Sample Category Title

EU’s Dombrovskis: Existing tariffs enough to shave Up to 1.4% off US GDP, hit EU by 0.2%

EU Economy Commissioner Valdis Dombrovskis acknowledged the US decision to pause reciprocal tariffs above 10% for 90 days as a positive step that opens the door to negotiations. However, he cautioned that the existing 10% duties still in place on nearly all countries continue to weigh on the global economy. Additionally, the US has not lifted its 25% tariffs on steel, aluminum, cars, and car parts—measures that remain a significant source of transatlantic economic tension.

Dombrovskis pointed to a model simulations indicating that the current US tariff structure could reduce US GDP by 0.8% to 1.4% through 2027. While the economic fallout for the EU is expected to be milder—around 0.2% of GDP—he warned that the damage could escalate dramatically if tariffs become entrenched or retaliatory actions intensify.

Under such a worst-case scenario, Dombrovskis said US GDP could fall by as much as 3.3%, with the EU losing up to 0.6% and global GDP shrinking by 1.2%. The impact on global trade would be particularly severe, with an estimated contraction of 7.7% over the next three years.

XAU/USD: Gold Rises Above $3.200 on Trade War Escalation

Gold surged above $3200 and hit multiple record highs on Friday, fueled by fresh rise in safe haven demand on growing worries over escalation of trade war and weaker dollar.

The latest decision of President Trump to put all tariffs on hold for 90 days but to exclude China from the deal and to increase import duties on Chinese goods to 125%, shook the world on Thursday, while China’s counter measures with the same rate of tariffs, sent fresh shockwaves through global markets on Friday.

Gold was the top market performer on Friday, along with other safe haven assets, such as Swiss franc and Japanese yen.

Mounting fears about the magnitude of the impact from intensifying trade conflict between the US and China, raise risk of recession and is likely to continue to fuel demand for the yellow metal.

The price may accelerate towards $3500 zone in coming months if two sides do not reach agreement.

Mild correction should be expected in the near term as a result of partial profit taking from strong rally in past three days, with limited dips to provide better levels for renewed entry into bullish market.

Broken psychological level at $3200 reverted to initial support, followed by former top $3167, which should ideally contain dips.

Fibo projections of the upleg from $2956 mark net targets at $3248, $3273 and $3298.

Res: 3237; 3248; 3273; 3298.

Sup: 3200; 3175; 3167; 3136.

