Sample Category Title

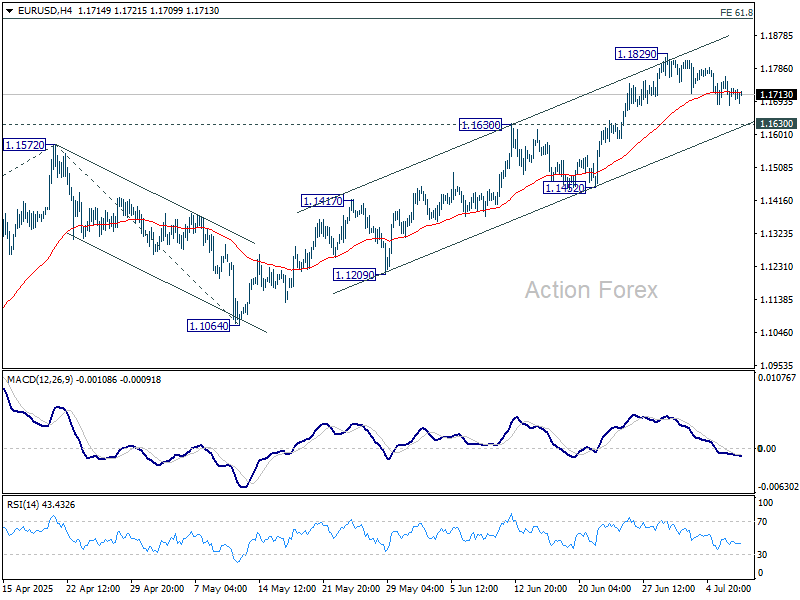

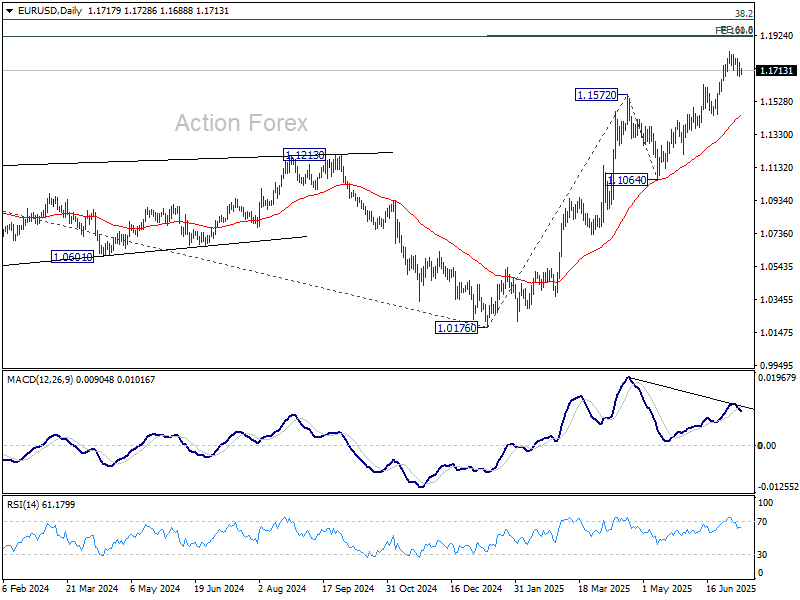

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More...

EUR/USD's consolidation from 1.1829 is still extending and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

Dollar Pauses as Markets Await FOMC Minutes, Overall Action Muted

Activity in the forex market cooled today as traders adopted a cautious stance ahead of June FOMC minutes. With no major surprises expected, the minutes are unlikely to shift current expectations for a Fed hold at the July 30 meeting. That baseline has been reinforced by the latest shift in trade war dynamics, after US President Donald Trump effectively pushed the tariff truce deadline back to August 1.

The new deadline means Fed will be making its next rate decision before key developments on trade materialize, leaving the central bank in the dark on one of the most important macro variables. With clarity on tariffs likely delayed, Fed officials have even more reason to stick with their current wait-and-see approach. The FOMC minutes may still offer insight into how dovish policymakers like Governor Christopher Waller and Michelle Bowman are positioning, but the broad tone is expected to remain cautious.

On trade, Trump said Tuesday evening that at least seven new tariff letters would be issued Wednesday morning, with more to follow later in the day. He also indicated the EU would be informed of its specific tariff rate “probably” within two days, but added that Brussels had grown more cooperative in recent talks.

