Sample Category Title

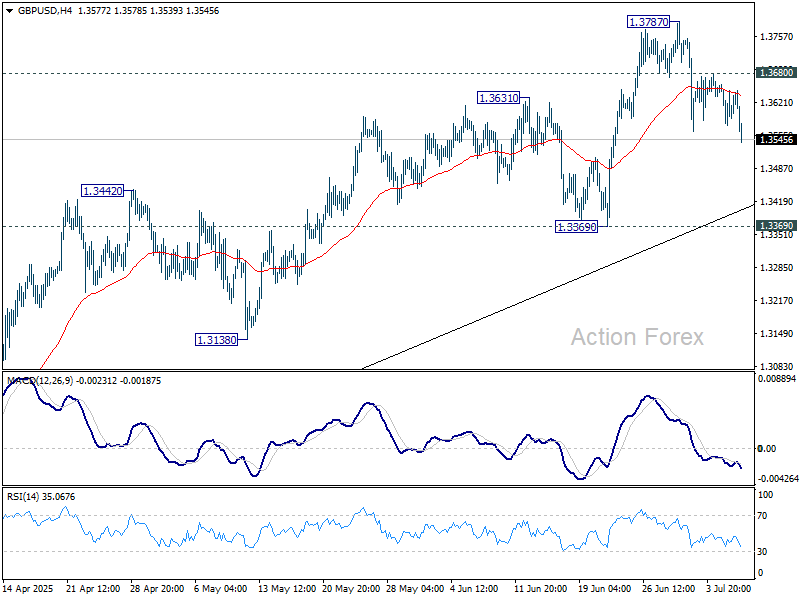

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3563; (P) 1.3614; (R1) 1.3652; More...

GBP/USD's correction from 1.3787 continues today and deeper fall might be seen. But downside should be contained by 1.3369 support to bring rebound. On the upside, above 1.3680 minor resistance will bring retest of 1.3787. Firm break of 1.3787 will resume larger up trend to 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2985) holds, even in case of deep pullback.

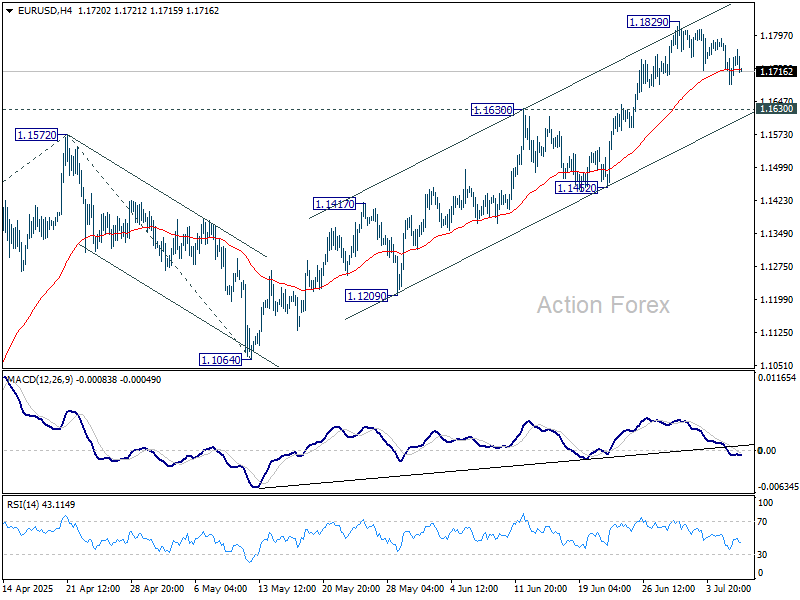

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1667; (P) 1.1729; (R1) 1.1770; More...

EUR/USD's correction from 1.1829 continues today and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Markets Unfazed by Trump Tariff Letters; Kiwi Outshone by Aussie ahead of RBNZ Hold

Global equity markets traded cautiously and remained stable on Tuesday, showing limited reaction to escalating US trade threats. Major European indexes moved in narrow ranges following modest gains in Asia, while US equity futures stayed flat. The restrained response suggests markets are neither complacent nor panicked as they assess the credibility and timing of new tariff risks.

Investor nerves were tested when US President Donald Trump confirmed that imports from 14 countries—including Japan, South Korea, Malaysia, and Indonesia—will face new tariffs ranging from 25% to 40%, starting August 1. However, the absence of immediate action and Trump’s ambiguous tone helped calm markets. “The deadline is firm, but not 100% firm,” he told reporters, suggested that the US remains open to renegotiation.

It's also noted that pushing the implementation date to August—beyond the previously expected July 9 deadline—helped ease fears of an imminent cliff edge. This delay gives key US trade partners more time to negotiate or soften the impact, explaining why risk sentiment has remained broadly resilient so far.

