Sample Category Title

How the ANZACs Might Handle the Trade Shock

This note discusses the key similarities and differences of the Australian and New Zealand economies with reference to how they might fare in this global trade shock.

Trade policy uncertainty is at extreme levels and could significantly impact the small open economies of Australia and New Zealand. Both countries could lose to some extent as global demand and the pattern of trade flows adjust. But beyond this common thread there are key differences that could determine how New Zealand and Australia will fare.

Trade and economic policy uncertainty has been very high for months now but really erupted this week. Financial markets swung wildly, especially in equity markets which ranged widely and where implied volatility levels have moved up towards the levels seen only during Covid, the 2012 European debt crisis and the 2008 global financial crisis.

There have been similar movements in the rules governing global trade flows. Tariff policies in the US and China especially have moved a lot – in some cases, in both directions. We are now in a transitional position of US tariffs of 10% tariffs on most countries and 145% tariff on China, while China has retaliated with 84% tariffs on US imports.

None of this is set in stone, as negotiations are ongoing, and US tariffs on non-Chinese imports are to be reviewed again in three months. And frankly, the US and China are not negotiating right now but are engaging in tit-for-tat retaliation. Hence uncertainty will remain very high.

There will be a lot of debate around the ultimate size of the change in global trade rules that the Australasian economies will need to adjust to. It’s hard to put a finger on the scale of that now. But it is interesting to reflect on the ways in which our economies might be both similarly and differently impacted as we go forward.

There are many common factors. Both countries are trade orientated; hence this global trade shock could have potentially profound implications for incomes and growth over both the short and longer term. We both have strong trade linkages with the US, China and South-east Asia. Hence weaker demand in those jurisdictions has the potential to impact our incomes – especially though lower export commodity prices.

We both have strong macroeconomic frameworks (including independent central banks) that should help us navigate any troubles to come. Our floating exchange rates will buffer us should very negative scenarios emerge. Our government debt loads are low and credit ratings top tier, providing resilience.

The bottom line in terms of the commonalities is that we are both exposed to the worsening global trade environment but have resilience factors which will help even as the global trade environment shifts to greater protectionism and balkanization of trade flows.

But there are also some key structural and cyclical differences that may matter. On the positive side of the ledger for Australia: its current account and fiscal position is unequivocally stronger than New Zealand’s and should imply more resilience to the global trade shock. Cyclically, Australian fiscal policy is easing from a position of strength, providing some support to consumption and growth. That will matter. Another key Australian strength is that it enters this period of uncertainty with stronger growth and output that is close to trend. Australian growth has been disappointing by historical standards, but the economy is not on the ropes already. The labour market in particular remains in decent shape, notwithstanding recent debates on whether the NAIRU is lower than previously appreciated and associated productivity questions.

On the New Zealand side of the ledger: a strength is that NZ is further through the monetary easing cycle than Australia – so there is more stimulus already in the pipeline. Both countries have room to ease if required, but Australian inflation may be a little higher than NZ inflation in core terms, reflecting the different positions in the cycle. New Zealand’s commodity prices have been strongly on the up in the last year as resilient demand has combined with constrained supply of agricultural export products.

New Zealand will be more resilient if global manufacturing weakens relative to consumption given its export focus on agricultural and food commodities compared to Australia’s industrial commodities and energy exports. Global industrial production could come off worse in the new tariff environment and supply chains may have further to adjust. People will still eat whereas global steel demand may or may not be resilient.

New Zealand’s main issue is that we go into this more uncertain environment with output significantly below trend, which is why policy has been easing. While the trade sector is well positioned to absorb a trade shock, it’s less the case for the domestic economy. A further issue is the New Zealand government is trying to tighten fiscal policy even though aggregate debt levels are low by global norms. The finance minister noted this week a determination to continue the consolidation process even in the face of a weaker global economy. That’s going to be a challenge.

The pattern of trade is quite interesting and could favour either country depending on how the global growth environment pans out. Australia’s trade is more heavily tilted towards China, North and South-east Asia. New Zealand is more reliant on trade with the US. Both countries have roughly the same sensitivity with respect to trade with developed countries. If US growth and consumption were to be hit relative to Asia, then New Zealand could be worse off. And of course, the opposite also applies.

The uncertainty around how the global economy will evolve means it’s hard to know whether there will be any ‘winners’ at the end of the day. Hopefully we both lose little in the end. But it’s important to consider the differences in the economies as we move forward into this mist of uncertainty.

