Sample Category Title

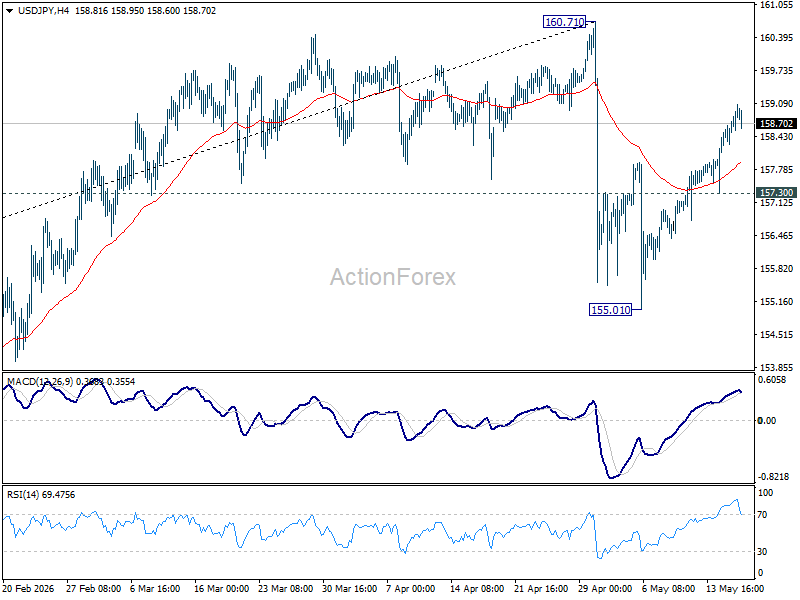

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.35; (P) 158.59; (R1) 158.99; More...

Intraday bias in USD/JPY remains on the upside at this point. Rise from 155.01 should target 160.71 high. But strong resistance is expected from there to start the third leg of the near term corrective pattern. On the downside, break of 157.30 minor support will argue that the third leg could have started, and target 155.01 support instead.

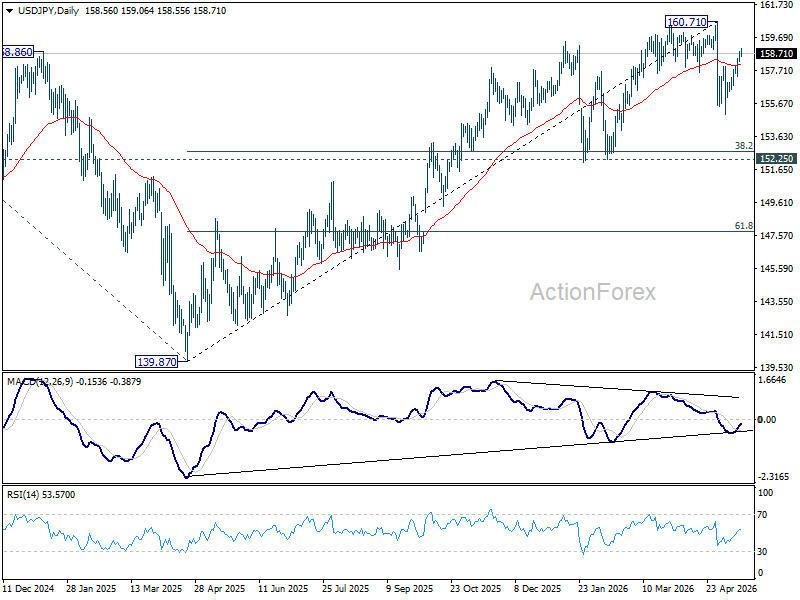

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.36) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

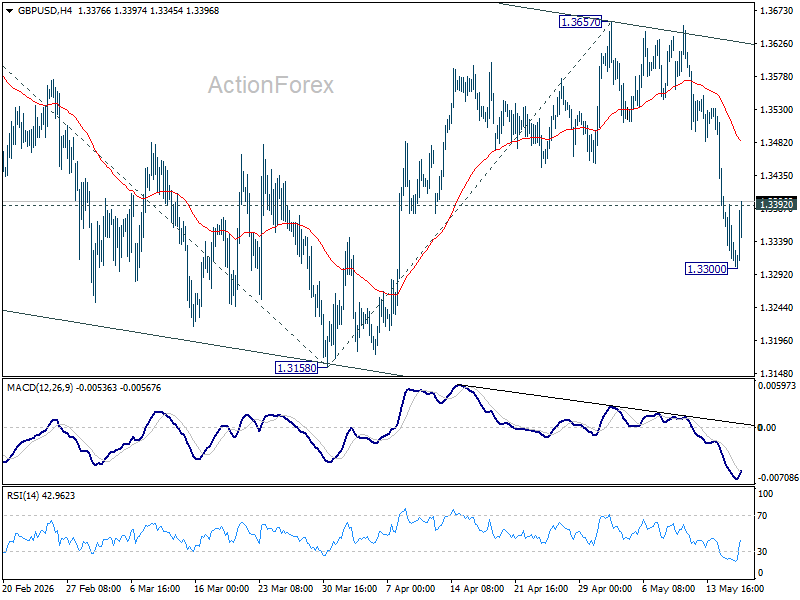

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3347; (R1) 1.3379; More...

Intraday bias in GBP/USD is turned neutral first with current recovery, and some consolidations would be seen above 1.3300 temporary low. Further fall is expected as long as 55 4H EMA (now at 1.3483) holds. Below 1.3300 will target a retest on 1.3158 support first. Decisive break there will target 100% projection of 1.3867 to 1.3158 from 1.3657 at 1.2948. However, sustained break of the EMA will dampen the bearish case and turn bias back to the upside for 1.3657 resistance instead.