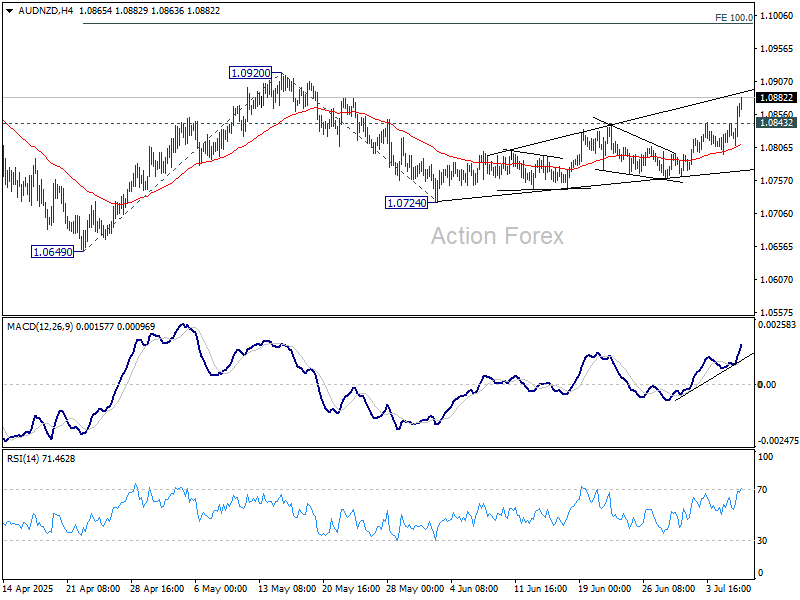

In the currency markets today, Australian Dollar outperformed sharply, gaining across the board after RBA defied expectations and held the cash rate steady at 3.85%. Speaking after the decision, RBA Governor Michele Bullock stressed that the hold was a matter of timing rather than a change in direction. She said the board preferred to wait for the full Q2 CPI report before confirming that inflation is heading sustainably toward target. Bullock emphasized that monetary policy remains well-positioned to respond if global conditions deteriorate further.

Overall, Kiwi followed Aussie as the second-best performer, with Loonie also firming. Yen lagged alongside Sterling and Dollar, while Swiss Franc and Euro were mixed.

Focus now turns to RBNZ, which is expected to keep its official cash rate unchanged at 3.25%. Recent inflation data has been mixed, and policymakers are looking for clearer signals before moving again. Holding now gives the RBNZ space to reassess in August with updated projections.

Technically, Aussie is currently outperforming Kiwi for the moment. AUD/NZD's rise from 1.0724 accelerated higher today and remains on track to retest 1.0920. Firm break there will resume whole rally from 1.0649 and target 100% projection of 1.0649 to 1.0920 from 1.0724 at 1.0995. Nevertheless, break of 1.0843 minor support will mix up the outlook and turn bias neutral first.

In Europe, at the time of writing, FTSE is up 0.07%. DAX is up 0.07%. CAC is down -0.33%. UK 10-year yield is up 0.051 at 4.643. Germany 10-year yield is up 0.05 at 2.695. Earlier in Asia, Nikkei rose 0.26%. Hong Kong HSI rose 1.09%. China Shanghai SSE rose 0.70%. Singapore Strait Times rose 0.40%. Japan 10-year JGB yield rose 0.052 to 1.490.

RBA skips July cut, prefers to wait a little more for clarity

RBA held its cash rate target at 3.85%, opting not to deliver the widely expected 25bps cut. The decision, passed by a 6-3 majority, reflected cautious optimism as the central bank noted more balanced inflation risks and a still-resilient labor market. However, the Board stopped short of declaring victory on inflation and flagged considerable uncertainty in the domestic and global outlook.

In its statement, RBA said it could afford to “wait for a little more information” to ensure inflation is sustainably heading toward its 2.5% target. The Board remains concerned about both demand and supply-side uncertainty, particularly in light of volatile global trade policy. RBA stressed that monetary policy remains "well-positioned" to respond quickly if conditions deteriorate.

RBA also issued a measured warning on the risks stemming from U.S. tariffs and global trade policy shifts, noting that while extreme outcomes may be avoided, the uncertainty itself could weigh on demand. Financial markets have rebounded on hopes of compromise, but the RBA highlighted the risk that firms and households could delay spending amid the policy fog.

Australia's NAB business confidence rises to 5, conditions rebound to 9

Australia’s business sentiment improved sharply in June, with NAB Business Confidence rising from 2 to 5, its highest trend level in over a year. Business Conditions surged from 0 to 9 after weakening for five straight months. The rebound was broad-based, with trading conditions jumping from 5 to 15, profitability returning to positive territory from -5 at 4, and employment conditions edging up from to 3.