European Commission President Ursula von der Leyen maintained a guarded tone, reaffirming that the bloc is working in good faith to strike a deal but remains prepared for all scenarios. A Commission spokesperson said talks were advancing and a deal could potentially be reached before the August 1 deadline.

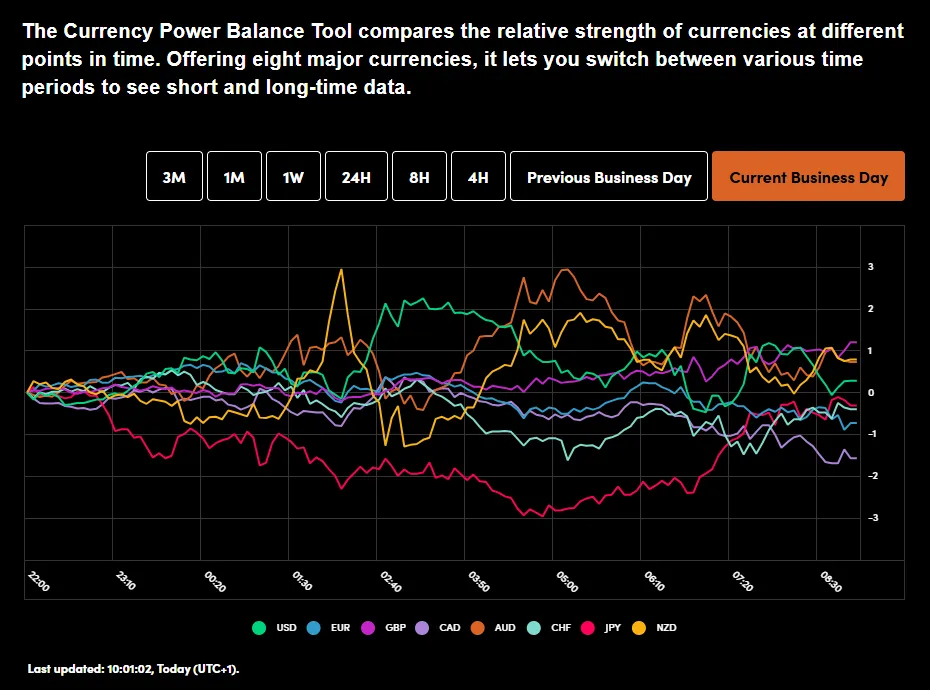

In terms of currency performance, Dollar continues to lead for the week, although it’s struggling to build further momentum, especially against European majors. Swiss Franc and British Pound remain firm, while the Japanese Yen lags sharply. New Zealand and Canadian Dollars are also under pressure, while Euro and Australian Dollar sit in the middle.

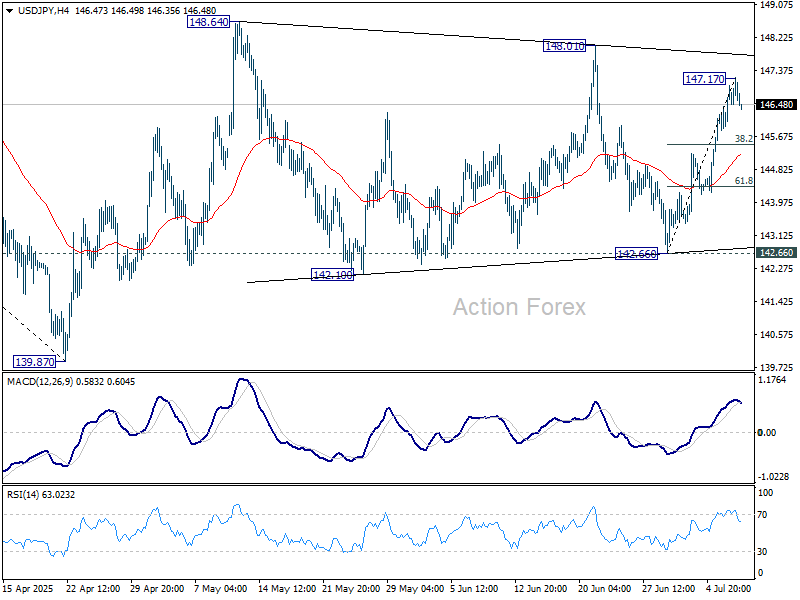

Technically, USD/JPY’s rally from 142.66 appears to be losing steam after hitting 147.17. A short-term pullback is increasingly likely. Recent price action suggests a triangle formation from 148.64, and the next dip may complete that pattern as the fifth leg. Downside would be contained by 61.8% retracement of 142.66 to 147.17 at 144.38. The pair should then be ready to rise through 148.64 to resume the whole rebound from 139.87. Let's see if it unfolds this way.

