Sample Category Title

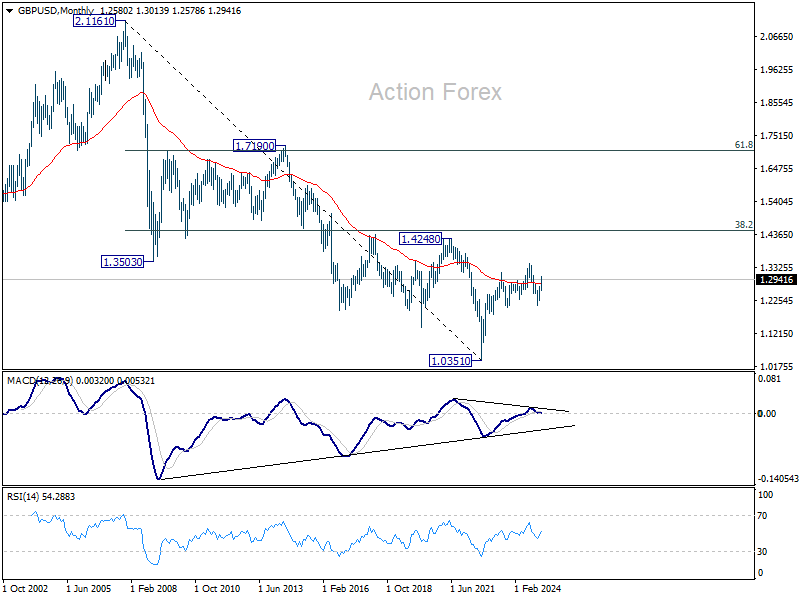

GBP/USD Weekly Outlook

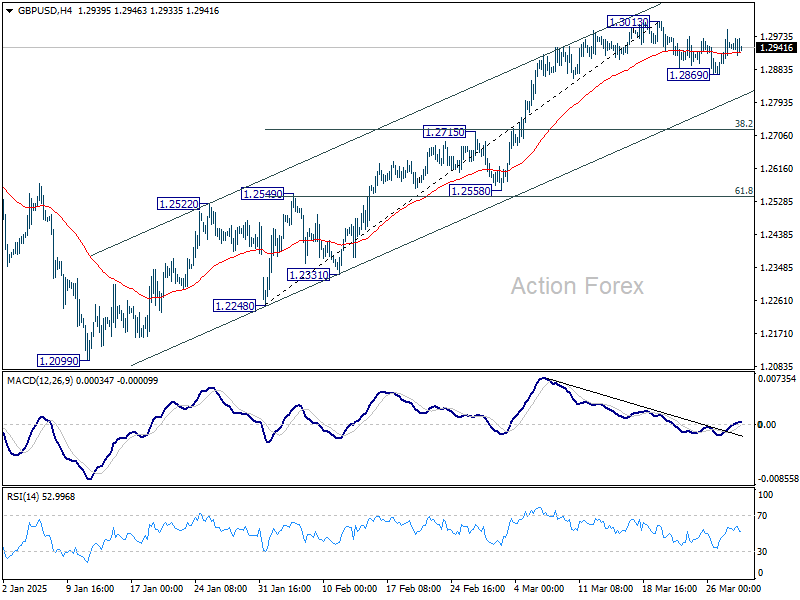

GBP/USD stayed in consolidation below 1.3013 last week. Initial bias stays neutral this week first. On the downside, below 1.2869 will bring deeper correction. But downside should be contained above 38.2% retracement of 1.2248 to 1.3013 at 1.2721. On the upside, break of 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

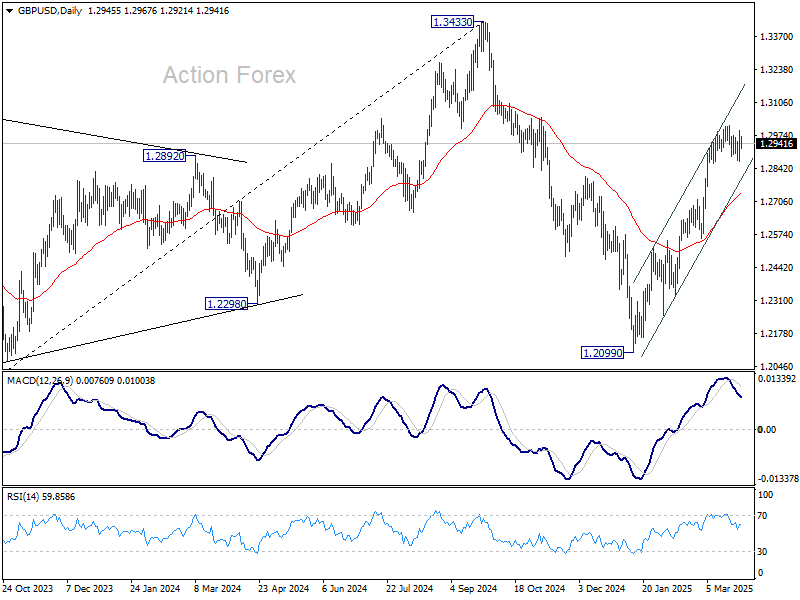

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance (2021 high). This will now remain the favored case as long as 1.2099 support holds.

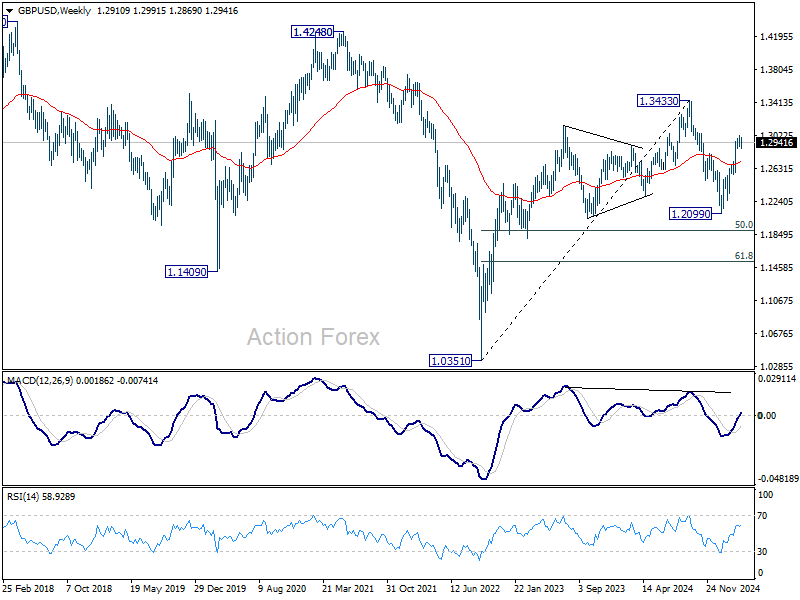

In the long term picture, price actions from 1.0351 (2022 low) are seen as a corrective pattern to the long term down trend from 2.1161 (2007 high) only. Outlook will be neutral at best as long as 1.4248 structural resistance holds, even in case of strong rebound.

