 07:00 | CHF |

| GDP Q/Q Q1 | |

| Actual | 0.70% |

| Consensus | 0.50% |

| Previous | 0.10% |

| Revised | 0.20% |

| 07:30 | CHF |

| Manufacturing PMI May | |

| Actual | 57.3 |

| Consensus | 54 |

| Previous | 54.5 |

| 07:50 | EUR |

| France Manufacturing PMI May F | |

| Actual | 49.7 |

| Consensus | 48.9 |

| Previous | 48.9 |

| 07:55 | EUR |

| Germany Manufacturing PMI May F | |

| Actual | 50.1 |

| Consensus | 49.9 |

| Previous | 49.9 |

| 08:00 | EUR |

| Eurozone Manufacturing PMI May F | |

| Actual | 51.6 |

| Consensus | 51.4 |

| Previous | 51.4 |

| 08:00 | EUR |

| Eurozone M3 Money Supply Y/Y Apr | |

| Actual | 2.70% |

| Consensus | 3.30% |

| Previous | 3.20% |

| 08:30 | GBP |

| Manufacturing PMI May F | |

| Actual | 53.9 |

| Consensus | 53.7 |

| Previous | 53.7 |

| 09:00 | EUR |

| Eurozone Unemployment Rate Apr | |

| Actual | 6.30% |

| Consensus | 6.20% |

| Previous | 6.20% |

| Revised | 6.30% |

| 13:30 | CAD |

| Manufacturing PMI May | |

| Actual | 52.9 |

| Consensus | |

| Previous | 53.3 |

| 13:45 | USD |

| Manufacturing PMI May F | |

| Actual | 55.1 |

| Consensus | 55.3 |

| Previous | 55.3 |

| 14:00 | USD |

| ISM Manufacturing PMI May | |

| Actual | 54.0 |

| Consensus | 52.6 |

| Previous | 52.7 |

| 14:00 | USD |

| ISM Manufacturing Prices Paid May | |

| Actual | 82.1 |

| Consensus | 85.3 |

| Previous | 84.6 |

| 14:00 | USD |

| ISM Manufacturing Employment Index May | |

| Actual | 48.6 |

| Consensus | |

| Previous | 46.4 |

| 14:00 | USD |

| Construction Spending M/M Apr | |

| Actual | 0.40% |

| Consensus | 0.30% |

| Previous | 0.60% |

| Revised | 0.20% |

US-Iran Endgame in Sight? Markets Vote for Peace as Oil, Yields and Dollar Fall

The dominant story across financial markets last week was not artificial intelligence, central banks, or economic data. It was a dramatic shift in expectations regarding the future of the US-Iran conflict. Investors increasingly embraced the view that the three-month war is moving toward a diplomatic resolution after reports emerged that negotiators had drafted a 60-day Memorandum of Understanding to extend the current ceasefire and establish a framework for broader de-escalation.

At the heart of the proposal is the Strait of Hormuz, the vital energy corridor that became the focal point of market fears throughout the conflict. According to reports, Iran would remove all restrictions on commercial shipping, clear underwater mines, and abandon plans to impose transit charges on passing vessels. In return, the United States would gradually dismantle its naval blockade and ease restrictions on Iranian oil exports. The framework effectively addresses the issue that posed the greatest threat to the global economy: a prolonged disruption to energy supplies.

Financial markets reacted immediately. Brent crude extended its steep retreat from earlier highs above $110 and breached $90 as traders priced in the prospect of normalized oil flows. The move represented a sharp reversal from the stagflation fears that dominated earlier in the past three months, when investors worried that a sustained closure of Hormuz could trigger another global inflation shock.

Bond markets reinforced the same message. The U.S. 10-year Treasury yield, which surged to 4.70% earlier in the month amid inflation concerns, reversed sharply lower and closed near 4.45%. The decline reflected growing confidence that the energy shock may not be severe enough to force another round of Federal Reserve tightening. Bond investors effectively voted against the worst-case inflation scenarios that had driven yields higher.

Equity investors were quick to embrace the improved backdrop. The removal of a major geopolitical risk arrived just as technology earnings and AI-related optimism remained exceptionally strong. Instead of worrying about oil prices and inflation, investors refocused on growth, productivity, and technology spending. The result was another powerful rally across global stock markets.

The biggest winners were once again technology-heavy markets. NASDAQ climbed to fresh records, while Nikkei and KOSPI surged to new highs. The synchronized advance reflected both relief over geopolitical developments and confidence that the AI investment cycle remains intact. European markets participated in the rally but continued to trail their U.S. and Asian counterparts.

