Sample Category Title

Keeping Tabs: Tariff Tracker Update

Summary

In the latest pause on tariff implementation, the window for deal-making is extended, but so too is the uncertainty that complicates capital spending decisions. This report unveils our latest tariff tracker featuring increased visibility into our process.

Pause Offers an Extended Window for Deal-Making

The post-Liberation day selloff in financial markets played a role in putting many of the most far-reaching aspects of the tariffs on ice. The net effect was not to eliminate the effective tariff rate, but rather to take it down from a Liberation Day peak of ~30% to something closer to 14% for the better part of the intervening weeks. The scheduled deadline of July 9 has been met with another pause, pushing off the implementation date for many countries to August. But, it is not entirely clear that every country has benefited from this stay of execution.

But What is the Tariff Rate in the Meantime?

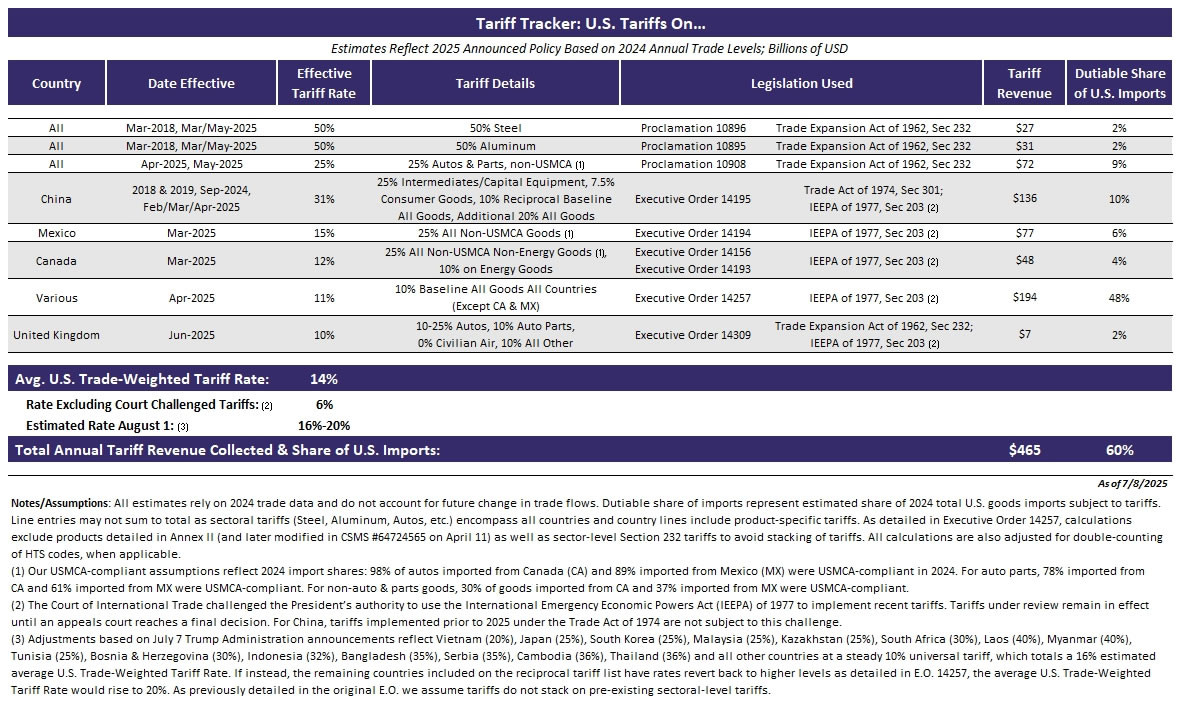

Our latest update of our Tariff Tracker reflects our attempt to comb through the various Executive Orders, Presidential Proclamations and social media posts to distill what it all means for trade and import costs. The ever-changing framework can make this effort a pencil-snapping frustration, but our best efforts put the current effective tariff rate at 14% based on current policy. That could rise to 16% by the start of August based solely on this week's country-specific announcements (the letters to the 15 impacted countries on July 7) and to as high as 20% if tariffs revert higher for the remaining 40 or so countries on the original reciprocal-tariff list from early April.

Putting off the increased levy will no doubt bring some short-term relief for impacted business owners and purchasing managers, though it does little to alleviate the pervasive sense of uncertainty that has scope to pare capital spending plans in the back half of the year. In the latest ISM manufacturing index, nine out of ten respondents from various industry groups called out tariffs as an impediment to activity in their sectors.

No Secret to Our Approach

We've put our methodology for the Tariff Tracker right in the tool itself in the "Notes/Assumptions" section. The goal is to be more transparent and show exactly how we landed where we did. The tracker pulls trade data at the detailed-HTS code level for each policy designated in the Presidential Documents section of the Federal Register. We adjust for things like tariff exclusions and double counting.

We don't claim to be experts on international trade law or even the inner workings of trade policy. Rather, this tool is intended as a macroeconomic resource and our best-effort attempt at tallying the potential broad impact of the trade war on the U.S. economy.

Source: U.S. Department of Commerce and Wells Fargo Economics

NY Fed survey: Inflation expectations ease, job security rises

US consumers grew more optimistic in June, with inflation expectations moderating and perceptions of job security improving, according to the latest New York Fed Survey of Consumer Expectations.

One-year-ahead median inflation expectations fell to 3.0%, reversing the recent uptick to 3.6% in April and returning to January levels. Longer-term expectations were unchanged at 3.0% for the three-year horizon and 2.6% for five years out.

Despite the easing in the overall inflation outlook, households still foresee higher costs in key sectors. Expectations for gas prices rose to 4.2%, while anticipated medical care inflation jumped to 9.3% — the highest since June 2023. Price expectations for college tuition and rent also climbed to 9.1%, and food inflation is still seen at a firm 5.5%. These category-specific pressures suggest that while headline inflation may be easing, households continue to feel cost pressures in essential areas.