Crypto Helped by Dollar Weakness

Market Picture

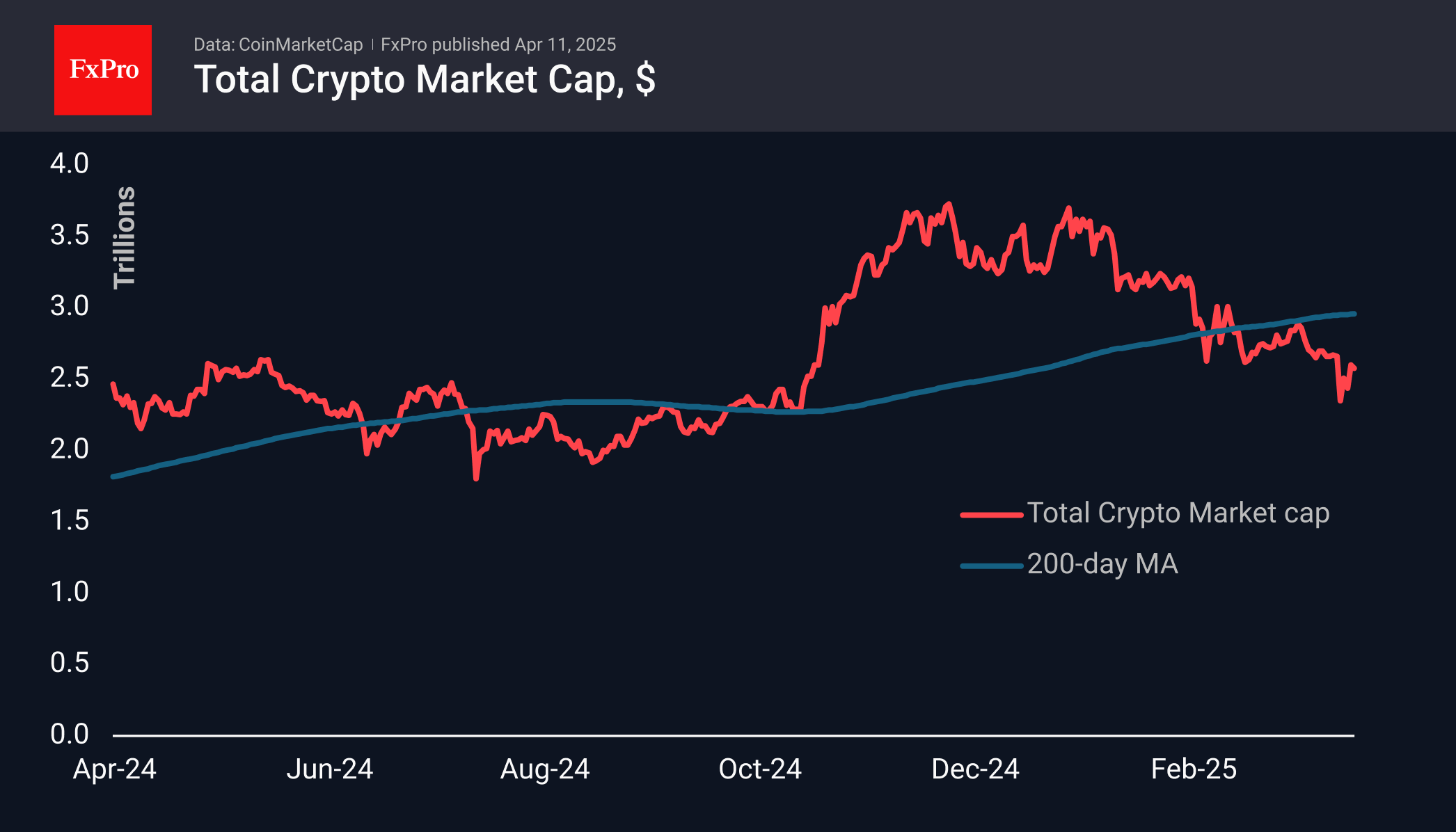

Crypto market capitalisation remained at $2.59 trillion on Friday morning, in line with the previous day’s values, despite a dip to $2.50 trillion overnight and a subsequent recovery on Friday morning. This contrasts with the slide in stock indices because a falling dollar supports cryptocurrencies. Like a rising tide, the dollar’s decline is lifting other assets.

Sentiment in the crypto market has returned to the extreme fear zone, sending the index to the 25 level.

