Sample Category Title

BoE’s Taylor backs steeper rate cuts as outlook deteriorates

BoE MPC member Alan Taylor warned today that the UK economy faces mounting risks to a soft landing, citing growing demand weakness and trade disruptions. In a speech, Taylor said his earlier forecast for a gradual disinflation and stable growth path is now at risk of being derailed in 2026.

“My reading of the deteriorating outlook suggested to me that we needed to be on a lower rate path, needing five cuts in 2025 rather than the market-implied quarterly pace of four,” Taylor said, citing recent shocks and global uncertainty that clouded his earlier view.

Taylor, who has consistently pushed for more aggressive easing, has voted for cuts in five of seven MPC meetings since joining last September—including a 50bps move in May followed by 25bps in June.

ECB’s Centeno: Must wait for more data before next move

Portuguese ECB Governing Council member Mario Centeno welcomed the return of Eurozone inflation to the 2% target, calling it "very good news." However, he also stressed that the ECB remains focused on assessing incoming data.

Centeno told Bloomberg TV that the ECB is “monitoring all possible numbers” and assessing various aspects of the Eurozone’s 20-member economy. “The current situation doesn’t mean that we need to rush into more interest-rate reductions,” he said. "We need to see data, we need to see the developments."

ECB’s Rehn warns of inflation undershoot risk, urges vigilance

Finnish ECB Governing Council member Olli Rehn warned that the Eurozone faces renewed risks of inflation falling below the 2% target as global uncertainties intensify. While acknowledging that risks to the outlook exist on both sides, Rehn said the downside appears more pressing. “The risk of staying below target is greater in my view, especially as our projections see price growth under target for 18 months,” he noted.

Rehn pointed to a trio of disinflationary forces — a strong Euro, lower energy prices, and rising tariffs — which he argued are weighing on both inflation and growth. “We need to be mindful of the risk of inflation staying persistently below 2%,” he said.

ECB’s Wunsch sees case for mild supportive stance as downside risks dominate

Belgian ECB Governing Council member Pierre Wunsch said the central bank may need a “mildly supportive” stance, especially if Eurozone recovery continues to lag. In an interview with Reuters, Wunsch noted “If the recovery is delayed — and it has been delayed a few times — and output is below potential, then being supportive is rational,” he said.

Wunsch highlighted several disinflationary forces at play, including lower energy prices, the strength of Euro, subdued wage growth, and the lack of tariff retaliation. He also flagged cheap Chinese imports as a contributing factor to weakening price pressures. “All these factors combined suggest that the upside risk is limited and the overall risk is to the downside,” he added.

With markets pricing in one final 25 basis point cut later this year, bringing the deposit rate to 1.75%, Wunsch said he was not uncomfortable with that view. “I don’t disagree with market pricing for interest rates,” he noted.

