Sample Category Title

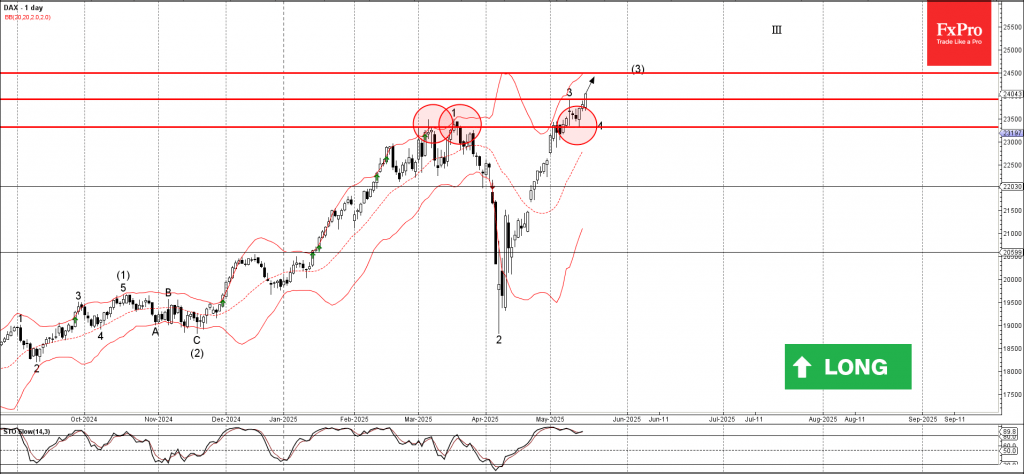

DAX Wave Analysis

DAX: ⬆️ Buy

- DAX reversed from the support level 23320.00

- Likely to rise to resistance level 24500.00

DAX index recently reversed from the key support level 23320.00 (former double top from March, as can be seen from the daily DAX chart below).

The upward reversal from the support level 23320.00 started the active minor impulse wave 5, which then broke above the minor resistance level 23925.00 (which stopped the previous impulse wave 3).

Given a clear daily uptrend, the DAX index can be expected to rise to the next resistance level 24500.00 (which is the target price for the completion of the active impulse wave (3)).

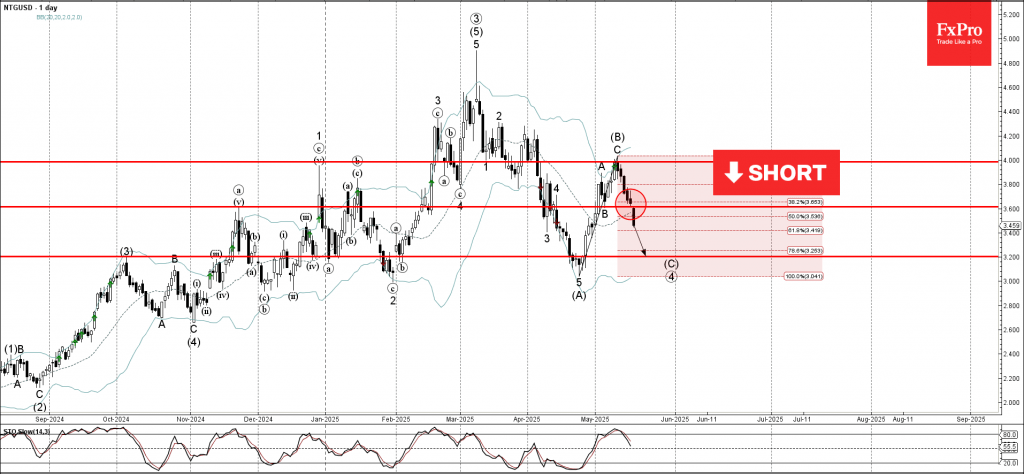

Natural Gas Wave Analysis

Natural Gas: ⬇️ Sell

- Natural Gas broke support zone

- Likely to fall to support level 240.00

Natural Gas recently broke the support zone between the support level 3.600 (which stopped the previous wave B) and the 50% Fibonacci correction of the previous ABC correction (B) from April.

The breakout of this support zone accelerated the active impulse wave (C) of the primary correction 4 from the start of March.