Foreign exchange markets painted a more cautious picture. Kiwi and Aussie led gains as risk sentiment improved, while Dollar and Yen underperformed. Yet compared with the dramatic moves in stocks, oil, and bonds, currencies appeared far less convinced. Investors may be optimistic, but they are also aware that the agreement remains unsigned and politically fragile. The market is pricing peace, but the next phase depends on whether diplomacy can deliver what investors have already started to assume.

Brent Breakdown Signals Markets Are Pricing Oil Normalization

The most important chart in global markets is still Brent crude. Last week's extension of the decline from 112.72 provided the strongest evidence yet that investors are increasingly pricing a diplomatic resolution to the US-Iran conflict and a gradual normalization of energy flows through the Strait of Hormuz. The selloff accelerated after the market gapped lower at the start of the week, reflecting growing confidence that the tentative ceasefire framework could ultimately evolve into a broader agreement.

Technically, the break below 55 D EMA (now 98.41), is a significant bearish development for the near term. More importantly, Brent has remained firmly below the moving average, suggesting the breakdown is not merely a temporary overshoot. While downward momentum has slowed as prices hit the lower trend line, there is still little evidence of bottoming. As long as resistance at 97.81 remains intact, the path of least resistance continues to point lower.

Attention is now turning to the lower trend line support (now at 92.0 area). Sustained trading below that support would open the way toward 61.8% retracement of 58.72 to 119.50 at 82.04. Some stabilization could emerge around that 82.04 zone as short-covering activity develops. However, if global oil supply continues normalizing and geopolitical risks continue fading, any rebound is likely to be capped below the 55 D EMA, setting the stage for a deeper decline through 82.04 at a later stage.

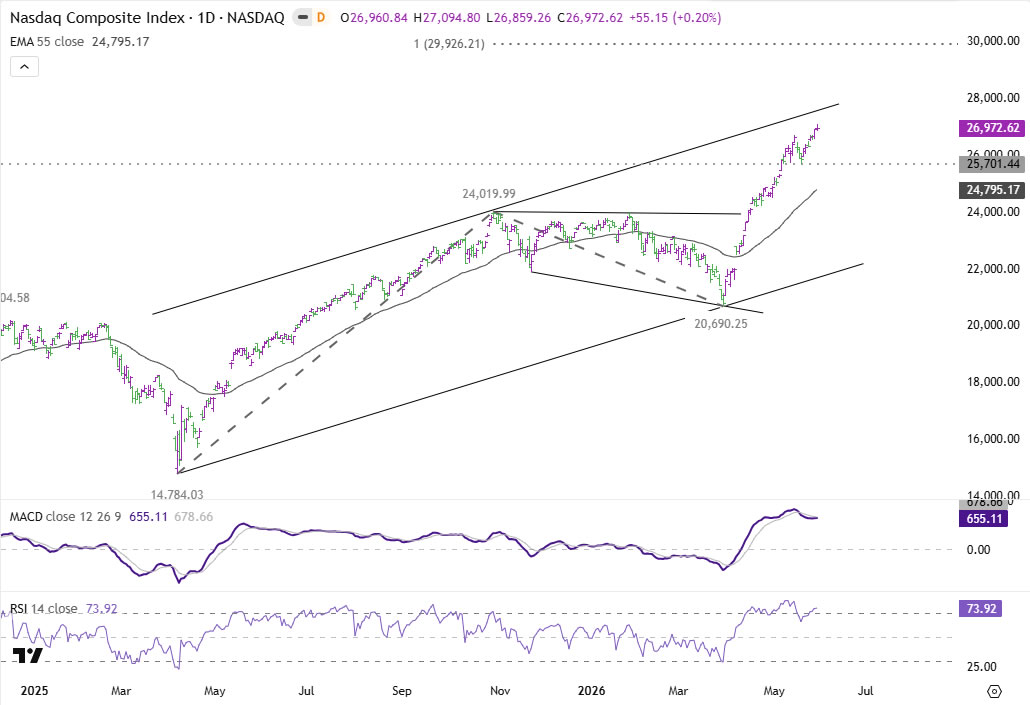

NASDAQ Surges as AI Optimism Reclaims the Narrative, 30,000 Next?

NASDAQ's powerful up trend extended further last week, with the index closing at a fresh record high of 26,972. The rally has now fully shaken off concerns surrounding the US-Iran conflict that dominated market sentiment earlier in the month. As fears of a prolonged disruption to global energy supplies faded and oil prices retreated sharply, investors quickly returned their focus to the theme that has driven equities for much of the past two years: artificial intelligence. Strong technology earnings and continued enthusiasm over AI-related capital spending have provided a powerful foundation for further gains.