In Europe, at the time of writing, FTSE is up 0.09%. DAX is up 1.26%. CAC is up 1.32%. UK 10-year yield is down -0.013 at 4.623. Germany 10-year yield is down -0.012 at 2.68. Earlier in Asia, Nikkei rose 0.33%. Hong Kong HSI fell -1.06%. China Shanghai SSE fell -0.13%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.016 to 1.507.

ECB’s Lane: Global uncertainty goes beyond tariffs, includes investment and security risks

ECB Chief Economist Philip Lane said in a speech today that the recent 25bps rate cut was necessary to prevent temporary inflation undershoots from becoming persistent. Speaking about the June policy decision, Lane emphasized the influence of falling energy prices, a stronger Euro, and a deteriorating materially changed outlook on ECB’s latest projections.

He also highlighted growing uncertainty over the international trade system, citing risks that extend beyond tariffs to include new non-tariff barriers, shifts in investment frameworks, and increased convergence between economic and national security policies.

Against this backdrop, Lane reaffirmed the ECB’s "meeting-by-meeting". He stressed that "data dependence also extends to the incoming data on policy settings outside the monetary domain", since shifts in international and domestic policy regimes are highly relevant for future inflation dynamics.

BoE's Bailey warns of financial vulnerabilities amid global fragmentation

BoE Governor Andrew Bailey cautioned on Wednesday that risks tied to geopolitical tensions and the fragmentation of global trade and financial markets remain high. Speaking on the evolving macroeconomic development, Bailey said the world economy faces “material uncertainty,” and warned that some geopolitical threats have already begun to crystallize, impacting financial market behavior.

He noted a “notable change” in the usual correlations between the US Dollar and other US assets such as equities and Treasury yields. This breakdown, Bailey warned, increases the likelihood of sharp corrections in risk assets, abrupt shifts in allocation, and prolonged periods of market dislocation. Such dynamics could expose vulnerabilities in market-based finance and ripple into the UK by tightening the availability and cost of credit.

Bailey also stressed that trade fragmentation, while geopolitical in nature, has clear economic consequences. “Fragmenting the world economy is bad for activity,” he said, citing basic trade theory. The knock-on effects, he added, would likely weigh on employment and global growth.

RBNZ holds at 3.25%, signals easing path remains open

RBNZ left its Official Cash Rate unchanged at 3.25% on Wednesday, in line with market expectations, but maintained a clear easing bias in its statement.

While headline inflation is projected to briefly rise toward the top of the 1–3% target band by mid-2025, policymakers expect it to return near 2% by early 2026, supported by spare economic capacity and waning domestic price pressures.

The policy path forward remains clouded by global headwinds, sue to rising tariff tensions and geopolitical uncertainty.

The statement noted that "If medium-term inflation pressures continue to ease as projected, the Committee expects to lower the Official Cash Rate further."

China CPI turns positive, but PPI slump deepens

China’s consumer inflation returned to positive territory in June for the first time in five months, with headline CPI rising 0.1% yoy, above expectations of -0.1% yoy. The improvement was driven by a 0.7% annual rise in core CPI — the strongest core reading since April 2024. The data suggests a modest pickup in domestic demand, although the pace remains fragile as headline inflation is barely above zero.

On the producer side, deflation deepened. PPI fell -3.6% yoy, marking its sharpest drop since July 2023 and extending a nearly three-year deflationary streak. The continued subdued industrial demand reflects the challenges facing China’s manufacturing sector.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1766; More...

EUR/USD's consolidation from 1.1829 is still extending and intraday bias stays neutral. Downside should be contained by 1.1630 resistance turned support to bring rebound. On the upside, firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

ECB’s Lane: Global uncertainty goes beyond tariffs, includes investment and security risks

ECB Chief Economist Philip Lane said in a speech today that the recent 25bps rate cut was necessary to prevent temporary inflation undershoots from becoming persistent. Speaking about the June policy decision, Lane emphasized the influence of falling energy prices, a stronger Euro, and a deteriorating materially changed outlook on ECB’s latest projections.