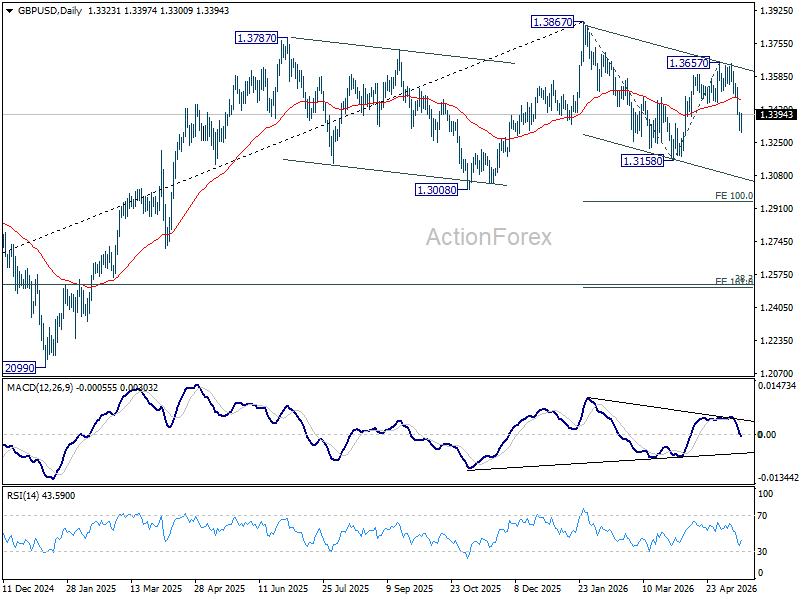

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

Markets Stabilize as Iran Proposal Reaches Washington Ahead of Trump Security Meeting

Markets stopped panicking — for now. After opening the week with a sharp risk-off move driven by surging oil prices and fears of wider Middle East escalation, traders shifted back into wait-and-see mode as the US session approached. Brent crude slipped back below $110, US futures recovered from deeper losses, and broader market sentiment steadied as investors reassessed whether diplomacy might still have one final opening left.

That stabilization was triggered by reports that Pakistan had delivered a revised Iranian proposal to Washington aimed at ending the war in the Middle East. Iranian officials later confirmed that Tehran’s position had indeed been conveyed to the American side through Pakistani mediation. While details remain unclear, the mere existence of a renewed diplomatic channel was enough to cool some of the panic that had swept through energy markets earlier in the day.

But markets are not suddenly optimistic. The mood is closer to conditional calm — a temporary pause because no new escalation has happened yet. Investors broadly understand that time may be running out for negotiations. US President Donald Trump’s Tuesday Situation Room meeting with national security advisers is now looming over global markets as the next major decision point. Reports indicate the White House is explicitly reviewing options for military action against Iran after diplomacy stalled further following the failed Trump-Xi summit last week.

Meanwhile, the oil market itself is becoming increasingly unstable beneath the surface. Reports that Europe could face shortages within weeks are colliding with the approaching end of the seasonal demand lull. As Memorial Day travel demand in the US and holiday consumption in the UK begin lifting fuel demand again, the oil market could enter a “non-linear” phase where physical shortages force buyers to bid aggressively for supply regardless of valuation.

That possibility matters because non-linear commodity moves tend to spread rapidly across the entire macro landscape. Higher oil feeds inflation fears, pushes Treasury yields higher, supports the Dollar, and pressures equities simultaneously. It also explains why traders remain reluctant to fully embrace today’s calmer tone even as Brent retreated from its highs.

In FX markets, Yen led losses as immediate panic hedging faded, while Sterling outperformed alongside Kiwi and Aussie as broader sentiment stabilized modestly. Dollar and Loonie also weakened slightly as oil pulled back from peak levels. Euro and Swiss Franc traded more defensively in the middles.

In Europe, at the time of writing, FTSE is up 0.45%. DAX is up 0.86%. CAC is down -0.32%. UK 10-year yield is down -0.06 at 5.122. Germany 10-year yield is down -0.013 at 3.157. Earlier in Asia, Nikkei fell -0.97%. Hong Kong HSI fell -1.11%. China Shanghai SSE fell -0.09%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield rose 0.041 to 2.746.

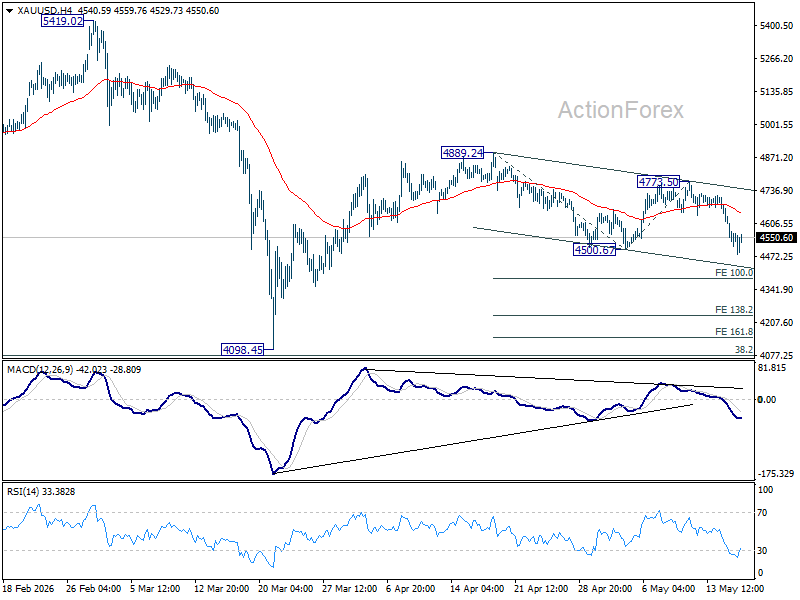

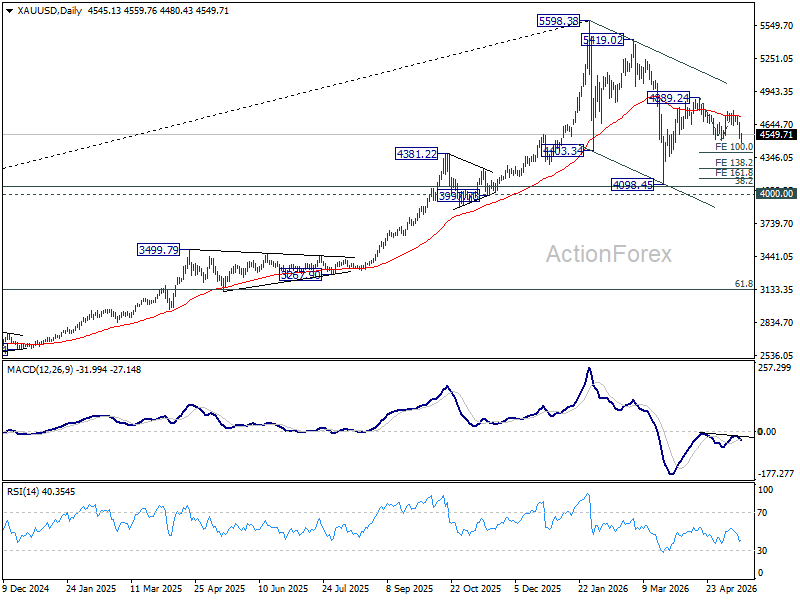

Gold Slips Below 4500, May Stabilize Near 4200 Unless Brent and Treasury Yields Break Crisis Levels

The latest drop in Gold below 4500 is being driven less by fading safe-haven demand and more by rising oil prices, Treasury yields, and “higher for longer” interest rate fears. The next key test sits near 4200. Read More.