Labor market sentiment strengthened, with the perceived probability of losing one’s job in the next 12 months falling to 14.0% — the lowest since December 2024. The improvement was broad-based across age and education groups.

Is the US Dollar Doomed or is a Correction Looming?

- US Dollar wallows near 3-year lows as bearish bets gather pace.

- Fed rate cut expectations and economic worries weigh.

- Trade and Trump-related uncertainty casts a shadow over the outlook.

- But is the gloom overdone?

Worst start to year in half a century

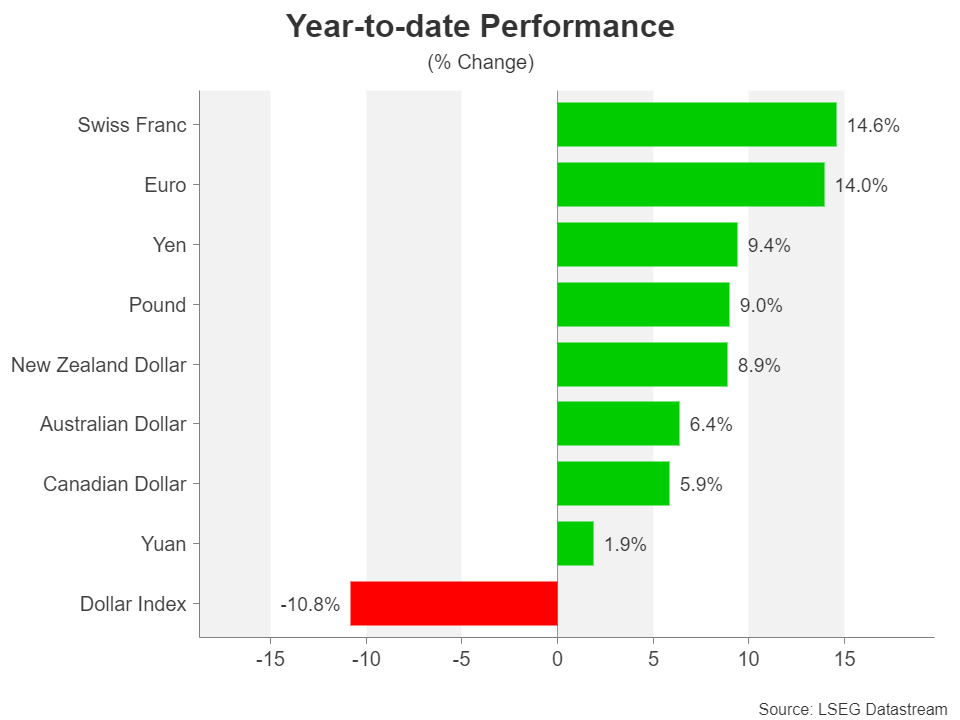

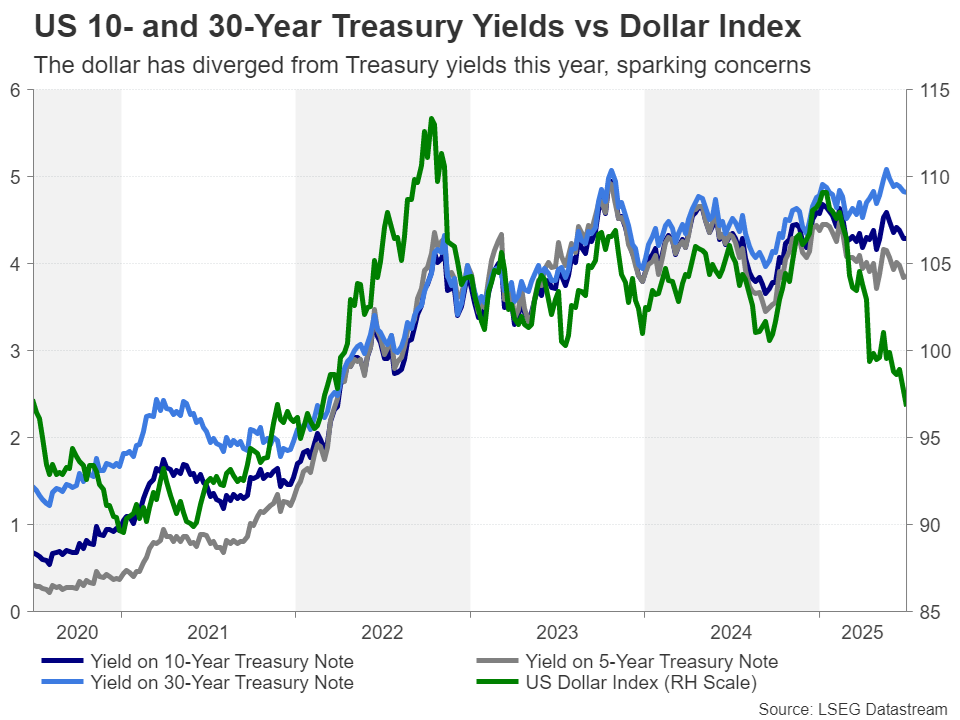

The US dollar index (DXY) just had its worst first six months of the year in more than half a century, losing over 10% against a basket of currencies. This closely watched dollar gauge, which measures it against six other major currencies – the euro, Japanese yen, pound, Canadian dollar, Mexican peso and Swedish krona – is currently trading at levels last seen in February 2022 before the Federal Reserve embarked on its aggressive tightening campaign.

Yet Fed policy remains tight, both in comparison to recent times and relative to other countries. So why is the dollar under so much pressure? Well, US politics has a lot to answer for. President Trump’s trade war has taken the shine off the world’s number one reserve currency, as higher tariffs have stoked fears of stagflation and a global recession.

The de-dollarization effect

But that’s not all. Trump’s protectionist and isolationist stance are seen as marking the end of US exceptionalism. Investors have also been spooked by Trump’s various attempts to undermine the rule of law, bypass the courts and overreach his executive powers as president.