USD/CHF: Safe Haven Swiss Franc Hits Highest Levels in a Decade vs US Dollar as Trade War Escalates

USDCHF fell to the lowest in ten years on Friday as safe-have Swiss franc shined on strong migration into safety, sparked by escalation of US-China trade war.

Friday’s drop of 1.7% until early US trading comes in extension of nearly 4% loss on Thursday (the biggest one-day drop in almost three years) and the pair is on track a weekly drop of around 4.5% (the biggest weekly fall since the second week of November 2022).

Fresh weakness broke below the floor of broader range on monthly chart that generates bearish signal of continuation of larger downtrend from parity zone (tops of Oct/Nov 2022) and exposes targets at 0.8000 (psychological) and 0.7840 (Fibo 76.4% of larger 0.7067/1.0343 uptrend).

Meanwhile, price adjustments on profit-taking could be anticipated, with likely limited upticks in very favorable environment for the Swiss franc, to provide better selling levels.

Swiss National Bank had no comments so far, but intervention to curb sharp gains of the national currency, cannot be ruled out.

Res: 0.8815; 0.8851; 0.8885; 0.8906

Sup: 0.8762; 0.8725; 0.8690; 0.8615

Sunset Market Commentary

Markets

The US of A is in decay. The improvised hawkish trade policy which will likely end in a US recession puts US assets for sale. China doesn’t back down. They raised tariffs on all US goods from 84% to 125%, still below the US level (145%) but starting tomorrow. The Chinese government vowed to resolutely counterattack and fight to the end. In a Ministry of Finance statement, Beijing states: “Given that American goods are no longer marketable in China under the current tariff rates, if the US further raises tariffs on Chinese exports, China will disregard such measures.” They call US actions a joke. President Xi Jinping warned that one that goes against the world risks being isolated themselves. The US trade policy in any case helps thawing the relation between the EU and US, as witnessed by talk on a late July summit, the Spanish visit to China and discussions on lowering tariffs on EV’s. In the meantime, the EC by name of President von der Leyen warned to expand the trade war to US services if talks during the 90-day pause in applying reciprocal tariffs fail. US President Trump is on a mission to narrow the US’s $1.21tn goods deficit with the world, but seems to forget the $295bn surplus on the services trade balance (financial services, travel, big tech,…). Taxing those services would be a huge and damaging measure.

It started with US equities, it spilled to long-term US Treasuries and now it arrived at the dollar. The trade-weighted dollar (DXY) lost the 2024 low (100.16) and briefly fell below the 2023 low (99.59) to test 62% retracement on the 2021-2022 USD-rally (98.98). Losing this support area would be highly significant from a technical point of view and suggest medium term full retracement to 89.21. EUR/USD already crushed this matching resistance zone (2024 top/2023 top/62% retracement at 1.1214/74/76). The pair set an intraday top at 1.1473, just below the 2022 top at 1.1495 which can be considered as intermediate resistance in the chase back to 1.2349. Apart from USD-weakness, the euro and other European assets (eg German Bunds) stand out as safe haven asset. Daily changes on the German yield curve currently range between -6.2 bps (2-yr) and -8.5 bps (30-yr). We see a different picture in the UK and the US where the very long end of the curve is again underperforming. A new Treasury sell-off is the key risk for the remainder of today’s session. The April Michigan consumer survey which grabbed market attention last months because of a huge spike in both short term (1y) and long term (5y-10y) inflation expectations only confirmed the stagflationary fears. Sentiment tumbled further (50. 8 from 57.0). At the same time 1-y inflation expectations jumped from 5.0% to 6.7%! LT expectations from 4.1% to 4.4% The US 30-y yield adds 6.0 bps and is holding near the 5.0% barrier (4.93). An uncontrolled sell-off has the potential to trigger emergency (liquidity) measures by the Fed (this weekend?) or a second Trump fold in the trade story.

News & Views

Brazilian inflation rose 0.56% M/M and 5.48% Y/Y in March, on the higher side of the consensus expectations and compared to 1.31% M/M and 5.06% Y/Y in February. All of the nine sub-components added to the monthly rise in inflation. The biggest contributor was food prices rising by 1.17% M/M (7.68% Y/Y). Indicators of core inflation and core services inflation still suggest persistent inflationary pressures. Bloomberg estimates the average of the core inflation measures of the BCB at 0.51% M/M. Y/Y inflation also moves further above the target band of the Central bank of Brazil (3.0% +/- 1.5% tolerance). The data confirm a scenario of another further rate hike at the May 7 monetary policy meeting, even the impact of global uncertainty might enter the debate. The central bank raised the policy rate from 13.25% to 14.25% at the previous meeting on March 19.

