Sample Category Title

EUR/USD Finds Footing at One‑Month Lows Near 1.160

- EUR/USD halts losses near April highs.

- Key test: break above SMA cluster overhead.

- Momentum signals show easing selling pressure.

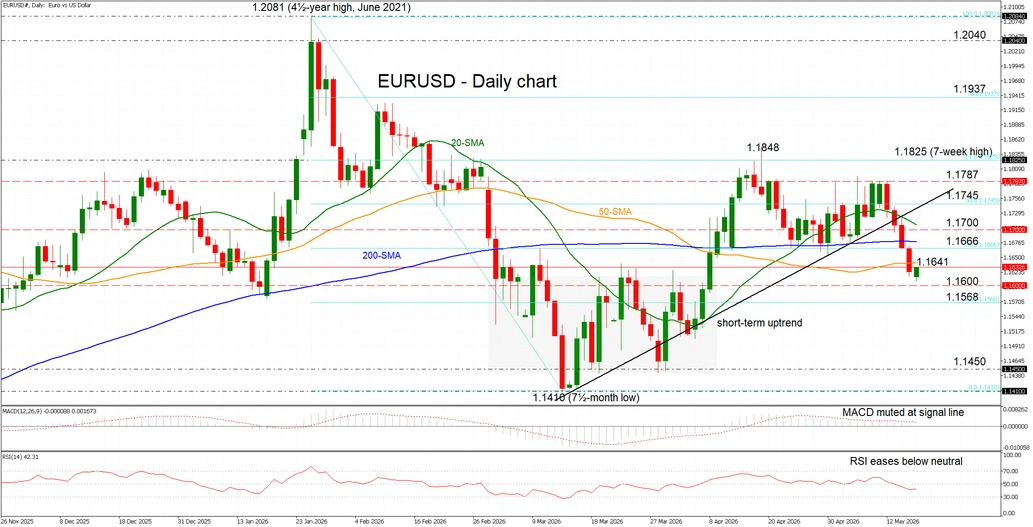

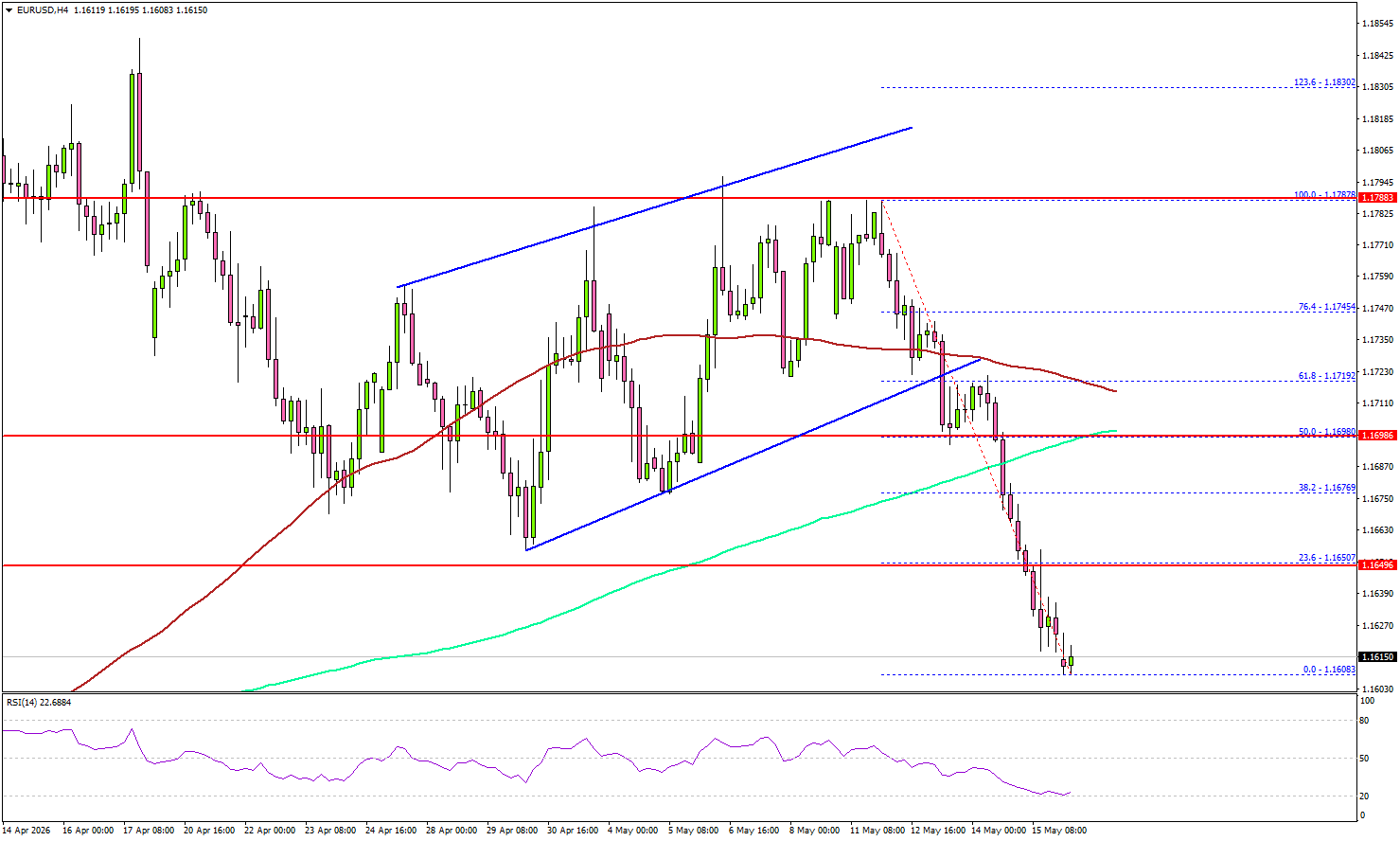

EUR/USD is attempting to stabilise after a four‑session pullback from the 1.1787 area to one‑month lows just above 1.1600, with the euro remaining under pressure against a firmer dollar amid renewed Middle East tensions and risk‑averse conditions.

Momentum indicators point to a pause in selling pressure, with the RSI flattening below neutral and the MACD stabilising around its zero and signal lines.

That said, the pair remains vulnerable after slipping below key levels, including the simple moving average (SMA) cluster and short‑term uptrend.

Resistance starts near the 50‑day SMA at 1.1641 and extends into the 1.1666-1.1745 zone, marked by the 38.2% and 50% Fibonacci retracements of the January-March decline and reinforced by the 20‑ and 200‑day SMAs. A break above this region could reopen the path toward 1.1787.

Support lies at the 1.1600 psychological level, followed by the 23.6% Fibonacci near 1.1568, before deeper losses toward multi‑month lows near 1.1410-1.1450.

Overall, EUR/USD is consolidating losses after breaking below its short‑term uptrend, though a recovery toward the SMA cluster and the 1.1700 area could ease downside pressure if support holds.

A Correction Is Inevitable