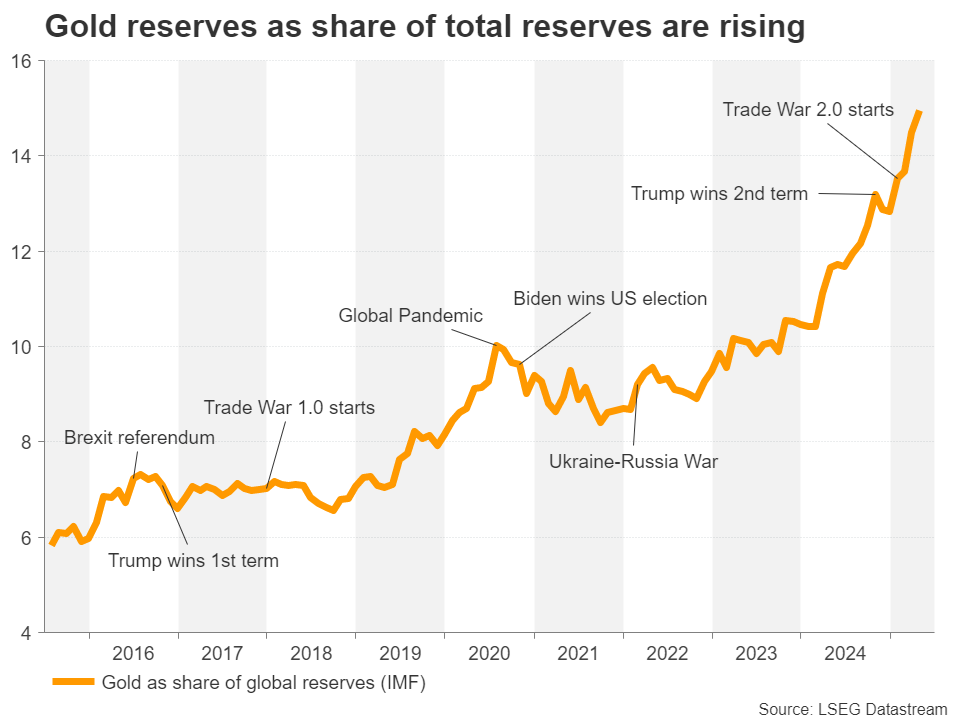

More concerning is the acceleration of de-dollarization by several, mainly emerging market countries, like China and Russia, in an effort to reduce their dependence on the US economy as well as become less vulnerable to sanctions by Washington. The dollar’s share of global reserves has fallen from over 70% at the turn of the century to just under 60% in 2024.

A twin deficit problem

America’s twin deficit problem is another long-running headache for the greenback. The Republican-led Senate just passed a tax and spending bill that looks set to add more than $3 trillion to America’s debt pile. And with investors not hopeful that Trump’s trade policies will slash the country’s massive trade deficit, the dollar is looking like a risky bet right now.

This “risk premium” of Trump’s presidency can be seen quite clearly when looking at the divergence between the US dollar and Treasury yields. The dollar has been in freefall since January, initially tracking the decline in yields. But US yields started to edge up once Trump launched his “Trade War 2.0”, as investors priced in fewer Fed rate cuts on the expectation that higher tariffs will revive inflation. Trump’s radical policies have also dented demand for Treasury bonds, further driving yields higher.

However, despite some jitters in the bond market, it doesn’t appear that demand for US bonds is about to fall off a cliff and Treasury yields have retreated from their recent highs as bond prices have risen. This underscores the perceived low risk of the US defaulting on its debt despite the recent developments.

Are stablecoins coming to the Dollar’s rescue?

One factor potentially helping US yields to stabilize is the recent surge in stablecoins, which is likely fuelling demand for Treasuries. Most stablecoins that are pegged to the dollar require their issuers to hold a certain reserve of US Treasuries, and this is also supportive of the dollar. But this carries its own risks, for example, in the event that issuers need to liquidate a large portion of their holdings, yields could spike higher.

Nevertheless, aside from the 12-day war between Israel and Iran that sparked a flight to safety, primarily towards the dollar’s way, it’s been unable to catch a break this year. Many investors remain deeply bearish about the US currency, even with the tariff war de-escalating significantly in recent weeks.

Trade deals may not offer much hope to Dollar bulls

A crucial test is coming up on July 9 when the 90-day delay of the reciprocal tariffs is set to expire. Trump’s big gamble to renegotiate better trade terms can only go two ways: the US reaches deals with its key trading partners or there’s enough progress to extend the pause, or, the US fails to agree to any substantive trade deals and reciprocal tariffs are reimposed.

In the first scenario, which is what the markets are betting, trade deals would end the uncertainty regarding future tariffs and in most cases, import duties won’t exceed the universal rate of 10% introduced on ‘Liberation Day’. The Fed has already said that it can overlook the inflation impact of the universal tariffs, as it’s likely to be a one-off temporary increase on goods prices.

Essentially, the upside risks to inflation would recede under this scenario, paving the way for the Fed to resume its rate cuts, and thereby pressuring the dollar. What’s significant here is that the Fed would be unpausing at a time when many other central banks are nearing the end of their easing cycle. Hence, why many investors have turned so bearish on the dollar.

Is stagflation inevitable?

In the second scenario, the absence of trade deals would raise the prospect of tariffs rising significantly above the 10% universal levy on imports from major trading countries, risking a flare up in US inflation. The Fed has already stated that if trade tensions were to escalate again, inflation would be its main priority rather than supporting the labour market.

This would inevitably give rise to stagflationary conditions, where interest rates are kept high to keep a lid on inflationary pressures even as the economy struggles to grow or enters an outright recession.

Historically, currencies don’t tend to benefit from comparatively higher interest rates during periods of stagflation as the benefits are offset by the negative outlook on the economy, making the case for a bearish dollar.