Natural Gas can be expected to fall to the next support level 3.200, which is the target price for the completion of the active impulse wave (C).

GBP/USD Rallies on Brexit Reset Deal, Dollar Weakness

On pace for its best six-monthly performance in over four years, 2025 has proven an interesting year for GBP/USD. In today’s session, GBP/USD trades higher on renewed trade policy optimism and a weaker dollar.

Key Takeaways

- Following the announcement of a major UK-EU trade deal this morning, GBP/USD trades +0.49% higher in today’s session, at around ~1.33468

- Recently, striking a first-of-its-kind trade agreement with the United States and a further deal with India, optimism about UK trade policy is boosting GBP/USD pricing, compounded by a general weakening of the US dollar

GBP/USD: UK-EU ‘reset’ deal dubbed the most significant since Brexit

Marketed as a ‘reset’ on relations, this morning’s announcement of a comprehensive UK-EU trade agreement has boosted sterling pricing and represents the third major trade deal the UK government has made in the last thirty days.

Spanning a range of crucial sectors, including fishing, energy, and agriculture, the agreement signifies a strengthening of UK-EU relations, which have been understandably shaky since the United Kingdom’s departure from the European Union in 2020.

As for GBP/USD pricing, the suggestion of further economic collaboration between the United Kingdom and the European Union has historically been positive for cable, with prices exceeding 1.34000 earlier today for the first time since May 6th.

