Sample Category Title

RBA Surprise Hold Lifts Aussie; Trump Tariff Threat Hits 14 Countries

Aussie rallied sharply on Tuesday after RBA unexpectedly held its cash rate steady at 3.85%, defying widespread expectations for a 25bps cut. While a majority of economists had penciled in an easing move, the 6-3 vote revealed deep divisions within the Board. It's unclear whether RBA’s decision was influenced at the last minute by escalating global trade risks. The US has begun sending formal letters to key trade partners with new tariff schedules, creating significant uncertainty for export-dependent economies like Australia. Yet, broader Asian markets appeared relatively calm. Equity indexes across the region posted modest gains

On the trade front, US President Donald Trump confirmed that 14 countries will face new blanket tariffs starting August 1. Signed letters detailed levies ranging from 25% to 40%. Trump’s executive order also pushed back the original July 9 deadline by three weeks, offering a narrow window for countries to negotiate bilateral deals.

The list of countries receiving tariff notices is sweeping and includes several key US trading partners: Japan, South Korea, Malaysia, Kazakhstan, South Africa, Laos, Myanmar, Tunisia, Bosnia and Herzegovina, Indonesia, Bangladesh, Serbia, Cambodia, and Thailand. The rates vary—25% for Japan, South Korea, Malaysia, Kazakhstan, and Tunisia; 30% for South Africa and Bosnia; 32% for Indonesia; 35% for Bangladesh and Serbia; 36% for Cambodia and Thailand; and 40% for Laos and Myanmar. The letters also warned that goods rerouted through third countries to evade tariffs would be penalized.

It's surprising that close US allies Japan and South Korea are also at the center of the storm, now facing 25% tariffs. Japan confirmed receipt of a proposal offering a potential reprieve if negotiations proceed swiftly. Prime Minister Ishiba said revisions to the letter remain possible depending on Tokyo’s response. South Korea echoed a similar stance, viewing the delay as a chance to resolve tariff concerns amicably.

The European Union was excluded from the list of affected countries. EU sources confirmed no tariff letters were received, and the bloc remains focused on finalizing a deal by mid-week. European Commission President Ursula von der Leyen’s recent “good exchange” with Trump was cited as a positive sign, though officials remain divided over the depth of any agreement.

In FX markets, Aussie leads gains for the day so far, followed by Kiwi and Euro. Dollar lags behind, alongside Yen and Loonie. Sterling and the Swiss Franc are trading mid-pack.

In Asia, at the time of writing, Nikkei is up 0.23%. Hong Kong HSI is up 0.78%. China Shanghai SSE is up 0.58%. Singapore Strait Times is up 0.47%. Japan 10-year JGB yield is up 0.05 at 1.488. Overnight, DOW fell -0.94%. S&P 500 fell -0.79%. NASDAQ fell -0.92%. 10-year yield jumped 0.047 to 4.395.

RBA skips July cut, prefers to wait a little more for clarity

RBA held its cash rate target at 3.85%, opting not to deliver the widely expected 25bps cut. The decision, passed by a 6-3 majority, reflected cautious optimism as the central bank noted more balanced inflation risks and a still-resilient labor market. However, the Board stopped short of declaring victory on inflation and flagged considerable uncertainty in the domestic and global outlook.

In its statement, RBA said it could afford to “wait for a little more information” to ensure inflation is sustainably heading toward its 2.5% target. The Board remains concerned about both demand and supply-side uncertainty, particularly in light of volatile global trade policy. RBA stressed that monetary policy remains "well-positioned" to respond quickly if conditions deteriorate.

RBA also issued a measured warning on the risks stemming from U.S. tariffs and global trade policy shifts, noting that while extreme outcomes may be avoided, the uncertainty itself could weigh on demand. Financial markets have rebounded on hopes of compromise, but the RBA highlighted the risk that firms and households could delay spending amid the policy fog.

