Sample Category Title

Bracing for Impact as Tariffs, Trade Talks Collide

European stocks trade higher on optimism that a trade deal will be announced very soon, and that tariffs applied to European exports to the US will be around 10%. That’s why the Stoxx 600 extended gains above the 50-DMA, though optimism remains largely concentrated in Europe. Elsewhere, the news is far less reassuring.

First, hopes of an extension to the current tariff pause—which ends today—were dashed after Donald Trump threatened that the August 1st deadline will be final, with no further extensions. Second, he slapped a 50% tariff on copper and announced that pharmaceuticals will face 200% tariffs within a year. The news sent COMEX copper futures to a record high, while copper prices on other platforms like India’s MCX dropped, on expectations that surplus supply would shift to alternative markets.

A 50% tariff will inevitably add to inflationary pressures, which had only just begun to level out. Later today, Federal Reserve (Fed) minutes are expected to confirm once again that officials believe aggressive tariff policies could stoke inflation in the second half of the year and limit the Fed’s ability to provide support to the US economy—even if that support isn't urgently needed given the resilience of US jobs data. That said, mass deportations are underway—and intensifying. A recent Dallas Fed study predicts that deportations could subtract 1 percentage point from US GDP and increase inflation by 0.16 to 0.21 percentage points.

In summary, Trump is sowing the seeds of higher inflation—and higher debt. To keep debt-to-GDP in check, the US would need to post strong growth, which may prove unrealistic. Consumer spending, a major driver of the US economy, is already showing signs of strain and revival of industrial production (the new American dream) may not fill in the gap as rapidly. For instance, the first few hours of Amazon’s Prime Day sales were 14% weaker than a year ago. Many sellers warned they would be unable to offer significant discounts due to tariff pressures—except for Amazon’s own products, which may be flying off the shelves at attractive prices for one last time, as inventories built up in anticipation of turmoil begin to dwindle.

In this environment, inflation-protecting assets look increasingly appealing. Companies with the ability to pass on price increases to clients—such as those in consumer staples, utilities, and healthcare—are strong inflation hedges. Homebuilders could also perform well if they can raise home prices faster than input costs rise. And of course, metals themselves are a natural hedge in a commodity-led inflationary environment. In this context, SPDR’s Metals and Mining ETF has recovered its early-2025 dip and is now approaching its record high from last November. The UK’s FTSE 100, rich in mining stocks, trades just a few points below its own ATH. However, Australian miners like BHP and Rio Tinto are under pressure this morning, as 50% tariffs could weigh on revenues—depending on how much cost absorption is required, and how demand responds to higher prices.

Interestingly, gold—which had been a top hedge against tariff risks—is losing steam. While the revival in tariff tensions might normally support the yellow metal, gold has slipped below its 50-DMA and is consolidating losses this morning.

Meanwhile, the US dollar—one of the biggest victims of Trump’s trade war—is recovering, even as the rest of the G10 complex comes under pressure. The EURUSD is testing the 1.17 support, Cable is nearing the 1.35 psychological level, and the kiwi held steady after the Reserve Bank of New Zealand (RBNZ) left rates unchanged—as expected—while leaving the door open to potential cuts in future meetings. The USDJPY surged past 147 amid escalating trade tensions with the US. The Nikkei remains under pressure near 40,000. Also in Japan, long-end yields are spiking, which could pose a threat to the recent global risk rally—as discussed yesterday—and is also dragging long-term global yields higher. The US 30-year yield flirted with 5% yesterday, while European yields rose to their highest levels in three weeks. Rising yields and borrowing costs are rarely good news for growth and earnings expectations—if anyone still cares.

In energy, US crude remains capped near its 200-DMA, with rising OPEC output and an uncertain global outlook weighing on appetite near the key resistance at $68.70/bbl. Silver, meanwhile, is consolidating near all-time highs in a bid to catch up with gold. The gold/silver ratio has just slipped below 90, with a move toward 80 needed to return to historical norms. And given that gold bulls appear to be stalling, silver may still have more room to run.