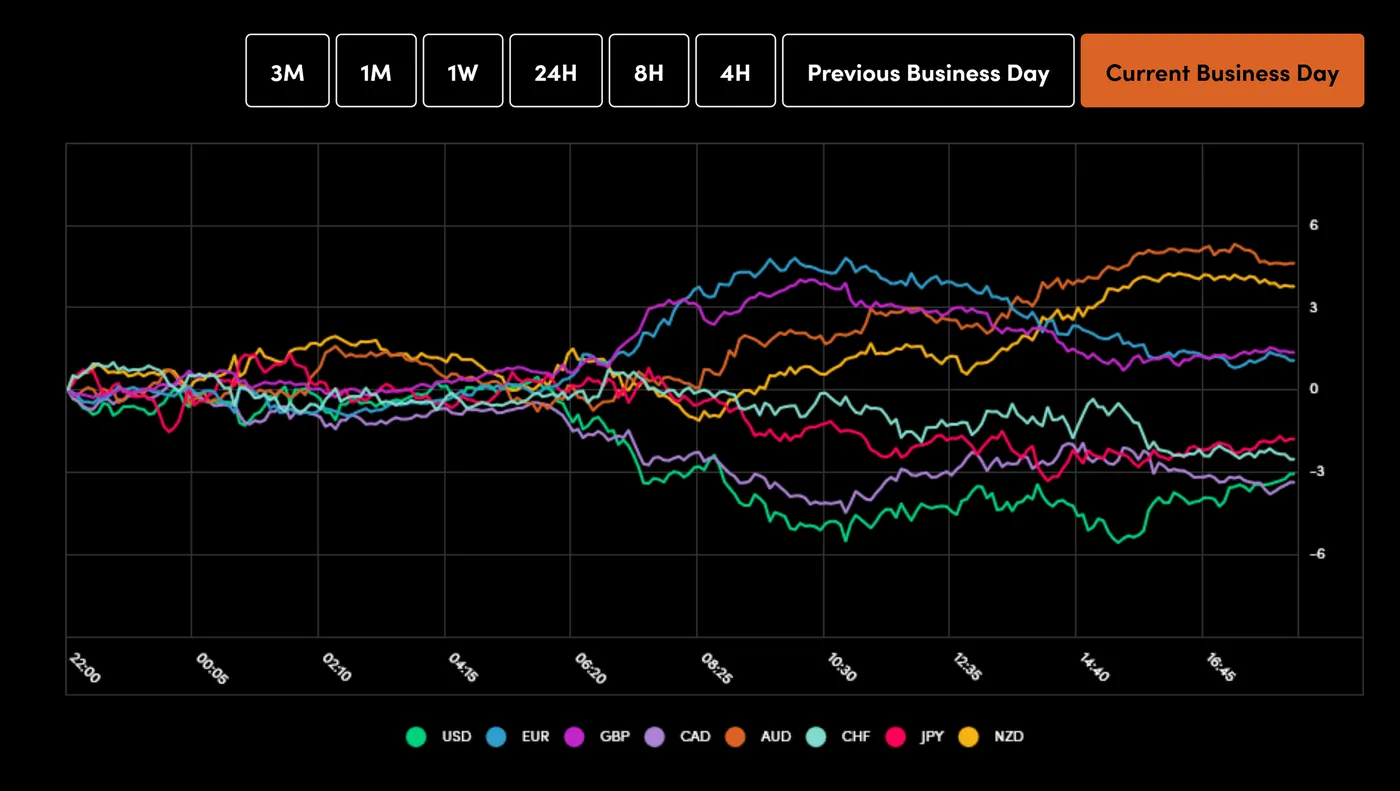

Currency Power Balance tool, OANDA Global Markets,19/05/2024

GBP/USD: Cable gains amplified by dollar weakness

With the recent downgrade of the United States’ credit rating serving as a somewhat unfortunate welcome to the weekend, the fallout of Moody’s report Friday evening has undeniably been negative for the greenback.

Downgrading outlook from stable to negative, the credit-rating agency raised questions over escalating national debt, quoting “Successive US administrations and Congress have failed to agree on measures to reverse the trend of large annual fiscal deficits and growing interest costs.”

Having stayed silent on the downgrade, the report could perhaps have come at a better time for President Donald Trump, who hopes to seek further congressional approval for his “big, beautiful” tax cut bill this week.

With the perception of the US economy somewhat swayed by Moody’s latest report, we can expect GBP/USD to gain in the short term.

GBP/USD technical analysis

- Remaining in an uptrend since January, GBP/USD outlook remains bullish in the medium to short term. Should price break above ~1.33757, bulls will likely target previous highs of 1.34442

- When using the 14-period RSI on the daily timeframe, GBP/USD markets are building bullish momentum, breaking above the SMA for the first time since early April, suggesting a potential for further moves to the upside

A chart showing the recent price action of GBPUSD. OANDA, TradingView, 19/05/2024

A chart showing the recent price action of GBPUSD. OANDA, TradingView, 19/05/2024

Fed’s Williams: Policy well positioned, Dollar concerns not yet materializing

New York Fed President John Williams noted that while the U.S. economy is currently performing well, rising uncertainty and shifting government policies warrant a patient approach on monetary policy.

He said monetary policy remains “slightly restrictive” and is “well positioned” to handle future developments.

“It’s going to take some time to get a clear view,” Williams said, emphasizing the Fed’s ability to “take our time” before making further moves.

Addressing concerns about the stability of Dollar assets, Williams acknowledged there are “rumors or concerns” stemming from recent fiscal and policy shifts. However, he downplayed immediate risks, noting that there have been no “major changes” in foreign inflows into the Treasury market.

Despite recent volatility in yields, he described bond markets as remaining “mostly range-bound.”.

