Sample Category Title

Fed’s Barkin downplays ADP miss, needs more data before acting

Speaking to Fox Business, Richmond Fed President Tom Barkin dismissed alarm over the unexpected drop in ADP employment, saying he’s more focused on the unemployment rate in Friday’s jobs report. With joblessness steady around 4.1% to 4.3% for over a year, Barkin suggested "that all feels like a pretty stable range". He also noted that slower job growth must be seen in context with a cooling labor force, particularly as immigration flows ease.

Asked whether a weak payrolls figure could prompt the Fed to cut rates in July, Barkin avoided specifics and emphasized that the decision would depend on a broader set of inputs. “There’s more we’re going to learn,” he said, citing upcoming inflation data, tariff developments, and the pending tax bill. His remarks signal continued caution inside the Fed, even as market expectations lean toward a cut by September.

Despite recent data noise, Barkin remained cautiously optimistic. “What I see is a solid economy — not a strong economy — but a solid economy, one where people are not yet pulling back,” he said.

Talks in Sintra Highlight the Central Bank Playbook Has Had a Makeover

The annual ECB Central Banking Forum in Sintra provided plenty of lessons on how central banks across Asia and the West are navigating the shifting economic landscape.

The three key themes emerged out of the annual ECB conference in Sintra:

- Asia and the West have different responses to the trade shock

- The decline of US dollar dominance will be slow

- Reliance on the neutral rate offers diminishing returns

The European Central Bank’s annual panel brought together leaders from the ECB, Bank of England, US Federal Reserve, Bank of Japan, and Bank of Korea to discuss risks central banks are facing when conducting monetary policy. Of note, three key themes stood out: how trade tensions, currency dynamics and neutral rates are shaping monetary policy outlooks. We see increasing divergence in policy paths and priorities, particularly between Asian and Western economies.

Comments from the BoJ’s Ueda and BoK’s Rhee underscored a growing divergence in how Asian and Western economies are responding to trade-related shocks. For Asia, the need for accommodative policy is not only evident—it is strategic. Rhee’s emphasis on a pre-emptive approach reflects the structural reality that Asian economies, with their large exposure to export markets and China, are more vulnerable to imported deflation and a slowdown in growth. With growth tracking below potential and inflation risks tilted downward, early rate cuts across the region, as we have previously argued, will help cushion against global volatility. This reinforces our view that Asian monetary policy will likely remain structurally looser than in the West.

By contrast, policymakers in Europe, the UK, and the US appear to be adopting a more reactive stance, partly because of uncertainty around whether the impact of tariffs is transitory or not. Fed Chair Powell’s framing of the pause as a “prudent” measure reflects uncertainty about how large and persistence tariff effects will be and how they transmit through economies.

The second key theme was that moving any shift away from the US dollar as a reserve currency will be a slow-moving process catalysed by ‘uncertainty’ and ‘unpredictability’ and braked by the absence of a viable alternative. In a speech in May, ECB President Lagarde noted that the euro could play a bigger role as a reserve currency. To earn the right to do so, though, in her view Europe needs a stronger geopolitical and legal foundation as grows its capital markets through a strong European economy. None of this will happen overnight.

Rhee added to the theme of a more gradual decline in the USD’s dominance by arguing that recent strength in the Korean won reflected a reversion to its fundamental value as domestic political uncertainty fades, rather than being mostly about the USD’s decline. He also pointed out that hedging ratios had provided strength to the won. This has also been seen in the Taiwanese dollar and Japanese yen, both currencies benefitting from domestic fund managers increasing their hedging ratios.

The final key theme was the role of neutral interest rates in today’s monetary policy frameworks. Across the panel, there was broad agreement that the uncertainty surrounding neutral rate estimates has widened considerably. Lagarde argued the concept of neutral also becomes less relevant in an environment of major shocks. In addition, the closer policy is to the uncertain estimates of neutral, the less of a guide to future direction it becomes.

As a result, central banks appear to be treating neutral not as a firm policy anchor, but as a guiding light, helping to gauge direction. There was also consensus that policy rates are not currently restrictive across all jurisdictions except the US and that estimates of neutral have risen in the post-pandemic era, an observation we have been making for some time.

Interestingly, this contrasts with recent developments in Australia, where the policy rate is still above most of the RBA’s model-based estimates of neutral. The panel’s discussion suggests that the RBA may be something of an outlier. This divergence highlights a broader challenge: as global shocks become more frequent and complex, reliance on slow-moving and uncertain estimates like the neutral rate may offer diminishing returns. For central banks, this means policy will need to remain adaptive, data-dependent, and increasingly open to qualitative judgment.

