Sample Category Title

EUR/USD Weakens Sharply After Key Support Finally Gives Way

Key Highlights

- EUR/USD started a sharp decline below the 1.1700 zone.

- It traded below a rising channel with support at 1.1720 on the 4-hour chart.

- GBP/USD could extend losses if it settles below 1.3300.

- USD/JPY is moving higher above the 158.50 resistance.

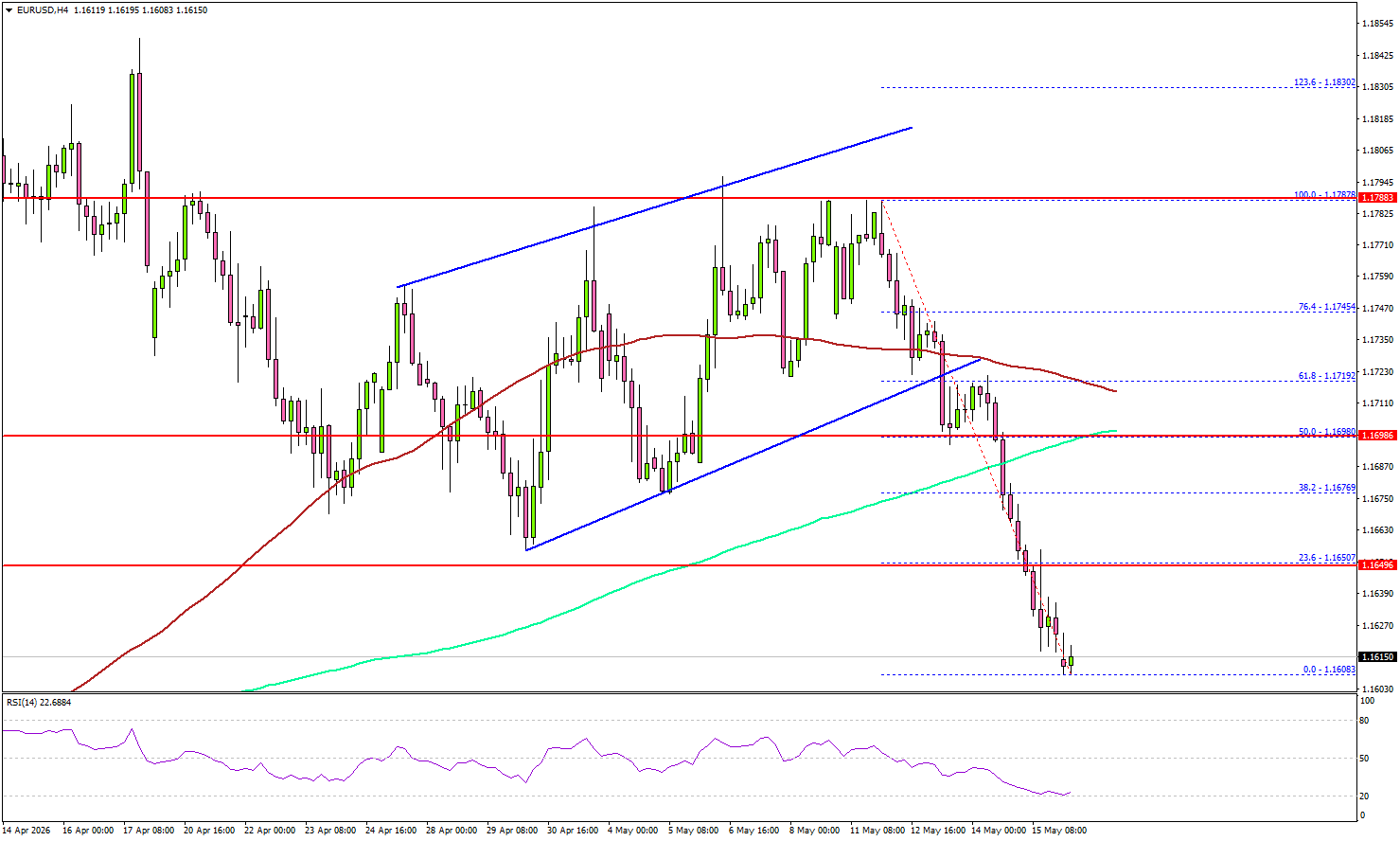

EUR/USD Technical Analysis

The Euro failed to stay above 1.1720 against the US Dollar. EUR/USD started a sharp decline below the 1.1700 and 1.1665 levels.

Looking at the 4-hour chart, the pair traded below a rising channel with support at 1.1720. The bears pushed the pair below 1.1620. A low was formed at 1.1602, and the pair is now consolidating losses well below the 23.6% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1602 low.

It is also well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the pair faces resistance at 1.1650.

The first major resistance sits at 1.1700, the 200 simple moving average (green, 4-hour), and the 50% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1602 low. A close above 1.1700 could open doors for gains above 1.1720 and the 100 simple moving average (red, 4-hour).

In the stated case, the bulls could aim for a move to 1.1800. If there is another decline, the pair could find bids near 1.1600. The first major support sits near the 1.1550 level.

The next support could be 1.1520. A close below 1.1520 might initiate a drop to 1.1450. Any more losses might open the doors for a drop toward the 1.1400 zone.

Looking at GBP/USD, the pair remained in a negative zone, and the bears could aim for a clear move below the 1.3300 support.

Upcoming Key Economic Events:

- NAHB Housing Market Index for May 2026 – Forecast 34.0, versus 34.0 previous.

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 in Asian trading as traders returned from the weekend facing a geopolitical backdrop that had deteriorated sharply on multiple fronts at once.

The failed Trump-Xi summit removed hopes for any immediate diplomatic stabilization. US President Donald Trump then escalated rhetoric dramatically with his “the Clock is Ticking” warning to Iran following talks with Israeli Prime Minister Benjamin Netanyahu. Hours later, markets were hit with reports of a drone strike near the UAE’s Barakah nuclear power plant. By Monday morning, the message from oil markets was becoming unmistakable: this conflict is entering a far more dangerous phase.

What changed over the weekend was not merely tension levels, but the character of the risk itself. A successful strike near nuclear-linked infrastructure in the Gulf fundamentally alters the psychology of the market because it demonstrates vulnerability. Even though no reactor was hit directly and no radiation leak occurred, one reactor reportedly shifted temporarily onto emergency diesel power. If energy-linked infrastructure can be reached once, it can be reached again.

At the same time, the diplomatic path appears dangerously close to collapse. Trump’s Tuesday meeting with national security advisers is being viewed by markets less as a symbolic consultation and more as a potential gateway toward expanded military operations. The broader conflict has already evolved far beyond isolated exchanges. Strait of Hormuz shipping remains near total disruption, proxy attacks are spreading across the region, and Gulf states are increasingly being pulled directly into the confrontation.

Technically, Brent may now be approaching a critical breakout phase. Immediate focus is on the 61.8% projection of 96.03 to 108.45 from 130.88 at 111.56. Decisive break there could unleash a rapid momentum extension toward 100% projection at 116.30 next.

More importantly, the larger converging triangle consolidation from 119.50 peak appears close to completion. If confirmed, the broader uptrend could be preparing to attack the 120 crisis threshold again — a level markets associate with systemic economic stress rather than simple commodity volatility.

From here, the oil market faces two radically different endings.

- The first is a short, intense military exchange involving coordinated strikes but followed by a rapid internationally enforced ceasefire. Under that outcome, Brent could spike toward $135–145 in a matter of days before collapsing sharply.

- The second, and more structurally dangerous scenario, would emerge if Tuesday’s White House meeting leads to a prolonged conflict involving sustained attacks on Gulf export or processing infrastructure. In that case, oil above $120 may no longer represent a temporary panic spike, but the beginning prolonged uptrend extension.

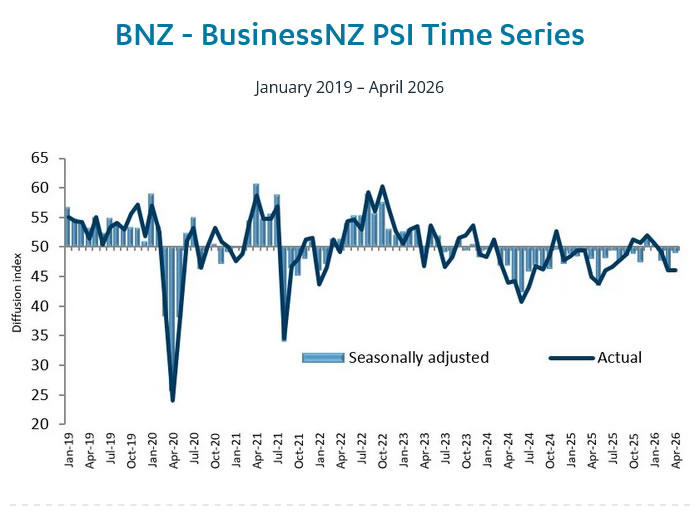

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, though activity remained in contraction territory as firms continued to grapple with rising fuel costs and disruption linked to the Middle East conflict. BusinessNZ Performance of Services Index improved from 46.2 to 48.9, but still below the 50 expansion threshold.