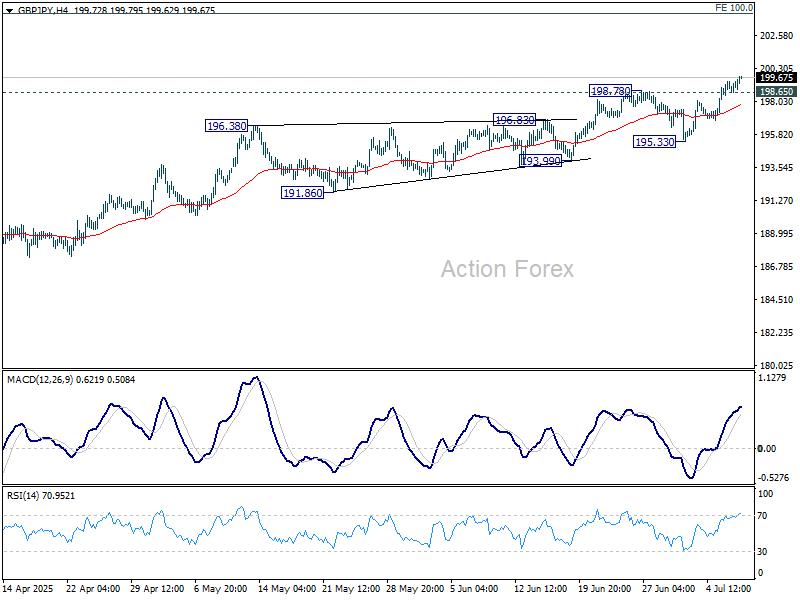

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.66; (P) 199.08; (R1) 199.63; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Firm break of 199.79 resistance will extend the rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14 next. On the downside, below 198.65 minor support will turn intraday bias neutral first. But outlook will continue to stay bullish as long as 195.33 support holds, in case of retreat.

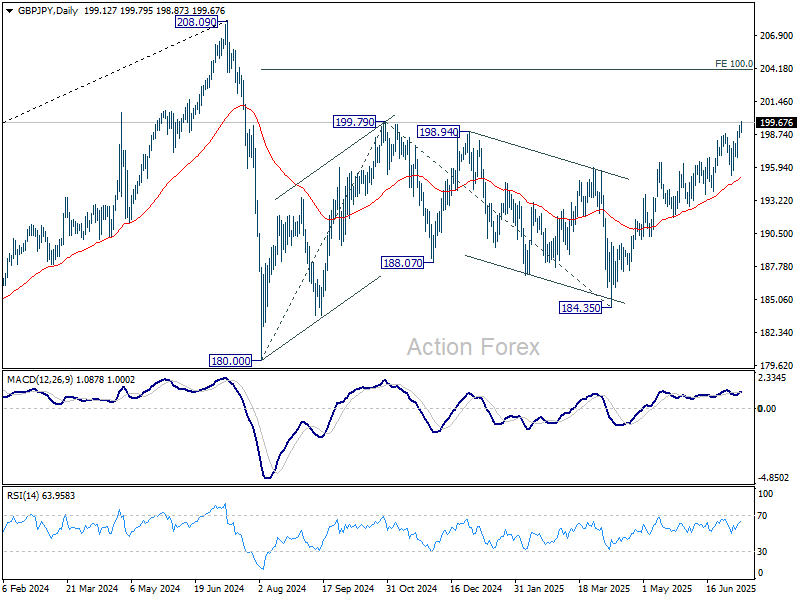

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Dollar Leads as Tariff Windfall Fuels Fiscal Hopes, Copper Soars on Tariff News

Dollar is leading the major currencies this week as investors digest an escalating trade war campaign from Washington. While steep tariffs typically raise concerns about disruption to global supply chains and demand, the Trump administration is clearly framing tariffs as a tool not only for reshoring production but also for offsetting revenue losses from recent tax cuts. That has introduced another dimensions to market interpretation, including the prospect of higher fiscal receipts even amid slower global growth.