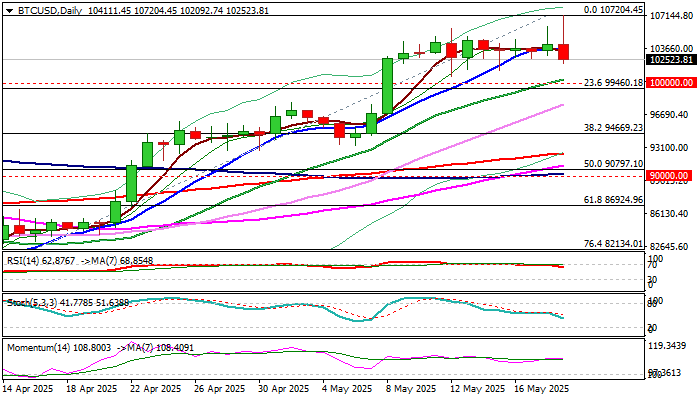

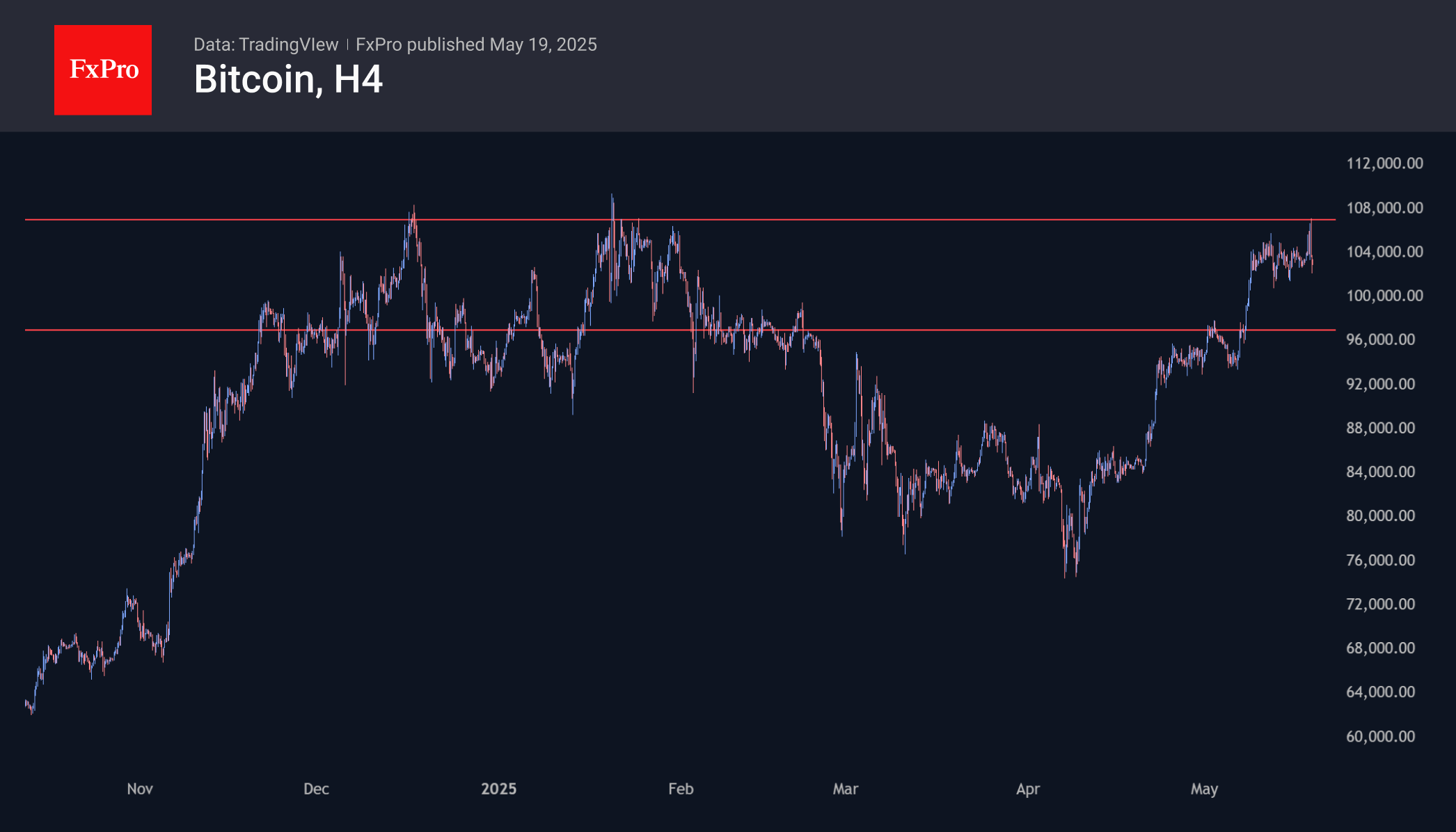

Bitcoin: BTCUSD Tumbles But Expected to Keep Overall Bullish Structure While Above 100K

BTCUSD accelerated lower on Monday, with 5K drop seen on quick pullback from sessions spike high to 107K zone.

Bitcoin reacted negatively to US rating downgrade and the price fell to the lower side of recent congestion (101K/107K) where it has been established after bulls faced strong headwinds on approach to new record high, but bids remained strong and limited dips.