The big story – and dominant market driver – is becoming the rapid selloff across sovereign bond markets, as bond yields in major economies, including the US and Japan, soared last week after a set of inflation numbers showed that price pressures accelerated faster than analysts expected due to Middle East-led energy price pressures.

Yes, it was predictable. The funny thing is that there is always a pivotal moment that delivers the “uh huh” moment to investors. Last week, that moment came with inflation numbers from major economies, while oil prices kept rising due to the lack of progress in Iran peace talks.

And this Monday, bond stress remains in the headlines, as US crude traded above $108pb earlier in the session, with upside risks remaining dominant as the prolonged Middle East conflict leads to a record decline in global oil reserves.

The Japanese 10-year yield hit 2.80% before bouncing lower, while the Nikkei sold off another 1% following Friday’s sharp 2% retreat, also dragging major US and European indices lower. Tech stocks took a hit simply because they have been carrying the latest rally on their shoulders.

In China, the latest economic data looked particularly bleak, with an unexpected fall in investment, an unexpected slowdown in industrial production, and a worrying decline in retail sales growth to near-zero in April, mostly due to a 15% plunge in car sales. The weakness was largely explained by heavy disruptions linked to the Iran war.

This morning, futures are in the red and the bearish mood is justified: rising inflation fuels hawkish central bank expectations, reinforces the outlook for higher rates, and weighs on valuations. This makes sense.