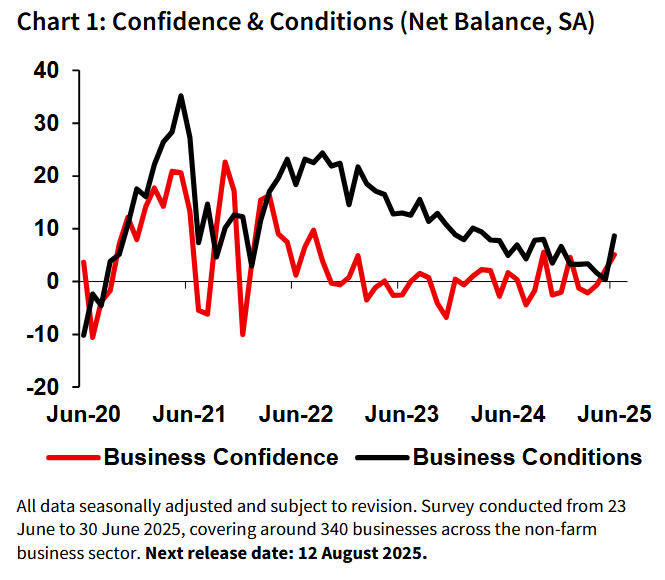

Australia's NAB business confidence rises to 5, conditions rebound to 9

Australia’s business sentiment improved sharply in June, with NAB Business Confidence rising from 2 to 5, its highest trend level in over a year. Business Conditions surged from 0 to 9 after weakening for five straight months. The rebound was broad-based, with trading conditions jumping from 5 to 15, profitability returning to positive territory from -5 at 4, and employment conditions edging up from to 3.

On the pricing side, signals were mixed. Labour cost growth eased slightly from 1.6% to 1.5% (quarterly equivalent), while purchase costs rose from 1.2% to 1.5%. Final product price growth ticked up from 0.5% to 0.6%, although retail price growth slowed to 0.6%, hinting at easing consumer price pressures despite supply-side stickiness.

NAB’s Gareth Spence said the data suggest momentum may be picking up into the second half of 2025. “While we know the monthly survey can be volatile, the hope is at least some of these trends will be sustained,” he noted, calling the jump in both confidence and conditions a positive surprise amid ongoing global uncertainty.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6463; (P) 0.6513; (R1) 0.6541; More...

AUD/USD rebounded notably today but stays below 0.6589 resistance. Intraday bias stays neutral and more consolidations could still be seen. Overall, further rally is still expected as long as 0.6372 support holds. On the upside, firm break of 0.6589 will resume the rise from 0.5913 and target 0.6713 fibonacci level.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).

RBA skips July cut, prefers to wait a little more for clarity

RBA held its cash rate target at 3.85%, opting not to deliver the widely expected 25bps cut. The decision, passed by a 6-3 majority, reflected cautious optimism as the central bank noted more balanced inflation risks and a still-resilient labor market. However, the Board stopped short of declaring victory on inflation and flagged considerable uncertainty in the domestic and global outlook.

In its statement, RBA said it could afford to “wait for a little more information” to ensure inflation is sustainably heading toward its 2.5% target. The Board remains concerned about both demand and supply-side uncertainty, particularly in light of volatile global trade policy. RBA stressed that monetary policy remains "well-positioned" to respond quickly if conditions deteriorate.

RBA also issued a measured warning on the risks stemming from U.S. tariffs and global trade policy shifts, noting that while extreme outcomes may be avoided, the uncertainty itself could weigh on demand. Financial markets have rebounded on hopes of compromise, but the RBA highlighted the risk that firms and households could delay spending amid the policy fog.

(RBA) Statement by the Reserve Bank Board: Monetary Policy Decisions

At its meeting today, the Board decided to leave the cash rate target unchanged at 3.85 per cent.

Inflation has continued to moderate.

Inflation has fallen substantially since the peak in 2022, as higher interest rates have been working to bring aggregate demand and supply closer towards balance. In the March quarter, headline inflation, which has partly been affected by temporary cost of living relief, was at the midpoint of the target range while trimmed mean inflation was at 2.9 per cent. The baseline forecast in May was for underlying inflation to continue to moderate to around the midpoint of the 2–3 per cent range with the cash rate assumed to follow a gradual easing path. While recent monthly CPI Indicator data suggest that June quarter inflation is likely to be broadly in line with the forecast, they were, at the margin, slightly stronger than expected. With the cash rate 50 basis points lower than five months ago and wider economic conditions evolving broadly as expected, the Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis.

The outlook remains uncertain.

Uncertainty in the world economy remains elevated. While the final scope of US tariffs and policy responses in other countries remains unknown, financial market prices have rebounded with an expectation that the most extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic activity, and there remains a risk that households and firms delay expenditure pending greater clarity on the outlook.