He also highlighted growing uncertainty over the international trade system, citing risks that extend beyond tariffs to include new non-tariff barriers, shifts in investment frameworks, and increased convergence between economic and national security policies.

Against this backdrop, Lane reaffirmed the ECB’s "meeting-by-meeting". He stressed that "data dependence also extends to the incoming data on policy settings outside the monetary domain", since shifts in international and domestic policy regimes are highly relevant for future inflation dynamics.

BoE’s Bailey warns of financial vulnerabilities amid global fragmentation

BoE Governor Andrew Bailey cautioned on Wednesday that risks tied to geopolitical tensions and the fragmentation of global trade and financial markets remain high. Speaking on the evolving macroeconomic development, Bailey said the world economy faces “material uncertainty,” and warned that some geopolitical threats have already begun to crystallize, impacting financial market behavior.

He noted a “notable change” in the usual correlations between the US Dollar and other US assets such as equities and Treasury yields. This breakdown, Bailey warned, increases the likelihood of sharp corrections in risk assets, abrupt shifts in allocation, and prolonged periods of market dislocation. Such dynamics could expose vulnerabilities in market-based finance and ripple into the UK by tightening the availability and cost of credit.

Bailey also stressed that trade fragmentation, while geopolitical in nature, has clear economic consequences. “Fragmenting the world economy is bad for activity,” he said, citing basic trade theory. The knock-on effects, he added, would likely weigh on employment and global growth.

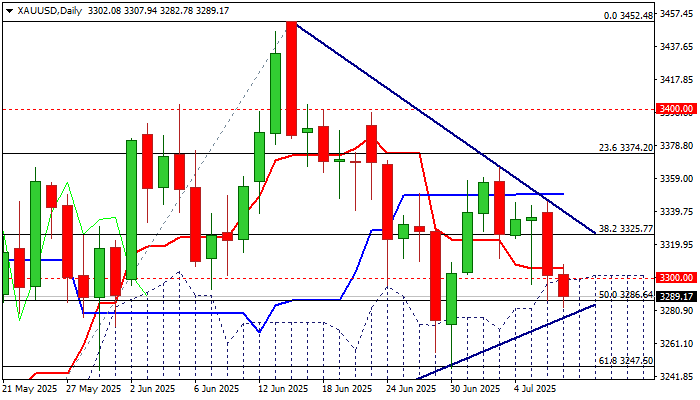

GOLD – Bears Tighten Grip and Probe Again into Daily Cloud

Gold remains in red for the second consecutive day, pressured by stronger dollar on risk aversion as uncertainty over US tariffs rises.

Bears probe again through pivotal support at $3300 (psychological / rising daily cloud top) in attempts to sustain break lower, after cloud contained several attacks recently.

Today’s action so far hold in the cloud, as bears cracked 50% retracement of $3120/$3452 ($3286) and eye next significant support at $3277 (triangle support line).

Daily studies are weak (Tenkan/Kijun-sen in bearish setup / negative momentum is strengthening) and supportive for further easing, with loss of $3277 trendline support to risk attack at key supports at $3247 (Jun 30 higher low/ Fibo 61.8%) and $3228 (daily cloud base).

Conversely, another failure to register daily close within the cloud, would ease immediate downside threats, but regain of $3225/36 (broken Fibo 38.2% / upper triangle boundary) will be required to sideline near-term bears and shift focus higher.

Fed minutes (due later today) are in focus for more details about Fed’s short-term rate outlook.

Res: 3300; 3308; 3325; 3338

Sup: 3277; 3247; 3228; 3205

China’s PPI Slides, Australian Dollar Steady

The Australian dollar is almost unchanged on Wednesday. In the European session, AUD/USD is trading at 0.6532, up 0.03% on the day.

China's PPI declines 3.6%

China's producer price index surprised on the downside in June, with a steep 3.6% y/y decline. This was below the May decline of 3.3% and the consensus of -3.2%. China has posted producer deflation for 33 successive months and the June figure marked the steepest slide since July 2023. Monthly, PPI declined by 0.4%, unchanged over the past three months.

The soft PPI report was driven by weak domestic demand and the continuing uncertainty over US tariffs. The lack of consumer demand was reflected in the weak CPI reading of 0.1% y /y, the first gain in four months. Monthly, CPI declined by 0.1%, following a 0.2% drop in May. There was a silver lining as core CPI rose 0.7% y/y, the fastest pace in 14 months.