What didn’t make sense was major indices rallying to ATH levels while investors KNEW inflation was going to become a problem as Middle East tensions dragged on. But strong AI earnings and solid guidance outweighed the risks, while CEOs of non-tech companies increasingly warned that the energy crisis was starting to eat into consumers’ purchasing power.

Now, this setup has been in place for more than two months, and central bankers have already expressed their views on what’s coming.

The European Central Bank (ECB) is expected to hike rates as soon as next month, while some hawkish voices are also growing louder at the Bank od Japan (BoJ). The Bank of England (BoE) is on slippery ground, with gilt yields also pressured by the political earthquake there. I wouldn’t touch sterling nor UK gilts at this moment. There is too much political uncertainty, making the fiscal policy path highly uncertain in a country where growth and productivity are both notably under pressure.

In the US, there has been a major shift: the probability of a December rate hike is now priced in at more than 50%. Activity in Federal Reserve (Fed) funds futures is now pricing in a 25bp+ rate hike for this December at above 50%. That’s a major shift for a Fed that was, until recently, expected to keep rates steady.

Remember, before the Iran war started, markets expected the Fed to CUT interest rates this year. The White House even chose Kevin Warsh partly because he was seen as someone who could help deliver lower rates if he were to become the next Fed chair. Today, markets are pricing a more than 50% chance of a December rate HIKE instead.

That’s not great news when equity prices are flirting with ATH levels and valuations already look stretched.

A correction is inevitable

The Nasdaq 100 PE ratio is above 38 today, meaning that a correction would actually be healthy to bring valuations back to a more reasonable — and down-to-earth — level.

If the Nasdaq 100 PE ratio were to move back toward its historical range — somewhere around 25x to 30x earnings — it would likely imply a meaningful pullback in equity prices unless earnings growth accelerates fast enough to justify current valuations.

How meaningful? Pure maths suggests that a move from 38x PE to 30x PE would imply roughly a 20–22% correction if earnings expectations remain unchanged. Assuming earnings continue to grow, however, a correction of 10–15% may be more reasonable. That would bring the Nasdaq 100 toward the 23.6% Fibonacci retracement level of the rally from April 2025 to today, near 26’600, and potentially toward 25’200, near the current 200-DMA. In theory, such a retreat should not reverse the positive trend, which would remain intact above the 24’800 level, but it would take some air out of the rally and allow for a healthier path higher.

This week

The focus will remain on Iran and the Strait of Hormuz, but also on UK inflation, FOMC meeting minutes, and flash PMI numbers across major economies.

On the earnings front, Nvidia is due to release earnings on Wednesday after the closing bell. Nvidia’s results have been one of the most important gauges of the health of the AI growth story. But that is no longer entirely the case. Nvidia chips are still considered the best in the market for training complex AI models, but running them also requires CPUs and memory chips. This is why memory chipmakers have increasingly taken over the rally, while traditional CPU makers and memory specialists like Intel and Micron have recently outperformed Nvidia, and Korean memory chipmakers continue to dominate headlines.

So I believe Nvidia earnings could temporarily divert investors’ attention away from geopolitical worries and soaring bond yields. But the bar is now set extremely high for Nvidia, and an earnings beat alone may not automatically trigger a positive market reaction.

Broad Weakness in Chinese Data Amid Deepening Oil Crises

In focus today

Focus will continue to be on developments in the Middle East and the bond market rout that has caused a sell-off in risk assets.

In Sweden, the Origo inflation expectations will be published. Given the clear focus on the credibility of the inflation target in last week's Riksbank minutes these are particularly interesting, even though the significance of the smaller survey for money market participants should not be overstated.

Overnight Japan's Q1 GDP figures will be released. Both the Tankan business survey and PMIs indicate the economy was on a reasonably solid footing in Q1, although the service sector has since slowed while remaining in expansionary territory.

During the week, notable releases include UK CPI inflation for April and the minutes from the Federal Reserve's April meeting on Wednesday, as markets look for further guidance after the divided rate decision. On Thursday, attention turns to flash PMIs for the US, euro area and UK. The week concludes on Friday with euro area negotiated wage data and Japanese inflation.