Underlying components were mixed but generally less weak. Activity/sales rose from 44.7 to 48.9, while employment improved from 46.6 to 48.5. New orders/business provided the brightest signal, climbing from 46.0 to 51.2 to return to expansion territory. However, supplier deliveries slipped from 47.2 to 46.6, while stocks/inventories edged up from 46.2 to 47.6.

BusinessNZ Chief Executive Katherine Rich said more than two-thirds of respondents continued to report negative conditions, with many citing fuel prices as a major pressure point. She warned that ongoing disruption to shipping through the Strait of Hormuz made a quick return to sector-wide expansion difficult to envision.

Smaller firms appeared particularly vulnerable, with the micro-business sub-index at just 44.4, while medium-large firms outperformed at 55.5.

| Component | March | April |

|---|---|---|

| Headline PSI | 46.2 | 48.9 |

| Activity / Sales | 44.7 | 48.9 |

| Employment | 46.6 | 48.5 |

| New Orders / Business | 46.0 | 51.2 |

| Stocks / Inventories | 46.2 | 47.6 |

| Supplier Deliveries | 47.2 | 46.6 |

Strong US Inflation Lifts Dollar, Pressures Risk Assets

US stocks fell toward the end of last week after CPI and PPI data came in higher than expected. This increased worries that US inflation may stay high, which pushed long-term US interest rates higher. Higher rates were negative for equities but helped strengthen the US dollar.

USD/JPY rose as the dollar strengthened and the yen stayed weak. There was no clear sign of direct yen-buying intervention from Japanese authorities. Some US officials suggested that higher interest rates in Japan would be a more effective way to support the yen. The yield on Japan’s 10-year government bond also rose to 2.72%, its highest level since 1997, as investors remained worried about Japan’s large government debt.

WTI oil moved back above $100 as negotiations failed to produce a positive result and supply concerns continued. In the UK, political uncertainty hurt Sterling as the prime minister lost support, causing GBP/USD and GBP/JPY to close near their weekly lows. Gold also fell as the stronger US dollar reduced demand.

Markets This Week

US Stocks

The Dow continued to face resistance near the highs from earlier in the year, while technology stocks remained more in favour with investors. However, Friday’s sharp fall, triggered by concerns about high US inflation, pushed the index below the 10-day moving average. This is a potentially negative technical signal. For this week, sideways to lower trading looks most likely. With few major economic indicators due, market attention is likely to remain focused on the inflation outlook. Buying near strong support may still offer opportunities, but traders should be cautious if selling pressure continues. Resistance levels are at 50,000, 50,500 and 51,000. Support is seen at 49,000, 48,500, 48,000, 47,000 and 46,000.

Japanese Stocks

Despite hitting a new record high, the Nikkei 225 closed lower last week as losses in US equities negatively impacted investor sentiment. Concerns about a potential increase in official Japanese interest rates to support the weak yen also weighed on Japanese stocks. The index has risen significantly in recent weeks, but with prices now below the 10-day moving average, sideways to lower trading looks more likely this week. Resistance is seen at 63,000, 64,000, 65,000, 66,000 and 67,000, while support is at 61,000, 60,000, 58,500 and 57,000.

USD/JPY

USD/JPY had a very strong week as higher-than-expected US inflation data widened the gap between long-term US and Japanese interest rates, encouraging more buying. High WTI oil prices also added pressure on the yen. Despite moving above 158.00, an area where the Bank of Japan has intervened before, there was no clear sign of intervention this time. The Bank of Japan may now consider whether an interest rate increase could help stop yen weakness, but that could also create risks for the Japanese economy. Last week’s move higher surprised many traders, but further gains may become more difficult from here. For this week, looking for selling opportunities ahead of 160.00 may be the best approach. Resistance is at 159.00, 160.00 and 160.50, while support is seen at 158.00, 157.00, 156.00, 155.00 and 154.00.

Gold

Higher long-term US interest rates and a stronger US dollar were negative for gold last week, pushing the market lower and leading to a sharp sell-off on Friday. Gold managed to hold support around the April lows, so range trading conditions are still in place for now. In the short term, the market looks a little oversold, which means support may continue to hold. However, the risk of a quick fall is increasing if the US dollar strengthens further and long-term US interest rates continue to rise. Resistance is at $4,750, $4,900, $5,000, and $5,100, while support is at $4,550, $4,500, and $4,400.

Crude Oil

Another week of headlines but no clear conclusion to the war in Iran, together with limited supplies from the Middle East, helped WTI crude oil continue to push higher above $100. There is always a risk of a quick fall if negotiations make progress, but for now the market remains supported. Short-term range trading looks like the best approach this week, as long as WTI can hold above $100. Resistance is at $110 and $120, while support is at $100, $90, $80, $75, $70, and $67.50.

Bitcoin

Bitcoin broke its recent uptrend last week as higher US interest rates and weaker US equities encouraged selling in relatively quiet market conditions. The 10-day moving average is now pointing lower, following the short-term downtrend. For this week, looking for selling opportunities close to the 10-day moving average may be the best approach. Resistance is at $80,000, $85,000, and $90,000, while support is at $75,000, $65,000, $60,000, and $55,000.

This Week’s Focus

- Monday: China Unemployment Rate and Industrial Production

- Tuesday: Japan GDP and Industrial Production, UK Unemployment Rate, EU Trade Balance, US Pending Home Sales

- Wednesday: UK CPI, EU CPI, US FOMC Meeting Minutes

- Thursday: Japan Trade Balance, Australia Unemployment Rate, EU HCOB Eurozone Manufacturing PMI, UK S&P Global Manufacturing PMI, US Housing Starts and S&P Global Manufacturing PMI

- Friday: Japan National CPI, UK Retail Sales, US Michigan Consumer Sentiment

While there are few major economic releases this week, the US FOMC Meeting Minutes will be the main event to watch. Markets may still see higher volatility than usual as the impact of stronger US inflation data continues to affect stocks, bonds, currencies, and gold.

USD/JPY will remain in focus, especially if the pair moves back toward 160. A move to this level could increase pressure on Japanese authorities to act, including possible yen-buying intervention. GBP/USD and GBP/JPY traders should also watch political developments in the UK, as uncertainty around the prime minister could continue to weigh on Sterling.

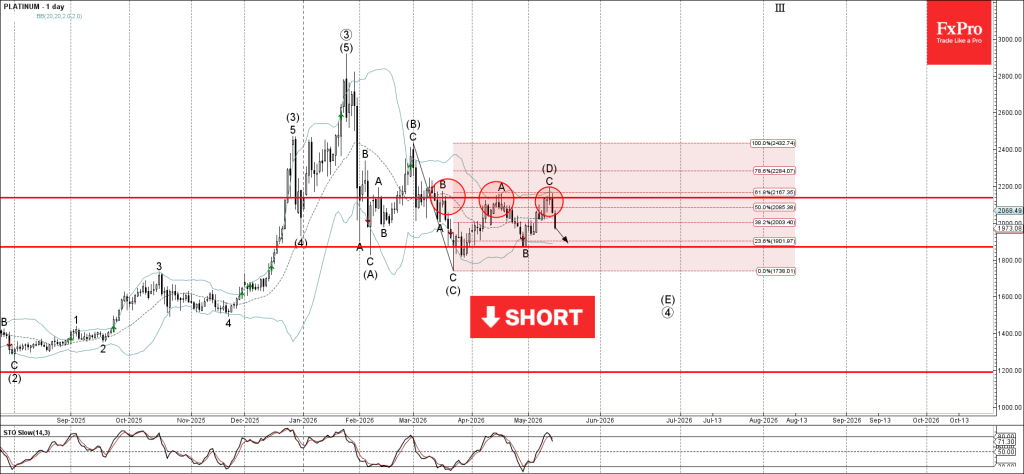

Platinum Wave Analysis

Platinum: ⬇️ Sell

- Platinum reversed from resistance level 2140.00

- Likely to fall to support level 1871.50

Platinum recently reversed down from the pivotal resistance level 2140.00 – which stopped earlier waves B and A – coinciding with the 61.8% Fibonacci correction of the downward impulse (C) from February.

The downward reversal from the resistance level 2140.00 started the active downward wave (E).

