Sample Category Title

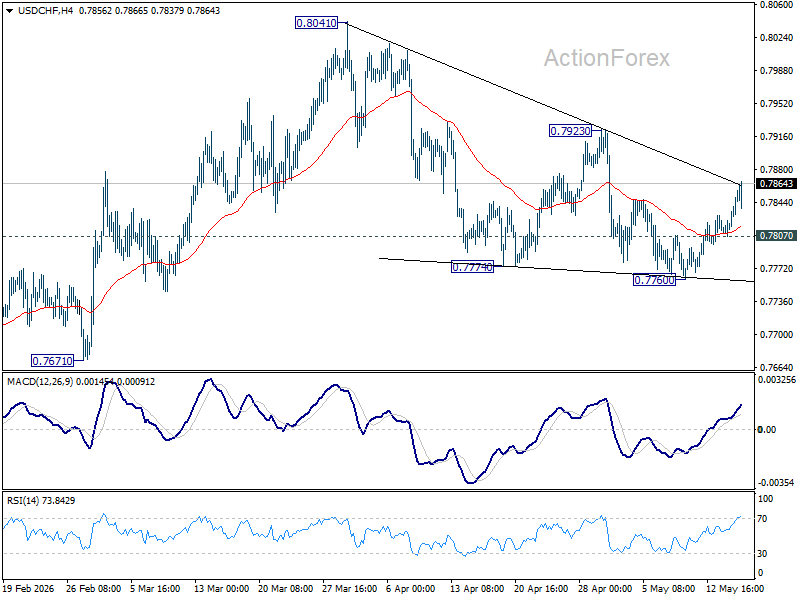

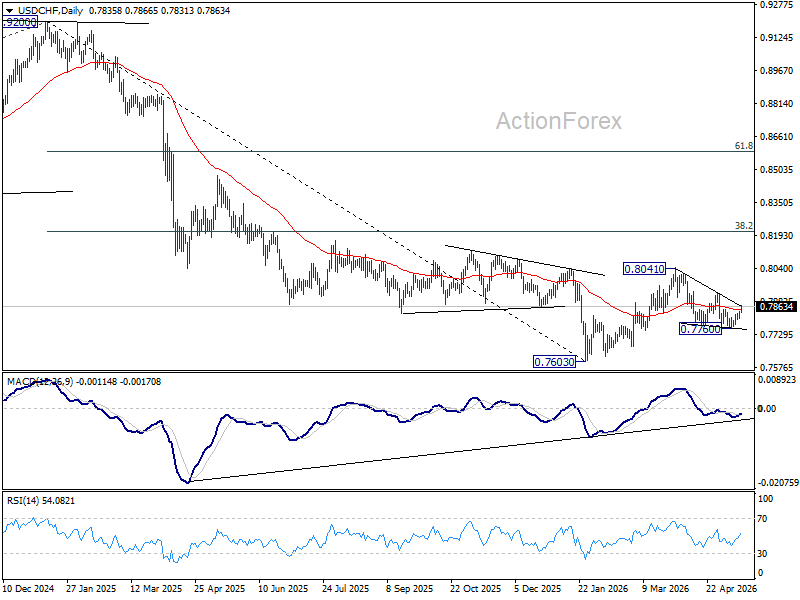

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7813; (P) 0.7826; (R1) 0.7846; More….

Intraday bias in USD/CHF remains on the upside as rebound from 0.7760 continues. Break of 0.7923 resistance will argue that fall from 0.8041 has completed as a three wave correction, and bring further rise to retest this high. On the downside, below 0.7807 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 55 W EMA (now at 0.8051) holds, fall from 0.9200 is expected to continue, as part of the larger down trend. Firm break of 0.7603 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.