On the pricing side, signals were mixed. Labour cost growth eased slightly from 1.6% to 1.5% (quarterly equivalent), while purchase costs rose from 1.2% to 1.5%. Final product price growth ticked up from 0.5% to 0.6%, although retail price growth slowed to 0.6%, hinting at easing consumer price pressures despite supply-side stickiness.

NAB’s Gareth Spence said the data suggest momentum may be picking up into the second half of 2025. “While we know the monthly survey can be volatile, the hope is at least some of these trends will be sustained,” he noted, calling the jump in both confidence and conditions a positive surprise amid ongoing global uncertainty.

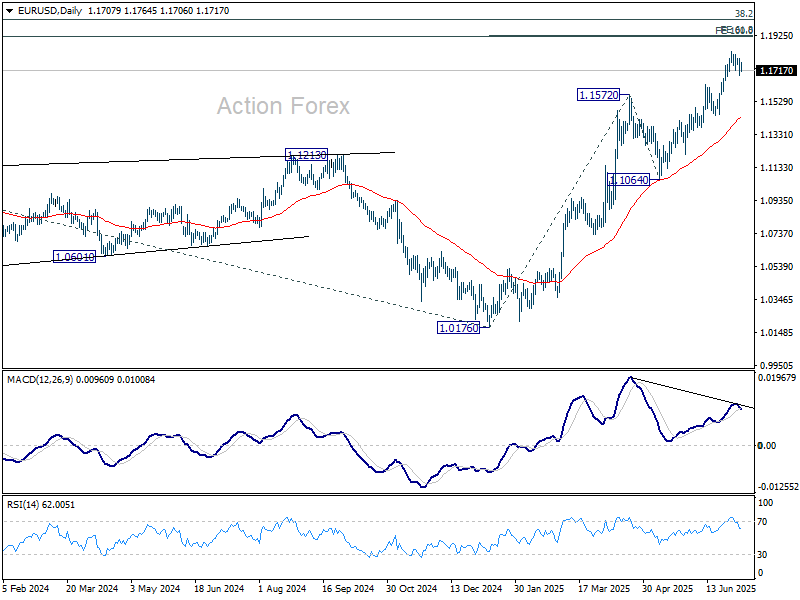

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1667; (P) 1.1729; (R1) 1.1770; More...

EUR/USD's correction from 1.1829 continues today and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Trump Tariff Dilemma, EU Trade Deal and DAX Back Above 24000

Asian stock markets remained steady despite the latest update on US President Donald Trump's tariff plans. On Tuesday, the dollar stayed strong, and oil prices dropped.

In the US, stock prices fell after Trump sent letters to 14 countries, including Japan and South Korea, announcing much higher tariffs on imports. However, the start of these tariffs has been delayed until August 1.

Asian Market Wrap

Most Asian stock markets went up as President Trump signaled he’s open to more trade talks, easing concerns after imposing heavy tariffs on several countries.

South Korea’s stock market jumped over 1.4%, and Japan’s Nikkei-225 index rose 0.2%. The MSCI regional stock index edged up 0.1% after small ups and downs earlier in the day. The South Korean Won got stronger, while the Dollar index dropped 0.2%. The Euro gained value after reports that the U.S. offered the EU a deal with a 10% tariff limit.

In Japan, 30-year government bond yields kept climbing. Meanwhile, Australia’s currency surged after the central bank surprised everyone by keeping interest rates unchanged.

European Open

Global stock markets were mostly steady or slightly higher on Tuesday as investors reacted calmly to the latest update on U.S. President Donald Trump's tariff plans.

On Monday, Trump sent letters to 14 countries, including major Asian trade partners like Japan and South Korea, announcing much higher tariffs on imports to the US.

However, the market response has been more cautious this time, unlike the sharp drops seen three months ago on "Liberation Day." This is because many expect countries to work on trade deals with the US before the new August 1 deadline.

In Europe, the STOXX 600 index stayed mostly unchanged, while the euro rose 0.4%. Reports suggest the EU won’t receive a letter about higher tariffs and could finalize a trade deal by Wednesday.

The EU aims to secure a temporary trade deal with the U.S. this week, which would lock in a 10% tariff rate past the August 1 deadline while working on a long-term agreement. Meanwhile, Bulgaria is set to take the final step to join the Eurozone as its 21st member next year, with EU finance ministers meeting on Tuesday to approve its application.

On the FX front, the euro hit a one-year high against the yen and was last up 0.4% on the day at 171.745.

The euro rallied against the dollar as well, rising 0.4% to 1.1735, partially recouping Monday's 0.67% loss.