Broader bullish bias is expected to remain while the price stays above psychological 100K level (reverted to solid support) and will keep in play hopes for renewed attacks at new all-time high and nearby psychological 110K barrier.

Daily studies remain bullish, despite violation of initial 10DMA support (103600) and contribute to expectations of prolonged consolidation (needs to hold above 100K) preceding fresh push higher.

Alternative scenario sees violation of 100K trigger as initial signal of deeper correction of 74389/107204 upleg.

Res: 105832; 107204; 109582; 110000

Sup: 101388; 100000; 99460; 97681

Sunset Market Commentary

Markets

Moody’s depriving the US from its Aaa credit rating late on Friday to some extent was a symbolic step. It didn’t bring profound, new insights on the US budget deficit and its debt (un)sustainability. However, it comes at the time when Congress is processing President Trump’s ‘Big Beautiful Bill’ that might reinforce the trends of unfunded spending via prolonged tax cuts, higher interest rate payments and debt climbing to levels not seen since immediately after WWII. With the market focus turning away from the trade truce of earlier last week, the Moody’s action put debt sustainability again in the spotlights. US assets were hit the hardest as the sell-US trade resumed. US yields add between 1 bp (2-y) and 6 bps (30-y). The 10-y tests 4.55%. The 30-y at 5%+, is coming closer to the 5.17% multi-year top from end 2023. The turmoil on US debt sustainability doesn’t inspire the Fed to leave its wait-and-see modus. Fed Bostic indicated that he is leaning to only one Fed rate cut this year as he remains mostly worried on the Fed’s inflation mandate. Of course, the US is not the only major industrialized economy facing budgetary challenges. As was the case with the early April US bond sell-off, UK gilts in particular look vulnerable to spill-over effects with the 30-y also adding 5.5 bps (5.45%). The 5.65% April top, the highest level since mid-1998, is again looming on the horizon. Moves in Japanese yields are more modest, but the 30-y yield is holding within reach of the 3% multi-year top touched last week. German yields range between little changed (2-y) and +3bps (30-y at 3.06%), off the intraday highs. Interestingly, today’s move had only limited impact on intra-EMU spreads (Italy-Germany 10-y spread +2 bps at a still low 103 bps). In its spring forecasts, the EC downgraded its EMU 2025 & 2026 growth forecast. The disinflationary impact from trade tensions is seen outweighing other upward divers. The EC sees inflation reaching 2% mid this year and averaging 1.7% next year. This disinflationary message from the EC initially only had limited impact on the intraday moves, but EMU bonds rebounded later in the session. Higher credit risk premia block last week’s positive equity momentum with US indices underperforming (S&P 500 -1.0%, Nasdaq -1.4%, EuroStoxx 50 -0.7%). No white smoke is expected from the Trump-Putin call later today.

Dollar losses initially were modest this morning, but gained traction during the European trading. DXY dropped from the 100.9 area to 100.3. Contrary to last week, the euro this time slightly outperforms the yen. EUR/USD rebounded from the 1.119 area to currently change hands near the 1.126 area. USD/JPY eases to 145. EUR/GBP (0.842) is losing marginal ground against the single currency. A rather wide-ranging deal between the UK and the EU, includes not only a defense and security partnership, but also an agreement on fishery and food standards and other regulation. Both parties also engaged to work to a solution on student exchange programs. However, for now any potential positives for the UK/sterling are overshadowed by the overall risk-off.

News & Views

The European Commission (EC) downgraded its real GDP growth forecasts in today’s spring update. They are conditioned on the current general US tariff rate of 10% and the 25% on steel, aluminum and cars and assume no EU retaliatory measures. Nor do they take in account the higher spending for defense because plans weren’t detailed enough yet. Euro area GDP would expand by 0.9% this year and 1.4% in the next. The weaker growth reflects a tariff-related hit to European exports, which would grow just 0.7% vs. 2.2% anticipated in the November update. Private consumption is the main engine powering the economy, alongside a rebound (although a less pronounced one than in November) of capital investments. Inflation is expected to cool more rapidly on the combination of lower energy prices, intensifying (Chinese) competitive pressures and a stronger euro. This is only partially offset by higher inflation in food and services. Prices in general would rise 2.1% in 2025 and 1.7% in 2026. EC budget deficit forecasts were raised from -2.9% in 2025 to 3.2% an would deepen further marginally in 2026 to 3.3%.