According to Reuters reporting and referring to domestic media and government sources, Japanese Prime minister Shigeru Ishiba today set up a task force to oversee trade talks with the US. The task force is presided by Economy Minister Akazawa. According to the local press, the Economy minister will on 17 April meet US trade representative Jamieson Greer and Treasury secretary Bessent. Akazawa indicates that US policy makers are interested in discussing non-tariff barriers but also FX policy. In this context, it won’t be easing for Japanese authorities to take action against a further rise of the yen against the USD. Aside from the negotiations with the US, Ishiba is also said have instructed his cabinet to compile an a supplementary budget as early as next week to put in place measures to respond to rising prices and to the effects of the high tariffs of the Trump administration for the Japanese economy.

US Michigan consumer sentiment crashes to 50.8; inflation expectations highest since 1981

US consumer sentiment plunged to 50.8 in April, far below expectations of 55.0 and down from 57.0 in March, according to the preliminary University of Michigan survey. This marks the fourth straight month of declines, with the index now down over 30% since December 2024.

The fall was broad-based: the current conditions gauge dropped from 63.8 to 56.5, while expectations fell from 52.6 to 47.2, highlighting growing concerns about economic prospects amid the intensifying trade war.

The timing of the survey is notable—it was conducted between March 25 and April 8, just before the US partially reversed some tariffs on April 9. Thus, the data largely reflects public reaction to the earlier escalation.

Perhaps the most alarming data point was the surge in year-ahead inflation expectations, which jumped from 5.0% to 6.7%—the highest since 1981. This marks the fourth consecutive month of half-percentage-point increases or more, underscoring the risk that inflation expectations could become unanchored.