Technically, upside momentum is showing some signs of moderation as NASDAQ approaches the upper boundary of its medium-term rising channel, currently near 27,600. However, there are no meaningful signs of a top forming yet. The index continues to register higher highs and higher lows, while pullbacks remain shallow and well supported by buyers. As long as this structure remains intact, the path of least resistance continues to point higher.

A decisive break above channel resistance could trigger another phase of upside acceleration. In that scenario, the next major target would be 100% projection of 14,784 to 24,019 from 20,690.25 at 29,926. That places the psychologically important 30,000 level firmly within reach.

On the downside, break of 25,701 support would be the first indication of short-term topping and suggest a deeper pullback toward 55 D EMA (now at 24,795) before the broader up trend resumes.

Bond Market Prices Out Worst-Case Inflation Scenario

The sharp reversal in U.S. Treasury yields last week may have been one of the clearest signals that markets are embracing a diplomatic resolution to the US-Iran conflict. After reaching a 16-month high clear to 4.70% on May 19 amid fears of a prolonged energy shock, the benchmark 10-year yield retreated aggressively and ended the week around 4.45%. The decline suggests bond investors are pricing out the most extreme inflation scenarios that dominated sentiment earlier in the month.

Technically, the break below 4.48 support-turned-resistance confirms that a short-term top is in place at 4.69. However, downside momentum has not yet become decisive. The initial decline stalled ahead of 38.2% retracement of 3.96 to 4.69 at 4.41%. That leaves the yield trapped in what could become a near-term consolidation range between 4.41 and 4.69 as markets await further clarity on both inflation and the progress of US-Iran negotiations.

The next directional move may depend heavily on geopolitics. A renewed escalation in the conflict or a resurgence in inflation pressures would likely be required to push yields back above 4.69. Conversely, a formal ceasefire agreement and continued decline in oil prices should trigger a decisive break below 4.41, signaling that the entire rise from 3.96 has already completed. In that scenario, deeper fall should be seen to 61.8% retracement at 4.24, with scope for an even deeper decline if inflation fears continue to fade.

Dollar Downtrend Back in Focus as Peace Trade Gains Momentum

One of the more interesting developments last week was the contrast between Dollar resilience and broader market trends. On one hand, the greenback did not suffer the kind of collapse typically associated with falling oil prices, easing geopolitical tensions, and surging equity markets. On the other hand, it also failed to generate any meaningful recovery despite lingering uncertainty surrounding the final approval of the US-Iran ceasefire framework. The result was a relatively subdued performance that left Dollar among the week's weaker currencies without triggering outright capitulation.

Technically, Dollar Index remains vulnerable after failing to sustain gains above 99.50. The retreat from 99.54 shifts immediate focus back to 55 D EMA (now at 98.77). Decisive break below that moving average would suggest the rebound from 97.63 was merely corrective and has already run its course. Such a development would likely encourage fresh selling pressure and place the January support zone at 95.55 back into focus.

The larger trend continues to favor Dollar weakness. The rebound from 95.55 earlier this year never managed to challenge the key 38.2% retracement of 110.17 (2025 high) to 95.55 (Jan low) at 101.13, leaving the broader sequence of lower highs intact. A break of above mentioned 97.63 support could be interpreted as indication that the decline from 110.17 (2025 high) is resuming.