The Sintra panel highlighted how risks are being interpreted by central banks across regions. Asian central banks, facing trade-driven deflation and sub-trend growth, are acting pre-emptively. Western policymakers remain more reactive, reflecting uncertainty around tariff impacts. While dissatisfaction with dollar dominance is growing, structural change will be slow, with the euro’s ascent still nascent. Though neutral rates remain a key reference point, their practical use is limited in today’s shock-prone environment, and when policy is already in the ballpark of neutral. As global conditions fragment, central banks are moving toward a more flexible, adaptive policy approach.

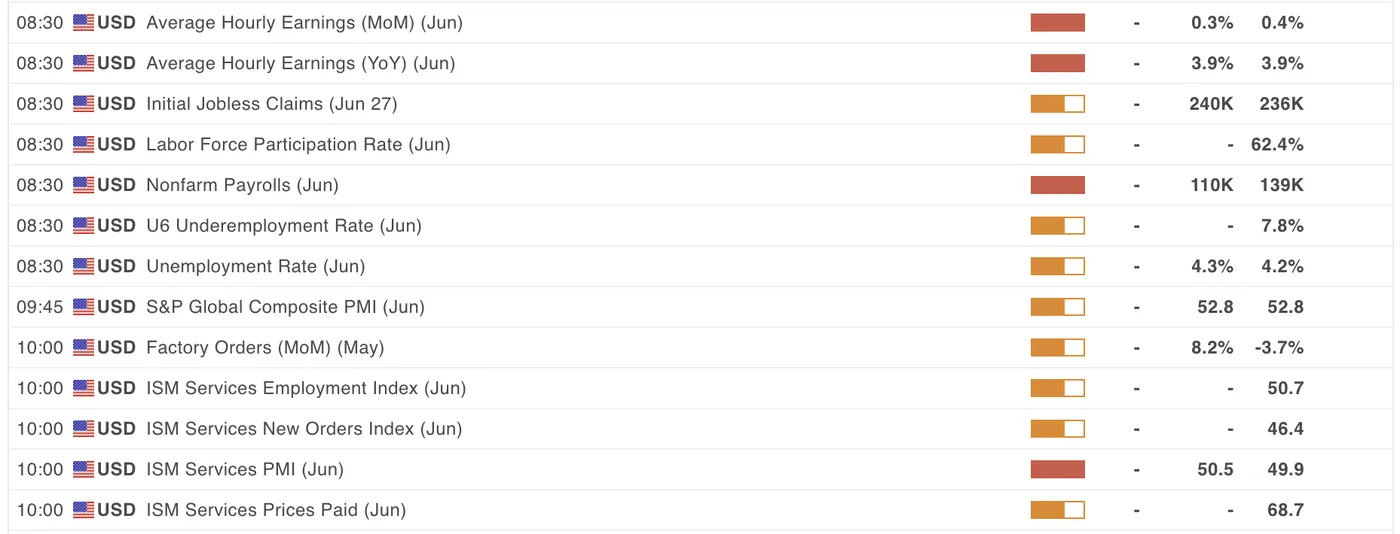

July Non-Farm Payrolls Preview

The upcoming Non-Farm Payrolls (NFP) report is set to be released tomorrow, with a consensus expectation of 110K, compared to the previous release of 139K.

While this data is typically released on the first Friday of every month, this month’s report comes on Thursday, July 3rd, due to Independence Day (July 4th), when US markets will be closed.

For those newer to trading, the NFP is one of the most market-moving data releases globally, as it offers insight into the health of the US labor market for the month that just concluded—with the Unemployment Rate also published at the same time.

The reason this data matters so much is because of the American consumption cycle, which is historically very strong. However, slowing job creation tends to reduce US consumer spending, which affects the performance of US stock indices, and consequently impacts demand for the US Dollar, in which most global assets are priced.

This creates a domino effect: a stronger or weaker US workforce can shift expectations around Federal Reserve policy—including the likelihood of interest rate hikes or cuts—which then ripples across to other central banks and currency markets.

Since the Great Financial Crisis (2008), Dollar demand has outperformed most major currencies, with US growth leading over other G7 economies, attracting significant global capital inflows. However, that dominance is beginning to fade, as Trump’s unpredictable policies and concerns over US fiscal and debt sustainability have made investors more cautious, encouraging greater international diversification.