However, this isn’t the only worst-case scenario for the dollar. It’s also possible, although not very likely, that stagflation can’t be avoided even in the situation where trade deals are struck, as the US economy continues to experience sticky price pressures. There are some worries that the Trump administration’s tough crackdown on migrants will generate labour shortages just as the economy is slowing down, pushing up wages, and in turn, inflation.

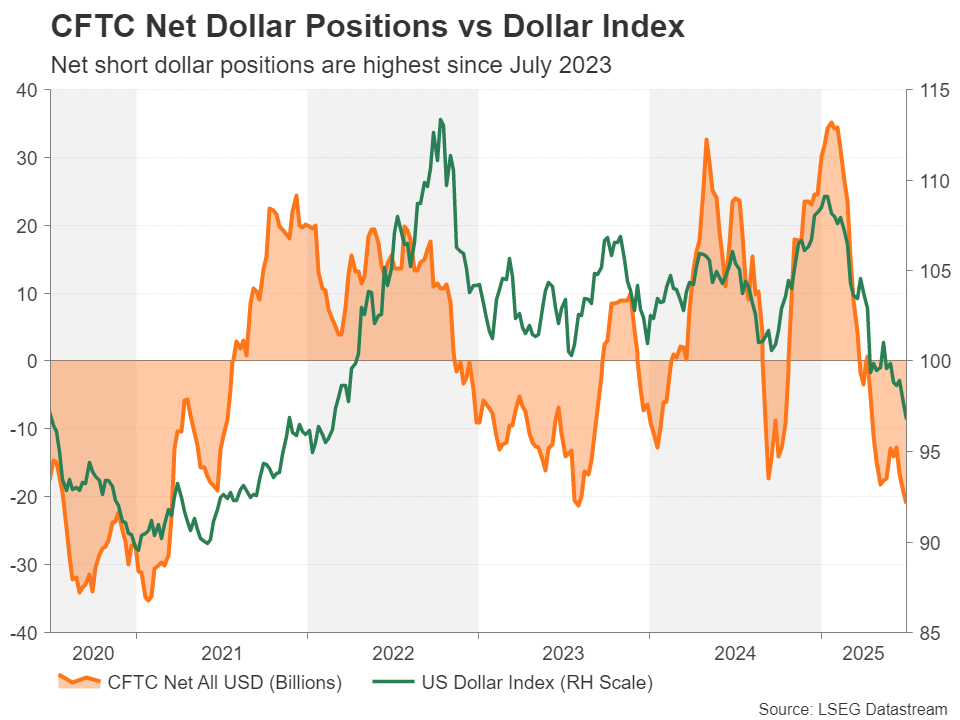

Dollar net short positions highest since 2023

So, it’s an all-round bearish picture for the dollar, whichever way the trade war plays out. The key question now is, how much lower can the dollar go? Large traders are the most bearish on the dollar since July 2023 according to CFTC data, suggesting that the downtrend may be nearing its end. Although historically, the net short positions don’t look too overcrowded.

From a purely technical perspective, the dollar index is displaying some signs of bottoming out, but only in the daily timeframe. In the weekly timeframe, which provides a more longer-term view, the rebound signals are much weaker and there could be a further downward wave to come before it reaches extremely oversold conditions, as the 50-day moving average (MA) is on path for a death cross with the 200-day MA. If the index were to suffer another round of selling, it could go as low as 94.60.

Dollar devaluation may be part of Trump’s plan

The risk going forward for traders who are waiting for a trend reversal will be trying to differentiate between a short squeeze brought on by short covering, and a genuine rebound. The scale of the dollar’s pullback makes it vulnerable to a short squeeze episode, potentially creating a false breakout.

At the same time, those investors who are overly bearish need to consider the fact there are several countries that a too weak dollar would cause significant problems for their own economies. Export-dependent economies such as the Eurozone, Japan, China and South Korea could struggle if the dollar index were to weaken beyond the 90.0 level, potentially prompting some intervention from their part.

Should the greenback continue to slide, it will be interesting to see whether the White House will try to talk up the currency at any point, or keep pressing the Fed to lower interest rates, amid speculation that the Trump administration is deliberately targeting a weaker dollar.

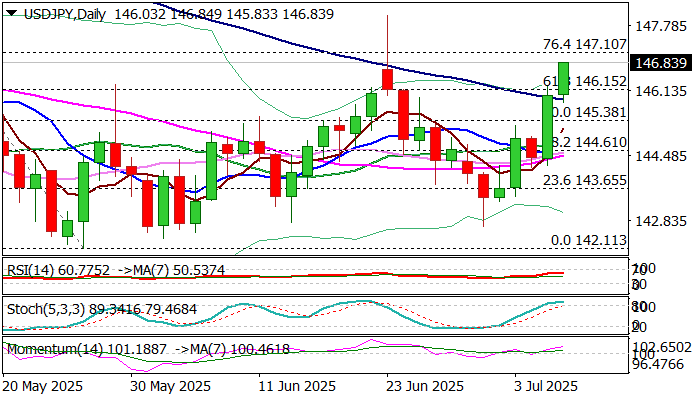

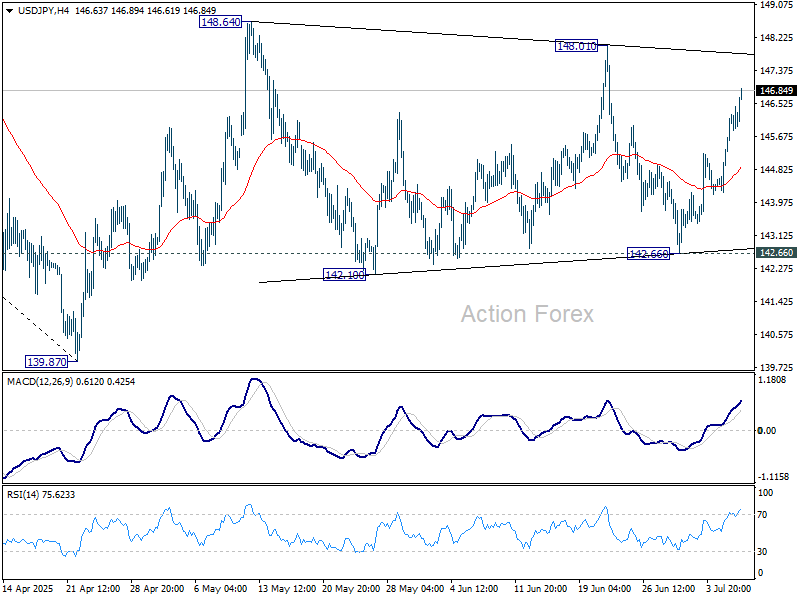

USD/JPY: Japanese Yen Remains Under Increased Pressure

Japanese yen fell across the board, with the recent weakness being sparked by President Trump’s decision to impose a 25% tariffs on imports from Japan.