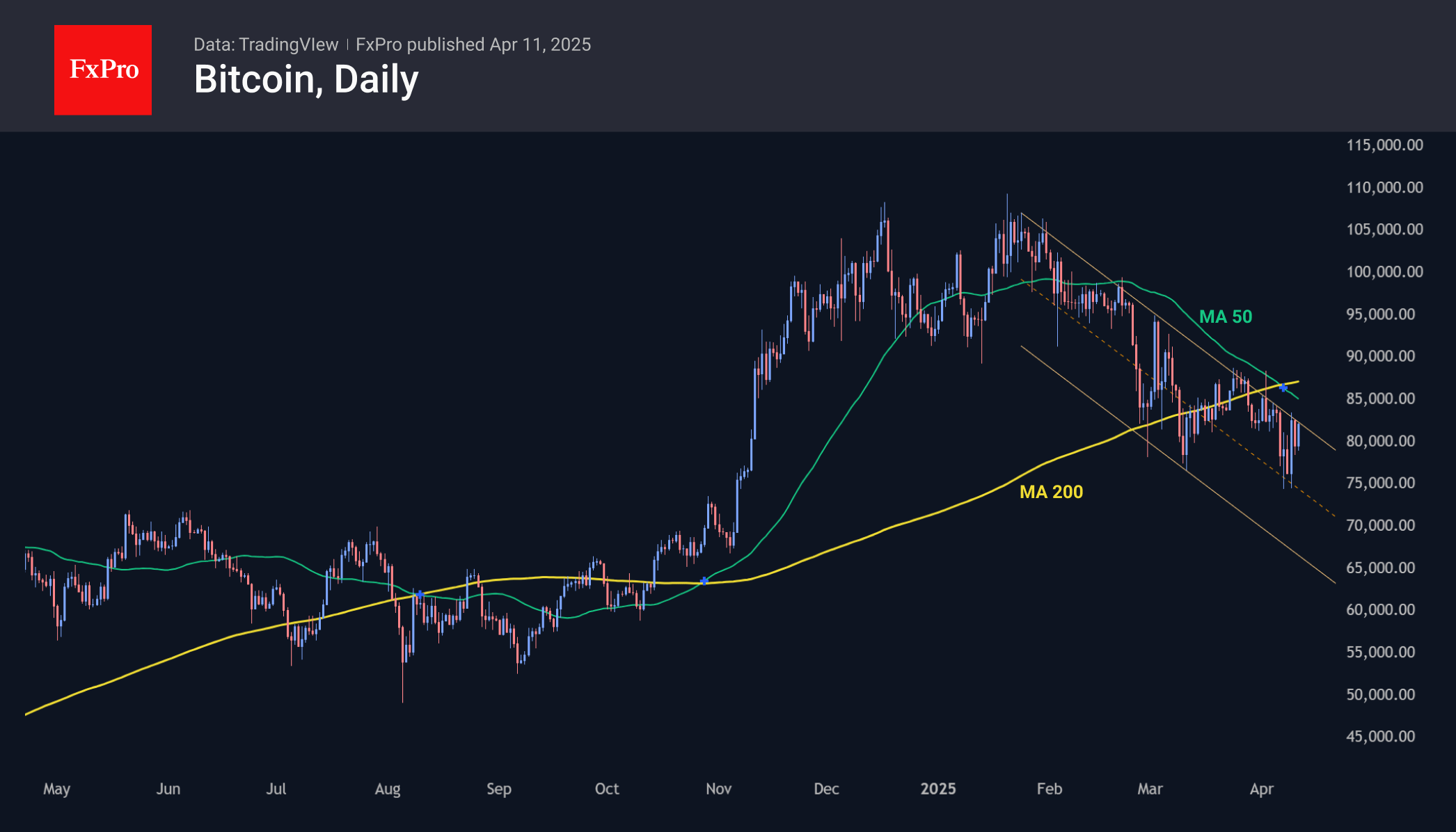

Bitcoin has been rising since early Friday, climbing above $81.4K, after closing just below $80K on Thursday. However, the first cryptocurrency has yet to confirm a growth reversal. The key area along the way is the $85K level, where the 50-day moving average passes. Its overcoming will be an important confirmation of the bullish sentiment, while fluctuations below it will remain market noise.

XRP and Tron found support this week on the decline to the 200-day moving averages. This small but encouraging signal suggests that market participants are still adhering to a ‘buy on dips’ strategy, believing in the continuation of the bullish trend.

News Background

A combination of on-chain metrics and technical indicators point to the need for Bitcoin to return above $93K to regain upward momentum, Glassnode noted. The correction has intensified selling by medium-term holdings, but their activity is slowing.

New Bitcoin sell-offs are possible in the coming weeks, but the bear market is likely to start in September, according to ‘il Capo of Crypto’. The analyst attributes this to the expected process of ‘global economic reset’, which may be accompanied by a major crisis – the first in BTC history.

The US Senate has approved the nomination of Paul Atkins to the post of SEC chairman. He is expected to focus on developing permanent standards for the regulation of digital assets.

The SEC authorised the listing and trading of options on spot Ethereum-ETFs from BlackRock, Bitwise and Grayscale. In September, the regulator already gave a similar authorisation for derivatives based on BTC-ETFs.

GBP/USD Peaks Above 1.3000 on UK GDP Beat, DXY Breaks Psychological 100.00 Barrier

- UK GDP grew by 0.5% in February 2025, exceeding forecasts and showing the strongest growth in 11 months.

- The US Dollar Index (DXY) fell significantly, reaching July 2023 lows.

- GBP/USD broke above the 1.3000 handle due to US Dollar weakness, with potential further gains depending on US dollar and tariff developments and upcoming UK data.

UK GDP was released this morning and showed the British economy grew by 0.5% in February 2025, bouncing back from a flat performance in January and beating forecasts of a 0.1% rise. This was the strongest growth in 11 months.

Industrial production jumped 1.5%, recovering from a 0.5% drop in January, thanks to a 2.2% increase in manufacturing. Notably, production of computers, electronics, and optical products rose sharply by 9.8%, while pharmaceuticals grew by 4.4%. Utilities went up by 2%, but mining fell by 3%.

The services sector grew by 0.3% after a 0.1% gain in January, driven by computer programming (up 2%), telecommunications (up 3.5%), and publishing (up 6.4%). Construction increased by 0.4%, bouncing back from a 0.3% drop, led by public works and repairs.

Looking at the quarter ending in January, the economy expanded by 0.6%.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar.

UK GDP - more noise than substance?

Monthly GDP data can be more noise than an accurate indicator. Last year, two strong months made up most of the growth in 2024, which seems unrealistic.

That said, the latest figures suggest there might be too much pessimism about the near-term outlook. Tariffs are a challenge, but their impact on UK producers is less direct. Instead, they could affect the UK through their effect on the US economy.

If US demand drops, it will eventually impact the UK. However, for now, the UK government’s big spending increase this year might provide some stability. Despite talk of spending cuts, real departmental spending is set to rise by 4% next year. Much of this will go towards wages, which should help support the economy.

Next week is a big week for the UK, with wage data and inflation data on the agenda. Jobs data will be key in the coming months and next week will provide market participants with another glimpse at the data.

In response to the data, the UK Chancellor of the Exchequer called the GDP data ‘encouraging’. The response from markets saw traders trim BoE bets after the data, with 85bps more cuts expected in 2025.

US Dollar Index (DXY) hits 2023 lows

US Dollar Index (DXY) Daily Chart, April 11, 2025

Source: TradingView

The dollar continued its fall on Friday as worries about the U.S. economy led investors to move away from U.S. assets and put their money into safer options like the Swiss franc, yen, euro, and gold.

The DXY sank as much 1.45% trading at a low of 99.44 which is a July 2023 low. This has seen a host of currencies gain ground against the Greenback with Cable being no exception.

Technical Analysis - GBP/USD

GBP/USD has been on a tear since the Monday low around the 1.2700 handle.