Platinum can be expected to fall to the next support level 1871.50 – which has been reversing the price from February.

Eco Data 5/18/26

| GMT | Ccy | Events | Act | Cons | Prev | Rev |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Apr | 48.9 | 46 | 46.2 | |

| 02:00 | CNY | Industrial Production Y/Y Apr | 4.10% | 5.90% | 5.70% | |

| 02:00 | CNY | Retail Sales Y/Y Apr | 0.20% | 2.00% | 1.70% | |

| 02:00 | CNY | Fixed Asset Investment (YTD) Y/Y Apr | -1.60% | 1.60% | 1.70% | |

| 14:00 | USD | NAHB Housing Market Index May | 37 | 34 | 34 |

| 22:30 | NZD |

| Business NZ PSI Apr | |

| Actual | 48.9 |

| Consensus | |

| Previous | 46 |

| Revised | 46.2 |

| 02:00 | CNY |

| Industrial Production Y/Y Apr | |

| Actual | 4.10% |

| Consensus | 5.90% |

| Previous | 5.70% |

| 02:00 | CNY |

| Retail Sales Y/Y Apr | |

| Actual | 0.20% |

| Consensus | 2.00% |

| Previous | 1.70% |

| 02:00 | CNY |

| Fixed Asset Investment (YTD) Y/Y Apr | |

| Actual | -1.60% |

| Consensus | 1.60% |

| Previous | 1.70% |

| 14:00 | USD |

| NAHB Housing Market Index May | |

| Actual | 37 |

| Consensus | 34 |

| Previous | 34 |

Bond Yields Explode Globally as Markets Enter “Triple Higher” Regime Following Underwhelming Trump-Xi Summit

Global financial markets entered a far more dangerous macro phase last week as the underwhelming Trump-Xi summit failed to deliver meaningful progress on reopening the Strait of Hormuz or easing broader geopolitical tensions. Instead of calming investors, the summit reinforced fears that the global economy may now be entering a prolonged period of structurally higher inflation driven by persistent energy disruption and tightening financial conditions.

The market reaction was swift and broad-based. Crude oil prices surged again, with Brent climbing back above $109 and WTI closing above $101 as traders increasingly concluded that the world is adapting to a continuing Hormuz blockade rather than preparing for its resolution. That reignited inflation fears globally and triggered an aggressive selloff in sovereign bond markets. US Treasury yields surged alongside gilt, bund, and Japanese government bond yields as investors rapidly repriced the outlook for interest rates under a “higher-for-longer” inflation regime.

The result was a powerful “Triple Higher” market environment dominated by higher oil prices, higher bond yields, and a stronger Dollar. That combination acted as a macroeconomic wrecking ball across global asset classes. Stocks surrendered earlier AI-driven gains late in the week, precious metals collapsed under the pressure of surging real yields and Dollar strength, and global risk sentiment deteriorated sharply as markets questioned how long the current inflation shock can persist before something in the global economy finally breaks.

Trump-Xi Summit Delivers Symbolism, Not Solutions

The Trump-Xi summit in Beijing was supposed to provide markets with a geopolitical release valve. Instead, it delivered high-level diplomatic symbolism without resolving any of the structural issues driving the current inflation and energy shock. Investors entered the meeting hoping for concrete progress on reopening the Strait of Hormuz, stabilizing global oil flows, and reducing tensions surrounding the U.S.-Iran conflict. By the end of the summit, however, markets were left increasingly convinced that the crisis could persist much longer than previously expected.

On the surface, both sides attempted to present the talks positively. Trump emphasized that China would significantly increase purchases of American crude oil and reiterated that both leaders wanted “the straits open.” China’s Foreign Ministry also stated that shipping routes “should be reopened as soon as possible” and called for a “comprehensive and lasting” ceasefire. But the carefully managed language masked a deeper reality: there was no operational framework, no enforcement mechanism, and no sign that Beijing was prepared to exert decisive pressure on Tehran to fully reopen Hormuz.

That failure mattered enormously for markets. Instead of pricing diplomatic de-escalation, oil traders returned to pricing a world where global energy flows are simply reorganized around continuing disruption. Trump’s comments about Chinese purchases of American oil reinforced the impression that Washington may be preparing for prolonged instability rather than expecting rapid normalization. Meanwhile, the broader trade announcements involving Boeing aircraft, soybeans, and purchase commitments were largely dismissed by investors as superficial headline agreements that left the deeper U.S.-China trade and technology confrontation fundamentally unchanged.

Global Bond Yields Explode as Inflation Fears Intensify

Global bond markets experienced one of the most aggressive synchronized selloffs in months last week as investors increasingly accepted that the inflation shock linked to the Strait of Hormuz crisis may persist far longer than previously expected. With the Trump-Xi summit failing to provide a geopolitical release valve, markets rapidly shifted toward pricing structurally higher inflation, tighter financial conditions, and a prolonged period of elevated interest rates across the world’s major economies.

US Treasury yields moved sharply higher at the center of the repricing. The benchmark 10-year yield surged through the psychologically important 4.5% level and settled near 4.59%, while shorter-dated yields also climbed aggressively as traders abandoned expectations for Fed rate cuts. Sticky inflation data, elevated oil prices, and resilient consumer demand reinforced fears that inflation could remain entrenched well into next year. At the same time, the beginning of Kevin Warsh’s leadership at the Federal Reserve added another source of hawkish repricing, with markets viewing the incoming Fed Chair as less willing to tolerate persistent inflation than Jerome Powell. Fed funds futures now imply around a 50% probability of at least one rate hike by year-end.

The global spillover was severe. In the UK, 10-year gilt yields climbed to 5.15%, a level not seen since mid 2008, reflecting a toxic combination of energy-driven inflation fears and mounting political anxiety surrounding Prime Minister Keir Starmer’s government. Germany’s 10-year bund yield rose to 3.14%, its highest level since 2011, as the Eurozone braced for a renewed inflation shock despite weakening growth momentum. Meanwhile, Japan experienced some of the sharpest moves globally, with the 10-year JGB yield reaching 2.73% - the highest yield since May 1997 on fiscal strain fears.

The Oil-Inflation Feedback Loop Tightens

At the center of last week’s market turmoil was an increasingly dangerous oil-inflation feedback loop that continued tightening financial conditions globally. With the Strait of Hormuz remaining effectively blocked and the Trump-Xi summit failing to deliver any credible reopening framework, crude oil prices surged again. Brent crude closed above $109 while WTI settled north of $101, reinforcing fears that the global economy may now be entering a prolonged period of structurally elevated energy costs.

The mechanism driving markets was clear throughout the week. Higher oil prices immediately intensified inflation expectations across major economies already struggling with sticky price pressures. That in turn triggered a sharp rise in global bond yields as investors rapidly pricing a world where policymakers must either maintain restrictive interest rates for much longer or tighten further to prevent energy-driven inflation from becoming embedded through wages and broader pricing behavior.

The resulting “Triple Higher” regime — higher oil, higher yields, and higher Dollar — acted as a powerful tightening force across nearly every asset class. Rising yields strengthened the Dollar through widening interest rate differentials and safe-haven demand, while tighter financial conditions simultaneously pressured equities, commodities, and precious metals.

Cross-Asset Damage Spreads Across Global Markets

The combination of surging bond yields, elevated oil prices, and tightening financial conditions triggered widespread damage across global asset classes last week. What initially began as a resilient AI-driven equity rally earlier in the week ultimately gave way to a broad risk-off reversal on Friday as markets increasingly struggled to absorb the implications of structurally higher inflation and interest rates.

Global equity markets came under heavy pressure as rising yields sharply increased discount rates and undermined valuations, particularly outside the technology sector. The Nikkei 225 fell more than -2% on the week, while Germany’s DAX dropped nearly -1.6% as European markets confronted both higher energy costs and deteriorating growth expectations. US stocks proved somewhat more resilient due to continued enthusiasm surrounding AI and mega-cap technology names, but even NASDAQ surrendered much of its earlier momentum by week’s end as Treasury yields accelerated higher. The sharp Friday selloff suggested that even the AI trade is not fully immune to the tightening pressure created by the “Triple Higher” regime.

Precious metals suffered some of the heaviest losses across markets. Gold plunged roughly -$170 over the week to close near $4,560 as surging real yields and broad Dollar strength overwhelmed any safe-haven demand generated by geopolitical tensions. Silver performed even worse, suffering a brutal late-week collapse as both higher real yields and fears surrounding industrial supply chains tied to China weighed heavily on sentiment.