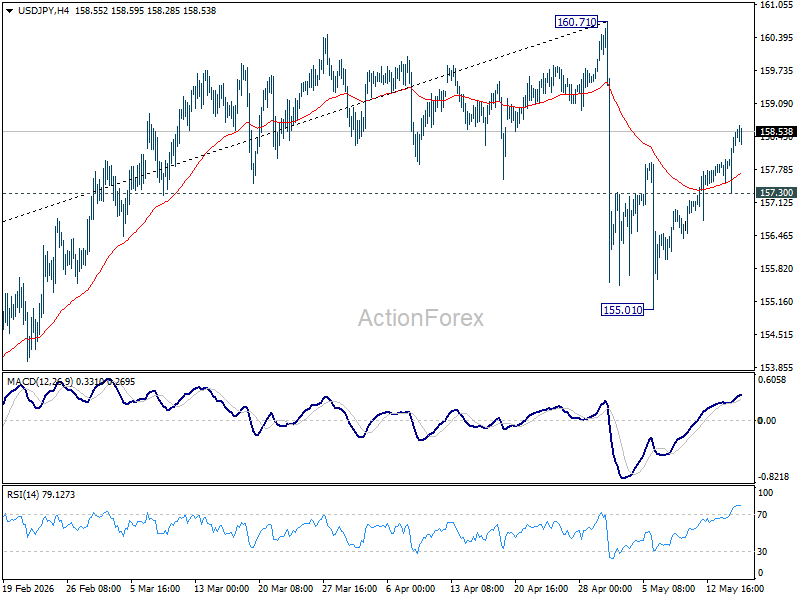

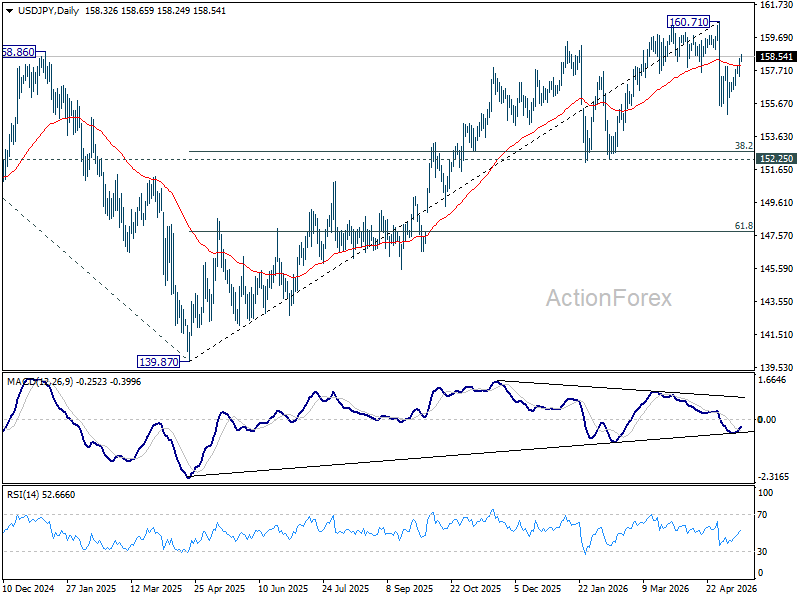

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.62; (P) 158.01; (R1) 158.74; More...

Intraday bias in USD/JPY remains on the upside as rise from 155.01 is in progress. As this rebound is seen as the second leg of the corrective pattern from 160.71, strong resistance should emerge from there to limit upside. On the downside, break of 157.30 minor support will argue that the third leg could have started, and target 155.01 support instead.

In the bigger picture, for now, corrective pattern from 161.94 (2024 high) is still seen as completed at 139.87. Rise from there is seen as resuming the long term up trend. So, break of 161.94 is expected at a later stage to resume the long term up trend. However, sustained break of 55 W EMA (now at 154.13) will dampen this view and bring deeper fall back towards 139.87 to extend the pattern from 161.94.

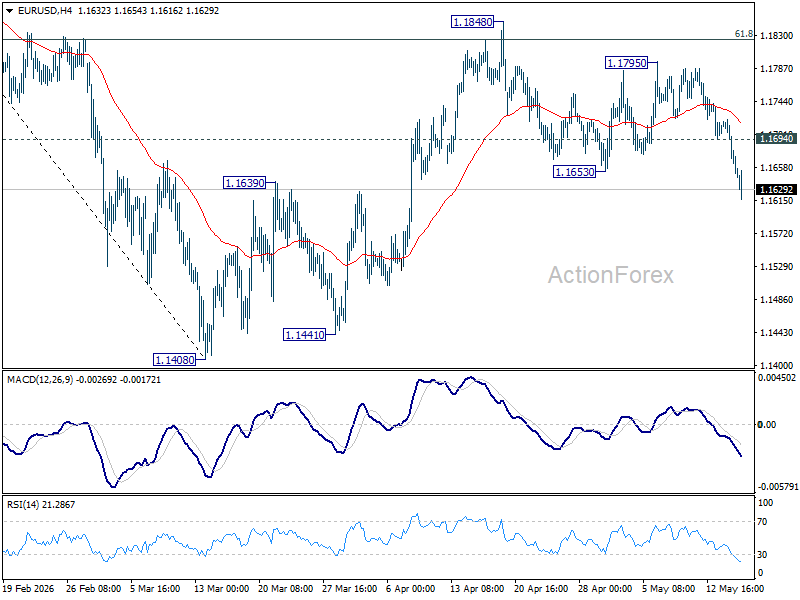

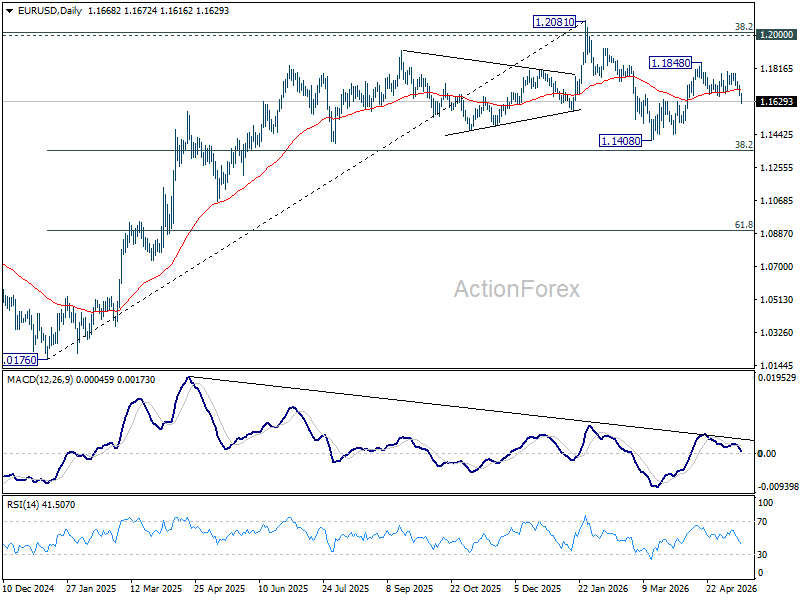

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1647; (P) 1.1684; (R1) 1.1703; More….