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 as failed diplomacy, military escalation, and the UAE infrastructure strike pushed the US-Iran conflict into a dangerous new phase. Read More.

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, with PSI rising from 46.2 to 48.9 and new orders returning to expansion territory. However, businesses continued to warn about rising fuel costs and shipping disruption linked to conflict in the Strait of Hormuz, while smaller firms remained under significant pressure. Read More.

China April Data Misses Across the Board as Domestic Demand Weakens Sharply

China’s April data deteriorated sharply, with retail sales nearly stalling at 0.2% yoy, industrial production slowing, and fixed asset investment unexpectedly turning negative. The weak figures reinforced concerns that rising geopolitical tensions and higher energy costs are weighing heavily on domestic demand. Read More.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3347; (R1) 1.3379; More...

Intraday bias in GBP/USD is turned neutral first with current recovery, and some consolidations would be seen above 1.3300 temporary low. Further fall is expected as long as 55 4H EMA (now at 1.3483) holds. Below 1.3300 will target a retest on 1.3158 support first. Decisive break there will target 100% projection of 1.3867 to 1.3158 from 1.3657 at 1.2948. However, sustained break of the EMA will dampen the bearish case and turn bias back to the upside for 1.3657 resistance instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

Gold is on a Selling Spree

- Investors are offloading the precious metal due to rising bond yields.

- The factors that have driven the dollar higher since March have returned.

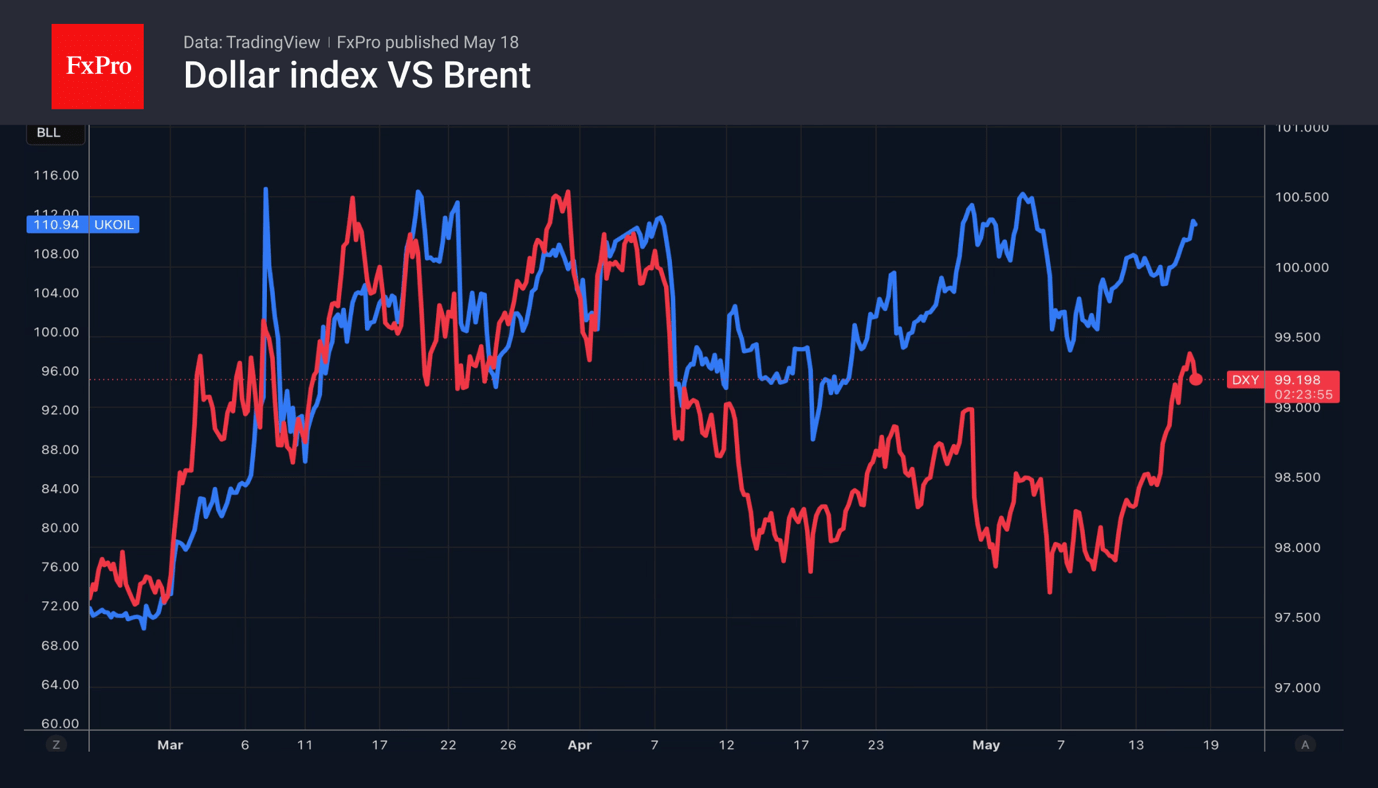

The US dollar posted its best weekly gain in the last two months on the realisation that the conflict in the Middle East is set to continue. The US-China summit failed to yield any breakthroughs on unblocking the Strait of Hormuz, and Donald Trump’s threats are not working. The adversaries are at an impasse, oil prices are rising, dragging up the DXY, the dollar index against a basket of the most popular currencies.