Setting aside overseas developments, private domestic demand appears to have been recovering gradually, real household incomes have picked up and there has been an easing in some measures of financial stress. However, businesses in some sectors continue to report that weakness in demand makes it difficult to pass on cost increases to final prices.

At the same time, various indicators suggest that labour market conditions remain tight. Measures of labour underutilisation are at relatively low rates and business surveys and liaison suggest that availability of labour is still a constraint for a range of employers. Looking through quarterly volatility, wages growth has softened from its peak but productivity growth has not picked up and growth in unit labour costs remains high.

There are uncertainties about the outlook for domestic economic activity and inflation stemming from both domestic and international developments. The March quarter national accounts confirmed that domestic demand has been picking up over the past six months. The forecasts in May were for growth in household consumption to continue to increase as real incomes rise. There is a risk that the pick-up is a little slower than earlier expected, which could result in continued subdued growth in aggregate demand and a sharper deterioration in the labour market than currently expected. Alternatively, labour market outcomes may prove stronger than expected, given the signal from a range of leading indicators.

There are also uncertainties regarding the lags in the effect of recent monetary policy easing and how firms’ pricing decisions and wages will respond to the balance between demand and supply for goods and services, tight conditions in the labour market and continued weak productivity outcomes.

Maintaining price stability and full employment is the priority.

The Board continues to judge that the risks to inflation have become more balanced and the labour market remains strong. Nevertheless it remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply. The Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis. It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia.

The Board will be attentive to the data and the evolving assessment of risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

Decision

The Board has decided to publish an unattributed record of votes in the post-meeting statement. Today’s policy decision was made by majority; 6 in favour, 3 against.

Australia’s NAB business confidence rises to 5, conditions rebound to 9

Australia’s business sentiment improved sharply in June, with NAB Business Confidence rising from 2 to 5, its highest trend level in over a year. Business Conditions surged from 0 to 9 after weakening for five straight months. The rebound was broad-based, with trading conditions jumping from 5 to 15, profitability returning to positive territory from -5 at 4, and employment conditions edging up from to 3.

On the pricing side, signals were mixed. Labour cost growth eased slightly from 1.6% to 1.5% (quarterly equivalent), while purchase costs rose from 1.2% to 1.5%. Final product price growth ticked up from 0.5% to 0.6%, although retail price growth slowed to 0.6%, hinting at easing consumer price pressures despite supply-side stickiness.

NAB’s Gareth Spence said the data suggest momentum may be picking up into the second half of 2025. “While we know the monthly survey can be volatile, the hope is at least some of these trends will be sustained,” he noted, calling the jump in both confidence and conditions a positive surprise amid ongoing global uncertainty.