Treasury Secretary Scott Bessent said Tuesday that the US has already collected USD 100B in tariff revenue this year and is on track for USD 300B by end-2025. That revenue projection has changed the narrative for some, who now view tariffs not just as inflationary trade barriers but also as sources of budget support. The broader economic impact remains uncertain—likely a mix of stagflationary forces—which helps explain why most Fed officials are still signaling caution over the pace and scale of monetary easing.

Markets will turn to FOMC minutes from June’s meeting for clarity. While the minutes are unlikely to shift the firm market consensus that the Fed will hold rates steady this month, they may shed light on the internal division within the Committee—especially whether dovish shifts from Governors Christopher Waller and Michelle Bowman were already emerging at that stage. For now, futures pricing continues to favor a cut in September, but confidence in additional moves this year has softened.

In the currency space, Aussie is second only to Dollar this week, buoyed by the RBA’s surprise decision to hold rates. The Swiss Franc is also firm as risk hedging remains elevated. At the other end, Yen is the weakest major, pressured by Tokyo’s inclusion in Trump’s tariff letters and ongoing concerns over Japan’s export vulnerability. Kiwi lags too, despite mildly recovery following RBNZ’s dovish hold, while Euro is also softer. Sterling and Loonie are trading in the middle of the pack.

On the trade front, US President Donald Trump on Tuesday proposed a 50% tariff on copper imports, adding to a list of escalating sectoral duties. Commerce Secretary Howard Lutnick said the administration is aiming to bring copper production back home, similar to earlier moves on steel and aluminum. Trump also teased potential 200% tariffs on pharmaceutical imports, reinforcing the administration’s aggressive stance heading into the August deadline.

Copper prices surged to fresh record highs on the news. But technically, copper may be nearing short-term exhaustion after hitting a 100% projection of 4.0018 to 4.9042 from 4.9039 at 5.8063. Upside potential should be limited for now. Though, any retreat should be contained by 5.1340 resistance turned support to bring rebound, to set the range for some sideway trading.

In Asia, at the time of writing, Nikkei is up 0.27%. Hong Kong HSI is down -0.89%. China Shanghai SSE is up 0.38%. Singapore Strait Times is up 0.21%. Japan 10-year JGB yield is up 0.008 at 1.498. Overnight, DOW fell -0.37%. S&P 500 fell -0.07%. NASDAQ rose 0.03%. 10-year yield rose 0.030 to 4.415.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that "If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further."

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.66; (P) 199.08; (R1) 199.63; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Firm break of 199.79 resistance will extend the rise from 184.35 to 100% projection of 180.00 to 199.79 from 184.35 at 204.14 next. On the downside, below 198.65 minor support will turn intraday bias neutral first. But outlook will continue to stay bullish as long as 195.33 support holds, in case of retreat.

In the bigger picture, price actions from 208.09 (2024 high) are seen as a correction to rally from 123.94 (2020 low). The pattern might still extend with another falling leg. But in that case, strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. Meanwhile, decisive break of 208.09 will confirm long term up trend resumption.

Gold Under Pressure — More Losses on the Horizon?