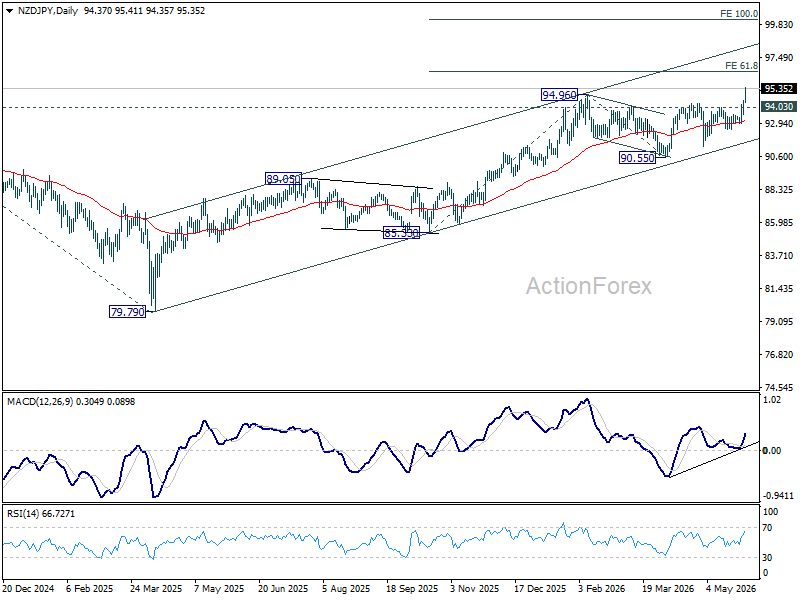

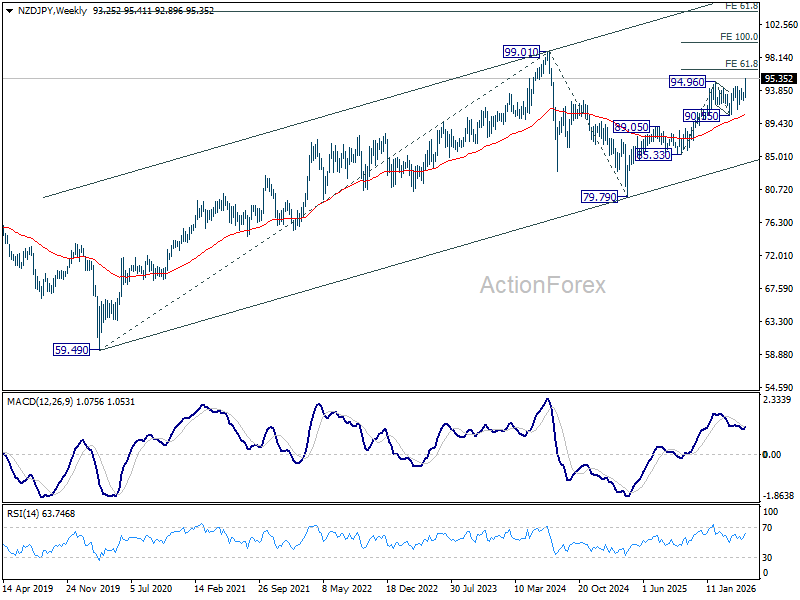

NZD/JPY Breakout Reflects RBNZ Hawkish Shift and Yen Weakness

NZD/JPY rallied strongly to become the week's top mover, gaining 2.45%, supported by a powerful combination of risk-on sentiment, a resurgent Nikkei, and growing expectations that the Reserve Bank of New Zealand may soon start its tightening cycle. While many currencies participated in the broader improvement in sentiment, NZD/JPY stood out because both sides of the pair moved decisively in its favor.

The Yen side of the equation was heavily influenced by developments in Japanese equities. Nikkei's decisive break above its medium-term rising channel resistance is a powerful technical signal that the rally is accelerating rather than exhausting itself. The index has become one of the world's strongest equity markets as investors aggressively rotate back into technology and AI-related themes. For Japanese investors, strong domestic equity performance continues to reduce demand for defensive Yen holdings.

Technically, further rally is expected in Nikkei as long as 63,799 resistance turned support holds. Firm break of 61.8% projection of 50,558 to 63,799 from 59,292 at 67,474 will pave the way through 70k psychological level to 100% projection at 72,532.

Such strength is likely to keep Yen under pressure. Although intervention concerns continue to discourage aggressive buying of USD/JPY near 160, they do little to prevent strength in Yen crosses where Dollar is not involved. As a result, NZD/JPY would be one of the cleanest vehicles for expressing bearish Yen views.

At the same time, New Zealand Dollar received substantial support from a dramatic shift in RBNZ expectations. The central bank maintained rates last week, but only after a 3-3 split vote that required Governor Anna Breman's casting vote to keep policy unchanged. More importantly, officials spent the rest of the week reinforcing the message that tightening is likely to come sooner rather than later, and perhaps more aggressively.

Several top policymakers effectively confirmed that July is now a live meeting for a rate hike. Even more striking was the refusal to rule out a larger move if inflation risks continue to build. Officials made clear they do not need to wait for the Q2 inflation report before acting. As a result, markets have shifted from debating whether the RBNZ will hike to debating whether a 25bps or 50bps move could ultimately be delivered at the next meeting.

NZD/JPY's medium term up trend resumed by breaking through 94.96 resistance last week. Further rise is now expected as long as 94.03 resistance turned support holds. Next target is 61.8% projection of 85.33 to 94.96 from 90.55 at 96.50. Decisive break there could trigger upward acceleration to 100% projection at 100.18, which is slightly above 100 psychological level.

In the bigger picture, NZD/JPY's rise from 79.79 (2025 low) is now looking more likely a five-wave impulse. That is, the correction from 99.01 (2024 high) could be totally completed with three waves down to 79.79. Up trend from 59.49 (2020 low) might be ready to resume. Firm break of above mentioned 96.50 projection level will solidify this long term bullish case.