Higher Yields and Risk Aversion Fuel Powerful Dollar Rally

Currency markets last week were dominated by broad Dollar strength as surging Treasury yields, rising oil prices, and deteriorating global risk sentiment combined to reinforce demand for the greenback. Dollar finished as the strongest major currency by a clear margin, benefiting simultaneously from widening yield advantages, safe-haven demand, and growing expectations that the Federal Reserve may need to maintain restrictive policy for much longer amid persistent inflation pressure.

The strength of Dollar was particularly notable because it occurred alongside weakness in both global equities and precious metals, highlighting how aggressively markets are prioritizing yield and liquidity over traditional inflation hedges. The Canadian Dollar finished as the second strongest performer, supported largely by the sharp rebound in crude oil prices and Canada’s commodity-linked exposure to the energy shock. Swiss Franc and Yen also outperformed most major peers as defensive positioning intensified late in the week, although both were ultimately overshadowed by the Dollar’s overwhelming yield advantage.

At the other end of the spectrum, Sterling was the weakest major currency as investors continued to price mounting political instability in the UK alongside rising fiscal and energy concerns. Kiwi and Aussie also underperformed as higher global yields and worsening risk sentiment pressured higher-beta currencies tied closely to global growth expectations and China demand. Euro finished near the middle of the pack, supported modestly by rising bund yields and growing expectations that the ECB may eventually need to tighten policy further if energy-driven inflation persists.

Outlook: The “Triple Higher” Regime May Persist Until Hormuz Reopens

The dominant macro theme heading into the coming weeks is likely to remain the “Triple Higher” regime of higher oil prices, higher bond yields, and a stronger Dollar. As long as the Strait of Hormuz remains effectively disrupted and global energy supply chains continue operating under severe strain, markets are unlikely to meaningfully reverse the inflation repricing that accelerated last week. .

Oil remains the most important variable in this entire macro framework. Markets are would continue to focus on physical shipping conditions rather than political headlines. The UAE’s accelerated effort to expand bypass pipeline capacity through Fujairah highlights how even regional producers are beginning to prepare for prolonged disruption rather than rapid normalization. As long as Hormuz remains restricted, Brent crude likely remains structurally supported in the $100-$115 range, keeping upward pressure on inflation expectations globally.

US 10-year Treasury yields breaking decisively above 4.5% may prove especially important technically and psychologically, as the move signals that markets are beginning to demand a larger inflation risk premium. If yields continue climbing toward the 4.75%-5.00% region, financial conditions could tighten significantly further and place much heavier pressure on equities and credit markets globally.

The key turning point for markets remains remarkably simple: a verified reopening of the Strait of Hormuz.

That is the single most important macro domino capable of breaking the current inflation-yield-Dollar feedback loop. If tanker traffic begins flowing reliably again and the geopolitical risk premium embedded in oil collapses, Brent crude could quickly fall by $15-$20 per barrel, sharply easing inflation fears and allowing bond yields to stabilize. But until markets see actual physical normalization — not merely diplomatic language — investors are likely to remain defensive and continue pricing persistent inflation risk.

The one important counterforce to this broader tightening regime remains the AI-driven equity boom, particularly in the U.S. The resilience of mega-cap technology stocks and continued optimism surrounding AI productivity gains have so far helped cushion broader equity weakness. If NASDAQ and S&P 500 can quickly resume their record runs after the recent pullback, risk appetite could partially offset safe-haven Dollar demand. However, even the AI trade may struggle to remain fully insulated if oil prices stay elevated and global yields continue rising aggressively.

The Kevin Warsh Repricing and Inflation Points: Markets Weekly Outlook

- Discover our Weekly Market Outlook, exploring themes and events that forged financial flows throughout the week.

- Markets are subject to significant repricing after the confirmation of Kevin Warsh as the next Fed Chairman, and this theme should continue to price throughout the coming week.

- A few inflation releases, including Canada and UK CPI, will continue to provide clarity into the market situation.

- Get ready for next week's action by exploring upcoming events across global markets.

Week in Review: Earnings Break Records, Pulling Markets Higher

Stock markets reached spectacular new highs just yesterday, heavily profiting from relentless artificial intelligence trends and a massive wave of record corporate earnings.

The S&P 500 aggressively breached the monumental 7,500 milestone, while the Dow Jones Industrial Average temporarily reclaimed the historic 50,000 mark as global risk appetite peaked.

Adding to this initial bullish momentum, the highly anticipated summit between President Trump and Chinese President Xi Jinping delivered a highly constructive geopolitical tone.

The two leaders established aligning views regarding the ongoing Middle East conflict and the general world order, with the two superpowers needing to collaborate.

Investors are now looking ahead to the next encounter between the two leaders, with an official invitation extended for President Xi to visit Trump in the United States in mid-September.

However, while these diplomatic developments generated better hopes for a sustainable peace process, financial markets are already rapidly turning the page on this theme.

Despite the midweek ecstasy, a much more dominant macroeconomic theme is now aggressively gripping the markets and causing widespread bloodshed ahead of the weekend.

Following the official Senate confirmation of Kevin Warsh as the next Federal Reserve Chairman, risk assets are subject to a brutal, significant repricing.

Ruthless bearish flows wiped out recent equity, metals and crypto gains as the US Dollar exploded higher at the direct expense of virtually all other asset classes.

Markets are hyper-focusing on the severe, long-term implications of a Warsh-led Federal Reserve. Institutional capital is actively preparing for a massive, systematic emptying of the central bank's balance sheet, which remains one of the new Chair's dearest ambitions.

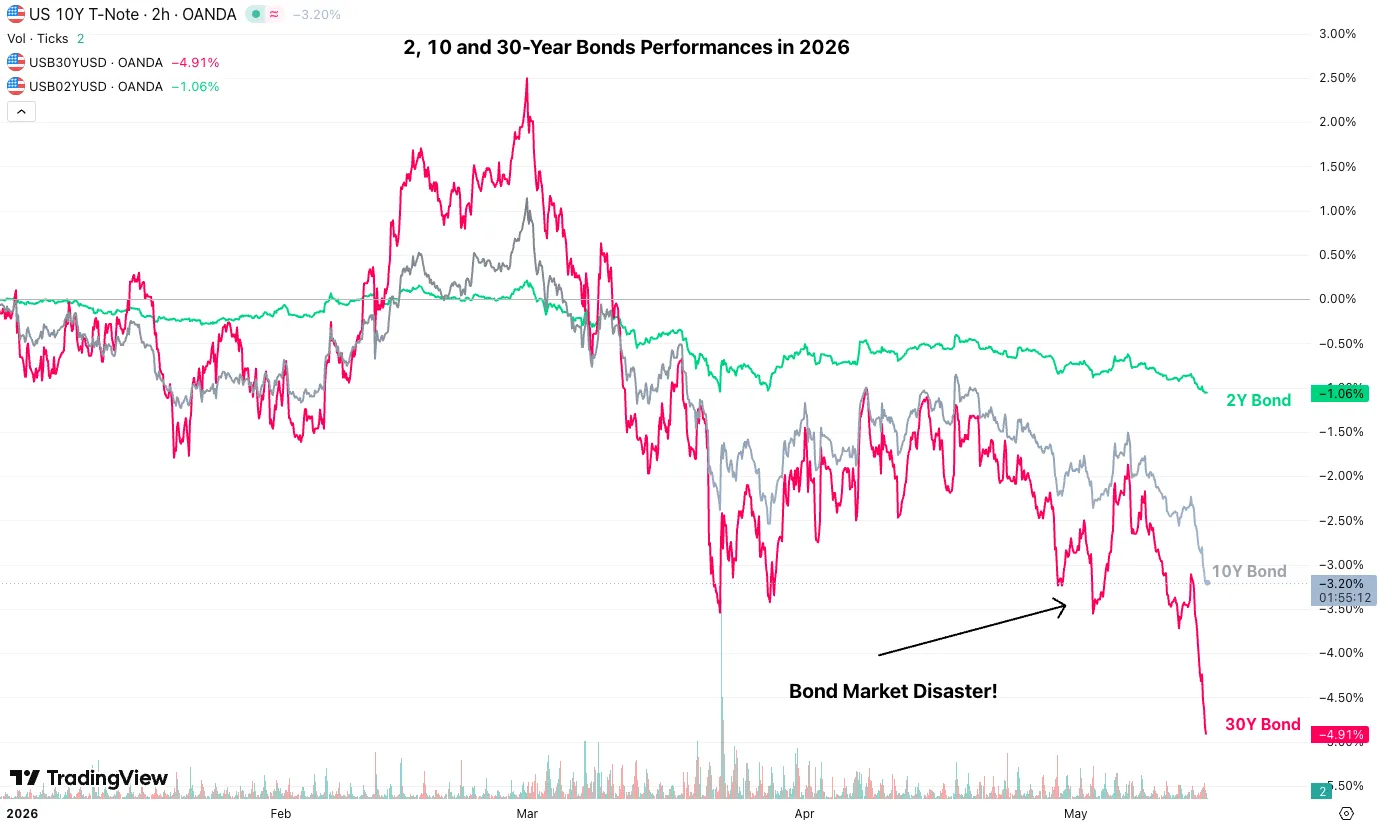

You can see this in the shocking action in bond markets, which threatens to trigger cascading effects into the broader market regime.