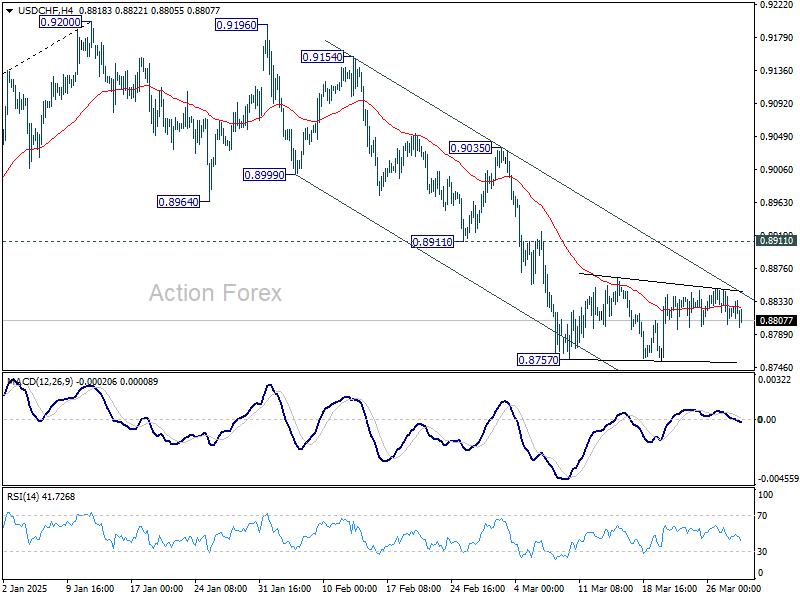

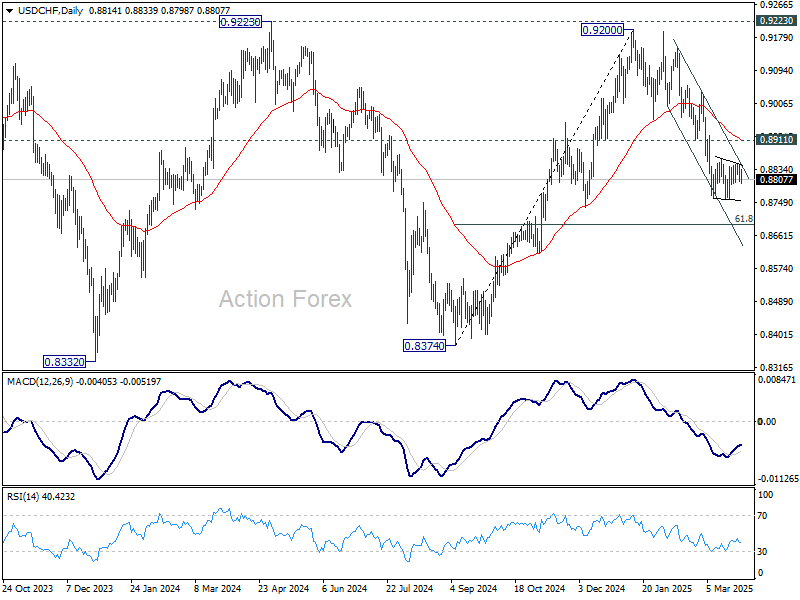

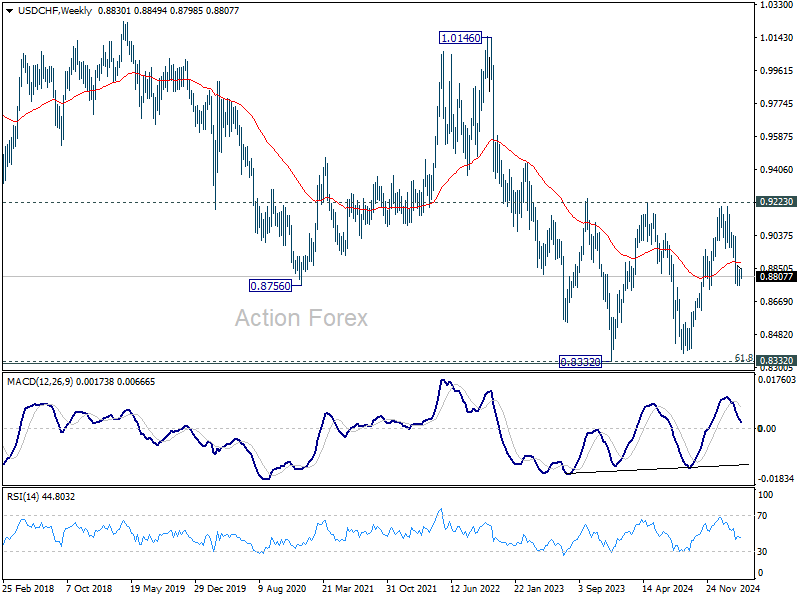

USD/CHF Weekly Outlook

USD/CHF stayed in consolidation above 0.8757 last week and outlook remains unchanged. Initial bias stays neutral this week and more consolidations could be seen. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). Fall from 1.0342 (2016 high) is seen as the second leg. Sustained break of 55 M EMA (now at 0.9115) will indicate that the third leg has already started. However, rejection by 55 M EMA again, followed by break of 61.8% retracement of 0.7065 to 1.0342 at 0.8317, will pave the way back to 0.7065.

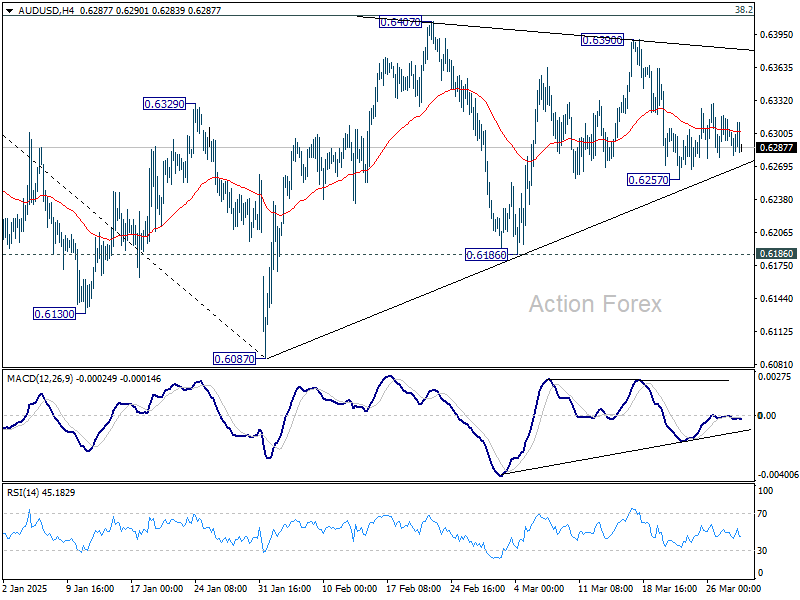

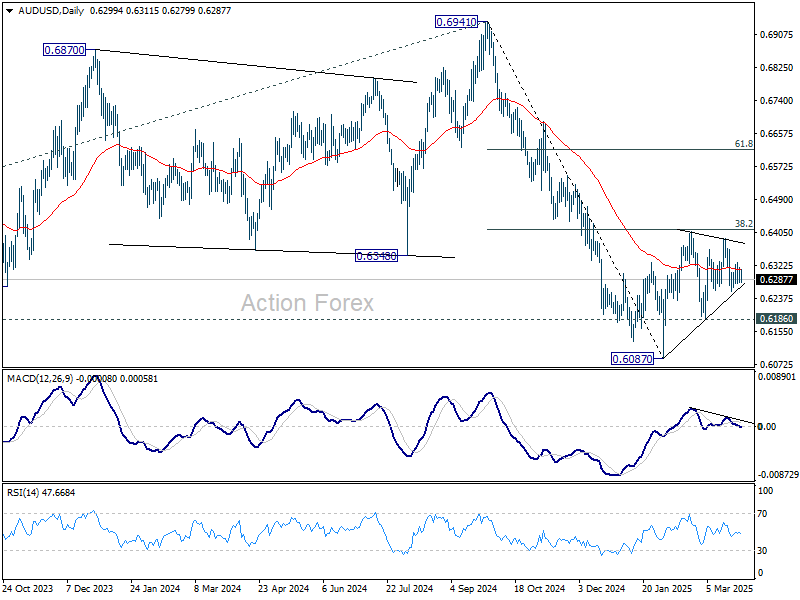

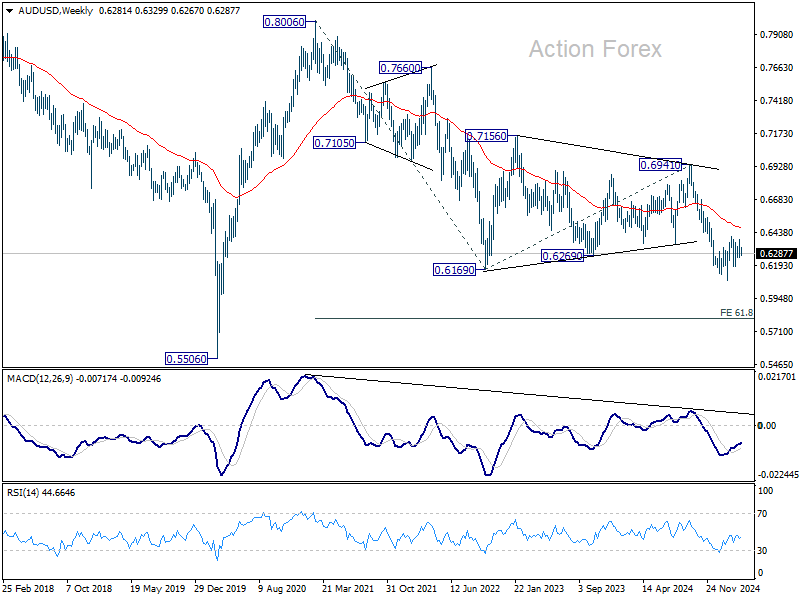

AUD/USD Weekly Report

Range trading continued in AUD/USD last week. Initial bias stays neutral this week first. On the downside, below 0.6257 will target 0.6186 support first. Firm break there will indicate that corrective pattern from 0.6087 has completed and larger fall from 0.6941 is ready to resume. For now, outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds, in case of recovery.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6474) holds.

In the long term picture, prior rejection by 55 M EMA (now at 0.6801) is taken as a bearish signal. But for now, fall from 0.8006 is still seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal. However, this view is subject to adjustment if current decline accelerates further.