There is a persistent sense of déjà vu in the markets. In March, the dollar strengthened as a safe haven and the currency of a net energy exporter. The US did indeed increase oil and petroleum product exports to a new record of 14.2 million barrels per day. In April, the USD index fell on rumours of an imminent end to the conflict in the Middle East. However, the reality turned out to be different. The opposing sides remain far apart, so the Strait of Hormuz blockade will continue.

Macquarie Group intends to remain bullish on the US dollar until the standoff between the US and Iran ends. Monex, citing a series of strong data on the US economy, argues that even after the conflict ends, the greenback will remain stronger than before. JP Morgan is recommending selling EURUSD for the first time in a year.

Conversely, Morgan Stanley believes that the euro will rise to $1.23 by the end of the third quarter due to lower hedging costs for European investors putting money into US assets.

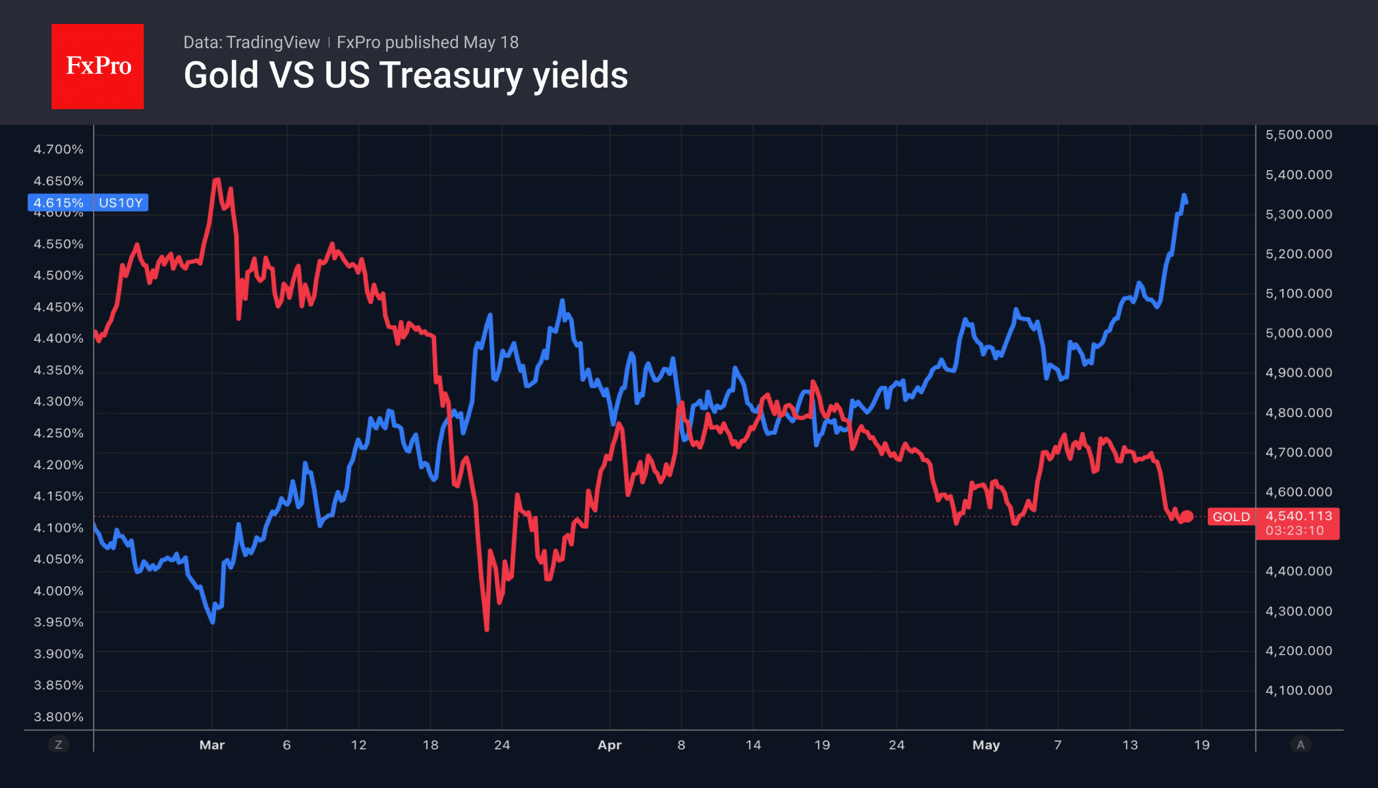

Gold has plummeted to its lowest level since late March amid rising global bond market yields. The yield on 10-year US Treasury bonds has reached its highest level since February 2025, while the yield on Japanese 30-year bonds has risen to its highest level since 1999. Investors are betting on tighter monetary policy worldwide. Yardeni Research is urging the Fed to face the facts and begin a cycle of monetary tightening. Otherwise, the Fed risks losing control of the Treasury market.

Meanwhile, Goldman Sachs estimates that central bank demand for gold bars will rise from 50 tonnes in the year to March to 60 tonnes for the remainder of the year. This should support gold. However, in the short term, the price will remain under pressure due to high liquidity demand from other markets.

China Flash – Data Shows Broad Based Weakness in April

Key takeaways: After rays of light in Q1, the Chinese data batch for April released overnight threw a bit of cold water on the recent signs of improvement in domestic demand. Retail sales growth dropped to a three-year low and the housing market continues to be weak. Industrial production and investments also disappointed. The weak domestic demand highlights the importance of exports as the only growth engine currently. With rising downside risks to global growth due to the Iran war, this engine could start to sputter soon. The renewed weakness in retail sales may be related to the uncertainty from the Iran war and calls for a step-up in economic stimulus. A strong GDP in Q1 of 5% y/y gave some cushion to meet the government's 4½-5% growth target but the renewed decline in activity should be a concern in Beijing.

Details

Retail sales dropped from 1.7% y/y to 0.2% y/y (consensus 1.9% y/y). The seasonally adjusted level also showed a big m/m decline after a move higher in March gave some hopes of improvement. Employment indicators show some improvement, though, which should give support to consumers.

Housing remains weak and the rays of light seen in the past months so far remains to be only rays. Home sales have not stabilized on a broad-based level (chart 2) despite some lift in the big cities. Construction starts also trend lower still and property investments declined 13.7% y/y ytd in April after falling 11.2% y/y ytd in March. Home prices are where you spot some rays of light as price declines keep easing (chart 6).