EUR/USD's decline continues today and the break of 1.1639 resistance turned support suggests that rebound from 1.1408 has completed as a corrective three-wave move at 1.1848. Intraday bias remains on the downside for retesting 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1694 resistance will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Dollar Surges as Markets Price Longer Hormuz Crisis and Persistent Inflation

Risk sentiment deteriorated sharply today as investors concluded that the Trump-Xi summit failed to deliver a credible diplomatic breakthrough on the Strait of Hormuz, forcing markets to begin pricing a longer-lasting inflation shock tied to prolonged energy disruption. Global equities and precious metals are sold off together as rising oil prices and higher Treasury yields tightened global financial conditions. Dollar surged broadly in response, supported simultaneously by rising US yields, inflation fears, and defensive risk positioning.

China’s Foreign Ministry stated on Friday that shipping routes “should be reopened as soon as possible” and called for a “comprehensive and lasting” ceasefire. However, Beijing provided no operational details regarding how such reopening would be achieved, nor any indication that China would actively pressure Tehran into ending disruption risks in the Strait.

At the same time, the core strategic issue surrounding Iran’s uranium enrichment program remains unresolved. While US President Donald Trump said that: “We don't want them to have a nuclear weapon,” neither side provided clarity regarding enrichment limits, inspections, or broader nuclear conditions. For markets, the central issue increasingly remains a “black box.”

Instead of signaling de-escalation, investors interpreted Trump’s comments regarding expanded Chinese purchases of US crude as evidence that Washington may be preparing for a prolonged disruption rather than expecting rapid normalization. Trump said after the summit: “China is going to buy oil from the US.” That statement appears to have shifted market thinking away from a “Hormuz reopening” scenario toward a “supply rerouting” scenario.

Markets had previously hoped Beijing would use its leverage as the largest buyer of Iranian oil to pressure Tehran toward reopening shipping routes. Instead, the summit outcome increasingly suggests that global energy trade may simply adapt around continuing disruption, leaving the geopolitical risk premium firmly embedded in oil markets.

That interpretation was reinforced further by comments from Iranian Foreign Minister Abbas Araqchi, who said Tehran has “no trust” in the U.S. and remains skeptical about Washington’s intentions. “Contradictory messages” from the Trump administration have complicated negotiations, Araqchi said, while describing Pakistan’s mediation efforts as being in “difficulty” rather than failed outright.

His comments directly highlighted the contradiction between Washington’s simultaneous military pressure campaign and diplomatic messaging. The remarks suggest any meaningful diplomatic off-ramp remains distant after the conclusion of the Trump-Xi summit.

Markets also reacted to reports that the United Arab Emirates will accelerate expansion of a major oil pipeline through Fujairah by 2027, significantly increasing export capacity that bypasses the Strait of Hormuz altogether. That development carries important symbolic significance. Regional producers themselves appear to be preparing for a world where Hormuz instability persists far longer than initially expected.

In currency markets, Dollar remained the strongest performer of the week by a clear margin, followed by Yen and Euro. Kiwi was the weakest currency, followed by Aussie and Swiss Franc. Sterling and Loonie traded in the middle.

In Europe, at the time of writing, FTSE is down -1.67%. DAX is down -1.75%. CAC is down -1.53%. UK 10-year yield is up 0.181 at 5.175. Germany 10-year yield is up 0.088 at 3.131. Earlier in Asia, Nikkei fell -1.99%. Hong Kong HSI fell -1.62%. China Shanghai SSE fell -1.02%. Singapore Strait Times fell -0.14%. Japan 10-year JGB yield rose 0.07 to 2.705.

Oil Surges Toward $110 as Trump-Xi Summit Signals Supply Rerouting, Not Hormuz Resolution

Oil markets rallied after traders concluded the Trump-Xi summit failed to resolve the Hormuz crisis and instead pointed toward a long-term rerouting of global energy flows. Read More.

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY climbed back toward the critical 160 level as surging US Treasury yields widened the US-Japan rate gap and intensified doubts over whether Japanese intervention can still effectively stabilize the Yen. Read More.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April as higher oil prices, chemical costs, and a weak Yen intensified imported inflation pressures, reinforcing expectations for further BoJ tightening. Read More.

New Zealand PMI Falls to 50.5 as New Orders Turn Negative

New Zealand’s manufacturing sector lost significant momentum in April as new orders fell into contraction territory and firms reported rising freight, fuel, and supply-chain pressures linked to the Iran war. Read More.

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY climbed back toward the critical 160 level as surging US Treasury yields widened the US-Japan rate gap and intensified doubts over whether Japanese intervention can still effectively stabilize the Yen. Read More.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April as higher oil prices, chemical costs, and a weak Yen intensified imported inflation pressures, reinforcing expectations for further BoJ tightening. Read More.