Let’s now explore:

- Seasonal trends for July payrolls

- Recent NFP surprises and how they’ve moved markets

- What potential reactions traders might expect from this key report

US Data releasing tomorrow morning, including NFP and ISM Services PMI

For all Market moving events, check the MarketPulse Economic Calendar

Seasonal trends for the July NFP release

July NFP (where Markets learn more about June jobs data) averages around 250,000 in since 2010, excluding 2020 due to COVID Recovery numbers significantly influencing typical trends (4.8 Million jobs created in the July 2020 NFP!).

Also excluding outstanding data points such as the 2010 -167K Census Layoffs and 2021 Later COVID Recovery (+850,000), the average for the July NFP is just above 200K.

3 most Recent Major Surprises and Market reactions on the USD and S&P 500

The most recent largest surprises (+100K) on the NFP Releases have all happened since 2021.

The most recent was in January 5, 2024: +106K surprise which led to US 10Y Yields rising by 10 bps, going from below to above 4% (yields were trending lower), with Yields trending higher after and Stock Indices stopped their correction leading to a 12% rise in the following 3 months.

Another major surprise, happening on June 7 2024 was negative: -55K relative to expectations which sent markets shaking with Hard Landing fears (that still did not materialize): Cuts started to price in leading to a 10% correction in Equity indices in July 2024 and Carry trades unwinding significantly.

In the same trend, 10Y Yields retracted severyly going from 4.40% in the beginning of June 2024 to lows of 3.63% in September 2024.

The third most recent surprise was on October 26 2023, as markets were trying to price in the first FED Cuts and expecting progressively slowing US Job creation - +166K surprise that sent stocks blazing 1.2% on the session and created a major bottom for downtrending prices. 10Y Yields shot up 11bps that session before trending down as markets were repricing a Soft Landing from high inflation trends.

What to Expect from this Upcoming Report

Equity Indices have been in a frenzy, rebounding sensationally from early 2025 Trump-tariffs leading to global recession fears.

A 20% correction from previous all-time highs led to the ongoing +30% recovery in all major US Indices, with Indices bottoming in April shortly after the Liberation Day announcements.

What's priced in:

Euphoric mood since the Israel-Iran conflict concluded led to new All-time highs in the Nasdaq and S&P, other global indices are also trading close or above their ATH. Markets which were scared of global activity slowing down due to tariff fears of imminent stagflation are scared-no-more, with the pricing of "TACO" Trades (Trump Always Chickens Out).

The idea is that despite menaces, deals are always found and the activity in the leading economy stays as strong. As a matter of fact, the Unemployment Rate hasn't ticked down despite consumer sentiment shooting down and recovering since January.

What to expect (subject to largely different reactions as markets are tough to predict):

A miss would create the most dramatic scenario, where one may expect USD selling to resume with markets getting confirmation on their fears for the US Economy – Sell Equities, Sell the USD, Yields down significantly, Gold up. The extent of such moves would depend on how big the miss is.

A beat would pursue the ongoing trend – Higher equities, higher yields due to more pricing out of FED Cuts, USD up significantly, Gold down, Oil up.

In line (+/- 5K) data would generate some profit taking – USD recovers slightly, some profit taking on Equities, slower but continued price discovery for US Equity indices, potential for rangebound price action, Gold retraces back down, yields up small.

Safe Trades for the upcoming NFP!