Industrial production declined from 5.7% y/y to 4.1% y/y. It is at odds with decent activity signals from the PMI statistics in April so it is not clear if it is noise or a real deterioration. Overall investment growth weakened to -1.6% y/y ytd coming from 1.7% y/y ytd in March.

The official unemployment rate declined from 5.4% to 5.2% but in seasonally adjusted terms it is moving broadly sideways. However, employment surveys have showed improvement over the past six months (chart 12).

USD/JPY Rises for Sixth Straight Day: Yen Back on the Cusp of Intervention

USD/JPY climbed to 158.93 on Monday, marking the yen's sixth consecutive session of decline. The Japanese currency is under pressure from a stronger dollar amid rising expectations that the Federal Reserve may raise interest rates this year to curb inflation.

US inflation is accelerating due to the energy shock caused by the ongoing Middle East conflict. At the same time, the US and Iran have yet to reach a peace agreement or make progress on reopening the Strait of Hormuz.

The USD/JPY exchange rate is once again approaching the key level of 160, where Japanese authorities intervened in the foreign exchange market to support the yen in late April.

Markets are closely monitoring the risk of fresh intervention by Tokyo. Additional attention has been drawn to statements from Japanese officials that authorities are ready to intervene in the foreign exchange market as many times as necessary.

Support for such expectations has also come from US Treasury Secretary Scott Bessent, who previously praised Japan's actions to stabilise the yen.

Technical Analysis

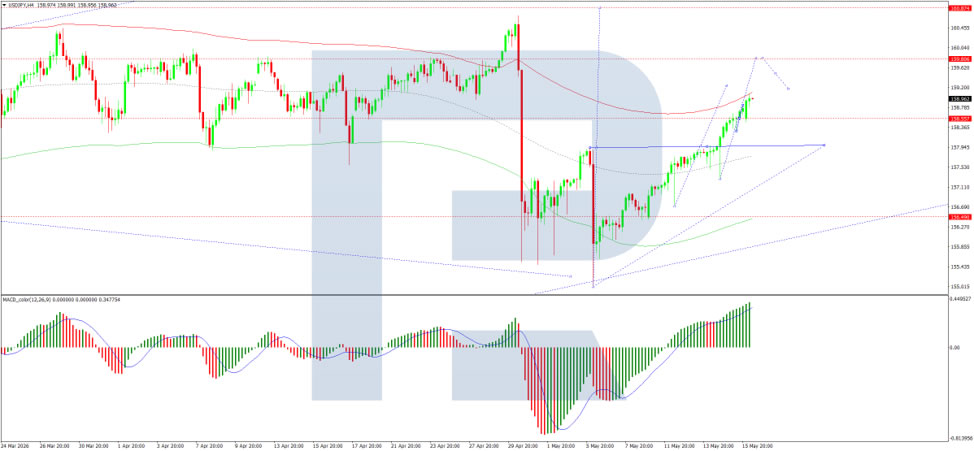

On the H4 chart, USD/JPY is trading within a consolidation range around 158.33 and is moving higher towards 159.30. A test of this level is likely, followed by a possible pullback to 158.30, with scope for a further decline towards 157.00. The MACD indicator supports this scenario, with its signal line above zero and pointing firmly upwards, indicating continued bullish momentum.

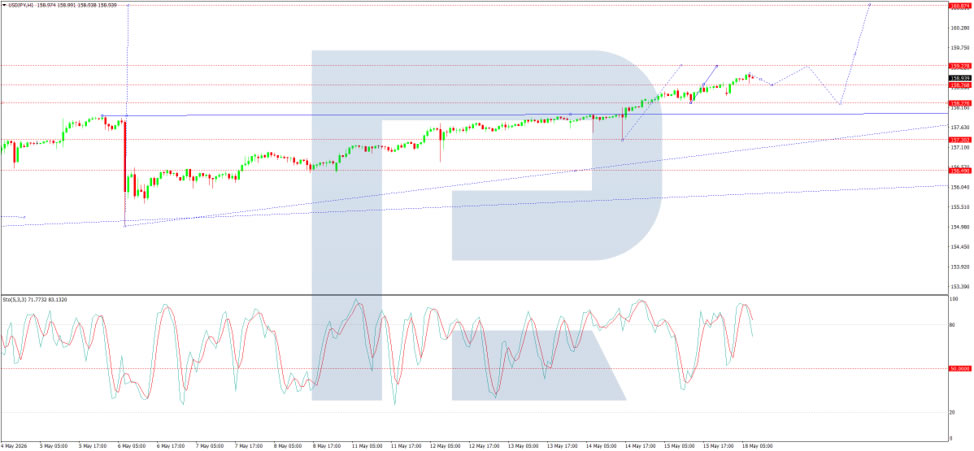

On the H1 chart, USD/JPY has reached 159.00 and is pulling back towards 158.80. A subsequent rise towards 159.30 is possible. The Stochastic oscillator confirms this scenario, with its signal line above 80 and pointing firmly downwards towards 50, indicating that short-term downside pressure may develop.

Conclusion

USD/JPY continues its six-day rally as the yen returns to intervention-warning territory. The dollar is being bolstered by expectations that the Fed may need to raise rates to combat inflation fuelled by the Middle East energy shock, while US-Iran negotiations remain stalled. With the pair approaching the psychologically critical 160 level, where Japanese authorities intervened in late April, markets are on high alert for potential official action. Tokyo has repeatedly signalled its readiness to intervene, and US Treasury Secretary Bessent has offered support for Japan's approach. Technically, further upside towards 159.30 appears likely before any pullback, but intervention risks may cap gains near current levels.

Gold Slips Below 4500, May Stabilize Near 4200 Unless Brent and Treasury Yields Break Crisis Levels

Gold came under renewed pressure earlier today, briefly breaching below $4,500 level as the recent decline resumed. Although the precious metal later recovered some ground, the broader near-term outlook remains tilted to the downside as rising oil prices continue driving Treasury yields and Dollar higher together. The combination is creating an increasingly difficult environment for non-yielding assets, particularly as markets begin repricing inflation and interest rate expectations again.

