Sample Category Title

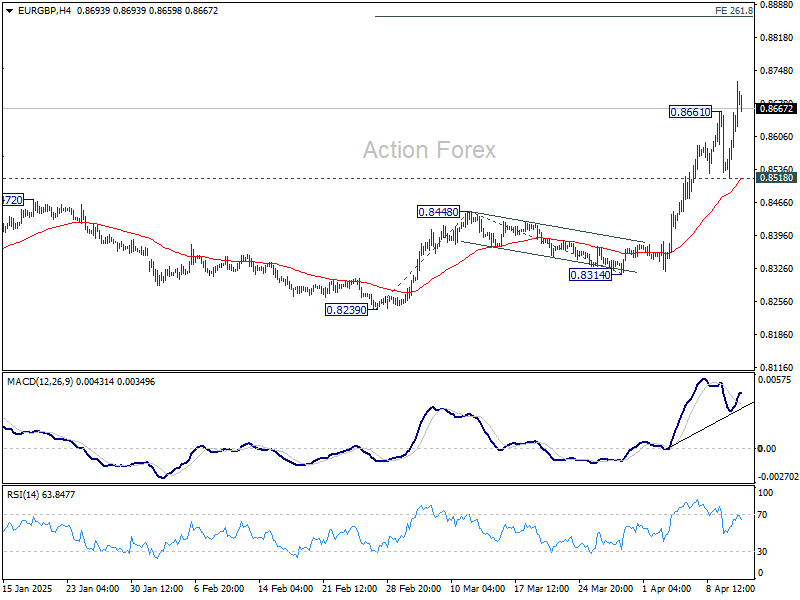

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8551; (P) 0.8606; (R1) 0.8691; More...

EUR/GBP's rally resumed after brief retreat and intraday bias is back on the upside. Current rise should target 261.8% projection of 0.8239 to 0.8448 from 0.8314 at 0.8861. On the downside, break of 0.8518 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, firm break of 0.8624 cluster resistance (38.2% retracement of 0.9267 to 0.8221 at 0.8621) should confirm the case of bullish trend reversal. That is down trend from 0.9267 (2022 high) has completed at 0.8221, just ahead of 0.9201 key support (2022 low). Further rise should be seen to 61.8% retracement at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