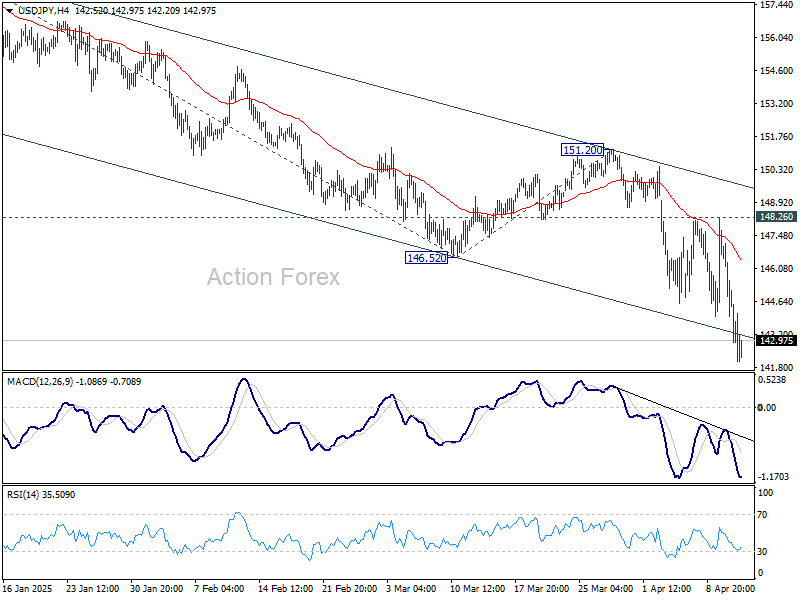

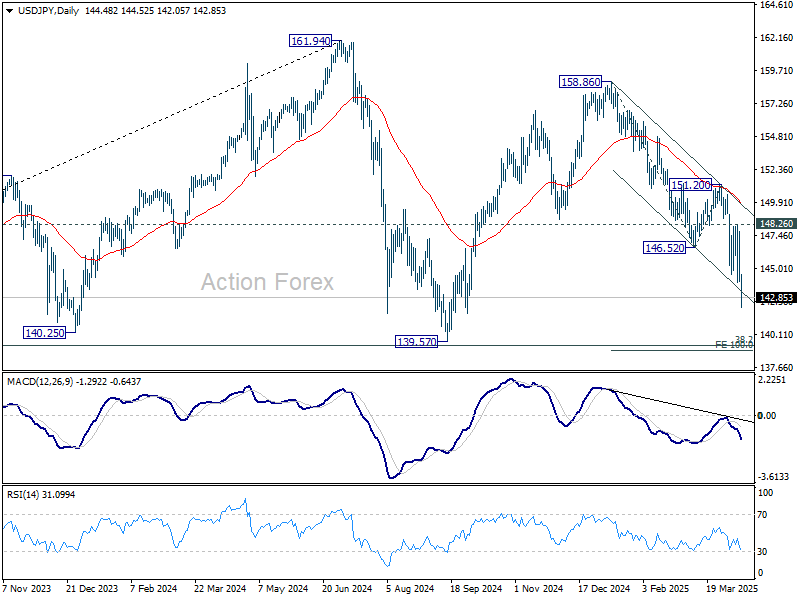

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.01; (P) 145.44; (R1) 146.86; More...

Intraday bias in USD/JPY remains on the downside for the moment. Current fall from 158.86 should target 139.57 support next. On the upside, break of 148.26 is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

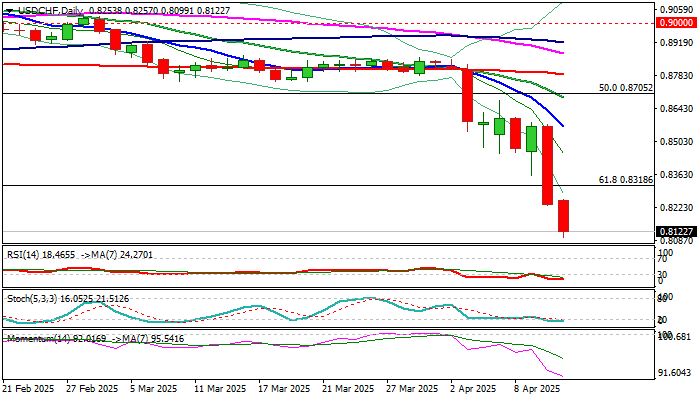

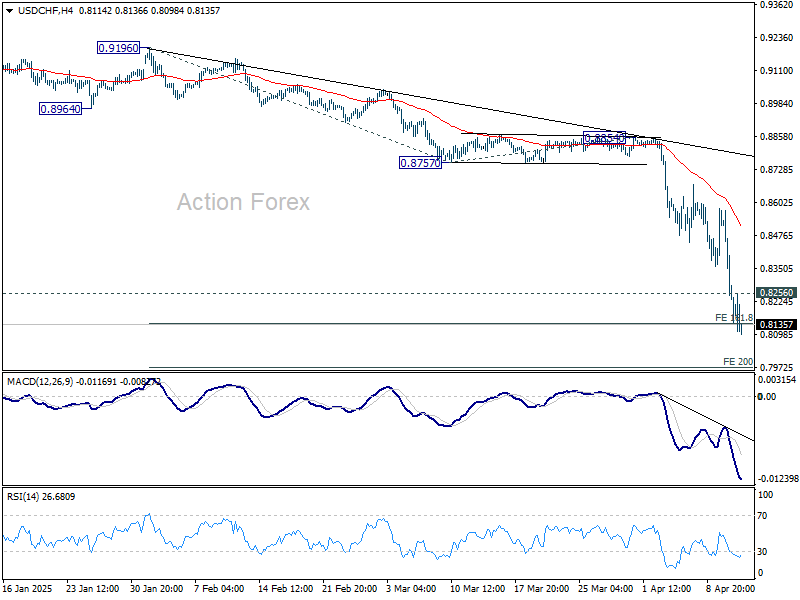

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8120; (P) 0.8350; (R1) 0.8467; More…

No change in USD/CHF's outlook and intraday bias stays on the downside. Next target is 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976. On the upside, above 0.8256 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