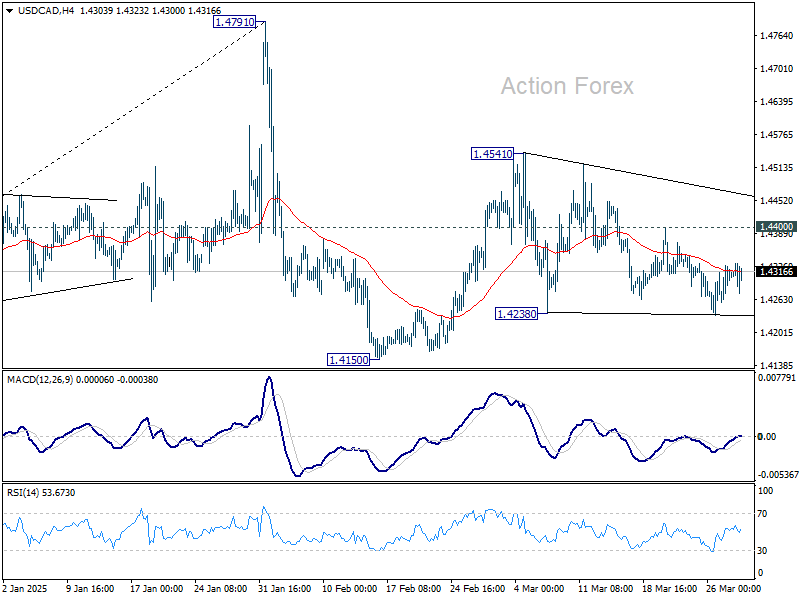

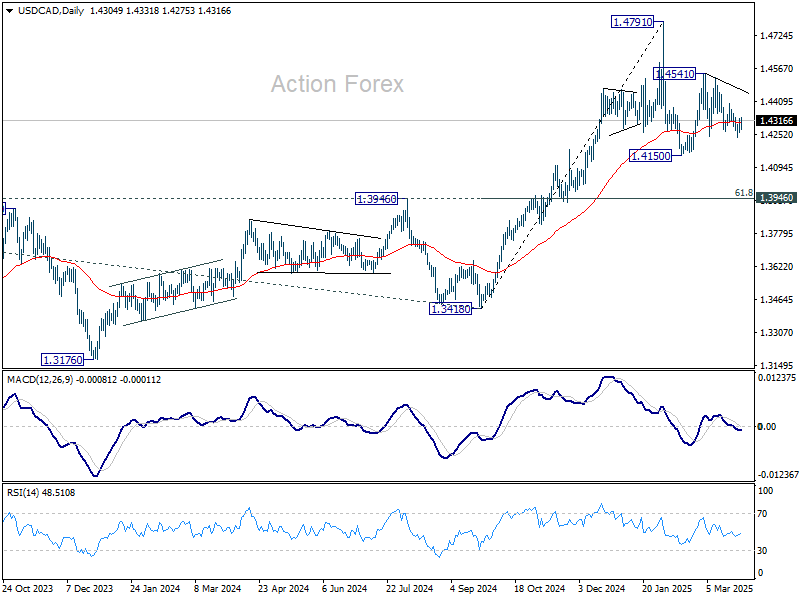

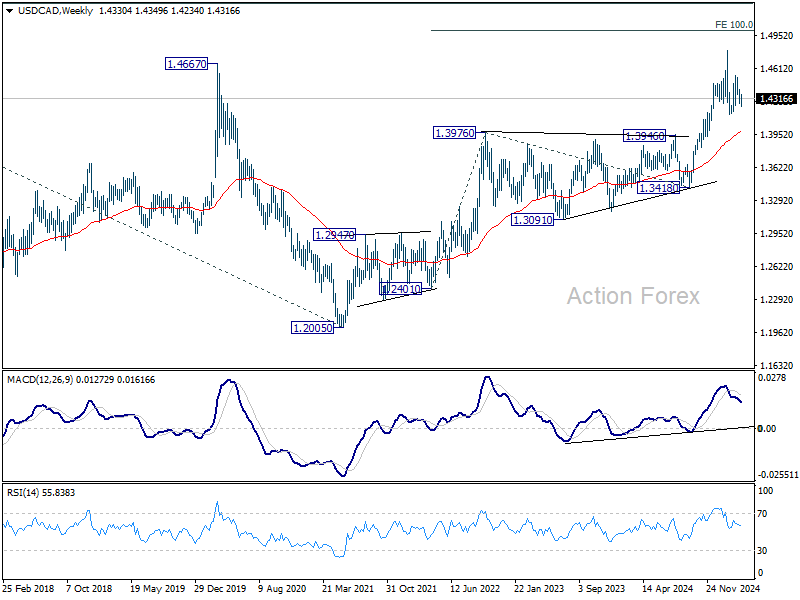

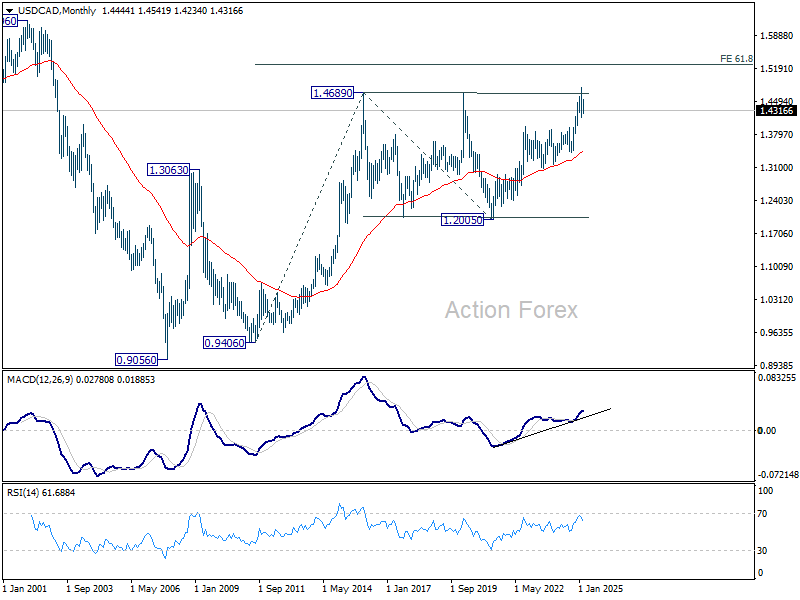

USD/CAD Weekly Outlook

USD/CAD gyrated lower last week but recovered after breaching 1.4238 support very briefly. Initial bias stays neutral this week first. Overall, corrective pattern from 1.4791 is still extending. On the upside, break of 1.4400 will argue that it's still in the second leg, and turn bias to the upside for 1.4541 resistance. On the downside, break of 1.4238 will suggest that the third leg has already started for 1.4150 and below.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

In the longer term picture, up trend from 0.9506 (2007 low) is in progress and possibly resuming. Next target is 61.8% projections of 0.9406 to 1.4689 from 1.2005 at 1.5270. While rejection by 1.4689 will delay the bullish case, further rally will remain in favor as long as 55 M EMA (1.3463) holds.