Yen suffered the biggest losses against US dollar and Australian dollar, after the Australia’s central bank surprised markets on decision to keep interest rates on hold.

USD JPY hit new two-week high, as strong rally extends into second consecutive day (up 1.6% since Monday’s opening).

Monday’s list and close above top of daily cloud generated bullish signal, which was boosted by today’s surge through next pivotal barriers at 145.91 (100DMA) and 146.15 (Fibo 61.8% of 148.64/142.11 downtrend.

Daily studies improved (14-d momentum bounced from the centreline and MA’s 10/20/55/100) turned to bullish setup, although overbought stochastic warning that bulls may face headwinds on approach to next targets at 147.00/10 (round-figure / Fibo 76.4%).

Some technical easing should be anticipated, but mainly as positioning for further advance, as long as fundamental conditions remain unchanged and negative for yen.

Broken 100DMA (145.91) should ideally hold, with extended dips to stay above cloud top (145.54) and keep bulls in play.

Firm break of 147.00/10 to open way towards 148.02 (June 23 spike high) and unmask key short-term barrier at 148.64 (May 12 peak).

Res: 147.10; 147.67; 148.02; 148.64.

Sup: 146.15; 145.91; 145.54; 145.20.

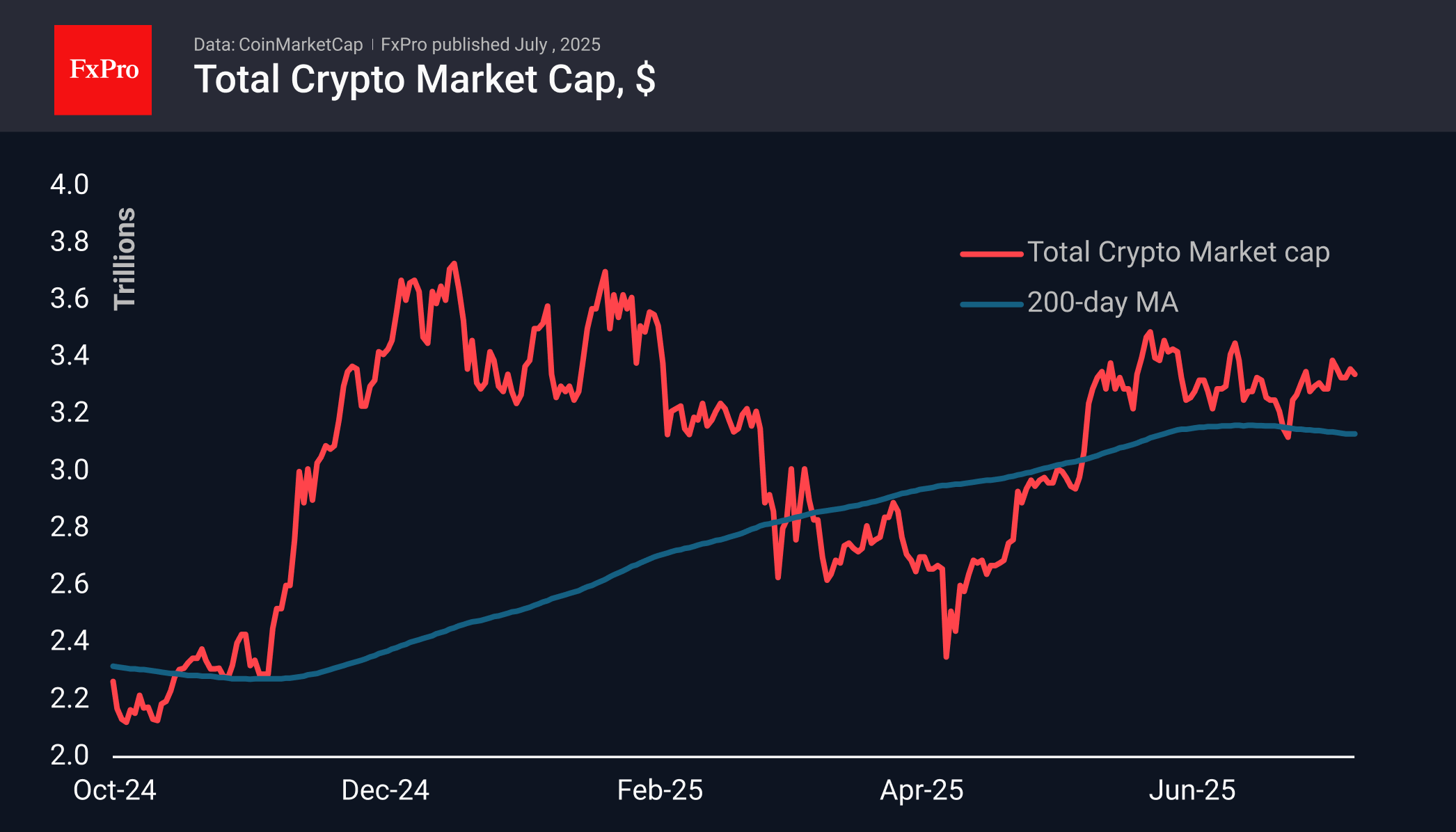

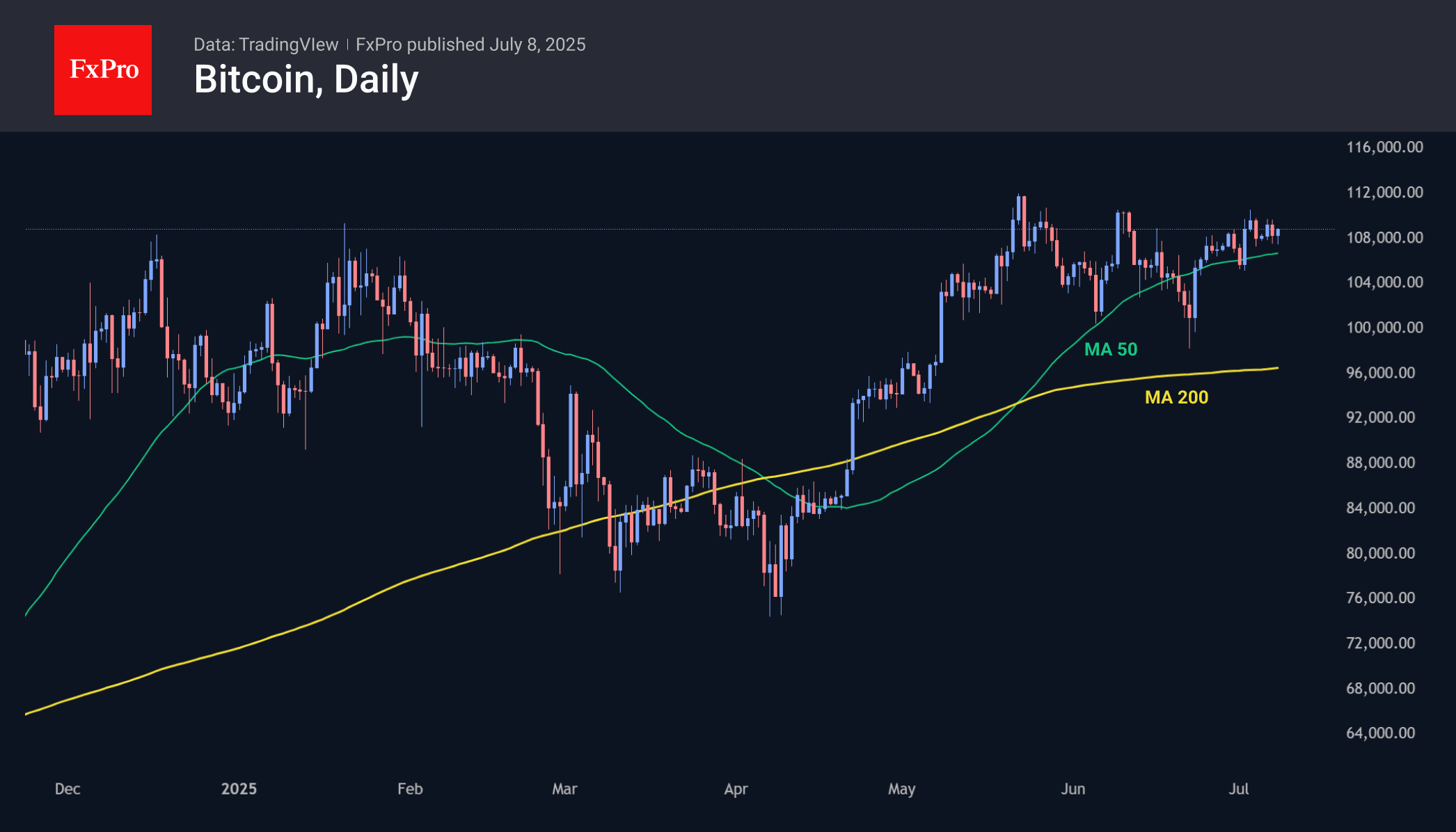

Crypto Market Continues to Rise, Stumbling Along the Way

Market Picture

The crypto market capitalisation retains its weekly growth of approximately 1.8%, losing about 0.6% over the last 24 hours to $3.35 trillion. This is another round of buyer indecision at high levels, even though declines were actively bought up. At the same time, capitalisation continues to move away from its 200-day moving average, indicating continued bullish sentiment.