The uncertainty over US President Trump's tariff policy continues to perplex the financial markets. Trump had promised a new round of tariffs against a host of countries on July 9 but he has delayed that deadline until August 1.

China, the world's second-largest economy after the US, has taken a hit from US tariffs, as China's exports to the US are down 9.7% this year, However, China has mitigated much of the damage as China's exports to the rest of the world are up 6%. There is a trade truce in effect between the two countries but the bruising trade war will continue to dampen US-China trade.

FOMC minutes - what will be Powell's tone?

With no tier-1 events out of the US today, the FOMC minutes of the June meeting will be on center stage. The Fed held rates at that meeting and Fed Chair Powell, who has taken a lot of heat from Donald Trump to cut rates, defended his wait-and-see-attitude, citing the uncertainty that Trump's tariffs are having on US growth and inflation forecasts.

AUDUSD Technical

- AUD/USD tested resistance at 0.6532 earlier. Above, there is resistance at 0.6543

- 0.6519 and 0.6508 are the next support levels

AUDUD 4-Hour Chart, July 9, 2025

RBNZ Rate Hold, Copper Volatility, DAX Makes a Move Toward Fresh Highs

Chinese stocks are set to hit their highest level in three years as investors hope for new steps to fight deflation and boost the economy. Meanwhile, copper prices dropped in London after President Donald Trump issued a new tariff warning.

Asian Market Wrap

The Shanghai Stock Exchange Composite Index rose 0.4%, reaching its highest level this year and the best close since January 2022. The CSI 300 index, a key measure of Chinese stocks, is also set for its highest close since December. Data showed that China’s factory prices continued to fall for the 33rd month, but consumer prices surprisingly increased in June.

In other news, Asian stocks dipped slightly by 0.1% as investors avoided risky moves after Trump escalated trade tensions.

China’s weak inflation is putting pressure on policymakers to introduce more stimulus to break the cycle of falling prices, profits, and wages. Investors are now looking to Beijing’s July Politburo meeting for stronger economic support after recent efforts to cut factory overcapacity.

RBNZ Pauses Rate Cuts, NZD Slips Toward Two-Week Lows

The New Zealand dollar dropped to 0.598, near a two-week low, after the Reserve Bank of New Zealand paused its rate cuts but hinted at more reductions if inflation slows.

The central bank kept its cash rate at 3.25%, following six cuts since August 2024. It’s being cautious due to 2.5% domestic inflation and global trade tensions that could raise prices.

However, the bank expects to lower rates further if inflation eases, and markets predict at least one more cut this year due to economic weakness.

European Open

European stocks edged up on Wednesday, boosted by defense shares, as investors watched for progress on a US-EU trade deal.

The STOXX 600 index rose 0.2% to 546.94 points. Defense stocks gained 1.1%, banks climbed nearly 1%, and energy shares were up 0.8%.

President Trump hinted at announcing EU export tariffs soon, while reports suggest EU negotiators are close to a deal with higher tariffs than the UK.

EssilorLuxottica shares jumped 5.1% after Meta reportedly acquired a 3% stake in the company.

On the FX front, The dollar rose 0.1% to 146.75 yen, hitting 147.19 earlier, marking a 1.5% weekly gain, the biggest since December. Japan, heavily reliant on exports, remains far from a trade deal, with its currency under pressure as talks stall and focus shifts to an upcoming election.

The euro stayed flat at 1.171 as the EU hopes to avoid U.S. tariffs and secure exemptions from the 10% baseline rate. The dollar index held steady at 97.60, while the British pound edged up to 1.36. The New Zealand dollar also rose slightly to 0.60.

Currency Power Balance

Source: OANDA Labs

Looking at commodities and Oil prices have recovered following a gap down over the weekend.

Gold struggled overnight and has failed to hold above the $3300/oz handle as optimism grows around trade deals. Interesting data from the World Gold Council yesterday which showed that Global Central Bank buying remains strong.

Global central banks' net gold purchases reached 20 tonnes in May, the highest in 3 months. This marks the 24th consecutive net monthly purchase.

Over the last year, central banks have bought an average of 27 tonnes of gold per month.

Economic Data Releases and Final Thoughts

Looking at the economic calendar, it remains a quiet one. The biggest events of the day will come from comments by Central Bank policymakers, with ECB and BoE policymakers on deck.

Later in the day we have the FOMC minutes as the Trump Administration continues to put pressure on the Fed publicly to cut rates.