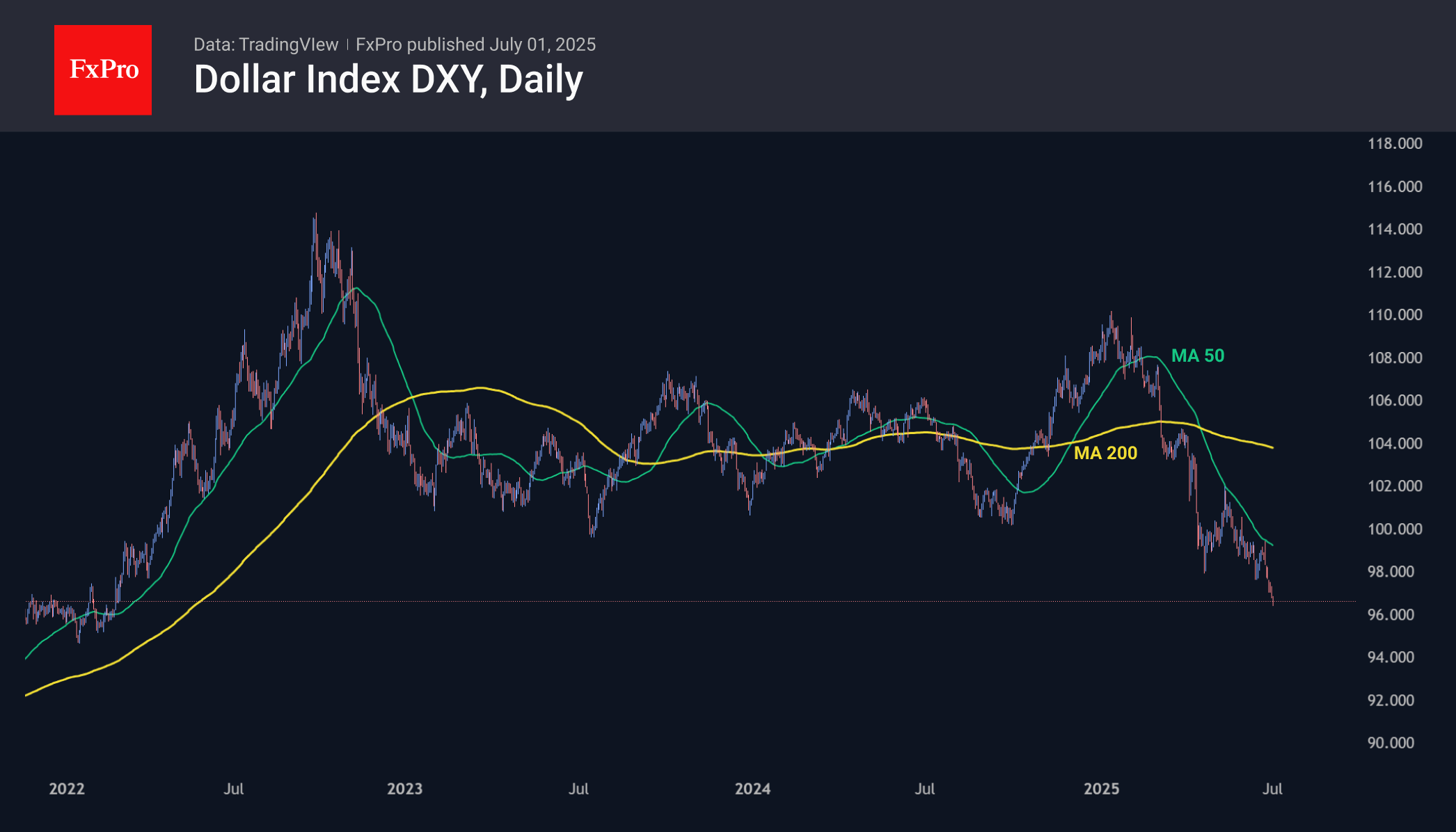

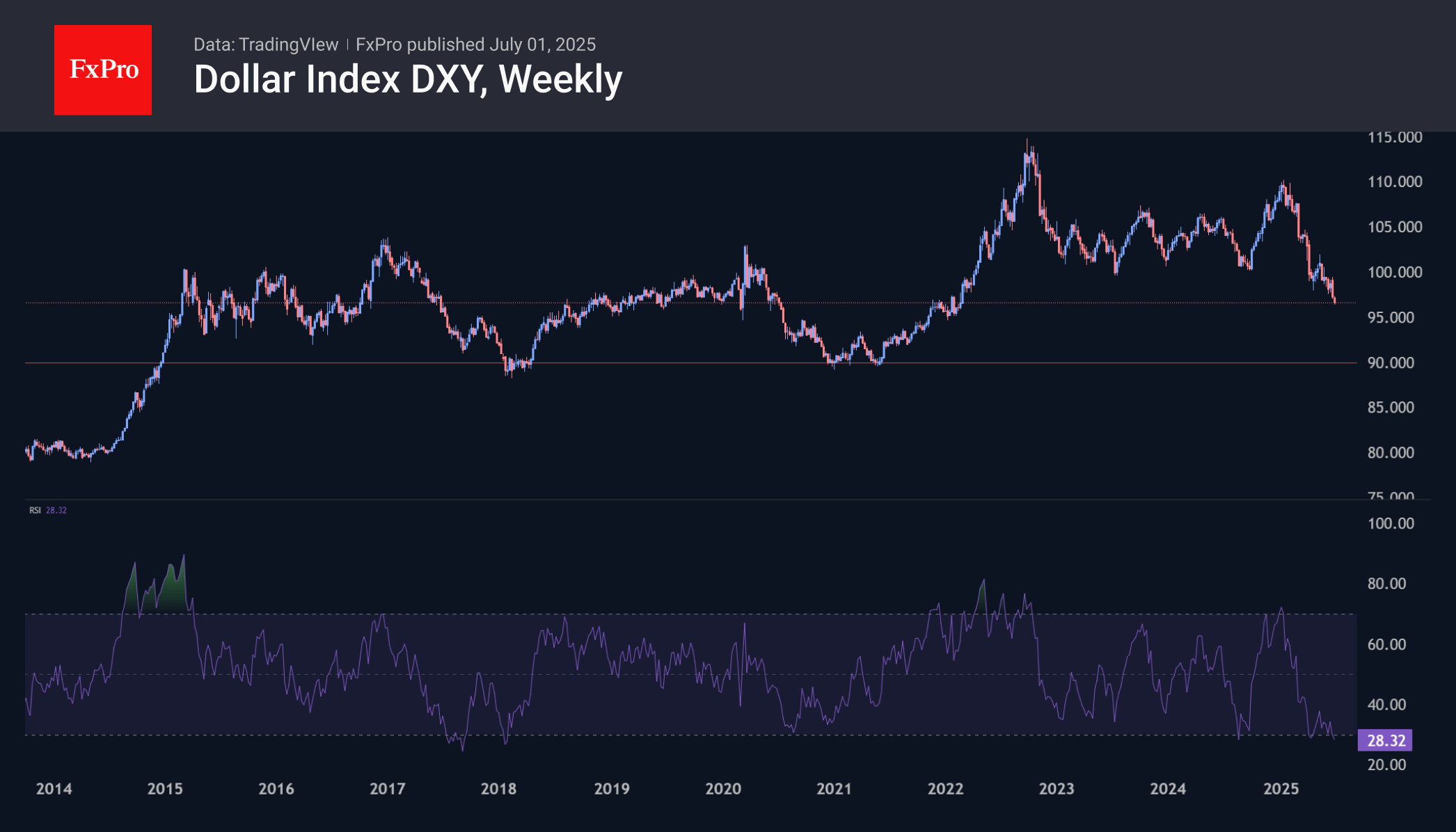

Dollar’s Reversal to Growth in Hands of Policymakers

The US dollar is retreating on all fronts, showing a daily decline since last Monday, when the military conflict between Israel and Iran came out of its hot phase and the tax bill in the US returned to the forefront.

Resuming its decline, interrupted by the bombing between Israel and Iran, the dollar index has been updating its more than three-year lows on a daily basis since the second half of last week. With total losses of over 12%, the first half of the year was the worst for the US currency since 1973, i.e. in the entire history of the free forex market.

A more neutral geopolitical background removed the ‘war premium’ from the dollar’s price and brought back the focus on Trump’s pressure on Powell and the discussion of Trump’s bill. This ‘One Big and Beautiful Bill’ promises to create a 7% budget deficit. The situation is not as serious as it was in September 2022 in Britain, but it is moving in the same direction.

However, we still see more influence in the changing mood of market participants, where expectations of a rate cut are growing. Markets are pricing in a 65% chance that there will be at least three cuts by the end of the year, almost double the figure a month ago.

On weekly timeframes, the RSI index has been updating its lows since early 2018, indicating an aggressive decline over the past seven years. This has dashed hopes for a bottoming out and rebound earlier this year.

The technical picture indicates the potential for the dollar to decline by another 7-8% to the 88-90 range on the DXY from the current 96.6. However, this is a rare case where the situation is in the hands of politicians. We turn our attention to representatives of the US Treasury and the Fed with comments on maintaining a strong dollar policy. Strong macroeconomic employment data this week may halt the dollar sell-off, but this is unlikely during a period of economic slowdown.