Bitcoin is hovering near $108.5K. Another attempt to develop growth last week resulted in increased sales, pushing the price back to the 50-day moving average. However, this line is an important medium-term support level, attracting buyers. On the other hand, last week’s activity confirmed that sales are picking up as the price approaches $110K, pushing the price down. Buyers are quickly letting off steam, making the market too nervous.

News Background

According to CoinShares, global investment inflows into crypto funds fell 2.5 times last week to $1.042 billion. Investments in Bitcoin increased by $790 million, Ethereum by $226 million, Solana by $22 million, XRP by $11 million, and Sui by $2 million.

Cryptocurrency ETFs saw inflows for the 12th consecutive week, bringing total assets under management to a new all-time high of $188 billion. The moderation of inflows into BTC suggests that investors are becoming more cautious as the asset approaches its historical highs, CoinShares notes.

According to The Block, Bitcoin’s on-chain activity and implied volatility have fallen to their lowest levels in nearly two years, despite the asset approaching historic highs.

Key indicators of activity in the cryptocurrency market point to the onset of a ‘summer lull,’ Glassnode notes. Trading volumes are at their lowest level in a year and continue to fall. A noticeable increase in the value of assets held by Bitcoin holders signals the risk of sell-offs in the event of a change in market sentiment.

The UAE authorities have denied reports that they are issuing ‘golden visas’ to cryptocurrency investors. Previously, the TON Foundation presented a programme for obtaining a 10-year UAE ‘golden visa.’ To participate, investors were offered to invest $100,000 in Toncoin (TON) and pay a fee of $35,000.