Broad US bond market since the beginning of 2026. Source: TradingView, May 15, 2026.

This aggressive trajectory possesses the terrifying potential to severely impact the foundational liquidity system that has supported global markets since the post-Great Financial Crisis era.

As this historic recalibration drains speculative excess from the financial system, this structural liquidity shift is the exact theme that continues to heavily dictate price action heading into next week and the coming months.

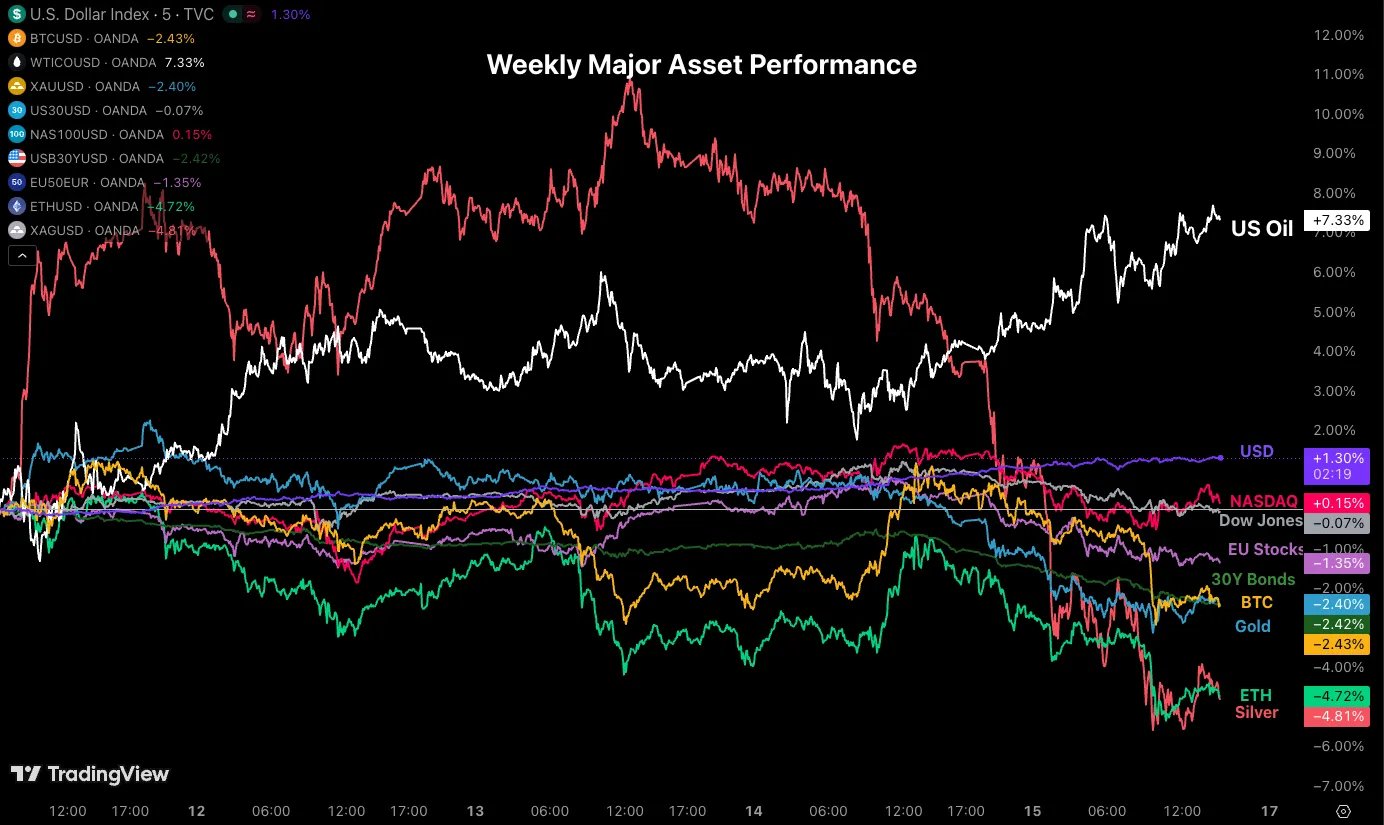

Weekly Performance Across Asset Classes

Weekly asset performance. Source: TradingView, May 15, 2026.

What could have been a dream-like week for major assets quickly turned into a dramatic rewinding, which took out more than what it gave.

When markets fear a drain in liquidity, it quickly brings back gigantic fears of a much more ruthless pre-GFC regime, where demand gets pushed and pulled by cyclical factors rather than the continuous support that it had seen in the past 17 years.

Stock markets, cryptos and metals, which had started the week on a rocketship, quickly turned back in the other direction, with most assets now down on the week.

The only exceptions remain WTI crude and the US Dollar.

The Week Ahead: G7 Meeting, UK and Canada CPI, and High-Tier PMI Reports

One of the key geopolitical events is the G7 meeting, which aims to provide more collaboration among members: Canada, France, Germany, Italy, Japan, the United Kingdom, and the United States.

In terms of broader markets, players will want to focus on the Kevin Warsh trade, bullish for the US Dollar and bearish on everything else.

Asia Pacific Markets: Australian Employment and Broad Economic Indicators

Next week's APAC calendar brings heavy volatility across major economies.

China kicks off with high-impact Industrial Production forecast at 5.9% and Retail Sales at 2.0%, before the PBoC holds interest rates at 3.0%.

Japan faces critical Q1 GDP data, with expectations for a 1.7% annualized print, ahead of Thursday's National CPI.

Australia navigates the RBA meeting minutes and Wednesday's pivotal employment report, projecting a steady 4.3% unemployment rate.

Finally, New Zealand traders prepare for Thursday's Q1 Retail Sales data.

Europe and UK Markets: UK Employment and Inflation, Along With Flurries of Economic Data

Get ready for a ton of action for the Old Continent.

In the UK, traders brace for Tuesday’s 4.9% unemployment rate and Wednesday’s critical CPI report, with headline inflation forecast at 3.3%. Thursday’s UK Services PMI is expected at 52.7.

In Europe, focus shifts to PMIs, projecting contraction in Germany at 48.4 and the broader Eurozone at 48.8.

Friday caps off the week with German Q1 GDP growth anticipated at 0.3%.

And do not forget a high number of ECB and BoE speakers throughout the week.

North American Markets: Canadian CPI, FOMC Minutes and US PMIs

Next week, North American markets face pivotal data as traders seek fresh direction. In Canada, Tuesday's crucial CPI report takes center stage, with previous core YoY inflation sitting at 2.5%, followed by Friday's retail sales forecast at 0.6%.

Meanwhile, US markets will hyper-focus on Wednesday's critical FOMC minutes for monetary policy clues.

The US narrative then shifts to economic health on Thursday, highlighted by preliminary Manufacturing PMI, previously 54.5, and Services PMI, previously 51.0.

Keep a close eye on US markets and bonds, particularly after the end-of-week turmoil.

Next Week's High-Tier Economic Events

Next week's economic calendar. Source: TradingEconomics.

Safe trades and keep an eye on US-Iran developments, along with the Warsh trade.

The Weekly Bottom Line: Changing of the Guard

Canada – A Calm Week Before the Inflation Test

Canadian financial markets were relatively steady this week, though rising bond yields signaled a modest firming in rate expectations. In the absence of major domestic data, markets were shaped by global forces, as oil price volatility and lingering inflation uncertainty pushed Government of Canada yields higher across the curve. The TSX index climbed during the week, while demand for the U.S. Dollar strengthened, causing the Canadian dollar to drop by three-tenths of a cent as persistent volatility directed flows toward the USD.