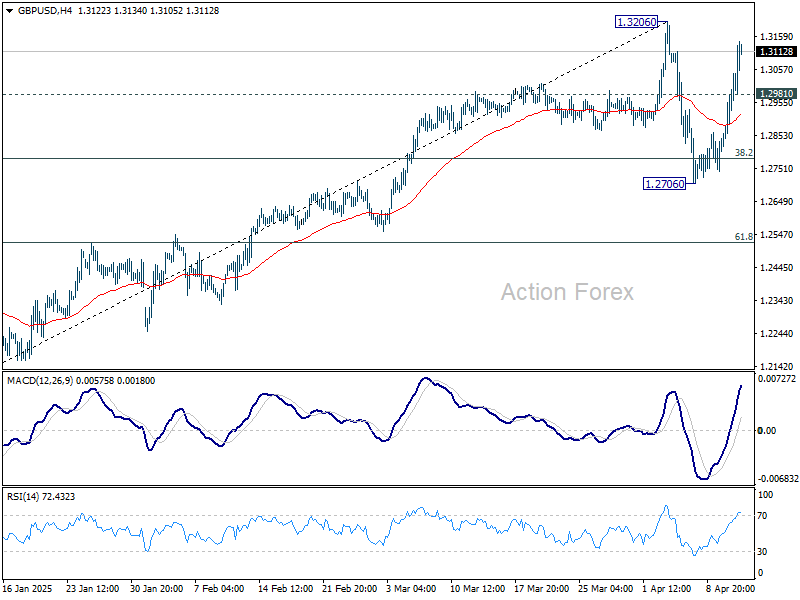

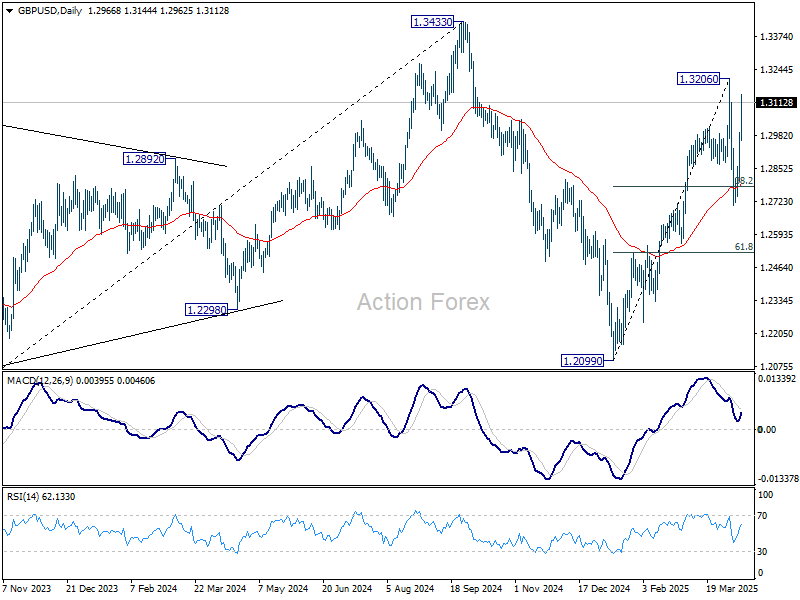

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2841; (P) 1.2918; (R1) 1.3049; More...

Intraday bias in GBP/USD remains on the upside for retesting 1.3206. Firm break there will resume the rally from 1.2099 towards 1.3433 high. On the downside, below 1.2981 minor support will turn intraday bias neutral again first. While corrective pattern from 1.3206 might extend, near term outlook will stay bullish as long as 1.2706 support holds, in case of another dip.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

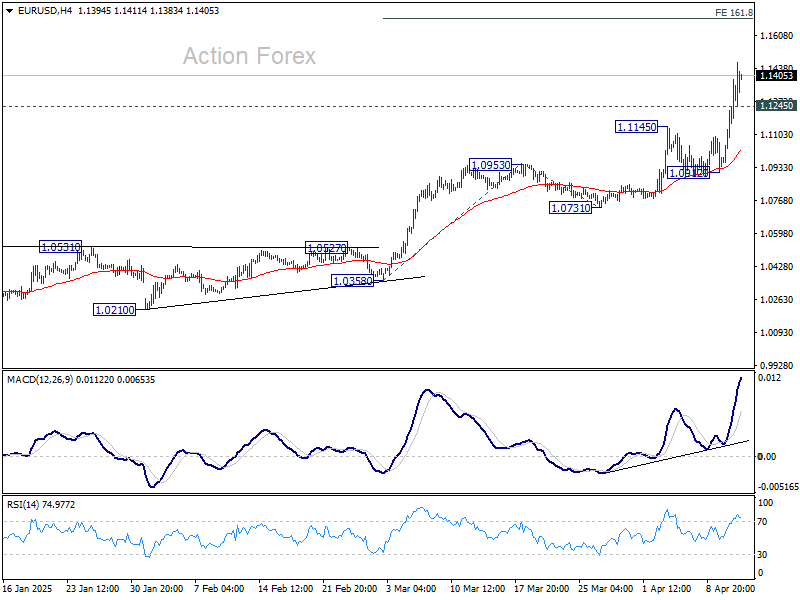

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1129; (R1) 1.1315; More...