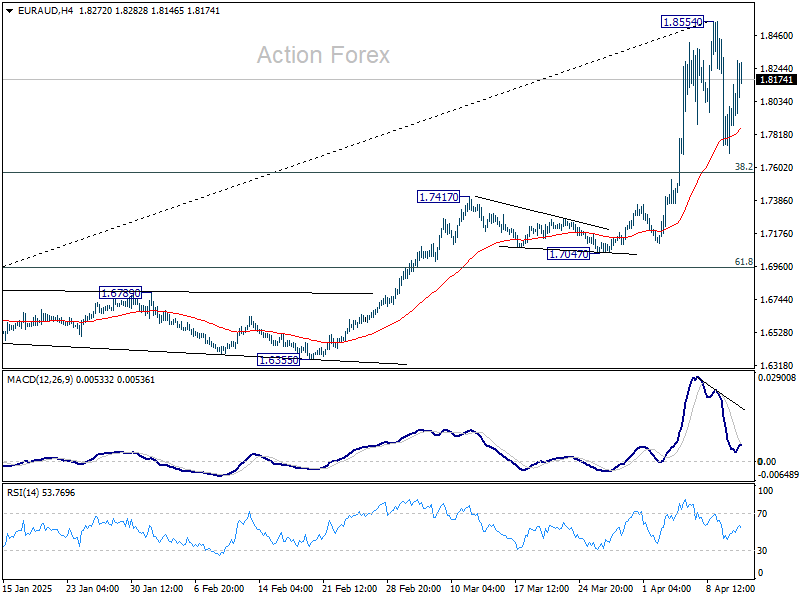

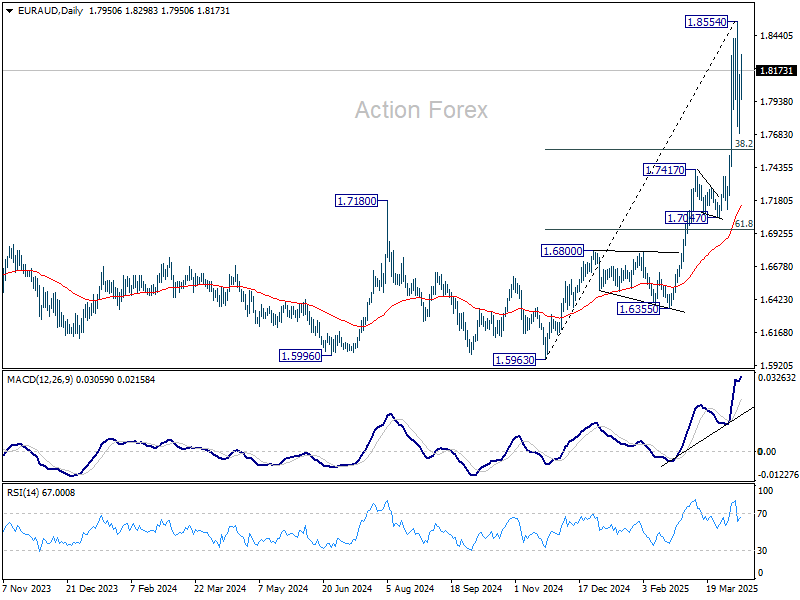

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7509; (P) 1.8033; (R1) 1.8319; More...

Intraday bias in EUR/AUD is turned neutral again with current recovery. Consolidations from 1.8554 could extend further. But in case of another dip, downside should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