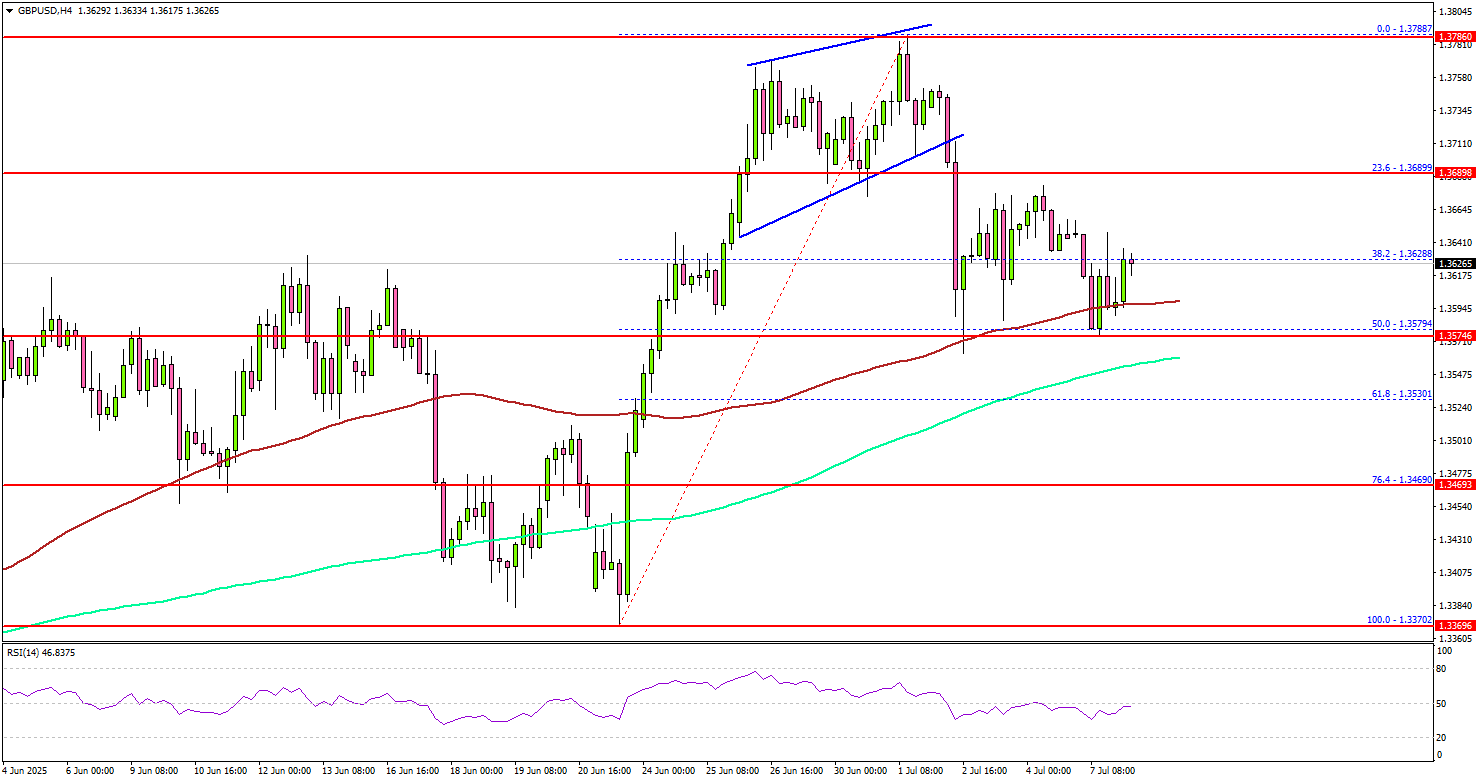

GBP/USD Retreats — Bulls Eye Bounce From Support

Key Highlights

- GBP/USD corrected gains from the 1.3800 resistance.

- It found support near 1.3580 and the 100 simple moving average (red, 4-hour).

- EUR/USD started a consolidation phase below the 1.1820 resistance.

- Gold prices could extend losses if there is a move below $3,280.

GBP/USD Technical Analysis

The British Pound failed to clear 1.3800 against the US Dollar. GBP/USD started a downside correction and traded below the 1.3700 level.

Looking at the 4-hour chart, the pair dipped below the 38.2% Fib retracement level of the upward move from the 1.3370 swing low to the 1.3788 high. The pair even dipped below the 1.3650 level before the bulls appeared.

The pair found support near the 50% Fib retracement level of the upward move from the 1.3370 swing low to the 1.3788 high at 1.3580. It remained stable above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

On the upside, the pair could face resistance near the 1.3660 level. The next key resistance sits near the 1.3720 level. A close above the 1.3720 level could set the pace for another increase. In the stated case, the pair could even clear the 1.3750 resistance. The next major stop for the bulls could be near the 1.3800 resistance.

On the downside, immediate support is near the 1.3580 level. The next key support sits near 1.3550. Any more losses could send the pair toward the 1.3500 support zone.

Looking at EUR/USD, the pair failed to extend gains above the 1.18200 resistance and recently started a short-term downside correction.

Upcoming Economic Events:

- EcoFin Meeting

- NFIB Business Optimism Index for June 2025 – Forecast 98.7, versus 98.8 previous.

Australian Dollar Outlook as Markets Prepare for Upcoming RBA Rate Decision

The Australian Dollar is coming off several weeks of strength, buoyed by broad market optimism and fading tariff concerns that have lifted global growth sentiment—typically a supportive backdrop for the AUD and other commodity-linked currencies.

Australia’s economy remains resilient, with the unemployment rate holding near 4.1%. However, the Reserve Bank of Australia (RBA) expects the number to gradually rise toward year-end, adding to the case for further monetary easing.

With that in mind, markets widely expect a 25 bps rate cut at the upcoming RBA meeting (Current 3.85% expected to get to 3.60%). While this move is largely priced in, surprises remain possible, especially as inflation—though easing—may be reignited by Trump’s tariffs on Chinese goods, which could spill over into Australia through trade channels.

AUD moves aren’t purely driven by domestic factors. Keep an eye on the US Dollar, which is rebounding to start the week, as well as China’s economic trajectory. Any slowdown from the Middle Kingdom—Australia’s top trading partner—could weigh on the Aussie, though current data doesn’t yet reflect such weakness.