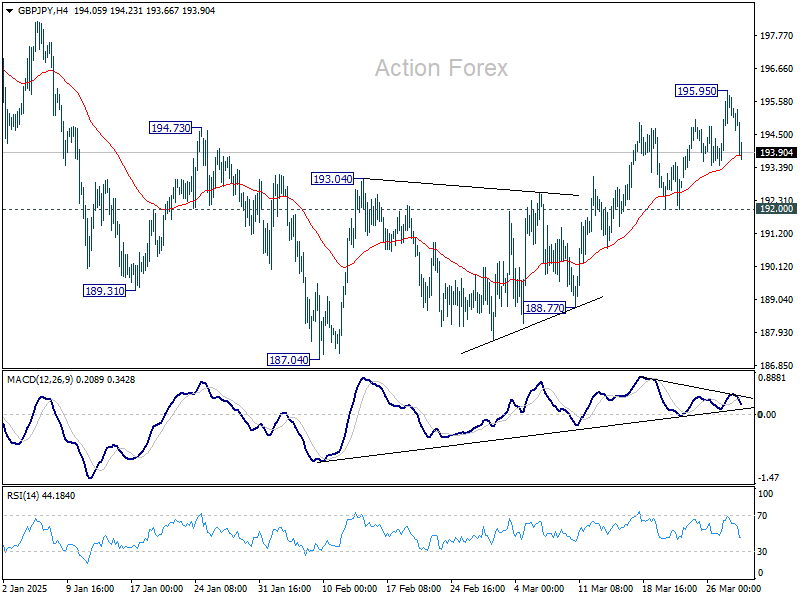

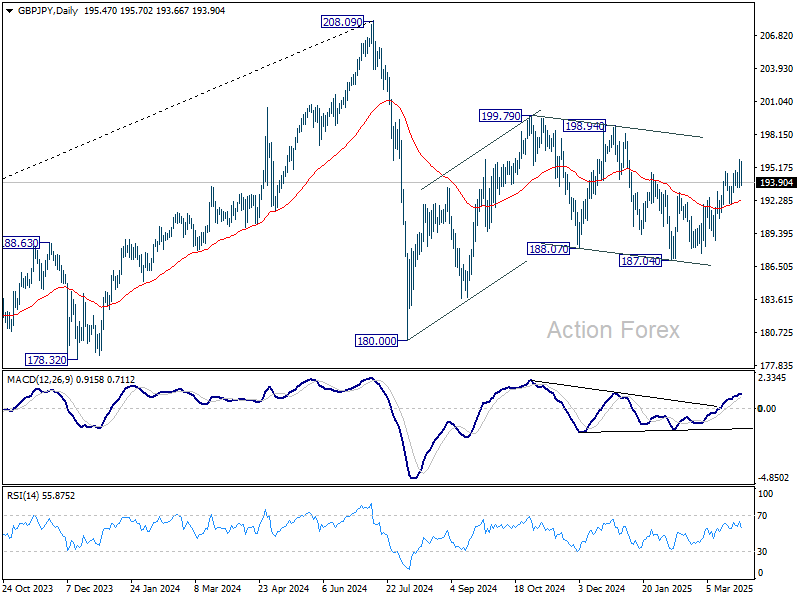

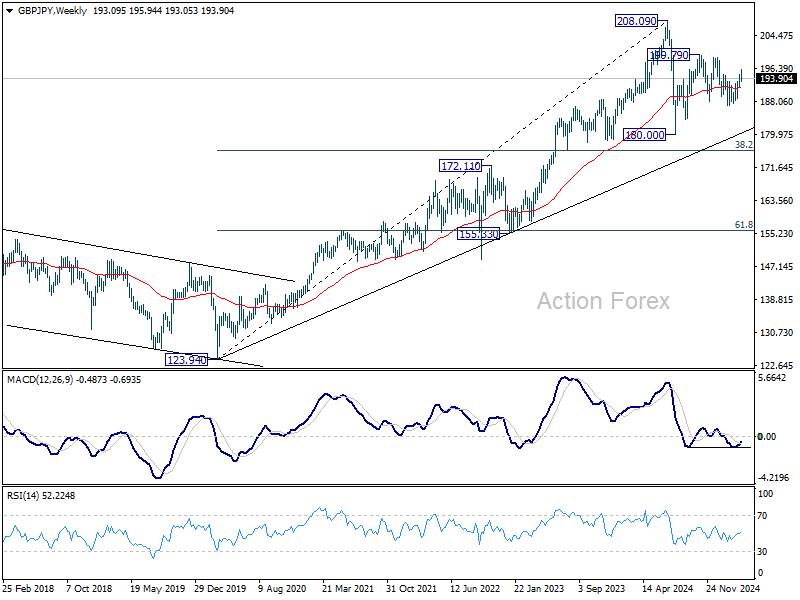

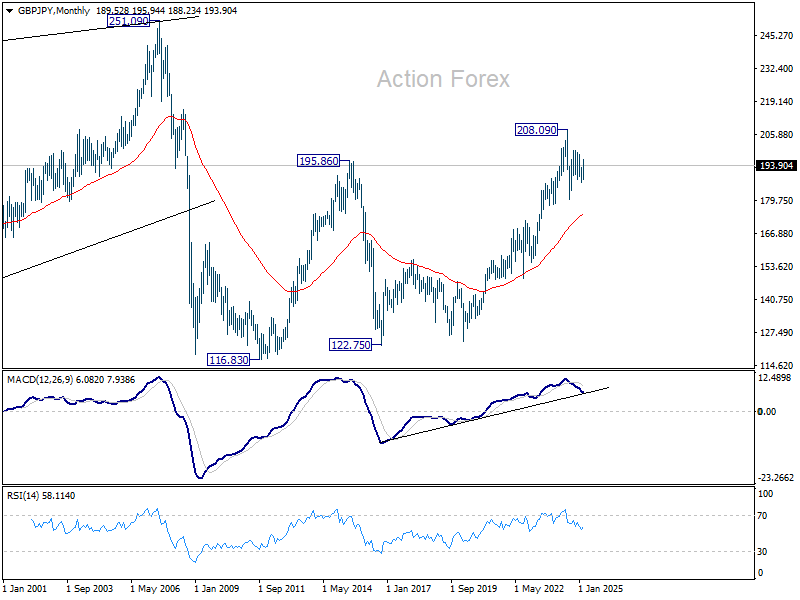

GBP/JPY Weekly Outlook

GBP/JPY's rise from 187.04 resumed last week, but retreated after hitting 195.95. Initial bias is turned neutral this week first. On the upside, break of 195.95 will extend the rally once again, to 198.94 resistance. However, firm break of 192.00 support will turn bias back to the downside for deeper fall. Overall, corrective pattern from 180.00 is still extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 174.68).

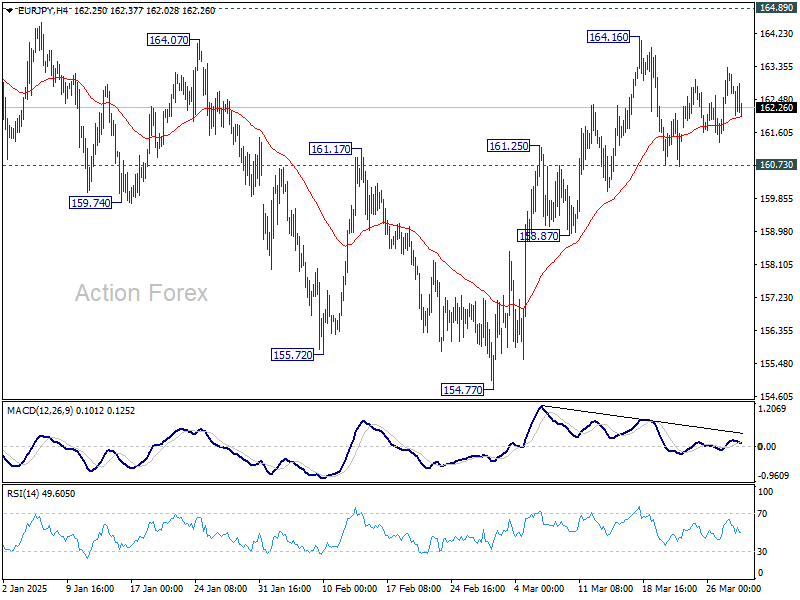

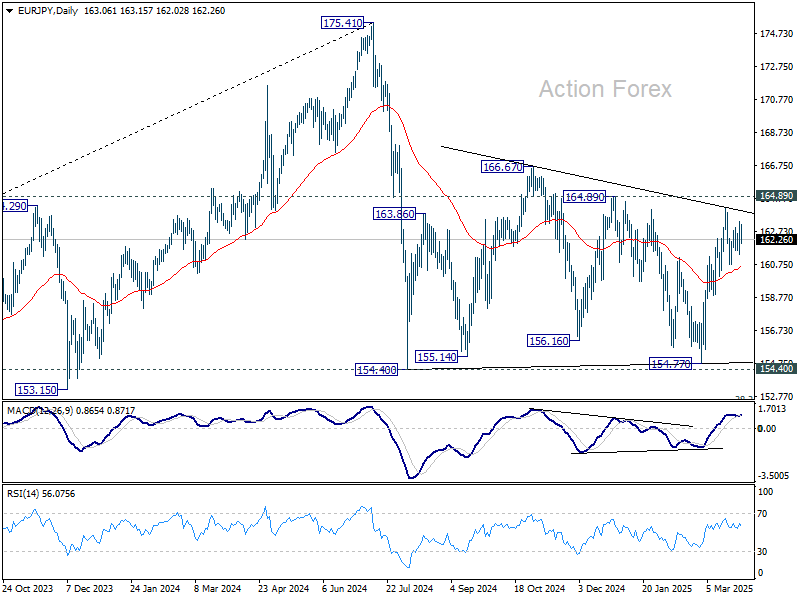

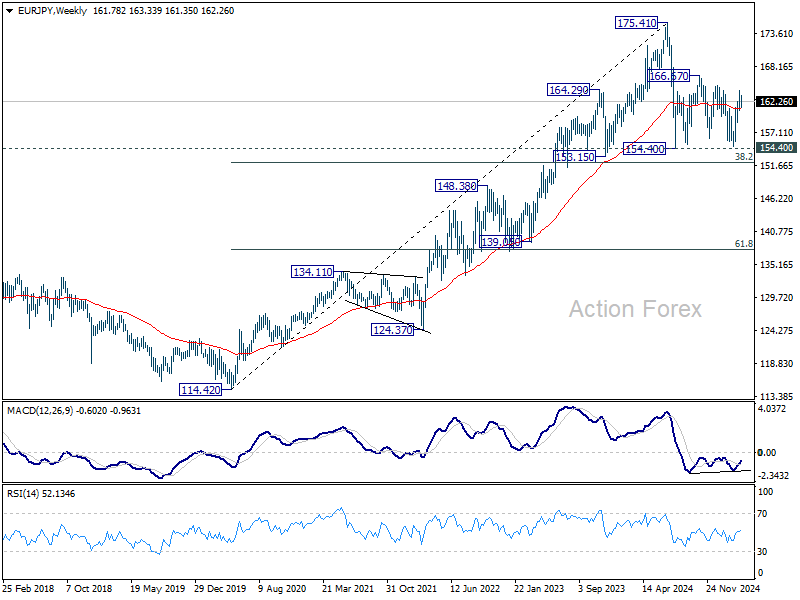

EUR/JPY Weekly Outlook

EUR/JPY stayed in sideway trading below 164.16 last week and outlook is unchanged. Initial bias remains neutral this week first. Further rise is in favor as long as 160.73 support holds. Above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, break of 160.73 will turn bias back to the downside for 158.87 support and below. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 148.94).