New Zealand PMI Falls to 50.5 as New Orders Turn Negative

New Zealand’s manufacturing sector lost significant momentum in April as new orders fell into contraction territory and firms reported rising freight, fuel, and supply-chain pressures linked to the Iran war. Read More.

Fed’s Williams Sees No Need for Rate Changes Right Now

Fed’s John Williams said policymakers see no urgent need to change interest rates despite rising inflation pressures tied to the Middle East conflict, emphasizing that longer-term inflation expectations remain stable for now. Read More.

Fed’s Barr Says Shrinking Balance Sheet Should Not Trump Financial Stability

Fed Governor Michael Barr warned that proposals to shrink the Fed’s balance sheet by weakening bank liquidity requirements could make the financial system more fragile rather than safer. His remarks highlighted growing debate inside the Fed ahead of the Kevin Warsh era. Read More.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1647; (P) 1.1684; (R1) 1.1703; More….

EUR/USD's decline continues today and the break of 1.1639 resistance turned support suggests that rebound from 1.1408 has completed as a corrective three-wave move at 1.1848. Intraday bias remains on the downside for retesting 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1694 resistance will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

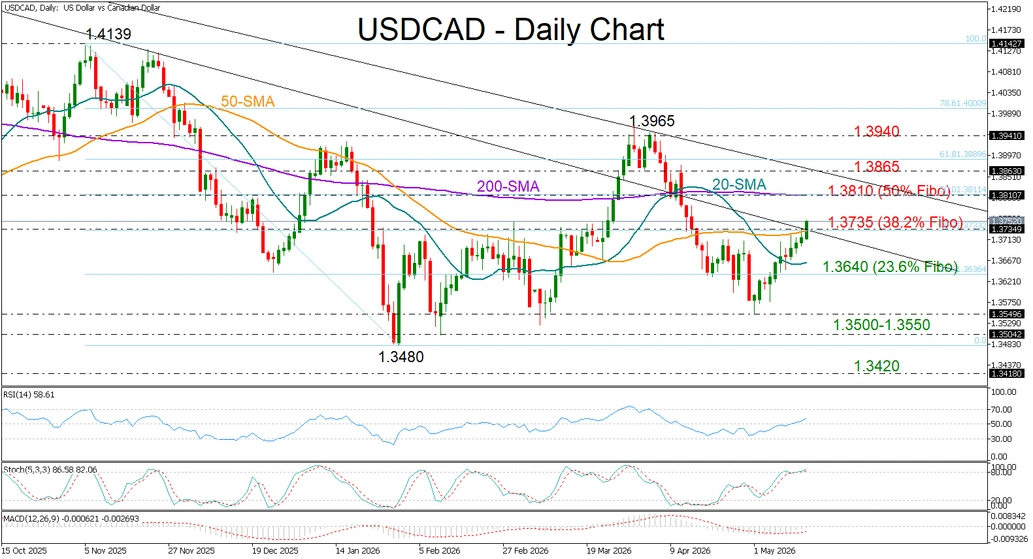

USD/CAD Turns Higher for Second Week, Tests 50-SMA

- USDCAD rises above 1.3700 as gains extend for second consecutive week.

- Technical bias remains positive, but caution emerges near 50-SMA.

USDCAD has traded mostly in positive territory since the beginning of May. After stabilizing around the 1.3500 region for the third time this year, the pair is now attempting to close above its 50-day simple moving average (SMA) near 1.3735. The move follows President Trump’s comments expressing limited patience over Iran-related tensions, while two-day talks with China conclude.

Both the RSI and the MACD suggest improving buying momentum. However, the stochastic oscillator, which is hovering in overbought territory, signals caution as the pair tests the 38.2% Fibonacci retracement of the November–February decline near 1.3735. A decisive break above this level could pave the way toward the 200-day SMA and the 50.0% Fibonacci retracement at 1.3810. Slightly higher, a critical battle could emerge around the descending trendline connecting the 2025 and 2026 highs near 1.3860.

If the pair fails to maintain momentum above the 50-day SMA, it could retreat toward the 23.6% Fibonacci level at 1.3640. A deeper pullback may then retest the 1.3500-1.3550 zone, a break of which could reinforce the broader bearish outlook and expose the 2024 support level at 1.3420.

Overall, USDCAD remains in a bullish short-term mode, with further gains likely if buyers manage to clear the 1.3735 resistance area decisively. Nevertheless, the broader outlook remains bearish as long as the pair stays below 1.3860.