The Rate Decision is coming up overnight at 00:30 A.M ET.

Australian Dollar Multi-Timeframe Chart Analysis

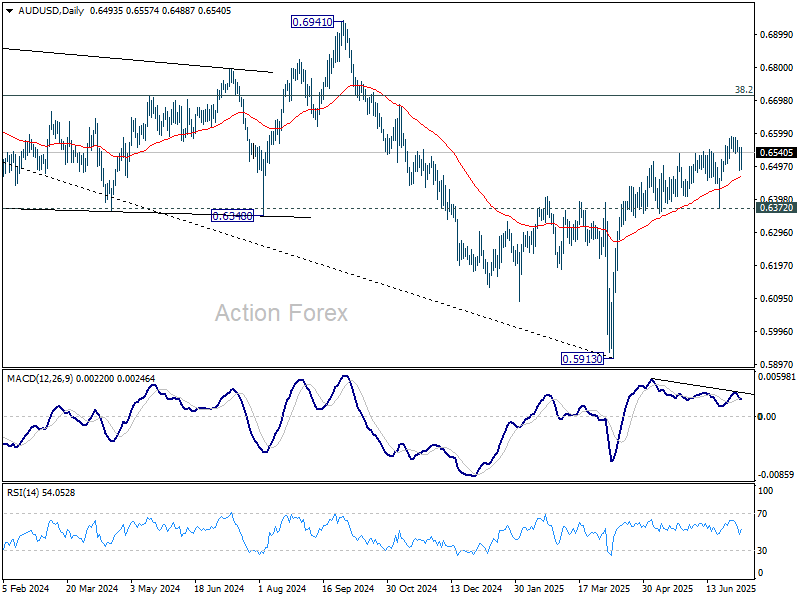

Weekly Chart — Where do we stand in the bigger picture?

The 2024 downtrend has been met with a sharp rebound as AUD buyers (and USD Sellers) came in strong – particularly after the Liberation Day selloff and consequent V-Shape rebound.

Prices are approaching the secular downtrend which will be essential to monitor – structural flows are leading to US Dollar outflows but time will tell if this effect is strong enough for an AUD Breakout. Despite cuts, as long as the Australian Economy stays strong, this idea might be gradually playing out.

Prices are consolidating on the weekly, hanging between the 20 week Moving average acting as support (0.6386) and the 200-week MA acting as longer-term resistance at 0.6718, 2 full handles from current prices.

Daily Chart

Dow Jones Daily Chart, July 7, 2025 – Source: TradingView

Prices have came back into the upwards Daily started that had started to form in March, with many touches on the upper and lower bounds confirming the strength of such a trend.

However, trends tend to change on key events such as tomorrow's rate decision; as long as there is no surprise to current cut expectations, players shouldn't expect any sudden breakout – watch for your pre-existing orders which may be triggered by rising volatility in the case of a surprise!

Daily levels to watch:

Resistance Levels:

- Daily resistance 0.6670 to 0.6740

- 0.6655 higher bound of the upwards channel

- 0.6580 most recent swing highs

Support Levels:

- 0.65 psychological level

- 0.6475 MA 50 and lower bound of channel

- Daily Support 0.63 to 0.64

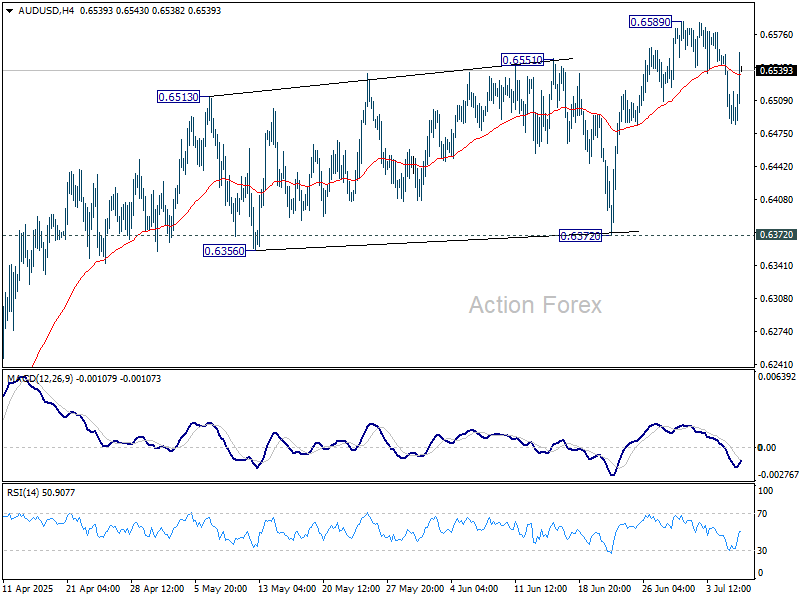

Hourly Chart

AUDUSD's short-term momentum is getting slightly bearish with the 50-H MA breaching the 200-MA, however technicals might not be as strong as markets approach the overnight Rate Decision.

Still, last week's strong US data has led to a strong reversal that has stalled at the 0.64864 immediate lows – a key level to watch for immediate strength analysis.

Momentum is back closer to neutral after a double bottom in RSI and the re-appearance of some USD Sellers.

For immediate resistance, watch the 0.6550 MA Confluence zone, and further upside reaction to last week highs.

Safe Trades!

Silver Consolidates Close to the 2012 Highs, Poised for a Breakout?

Metals have seen a strong multi-year performance, largely driven by post-COVID currency depreciation. The widespread use of Quantitative Easing (QE) and balance sheet expansions by central banks put fiat currencies under pressure, giving precious metals a solid fundamental tailwind.

In contrast, the 2022 global rate-hiking cycle helped restore some purchasing power to fiat currencies, temporarily capping gains in metals as tighter monetary policy reined in inflation expectations – but this effect has waned as Policy Rates have started to go down globally since their 2023 peaks.

A comparable period unfolded between 2004 and 2011, when Gold rose from around $400 to a high of $1,880 per ounce, propelled by QE1 following the 2008 Global Financial Crisis.

Gold has more than doubled its value since October 2022 lows and has dragged other precious metals upwards such as Platinum, Palladium or Silver.

Silver followed a similar trajectory, rallying from $6 to an all-time high of $49.80, before retreating in the years that followed. This correction was in part driven by a supply response, as miners ramped up production in response to soaring prices.

Silver Analysis from Monthly to 4H Timeframes

Silver Monthly Chart

Silver Monthly Chart, from 2002 to Today July 7, 2025 – Source: TradingView

The precious metal is currently trading in the 2012 range ($27 to $37) after breaking out from the previous $15 to $27 2020 to 2023 range.

Prices seem to be arriving close to overbought in the monthly chart, however the RSI is not there yet and the past few months of buying have printed strong thrust into the ongoing trend.

The metal is currently forming the premises of a monthly upwards channel, indicating potential resistance around $41 but has first to overpass the 2012 $37.50 highs to get there.

Silver Daily Chart

Silver Daily Chart July 7, 2025 – Source: TradingView

Lower timeframes give more clarity on how the current impulsive move up is going – a major push from Feb 2024 $24 lows took the metal to $32 before retracting and forming the ongoing steeper Weekly Channel.

Liberation Day created a sharp selloff from $34 to $28 before the general market recovery and Dollar outflows took prices to decade highs.

Prices have consolidated largely since the Israel-Iran $37.31 highs, taking the RSI from overbought to current neutral levels – as the 20 Day Moving Average finally caught up, the rest is to see if buyers use this technical support to generate another impulsive move.

Silver 4H Chart

Silver 4H Chart July 7, 2025 – Source: TradingView

Silver has been consolidating in a $2 range from $35 to $37 particularly since the Israel-Iran war created newfound demand for safe-havens and Silver, despite not being the first asset for flight-to-safety, can still be considered as such.

An interesting pattern can be in developments in the 4H Chart, as the selling from the weekly open just stopped at its 50 period MA, close to the middle of the range.

A failure to regain the lower part of the range substantially raises the probability of an upside breakout.

In the meantime, prices will have to at least hold this week's $36.15 lows.

Levels to add on your charts:

Support Levels:

- $36.40 MA 50 immediate support

- $35 to $35.50 last swing lows + 4H MA 200

Resistance Levels:

- $37 to $37.50 (2012 highs)

- Potential Resistance $38 to $38.5 (Fibonacci extension)

- Potential Resistance + High of Weekly Channel $39 to $40 (1.618 Fib extension)

Safe Trades!