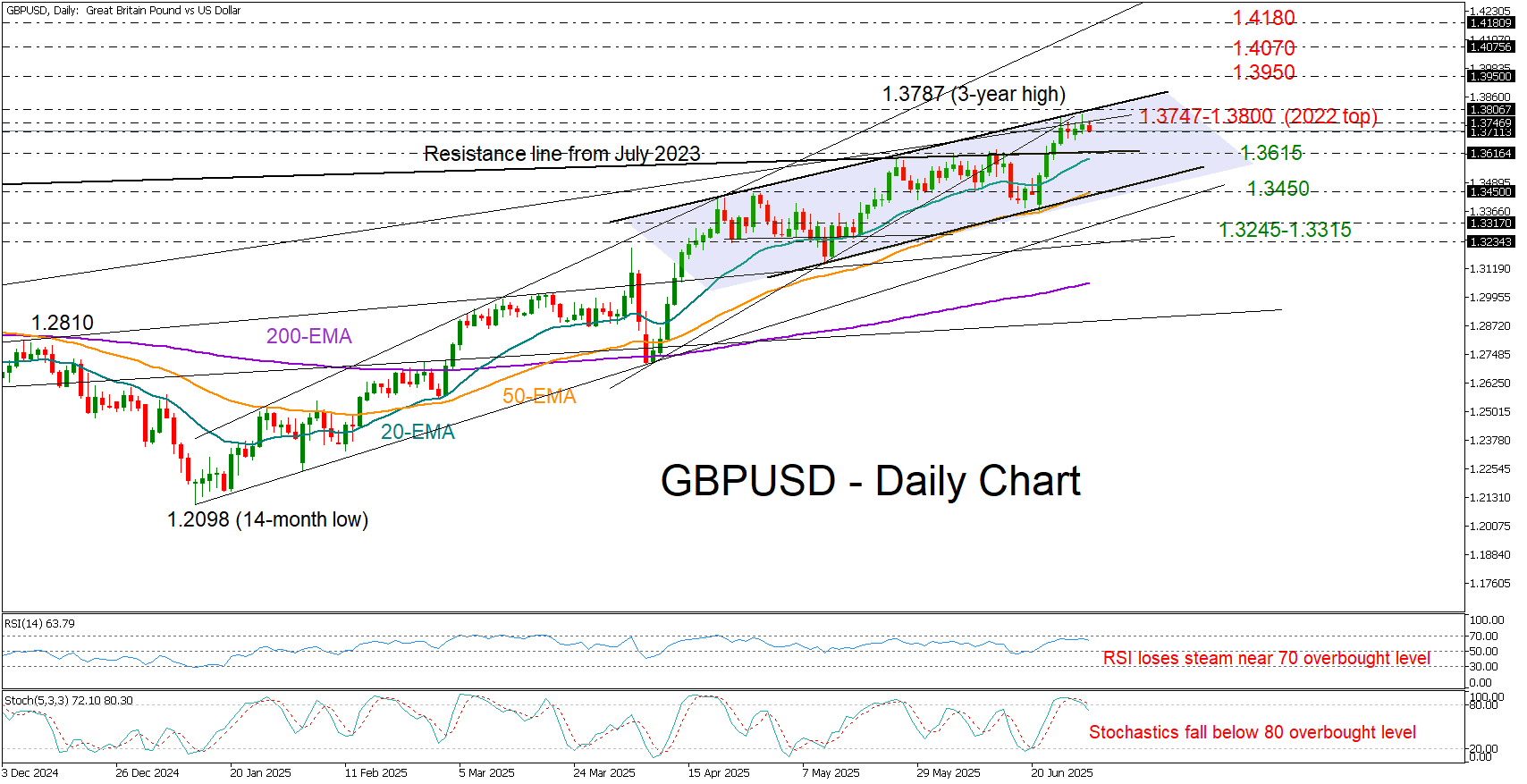

GBP/USD at Top of a Bullish Channel

- GBPUSD loses momentum near three-year high, tests the channel’s upper band.

- Short-term bias remains bullish, but overbought conditions are evident.

- Bullish outlook remains intact above 1.3450.

GBPUSD began July’s trading with sluggish momentum, following five consecutive months of gains that pushed the price to a three-year high of 1.3787 on Monday.

Much of the pair’s ascent is due to the dollar’s weakness, while the Bank of England’s gradual approach to rate cuts has been a positive catalyst too. Speaking on a panel with global peers in Portugal, BoE Governor Andrew Bailey reminded investors that interest rates are expected to decline further, while also hinting at a potential slowdown in quantitative tightening, clouding the outlook for the remainder of the year.

In the meantime, the RSI and the stochastic oscillator are issuing a warning about overbought conditions near the 2022 high of 1.3747 and the upper boundary of the bullish channel. The formation of small candlesticks at the top of the uptrend also reflects a degree of hesitation among traders.

If bearish pressure emerges, the pair could retreat towards the former resistance zone at 1.3615, where the 20-day exponential moving average (SMA) is converging. The 50-day EMA may provide additional support near the channel’s lower boundary at 1.3450, while the ascending trendlines at 1.3320 and 1.3235 could be the next levels to watch.