The move has largely been facilitated by US Dollar weakness rather than GBP strength and that has continued today as the DXY breached the psychological 100.00 barrier.

The weakness in the US Dollar has allowed GBP/USD to break above the 130.00 handle with the 2025 highs now in sight.

Further bullish moves may largely depend on the US dollar and tariff developments as markets wait on UK data next week.

Immediate resistance rests at previous highs around the 1.3200 handle, with the 1.3250 and 1.3400 levels up next.

A pullback for cable will bring the 1.3000 level back into focus before the 1.2864 and 1.2700 handles come into focus.

GBP/USD Daily Chart, April 11, 2025

Source: TradingView.com

Support

- 1.3000

- 1.2864

- 1.2700

Resistance

- 1.3200

- 1.3250

- 1.3400

EUR/USD Hits Three-Year High as the US Dollar Suffers Heavy Losses

The EUR/USD pair is in strong demand, surging to a three-year peak near 1.1330.

Key factors driving EUR/USD Movements

The market remains highly sensitive to growing investor concerns over the US economic outlook. Declining confidence in US assets continues to weigh on the USD.

Fears persist over the potential fallout from Donald Trump’s tariff policies. Although the imposition of steep tariffs has been delayed by 90 days, concerns about a slowdown in economic activity remain acute.

Current tariffs on Chinese goods stand at 145%, escalating trade tensions between the US and China and further dampening market sentiment. Meanwhile, the European Union has opted to suspend its retaliatory measures for the same 90-day period, with negotiators seeking a compromise.

The US dollar came under further pressure following the latest inflation data. The core consumer price index (CPI) rose by 2.8% year-on-year in March – the slowest pace since spring 2021. These figures have reinforced expectations of an imminent Federal Reserve rate cut.

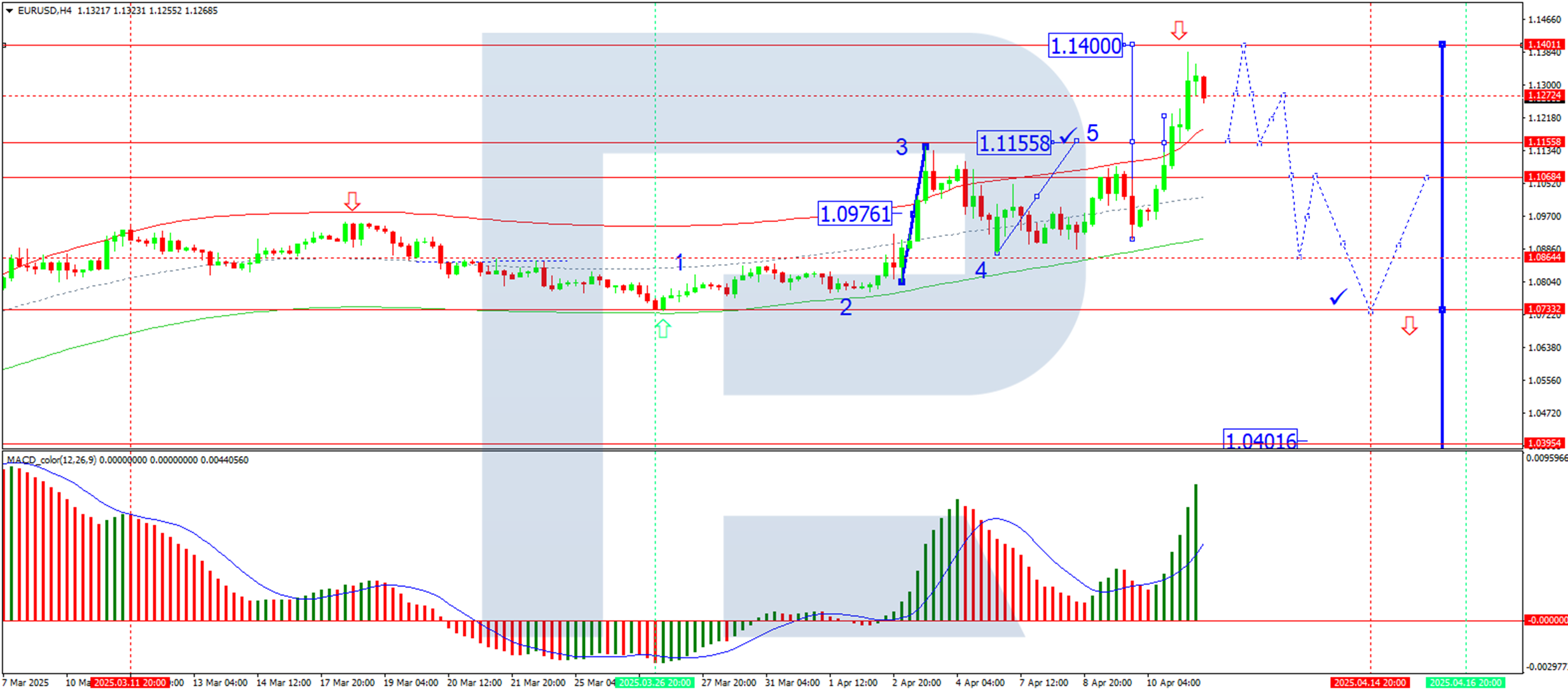

Technical Analysis: EUR/USD

H4 Chart Outlook

- The pair found support at 1.1155 before rallying to 1.1380

- A correction towards 1.1155 is possible in the near term

- Once this pullback concludes, another upside move towards 1.1400 may follow, marking the end of the current bullish wave