Sunset Market Commentary

Markets

Japanese yields for a second day straight surged around 10 bps at the very long end of the curve. The 30-year bond yield is now up 20 bps since the start of the new week and just 13 bps shy of the record-high (3.2%) seen mid-May. Investors are turning nervous ahead of the July 20 elections in the Japanese Upper House of parliament. PM Ishiba is already running a minority government after snap elections last year and his approval rates are low (which by the way also helps explain Japan’s staunch stance in the US trade talks). Losing the Upper House elections could further strip the ruling coalition of its powers. To win voters over, markets fear another dose of stimulus at a time of already unsustainable public finances. The Japanese case serves as a reminder for the rest of the world, be it the UK, US or Europe and is already overshadowing the trade theme again. All three regions see the long end of the curve underperforming, the UK taking the lead. The fiscal situation in the country is getting a lot of market attention with the October budget being the next key event. Chancellor Reeves’ faces a potential £30bn hole that investors fear can only be found by changing (ie. loosen) the set of self-imposed fiscal rules. And as it happened, the UK’s fiscal watchdog (Office for Budget Responsibility) today flagged the “unsustainable” outlook in its annual fiscal risk report. It warned for a rapidly rising debt burden amid an aging population pushing up health care and pension spending and mounting climate and geopolitical risks. Adding to the problem of supply is waning demand from pension schemes. The 30-yr gilt yield adds 7 bps today with the 1998 high seen in May now just 20 basis points away. US rates add between 1.4 and 4.5 bps in a bear steepener. The 30-yr, currently 4.96%, is suddenly aiming for 5% again. And in Germany, raters add 5+ bps with the 30-yr tenor being 10 bps shy of a 14-yr high. The rest of the curve also shifts a couple of basis points higher too though. This could be the result of the EU and US potentially closing in on a trade agreement. Politico reported yesterday of a US proposal for a universal 10% (ie the floor) tariff with some exceptions here and there. Such a deal would be on the better side of expectations. It also lowers (or even removes) the already questionable need for a last ECB rate cut markets are currently pricing in, hence the near-parallel curve shift today. In any case, the general extension of the tariff deadline from July 9 to August 1 (USTS Bessent last week referred to an even later date on Labour Day, Sep 1) raises chances of finding common ground one way or another. The chair of the council of economic advisors, Miran, said there could be more trade deals by the end of the week.

The Japanese yen underperforms major global peers on currency markets. Japan was slapped by a 25% tariff as president Trump raises the pressure on a country that dug in for electoral motives. USD/JPY marches higher towards 146.65. EUR/JPY moves beyond a final resistance at 171.56 ahead of the July 2024 record high (175.43). The Aussie dollar is on the other side of the FX spectrum. AUD/USD rebounds to 0.654. The RBA unexpectedly stood pat on rates this morning (3.85%) over the risk that some CPI components may be above-forecast. Governor Bullock did say it is a matter about timing, not direction. An August cut is almost fully priced in. In between we find some muted moves in EUR/USD (unchanged around 1.1715). Rising risk premia weigh on sterling, pushing EUR/GBP higher north of 0.86.

News & Views

CPI consumer price inflation in Hungary in June rose 0.1% M/M and 4.6% Y/Y (was 0.2% and 4.4% in May). The outcome was close to expectations. The Hungarian central bank’s (MNB) core inflation estimate fell from 4.8% Y/Y to 4.4%. The bank indicated that both headline and core inflation were in line with its June inflation forecast. The increase was primarily due fuel prices as they decreased to a lesser extent than in the previous month. The MNB also indicated that price and margin restriction measures from the government had a significant inflation-reducing effect. The greatest effect was due to the price margin cap on food prices but the effect on household goods, which came into effect in May, also fully appeared. In addition, voluntary price restrictions by banks and telecoms are also holding down inflation. Annual inflation of tradables slowed to 2.5% from 2.9%. Annual inflation of market services was 0.4% M/M but still rose at 6.7% Y/Y. With inflation still holding well above the 3.0% +/- 1.0% target range of the MNB, today’s data justify the MNB indicating that policy will have to remain at the current restrictive level (6.5%) for some time to come. The forint trades little changed just below the EUR/HUF 400 level.

US: Small Business Optimism Falls Modestly in June

The NFIB's Small Business Optimism Index fell 0.2 points to 98.6 in June, coming in on-par with market expectations.

Four out of ten subcomponents deteriorated on the month, four improved, and two remained unchanged. The largest declines came from the share of businesses reporting current inventory levels as too low (down 6 points to -5%) and expectations for higher real sales over the second half of the year (down 3 points to 7%). A silver lining was the share of firms reporting higher real sales in the current quarter improved (up 4 points to -22%). Expectations for the economy to improve in the second half of the year declined (down 3 points to 22%).

The net share of businesses planning to increase employment rose 1 point to 13%. The share of firms with unfilled job openings rose 2 points to 36%. Quality of labor concerns were unchanged in June, with 16% of business owners identifying this as their top business problem.

The net share of firms currently increasing employee compensation rose 7 points to 33%, while the net share planning to do so over the next three months fell 1 point to 19%. The share of businesses 'raising' average selling prices rose 4 points to 29% while the share of those 'planning’ to raise average selling prices also rose 1 point to 32% - a 15-month high.

Key Implications

Small business confidence remained steady in June at relatively subdued levels as uncertainty remained elevated. The number one concern for small businesses continued to be taxes, as Congress worked to pass the One Big Beautiful Bill Act (OBB) and prevent the end of year tax hike resulting from the expiration of the 2017 Tax Cuts & Jobs Act. With the OBB now signed into law, concerns related to tariffs are likely to return as a top-of-mind concern for small businesses.

It is likely that tariffs have begun to apply upward pressure to selling prices, with the share of small businesses currently raising prices or planning to do so continuing to rise. For the broader economy, we have not yet seen the increase in the producer price index filter through to consumer prices, but as small businesses typically have thinner profit margins it may be the case that the higher costs cannot be forestalled in their transmission to consumers. With many of the reciprocal tariff rates announced in recent days appearing to be unchanged relative to April 2nd, trade uncertainty is likely to remain elevated through the new August 1st deadline.