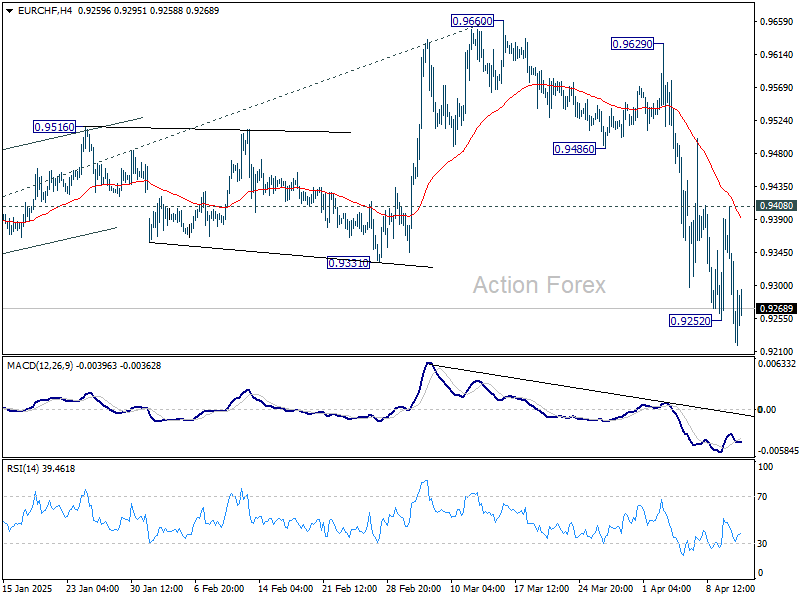

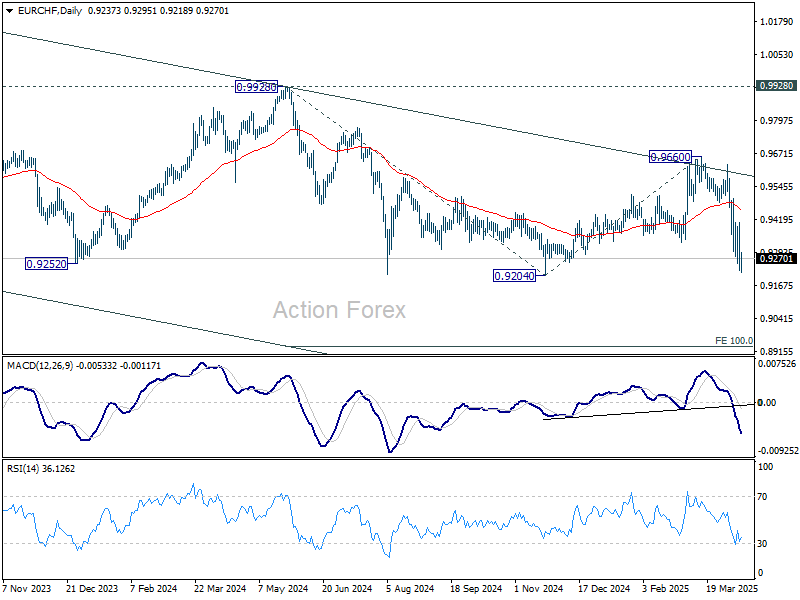

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9166; (P) 0.9288; (R1) 0.9350; More....

EUR/CHF's fall from 0.9660 resumed after brief recovery and intraday bias is back on the downside. Firm break of 0.9204 key support will confirm larger down trend resumption. On the upside, break of 0.9408 resistance is needed to confirm short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. Next target is 100% projection of 0.9928 to 0.9204 from 0.9660 at 0.8936.

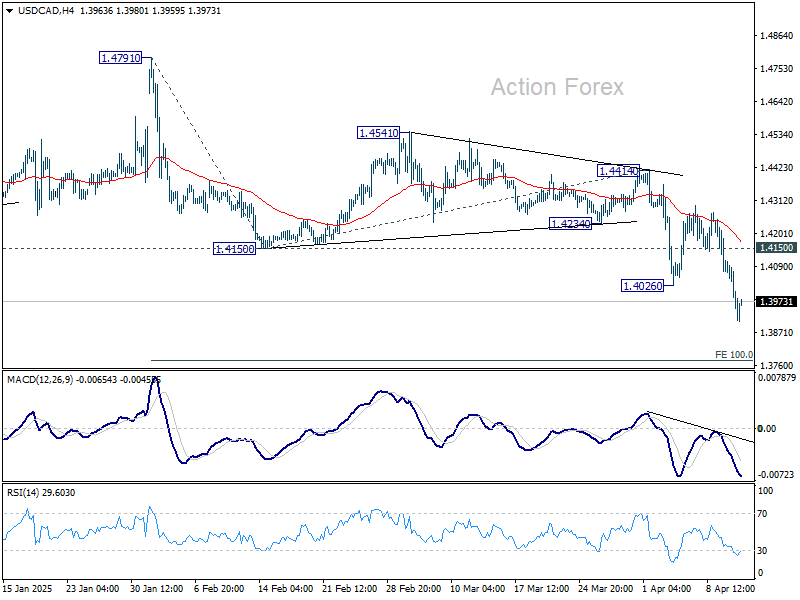

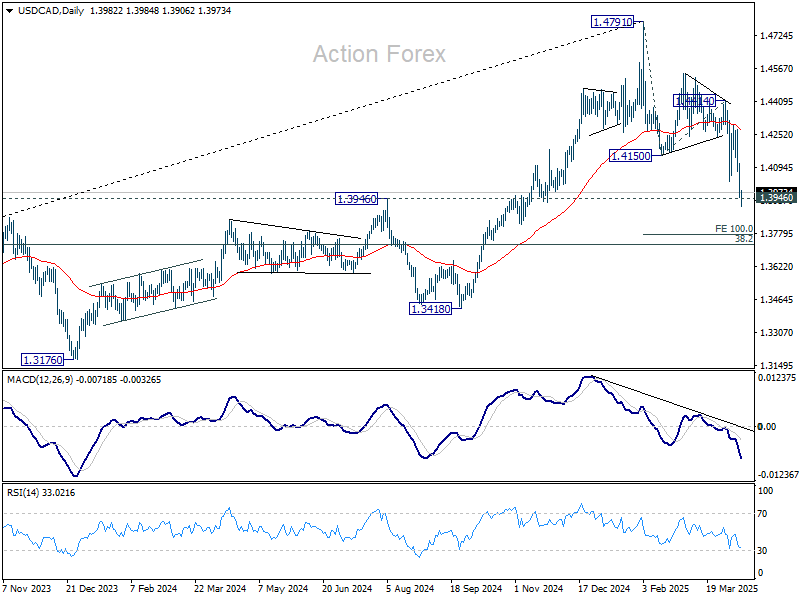

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3920; (P) 1.4015; (R1) 1.4080; More...