The Australian dollar was the star performer on Tuesday, jumping over 1% after the Reserve Bank of Australia surprised markets by keeping interest rates unchanged. It was last up 0.8% at 0.6545.

The New Zealand dollar rose 0.38% to 0.60245, while the British pound increased 0.3% to 1.3642.

China's yuan briefly dropped to a two-week low against the dollar due to renewed worries about US tariffs. However, it bounced back after major state-owned banks stepped in to support the currency.

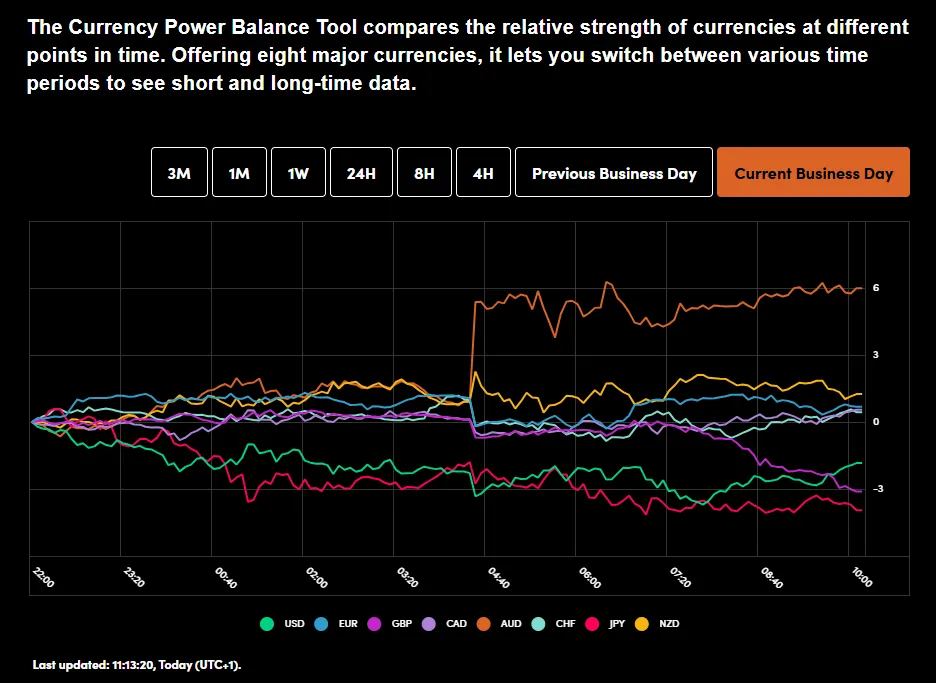

Currency Power Balance

Source: OANDA Labs

Looking at commodities and Oil prices have recovered following a gap down over the weekend. Markets appear to be hopeful that trade deals may spur on a bigger rally despite OPEC + further unwinding production cuts.

Gold has also rallied following a brief foray below the 3300/oz handle. This morning Gold is a bit more tentative trading around 3320/oz which is some way off the Asian session highs around 3346/oz.

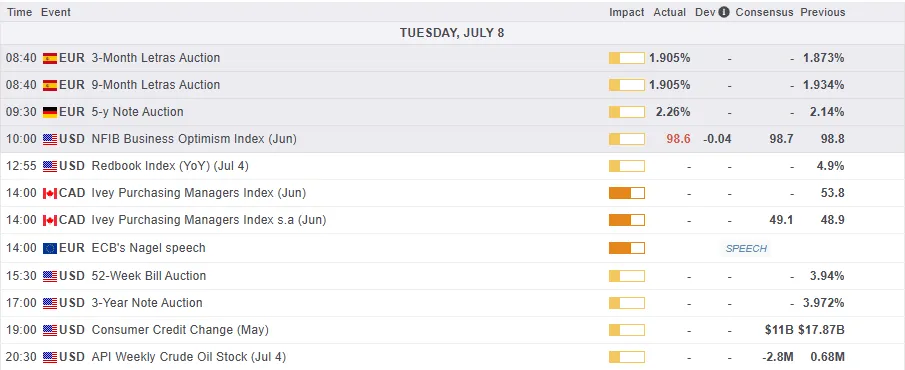

Economic Data Releases and Final Thoughts

Looking at the economic calendar, it remains a quiet one. There are no high impact data releases from the EU, UK or US ahead today.

Thus I am expecting tariff and trade deal chatter to dominate matters today and for the majority of the week ahead.

We will have some comments from ECB policymaker Nagel later today while we will also get a glimpse at the NY Fed inflation expectation number.