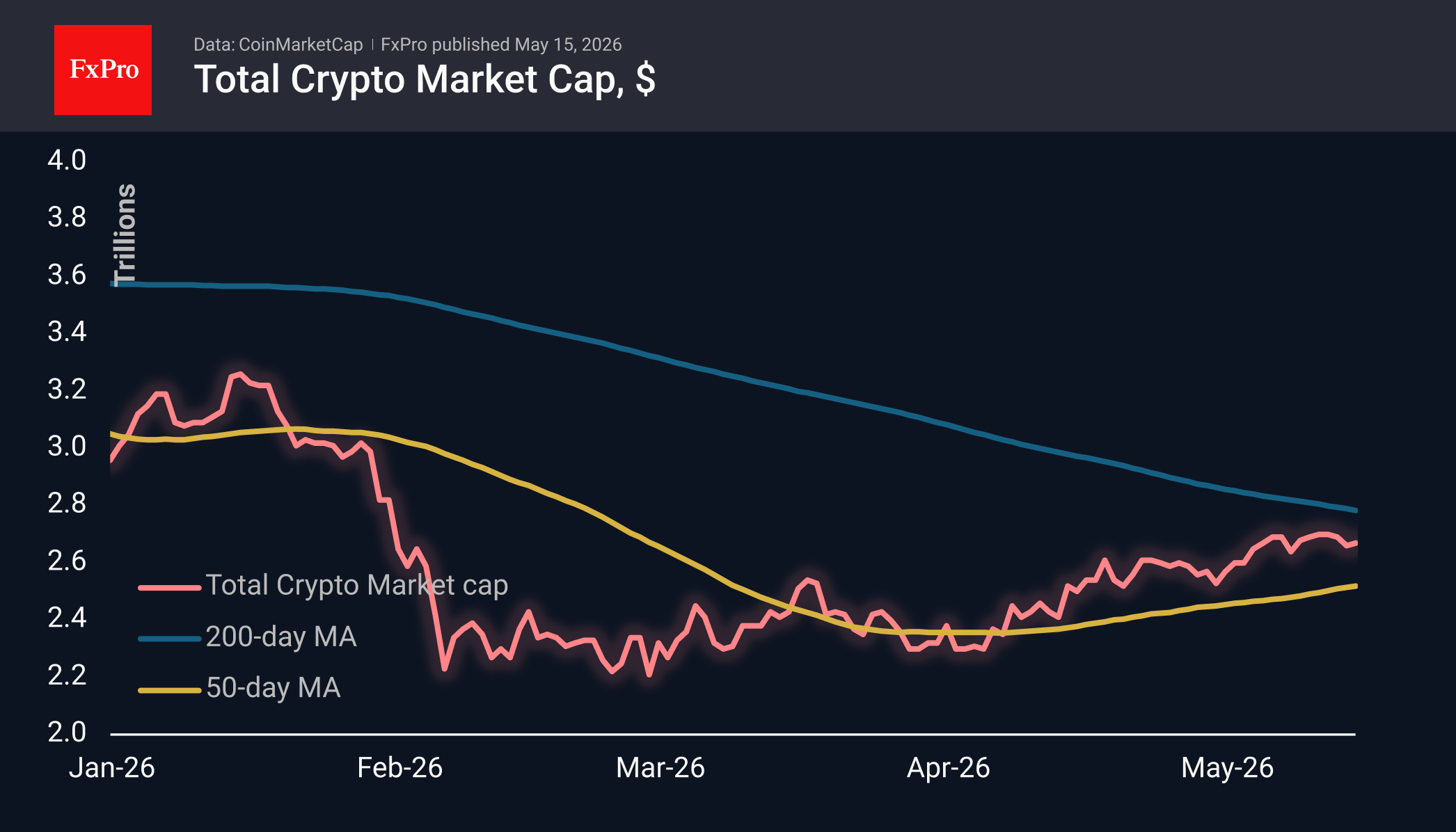

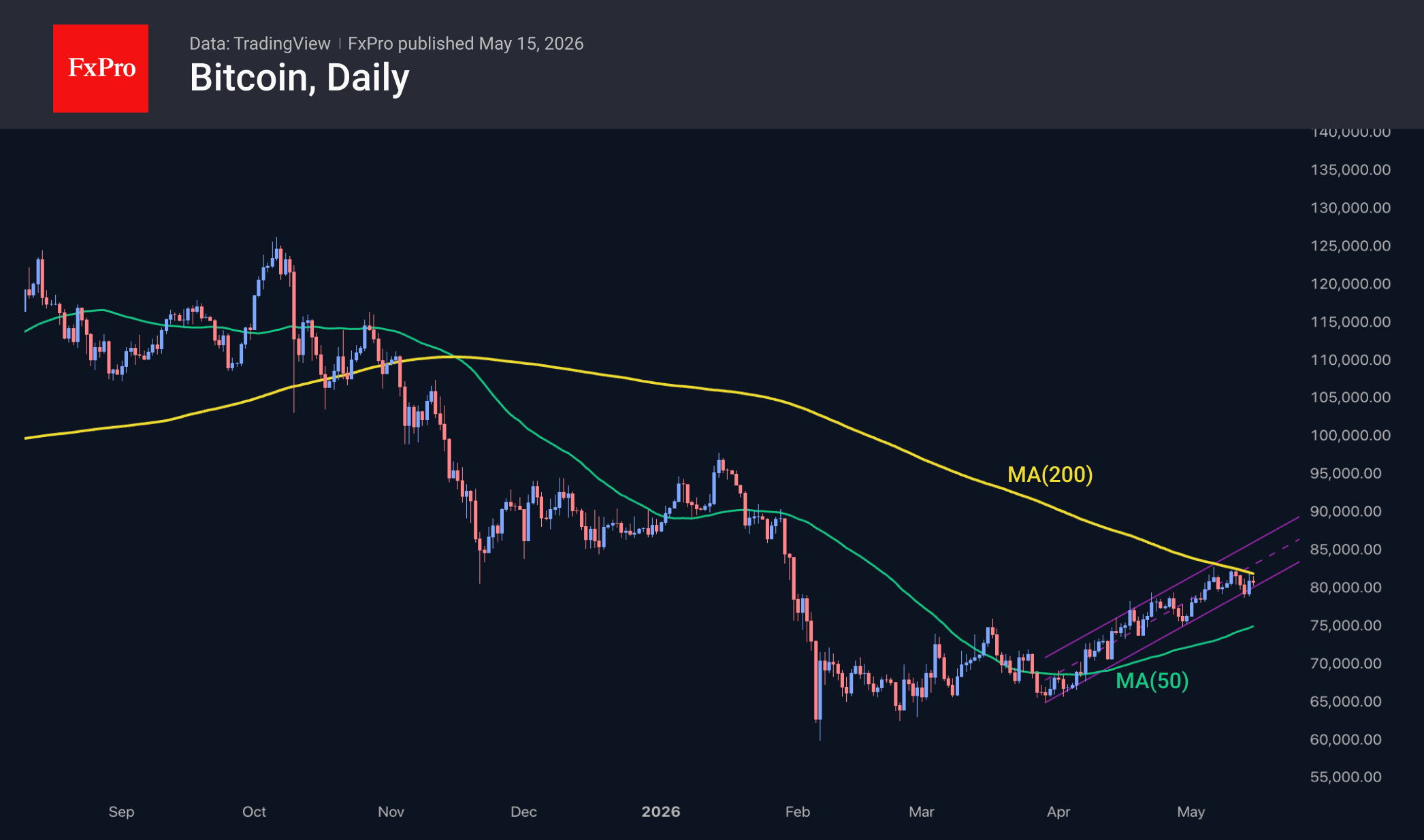

Sellers are Pressing Down on Crypto

Market Overview

The crypto market is trading within a narrow range, having bounced off its upper boundary at $2.73T and retreated to $2.67T at the time of writing. New records on the US stock market have spurred crypto buyers into action, but this has proved insufficient to break through key resistance levels. We attribute this weak performance to the strengthening of the dollar, as evidenced by gold’s dynamics. Over the past 24 hours, the top performers among the most liquid coins have been Dash (+4%), Zcash (+3.8%) and Uniswap (+3.1%), while fewer coins are losing ground, with the most significant losses seen in Internet Computer (-8%), Aptos (-1.1%) and Official Trump (-0.8%).

Riding a wave of optimism in equities, Bitcoin rose once again towards $82K, hitting the 200-day moving average once more. This is usually a signal line, but in May, it is acting as an impenetrable resistance level, capping the price from above. As a result, early on Friday, the price once again found itself just above $80K. The prevailing cautious sentiment in equities early on Friday is intensifying the outflow from cryptocurrencies, setting the stage for a decline towards the lower end of the range at $79K by the end of this week.

News Background

Institutional players are using the recent recovery to take profits, and this is not driven by fear or panic, according to Glassnode. CryptoQuant considers the risk of a further decline in Bitcoin to be real against this backdrop.

Activity among companies buying crypto assets for their reserves has also declined. According to Bitfinex, the volume of Bitcoin purchases by large companies has fallen by 80% over the week.

The volume of Ethereum in staking has exceeded 85 million coins — this is more than 70% of the cryptocurrency’s total supply, SharpLink has calculated. ETH reserves on exchanges also continue to decline, which may exacerbate the asset’s shortage.