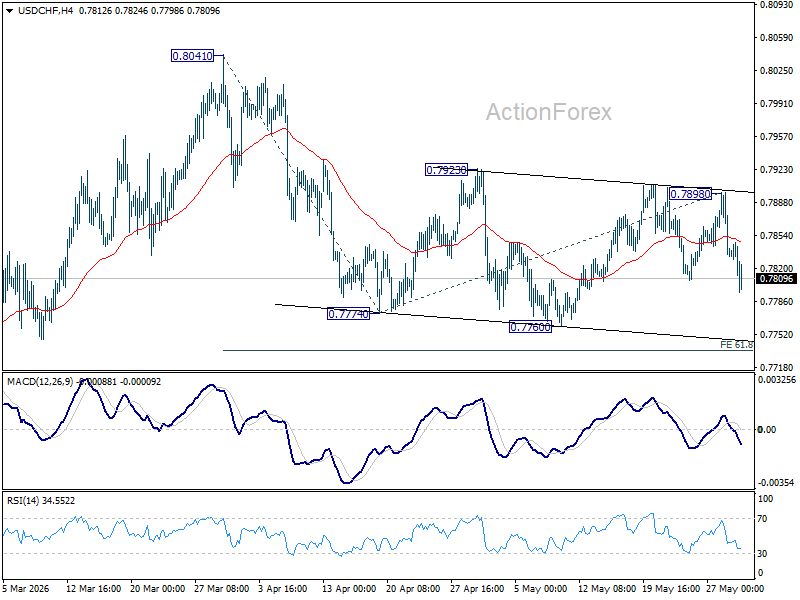

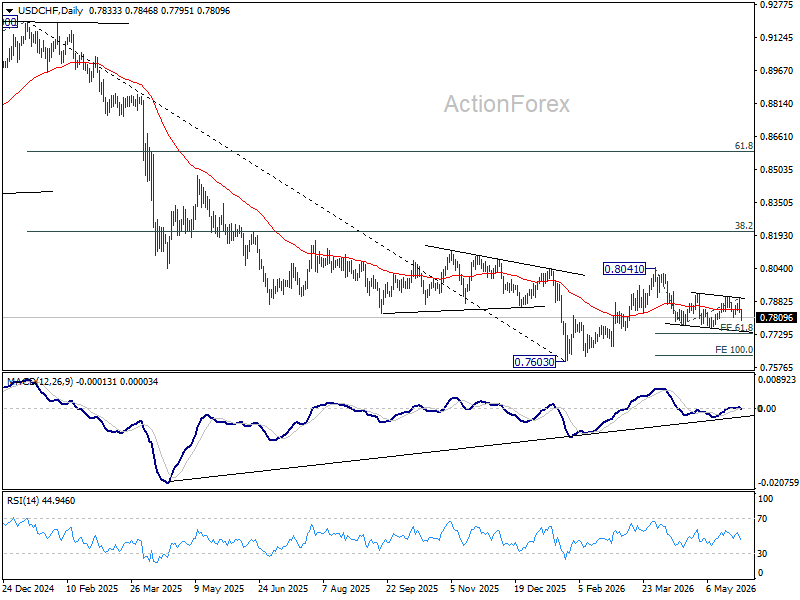

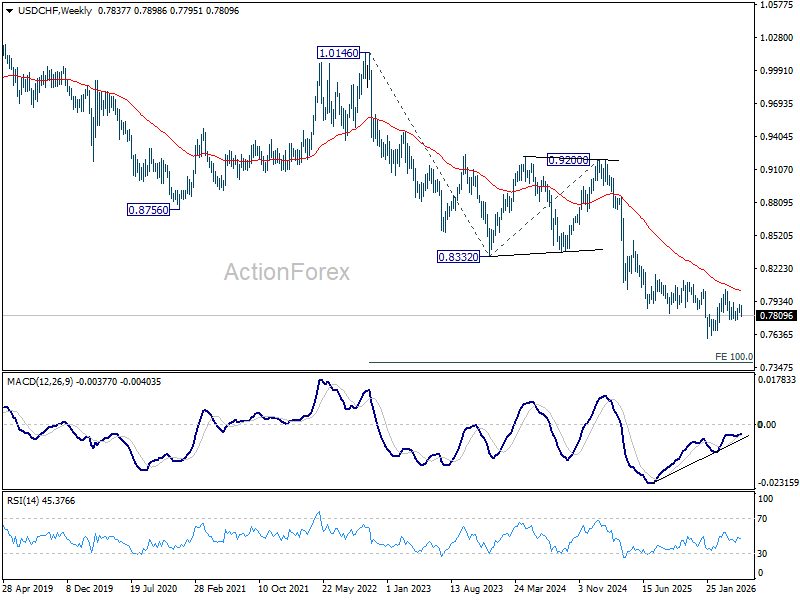

USD/CHF Weekly Outlook

The late break of 0.7807 support suggests that USD/CHF's corrective rebound has completed. Initial bias is back on the downside this week for retesting 0.7760 first. Firm break there will resume the fall from 0.8041. Next target will be 61.8% projection of 0.8041 to 0.7774 from 0.7898 at 0.7733. Risk will now stay on the downside as long as 0.7898 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 0.8028) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

In the long term picture, price action from 0.7065 (2011 low) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the downtrend. But in either case, outlook will stay bearish as long as 0.8756 support turned resistance holds (2021 low). Retest of 0.7065 should be seen next.