Key Highlights

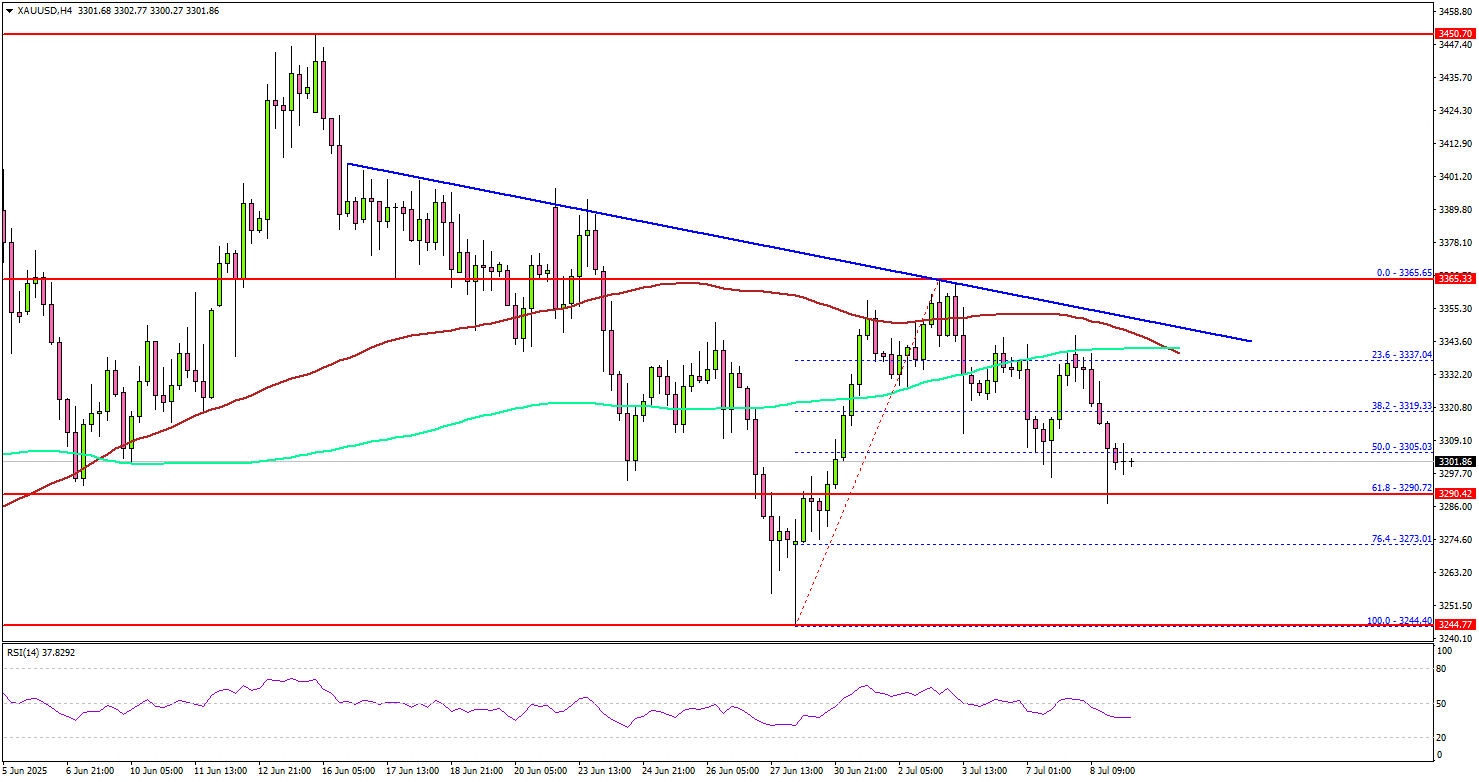

- Gold started a fresh decline from the $3,375 resistance.

- A key bearish trend line is forming with resistance at $3,350 on the 4-hour chart.

- WTI Crude Oil prices could struggle to climb above the $69.25 resistance.

- USD/JPY started a fresh increase above the 145.50 resistance.

Gold Price Technical Analysis

Gold prices failed to extend gains above $3,400 and reacted to the downside. There was a steady decline below the $3,380 and $3,360 support levels.

The 4-hour chart of XAU/USD indicates that the price settled below the $3,350 level, the 100 Simple Moving Average (red, 4 hours), and the 200 Simple Moving Average (green, 4 hours). Recently, there was a correction wave, but upsides were limited above $3,360.

Besides, there is a key bearish trend line forming with resistance at $3,350 on the same chart. On the downside, initial support is near the $3,290 level.

The first key support is $3,280. The next major support is near the $3,272 level. The main support is now $3,245. A downside break below the $3,245 support might call for more downsides. The next major support is near the $3,220 level.

On the upside, immediate resistance is near the $3,350 level and the trend line. The next major resistance sits near the $3,360 level. The main barrier could be $3,380.