The altcoin market has shown the first signs of recovery following a 50% drop from previous highs, notes analyst Darkfost. At the same time, liquidity remains limited, which is hindering the start of a sustained alt season.

Kevin Warsh, confirmed this week as the new Fed chair, has described Bitcoin as an “important asset” that helps authorities assess the state of the economy. He has invested in several crypto projects and holds Solana and Optimism tokens.

Following several months of discussions due to disagreements between banks and crypto companies, the US Senate Banking Committee on Thursday approved the CLARITY Act, a bill on the structure of the cryptocurrency market. The bill will now be put before the full Senate for consideration. Bankers fear that the yield on stablecoins stipulated in the bill will lead to an outflow of funds from bank deposits.

Gold Falls on US Inflation Concerns as Week Ends in Losses

Gold continued its decline on Friday, falling to 4,619 USD per ounce. The week is set to close with losses of around 1%, as mounting US inflation puts pressure on the market. Rising prices reinforce expectations that the Federal Reserve may maintain elevated rates for longer or even resume rate hikes.

Data released this week showed that US manufacturing inflation rose at its fastest pace since 2022 in April, while consumer prices recorded the most significant increase since 2023.

The primary driver of inflationary pressure remains the ongoing conflict in the Middle East and disruptions to supplies through the Strait of Hormuz, which continue to influence global energy markets.

In this context, the market has largely ruled out a Fed rate cut for 2026. Some investors are even pricing in the possibility of a further rate hike by December.

Investor attention was also drawn to the meeting between US President Donald Trump and Chinese President Xi Jinping, during which ensuring open navigation through the Strait of Hormuz to support global energy trade was a key topic.

Separately, the market is keeping an eye on India, where authorities have further tightened regulations on gold imports as part of measures to support the rupee.