Economic and market news

What happened overnight

Chinese data for April were weak across the board. Retail sales dropped from 1.7% y/y to 0.2% y/y (cons: 1.9% y/y) and industrial production slipped from 5.7% y/y to 4.1% y/y (cons: 6.0% y/y). Investment growth fell back into negative at -1.3% y/y ytd from 1.7% y/y ytd in March. Home prices kept declining, though at a slightly slower pace, with new home prices down 0.19% m/m (prior: -0.21% m/m) while home sales also fell. The broad-based weakness may be related to the renewed uncertainty from the Iran war and calls for a step-up in economic stimulus. Strong 5% y/y GDP in Q1 gave some cushion for the 4½-5% target but the loss of momentum is concerning, especially as exports remain the only growth engine and face headwinds from high energy prices.

Developments in the US-Iran war continue to underscore the global economic stakes. Eurogroup President Pierrakakis warned ahead of Monday's G7 finance ministers' meeting that reopening the Strait of Hormuz and securing a lasting ceasefire are vital to contain energy and inflation pressures, with long-term borrowing costs already rising. Oil prices continue to climb, with brent crude reaching USD111/bbl overnight. President Trump met top national security officials on Saturday to discuss "the path forward" on Iran, later warning Tehran on social media that it "better get moving, FAST, or there won't be anything left of them". The IEA warns that global oil inventories are falling at a record pace towards critical levels, while new drone attacks on critical infrastructure, including the UAE's Barakah nuclear plant, highlight growing regional security and supply risks.

What happened over the weekend

In the UK, Labour's decision to let Andy Burnham seek a return to parliament sharpens the leadership crisis facing Prime Minister Keir Starmer after heavy local election losses, which have already prompted intensified calls for him to resign. Burnham, a more left-leaning figure and favourite to challenge Starmer, must first win a tight Makerfield by-election against Reform UK. Recent GBP weakness and higher gilt yields underline market worries over potential pressure for looser fiscal policy.

The Xi-Trump meeting in Beijing on 14-15 May did not provide any surprises. Stability was highlighted as a priority and China emphasized the importance of the Taiwan issue but did not manage to change US language on the topic. Both Xi and Trump stated that the Strait of Hormuz should be open and agreed Iran should not have nuclear weapons. But it has done little to ease tensions. China agreed to buy more US agricultural goods and 200 Boeing airplanes but if anything, the trade part was underwhelming. Nevertheless, continued stability between the two nations is probably the best we can hope for and that seems to be achieved for now.

In the US, April retail sales came in on the strong side of expectations, with higher gasoline prices boosting headline nominal growth. Underlying demand also appeared firm, as the 'core' retail control group rose a solid 0.5% m/m SA, following a strong 0.8% gain in March. The figures point to still‑resilient consumer spending despite mounting price pressures.

Equities: Equities fell on Friday, and the tone remains weak this morning. Asian markets are lower, and US and European futures are also trading softer, as the global bond sell-off continues and oil prices extend gains amid the still unresolved Iran/Hormuz situation.

Friday's equity session was telling. Energy was the only sector higher, supported by the move in oil, while defensive, low-volatility and value factors outperformed.

But importantly, this was not a clean stagflation trade. Materials and commodity-related equities were also sold, and both gold and silver were under pressure last week, especially on Friday.

That matters. If the market were simply pricing a stronger nominal growth environment, cyclicals and commodities should have held up better. Instead, the message from markets is more uncomfortable: this is increasingly about higher long-end yields driven by fiscal concerns, inflation risk and oil and not by growth alone.

FI and FX: Last week culminated with a broad-based sell-off in global fixed income market with e.g. US Treasuries completing the worst week in a year. This sell-off has continued overnight with e.g. 30Y US treasury yields jumping to multi-decade highs around 515bp. Notably the rise in yields has been broad based across curves and we have generally seen a modest steepening pressure in 2s10s while the 10s30s part has flattened. The negative nature behind the rise in global real rates has taken its toll on risk sensitive assets with equities posting losses equally across both cyclical- and defensive sectors highlighting the broad-based downscale in risk. Only energy has risen mirroring the continued move higher energy prices with Brent crude moving above USD 111/bbl overnight. In FX markets the reaction has been to send the USD higher while not least the CEEs, ZAR, Antipodeans, SEK and GBP have come under pressure. EUR/USD is at the time of writing trading at 1.1625 - the lowest level since "TACO-Tuesday" in early April. With most of Europe vacating Friday the opening to this session will be extra important for FI and FX markets.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1603; (P) 1.1637; (R1) 1.1658; More….