A clear move above the $3,380 resistance could open the doors for more upsides. The next major resistance could be $3,400, above which the price could rally toward the milestone level of $3,420.

Looking at WTI Crude Oil, the price is showing signs of a recovery wave but could face hurdles near the $69.25 zone.

Economic Releases to Watch Today

- FOMC Meeting Minutes.

- US Wholesale Inventories for May 2025 (preliminary) – Forecast -0.3%, versus -0.3% previous.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that "If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further."

(RBNZ) OCR: 3.25% – OCR unchanged

The Monetary Policy Committee today agreed to hold the Official Cash Rate at 3.25 percent.

Annual consumers price inflation will likely increase towards the top of the Monetary Policy Committee’s 1 to 3 percent target band over mid-2025. However, with spare productive capacity in the economy and declining domestic inflation pressures, headline inflation is expected to remain in the band and return to around 2 percent by early 2026.

Elevated export prices and lower interest rates are supporting a recovery in the New Zealand economy. However, heightened global policy uncertainty and tariffs are expected to reduce global economic growth. This will likely slow the pace of New Zealand’s economic recovery, reducing inflation pressures.

The economic outlook remains highly uncertain. Further data on the speed of New Zealand’s economic recovery, the persistence of inflation, and the impacts of tariffs will influence the future path of the Official Cash Rate.

If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further.

Summary Record of Meeting – July 2025

Annual consumers price index inflation remains within the Monetary Policy Committee’s 1 to 3 percent target band. While inflation is expected to approach the top of the target band in Q2 and Q3 of 2025, spare productive capacity and declining core inflation are consistent with headline inflation returning to the midpoint over the medium term. The Committee noted that the outlook for medium-term inflation pressures in New Zealand has evolved broadly in line with the May MPS projections. The pace of recovery in domestic consumption and investment remains weak, reflecting heightened caution in the face of global policy shocks and uncertainty. But strong export prices and recent monetary policy easing are expected to support the economic recovery.

Global economic growth is expected to weaken

Global growth is expected to slow over the second half of 2025, reflecting the uncertain consequences of trade protectionism. However, the Committee noted that fiscal expansion in the euro area, the US, and China may counter some of the downside risks.

On balance, increased protectionism is expected to result in less inflationary pressure for New Zealand. While tariffs are likely to be inflationary in the US, forecasts for inflation in China and emerging Asia have been lowered recently, partly reflecting an appreciation in some Asian currencies.

The Committee discussed recent developments in global financial markets. Weaker investor sentiment for US dollar assets has contributed to rising term premia in the bond market and depreciation of the US dollar. Rising term premia in the US, and global fiscal expansion, have contributed to higher long-term bond yields in other advanced economies.

Domestic financial conditions have continued to ease

The Committee noted that, despite global factors, domestic financial conditions are evolving broadly as expected. Mortgage and deposit interest rates have continued to decline, reflecting a lower OCR, strong bank liquidity, and soft credit growth. The average interest rate on the stock of mortgages is expected to continue to decline in coming quarters as more mortgage holders refix at lower one to two year fixed-term interest rates. Close to half the stock of mortgages is due to reprice during the September and December 2025 quarters.

Domestic economic activity is expected to gradually recover

In aggregate, GDP growth over the December and March quarters was stronger than expected, reflecting a pick-up in household consumption and business investment. But higher frequency indicators suggest weaker than expected growth in April and May. Taken together, this suggests the current level of economic activity is broadly consistent with the Committee’s judgement in May. Overall, there remains significant spare capacity in the New Zealand economy. Higher export prices and monetary policy easing should contribute to a gradual recovery in economic activity.

Inflation is expected to rise towards the top of the target band in mid-2025

Annual consumers price index inflation increased to 2.5 percent in the March 2025 quarter. Inflation is expected to increase further in the June and September quarters, towards the top of the MPC’s inflation target band. The near-term increase in inflation is due to a pick-up in food prices and elevated administered price increases. Inflation is expected to fall over late 2025 and return to around the mid-point of the target band by early 2026, as significant spare capacity in the economy further reduces domestic inflation pressures.