EU leaders gave initial approval to the €150n loan plan to help fund a defense infrastructure on a European level, the Financial Times reported. The formal green light is expected for next week. The European Commission will raise the money on capital markets before distributing it to member states as loans. The money can be spent on products where at least 65% of the components’ value are from arms companies in the EU, Ukraine, Iceland Lichtenstein, Norway and Switzerland. Third countries’ arms companies can account for a maximum of 35% of the purchase, unless they sign a bilateral defense pact with the EU. The EU and UK have signed such a deal today.

New Zealand Dollar Higher as US Credit Rating Downgraded

The New Zealand dollar has posted strong gains on Monday. Ahead of the North American session, NZD/USD is trading at 0.5912, up 0.53% on the day.

US dollar slips on Moody's downgrade

The US dollar is trading lower today against the major currencies, following a surprise downgrade to the US' credit rating on Friday. Moody's cut the long-term credit rating by on notch from "Aaa", the highest rating, to "Aa1". Moody's cited the country's "large annual fiscal deficits and growing interest costs". The move is largely symbolic as all other major credit rating agencies have pegged the US at "Aaa" and Moody's is simply joining the club. Still, investors have reacted by sending the US dollar broadly lower.

US Treasury yields jumped after Moody's decision. The 30-year Treasury yield jumped above 5% for the first time in six weeks and the 10-year yield pushed above 4.5%.

While Moody's was highlighting concerns over US fiscal policy, President Trump is pushing a bill that will provide massive tax cuts and further increase the US' debt. Currently, the debt stands at $36 trillion and Trump's bill would add $3 trillion to $5 trillion in debt.

China posts mixed data

In China, the week started with mixed data for April. Industrial production dropped to 6.1% from 7.7% but beat the market estimate of 5.5%. Retail sales fell to 5.1%, down from 5.9% and below the market estimate of 5.9%. Consumers are anxious about the economic uncertainty, especially the impact of the US-China trade war. The two sides have agreed to temporarily slash tariffs while they try to hammer out a trade deal which would go a long way at calming nervous investors.