Inflation expectations may paint a picture for market participants especially after US Treasury Secretary Scott Bessent said the US will experience growth without inflation, something which until now has been a sticking point.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - DAX Index

From a technical standpoint, the DAX has been moving higher this morning on optimism that the EU will strike a deal with the Trump administration.

The EU is looking to secure a temporary deal which would cap tariffs at 10% past the August 1 deadline while working on a long-term agreement.

This appears to have given EU stocks a boost this morning and this comes despite a drop off in both German imports and exports.

The DAX has broken above the 24000 handle with the next key resistance at 24330. A break above this level may lead to further gains especially if the proposed 10% tariff is agreed between the EU and US.

DAX Daily Chart, July 8. 2025

Source: TradingView.com (click to enlarge)

Support

- 24000

- 23727

- 23471

Resistance

- 24330

- 24500

- 24750

EUR/USD Declines as Markets Await US Tariff Developments

The EUR/USD pair dropped to 1.1746 on Tuesday, with the US dollar holding a slight edge before correcting. The greenback faced pressure after Donald Trump announced new tariffs on 14 countries that have yet to secure trade agreements with the US.

Among the affected nations were major exporters such as Japan and South Korea, which will face a 25% duty on their goods starting 1 August.

Trump also signed an executive order delaying the deadline for reciprocal tariffs from 9 July to 1 August, granting more time for negotiations.

Additionally, he warned of a further 10% tariff on countries aligned with the anti-American BRICS policy, coinciding with the bloc’s summit in Brazil.

Earlier in the week, the US dollar had strengthened as trade tensions eased, and expectations of a Federal Reserve rate cut diminished. A robust June labour market report weakened the case for imminent monetary easing, with markets now all but dismissing the likelihood of a July rate reduction.

Technical Analysis: EUR/USD

H4 Chart:

On the H4 chart, EUR/USD saw an upward wave to 1.1747, with a consolidation range now forming around this level. A potential expansion to 1.1760 is possible, followed by a likely decline to 1.1650, which would set the boundaries of this range. If the pair breaks above the range, gains could extend towards 1.1885. Conversely, a downside break may trigger a fall to 1.1611, with further downside potential towards 1.1570. This outlook is supported by the MACD indicator, where the signal line remains below zero, indicating a sharp downward trend.

H1 Chart:

On the H1 chart, the pair continues consolidating around 1.1717, with an expected upward expansion to 1.1777. However, the bullish momentum appears exhausted, and a downward wave to 1.1700 could materialise at any moment, potentially extending to 1.1611. The Stochastic oscillator reinforces this view, with its signal line below 80 and trending downward towards 20.

Conclusion

The EUR/USD remains under pressure amid uncertainties over tariffs and shifting expectations for the Fed’s rate outlook. Technically, the pair shows limited upside potential, with key support levels at 1.1650 (H4) and 1.1611 (H1). A break lower could accelerate declines, while an upward breakout may signal a short-term recovery.

Australian Dollar Strengthens Following RBA Decision

Today, the AUD/USD pair experienced a spike in volatility. According to ForexFactory, analysts had forecast that the Reserve Bank of Australia (RBA) would cut interest rates from 3.85% to 3.60%. However, the market was caught off guard as the central bank opted to keep rates unchanged.

The RBA stated the following:

→ It remains cautious in its inflation outlook and awaits further evidence confirming that inflation is on track to return to the 2.5% target.

→ The decision to hold the rate was made by a vote of six to three — a rare instance of a split opinion among committee members.

The initial market reaction to the RBA’s unexpected move was a sharp appreciation of the Australian dollar. However, this was followed by a quick pullback in the minutes that followed (as indicated by the arrows).

Technical Analysis of the AUD/USD Chart

Since early July, price action in AUD/USD has been forming a descending channel (marked in red). In this context:

→ Today’s sharp rally and subsequent retracement underscored the significance of the upper boundary of the channel;

→ The pair tested a previously broken ascending trendline (the lower line of the blue channel);

→ Although the price briefly rose above the 0.65450 level, this area may now act as resistance going forward.

There is a possibility that, as forex trading unfolds throughout the day, AUD/USD could retreat towards the median line of the descending channel. Such a move could be interpreted as follows:

→ The initial reaction to the RBA decision may have been premature;

→ Selling pressure persists, which might trigger a move towards the support zone near 0.64850.

Looking ahead, the trajectory of AUD/USD in July 2025 will be largely influenced by developments surrounding a potential trade agreement between the United States and other countries, including Australia.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Asian Stocks Climb Despite New US Tariff Threats; AUD Rebounds, Gold Stabilizes

Despite US President Trump issuing 14 new tariff letters on Monday, 7 July, Asian stock markets defied expectations. Unlike the sharp sell-off following the 1 April “Liberation Day” tariff announcement, regional indices rallied, many reaching three- to five-day highs in today’s Asian mid-session.