Given the limited data releases I am expecting tariff and trade deal chatter to dominate matters today and for the majority of the week ahead.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the Day - DAX Index

From a technical standpoint, the DAX has been moving higher this morning on optimism that the EU will strike a deal with the Trump administration.

The DAX is currently trading above the previous range high at 24330. A daily candle close above this level may lead to further upside.

Bulls do appear in control for now with trade talks ongoing.

A pullback to 24330 may provide would be bulls with potential long opportunities on an intraday basis. However, I would caution that without a daily candle close above the range (highlighted red/pink zone) a pullback toward the 24000 handle could materialize.

DAX Daily Chart, July 8. 2025

Source: TradingView.com (click to enlarge)

Support

- 24000

- 23727

- 23471

Resistance

- 24479

- 24500

- 24750

EUR/JPY Hits 12-Month High

As the chart indicates, the EUR/JPY pair has risen above ¥172 per euro — a level last seen in July 2024.

Since early June, the exchange rate has increased by approximately 5.6%. This upward movement is driven by a combination of factors, including:

→ Divergence in central bank policy: The European Central Bank’s key interest rate remains significantly higher than that of the Bank of Japan, making the euro more attractive in terms of yield compared to the yen.

→ US trade tariffs on Japan: The potential imposition of 25% tariffs by the United States on Japanese goods poses a threat to Japan’s export-driven economy, placing downward pressure on the national currency.

→ Eurozone expansion and consolidation: News of Bulgaria’s potential accession to the euro area is strengthening investor confidence in the single currency.

→ Weakness in the US dollar: As the US Dollar Index fell to its lowest level since early 2022 this July, demand for the euro has grown, positioning it as a key alternative reserve currency.

Can the rally continue?

Technical Analysis of EUR/JPY

For several months, the pair traded within a range of approximately ¥156–165 per euro, but has recently broken above the upper boundary of this channel. Based on technical analysis, the width of the previous range implies a potential price target in the region of ¥174 per euro.

It is noteworthy that the rally gained momentum (as indicated by the arrow) following the breakout above the psychological threshold of 170, a sign of bullish market dominance. At the same time, the RSI has surged to a multi-month high, signalling moderate overbought conditions.

Under these circumstances, the market may be vulnerable to a short-term correction, potentially:

→ Towards the lower boundary of the ascending channel (shown in orange);

→ To retest the psychological support around ¥170.

That said, a reversal of the prevailing trend would likely require a significant shift in the fundamental backdrop — for example, progress towards a trade agreement between Japan and the United States.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Elliott Wave Outlook: DAX Set to Rally Higher in Wave 5

Since April 7, 2025, the DAX Index has been advancing in a clear impulsive cycle, originating from a low that has set the stage for a structured upward movement. The initial advance, wave 1, concluded at 20468.43. It was followed by a corrective pullback in wave 2, which found support at 19384.39. The subsequent rally in wave 3 was robust, peaking at 24479.42, as depicted on the 1-hour chart. Wave 4 unfolded as a zigzag Elliott Wave pattern, characterized by a decline in wave ((a)) to 23360.16. A recovery in wave ((b)) took place to 23711.73, and a final dip in wave ((c)) to 23047.13, completing the corrective wave 4.

The Index then resumed its upward trajectory in wave 5, structured as an impulse in a lesser degree. From the wave 4 low, wave (i) reached 23481.97. A minor pullback in wave (ii) followed which ended at 23080.29. The rally then continued with wave (iii) peaking at 23812.79, a slight correction in wave (iv) to 23466.73, and the final leg, wave (v), concluding at 241200.82, marking the completion of wave ((i)).

A corrective wave ((ii)) found support at 23620.42, and the Index has since turned higher in wave ((iii)). As long as the pivot low at 23407.13 holds, the DAX is expected to extend its gains, with pullbacks likely finding support in a 3, 7, or 11 swing structure. This analysis suggests continued bullish momentum in the near term, with key support levels providing opportunities for further upside.

DAX 60-Minute Elliott Wave Technical Chart

DAX Elliott Wave Technical Video

https://www.youtube.com/watch?v=BBtvMboAusU

Gold Drops Below $3,300 as Fed Rate Forecasts Shift

Gold prices fell below 3,300 USD per troy ounce on Wednesday, extending losses after a 1% decline the previous day. The downward pressure stemmed from the Federal Reserve’s cautious stance, which partially offset concerns over escalating trade tensions.