USD/CAD's fall from 1.4791 resumed by breaking through 1.4026 and intraday bias is back on the downside. Sustained break of 1.3946 will carry larger bearish implication. Next target is 100% projection of 1.4791 to 1.4150 from 1.4414 at 1.3773. On the upside, break of 1.4150 support turned resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, focus is now on 1.3976 resistance turned support (2022 high), which is close to 55 W EMA (now at 1.4001). Strong rebound from there will retain medium term bullishness. That is, up trend from 1.2005 is still in progress for breaking through 1.4791 at a later stage. However, sustained break there should confirm medium term topping at 1.4791. Deeper correction would be seen to 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727.

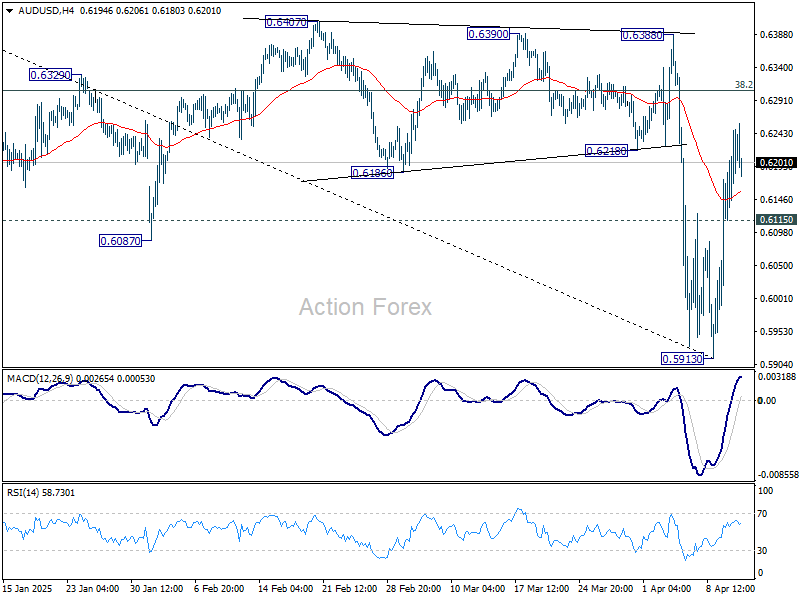

AUD/USD Daily Report

Daily Pivots: (S1) 0.6143; (P) 0.6197; (R1) 0.6277; More...

A short term bottom should be formed at 0.5913 with break of 55 4H EMA (now at 0.6158). Intraday bias is now on the upside for 38.2% retracement of 0.6941 to 0.5913 at 0.6316. Sustained break there will target 61.8% retracement at 0.6548. On the downside, below 0.6115 minor support will turn intraday bias neutral again first.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 0.6388 resistance holds.

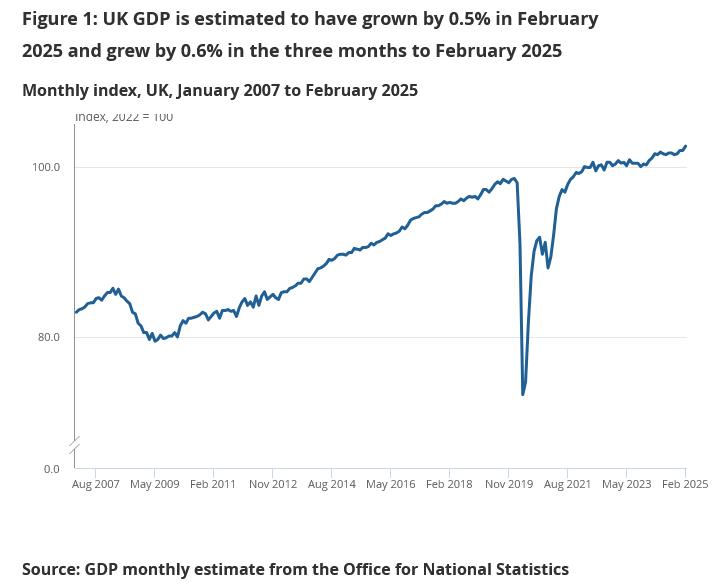

UK GDP rises 0.5% mom in Feb, broad-based growth

The UK economy delivered a strong upside surprise in February, with GDP expanding by 0.5% mom, far exceeding market expectations of just 0.1% mom. All three major sectors contributed to the growth: services rose by 0.3% mom, production surged by 1.5% mom, and construction edged up 0.4% mom.