EUR/USD's rally is still in progress and intraday bias stays on the upside. Current rise form 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694. On the downside, below 1.1245 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well above 1.0912 support to bring another rally.

In the bigger picture, break of 1.1274 (2024 high) indicates resumption of whole up trend from 0.9534 (2022 low). Next target is 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 55 D EMA (now at 1.0745) holds.

Dollar Selloff Extends Into Week’s End, Trade Talks With EU and JP Offset China Escalations

Financial markets showed signs of stabilization since European session, despite another round of retaliatory tariff hikes from China. While the latest move saw China raise levies on US goods to 125% from 84%, the response was widely anticipated and thus well absorbed by investors. Both President Donald Trump and President Xi Jinping have maintained uncompromising stances, so markets had largely priced in another step in the tit-for-tat trade war. The absence of any conciliatory tone keeps tensions high, but the predictability of the escalation appears to have dulled the market impact.

Also, China's latest move may have reached a symbolic peak. In a strongly worded statement, China’s finance ministry noted that at current tariff levels, “there is no longer a market for US goods imported into China,” implying that further retaliation may be economically futile. “If the U.S. government continues to increase tariffs on China, Beijing will ignore,” it added.

Some of the bearish sentiment from the US-China standoff is being offset by more constructive developments on other trade fronts. Negotiations between the US and both the European Union and Japan appear to be gaining traction. EU trade commissioner Maroš Šefčovič is scheduled to visit Washington on April 14 to meet US officials and continue discussions on tariff matters. Meanwhile, Japan’s newly formed task force, led by Economy Minister Ryosei Akazawa, is preparing for key meetings on April 17 with US Treasury and trade representatives.

Despite the stabilization in broader risk sentiment, Dollar continues to bleed, extending a week-long selloff and positioning itself as the worst performer among major currencies. Sterling is tracking as the second weakest despite a strong UK GDP report. Loonie follows closely behind, pressured by declining oil prices and general risk aversion.

Swiss Franc stands out as the week’s clear winner, underpinned by its status as the undisputed safe-haven, while Kiwi and Euro are also among the strongest performers. Aussie and Yen are positioning in the middle.

Eyes are now on the University of Michigan consumer sentiment report. Any significant surprises in that data could prompt a final reshuffling of currency rankings before markets settle for the weekend.

In Europe, at the time of writing, FTSE is up 0.50%. DAX is down -1.26%. CAC is down -0.45%. UK 10-year yield is up 0.048 at 4.699. Germany 10-year yield is down -0.067 at 2.516. Earlier in Asia, Nikkei fell -2.96%. Hong Kong HSI rose 1.13%. China Shanghai SSE rose 0.45%. Singapore Strait Times fell -1.83%. Japan 10-year JGB yield fell -0.031 to 1.346.

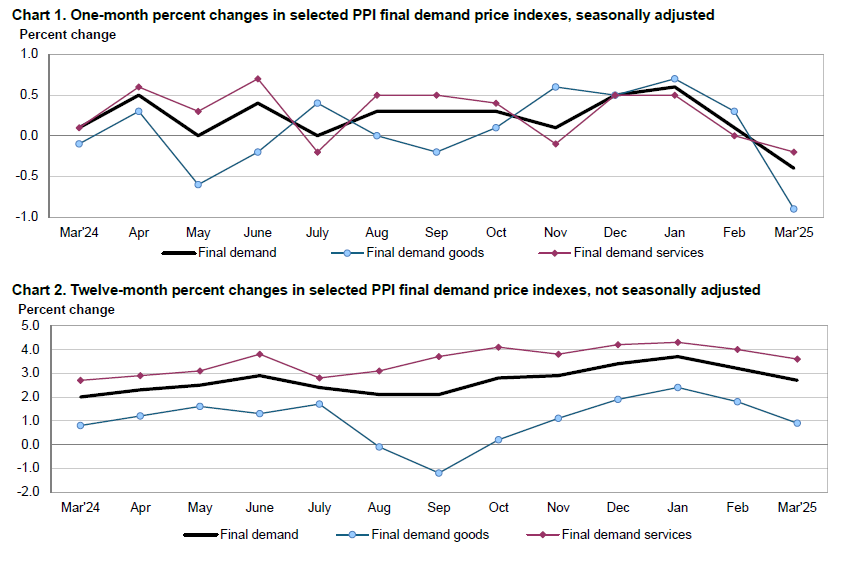

US PPI unexpectedly falls -0.3% mom in March

US producer prices posted a surprise decline in March, with the headline PPI for final demand falling -0.4% mom, well below expectations of a 0.2% mom rise.