NZD/USD Technical

- NZD/USD is testing resistance at 0.5911. Above, there is resistance at 0.5941

- 0.5888 and 0.5858 are the next support levels

NZDUSD 1- Day Chart, May, 19, 2025

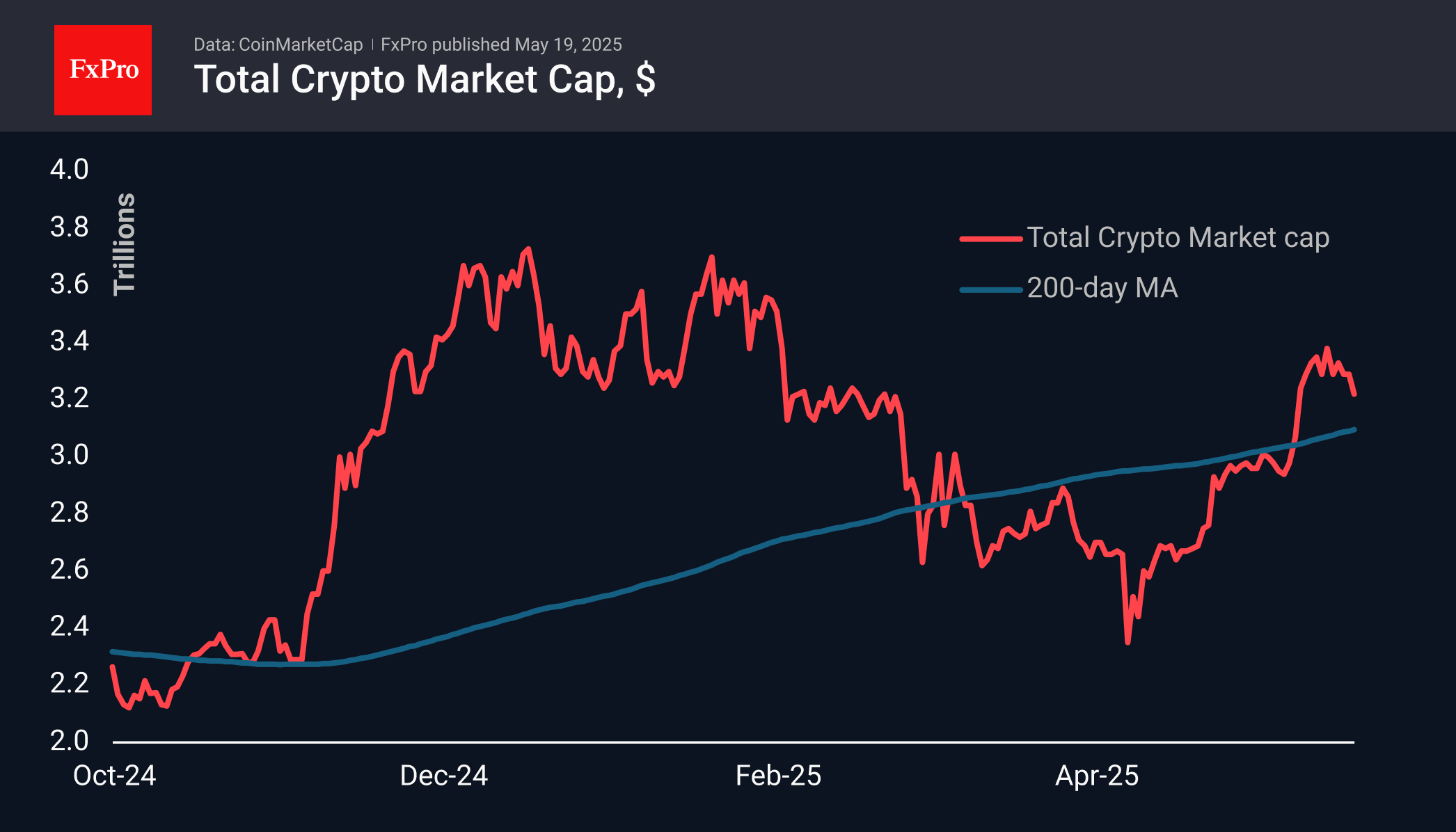

Bears Have Stopped Growth in Crypto

Market Picture

On Monday, the cryptocurrency market declined more than 4% compared to the previous week. The bears successfully neutralised several attempts to cross the $3.36 trillion mark, which weakened the participants’ sentiment and led to the return of capitalisation to the $3.24 trillion level. The area down to $3 trillion could be an easy target for the bears, as the market may need a tactical pause to consolidate its strength.