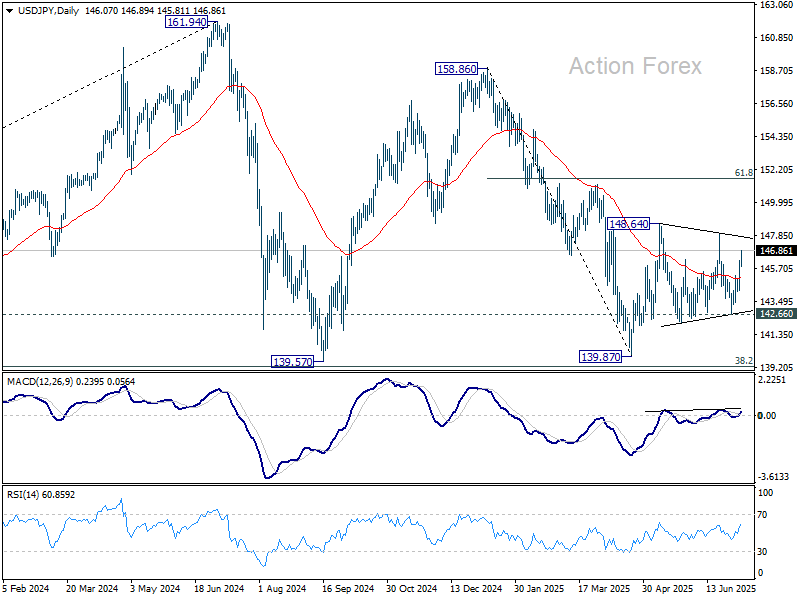

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 144.73; (P) 145.48; (R1) 146.83; More...

USD/JPY's rebound accelerates higher today but after all, it's still bounded in range of 142.66/148.01.On the upside, firm break of 148.01 resistance will resume the rise from 139.87 to 61.8% retracement of 158.86 to 139.87 at 151.22. However, break of 142.66 will bring deeper fall back to retest 139.87 low.

In the bigger picture, price actions from 161.94 (2024 high) are seen as a corrective pattern to rise from 102.58 (2021 low). There is no clear sign that the pattern has completed yet. But still, strong support is expected from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound.

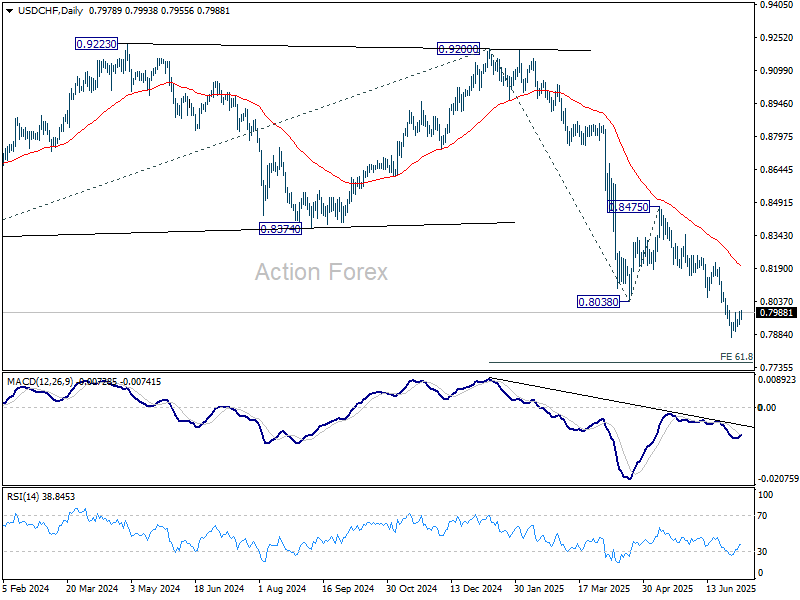

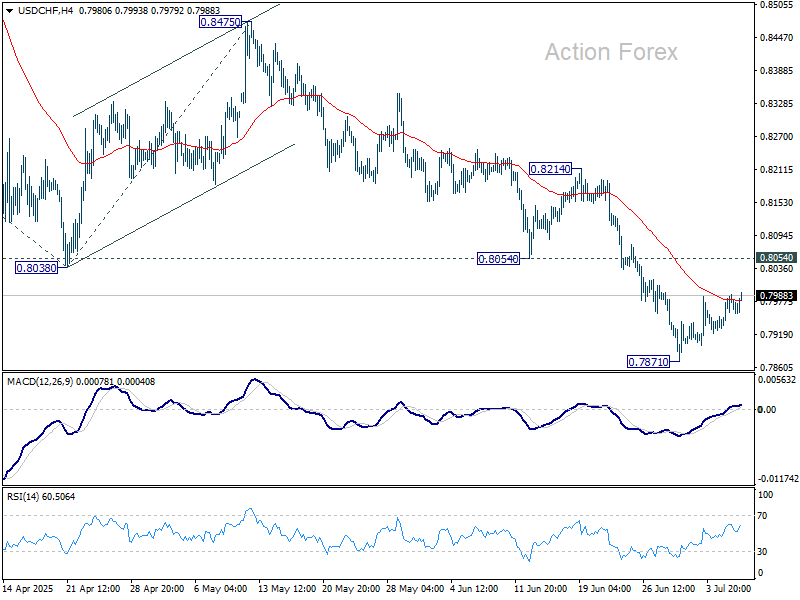

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7948; (P) 0.7970; (R1) 0.8003; More….

USD/CHF's consolidation from 0.7871 is extending and intraday bias stays neutral. Stronger recovery cannot be ruled out, but upside should be limited by 0.8054 support turned resistance to bring another fall. Below 0.7871 will extend the larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757. Firm break there will pave the way to 100% projection at 0.7313 next.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8475 resistance holds.