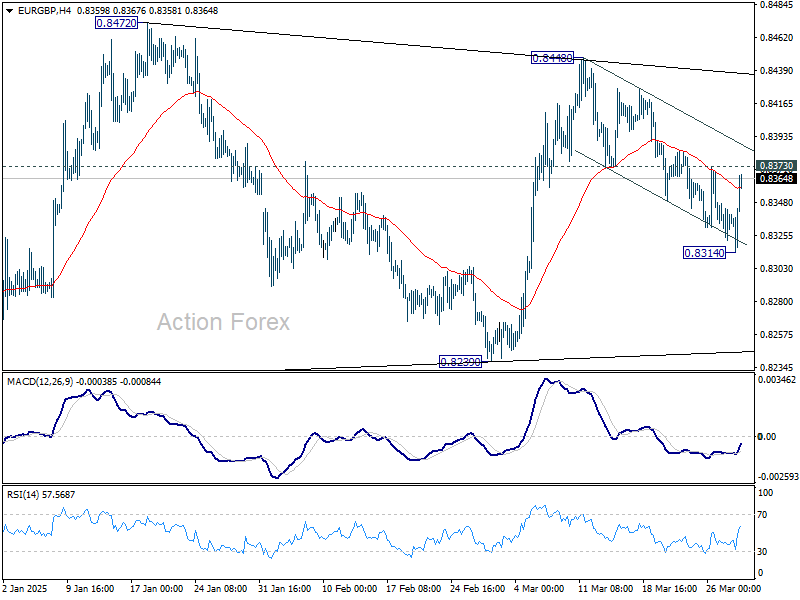

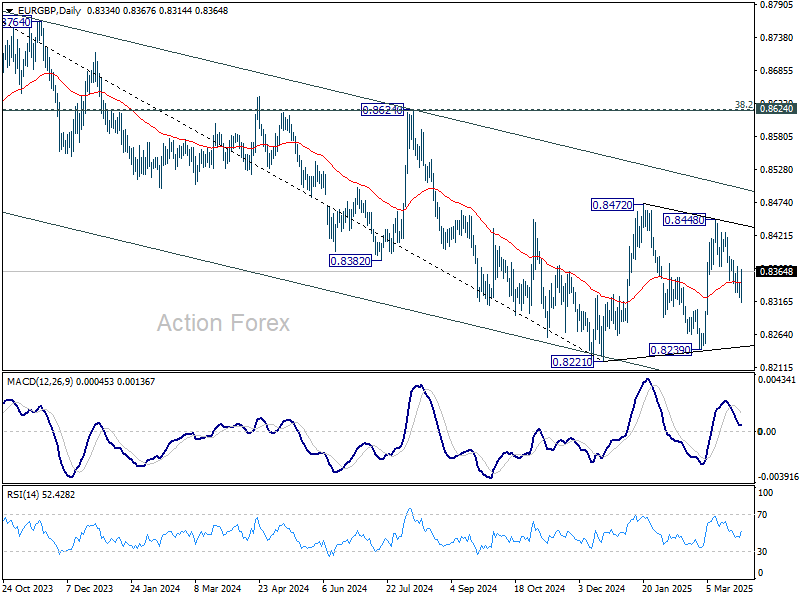

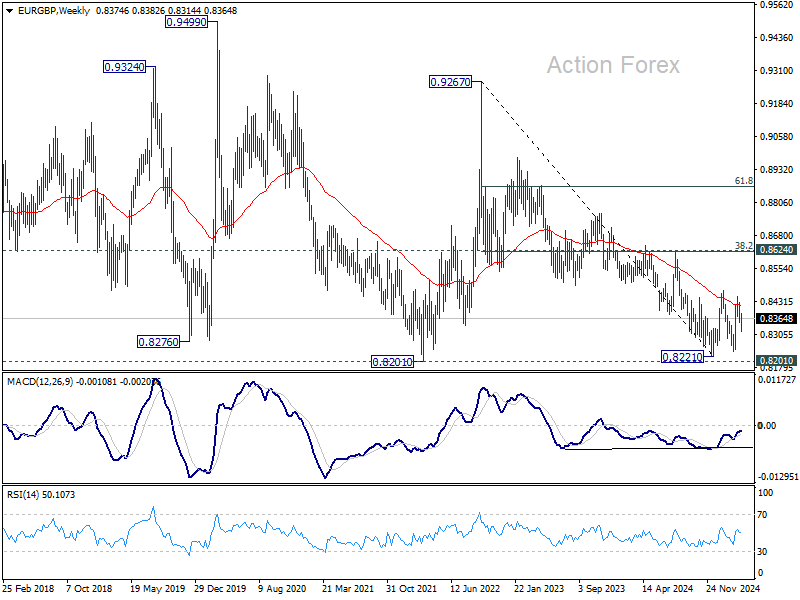

EUR/GBP Weekly Outlook

EUR/GBP gyrated lower last week and broke 55 D EMA (now at 0.8347). But subsequent strong recovery mixed up the near term outlook. Initial bias is turned neutral this week first. On the downside, below 08314 will bring deeper fall back to 0.8239 support. However, firm break of 0.8373 minor resistance will argue that fall from 0.8448 is merely a correction and has completed. Retest of 0.8448 should be seen next.

In the bigger picture, EUR/GBP is still bounded inside medium term falling channel. While rebound from 0.8221 might extend higher, it could still develop into a corrective pattern. Overall outlook will be neutral at best and down trend from 0.9267 (2022 high) could extend, at least until decisive break of channel resistance (now at 0.8495).

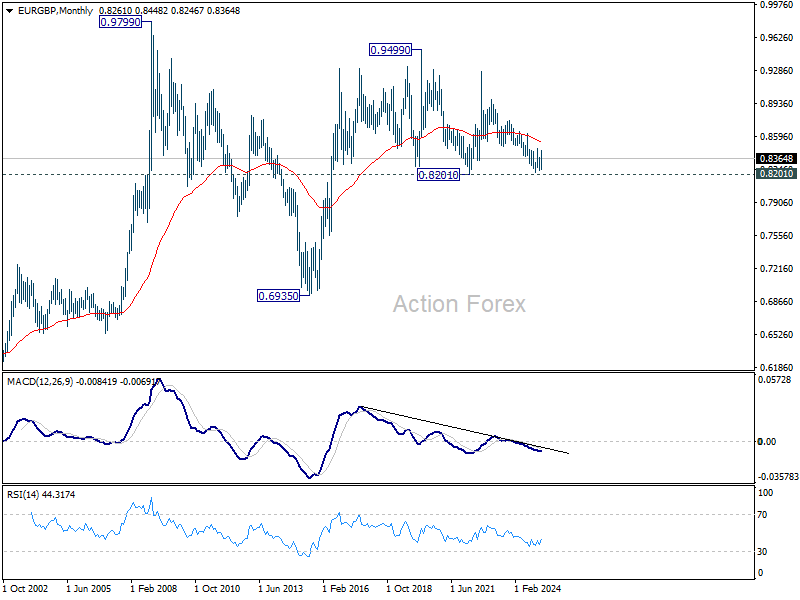

In the long term picture, price action from 0.9499 (2020 high) is seen as part of the long term range pattern from 0.9799 (2008 high). Range trading should continue between 0.8201 and 0.9499, until there is clear signal of imminent breakout.

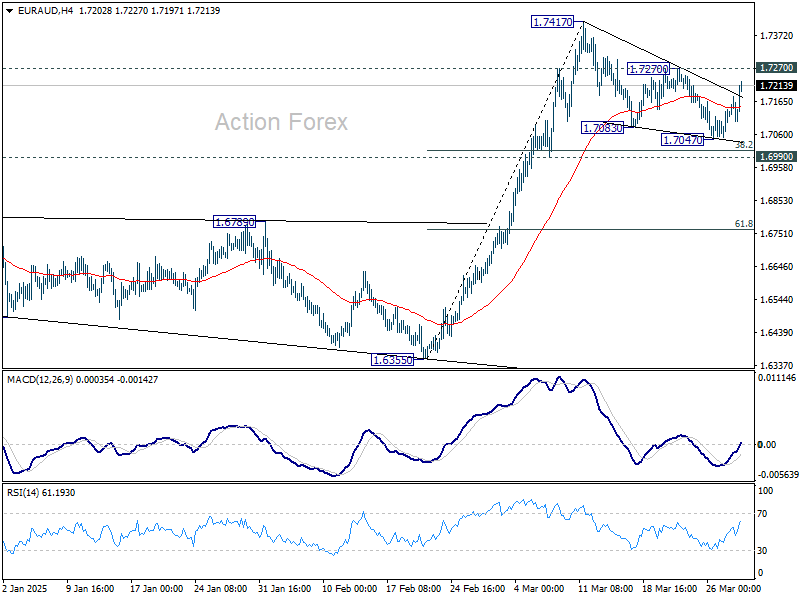

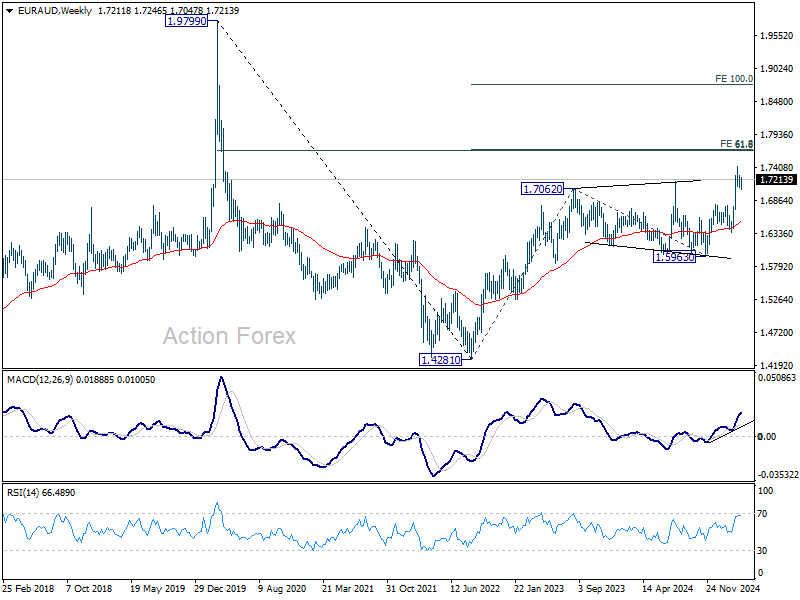

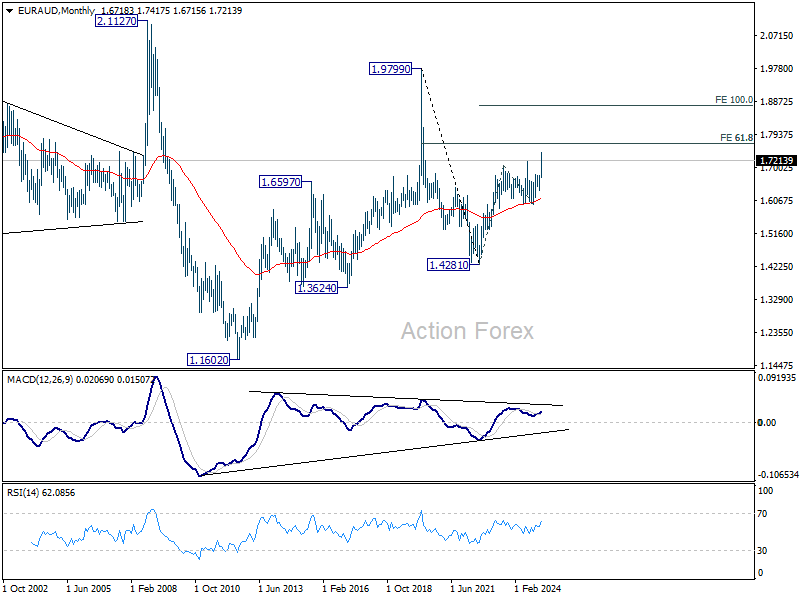

EUR/AUD Weekly Outlook

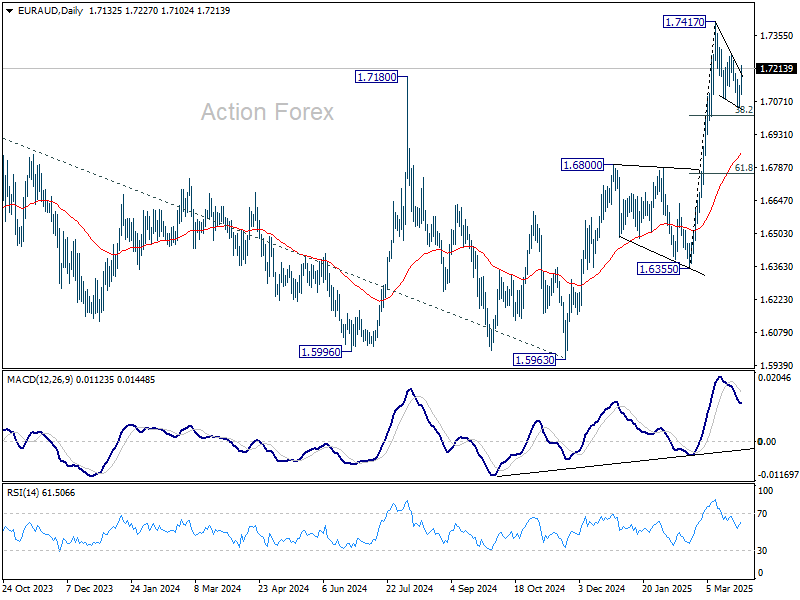

EUR/AUD's correction from 1.7417 extended lower last week but was supported by 1.6900 support as expected so far. Initial bias remains neutral this week and further rise is expected. On the upside, above 1.7270 resistance will argue that the correction has completed, and bring retest of 1.7417. Firm break there will resume larger rise from 1.6335.