The key driver behind Gold’s weakness is the oil-led inflation shock developing alongside escalating Middle East tensions. Brent crude’s surge above $111 has reinforced expectations that major central banks, especially the Federal Reserve, may need to keep interest rates elevated for longer despite slowing global growth. Higher oil prices feed directly into inflation expectations, which in turn lift benchmark yields and support the Dollar.

Technically, Gold remains vulnerable while 55 4H EMA (now at 4,649.90), caps rebounds. Further decline is expected toward 100% projection of 4,889.24 to 4,500.67 from 4,773.50 at 4,384.93. However, downside momentum has not yet become disorderly, and there should be meaningful support emerging between the 4,200 and 4,300 region. In particular, 138.2% projection level at 4,236.49 would likely provide a floor for stabilization. Overall, the current decline is viewed as the second leg of the broader corrective pattern from 4,098.45 low.

Still, that relatively stable outlook depends heavily on oil and bond markets remaining contained. If Brent crude remains below $120 crisis threshold and US 10-year Treasury yields stay below 5%, Gold should stabilize around the mentioned 4200/4300 region and then attempt a rebound. However, decisive break of either of those macro levels would likely trigger another wave of aggressive selling in Gold, quickly exposing the key psychological support around 4,000.

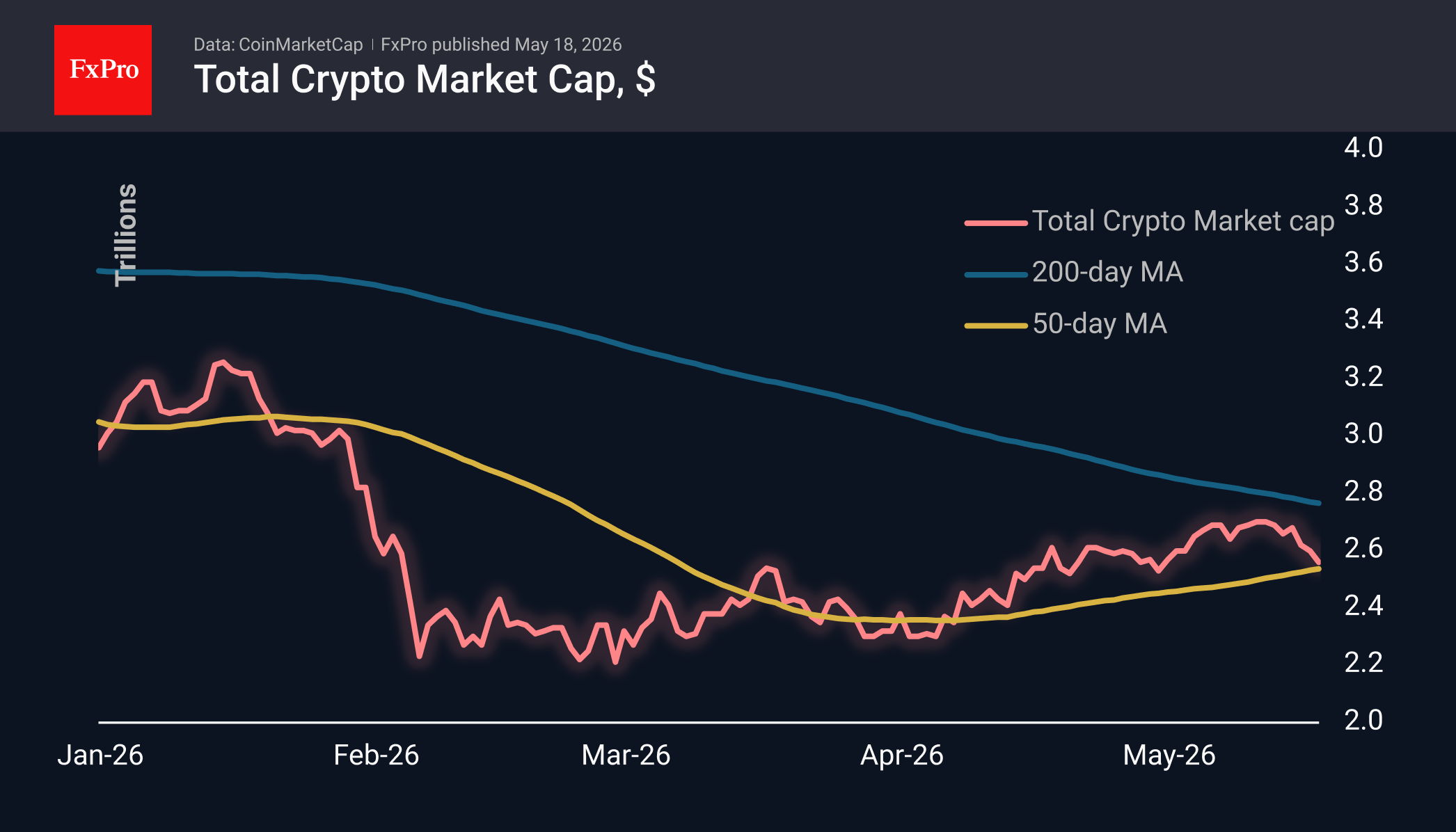

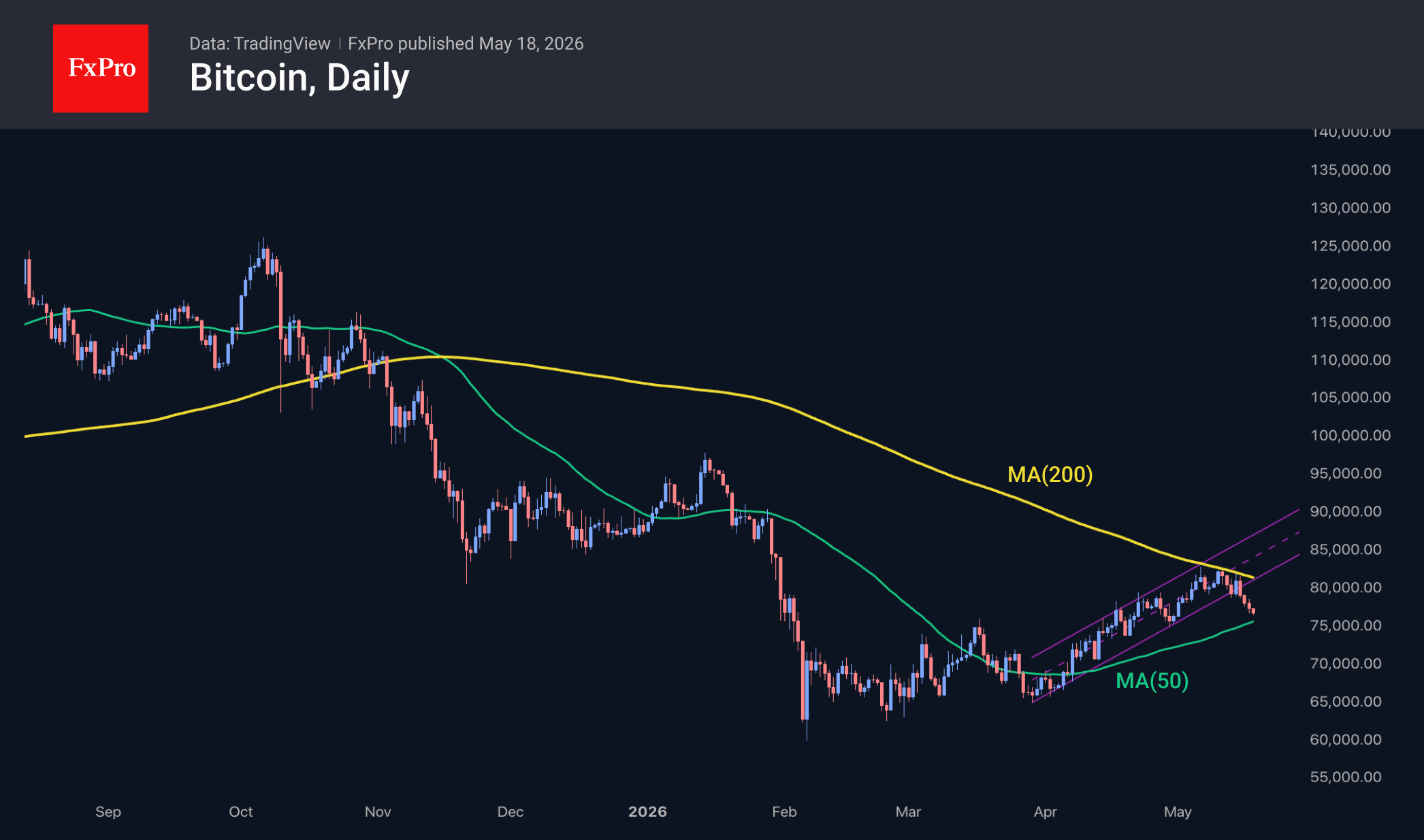

Bitcoin on the Brink of a Knockdown

Market Overview

The crypto market capitalisation has fallen by 5.2% over the past seven days to $2.56 trillion, with the decline accelerating in the second half of the week. Over the past 24 hours, the decline amounted to 1.5%, with selling pressure mounting at the start of Asian trading and a pullback towards the 50-day moving average and the lows seen in late April. The market is thus approaching a point at which the bulls’ strength will be tested. A move lower would technically break the uptrend that has been in place since early April, and dash hopes of an end to the bear market that has been ongoing since October. Among the most active coins, roughly one in ten is rising, with the heaviest losses seen in Bitcoin Cash (-11.6%), Official Trump (-5.5%) and Doge (-4.6%). Zcash (+3%), Toncoin (+1.8%) and Cosmos (+0.9%) are gaining ground.