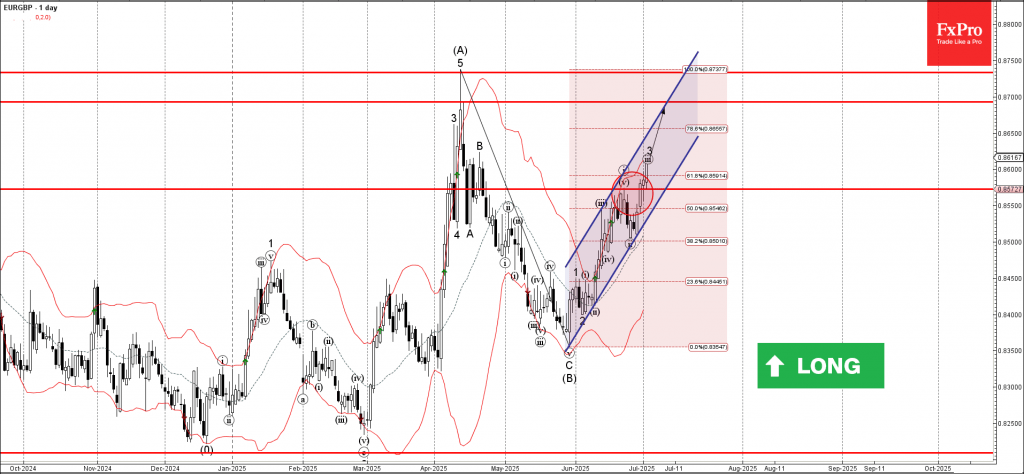

EURGBP Wave Analysis

EURGBP: ⬆️ Buy

- EURGBP broke resistance zone

- Likely to rise to resistance level 0.8700

EURGBP currency pair recently broke the resistance zone between the resistance level 0.8570 (which stopped the previous impulse wave i at the end of June) and the 61.8% Fibonacci correction of the downward impulse (B) from April.

The breakout of this resistance zone accelerated the active minor impulse wave 3 of the intermediate impulse wave (C) from May.

EURGBP currency pair can be expected to rise to the next resistance level 0.8700 (which is intersecting with the daily up channel from May).

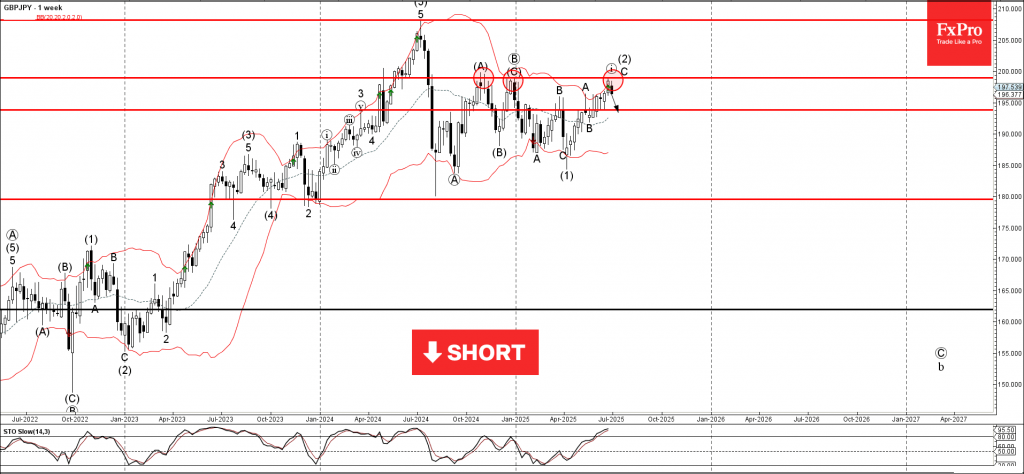

GBPJPY Wave Analysis

GBPJPY: ⬇️ Sell

- GBPJPY reversed from resistance zone

- Likely to fall to support level 193.85

GBPJPY currency pair recently reversed down from the resistance zone between the strong resistance level 199.000 (which has been reversing the price from last October) and the upper weekly Bollinger Band.

The downward reversal from this resistance zone stopped the C-wave of the previous ABC correction (2) from April.

Given the strength of the resistance level 199.000 and the overbought weekly Stochastic GBPJPY currency pair can be expected to fall to the next support level 193.85.