- This scenario is supported by the MACD indicator, with its signal line above zero and pointing firmly upwards

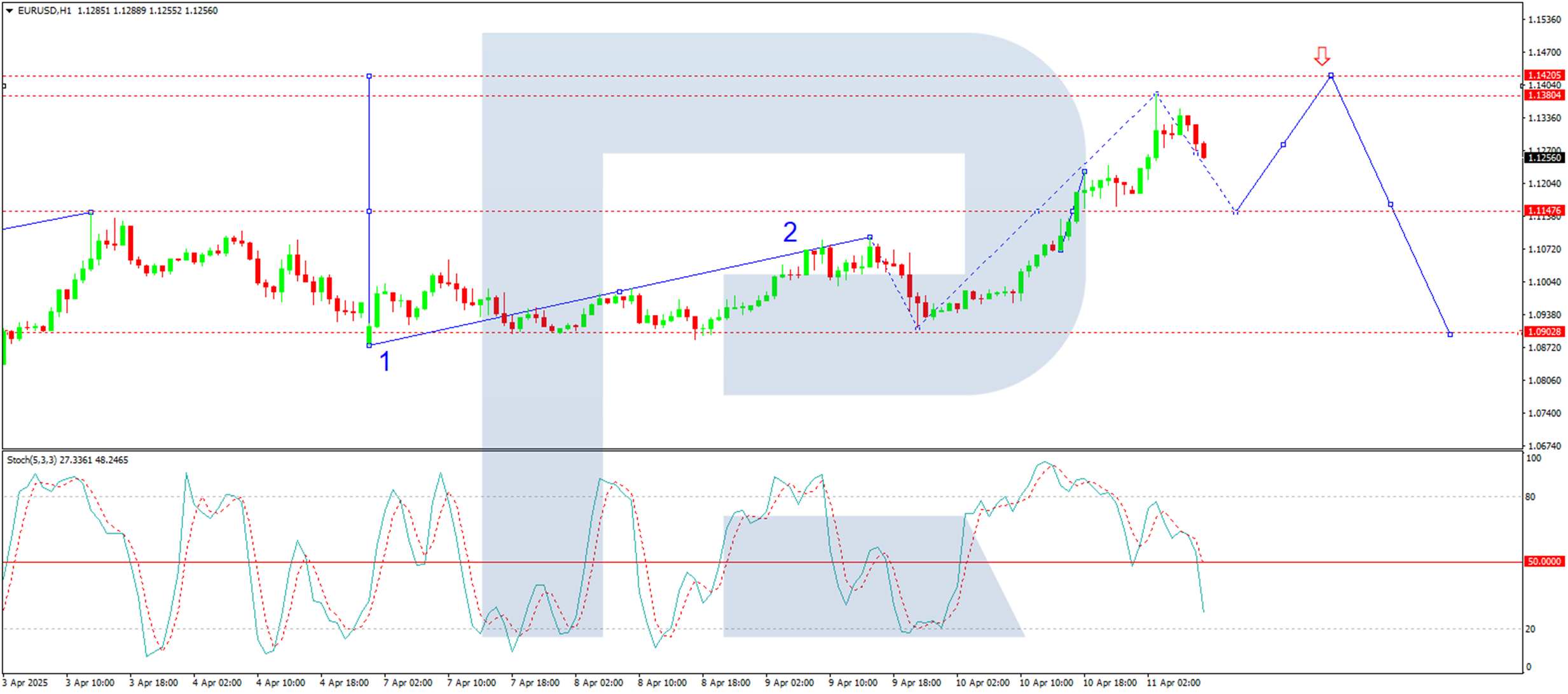

H1 Chart Outlook

- The market has achieved its local bullish target at 1.1380

- A corrective phase is forming, with 1.1155 as the next key level

- A rebound towards 1.1400 could occur later today, but a subsequent decline to 1.0900 could then come into play

- The Stochastic oscillator aligns with this view, as its signal line sits below 50 and is trending downwards towards 20

Conclusion

The EUR/USD rally reflects broad USD weakness, driven by economic concerns, trade tensions, and softening inflation. While a short-term correction is likely, the pair could extend gains towards 1.1400 before a deeper pullback materialises.

EUR/USD Hits Highest Level in Over Three Years

This morning, the euro surged above the 1.3000 mark against the US dollar for the first time since February 2022.

Throughout this week, the EUR/USD pair has broken through the highs of both 2023 and 2024.