Intraday bias in EUR/USD remains on the downside as fall from 1.1848 is in progress. As noted before, rebound from 1.1408 could have completed as a corrective three-wave move. Deeper fall should be seen to retest 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1654 minor resistance will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1542). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

Oil and Yields Jump as Trump’s Security Meeting to Decide Next Step on Iran

Markets are beginning the week with a familiar but dangerous message: oil higher, yields higher, Dollar higher. Brent crude blasted above $111 in Asian trading while US 10-year Treasury yields climbed above 4.6%, extending the “Triple Higher” regime started lats week. Equities across Asia fell as investors rushed to price a worsening geopolitical backdrop, though selling stabilized somewhat into the afternoon as traders shifted into wait-and-see mode ahead of Washington’s next move.

The key issue now is no longer whether tensions are elevated. Markets already know that. The real question is whether the US-Israel-Iran conflict is about to enter a much more dangerous phase capable of producing further disruption to the global energy system. That fear intensified sharply over the weekend after the Trump-Xi summit failed to produce any meaningful diplomatic breakthrough on Iran or the Strait of Hormuz situation.

Attention now turns squarely to Trump’s scheduled Tuesday meeting with national security advisers in the White House Situation Room. According to multiple reports, the meeting will focus on military options regarding Iran after negotiations stalled further. Markets are treating the meeting as a potential turning point that could determine whether the conflict remains within the current framework of “managed tensions” or transitions into a broader and more dangerous phase involving expanded military operations and heightened risks to Gulf energy infrastructure.

In the week ahead, markets will also need to navigate several major economic events that could reshape rate expectations across currencies. The FOMC minutes will be scrutinized for signs of how impatient policymakers were becoming with the latest oil surge, while US PMIs will test whether growth momentum remains resilient enough for rates to stay elevated.

Elsewhere, UK CPI could become especially important for sterling and the BoE as Britain faces both political uncertainty and imported energy inflation pressure. Japan’s national CPI may further strengthen expectations for a June BoJ hike as Yen weakness amplifies imported inflation risks. Australia’s employment data and RBA minutes will shape whether another rate hike stayed in the discussion, while Canada’s CPI report will reveal whether the BoC can continue treating inflation pressures as temporary despite surging oil prices globally.

Key Economic Events — Week Ahead

| Currency | Event | Date |

|---|---|---|

| USD | FOMC Meeting Minutes | Wed, May 20 |

| USD | Flash PMI Manufacturing/Services | Thu, May 21 |

| EUR | Eurozone, Germany, France Flash PMI Manufacturing/Services | Thu, May 21 |

| GBP | UK CPI/Inflation Rate | Wed, May 20 |

| GBP | UK Flash PMI Manufacturing/Services | Thu, May 21 |

| GBP | UK Retail Sales | Fri, May 22 |

| JPY | Japan National CPI/Inflation Rate | Fri, May 22 |

| AUD | RBA Meeting Minutes | Tue, May 19 |

| AUD | Australia Employment Change/Labour Market Data | Thu, May 21 |

| CAD | Canada CPI/Inflation Rate | Tue, May 19 |

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 as failed diplomacy, military escalation, and the UAE infrastructure strike pushed the US-Iran conflict into a dangerous new phase. Read More.

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, with PSI rising from 46.2 to 48.9 and new orders returning to expansion territory. However, businesses continued to warn about rising fuel costs and shipping disruption linked to conflict in the Strait of Hormuz, while smaller firms remained under significant pressure. Read More.

China April Data Misses Across the Board as Domestic Demand Weakens Sharply

China’s April data deteriorated sharply, with retail sales nearly stalling at 0.2% yoy, industrial production slowing, and fixed asset investment unexpectedly turning negative. The weak figures reinforced concerns that rising geopolitical tensions and higher energy costs are weighing heavily on domestic demand. Read More.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1603; (P) 1.1637; (R1) 1.1658; More….