Most Asian stock markets rally despite fresh US tariff warnings

The market reaction suggests growing scepticism about the White House following through decisively on tariff threats. While the letters outlined tariff rates ranging from 25% to 40% on exports from Japan, South Korea, South Africa, and several Southeast Asian nations (e.g., Malaysia, Thailand, Indonesia, Cambodia, Myanmar, and Laos), Trump extended the 9 July tariff deadline to 1 August and even hinted at a further extension to finalize trade negotiations.

European stock markets outperformed US

Hong Kong’s Hang Seng Index rose 0.7%, and Singapore’s Straits Times Index continued its record-breaking run, climbing 0.6% to an all-time intraday high of 4,057. South Korea’s KOSPI 200 surged 2%, while Japan’s Nikkei 225 edged up 0.4%.

Meanwhile, European stock markets outperformed the US. With Europe spared from the latest round of tariff letters and reports of a possible US-EU trade deal emerging this week, the German DAX gained 1.2%, reaching a four-day high. In contrast, the S&P 500 dropped 0.8%, trimming earlier losses of 1.25%. US equity futures showed mild recovery in Asia, with the S&P 500 and Nasdaq 100 E-minis up 0.1% and 0.2%, respectively.

FX markets mixed as AUD rebounds on RBA Surprise

Currency markets were mixed. The Australian dollar led gains, rising 0.7%, followed by the New Zealand dollar (+0.4%) and the euro (+0.2%), while the Japanese yen weakened 0.1%.

The AUD/USD posted a bullish reversal, reclaiming its 20-day moving average at 0.6520 as support. Although traders had anticipated a 25-bps rate cut by the RBA, the central bank held rates steady at 3.5%, citing trade-related uncertainty and choosing to monitor conditions before acting.

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Start of a potential impulsive bullish sequence for Hang Seng Index

Fig 2: Hong Kong 33 CFD Index minor trend as of 8 July 2025 (Source: TradingView)

The recent 4% minor corrective decline seen on the Hong Kong 33 CFD Index (a proxy of the Hang Seng Index futures) from the 25 June high to the 4 July low is likely to have ended. The Hong Kong 33 CFD Index is now likely to be in the process of undergoing a potential fresh impulsive bullish sequence within its medium-term uptrend phase.

The hourly RSI momentum indicator has shaped a bullish divergence condition as its oversold region and staged a bullish momentum breakout on Monday, 7 July (see Fig 2).

Watch the 23,690 key short-term pivotal support for the next intermediate resistances to come in at 24,270, 24,490, and 24,850.

On the other hand, failure to hold at 23,690 negates the bullish tone for a slide towards the next support at 23,450 (also the 50-day moving average), and only a break below it sees a deeper corrective decline to expose the next intermediate support at 23,060 in the first step.

RBA Split Decision, Opts to Wait Until August

In a decision split 6 in favour, 3 against, the RBA Board decided to wait before cutting rates. It wasn’t a shoo-in to cut, and in the end, the RBA chose caution over decisiveness.

- The RBA Monetary Policy Board defied widespread expectations and kept the cash rate on hold at its July 2025 meeting. The post-meeting statement noted the gradual recovery in private sector demand and a tight labour market as justification for the decision. It also said that the Board judged that it could wait for a “little more information”, which the Governor subsequently clarified included the quarterly CPI and another labour force release.

- In its May minutes, the Board had expressed a preference to be “cautious and predictable” in its conduct of monetary policy. Today it erred on the side of the former. The general tone of today’s post-meeting statement was of a central bank that has not been updating its view of the economy that quickly.

- The decision was split 6–3. In the post-meeting media conference, Governor Bullock emphasised that this was a question of timing, not direction. A majority of Board members simply opted to wait for more information, principally the Q2 CPI release.

- We read the tone of the media conference as flagging that the rate cut is still on for August, provided the trimmed mean inflation rate for June quarter does not surprise too much on the upside. Accordingly, we reinstate the likely timing of the next cut to August, though there is a small chance even this is delayed. We also retain the spread-out timing (November, February, May) of subsequent cuts as being in line with the cautious approach the RBA has flagged.

- At the media conference, the Governor confirmed that, should market pricing again move out of line with what the RBA ends up doing, the RBA will not use an inter-meeting speech to guide market expectations, as this would prejudge the Board’s subsequent decisions.