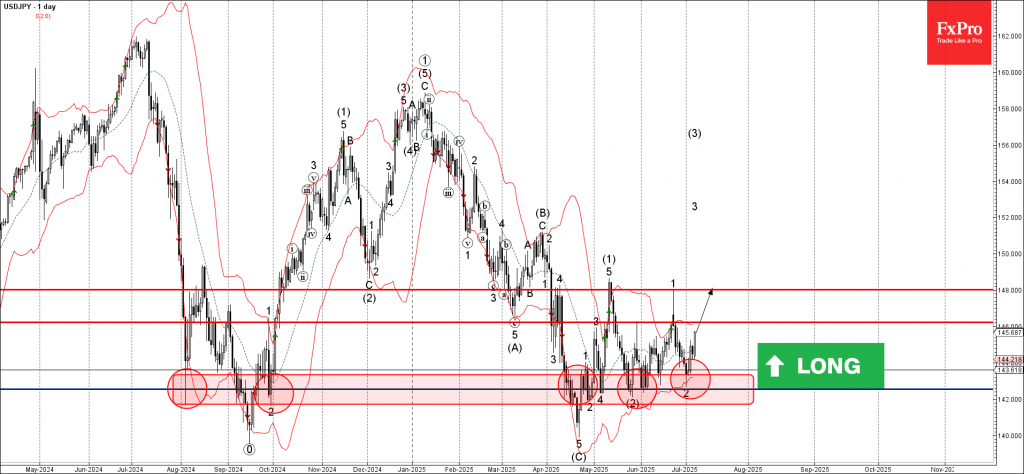

USDJPY Wave Analysis

USDJPY: ⬆️ Buy

- USDJPY reversed from long-term support level 142.50

- Likely to rise to resistance level 148.00

USDJPY currency pair recently reversed up from the support zone located between the long-term support level 142.50 (which has been steadily reversing the price from August of 2024, as can be seen from the daily USDJPY chart below) and the lower daily Bollinger Band.

The upward reversal from this support zone stopped the previous short-term ABC correction 2 from the end of June.

Given the strength of the support level 142.50 and the strongly bearish yen sentiment seen today, USDJPY currency pair can be expected to rise to the next resistance level 148.00 (top of the previous waves 4, (1) and 1).

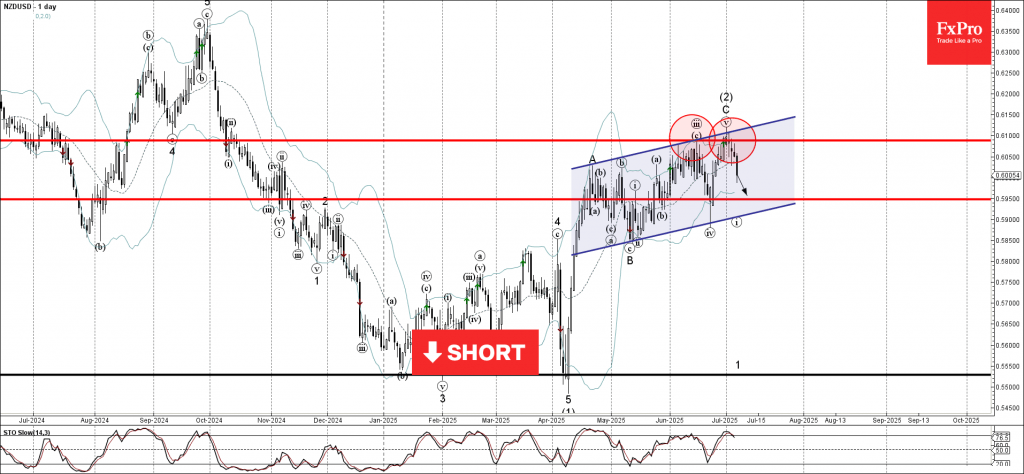

NZDUSD Wave Analysis

NZDUSD: ⬇️ Sell

- NZDUSD reversed from resistance level 0.6100

- Likely to fall to support level 0.5950

NZDUSD currency pair recently reversed down from the key resistance level 0.6100 (which has been steadily reversing the price from October, as can be seen from the daily NZDUSD chart below) – intersecting with the upper daily Bollinger Band and the resistance trendline of the daily up channel from April.

The downward reversal from the resistance level 0.6100 stopped the previous medium-term impulse ABC correction (2) from the start of April.

Given the strength of the resistance level 0.6100, NZDUSD currency pair can be expected to fall to the next support level 0.5950.