Intraday bias in EUR/USD remains on the downside as fall from 1.1848 is in progress. As noted before, rebound from 1.1408 could have completed as a corrective three-wave move. Deeper fall should be seen to retest 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1654 minor resistance will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1542). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

China April Data Misses Across the Board as Domestic Demand Weakens Sharply

China’s economic data deteriorated sharply in April, with industrial production, retail sales, and fixed asset investment all missing expectations as domestic demand weakened against a backdrop of prolonged Middle East conflict and rising external uncertainty.

Industrial production growth slowed from 5.7% yoy to 4.1% yoy, well below expectations of 5.9% yoy. Retail sales provided the biggest disappointment, decelerating sharply from 1.7% yoy to just 0.2% yoy, missing forecasts of 2.0% yoy and signaling that household consumption remains extremely subdued. Meanwhile, fixed asset investment contracted by -1.6% ytd yoy, reversing from the 1.7% growth recorded in the January-March period and falling far short of expectations for a 1.6% increase.

At a press briefing, National Bureau of Statistics spokesperson Fu Linghui said the Chinese economy had shown “strong resilience” despite elevated energy prices, supply chain disruption, and the prolonged Middle East conflict. However, he also acknowledged mounting external uncertainties and rising cost pressures on businesses, adding that some enterprises continued to face operational difficulties.

| Indicator | Previous | April | Expectation |

|---|---|---|---|

| Industrial Production (yoy) | 5.7% | 4.1% | 5.9% |

| Retail Sales (yoy) | 1.7% | 0.2% | 2.0% |

| Fixed Asset Investment (ytd yoy) | 1.7% | -1.6% | 1.6% |

Trump-Xi Summit Disappoints, Inflation Fears Fuel Bond Yield Surge

Key Takeaways

- The Trump-Xi Beijing summit delivered limited concrete progress, disappointing markets that had hoped for broader trade and geopolitical breakthroughs, while renewed warnings over Taiwan tensions kept regional risk sentiment fragile.

- Rising inflation pressures and surging global bond yields reinforced fears that the Federal Reserve may eventually shift toward rate hikes rather than cuts, with the US 10-year Treasury yield climbing to 4.59%.

- The AI-driven equity rally is increasingly viewed as overconcentrated, with growing concerns that elevated valuations in semiconductor and AI infrastructure stocks could face pressure from rising yields and sector rotation ahead of NVIDIA earnings.

- Chart of the day: WTI crude’s minor bullish structure remains intact after a strong rebound from 20-day and 50-day moving averages, with key short-term support at $103.40/bbl.

Top Macro Headlines

- Trump-Xi Beijing summit concludes with limited progress: The highly anticipated two-day meeting between US President Donald Trump and Chinese President Xi Jinping concluded in Beijing with few concrete agreements. While pledging a three-year "strategic stability" truce, Xi issued his bluntest warning yet on Taiwan, stating it could lead to "clashes" and create a "highly dangerous situation". On trade, China agreed to purchase only 200 Boeing jets, well short of the 500 investors expected.

- Gundlach and Wall Street warn of Fed rate hikes: DoubleLine Capital CEO Jeffrey Gundlach warned that stubborn inflation and a commodity boom could force the Federal Reserve to implement interest rate hikes rather than cuts. This aligns with a growing chorus on Wall Street, which is pricing out 2026 rate cuts entirely, shifting expectations toward tightening as the Fed's preferred inflation gauge runs at more than double its target rate.

- Global bond yields surge, threatening stock rally: Global bond yields marched higher over the weekend, with the US 10-year Treasury yield climbing to 4.59%. A steep rise in yields may start to pose a direct valuation threat to the global equity market rally, with the magnificent rallies seen in semiconductor and AI infrastructure-related equities since the end of March 2026.

- Goldman warns AI-fueled market rally overconcentrated: Goldman Sachs cautioned that the AI-driven stock surge powering the S&P 500 to repeated records is morphing into "one big trade," exposing investors to heightened systemic risk. Concurrently, J.P. Morgan data revealed that AI-related industries now command more than half of the total S&P 500 weight.