Risks to the global outlook remain elevated

The Committee discussed several key risks around the economic outlook. There remains significant uncertainty about global tariff policy, and how this will affect the global economy. As outlined in the alternative scenarios in the May MPS, recently announced tariffs could result in higher or lower medium-term inflation pressure for New Zealand than assumed in the central scenario. The costs of trade could increase by more than assumed as global supply chains adapt to trade barriers, increasing inflationary pressure. Conversely, policy uncertainty could lower global investment, and trade diversion could lower import prices by more than currently assumed, lowering inflation pressure.

The Committee noted the risk that large economic policy shifts overseas, and concerns about sovereign risk, could result in additional financial market volatility and increased bond yields. Conflict in the Middle East and Ukraine has contributed to volatility and heightened uncertainty around global energy prices. A re-escalation in conflict would present upside risk to energy prices. However, increased oil supply from OPEC could mitigate this risk.

The domestic economic outlook remains uncertain

The Committee noted uncertainty about the speed with which the domestic economy would continue recovering. Some members highlighted that prolonged economic uncertainty might induce further precautionary behaviour by households and firms. Such actions risk becoming mutually reinforcing and weigh on aggregate demand, slowing the economic recovery. The recent weaker than expected higher frequency indicators could be consistent with this.

In contrast, other members emphasised stronger household consumption and business investment in the March quarter, along with higher surveyed investment intentions in the June quarter, as possible signals of a recovery in interest rate sensitive parts of the economy.

The Committee noted that there were upside and downside risks to the medium-term outlook for inflation. With higher inflation expected in the near term, some members underlined a risk that this could lead to more persistently elevated price- and wage-setting behaviour. Members also discussed the risk that administered price inflation could remain high for a prolonged period. However, other members emphasised the large negative output gap, moderate wage inflation and job insecurity, and continued weakness in house prices. Together with the broad-money-to-nominal-GDP ratio being well below its pre-pandemic trend, this could provide confidence that inflationary pressures remain contained.

The Committee agreed to hold the OCR at 3.25 percent

The Committee discussed the options of cutting the OCR by 25 basis points to 3 percent or keeping the OCR on hold at 3.25 percent at this meeting.

The case for lowering the OCR at this meeting highlighted weak near-term growth momentum and the risk of prolonged weakness in economic activity from excess caution by households and businesses in the face of economic uncertainty. This could lead to downward pressure on medium-term inflation. Some members emphasised that further monetary easing in July would provide a guardrail to ensure the recovery of economic activity, whilst being consistent with price stability.

The case for keeping the OCR on hold at this meeting highlighted the elevated level of uncertainty, and the benefits of waiting until August in light of near-term inflation risks. Some members emphasised that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve. It would also allow more time to observe developments in the global economy.

On Wednesday 9 July, the Committee reached consensus to hold the OCR at 3.25 percent.

Subject to medium-term inflation pressures continuing to ease in line with the Committee’s central projections, the Committee expects to lower the Official Cash Rate further, broadly consistent with the projection outlined in May.

Attendees

Members of MPC: Christian Hawkesby (Chair), Bob Buckle, Carl Hansen, Karen Silk, Paul Conway, Prasanna Gai

Treasury Observer: Dominick Stephens

MPC Secretaries: Chris Bloor, Evelyn Truong

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

A Look at US Indices & US Dollar After the Latest Drama from Trump Administration

Markets seem to be shrugging off of the latest dramatic deadline pushback from the Trump Administration – after menacing Japan, South Korea and other Asian countries for 25% tariffs in a letter sent yesterday that sent markets shaking, the renewed TACO trade is in getting priced in.

The July 9th deadline recently got pushed back again to August 1st, allowing trade negotiations to continue.

Markets got scared yesterday and the Dow particularly suffered from the headlines, closing down 0.94% from its open.