In the bigger picture, the breach of 1.7180 key resistance (2024 high) suggests that up trend from 1.4281 (2022 low) is resuming. Sustained trading above 1.7180 will confirm and target 61.8% projection of 1.4281 to 1.7062 from 1.5963 at 1.7682, which is also close to 61.8% retracement of 1.9799 (2020 high) to 1.4281 at 1.7691. For now, this will remain the favored case as long as 1.6800 resistance turned support holds, even in case of deep pullback.

In the longer term picture, rise from 1.4281 is seen as the second leg of the pattern from 1.9799 (2020 high), which is part of the pattern from 2.1127 (2008 high). As long as 55 M EMA (now at 1.6099) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

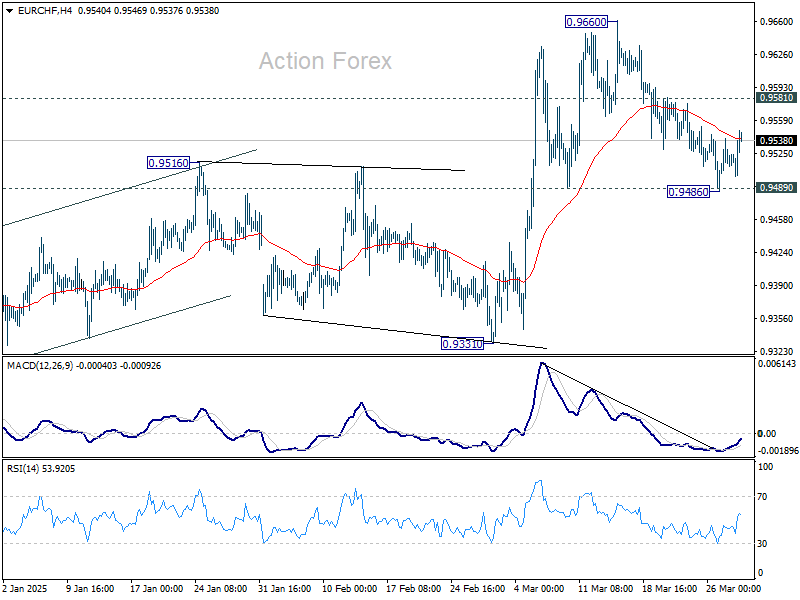

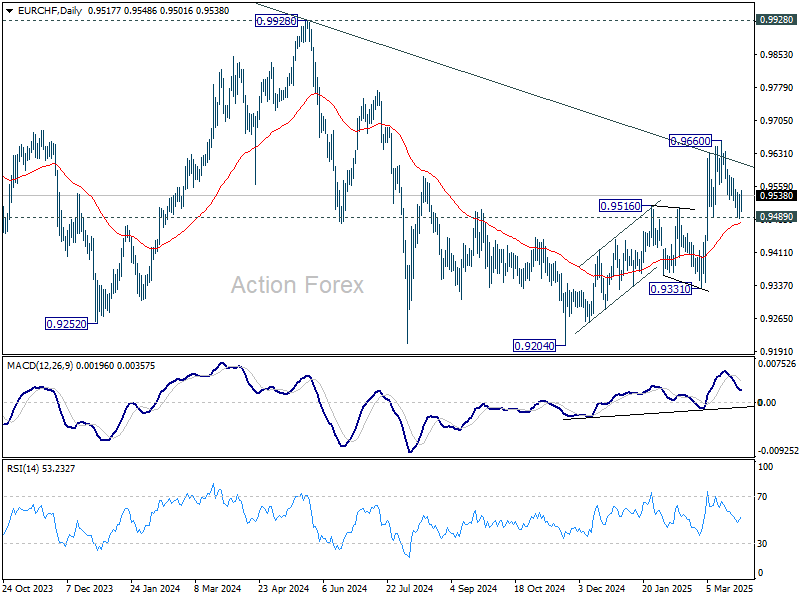

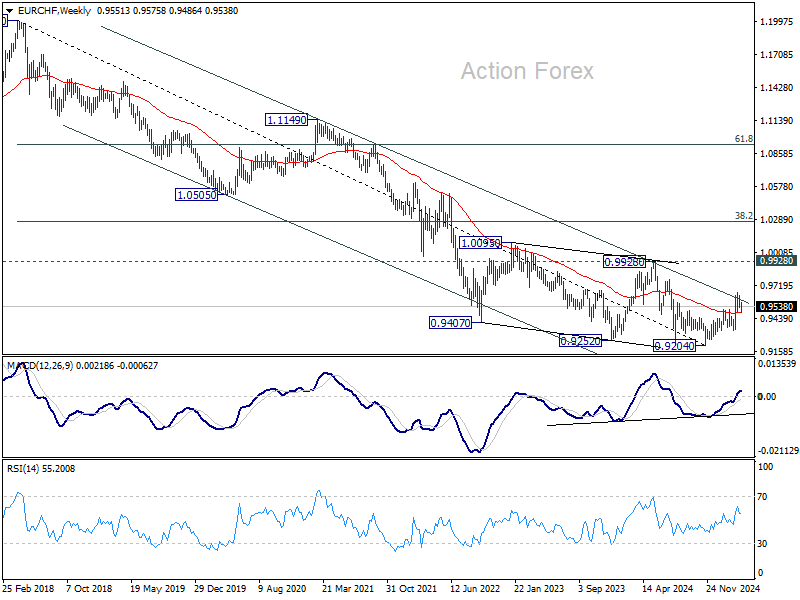

EUR/CHF Weekly Outlook

EUR/CHF gyrated lower as corrective fall from 0.9660 extended, but recovered after drawing support from 0.9489. Initial bias stays neutral first and further rally is expected. On the upside, above 0.9581 minor resistance will indicate that the pullback has completed and bring retest of 0.9660 high. Firm break there will resume whole rise from 0.9204. However, sustained break of 0.9489 will dampen this view, and bring deeper fall back to 0.9331 support next.

In the bigger picture, prior strong break of 55 W EMA (now at 0.9491) is a medium term bullish sign. Sustained break trading above long-term falling channel resistance (at around 0.9610) would suggest that the downtrend from 1.2004 (2018 high) has bottomed at 0.9204. Stronger rally should then be seen to 0.9928 key resistance at least.

In the long term picture, bullish signs are emerging. However, the important hurdle at 0.9928 resistance, which is close to 55 M EMA (now at 0.9960), is needed to be taken out decisively before considering long term trend reversal. Otherwise, outlook is neutral at best.

Markets Rush to Safe Haven as Tariff Clock Ticks Down

While US investors managed to stay relatively composed through most of last week, the calm cracked heading into the weekend. Stocks saw extended selloffs, Treasury yields dropped, and Gold surged to yet another record high — all classic signs of a decisive flight to safety. With risk appetite now clearly under pressure, traders are no longer waiting to see what happens next. They’ve begun positioning defensively ahead of April 2, dubbed “Liberation Day,” when the US is expected to announce sweeping reciprocal tariffs.

That looming event, along with inevitable retaliatory measures from trading partners, has injected a fresh wave of uncertainty into the outlook. Risk-off sentiment is likely to dominate US markets in the near term, at least until the full scale of the tariff fallout becomes clear — including possible re-retaliations.

A big question is whether European markets, which showed notable resilience through March, can continue to defy the global jitters. Stocks in Germany and the UK have largely outperformed US peers, and Euro has led major currencies higher for the month. But the divergence might be tested soon, especially if the trade conflict spills into sectors crucial to the Eurozone's export-heavy economy.

Meanwhile, forex markets have remained relatively stable, with most major pairs stuck inside the prior week's ranges. Kiwi was the lone exception. However, late-week price action across several currency pairs — particularly EUR/USD — suggests that breakouts may be imminent. The common currency is showing signs of bullish potential, with traders watching closely to see whether March strength can evolve into something even more meaningful.

Ultimately, April could be a make-or-break month for the Euro. Either it confirms a genuine bullish turn, reversing the multi-decade downtrend, or it becomes just another short-lived bounce in a longer-term bearish cycle. Otherwise, the March rally risks being remembered as another false dawn in the common currency’s struggle to reverse its long-term decline.