On a three-month rolling basis, real GDP grew by 0.6% to February 2025 compared to the previous three months, driven largely by a 0.6% rise in services output and a 0.7% gain in production. Construction, however, was flat over the period.

Back to Red

Tariff-pause optimism didn’t last long. Although the European markets followed the US to the upside, mood in the US turned increasingly sour and led to another wave of selloff as the trade war escalated with China. China announced to restrict the US movie imports and the US increased its tariffs on Chinese goods to 145%. The S&P500 gave back 3.50%, the tech-heavy Nasdaq tanked more than 4% as Dow Jones fell 2.5%, shedding more than 1000 points. On the individual level, Disney lost 6%, while the owner of Temu, PDD, lost a similar amount. Gold soared past the $3200 per ounce!

The futures are slightly positive this morning but note that the US selloff accelerated after the European close so there should be a certain catch up today. Broadly the direction remains pretty clear – big jumps are as disquieting as big selloffs; a 3-4% rebound for an index is hardly sustainable when investors remain worried about the trade war uncertainties, the potential impact on the economic growth, on inflation and on jobs.

And this is the message that investors emphasized yesterday. The broadly softer-than-expected US inflation data hardly saw any positive reaction from the markets. The data itself was unusually weak. Both headline and core inflation came in softer than expected on a yearly basis. And on a monthly basis, the headline CPI printed a negative number for the first time since July last year, services excluding housing and energy also fell. The latter would normally boost the dovish Federal Reserve (Fed) expectations and risk appetite. But not this time. The US 2-year yield remains under pressure due to the rising bets that the Fed will soon step in, but the latter doesn’t necessarily bring appetite along. In fact, the tariffs are expected to fuel inflationary pressures and limit the Fed’s action scope. Amazon, for example, warns that US consumers will see the tariffs passed on to them.

Stress in bonds is bad, bad news

The fact that the volatility spreads into the government bond markets is not good news because it hits the pockets of the market that you (as a government) want to keep safe – like the pension funds for example. Therefore, I believe that if Trump backing down won’t calm bond investors’ nerves, the Fed will be the next to step in. This is what the Bank of England (BoE) did this week: they temporarily stopped the sale of long-dated bonds in their QT program to ease the pressure on gilt markets. In the US, we haven’t yet seen an encouraging stabilization across the treasury markets following Trump announcement. The US 10-year yield rebounded back to 4.45%, while the 30-year yield is consolidating below the 5% psychological mark. Investors also flee the US bonds on fear of exploding debt due Trump’s tax cut plans. This week the US Senate passed a budget plan that clarifies parameters on tax cuts and debt ceiling increase. Bloomberg estimates that the changes could allow the US government to deliver $5.3 trillion worth of tax cuts over the next decade and rase the debt ceiling by $5 trillion. Tax cuts are good for corporations and valuations BUT if the yields must rise in return, the positive impact will be thrown under the bus.

Today begins the US earnings season. Big banks will open the dance with their Q1 earnings and projections - amid trade uncertainty and severely deteriorating growth projections - will take the center stage and shape investor sentiment. The forecasts will be revised lower, but how low remains to be seen. TSMC for example reported stronger-than-expected sales in Q1, sales increased by a whooping 42% - the fastest since 2022. Normally, such an update would boost appetite for Nvidia – and it certainly limited losses – but Nvidia closed the session nearly 6% lower as no one knows if Taiwan would avoid import taxes even with TSMC’s pledge to invest up to $165bn in the US. I guess we will see...