Technical Analysis

On the H4 XAU/USD chart, gold has broken below 4,639 USD and is moving lower towards 4,550 USD. A corrective rebound to 4,630 USD (testing from below) is possible, followed by a further decline towards 4,500 USD. The MACD indicator confirms the current bearish momentum, with its signal line below the centre line and pointing firmly downwards.

On the H1 chart, gold has broken below the 4,639 USD level and continues to move lower towards 4,555 USD. A rebound towards 4,639 USD may follow before a further decline towards 4,550 USD. The Stochastic oscillator supports this scenario, with its signal line below 20 and pointing firmly downwards, indicating continued downside pressure.

Conclusion

Gold remains under pressure as US inflation data strengthens the case for sustained or higher interest rates. Short-term technical indicators suggest further downside potential, although temporary corrections may occur. Geopolitical developments and policy decisions in major economies will continue to dictate market sentiment.

Oil Surges Toward $110 as Trump-Xi Summit Signals Supply Rerouting, Not Hormuz Resolution

The Trump-Xi summit was supposed to calm oil markets. Instead, it may have convinced traders that the global energy system is adapting to a prolonged Hormuz disruption rather than preparing for its resolution.

Brent crude surged toward $110 today after traders reassessed the implications of comments made by US President Donald Trump following his two-day meeting with Chinese President Xi Jinping in Beijing. Rather than signaling coordinated pressure on Iran to fully reopen the Strait of Hormuz, Trump emphasized plans for significantly expanded Chinese purchases of American oil exports.

“They’ve agreed they want to buy oil from the United States,” Trump said in an interview with Fox News. “We’re going to start sending Chinese ships to Texas and to Louisiana and to Alaska.”

That message appears to have fundamentally altered market psychology.

Before the summit, many investors had hoped Beijing would use its leverage as the largest buyer of Iranian oil to pressure Tehran into ending shipping disruptions and reducing tensions in the Gulf. A credible Hormuz reopening would likely have triggered a sharp collapse in crude prices by removing much of the war premium embedded in energy markets.

But instead of hearing a pathway toward reopening the Strait, markets increasingly heard something very different: a rerouting of global supply chains around a continuing disruption.

That distinction matters enormously.

If China increasingly replaces Iranian barrels with American energy supplies, Beijing may have less strategic incentive to defend Iranian export infrastructure or oppose more aggressive US actions against Tehran. Some traders interpret the summit outcome as raising — not lowering — the probability of future military escalation.

As a result, oil markets are beginning to shift toward pricing a more structural fragmentation of global energy trade flows. The summit did not solve the war. It may simply have reorganized the winners and losers. That helps explain why oil prices are accelerating higher rather than retreating despite two days of high-level diplomacy.

Technically, as Brent crude's rise from 96.03 resumed through 108.45 resistance today, the key focus is on 61.8% projection of 96.03 to 108.45 from 103.88 at 111.56. Firm break there could prompt upside acceleration to 100% projection at 116.30.

More importantly, any upward acceleration through 115.30 resistance the first indication that whole converging triangle pattern from 119.50 high made in March has completed. That could set up long term up trend resumption through the key 120 psychological barrier.

GBP/USD: Sterling Under Pressure Despite Strong GDP Data

Fundamental Background

UK GDP grew by 0.6% in the first quarter of 2026, notably above the revised 0.2% reading recorded in the fourth quarter of 2025. The main contribution came from the services sector, which expanded by 0.8%. Nevertheless, strong macroeconomic data failed to support sterling: CPI inflation accelerated to 3.3% year-on-year in March, up from 3.0% in February, mainly due to higher motor fuel prices linked to the Middle East conflict.

At its meeting on 30 April, the Bank of England kept the base rate unchanged at 3.75% in an 8–1 vote, while several MPC members signalled the possibility of further tightening should inflationary pressure persist. According to the International Monetary Fund, UK GDP growth in 2026 is expected to reach only 0.8%, representing the largest downgrade among G7 economies.

Technical Picture

From 6 April to 1 May, GBP/USD developed an upward trend supported by a rising trendline. As the pair approached the peak, price action became increasingly compressed, forming a reversal structure with a dense profile concentration in the 1.3480–1.3580 range amid growing selling pressure. After breaking below the trendline and moving outside the profile range, the pair accelerated lower.

GBP/USD is now trading below the horizontal volume zone, signalling continued seller dominance. The lower boundary of the profile, followed by the POC area at 1.3515–1.3520, serves as the nearest reference zone for buyers. If the pair regains the upper boundary of the profile at 1.3580, the next resistance level stands at 1.3650 near the trend highs.

Support around 1.3380 corresponds to the price extremes that preceded the April rally and acts as an important structural support area, which the pair has nearly reached. This limits the room for further downside within the current move.

The RSI + MAs indicator shows readings of 26, 38 and 43. The moving averages remain pointed lower, reflecting ongoing pressure. However, the RSI has already entered oversold territory, which should be taken into account.

Key Takeaways

Strong first-quarter GDP data has not eased concerns over inflation and monetary policy uncertainty, and this fundamental conflict is likely to determine the pair’s future direction. From a technical perspective, the main RSI + MAs reading has entered oversold territory, although there are still no clear signs of a reversal.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

How Long Can AI Ignore Yields?