Should a bullish breakout occur above 1.3800, the next resistance may appear near 1.3950, a level derived from the June–August 2021 highs. Further up, the rally could pause around 1.4070 before potentially targeting the 2025 resistance line at 1.4180.

Overall, the recent bullish push in GBPUSD appears to have reached a critical pivot point, increasing the likelihood of a pullback or a period of consolidation. Nevertheless, only a break below the channel at 1.3450 would raise concerns about a potential bearish trend reversal.

Eurozone unemployment unexpectedly rises to 6.3% in May

Eurozone unemployment rate edged higher to 6.3% in May, missing expectations for an unchanged reading at 6.2%. Eurostat data showed 10.83m people unemployed in the Eurozone, part of a total 13.05m across the EU.

The broader EU jobless rate held steady at 5.9%, but the number of unemployed rose by 54k in the Eurozone and by 48k in the EU compared to April.

EUR/USD Analysis: Rally May Be Under Threat

The euro has appreciated by approximately 15% against the US dollar this year, as confidence in the United States continues to wane. As ECB Chief Economist Philip Lane noted in an interview at CNBC: “There is a degree of reorientation by global investors towards the euro.”

At the same time, officials at the European Central Bank have expressed concern that the rapid strengthening of the euro could undermine efforts to stabilise inflation at 2%. They warn that a move above $1.20 may pose risks for inflation and the competitiveness of export-oriented firms — an issue raised during the ECB’s ongoing ECB Forum on Central Banking in Portugal.

Could EUR/USD Reach the $1.20 Level?

From a technical analysis perspective, EUR/USD is showing bearish signals:

→ If the early April rally (coinciding with Trump’s announcement of new tariffs) is taken as the initial impulse wave A→B, and the May low is interpreted as the end of the B→C corrective move, then, according to Fibonacci Extensions, the pair has now risen to a key resistance zone around 1.1850 (as indicated by the arrow on the chart).

→ In addition, the RSI indicator signals strong overbought conditions, while the price is hovering near the upper boundary of the ascending channel — a level that typically acts as resistance.

Given these factors, we could assume that EUR/USD may be in a vulnerable position, potentially facing a short-term correction — possibly towards the lower boundary of the channel, reinforced by support at the 1.1620 level. However, this does not negate the longer-term bullish outlook for the euro amid prevailing fundamental conditions.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

EUR/USD Extends Rally for Ninth Consecutive Day as Dollar Remains Weak

The EUR/USD pair soared to 1.1801 on Wednesday, marking its ninth consecutive day of gains. The US dollar remains under heavy pressure due to expectations of a dovish shift in Federal Reserve policy and growing concerns over President Donald Trump’s fiscal strategy.

Fed maintains cautious stance while fiscal worries mount

On Tuesday, Fed Chair Jerome Powell reiterated that the central bank will maintain a wait-and-see approach, but he did not rule out a potential rate cut at the next meeting. Powell emphasised that future decisions would depend on economic data, adding that the Fed could have already cut rates were it not for inflationary pressures from Trump’s tariffs.

Meanwhile, the US Senate narrowly approved a massive tax and budget package expected to increase the national debt by 3.3 trillion USD. The bill now returns to the House of Representatives for final approval, fuelling further concerns over the US fiscal outlook.

Key data ahead to guide the market

Investors are now awaiting crucial US employment data:

- Wednesday: ADP report on private sector employment

- Thursday: June labour market statistics

These releases could provide further clarity on the Fed’s next policy steps.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD has completed a growth wave to 1.1777, with a consolidation range forming around this level. Today, an upward expansion is expected to 1.1848, followed by a decline to 1.1750, marking the range boundaries. An upward breakout could extend the range to 1.1885, while a downward breakout would open the potential for a decline to 1.1430. The MACD indicator confirms this outlook, with its signal line above zero and exiting the histogram zone, suggesting an approaching correction as it nears the zero line.

On the H1 chart, EUR/USD continues forming a consolidation range around 1.1777. Today, an expansion upwards to 1.1848 is likely. However, it is essential to note that the growth potential is nearly exhausted, and the market may soon begin a downward trend towards 1.1660, with the potential to extend to 1.1616. The Stochastic oscillator confirms this scenario, with its signal line below 80 and pointing sharply downward towards 20, indicating the building of bearish momentum.