Bitcoin appears to be in the bears’ grip. Repeated failures to break above the 200-day moving average have sent the market into a downtrend, pushing the price of the leading cryptocurrency down to $76.6K. A 6% loss over less than four days is hardly a capitulation, but rather a disappointment for those who actively bought crypto in April. This corrective pullback has knocked the price out of the growth channel of the past month and a half. However, the uptrend is not formally considered broken until the price falls below previous local lows. And right now, the market is teetering on the edge. A breach below $76K could be followed by an acceleration of the decline, with potential targets near $65K.

News Background

According to SoSoValue, net outflows from spot BTC ETFs amounted to $1 billion over the week, the highest since late January. Outflows from US spot Ethereum ETFs have persisted for two of the last three weeks, totalling $255 million over the week.

Bitcoin has returned to the average purchase price for short-term whales for the third time since October — the $79K–$80K range, notes analyst MorenoDV. The previous two similar tests in October 2025 and January 2026 ended in heavy selloffs.

Bitcoin’s share on centralised crypto exchanges has fallen to 5.6% of the total coin supply, a six-year low, according to Santiment. Large investors continue to move BTC into long-term storage outside of trading platforms.

Ethereum’s correlation with Bitcoin and the technology sector will weaken in the future. Growth drivers will be the development of DeFi, the tokenisation of real-world assets, and the integration of AI into blockchain, according to SharpLink, a company accumulating Ethereum in its reserves and the second largest in terms of volume after BitMine.

Strategy is prepared to sell part of its BTC holdings to repurchase its own convertible bonds, according to a filing with the SEC. The company plans to spend approximately $1.38 billion on the buyback, with the transaction scheduled to close by 19 May.

Following the latest adjustment, Bitcoin mining difficulty increased by 3.12% to 136.61 T. The figure has fallen by approximately 8% since the start of the year and is more than 12% below the all-time high recorded in October.