Why Is EUR/USD Rising?

Amid the whirlwind of news surrounding the imposition and suspension of tariffs in US–EU trade, one dominant factor stands out — the sell-off of US bonds.

According to Reuters, long-term US Treasury bonds are being heavily sold this week. The yield on 10-year notes has jumped from 3.9% to around 4.4%, marking the steepest increase in yields since 2001. This may reflect a reaction by foreign holders of US debt to sanctions imposed by the White House, combined with growing uncertainty about the US economy — especially as recession fears gain more media attention.

As a result, the US dollar is showing weakness against a range of currencies, including the Japanese yen, Swiss franc, and the euro.

Technical Analysis of EUR/USD

The chart reveals a clear ascending channel (marked in blue), with the price repeatedly interacting with its upper, lower, and median boundaries — highlighted with markers and arrows.

Current bullish sentiment has pushed the pair towards the upper boundary of this channel. It’s possible this resistance line could halt further gains, potentially leading to a correction — perhaps down to the 1.11 level, which previously acted as a strong resistance point.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

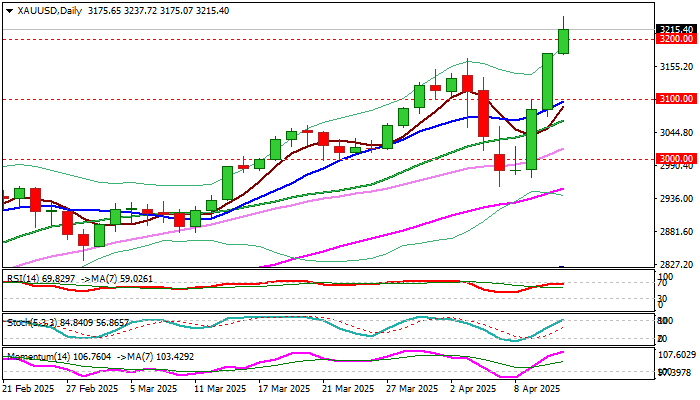

Gold Price Surpasses $3,200 for the First Time in History

According to the XAU/USD chart today, the price of an ounce of gold is fluctuating above the $3,200 level on global exchanges — a level never reached before.

Since the beginning of 2025, gold has gained approximately 22%.

Why Is Gold Rising Today?

Today’s bullish momentum in the gold market is driven by two key factors.

First, inflation data. Figures released yesterday for the CPI (Consumer Price Index) revealed a slowdown in inflation in the United States. This suggests a greater likelihood of monetary policy easing by the Federal Reserve. According to Reuters, gold prices now reflect expectations of three interest rate cuts by the end of 2025 — and lower rates typically support a stronger XAU/USD.

Second, fears of a global recession. Although US President Donald Trump has introduced a 90-day delay on the implementation of international trade tariffs, this does not apply to China, where tariffs have been increased to a striking 145%. Traders fear that Beijing could retaliate by raising tariffs on US goods beyond the current 84%.

Technical Analysis of XAU/USD

At present, the gold market is showing strong upward momentum, which began in early March (as illustrated by the blue trend channel). Key points include:

→ A breakout above the upper boundary of the channel;

→ The RSI indicator suggests a potential bearish divergence forming.

This points to the possibility of a short-term pullback into the blue channel, which would be a natural correction — especially considering the rapid $200 surge from $3,000 to $3,200 over just two days. However, given the current news backdrop, it seems unlikely that the bulls will relinquish control anytime soon.

For long-term gold price forecasts → read the article: Analytical Gold Price Predictions for 2025 and Beyond.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

We Don’t fight the Sell America Trade, Not in Treasuries and Not in Dollar.

Markets

US President Trump on Wednesday announcing a pause in the roll-out of reciprocal tariffs beyond the 10% base rate (expect for China) apparently wasn’t the game changer and confidence reset that the government hoped for. Yesterday’s price action indicated instead investors took it as an opportunity to sell America on up-ticks. US equities fell prey to a substantial retracement on Wednesday’s historic rebound (Nasdaq -4.31%). Developments in the US Treasury market are even far more worrisome. Softer than expected US March CPI inflation were only a footnote. The US yield curve again steepened. The 2-y easing 4.6 bps was no more than technical trading, assessing ongoing Fed guidance that the stagflationary impact of tariffs is a reason to stay on hold for longer. However, red alert is still flashing at the very long end of the US Treasury curve. The closely watched 30-y US Treasury Auction showed decent bidding metrics. So far the good news. The auction however, in no way was able to arrest the intraday slide in US long bonds. In the end, the 30-y yield again added 13.75 bps. Also remarkable: the rise was driven by a sharp move in the real yield. In the current environment, this suggests a higher risk premium, rather than anything else. Even more striking. The divergence with the performance of German Bunds couldn’t have been bigger. ST German yields rise marginally (a limited easing of ECB rate cut bets), but as the day proceeded, the Bund contract soon captured a solid safe haven bid. The 10-y yield more than fully reversed the rise at the open to close even 1.1 bp lower. Investors looking for a new safe haven alternative in German Bunds? Something to watch out for. Even so, the underperformance of Treasuries/outperformance of Bunds is currently going hand-in-hand with aggressive USD selling and a strong outperformance of the euro. With the yen (USD/JPY 143.5 area) and the Swiss franc (EUR/CHF 0.927) also attracting safe haven buying interest. Red alert also in the DXY index (100.4). The 2023/2024 lows (99.6/101.15) are already under test. A break of 98.98 (62% retracement of 2021/2022 rise) would signal a further sharp deterioration. Similar narrative for EUR/USD. EUR/USD 1.1276 (2023 top) is at risk of breaking. Another indication of the sell-Amerika on (quasi non-existing) upticks.