US Consumer Sentiment in Focus

In focus today

In the US, the University of Michigan's preliminary consumer sentiment survey for April is set for release. The March edition revealed a significant decline in consumer sentiment, alongside soaring inflation expectations. Markets anticipate the index to decrease further from 57.0 to 55.0.

We will also look out for the release of March PPI data, which could reveal some insights into how the preparation for tariffs has impacted producer costs.

In the euro area, ECB's Lagarde is scheduled to speak at the Eurogroup meeting in Warsaw. As the ECB is now in its silent period, we will not get any policy signals.

In Sweden, the final Swedish inflation data for March will be released this morning at 8.00 CET. The flash estimates undershot both our own and consensus expectations, making today's release important to understand future price developments. Food prices were likely one of the items that came in on the low side compared to forecasts, although they are unlikely to be the only category to do so. We expect the final release to mirror the flash figures, expecting CPI at 0.5% y/y, CPIF at 2.3% y/y and core inflation (CPIF excluding energy) at 3.0% y/y.

Economic and market news

What happened overnight

Overnight, markets adopted a risk-off stance despite yesterday's positive consumer price data. The dollar's sharp decline pushed the EUR/USD above the 1.13 mark this morning, while gold prices surged to a record-high, breaching the USD 3200 per troy ounce. Additionally, the sell-off in US Treasuries intensified, driving the 10-year yield climbing to around 4.45.

What happened yesterday

In the global trade war, the EU announced a pause of retaliatory tariffs to facilitate negotiations, though Commission President von der Leyen cautioned that the tariffs could be reinstated if negotiations are unsatisfactory. Additionally, President Trump escalated the ongoing trade war by raising tariffs on Chinese imports to 125%, now making the effective tariff rate 145%.

In the US, yesterday's key event was the March CPI release, which alongside core CPI surprised to the downside at -0.1% m/m (cons: 0.1%) and 0.1% m/m (cons: 0.3%). Energy prices contributed negatively to the headline figure, while food inflation accelerated. On the core front, goods prices declined from the previous month, and core services inflation also slowed considerably, potentially indicating weakening pricing power among firms. This pre-Liberation Day data warrant cautious interpretation, yet it indicates that broader inflation pressures were relatively subdued ahead of tariffs announcements. The market reaction remained modest. For more insights, see Global Inflation Watch - Disinflation continued ahead of Trump's tariff salvo, 10 April.

In Norway, the eagerly awaited March inflation figures were released, following February's topside surprise, which led Norges Bank to maintain its March policy stance. The figures revealed an annual core inflation rate of 3.4% (prior 3.43%), consistent with both consensus and Norges Bank. Headline inflation registered at 2.6% y/y, slightly below Norges Bank's estimate of 2.7%. However, the core measure remains the most important for policy setting. The details revealed less pronounced increases in air fares and restaurant prices compared to last year, while food prices continued to rise. Consequently, services ex. rent decreased from 3.8 % to 3.5 % whereas domestic goods increased from 7.0% to 7.6% y/y.

In Sweden, February GDP, production and consumption indicators came in as a mixed bag. GDP and production declined -1.5% m/m (prior: -0.5%) and -0.2 % m/m (prior: -0.8 %), respectively whereas consumption increased 1.1% m/m (prior: -0.7%). The data appears somewhat inconsistent, given that consumption carries a significant weight in GDP calculation.

In Denmark, March CPI inflation declined sharply to 1.5% from 2.0% (cons:1.7%), particularly driven by electricity prices. Package holidays showed the largest downside surprise with a 16.5% m/m decrease, which is expected to correct. Core price pressures in Denmark remain muted, consistent with an annual inflation rate of less than 2%.

Equities: Equities retreated on Thursday. However, equities are simply the derivative of what is happening in the FX- and bonds market right now. On top of the financial stress building, the FX swings mean uncharted history for local export companies, trying to defend margins in the US when demand is dropping and FX is making products appear more expensive, on top of tariffs... However, this is not yet visible in European markets where futures are holding up well this morning. US markets sold off yesterday though, with MAG 7 companies leading declines. This was a broad selloff, with 429 of the 500 S&P companies retreating. However, with the rally in the prior session, US equities are still outperforming European ones even on a sector-for-sector basis since April 2nd. Hence, one should probably see the retreat in US markets as reversion to global markets. It should be noted that it was not risk-off everywhere, retail investors were more buoyant sending bitcoin 4% higher but they are typically a lagging and not a leading indicator.