Sunrise Market Commentary

Markets

Domestic and global topics triggered an accelerating sell-off in both on bond and equity markets with especially the long end of the bond curves underperforming. Yields in the UK, German/EMU and Japan hit “highest levels since…”. US Treasuries which recently reacted more muted also incurred ‘more-than-modest’ losses. The UK again severed as a point in case. At 5.85% , the UK 30-y yield closed at levels not seen since May 1998. UK yields rose between 12.3 bps (2-y) and 19.2 bps (30-y). Markets a are pricing a Andy Burham ‘risk premium’ as the Manchester Major is preparing a path to challenge Keir Starmer’s position as PM via a local by-election next month. Other developed countries are not in exactly the same political situation of the UK, but the nature of challenges is similar. The war in the Middle East and disruptions in supply of oil and other commodities on Friday further raised risk premia on global markets, as headlines suggested that the US and Iran are not moving any closer to any workable agreement to end the war and reopen the Strait of Hormuz. Brent oil closed at $109.2/b. US President Trump this weekend again showed impatience with Iran not giving in to US demands. It illustrates the persistence to the (military & political) stalemate. Trump’s visit to China at least also didn’t bring any specific help for a solution to the conflict. US yields on Friday jumped between 5.2 bps (2-y) and 11.2 bps (10-y). The US 2-y yield now rose well beyond the 4% barrier. Markets are pondering a scenario were the Fed will be forced to raise its policy rate around the turn of the year. German yields added between 8.6 bps (2-y) and 12.4 bps (10-y). At 3.67%, the 30-y yield is touching highest levels since mid-2011. EMU money market are embracing a scenario where the ECB will raise its policy rate by at least 75bps by the turn of the year. For equities, the bond market rout this time wasn’t compensated for by positive earnings headlines. US indices declined up to 1.54 % (Nasdaq). The Euro Stoxx 50 lost 1.81%. The global risk sell-off this time was hefty and clear enough for the USD to reclaim its traditional safe haven role. DXY closed the week at 99.28, to be compared to sub 98 levels at the start of last week. EUR/USD dropped below intermediate support at 1.1655 to close near 1.1625. After a long period of remarkable resilience, sterling also fell prey to the risk sell-off, with EUR/GBP closing north of 0.87.

This morning, the market narrative doesn’t look much different from Friday, with most Asian equites deepening losses. The eco calendar is thin today. So, Friday’s theme’s will still set the tone. We continue to look for comments from ECB members to further clarify their reaction function. This week in the UK, we well get the monthly eco update including inflation data on Wednesday. On Thursday, PMI data will give a new ad-hoc eco and inflation update.

News & Views

The Japanese Prime Minister Takaichi instructed the finance ministry to compile an extra budget to tackle rising commodity prices. She had previously said such measures weren’t necessary but with prices of the likes of oil stubbornly high and rising and reserve funds for other relief measures (e.g. the JPY 170 gasoline price cap) running dry, Takaichi is now changing tac. An extra budget this early in the new fiscal year means it will most likely be funded through additional borrowing. Although its scale isn’t decided yet, fragile (global) bond markets already hit by inflation and fiscal fears are on tenterhooks. Japanese yields are surging this morning with the 40-yr tenor at some point up 17 bps. Gains currently amount to 7 bps at the longest segments of the curve (30-yr-40yr), still enough for the highest levels since its inception. Rising risk premia pressure the yen towards USD/JPY 159 with much of the FX interventions end-April and early-May being undone.

S&P rating agency raised Bulgaria’s credit outlook to positive from stable while keeping the rating at BBB+. It reflects “the potential for Bulgaria's income levels and growth to strengthen, supported by improved political stability, planned reforms, and EU fund disbursements.” This followed a breakthrough in Bulgaria’s five year political stalemate after former president Radev’s party secured an absolute parliamentary majority in the April 19 snap elections. Political paralysis is expected to make way for reforms which combined with Eurozone entry should support Bulgaria's gradual income convergence with that of peers. Economic growth is seen at averaging 2.6% through 2029 with the Middle East conflict only a moderate drag in the short term due to the country’s diversified energy mix. 2026 inflation could amount to 5.3%, materially up from 3.5% expected earlier due to energy prices. Budgetary performance has weakened in recent years, but S&P sees gradual consolidation from the 3.5% of GDP in 2025

Gold Slips As WTI Crude Oil Rally Gains Fresh Momentum

Gold price extended losses below $4,650 before the bulls appeared. WTI Crude oil prices are rising and could climb further higher toward $105.

Important Takeaways for Gold and WTI Crude Oil Prices Analysis Today

- Gold price failed to clear $4,800 and declined steadily against the US Dollar.

- There is a key bearish trend line forming with resistance at $4,625 on the hourly chart of gold at FXOpen.

- WTI Crude oil prices are moving higher above the $100.00 pivot zone.

- There is a connecting bullish trend line forming with support at $101.80 on the hourly chart of XTI/USD at FXOpen.

Gold Price Technical Analysis

On the hourly chart of Gold at FXOpen, the price failed to settle above $4,800 and reacted to the downside, as discussed in the previous analysis. The price traded below $4,750 and $4,700 to enter a short-term bearish zone.

There was a sharp drop below $4,650. The price settled below the 50-hour simple moving average, and RSI dipped below 30. Finally, it tested the $4,480 zone. A low was formed at $4,480, and the price is now correcting some losses.

Immediate hurdle on the upside is $4,550 or the 23.6% Fib retracement level of the downward move from the $4,775 swing high to the $4,480 low. The first major barrier for the bulls could be $4,625 and the 50% Fib retracement. There is also a key bearish trend line forming with resistance at $4,625.

A close above $4,625 could initiate a recovery wave to $4,710. An upside break above $4,710 could send Gold price toward $4,780. Any more gains may perhaps set the pace for an increase toward $5,000.

If there is no fresh increase, the price could continue to move down. Initial support on the downside is near the $4,480 level. The first key area of interest might be $4,420. If there is a downside break below $4,420, the price might decline further. In the stated case, the price might drop to $4,200.

WTI Crude Oil Price Technical Analysis

On the hourly chart of WTI Crude Oil at FXOpen, the price started a fresh increase from $95.20 against the US Dollar. The price gained bullish momentum after it broke $98.00.

There was a sustained upward movement above $99.50 and $100.00. The bulls pushed the price above the 50-hour simple moving average, and the RSI climbed toward 80. A high was formed near $103.85 before there was a minor pullback. The price declined toward the 23.6% Fib retracement level of the upward move from the $95.23 swing low to the $103.85 high.

However, the bulls are active above $102.00. Immediate resistance is near $103.80. If the price climbs further, it could face hurdles near $104.25.

The next major stop for the bulls might be $105.00. Any more gain might send the price toward $106.50. Conversely, the price might correct gains and test a connecting bullish trend line with support at $101.80.

The next area of interest on the WTI crude oil chart could be $99.45 and the 50% Fib retracement. If there is a downside break, the price might decline to $97.00. Any more losses may perhaps open the doors for a move toward $95.20.

Start trading commodity CFDs with tight spreads (additional fees may apply). Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.