Wall Street Sinks as Markets Front-Run Trump's "Liberation Day" Tariff Blitz

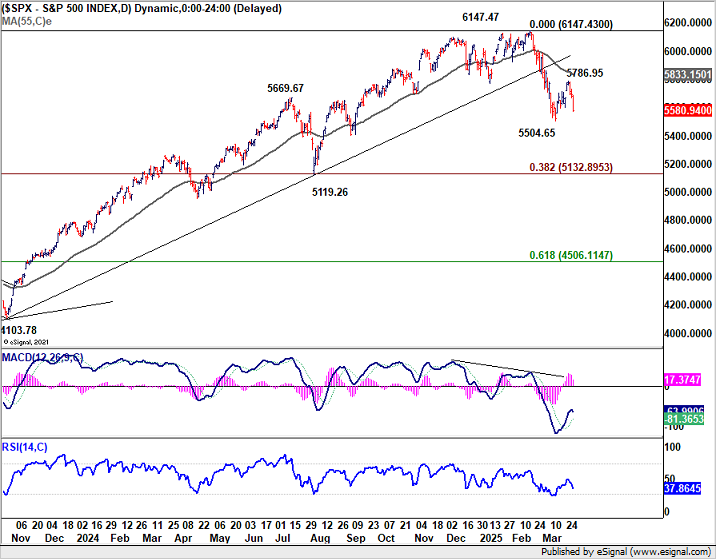

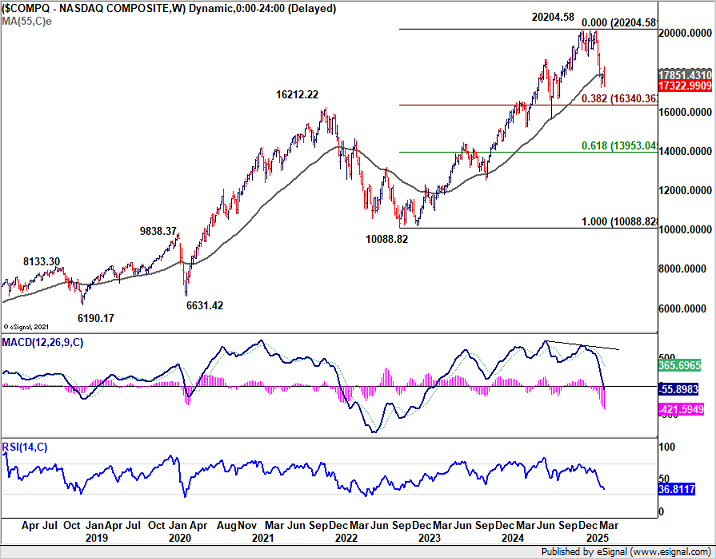

US equities closed out the week with sharp losses, as fears over the looming escalation in trade tensions and persistent inflation sent risk sentiment spiraling. S&P 500 fell -1.53% on the week, while DOW dropped -0.96%. Tech bore the brunt of the selloff, with NASDAQ sliding -2.59%. That puts the NASDAQ on track for a painful monthly decline of over -8%, which would mark its worst monthly performance since December 2022.

The market is being squeezed from two ends. On one side, uncertainty over the scope and scale of US tariffs is weighing on sentiment. On the other, resilient inflation data, especially in core readings, is reinforcing expectations that Fed will keep interest rates higher for longer. Together, these twin pressures are raising fears of a broader slowdown in consumer spending, business investment, and overall economic growth, with the risk of tipping the US into recession.

Trump’s steel and aluminum tariffs have already been in place, but tensions intensified last week as he announced a fresh 25% levy on imported cars and auto parts. That was a mere prelude to what he has dubbed “Liberation Day” on April 2, when the broader reciprocal tariff regime is expected to be unveiled. Stock markets may already be bracing for impact, with traders possibly front-running the announcement, despite the usual quarter-end rebalancing flows.

The broader concern is that even after the April 2 announcement, the tariff saga won’t be over. Canada and the EU are almost certain to respond with retaliations, and China’s stance remains unclear. Others, like the UK and Australia, are expected to hold back. But should retaliation begin to pile up, there is every chance that Trump will double down with even more aggressive measures, setting off a full-blown global trade war.

Still, there is a glimmer of hope. If current market anxiety is more about the "uncertainty" surrounding tariffs rather than the "actual impact" of tariffs themselves, there may be room for a sentiment rebound once the details are made clear — hopefully sometime in Q2.

But that’s a big assumption, and one that relies heavily on the scope, implementation, and global response to the tariffs.

Technically, S&P 500's rebound from 5504.65 should have completed at 5786.95, ahead of falling 55 D EMA (now at 5833.15). Focus for the next few days will be back on 5504.65 support. Firm break there will resume the corrective decline from 6147.47 high to 38.2% retracement of 3491.58 to 6147.43 at 5132.89. Strong support should be seen there to contain downside and bring rebound, at least on first attempt.

Similarly, NASDAQ's corrective recovery from 17238.23 should have completed at 18281.13, ahead of falling 55 D EMA (now at 18608.86). Break of 17238.23 in the next week days will resume the corrective fall from 20204.58 to 38.2% retracement of 10088.82 to 20204.58 at 16340.36. Strong support should be seen there to bring rebound, at least on first attempt. However, firm break there will pave the way to 15708.53 support next.

Yields Tumble on Safe Haven Flows, Dollar Index Relatively Resilient

US 10-year Treasury yields fell sharply on Friday, even as core PCE inflation surprised to the upside. The data highlighted persistent inflationary pressures, with the core PCE accelerating to 2.8% yoy, above expectations and well above Fed’s 2% target. Typically, such data would push yields higher as markets price out rate cuts. However, Friday’s yield decline suggests a different narrative dominated—one of risk aversion.

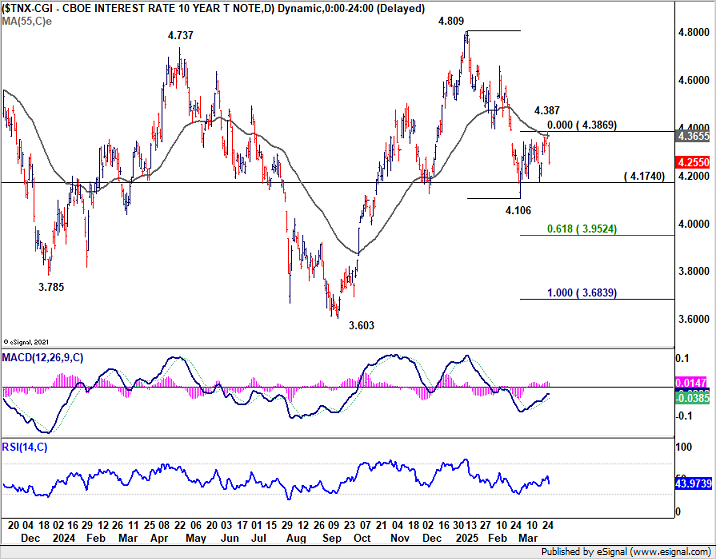

Technically, corrective recovery from 4.106 could have already completed at 4.387 after hitting falling 55 D EMA (now at 4.3650). Break of 4.174 support will argue that the whole decline from 4.809 is ready to resume through 4.106 short term bottom. Next target will then be 61.8% projection of 4.809 to 4.106 from 4.387 at 3.952, which is below 4% psychological level.

More importantly, the next fall will solidify that decline from 4.809 is another leg inside the medium term pattern from 4.997 (2023 high) with risk of extending to 3.603 (2024 low) and below.

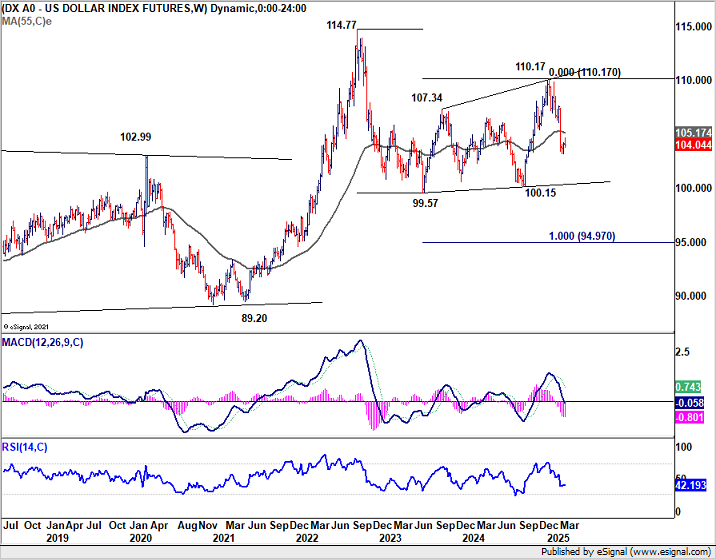

Dollar Index only dipped slightly on Friday and the development argues that corrective recovery from 103.19 might still extend. But even in case of another rise, upside should be limited by 55 D EMA (now at 105.64). Break of 103.19 will resume the fall from 110.17 to 100.15 support next.

Crucially, the next fall will further solidify the case that decline from 110.17 is the third leg of the pattern from 114.77 (2022 high). Break of 100.15 support will pave the way through 99.57 (2023 low) to 100% projection of 114.77 to 99.57 from 110.17 at 94.97.

March Belongs to Europe, But Can Momentum Survive April’s Storm?

Despite rising global trade tensions and the looming threat of reciprocal US tariffs, European currencies and assets have emerged as the standout performers for March. In the equity space, major European indices like Germany’s DAX and the UK’s FTSE have remained relatively insulated from the sharp selloff seen on Wall Street.

Meanwhile, Euro has led the charge in the currency markets, with Sterling and, to a lesser extent, Swiss Franc following closely. The coming weeks will be critical in determining whether this resilience in European markets can be sustained or even turn into renewed momentum.

Technically, with 8474.41 resistance turned support intact, FTSE's price actions from 8908.82 are viewed as a sideway consolidation pattern only. Larger up trend is expected resume through 8908.82 to 100% projection of 7404.08 to 8474.41 from 8002.34 at 9072.67 at a later stage.