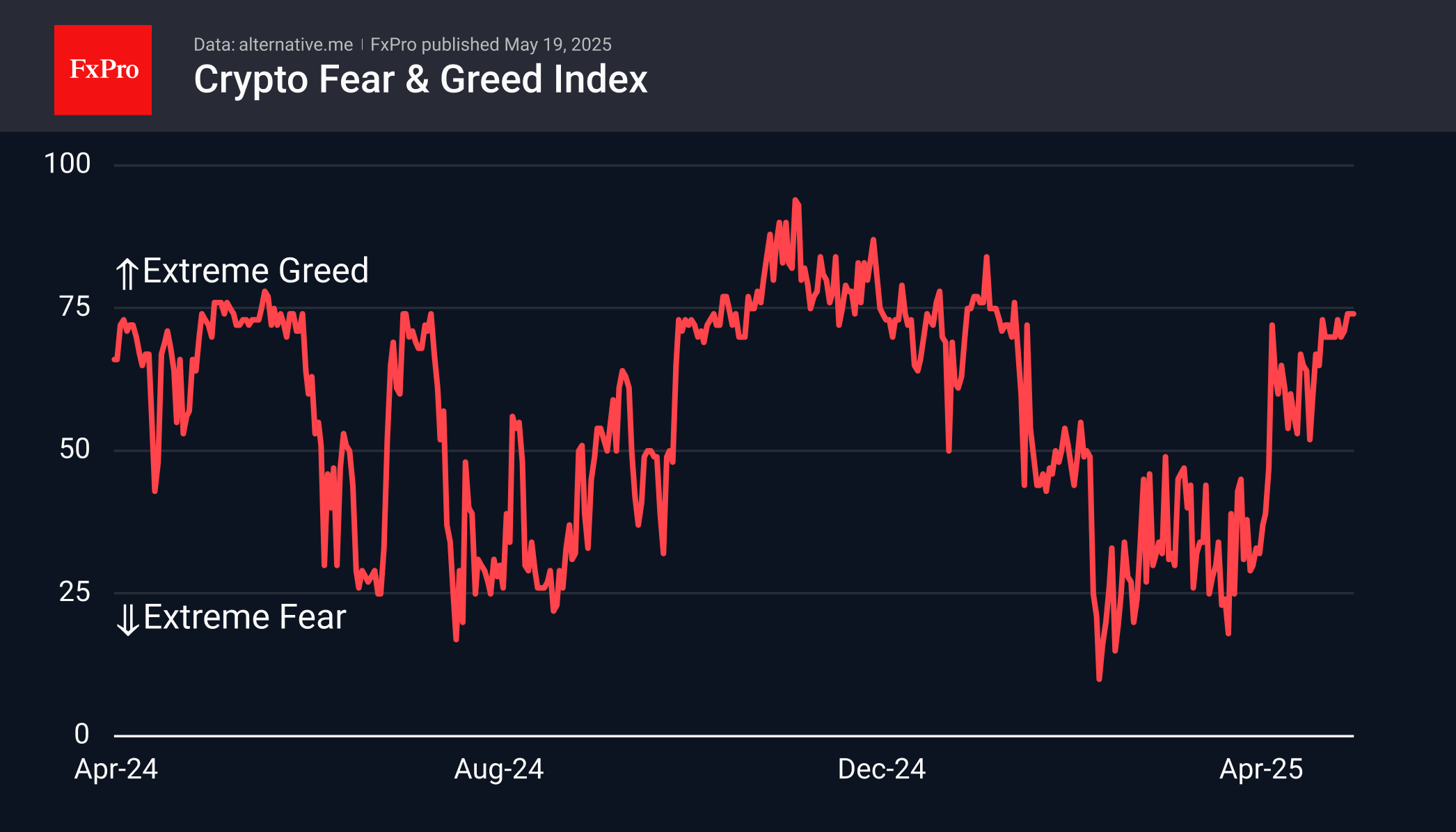

The Cryptocurrency Market Sentiment Index stabilised over the weekend at 74, close to extreme greed territory and the highest values since late January. These readings leave room for growth for both the sentiment index and prices.

Bitcoin hit the $107K level on Monday morning, triggering an intensified sell-off and quickly pulling back below $102K. During the European session, BTC stabilised around $103K, close to the average level of the last 10 days ($103.4K). A failed growth attempt could lead to a short-term pullback to $97K.

News Background

Significant inflows into spot bitcoin ETFs in the US have continued for four consecutive weeks. According to SoSoValue, net inflows into spot BTC-ETFs totalled $603.7 million over the past week, the lowest in eight weeks. Cumulative inflows since bitcoin-ETFs were approved in January 2024 totalled $41.77 billion, while net inflows into ETH-ETFs totalled $41.6 million last week, rising to $2.51 billion since July 2024.

HTX Research noted that lower US inflation and increased institutional participation support the current rally in the cryptocurrency market. Nevertheless, when key technical support levels are broken, the current consolidation may lead to a local correction.

JPMorgan believes that Bitcoin is likely to outperform gold in the second half of the year, thanks to corporate buying and growing support from US states. The shift in sentiment has already been evident in the past three weeks, with capital shifting from precious metals ETFs to spot BTC-ETFs.

According to the Fireblocks survey, 90% of banks, financial institutions, fintech companies and payment services plan to use or are already using stablecoins, focusing primarily on cross-border payments. Among the advantages mentioned by respondents, the first place is occupied by faster settlements.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.01; (P) 145.56; (R1) 146.19; More...

Intraday bias in USD/JPY stays neutral at this point. Fall from 158.86 might have completed at 139.87 already. Further rise is in favor as long as 144.02 support holds. Above 148.64 will target 61.8% retracement of 158.86 to 139.87 at 151.60 next. However, firm break of 144.02 will bring retest of 139.87 low instead.

.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.