The drop was driven largely by a -0.9% mom decline in final demand goods, while final demand services also slipped -0.2% mom.

On an annual basis, PPI slowed to 2.7% year-on-year from 3.2%, also below forecasts.

PPI excludes food, energy, and trade services, rose just 0.1% mom on the month, with the year-on-year rate at 3.4%.

EU’s Dombrovskis: Existing tariffs enough to shave up to 1.4% off US GDP, hit EU by 0.2%

EU Economy Commissioner Valdis Dombrovskis acknowledged the US decision to pause reciprocal tariffs above 10% for 90 days as a positive step that opens the door to negotiations. However, he cautioned that the existing 10% duties still in place on nearly all countries continue to weigh on the global economy. Additionally, the US has not lifted its 25% tariffs on steel, aluminum, cars, and car parts—measures that remain a significant source of transatlantic economic tension.

Dombrovskis pointed to a model simulations indicating that the current US tariff structure could reduce US GDP by 0.8% to 1.4% through 2027. While the economic fallout for the EU is expected to be milder—around 0.2% of GDP—he warned that the damage could escalate dramatically if tariffs become entrenched or retaliatory actions intensify.

Under such a worst-case scenario, Dombrovskis said US GDP could fall by as much as 3.3%, with the EU losing up to 0.6% and global GDP shrinking by 1.2%. The impact on global trade would be particularly severe, with an estimated contraction of 7.7% over the next three years.

UK GDP rises 0.5% mom in Feb, broad-based growth

The UK economy delivered a strong upside surprise in February, with GDP expanding by 0.5% mom, far exceeding market expectations of just 0.1% mom. All three major sectors contributed to the growth: services rose by 0.3% mom, production surged by 1.5% mom, and construction edged up 0.4% mom.

On a three-month rolling basis, real GDP grew by 0.6% to February 2025 compared to the previous three months, driven largely by a 0.6% rise in services output and a 0.7% gain in production. Construction, however, was flat over the period.

NZ BNZ manufacturing falls to 53.2, new orders signal trouble ahead

New Zealand’s BusinessNZ Performance of Manufacturing Index slipped slightly from 54.1 to 53.2 in March, but remained firmly in expansion territory. Production climbed to 54.2, the highest level since December 2021. Employment also posted a robust 54.7, marking its strongest result since mid-2021. However, a decline in new orders, which dipped below the 50-neutral mark to 49.6, raises concerns about the durability of this rebound.

BusinessNZ’s Catherine Beard acknowledged the resilience in activity and employment, but highlighted persistent challenges. Despite improving sentiment, nearly 58% of surveyed manufacturers cited negative conditions, pointing to weak demand, fewer new orders, and uncertainty across both domestic and export channels.

BNZ Senior Economist Doug Steel noted that the PMI data supports the case for manufacturing GDP growth in early 2025. Still, he cautioned that risks to the outlook are clearly tilted to the downside, "given recent extreme volatility on global markets following rapidly evolving US-driven trade policy changes."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1129; (R1) 1.1315; More...

EUR/USD's rally is still in progress and intraday bias stays on the upside. Current rise form 1.0176 should target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694. On the downside, below 1.1245 minor support will turn intraday bias neutral and bring consolidations. But downside should be contained well above 1.0912 support to bring another rally.

In the bigger picture, break of 1.1274 (2024 high) indicates resumption of whole up trend from 0.9534 (2022 low). Next target is 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 55 D EMA (now at 1.0745) holds.

US PPI unexpectedly falls -0.3% mom in March

US producer prices posted a surprise decline in March, with the headline PPI for final demand falling -0.4% mom, well below expectations of a 0.2% mom rise.

The drop was driven largely by a -0.9% mom decline in final demand goods, while final demand services also slipped -0.2% mom.

On an annual basis, PPI slowed to 2.7% year-on-year from 3.2%, also below forecasts.

PPI excludes food, energy, and trade services, rose just 0.1% mom on the month, with the year-on-year rate at 3.4%.