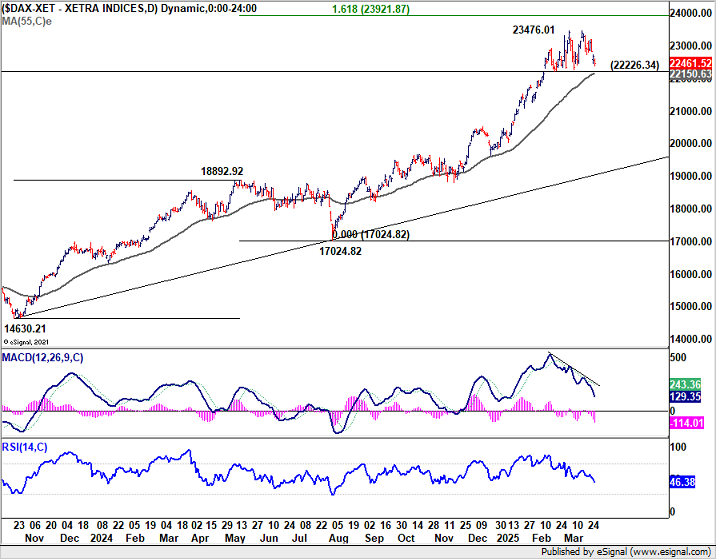

As for the stronger DAX, outlook is staying bullish with 22226.34 support intact, which is close to 55 D EMA (now at 22150.63). Another rise is till expected to 161.8% projection of 14630.21 to 18892.92 from 17024.82 at 23921.87, or even further to 24000 psychological level.

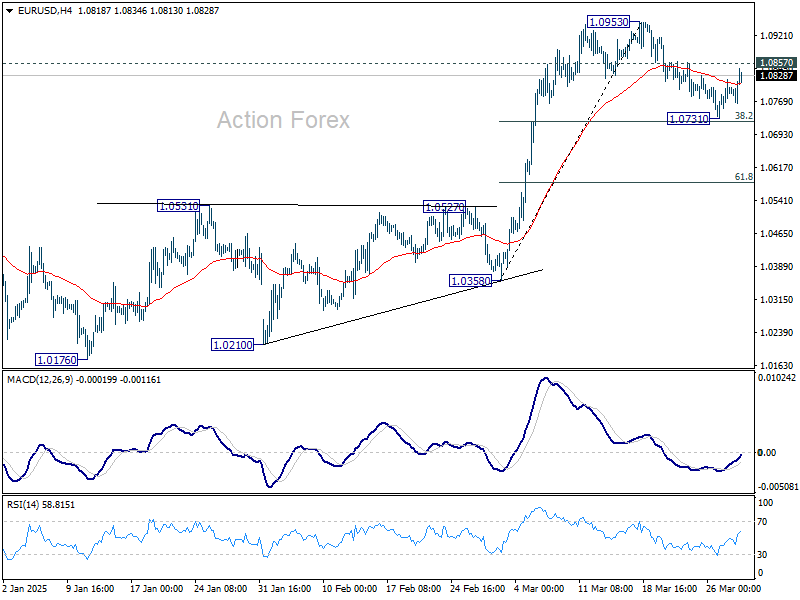

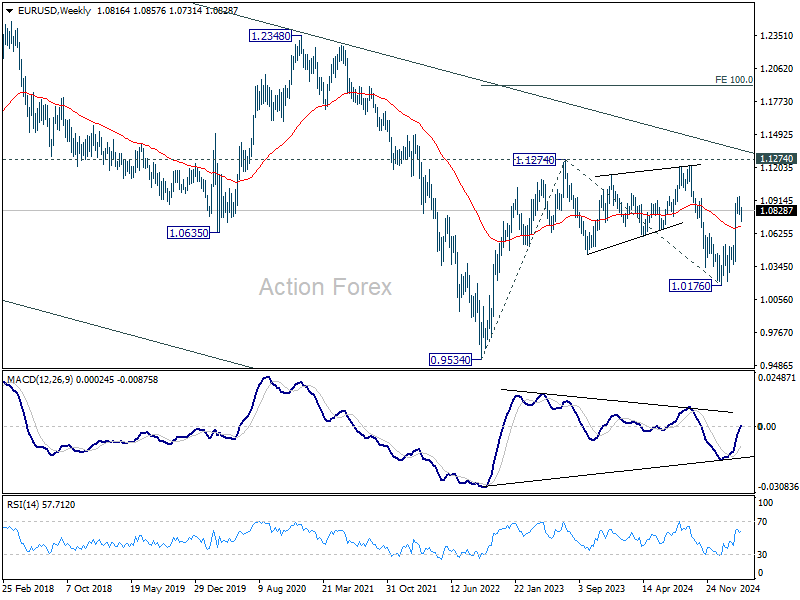

It's also important for EUR/USD. The near term pull back from 1.0953 could have already completed at 1.0731, ahead of 38.2% retracement of 1.0358 to 1.0953 at 1.0726. Break of 1.0857 minor resistance should affirm this bullish case, and push EUR/USD through 1.0953 to resume the whole rally from 1.0176.

More significantly, the next rally would set up EUR/USD for a test on key resistance between 1.1274 (2023 high) and multi-decade falling channel resistance (now at around 1.1380). This resistance zone is crucial to determine whether EUR/USD is reversing the long term down trend.

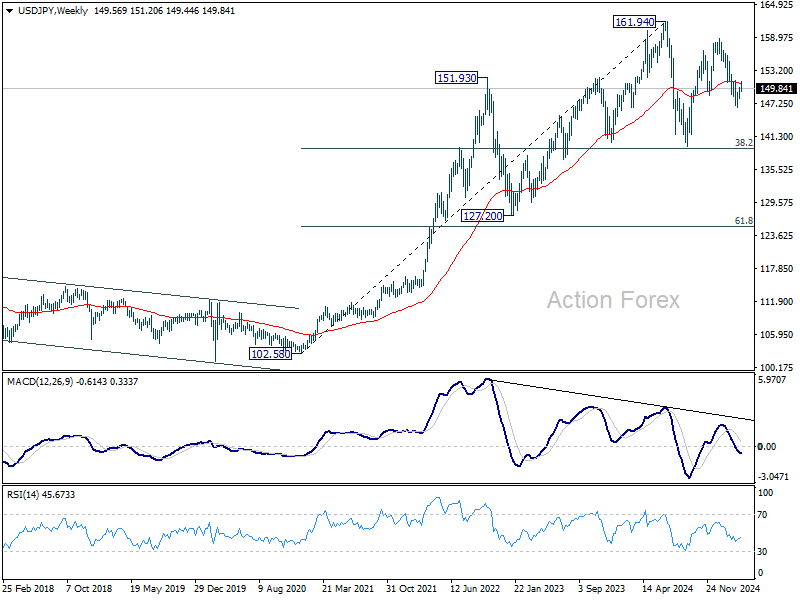

USD/JPY Weekly Outlook

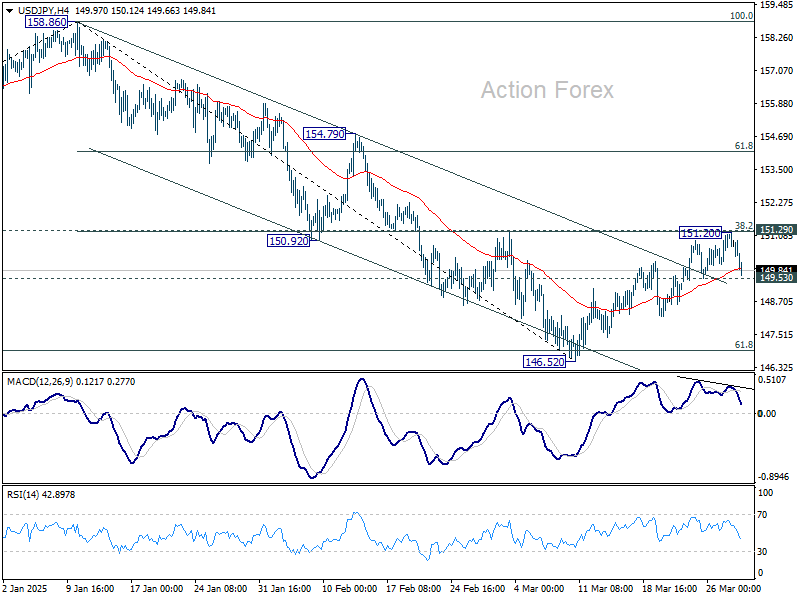

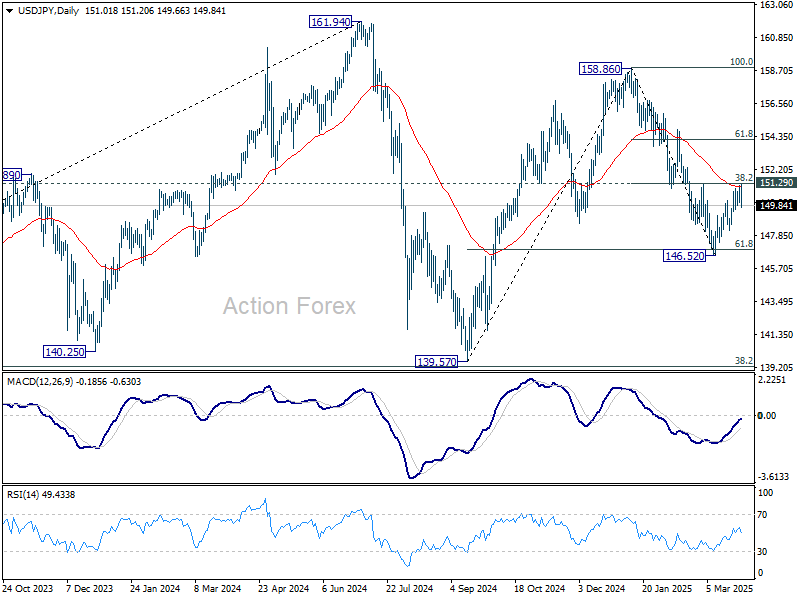

USD/JPY recovered further to 151.20 last week but retreated sharply ahead of 151.29 cluster resistance (38.2% retracement of 158.86 to 146.52 at 151.23). Initial bias remains neutral first and outlook stay bearish. On the downside, below 149.53 minor support will argue that the corrective recovery has completed and bring retest of 146.52 low. Firm break there will resume whole fall from 158.86. However, firm break of 151.23/9 will turn bias back to the upside for 154.79 resistance instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. A medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 136.94).