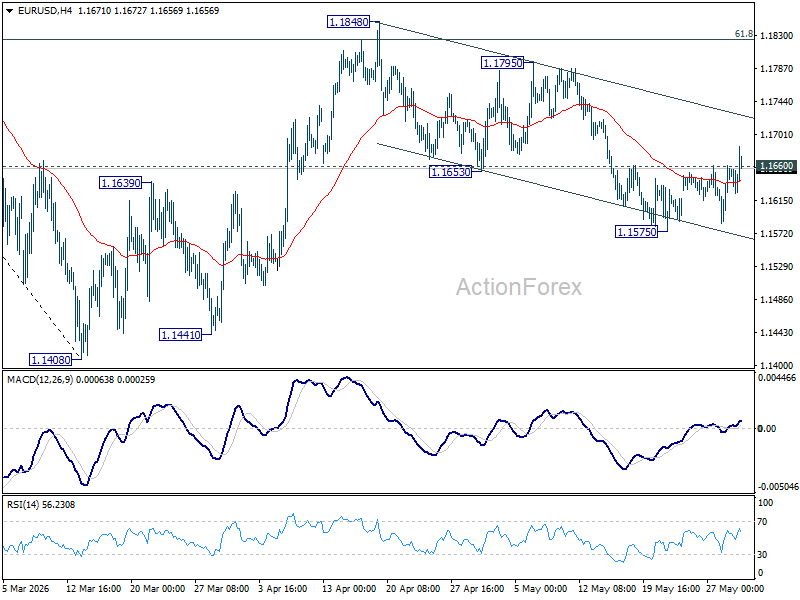

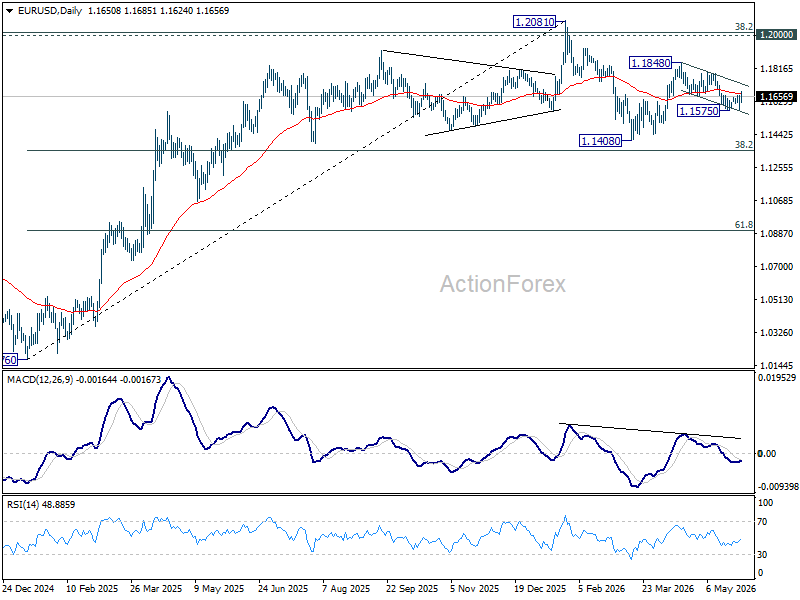

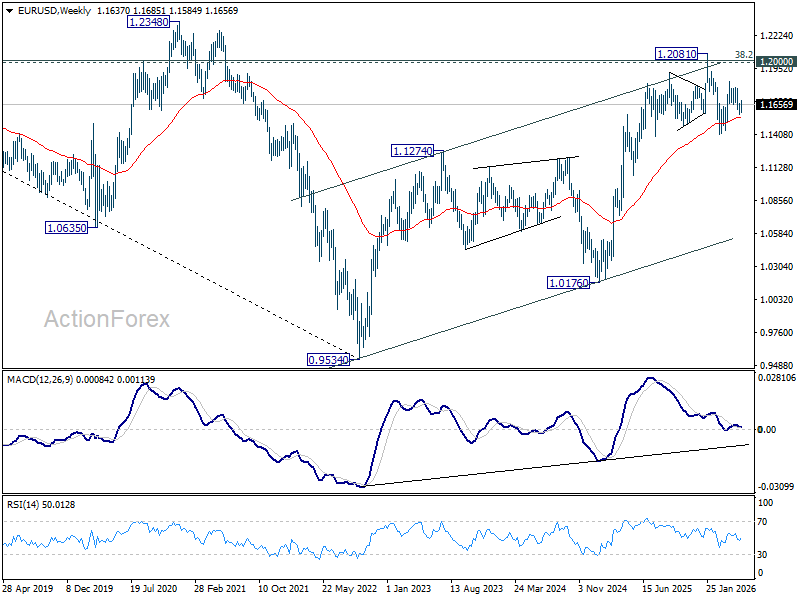

EUR/USD Weekly Outlook

EUR/USD's late break of 1.1660 resistance argues that a short term bottom was already formed at 1.1575. More importantly, fall from 1.1848 could have completed as a three wave-correction. Initial bias is mildly on the upside this week for 1.1795 resistance first. For now, risk will stay on the upside as long as 1.1575 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1542). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

In the long term picture, 38.2% retracement of 1.6039 to 0.9534 at 1.2019, which is close to 1.2000 psychological level is the key for the outlook. Rejection by this level will keep the multi decade down trend from 1.6039 (2008 high) intact, and keep outlook neutral at best. However, decisive break of 1.2000/19, will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