- Bill Ackman builds hefty stake in Microsoft: Pershing Square revealed a contrarian core position in Microsoft. Famed investor Bill Ackman is betting against the popular market trade of selling software firms to buy chipmakers, arguing that Microsoft's enterprise software suite remains deeply embedded and insulated from AI rivals.

Key Macro Themes

- Vanishing rate cuts and tightening fears: Persistent inflation, driven heavily by energy and commodity shocks, has completely upended the global monetary outlook. Investors are rapidly moving from a "higher-for-longer" stance to actively positioning for potential rate hikes under incoming Fed Chair Kevin Warsh.

- Geopolitical friction and supply-chain vulnerabilities: The US war in Iran and the ongoing closure of the Strait of Hormuz continue to impose structural inflation constraints on the global economy. While the physical ceasefire holds, the lack of a diplomatic breakthrough keeps WTI and Brent crude elevated near $105-110/bbl.

- Extreme equity concentration in the AI supercycle: With the AI ecosystem now exceeding 50% of the S&P 500's weight, the market's technical structure is highly sensitive to thematic rotation or an options market correction.

Global Market Impact

Equities: Wall Street pulled back ahead of the weekend, with the S&P 500 closing lower at 7,409, putting a pause to its prior 6-week run of weekly gains with a loss of 0.4% for the week of 11 May. Tech shares led the decline as investors re-evaluated software vs. hardware valuations.

Fixed Income: Bond markets experienced heavy selling. The US 10-year Treasury yield climbed to 4.59%. Long-term UK bond yields climbed to their highest levels since 1998 on fiscal deficit concerns due to political instability within the ruling Labour Party's leadership.

FX: The US Dollar retained broad structural strength as rate cut expectations evaporated. The Japanese Yen and British Pound remained defensive against greenback dominance, as both ended with weekly losses of 2.3% and 1.3%, respectively.

Commodities: WTI and Brent crude oil surged 3% last Friday to settle at $109.48 and $105.86/bbl, respectively, due to the ongoing closure of the Strait of Hormuz. Spot Gold corrected lower by 2.4% to settle at $4,540/oz under pressure from higher global bond yields.

Asia Pacific Impact

- Stock markets and supply chains: High energy import costs continue to pressure regional growth, with India's stock market down around 10% YTD. In South Korea, Samsung Electronics and its labor union are scheduled to resume high-stakes pay negotiations today to avert a threatened 18-day strike that could disrupt global memory chip supplies. S&P 500 and Nasdaq 100 E-mini futures extended their losses to 0.6% to 0.7% in today's Asia opening session at this time of writing.

- Currencies: The Indian Rupee was flagged as Asia's worst-performing currency due to the crude oil price shock. The offshore Yuan weakened in line with other regional currencies after China's summit talks concluded. Xi's blunt language regarding Taiwan leaves the regional complex highly sensitive.

- Regional policy actions: To combat currency depreciation and macro strains, the Indian government has initiated emergency solutions, including tightening controls on gold imports and cracking down on domestic fuel consumption.

Top 3 Economic Data/Events to Watch Today

- CN House Price Index, Retail Sales, Industrial Production (Apr) - 10.00 am SGT Impact: USD/CNH, Hang Seng Index, China A50, AUD/USD

- Trailing impact of US 10-year bond yield above 4.59% Impact: US Treasuries, growth stocks, USD, Gold

- Market positioning ahead of NVIDIA Q1 earnings release on Wednesday, 20 May Impact: US semiconductor stocks, Nasdaq 100, S&P 500

Chart of the Day: WTI Crude Bullish Revival from 20-Day and 50-Day MAs

Fig. 1: West Texas oil CFD minor trend as of 18 May 2026. Source: TradingView.

After a retest on its 20-day and 50-day moving averages on Monday, 11 May 2026, the West Texas oil CFD, a proxy of WTI crude oil futures, surged by 9% to hit a two-week high.

The current minor uptrend from its 6 May 2026 low remains intact within a medium-term sideways range configuration since the 9 March 2026 high of $119.54.

Watch the $103.40 key short-term pivotal support, and a clearance above $108.20 sees the next intermediate resistance coming in at $112.84 before the medium-term range resistance of $116.56/119.54.