Conclusion

The EUR/USD maintains its strong rally amid dovish Fed expectations and US fiscal concerns, with resistance levels at 1.1848 and 1.1885. Support lies at 1.1750, 1.1660, and 1.1616. Upcoming employment data will be crucial in determining whether the pair sustains its upward trend or reverses into a corrective phase.

Nikkei 225 Rebounds from Support Despite Trump’s Tariff Threats

A sector rotation took centre stage in the US stock market on Tuesday, 1 July, as investors pulled out of mega-cap technology stocks. The Nasdaq 100 slid -0.90%, underperforming significantly, while the Dow Jones Industrial Average rose 0.9% for its fourth consecutive gain, closing at 44,495—just 1% shy of its all-time intraday high of 45,074 from December 2024.

US Senate vote pressures Tech giants

The sell-off in tech was triggered by the Senate’s approval of President Trump’s US$3.3 trillion tax and spending cut package. The legislation included the rejection of a proposal that would have limited individual US states from regulating artificial intelligence, delivering a blow to tech giants such as Microsoft, Meta Platforms, and Nvidia.

Fed and BoJ hold cautious policy stance

Speaking at the ECB Forum on Central Banking, Fed Chair Jerome Powell maintained his cautious “wait and see” stance on rate cuts, drawing further criticism from President Trump. Similarly, BoJ Governor Kazuo Ueda reiterated that the central bank will wait for more data, particularly around inflation and tariff impacts, before tightening further.

While the BoJ left its policy rate unchanged at 0.5% in June (a 16-year high), markets still anticipate one more 25-basis-point hike in Q4.

US dollar weakens further, but pace slows

The US dollar extended its losing streak to seven sessions on Tuesday, though at a slower pace, with the US Dollar Index down -0.1%. In today’s Asia session, the greenback is trading flat overall, registering minor gains against the euro (+0.08%) and yen (+0.14%), while holding steady against the pound and Australian dollar.

Asia equities mixed; Nikkei lags on tariff fears

Asia Pacific markets opened mixed. Japan’s Nikkei 225 underperformed with an intraday drop of -0.12%, following an early dip of -1% that tested the 39,390 support level. The slide came after President Trump threatened to raise tariffs on Japanese exports to 30%-35%, up from a proposed 24%, as trade negotiations falter ahead of the 9 July reciprocal tariff deadline.

Meanwhile, Hong Kong’s Hang Seng Index reopened from a public holiday with a 0.6% intraday gain, and Singapore’s Straits Times Index extended its rally by 0.5%, setting a new all-time intraday high of 4,010.

Gold holds gains above support ahead of US jobs data

Gold (XAU/USD) continues to consolidate near US$3,340, supported by its 50-day moving average at US$3,318. After a two-day rally that delivered a 2.9% gain, momentum has paused near the 20-day moving average resistance at US$3,360. Traders are now awaiting the US ADP Employment Change report for cues on the next directional move.

Economic data releases

Fig 1: Key data for today’s Asia mid-session (Source: MarketPulse)

Chart of the day – Nikkei 225 bounces from support, bullish trend remains intact

Fig 2: Japan 225 CFD Index minor trend as of 2 July 2025 (Source: TradingView)

The recent minor corrective decline of -3.4% seen on the Japan 225 CFD Index (a proxy of the Nikkei 225 futures) from its 30 June 2025 intraday high of 40,852 to 2 July 2025 intraday low of 39,527 has stalled at an intermediate key support inflection area.

Firstly, the lower boundary of a minor ascending channel has been in play since the last Monday, 23 June low. Secondly, the 50% Fibonacci retracement of the prior steep bullish breakout rally from 23 June 2025 low to 30 June 2025 high. Thirdly, the minor corrective decline of -3.4% may mark the end of a minor corrective wave 4 sequence, and the next possible move on the Japan 225 CFD Index may see the start of a minor bullish impulsive wave 5 sequence based on the Elliot Wave Principle (see Fig 2).

In addition, the hourly RSI momentum indicator has traced out a bullish divergence condition yesterday at its oversold region and staged a bullish breakout above a parallel descending resistance. These observations suggest yesterday’s downside momentum has eased.

Watch the 39,390 key short-term pivotal support for the next intermediate resistances to come in at 40,4040, 40,335, and 40,850/41,050 in the first step.

On the flip side, a break below 39,390 negates the bullish tone for an extension of the minor corrective decline to expose the next immediate supports at 39,145 and 38,850 (pull-back of the former range resistance from 13 May 2025 and close to the 20-day moving average).