Participants learn from their mistakes, and knowing with who they are treating, they are starting to put less emphasis on all the headlines.

US President Donald Trump is the author of the 1987 The Art of the Deal publication, reminding that words and talks are just a part of negotiation schemes.

Sentiment is currently mixed and the current session is not showing any signs of concrete direction – The Dow opened down small, and the Nasdaq and S&P 500 are up small from the latest pushback.

Only the US Dollar is appreciating from the most recent tariff headwinds, leaving markets waiting again.

A look at US Indices & Dollar Index intra-day charts after the latest Tariff Drama

Nasdaq 100 1H Chart

Nasdaq 1H Chart, July 8, 2025 – Source: TradingView

The Nasdaq is starting to form a local top as sentiment goes from Ecstatic to Confusion.

Last week was all about renewed hopes for conclusion of deals and better US Data, leading to new all-time highs for the Tech-focused index.

The 1H 50-period Moving Average is appearing as immediate Resistance and the current open is mixed, tilting slightly bearish with the RSI in the selling region

Levels to place on your charts:

Resistance Zones:

- Current ATH (CFD) – 22,922

- Current main resistance 22,900

- 1H MA 50 - 22,750

Support Zones:

- Immediate Pivot – 22,700 Region (above = bullish, below = bearish)

- 1H MA 200 – 22,615

- Current Support Zone 22,450

- Previous ATH Support Zone 22,250

S&P 500 1H Chart

S&P 500 1H Chart, July 8, 2025 – Source: TradingView

Very similar reactions for the S&P 500, as sellers are starting to come in from the failure to breach the 6,300 key level.

One thing to spot for current sentiment and probabilities of newer trends is the reaction to the immediate pivot (level detailed just below).

One thing that tilts the technicals to slightly bearish is the break of the past week's upward trendline, similar to the Nasdaq – Keep an eye on this one.

Levels to place on your charts:

Resistance Zones:

- Current Resistance around 6,300

- Current ATH (CFD) – 6,290

- 1H MA 50 – 6,245

Support Zones:

- Current Pivot 6,220

- 1H MA 200 – 6,206

- Current Support Zone around 6,130

Dow Jones 1H Chart

Dow Jones 1H Chart, July 8, 2025 – Source: TradingView

The Dow is looking a bit more concretely bearish after failing to surpass its 45,060 all-time highs while forming a double-top at 44,910.

Some buyers have just stepped in but the Daily picture is still close to unchanged – Markets are preparing for more headlines as the msot recent drama from the US Administration just provided more uncertainty, once again.

Levels to place on your charts:

Resistance Zones:

- Current Resistance 44,800 to 45,060

- Current highs – 44,910

- 1H MA 50 – 44,544

Support Zones:

- 1H MA 200 44,175

- Current Pivot 44,000 Zone (+/- 100 points)

- 43,000 Main Support Zone

Dollar Index 1H Chart

Dollar Index 1H Chart, July 8, 2025 – Source: TradingView

Although trading close to overbought levels, the US Dollar is starting to look technically less bearish than it was in the past weeks – particularly as the DXY recently touched the target of its Weekly, massive Head and Shoulders (lows around 96.50).

Prices just broke out from the Main descending channel as uncertainty and still heavily one-sided selling positioning is leading to position covering.

Watch for either a reversal upwards, a concrete breakout can be expected above the 98.00 psychological handle – or rangebound action at current levels.

Levels to place on your charts:

Resistance Zones:

- Immediate Pivot 97.60 to 97.80

- Current Resistance 98.00 Zone

- Main Resistance 99.20 to 99.40

Support Zones:

- 1H MA 50 97.25

- Current Low Consolidation Support 97.00 Zone

- 2025 Lows around 96.50

Safe Trades!