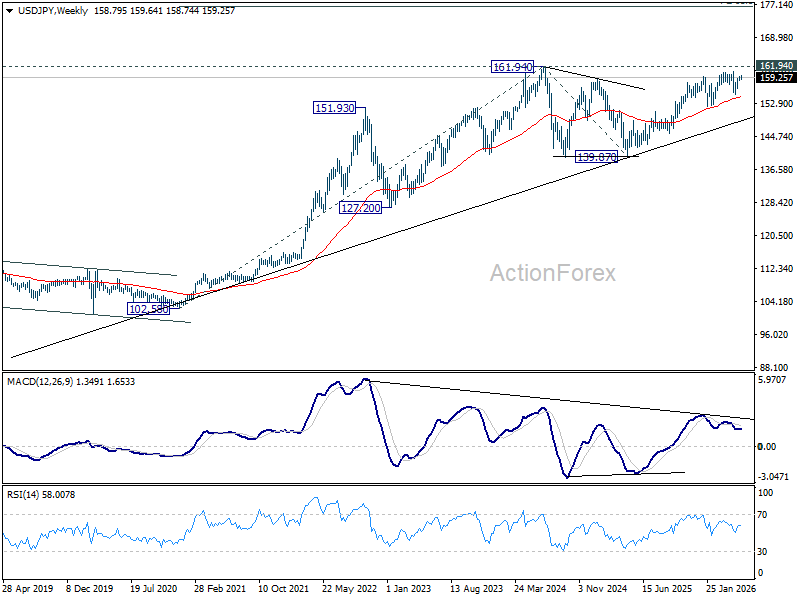

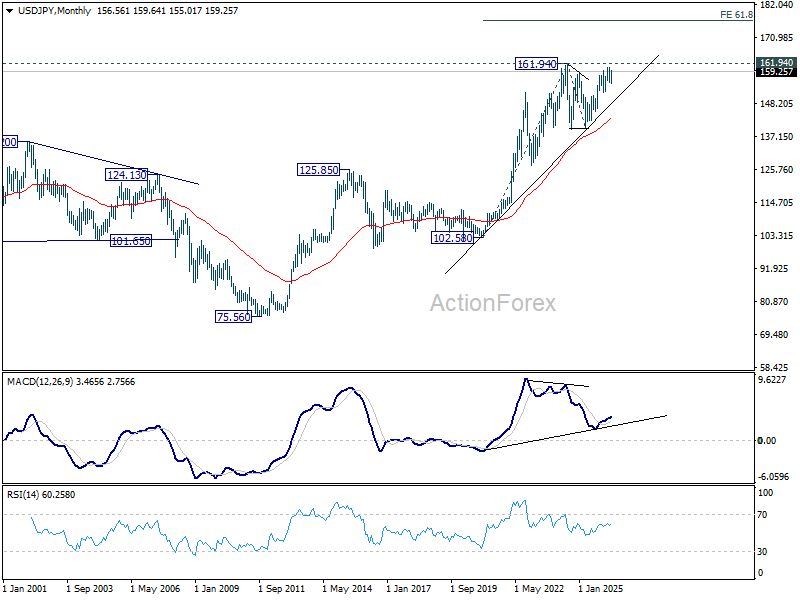

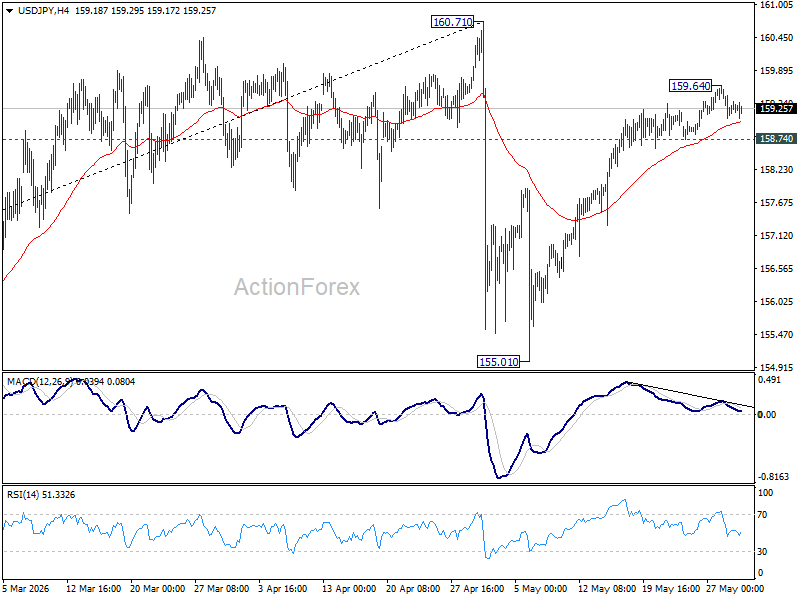

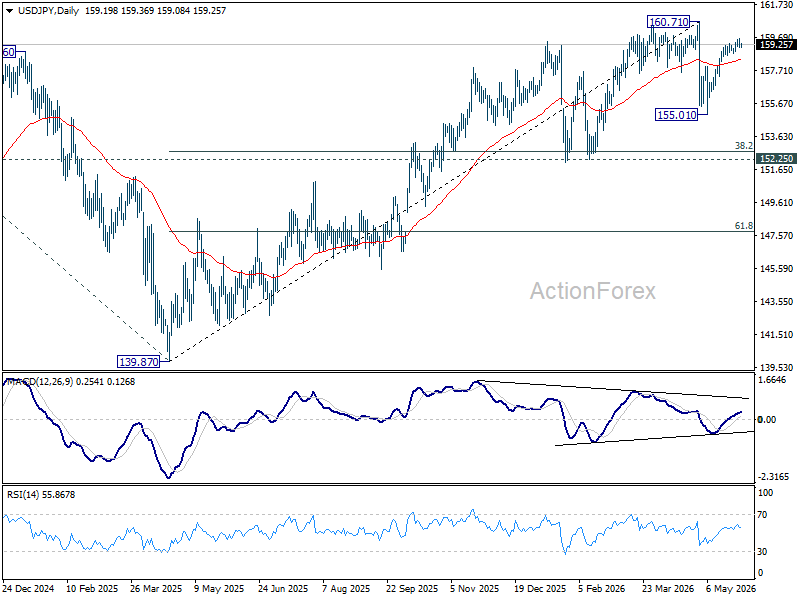

USD/JPY Weekly Outlook

USD/JPY edged higher to 159.64 last week but retreated since then. Rise from 155.01 is seen as the second leg of the corrective pattern from 160.71. While another rally cannot be ruled out, strong resistance should be seen from 160.71 to bring reversal. Considering bearish divergence condition in 4H MACD, firm break of 158.74 support will argue that the rise from 155.01 has completed already. Intraday bias will be back on the downside for 55 D EMA (now at 158.36) and below.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.36) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

In the long term picture, up trend from 75.56 (2011 low) is still in progress and might be ready to resume. Firm break of 161.94 will target 61.8% projection of 102.58 (2020 low) to 161.94 (2024 high) from 139.87 at 176.55 in the medium term. Long term outlook will stay bullish as long as 139.87 support holds, even in case of deep pullback.