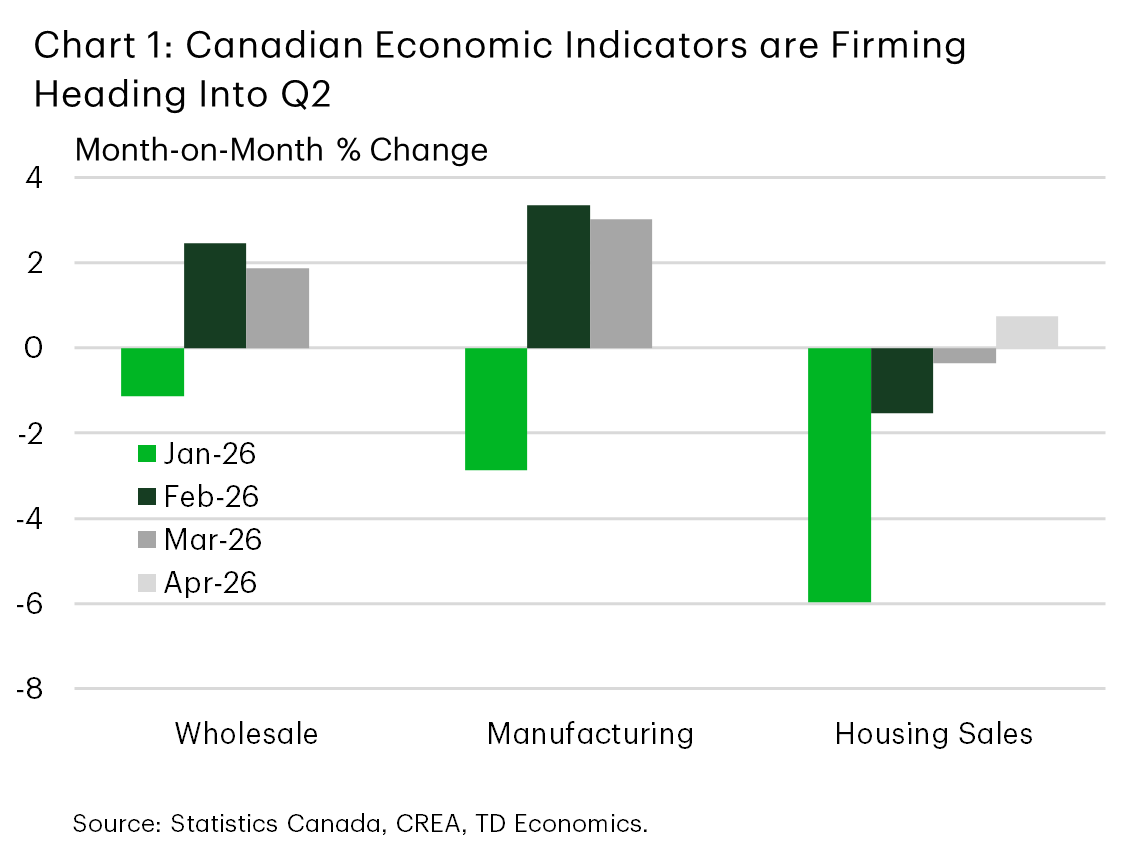

This week’s data offered a more incremental read on economic conditions (Chart 1). March wholesale trade and manufacturing sales firmed up the trajectory of goods-sector activity, with early indications pointing to some stabilization following a soft start to the year. While neither release is likely to materially alter the broader growth backdrop, they will help refine tracking for first quarter GDP, which points to modest growth.

Meanwhile in the housing market, April home sales edged higher, consistent with our view that activity should see a bounce back in second quarter. Housing starts data also beat consensus expectations. Stepping back, we still expect only a gradual improvement in housing conditions in 2026, as high borrowing costs, affordability issues, and slower population growth continue to dampen demand and construction.

In a week with little economic data, the Bank of Canada’s Summary of Deliberations reinforced uncertainty around the policy outlook. While higher energy prices are expected to raise inflation soon, Governing Council judged there’s scope to remain patient and hold rates steady as the economy evolves as expected. They emphasized the outlook remains highly dependent on incoming data, with risks in both directions. Persistent strength in oil prices could broaden inflation pressures and warrant tighter policy, while weaker growth tied to trade or external shocks could necessitate easing, given uncertainty around the remaining slack in the economy.

Alongside the monetary policy update, reports of ongoing negotiations between Ottawa and Alberta over industrial carbon pricing and a potential west coast pipeline point to a shift toward aligning climate policy with major project development. Such efforts could help improve investment clarity in Canada’s energy sector, with implications for longer-term growth capacity.

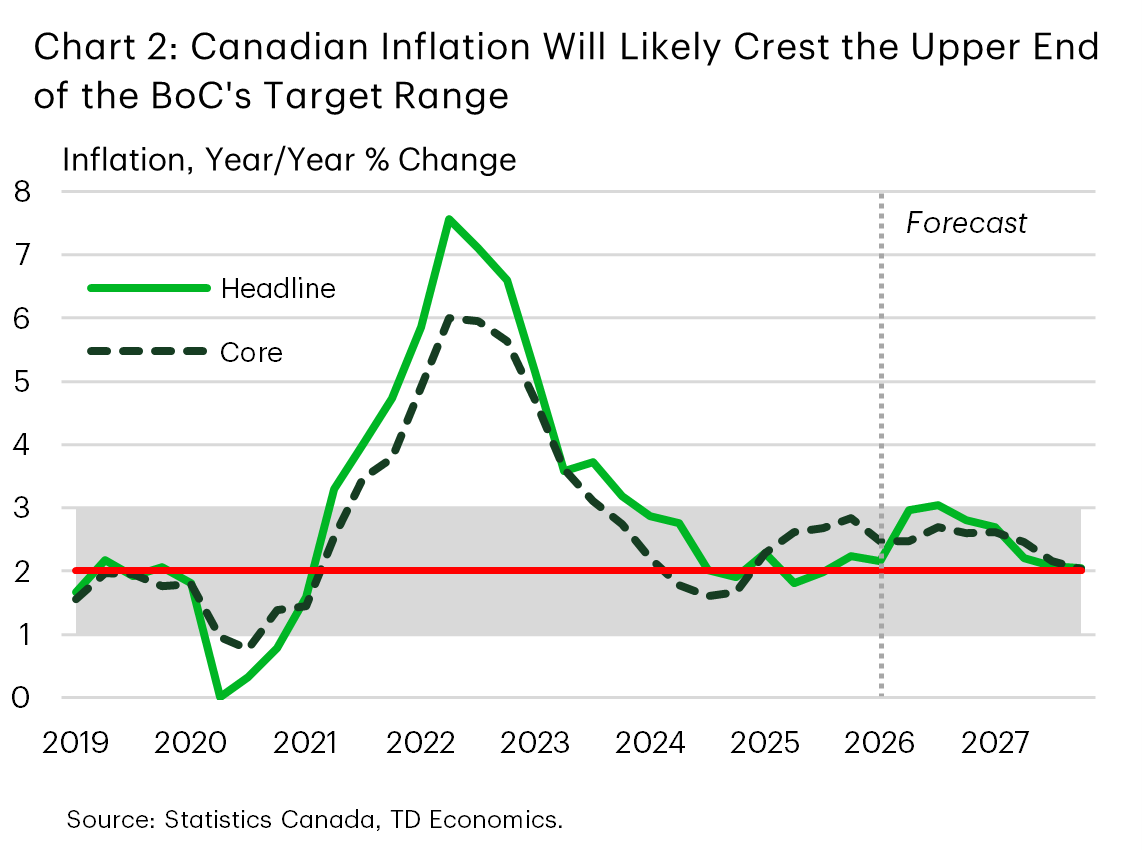

This week’s developments reinforce a familiar theme: an economy growing modestly but facing elevated uncertainty, and a central bank firmly in wait-and-see mode. Attention now turns to next week’s April inflation (CPI) release, where inflation is expected to move higher on energy base effects. We expect headline inflation to peak around 3% later this year before easing back toward target (Chart 2). The key question will be whether price pressures remain contained or begin to broaden more meaningfully into core components.

U.S. – Changing of the Guard

The changing of the guard at the Federal Reserve was formalized this week, as Kevin Warsh was confirmed by the Senate as Powell’s successor on Wednesday. This means Jerome Powell’s eight-year term as Chairman came to an end on Friday. Warsh takes the helm at a time when inflation pressures are rising sharply on the back of elevated global energy prices. Details on a potential resolution to the conflict in Iran remained elusive this week, which led to a 9% uptick in WTI oil prices. Equity markets were roughly unchanged on the week, with the S&P 500 rising 0.2%, as U.S. Treasury yields spiked by roughly 20 basis points, reflecting stronger inflation readings.