FI&FX: US equities had a rough session throughout Thursday's session, dropping between 3.5-4.5% throughout the session, while European equities caught up with the global rebound on Wednesday evening following the 90-day tariff pause announcement. EUR/USD has continued moving higher since yesterday, and the cross is trading very close to 1.135 this morning. Havens such as CHF, JPY and gold have been bid since the sentiment turned sour again, while both SEK and NOK have fully reversed the strengthening against EUR seen on Wednesday. Long-end US Treasury yields have risen yesterday with the 10Y tenor almost 25bp higher at 4.45%, while the 2Y point is down 10bp following the soft CPI figures. Brent is trading at USD63.1/bbl. this morning, and the NIKKEI 225 index has shed almost 4% since yesterday.

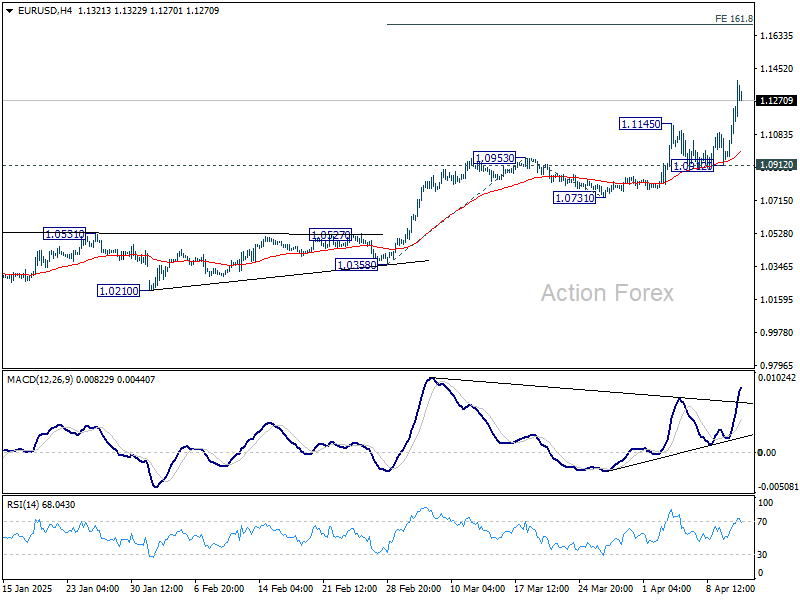

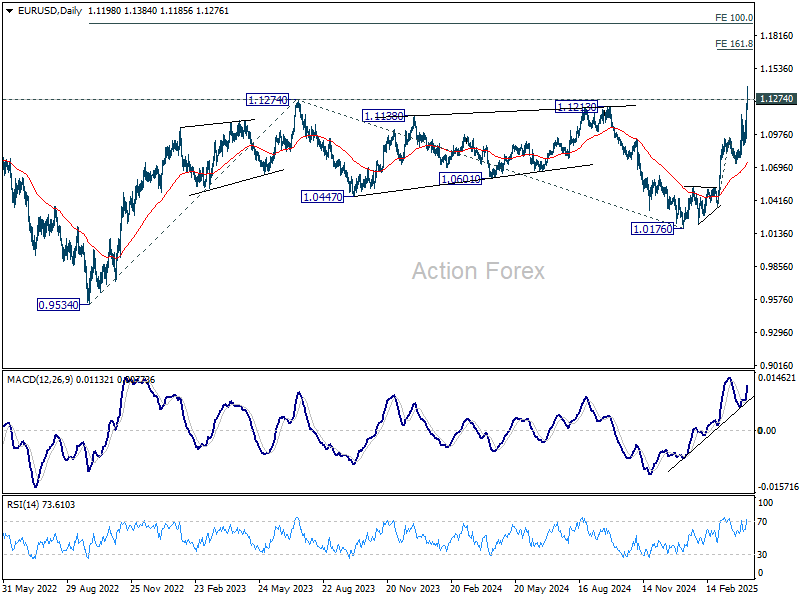

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1016; (P) 1.1129; (R1) 1.1315; More...