Risk sentiment in Asia this morning remains fragile (Nikkei -3.6%). The dollar and US treasuries struggle to avoid further losses. Regarding the data, University of Michigan consumer confidence will be closely watched. Another jump in inflation expectations (already expected at 5.2% 1-y ahead and at 4.3% for 5-10 y) would give (US Treasury) investors a highly uncomfortable feeling going into the weekend. We don’t fight the sell America trade, not in US Treasuries and not in the dollar. A confirmed break in EUR/USD would in a first instance bring the 1.1495 2022 intermediate top in the picture. The 2021 top stands at 1.2349. In the UK, February production data this morning were better than expected. It’s doubtful this will change fortunes for sterling (against the euro). The EUR/GBP pair already tested the 0.87 barrier. In the UK, the focus also remains at the long end of the Gilts curve with the 30-Y yield still uncomfortably high at 5.43%.

News & Views

Hong Kong-based newspaper the South China Morning Post reported that to EU officials are planning to make a visit to China for a meeting with Chinese president Xi Jinping in late July. People familiar with the matter indicate that EC von der Leyen and European Council President Costa agreed to the summit which breaks with protocol since the EU and China previously met in China as well. In more signals that the hawkish US trade policy is improving ties between the two blocks, Handelsblatt yesterday reported that they started talks on abolishing EU tariffs on Chinese EV’s while Spanish PM Sanchez concluded his visit to the country by calling for mutually beneficial relations and to promote balanced trade and investments.

Bank of England governor Breeden commented on the escalating trade war and the unravelling of leveraged trades in the US Treasury market. Regarding trade, she singled out a potential weakening in the UK currency as key in defining the inflation outlook by making UK imports more expensive. It has not happened yet, but “that could change”. On the turbulence in the Treasury market, she said that it’s not obvious that the right thing to do is to intervene in the gilt market. The long end of the UK curve underperformed as well with the UK 30-yr yield reaching its highest level since 1998 and bringing back the echo of the Truss-Kwarteng crisis. “What we can do is be aware of what’s going on and have repo facilities, ways of providing liquidity to the system to try and ensure that whatever trading happens, happens as smoothly as possible.”..

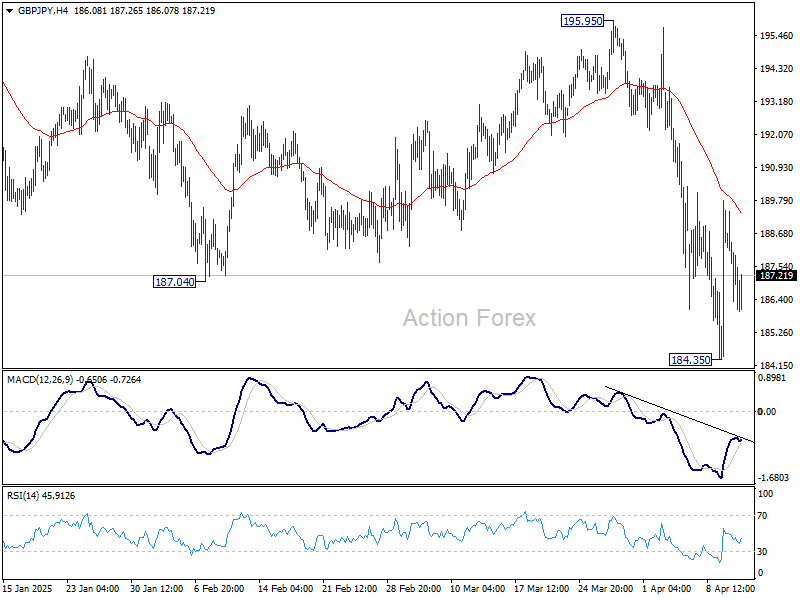

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.94; (P) 187.77; (R1) 189.19; More...