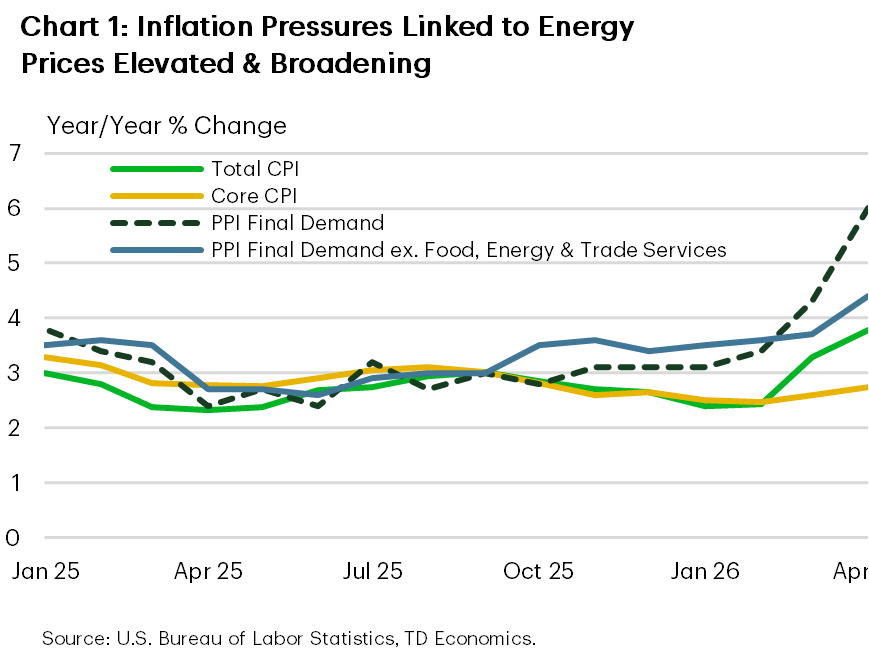

In terms of economic data releases, the inflation data for April was the biggest news item. Headline CPI hit a three-year high of 3.8% year-on-year (y/y), on the back of rising energy prices (Chart 1). Stripping out energy and food products, core CPI accelerated for a second consecutive month to 2.7% y/y, partly owing to the feedthrough of energy prices to categories like airline fares. Broad-based passthrough to non-energy categories was absent from the report, but with energy prices rising through early May, subsequent reports may be less benign, particularly if no resolution is reached over the near-term.

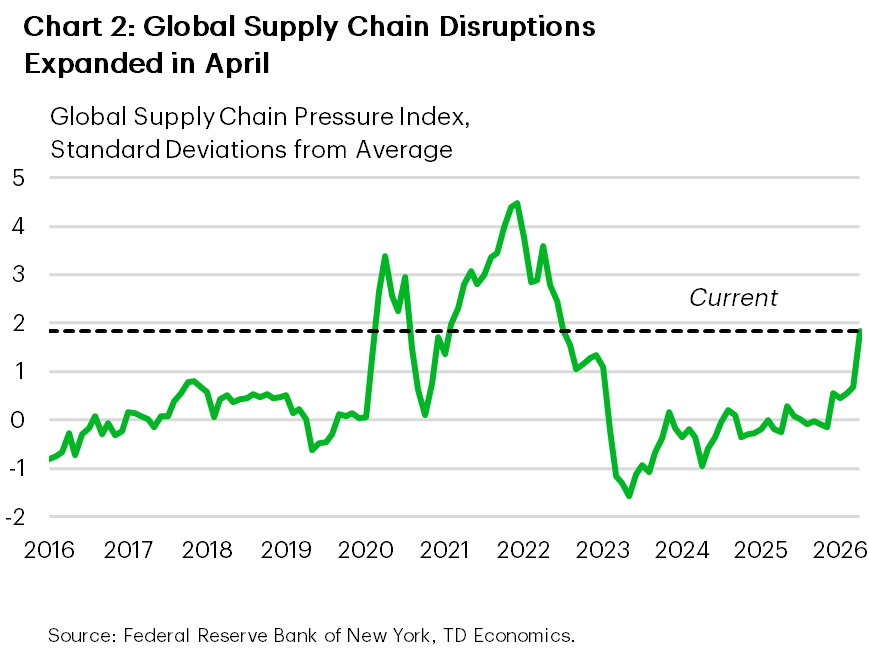

Upstream, the influence of higher energy prices was similarly evident for producers in April, with the Producer Price Index up 6% y/y. Selling price pressures have not been this elevated since late 2022, as global supply chain disruptions have begun to converge with those seen during the initial aftermath of the pandemic (Chart 2). The impacts of these developments on businesses, and the follow-through to consumers, will be monitored closely by the Federal Reserve.

To that end, the April retail sales report provided an early snapshot of consumer health. It showed a solid gain of 0.5% month-on-month in nominal terms, but after adjusting for inflation, sales fell 0.2%. This likely reflected, in part, the comparable contraction in real earnings during the month, which, if sustained, would continue to weigh on consumption going forward. A near-term resolution to the Iran conflict would help ease some of this pressure, although the effects would likely be gradual as supply disruptions take time to fully unwind. Taken together, these crosscurrents leave the near-term policy outlook highly dependent on incoming inflation data.

Against this backdrop, Fed officials in public remarks this week flagged concerns about the inflation reports. Several officials, including Chicago Fed President Goolsbee and Boston Fed President Collins, noted that tighter financial conditions may be required to quell emerging inflationary pressures. The balance of opinion among officials emphasized that a neutral stance would be appropriate over the near term to allow time to assess incoming data. As of the time of writing, financial market pricing for a rate hike by year-end has risen to 40%.

Economics Week Ahead

Next week’s release of the April FOMC minutes will shed light on how members of the committee saw the Fed’s next move as balanced between a hike and a cut. U.S. housing data, meanwhile, point to a moderating construction backdrop, as March’s rebound in starts likely overstated momentum amid a 2.6% year‑to‑date decline in permits and continued affordability pressures. In Canada, inflation remains elevated but mixed, with headline near 3.4% and softer core measures around 2.1–2.2%, keeping the Bank of Canada cautiously tilted toward further tightening. In the UK, easing labor market conditions—wage growth near 3.8% and declining vacancies—contrast with still‑firm inflation around 3.0%+, leaving policy finely balanced. In China, growth remains uneven but steady, with industrial production near 5.9% and retail sales around 1.9%, as strong manufacturing offsets softer domestic demand and points to a gradual cooling ahead.

United States:

- FOMC Minutes (Wednesday), Housing Starts (Thursday)

G10 Economies:

- Canada CPI (Monday), UK Labor Market Overview & CPI (Tuesday & Wednesday)

Emerging Markets:

- China Retail Sales & Industrial Production (Monday)

U.S. Week Ahead

FOMC Minutes • Wednesday

The minutes to the April 29 FOMC meeting will provide details on where the Committee stood just ahead of the leadership transition to Chair Warsh. Three voters dissented to the easing bias maintained in April’s post-meeting statement (even as they agreed with the decision to keep the fed funds rate unchanged), highlighting growing discomfort with signaling cuts as the default next move.

We will be looking at the minutes to see the extent to which non-voters shared the view that the Fed’s next move is equally likely to be a hike as a cut. Heading into the April meeting, policymakers had received more favorable employment data but were seeing renewed risks to inflation, a dynamic that has since intensified. This will make any discussion of the conditions that would warrant rate hikes more salient to the current policy outlook. At the same time, the departure of Governor Miran suggests the minutes may overstate the degree of dovish support on the Committee.

Even with a more hawkish tone likely to come through, we expect the minutes to indicate that most participants still favored holding rates steady for some time while they assess how the energy shock feeds through to inflation and the labor market.

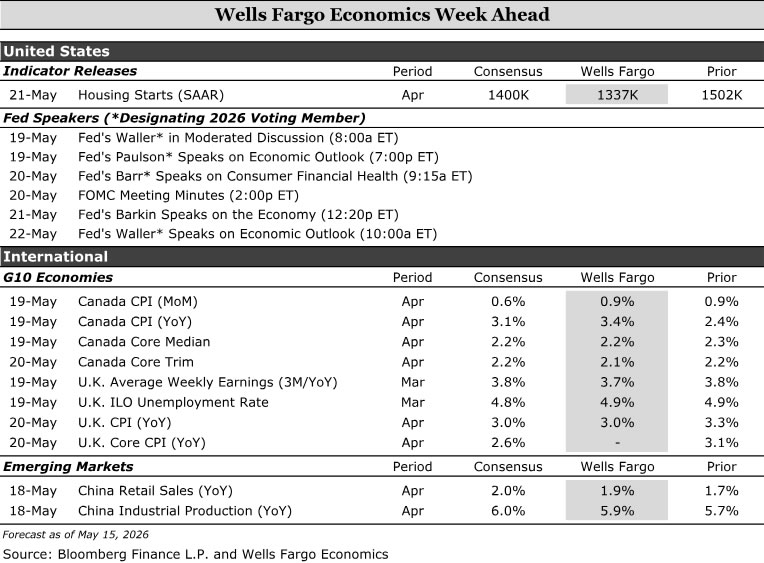

Housing Starts • Thursday

Residential construction appears to be downshifting. Total housing starts rose strongly during March, with gains registered across both the single-family and multifamily categories. Although the improvement is an encouraging sign activity is not contracting sharply, our sense is the monthly gain was mostly payback from February's weather-related slowdown and vastly overstated the underlying moderating trend in new construction.