US President Donald Trump dismissed any further delays to tariff hikes set for 1 August, announcing additional aggressive measures. These include a 50% duty on copper imports, potential 200% tariffs on pharmaceuticals, and a 10% levy on goods from BRICS nations.

Another key factor weighing on gold was the neutral Fed outlook regarding a rate cut in July. Last week’s strong US jobs report alleviated fears of an economic slowdown, reducing expectations of imminent monetary easing.

The new tariffs could exacerbate inflationary pressures in the US, potentially limiting the Fed’s room for future rate reductions.

Investors are now awaiting the June FOMC meeting minutes, due later today, for further clues on the central bank’s policy direction.

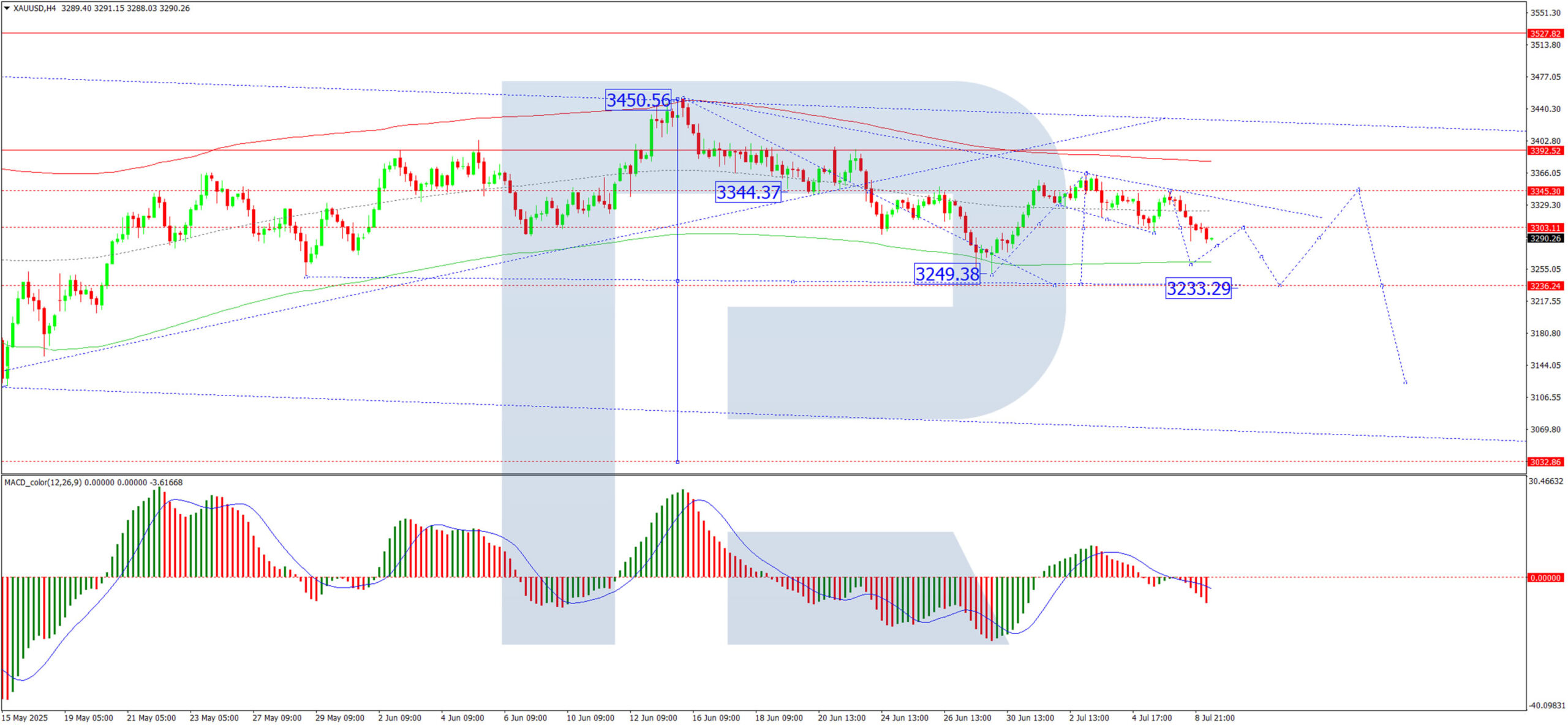

Technical Analysis: XAU/USD

H4 Chart:

The XAU/USD pair is forming the fifth wave of a downward structure, targeting 3,233. Upon completion, a corrective wave towards 3,344 may follow before a potential resumption of declines to 3,121. This outlook is supported by the MACD indicator, whose signal line is below zero and trending sharply downward.