The RBA Monetary Policy Board has defied market pricing and the great majority of private sector economists’ views (including ours) by opting to keep the cash rate on hold at 3.85%. As we noted when we moved the expected August cut to the July meeting, cutting this month was not the ‘shoo-in’ that markets expected. The RBA has been a reluctant rate-cutter in recent months, especially earlier in the year. Still, the decision to hold is surprising, and the 6–3 split vote shows how finely balanced the decision was. Given the lack of consensus on the Board, the low information content of the post-meeting statement was not that surprising; this was the text a split Board could agree upon.

While votes are unattributed, we think it is unlikely that the external Board members all voted to hold while the Governor, Deputy Governor and new Treasury Secretary all voted to cut. It is more likely that the Governor, Deputy and some external Board members aligned to a staff recommendation to hold, but not all the external members were convinced to wait.

While underlying inflation is now clearly inside the 2–3% target range and headed down, the post-meeting statement chose to highlight the 2.9% year-ended rate for trimmed mean inflation as at the March quarter. More than half the information from this calculation is very stale data from the middle of last year. In the post-meeting media conference, the Governor claimed that other observers were more focused on headline inflation. In our view, this is a misreading of the current debate. Reasonable estimates of the current pulse of trimmed mean inflation – using either the monthly indicator trimmed mean or a shorter-run calculation on the quarterly data than a year-ended percentage change – are noticeably lower than 2.9%.

There is also little sign of an update in the RBA’s read of the economy in the rest of the statement text. The pick-up in private sector demand was again highlighted, even though the RBA had to revise down its near-term consumption forecast in successive SMPs. Weak productivity growth was cited twice despite the vagaries of measurement and the low information value it has for future inflation. In the media conference, the Governor discussed the “conundrum” that productivity growth has been weak and unit labour costs are strong, but inflation is coming down. We would argue that part of the issue has been compositional shifts in measurement, and part of it is that the RBA is over-indexing on the idea that prices are a (mostly constant) markup over costs.

The statement noted that “The Board judged that it could wait for a little more information to confirm that inflation remains on track to reach 2.5 per cent on a sustainable basis.” It is not clear why the currently available information was not enough to make this judgement. In the media conference, the Governor clarified that in five weeks’ time, the quarterly CPI, another monthly labour force release and refreshed forecasts would be available.

The main other lesson from today’s decision is the step change it implies for the RBA’s approach to communication. With the Monetary Policy Board more explicitly central to the decision-making process (in form only – they always were central in substance), the RBA Governor will be unwilling to push back on market pricing in between meetings because they will want to avoid pre-judging what the Board decides, or prejudicing the deliberations, at the next meeting. This means that episodes of the RBA surprising market pricing, as it has done today, will be more common. This is one of the downsides of the RBA Review recommendations. Not only are there fewer inter-meeting speeches by the senior officials now that there is a press conference instead, but those opportunities might also not be used to steer market pricing.

We read the tone of the media conference as flagging that the rate cut is still on for August, provided the trimmed mean inflation rate for June quarter does not surprise too much on the upside. Accordingly, we reinstate the timing of the next cut to August. We also retain the spread-out timing (November, February, May) of subsequent cuts as being in line with the cautious approach the RBA has flagged.

There is a (small) risk that even August is too soon for the RBA, if the CPI surprises on the upside. Our own current nowcast for June quarter is marginally above what their May SMP forecasts seem to imply. The Governor also mentioned that the data might come in slightly above their forecasts.

In addition, the spread-out timing highlights the risk that the RBA will be surprised on the downside by inflation later this year and need to catch up. This adds to the probability that our current base-case of 2.85% ends up being correct, rather than something higher.

Prolongs the Period of Limited Visibility Both for Markets and for Monetary Policymakers

Markets

The US yesterday made a next step in the strategy that it considers necessary to ‘eliminate the Trade Deficit disparity’ with trading partners. The US sent letters to 14 trading partners informing them of new tariffs it will impose on August 1. The tariffs are mostly close to, sometimes slightly lower compared to what was announced at Liberation Day. Some examples. South Africa faces a tariff of 30%, Indonesia 32%, Malaysia 25% and Thailand 36%. Major trading partners Japan and South Korea were both informed of a 25% tariff. They are still involved in trade negotiations, but the US apparently wants to put some pressure for them to make further concessions as this is difficult due to the domestic political context (e.g. July 20 Upper House elections in Japan). Next to sending letters, the US administration also delayed the global new deadline for reciprocal tariffs to August 1. It also warns that if nations decide to raise their tariffs (retaliation) they will again be added to the tariff applied for that country. The EU didn’t receive any letter. Sources suggest that the EU is moving closer to a deal with the US but it aims to reach some exceptions on the baseline 10% and some ad hoc specifications/adjustments to sector tariffs. However, negotiations are still ongoing and an agreement needs the final approval President Trump. Markets apparently basically saw the current move as a ‘delay’ of the July 9 deadline allowing for further negotiations/modifications. De facto this also prolongs the period of limited visibility both for markets and for monetary policymakers including the Fed. In this respect, expectations of Fed policy later this year hardly changed. The market still sees a cumulative 50 bps of rate cuts this year. US yields rose between 1.5 bps (2-y) and 5.4 bps (30-y). The underperformance at the long end of the curve was broad-based, probably partially driven by higher LT Japanese yields. German yields added 2.0/3.6 bps across the curve. US equities dropped after the publication of the first letters, but finished off the intraday lows (S&P 500 -0.79%). Uncertainty on the economic impact for US trading patterns supported the dollar (DXY at 97.48 from 96.96, EUR/USD 1.171 from 1.178; USD/JPY 146.05 from 144.4).