This week’s summit between Donald Trump and Xi Jinping went pretty well. Except for a few sticky points around Taiwan. The two leaders complemented each other. Trump was soft and conciliatory, while Xi Jinping struck a firmer tone, invoking the “Thucydides Trap” — the idea drawn from the rivalry between ancient Athens and Sparta that war can become inevitable when a rising power challenges a dominant one. Yet, the two countries agreed to ease trade tensions – mostly on non-critical sectors. China even agreed to help with the Iran negotiations.

Markets rallied, ignoring the ongoing Middle East tensions and their impact on prices and inflation figures. Because yes, inflation data released throughout this week confirmed rising price pressures in the Eurozone, and warned that inflation at both the consumer and producer levels was accelerating faster than expected in the US. The latest US PPI data jumped to 6% – the highest in more than three years – as energy prices spiked, while the Japanese PPI print this morning echoed a similar rise: it came in at an eye-watering 5%, the highest since mid-2023.

Rising inflation kept pushing bond yields higher, reflecting continued hawkish pricing across global central bank expectations. The US 2-year yield spiked past 4%, while the Japanese 10-year yield rose nearly 3.80% this morning to around 2.75% – far above the 1.75% level pointed to as the threshold where Japanese institutional investors (life insurers, pension funds, banks) could start seriously preferring domestic bonds over hedged foreign debt, remember.

US crude is pushing higher, above the $102pb level this morning, as traders swing between conflicting announcements from Trump, first saying that the US could live without the Strait of Hormuz, before urging its reopening a few hours later. US oil inventories fell by 4.3 million barrels last week, and by around 12 million barrels over the past three weeks, as US crude exports rose to help fill the Middle East supply gap. Energy prices will likely remain elevated given the little progress made in Middle East talks in the short run.

Many consumer-facing companies have been insisting that US consumers are running out of money. The retail sales data yesterday hinted at resilience in April, but underneath the surface, 13.1% of US credit card balances are now 90+ days delinquent — the highest level since 2011. It means that Americans borrow to spend, and delay their credit repayments. That’s a ticking bomb.

But guess what? The S&P500 and Nasdaq both hit record highs yesterday. No Matter What.

And indeed, Big Tech has done amazingly well since the beginning of the Iran war, somewhat shrugging off rising energy costs and supply disruption risks. It’s not that these companies aren’t paying for energy, but the AI growth outlook – and optimism that it will accelerate revenue generation – is outweighing the geopolitical challenges.

Roundhill’s Mag7 ETF rebounded nearly 30% since the war dip, hitting a fresh ATH yesterday, supported by strong earnings and even stronger guidance. Cerebras Systems, an AI chip company that went public yesterday, surfed on a giant wave, jumping around 70% on its first day as a publicly traded company and giving it a market cap of around $95bn – the biggest IPO of the year so far.

Investors totally brushed aside the circular deal worries, and their frustration with the massive AI spending increasingly financed by debt. No one cares about rising yields, either. And that’s curious.

Yes, tech stocks performed very well during the latest Fed tightening cycle post-2022, aimed at fighting the post-Covid and Ukraine war-led energy crisis. One of the reasons was that Big Tech companies had ample free cash flow and relatively lower debt, which made them less sensitive to interest rate hikes, defying the theory that growth stocks should be hit harder by higher rates as their valuations depend heavily on future revenues that become less valuable when discounted at higher interest rates.

Today, investors treat tech stocks the same way: thinking they could defy the Iran war, rising energy prices, rising inflation expectations and the prospect of tighter-than-otherwise monetary policy.

The problem is this: massive capital expenditure is eating into their free cash flow and obliging them to seek funding through... bond markets. Huh. It makes Big Tech companies more vulnerable to interest rates compared to earlier cycles.

Take Amazon’s 1.5% coupon bond due June 2030. It now yields around 4.40%; it covers US inflation and still offers a certain premium, but the price is falling as inflation expectations push US yields higher. That means the cost of borrowing is rising for these tech companies that are – together – expected to spend up to $1 trillion in AI infrastructure this year.

That’s the cost side.

And what happens if they back down? What happens if they decide to reduce spending?

It could be worse. Because current valuations are fueled by the prospect of future AI-led revenue. But if companies stop investing, they could hit capacity constraints that limit income potential – a scenario that is not favourable for valuations.

Second, the circular nature of these deals suggests that if one company backs down, it could trigger a domino effect across the rest of the companies in the same circle...

Big Tech today stands at an important crossroads. Investors have digested the massive AI spending, the circular deals and the high valuations, yet for the rally to extend further, the macroeconomic backdrop also needs to remain supportive.

And today, looking at global yields, the macro backdrop is not supportive.

The longer the Middle East war drags on, the higher energy prices rise – fuelling inflation expectations and borrowing costs, and increasing the cost of building that extra data centre.

This, I believe, is a red flag that many tech investors have been ignoring, blinded by shiny earnings and even shinier earnings expectations.

But keep in mind that these expectations do not fully reflect the risk of another period of sticky inflation. And this time, Big Tech has less cash in hand to weather the stormy seas.

Alas, there is one more possibility — the one being priced in today — that the war will end, inflation and yields will come down, and markets will further rally on relief.