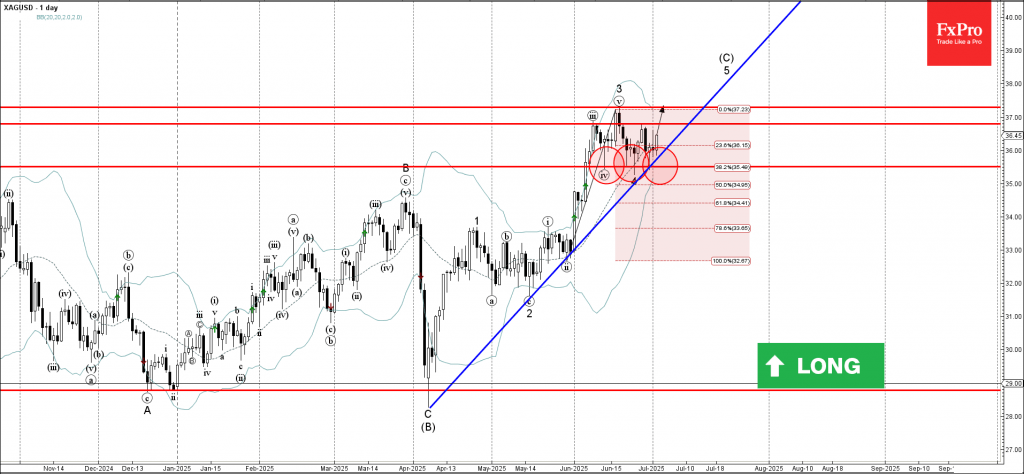

Silver Wave Analysis

Silver: ⬆️ Buy

- Silver reversed from support level 35.50

- Likely to rise to resistance level 37.30

Silver recently reversed up with the daily Hammer from the support level 35.50 (which stopped the previous waves (iv) and 4, as can be seen from the daily Silver chart below).

The support level 35.50 was strengthened by the 38.2% Fibonacci correction of the upward impulse from May and the support trendline from April.

Given the clear daily uptrend, Silver can be expected to rise further to the next resistance level 36.80 – the breakout of which can lead to further gains toward 37.30.

Trump Threatens Tariff on Japan as Deadline Looms, Yen Dips

The Japanese yen is negative ground on Thursday. In the North American session, USD/JPY is trading at 144.06, up 0.47%.

US-Japan trade talks stumble over .... rice

The US and Japan are racing to reach a trade deal before a deadline of July 9. There are some serious roadblocks to a deal, including the current US tariff of 25% on Japanese cars and opening Japan's agricultural sector, particularly rice. President Trump has insisted that Japan import American-grown rice, but the Japanese government says that is unacceptable.

Japan's Economy Minister Ryosei Akawaza said earlier this week that Japan would not "sacrifice the agricultural sector", while Farm Minister Shinjiro Koizumi said that foreign rice imports would threaten Japan's food security.

US nonfarm payrolls expected to drop to 110 thousand

It's a shortened week in the US due to the Fourth of July holiday on Friday. The US will release the June employment report on Thursday, with all eyes on nonfarm payrolls.

Nonfarm payrolls eased slightly in May to 137 thousand from 147 thousand and the downward trend is expected to continue, with a consensus of 110 thousand for June. This would mark the weakest pace of job growth since 2020, with the exception of a meltdown in job growth in Oct. 2024.

The Federal Reserve will also be monitoring the nonfarm payroll report. The US labor market has been weakening and the Fed is concerned that the jobs market could show a sharp deterioration. Currently, the most likely date for the next Fed rare cut is September, but a soft NFP reading south of 90 thousand would boost the case for a cut at the July 30 meeting.

The Fed has maintained a wait-and-see stance since Nov. 2024 but that is expected to change in the fourth quarter, where we could see up three rate cuts.

USD/JPY Technical

- There is support at 142.64 and 141.86

- 143.45 and 144.23 are the next resistance lines

USDJPY 1-Day Chart, July 2, 2025

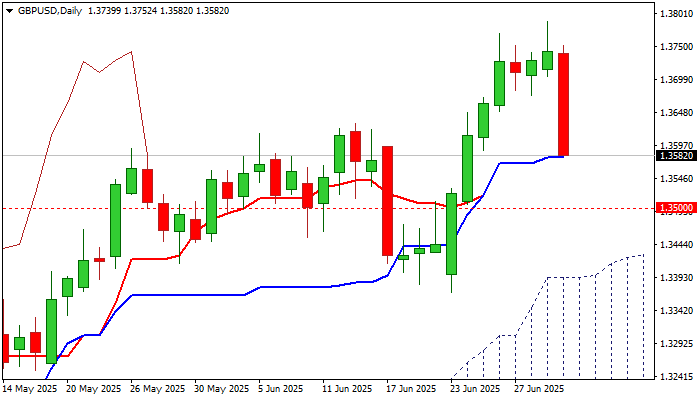

GBP/USD: Cable Falls Sharply on Political Turmoil in UK

British pound fell across the board on Wednesday following fresh political storm in the UK, after finance minister Reeves’ budget plan was strongly hurt by a series of significant changes in welfare reform bill that undermined the position of the fin min Reeves, as well as PM Starmer, who gave his full support to the finance minister.

Fresh weakness (Cable was down almost 1% for the day) adds to reversal signal that is developing on daily chart, as today’s action was shaped in long bearish candle, after the pair has registered six consecutive daily gains.