Intraday bias in EUR/USD Is back on the upside with break of 1.1145. Also, the break of 1.1274 indicates large up trend resumption. Further rise should be seen to 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694. For now, near term outlook will remain bullish case long as 1.0912 support holds, in case of retreat.

In the bigger picture, break of 1.1274 (2024 high) indicates resumption of whole up trend from 0.9534 (2022 low). Next target is 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through the multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 55 D EMA (now at 1.0745) holds.

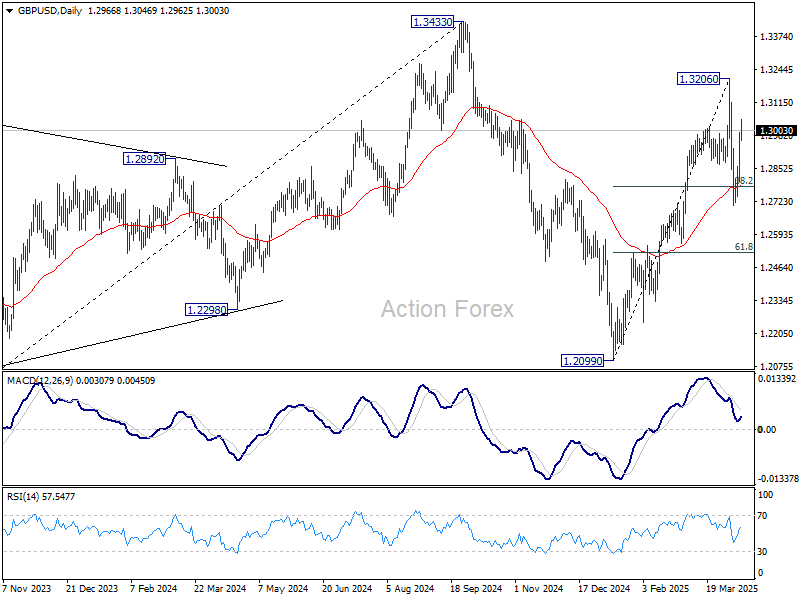

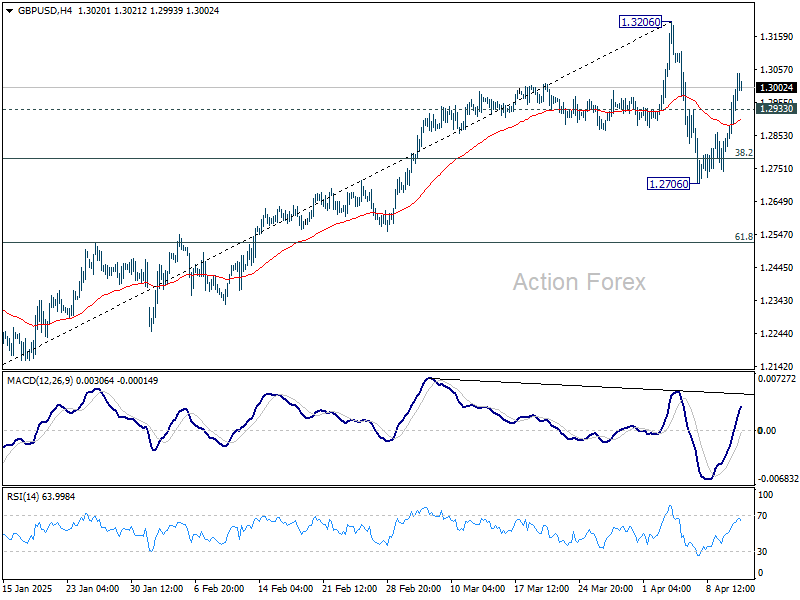

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2841; (P) 1.2918; (R1) 1.3049; More...

Intraday bias in GBP/USD is back on the upside with firm break of 1.2933 minor resistance. Retest of 1.3206 should be seen first. Break there will resume the rally from 1.2099 towards 1.3433 high. For now, near term outlook will stay bullish as long as 1.2706 support holds, in case of another dip.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.