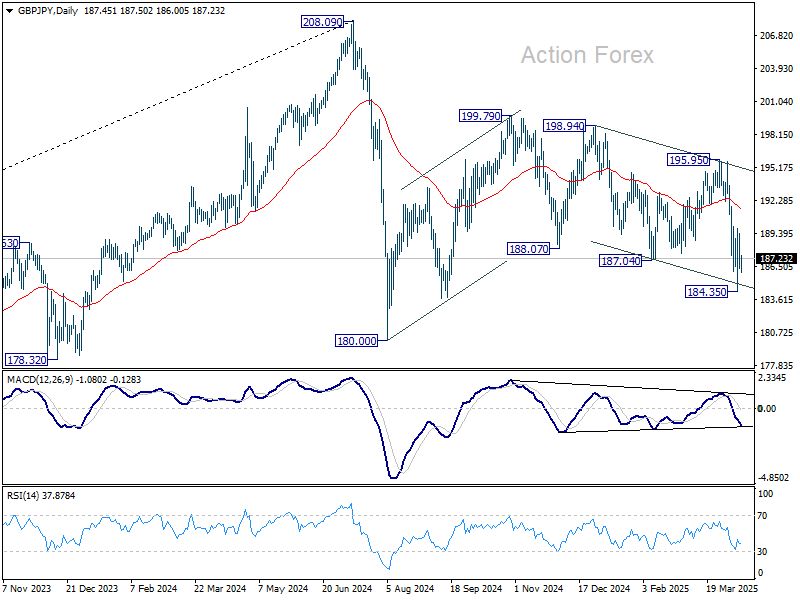

Intraday bias in GBP/JPY remains neutral for the moment. Risk will stay mildly on the downside as long as 55 4H EMA (now at 189.56) holds. Break of 184.35 will resume the whole fall from 199.79. Nevertheless, sustained trading above 55 4H EMA will bring stronger rally back to 195.95 resistance instead.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

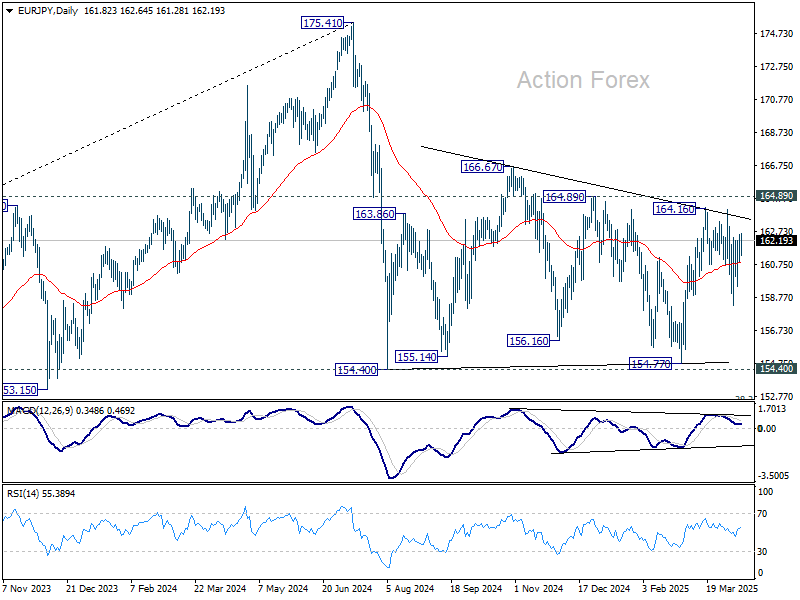

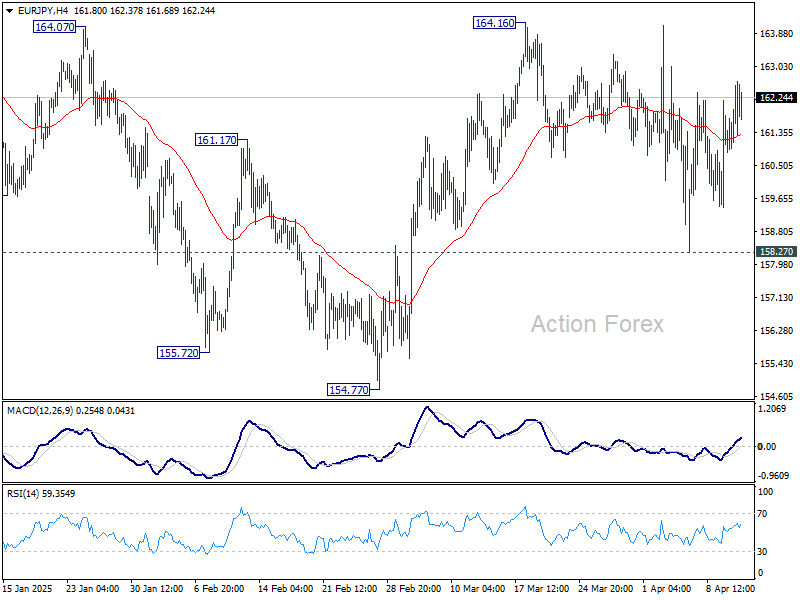

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.93; (P) 161.76; (R1) 162.64; More...

Intraday bias in EUR/JPY remains neutral for the moment. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.