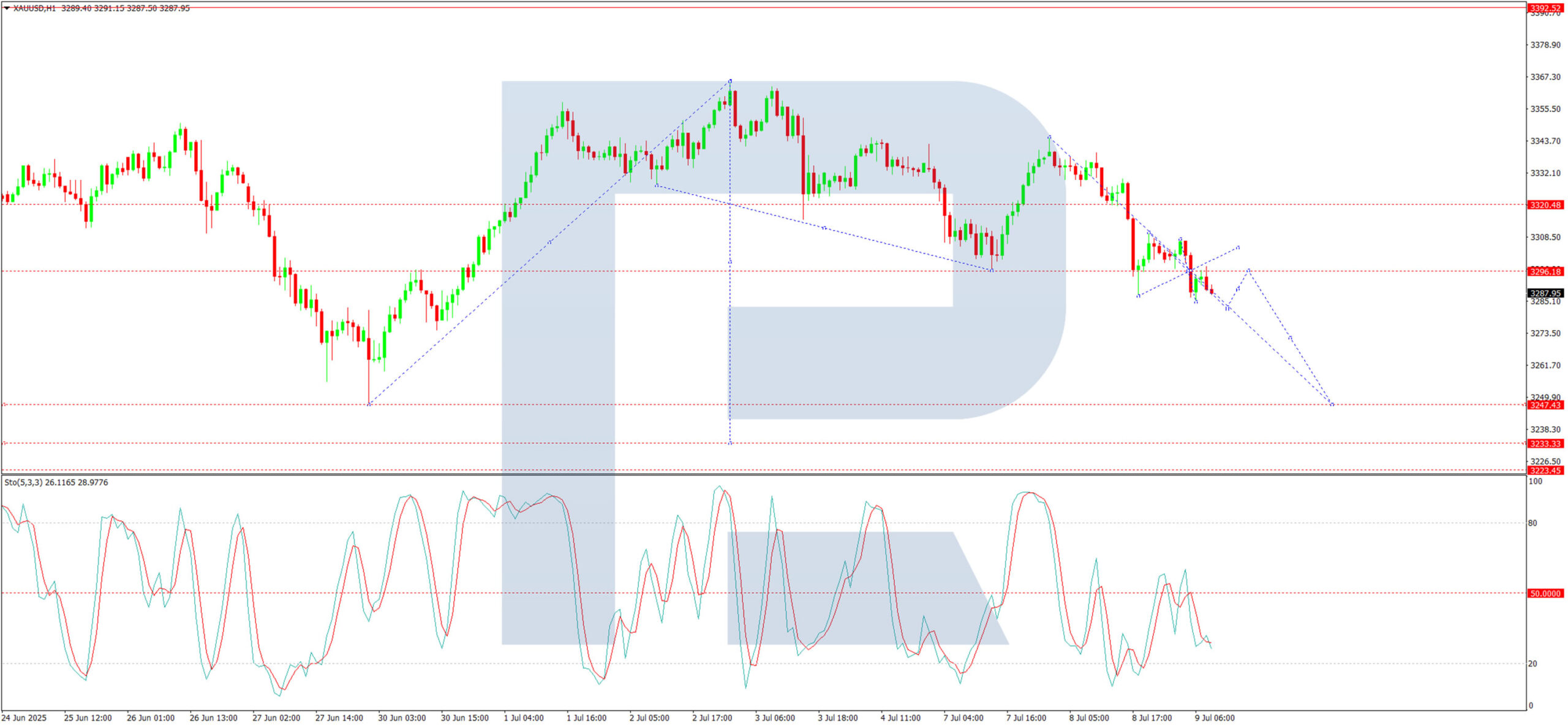

H1 Chart:

The pair has established a downward wave to 3,286, followed by a tight consolidation range near 3,296. Today, we anticipate a drop to 3,282, followed by a retest of 3,296 (from below). A breakout below this range could extend losses towards 3,247 – a near-term target. The Stochastic oscillator aligns with this view, with its signal line sitting below 50 and trending downward towards 20.

Conclusion

Gold remains under pressure amid shifting Fed expectations and trade uncertainties. A bearish technical structure suggests further downside potential unless key support levels hold.