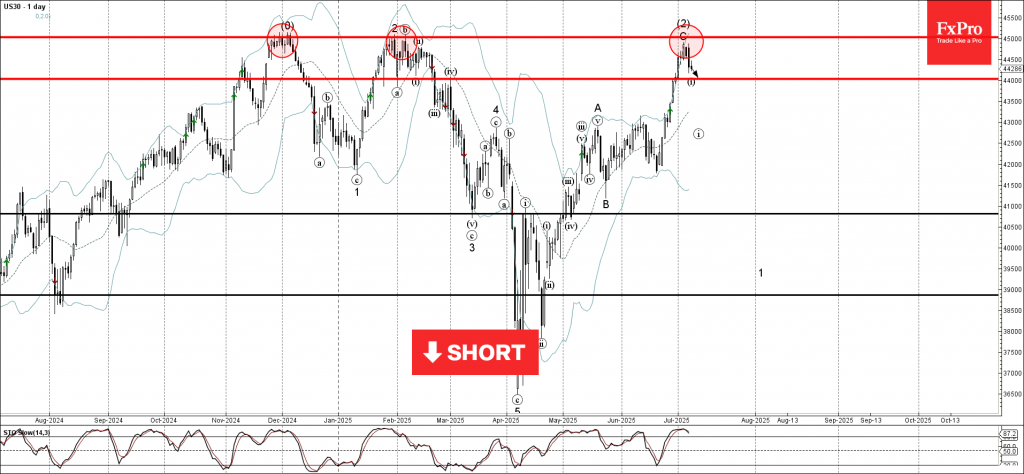

Dow Jones Wave Analysis

Dow Jones: ⬇️ Sell

- Dow Jones reversed from long-term resistance level 45000.00

- Likely to fall to support level 44000.00

Dow Jones index recently reversed down from the resistance zone located between the long-term resistance level 45000.00 (which has been steadily reversing the price from the end of November) and the upper daily Bollinger Band.

The downward reversal from this resistance zone stopped the previous medium-term ABC correction (2) from the start of April.

Given the strength of the resistance level 45000.00 and the overbought daily Stochastic, Dow Jones index can be expected to fall to the next support level 44000.00 (target price for the completion of the active impulse wave i).

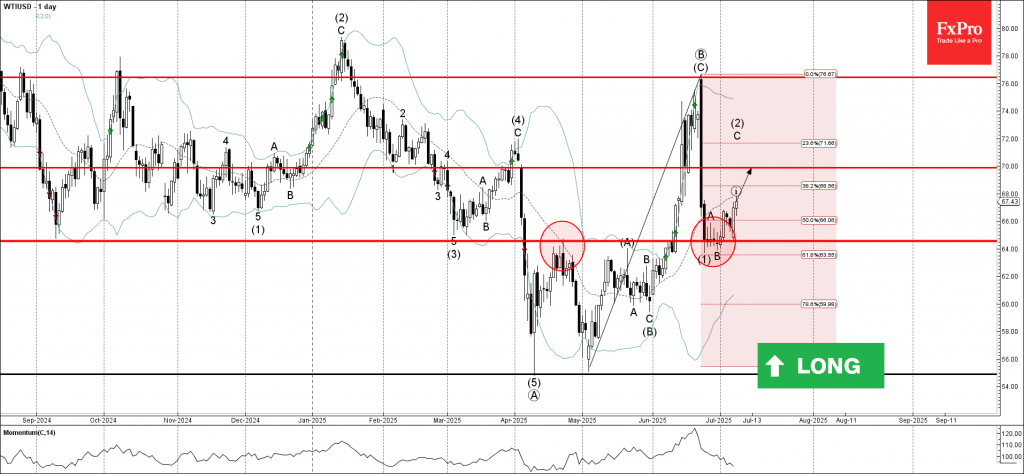

WTI Crude Oil Wave Analysis

WTI crude oil: ⬆️ Buy

- WTI crude oil reversed from the support zone

- Likely to rise to resistance level 70.00

WTI crude oil recently reversed up from the support zone located between the key support level 64.55 (former resistance from the end of April), the lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from May.

The upward reversal from this support zone started the active medium-term ABC correction (2).

WTI crude oil can be expected to rise to the next round resistance level 70.00 (target price for the completion of the active impulse wave i).