So far this year, building permits have trended lower and were down 2.6% on a year-to-date basis in March. The slowdown has been most apparent within single-family, largely reflecting increased caution on the part of home builders stemming from ongoing buyer affordability challenges, soft new home sales, and elevated inventory levels. Multifamily permits have outperformed, which we attribute to firming apartment market conditions as well as a slightly lower cost of capital. Taking all of these factors into consideration, we expect housing starts declined to a 1,337K unit pace in April, lower than the current consensus estimate.

G10 Week Ahead

Canada CPI • Monday

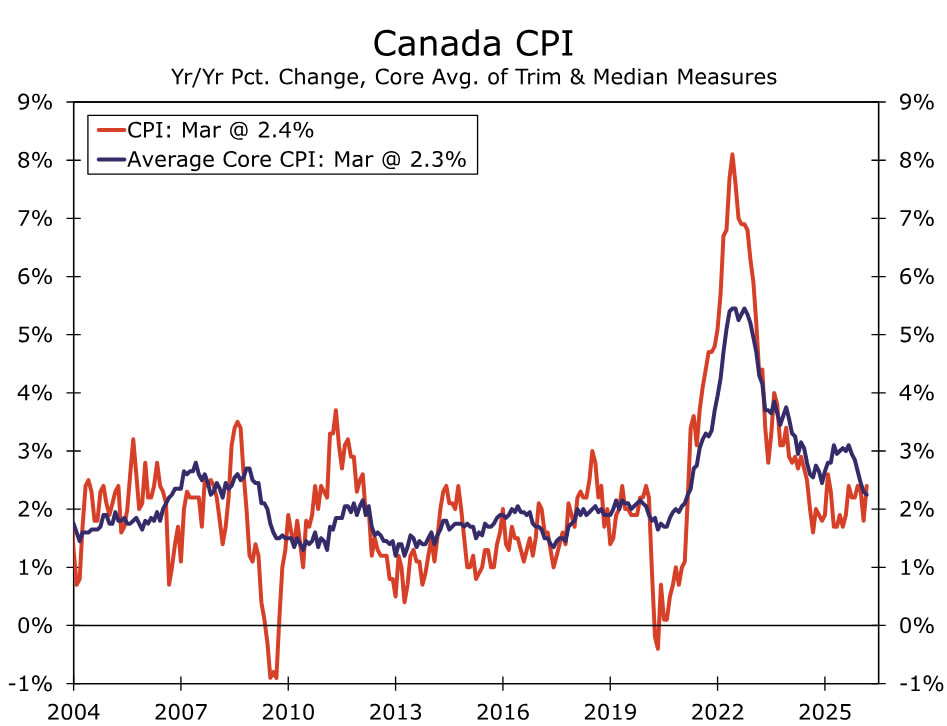

We expect headline inflation to rise another 0.9% month-over-month in April, following a similar print in March, lifting year-over-year inflation to 3.4%. Core measures, including trimmed mean and weighted median inflation, are likely to show a further month of softening, aided by favorable base effects. We look for both trimmed mean and weighted median inflation to ease to 2.1% and 2.2% year-over-year, respectively. That said, April is likely to mark an inflection point for core inflation, with signs of underlying price pressures beginning to broaden. With headline inflation running well above the upper end of the Bank of Canada’s target range and underlying inflation set to reaccelerate, we continue to expect the Bank of Canada (BoC) to hike rates at its July meeting. The policy rate remains at the bottom of its estimated neutral range, and we expect downside risks to the BoC's outlook to diminish as the July 1 USMCA deadline passes without new tariffs, leaving the parties locked into a prolonged annual review process.

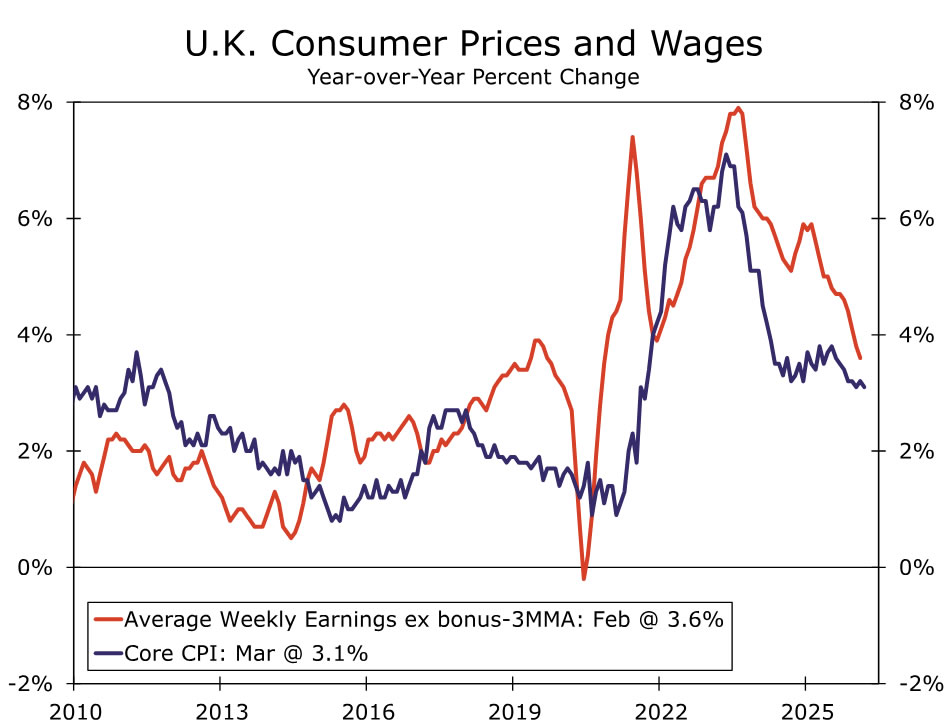

UK Labor Market Overview & CPI • Tuesday & Wednesday

U.K. labor and wage data on Tuesday and April CPI on Wednesday will give market participants a fresh read on wage dynamics and inflationary pressures as Bank of England (BoE) policymakers weigh the appropriate response to an energy-driven price shock against a fundamentally weaker labor market. For the three months to February, average weekly earnings growth eased to 3.8% year-over-year, marking the first sub-4% total pay reading since 2020. The broader labor market has continued to loosen gradually, with vacancies at 711K, the lowest since early 2021, and payrolled employees down 65K on the year in the March early estimate. Pay growth is expected to ease slightly further, though base effects and the recent National Living Wage uplift warrant attention.

Turning to prices, Wednesday’s release follows March’s upside surprise of 3.3% year-over-year, with services inflation at 4.5% and core at 3.1%. The BoE’s April Monetary Policy Report projects headline CPI to ease to 3.0% year-over-year, largely reflecting base effects. Any new upward pressure from energy showing up in the data would therefore require a closer look at the underlying components.

While 2026 public pay awards and the bulk of private sector wage settlements were largely completed before the energy shock and the labor market has visibly loosened, we still see risks to second-round effects skewed to the upside even if they do not show up via the wage channel this year. With energy and fertilizer prices still rising amid the ongoing conflict, the pass-through to core goods and food prices argues for a more pre-emptive stance, in our view. As such, and as noted in our May international outlook, we look for a 25 bps hike to 4.00% in July, with a further Q4 move to 4.25% contingent on Middle East developments.

`

`

EM Week Ahead

China Retail Sales & Industrial Production • Monday

Next week's retail sales and industrial production data for April will provide an early read on how China's economy fared at the beginning of the second quarter. China's economy got off to a solid start in 2026, outperforming expectations, although growth has been somewhat uneven. Strength has been largely driven by firmer manufacturing production, solid external trade performance and front-loaded fiscal stimulus, while domestic demand has remained relatively weak. To that point, March activity data showed some stabilization, with industrial production growth firming to 5.7% year-over-year and retail sales growth rising to 1.7%. However, China's April PMIs suggest conditions may have softened at the start of Q2, as export-backed manufacturing resilience contrasted with contractions in services and construction. As such, we expect both measures grew at a somewhat slower pace in April and look for year-over-year industrial production growth of 5.9% and retail sales growth of 1.9%.

Looking at the bigger picture, we expect recent strength in China's economy to gradually abate in the second half of 2026. The boost from fiscal stimulus should fade over time, while higher energy prices and tighter energy supply could become more meaningful headwinds. Accordingly, we look for China's annual GDP growth to ease to 4.5% in 2026, before slowing further to 4.3% in 2027.