Asian equity markets modestly rebound as investors apparently appreciate room for further negotiations. The dollar eases slightly (DXY 97.36; EUR/USD 1.1738, USD/JPY unchanged near 146). As visibility remains low also for the Fed as long as the trade negations continues, some further technical trading (rather than sustained further gains) might be on the cards for the US dollar. On the interest rate markets we again keep close eye at the long end of the yield curves. The Japan 30-y yield again jumps 9 bps (3.07%) and keeps debt sustainability as a live theme. The market focus will remain on the US trade policy (e.g. news on progress with the EU). The eco calendar again only contains second tier data. The US Treasury will sell $58 bln of 3-y notes.

News & Views

The Reserve Bank of Australia surprised by keeping the policy rate unchanged at 3.85% this morning. Another cut to 3.6% was widely expected. The central bank said inflation broadly moved according to the May forecast but nevertheless spotted some upside surprises “at the margin”. With rates now 50 bps lower than a few months ago and wider economic conditions evolving broadly as expected, the RBA believes it can wait for a little more information (and therefore confirmation) that inflation is sustainably returning to the 2.5% target. And while the outlook remains uncertain, especially regarding trade, the RBA sees private domestic demand recovering and household incomes picking up, in part thanks to a still-tight labour market. Australian swap rates jump more than 12 bps at the front end of the curve, allowing AUD/USD to recover most of the losses incurred yesterday and thereby preserving the upward sloping trend channel. The pair is currently trading around 0.654, up from 0.649 at the open.

UK house prices again failed to grow in June, data from one of the country’s biggest lenders showed. After contracting by 0.3% in May, average housing prices were unchanged last month just shy of £300k. The numbers chime with last week’s findings of the Nationwide Building Society that showed the biggest price drop since early 2023. The housing market struggles to recover amid buyers being hit by a rise in stamp duty in April. Sellers, meanwhile, are flocking to the market with the number the highest in a decade, data from Rightmove revealed, pressuring prices from the supply side.

5-Swing Elliott Wave Sequence in FTSE Supports Bullish Bias

The ongoing rally in the FTSE Index, originating from the April 7, 2025 low, continues to unfold as a five-wave impulse structure within the Elliott Wave framework. This signals sustained bullish momentum. From the April 7 low, wave 1 peaked at 7984.19. Wave 2 pullback followed which concluded at 7599.56. The index then surged in wave 3, reaching 8902.4. The subsequent wave 4 correction manifested as a double three Elliott Wave structure, as evidenced on the 1-hour chart. From the wave 3 peak, wave (w) declined to 8809.91. It was then followed by a wave (x) recovery to 8858.56. The decline in wave (y) reached 8741.4, completing wave ((w)) in a higher degree. The rally in wave ((x)) peaked at 8831.9 before the index resumed lower in wave ((y)). Within this decline, wave (a) ended at 8757.97. Wave (b) ended at 8792.43, and wave (c) concluded at 8706.91, finalizing wave ((y)) of 4.

The FTSE has since turned higher in wave 5, requiring a break above the wave 3 high of 8902.4 to negate the possibility of a double correction. The structure from the wave 4 low is developing as a five-swing sequence, reinforcing the bullish outlook. From wave 4, wave (i) reached 8818.44, wave (ii) corrected to 8726.92, wave (iii) advanced to 8828.16, and wave (iv) pulled back to 8738.99. The final wave (v) concluded at 8837.75, completing wave ((i)) in a higher degree. A wave ((ii)) pullback is anticipated, likely correcting the cycle from the June 26, 2025 low in a 3, 7, or 11-swing pattern before resuming higher, provided the pivot at 8706.91 remains intact. This structure underscores a robust bullish bias, with the index poised for further upside as long as key support levels hold.

FTSE 60-Minute Elliott Wave Technical Chart

FTSE Elliott Wave Technical Video

https://www.youtube.com/watch?v=ViZWtU9bvqs