Technical picture weakens on daily chart as south-heading 14-d momentum is cracking the centreline, in attempts to break into negative territory and bears pressure important support at 1.3579 (50% retracement of 1.3370/1.3788, reinforced by converged daily Tenkan/Kijun-sen) while situation on 4-hr and hourly charts shows that bears gained control.

Break of 1.3579 trigger to open way for further weakness and expose targets at 1.3530 (Fibo 61.8%) and 1.3500 (psychological) guarding more significant support at 1.3397 (top of ascending and thickening daily cloud).

Broken 200HMA (1.3642) offers solid resistance, along with 1.3674 (low of recent range).

Res: 1.3618; 1.3642; 1.3674; 1.3712.

Sup: 1.3530; 1.3500; 1.3469; 1.3397.

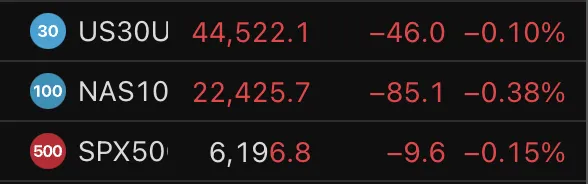

US Stocks Point to Muted Reaction at Open Despite Big ADP Jobs Miss

This morning's ADP release was not enough to trigger large volatility in Markets. The data came in at -33K vs a consensus of 95K, a consequential miss that led to a subdued market reaction.

US Equity futures had gone up in the overnight session with the S&P 500 just grazing new all-time highs (6,229 on its CFD) and markets are now correcting, with however a slow but steady grind.

ADP Employment measures private employment by US Firms and concerns around 30 millions of Americans , which represents a bit less than 10% of the US Population – Its correlation to the Non-Farm Payrolls data is not significant, a reason why reactions to ADP releases are less accentuated than the more global US NFP.

The miss is nonetheless quite large and it will be interesting to see in the upcoming months how Trump's policies influence the difference in Private and Public US Employment, if there are disparities and how much of a difference in the economy this potential disparity generates.

The current picture in US Indices point to similar rebalancing flows from Tech to Consumer Defensive/Manufacturing with the Nasdaq again leading on the downside (-0.40%) and the Dow Jones on top of Indices (-0.10%) – Futures point towards a small gap down at the 9:30 opening Bell.

US Indices CFD performance, July 2, 2025 – Source: TradingView

Nasdaq vs Dow Jones Relative strength in the past 10 years

Dow Jones vs Nasdaq, July 2, 2025 – Source: TradingView

This chart takes a peak at a comparison from Nasdaq prices relative to the Dow Jones – Since its advent in 1971, the Tech-Focused index has quite largely overperformed the more defensive Industrial Dow.

Prices in both indices are not calculated the same way, however the idea stays the same – The downtrend is slowing down, but still active, a bottom might be getting formed.

The ratio is now only 2 to 1 in terms of pure pricing and it seems that markets might start to change their appetite from the Nasdaq to the Dow – It is still very early to say this but might be worth taking a look.

Dow Jones and Nasdaq 4H Charts

Dow Jones 4H

Dow Jones 4H Chart, July 2, 2025 – Source: TradingView

Momentum is back to neutral after yesterday's overbought conditions stopped the bulls in their charge upwards.

Look for immediate support around 44,315 to 44,330, a confluence with the 4H MA 50 and the upwards trendline that is leading current flows.

For bears, look at either a failure to hold the trendline mentioned right before, or at a rejection of the local top at 44,702, which may not be reached if tomorrow's data comes in with a negative surprise.

Nasdaq 4H Chart

Nasdaq 4H Chart, July 2, 2025 – Source: TradingView

The Nasdaq chart looks more balanced, subject to bear strenght compared to the US 30 chart seen right before.

Prices broke through the upwards trendline that lead to the new All-time high price discovery (22,751 on the CFD) and have started to form what resembles a Head and Shoulders pattern – To supplement that, both the MA 20 and 50 are acting as immediate resistance and are starting to slope downwards.

RSI Momentum is also in the same direction but close to oversold, therefore it will be key to see how markets react to the upcoming Opening Bell.

Levels to watch for the Nasdaq:

- Local ATH Top – 22,700 Region Resistance

- Pivot Zone 22,450

- Previous ATH Support Zone 22,250 (confluence with 4H MA 200)

Safe Trades!