However, a break and an hourly close below $103.40 invalidates the bullish tone for another round of choppy minor corrective decline towards the next intermediate supports at $100.25 and $97.40, also the area of the 20-day and 50-day moving averages.

EUR/USD Weakens Sharply After Key Support Finally Gives Way

Key Highlights

- EUR/USD started a sharp decline below the 1.1700 zone.

- It traded below a rising channel with support at 1.1720 on the 4-hour chart.

- GBP/USD could extend losses if it settles below 1.3300.

- USD/JPY is moving higher above the 158.50 resistance.

EUR/USD Technical Analysis

The Euro failed to stay above 1.1720 against the US Dollar. EUR/USD started a sharp decline below the 1.1700 and 1.1665 levels.

Looking at the 4-hour chart, the pair traded below a rising channel with support at 1.1720. The bears pushed the pair below 1.1620. A low was formed at 1.1602, and the pair is now consolidating losses well below the 23.6% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1602 low.

It is also well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). On the upside, the pair faces resistance at 1.1650.

The first major resistance sits at 1.1700, the 200 simple moving average (green, 4-hour), and the 50% Fib retracement level of the downward move from the 1.1787 swing high to the 1.1602 low. A close above 1.1700 could open doors for gains above 1.1720 and the 100 simple moving average (red, 4-hour).

In the stated case, the bulls could aim for a move to 1.1800. If there is another decline, the pair could find bids near 1.1600. The first major support sits near the 1.1550 level.

The next support could be 1.1520. A close below 1.1520 might initiate a drop to 1.1450. Any more losses might open the doors for a drop toward the 1.1400 zone.

Looking at GBP/USD, the pair remained in a negative zone, and the bears could aim for a clear move below the 1.3300 support.

Upcoming Key Economic Events:

- NAHB Housing Market Index for May 2026 – Forecast 34.0, versus 34.0 previous.

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 in Asian trading as traders returned from the weekend facing a geopolitical backdrop that had deteriorated sharply on multiple fronts at once.

The failed Trump-Xi summit removed hopes for any immediate diplomatic stabilization. US President Donald Trump then escalated rhetoric dramatically with his “the Clock is Ticking” warning to Iran following talks with Israeli Prime Minister Benjamin Netanyahu. Hours later, markets were hit with reports of a drone strike near the UAE’s Barakah nuclear power plant. By Monday morning, the message from oil markets was becoming unmistakable: this conflict is entering a far more dangerous phase.

What changed over the weekend was not merely tension levels, but the character of the risk itself. A successful strike near nuclear-linked infrastructure in the Gulf fundamentally alters the psychology of the market because it demonstrates vulnerability. Even though no reactor was hit directly and no radiation leak occurred, one reactor reportedly shifted temporarily onto emergency diesel power. If energy-linked infrastructure can be reached once, it can be reached again.

At the same time, the diplomatic path appears dangerously close to collapse. Trump’s Tuesday meeting with national security advisers is being viewed by markets less as a symbolic consultation and more as a potential gateway toward expanded military operations. The broader conflict has already evolved far beyond isolated exchanges. Strait of Hormuz shipping remains near total disruption, proxy attacks are spreading across the region, and Gulf states are increasingly being pulled directly into the confrontation.

Technically, Brent may now be approaching a critical breakout phase. Immediate focus is on the 61.8% projection of 96.03 to 108.45 from 130.88 at 111.56. Decisive break there could unleash a rapid momentum extension toward 100% projection at 116.30 next.

More importantly, the larger converging triangle consolidation from 119.50 peak appears close to completion. If confirmed, the broader uptrend could be preparing to attack the 120 crisis threshold again — a level markets associate with systemic economic stress rather than simple commodity volatility.

From here, the oil market faces two radically different endings.

- The first is a short, intense military exchange involving coordinated strikes but followed by a rapid internationally enforced ceasefire. Under that outcome, Brent could spike toward $135–145 in a matter of days before collapsing sharply.

- The second, and more structurally dangerous scenario, would emerge if Tuesday’s White House meeting leads to a prolonged conflict involving sustained attacks on Gulf export or processing infrastructure. In that case, oil above $120 may no longer represent a temporary panic spike, but the beginning prolonged uptrend extension.

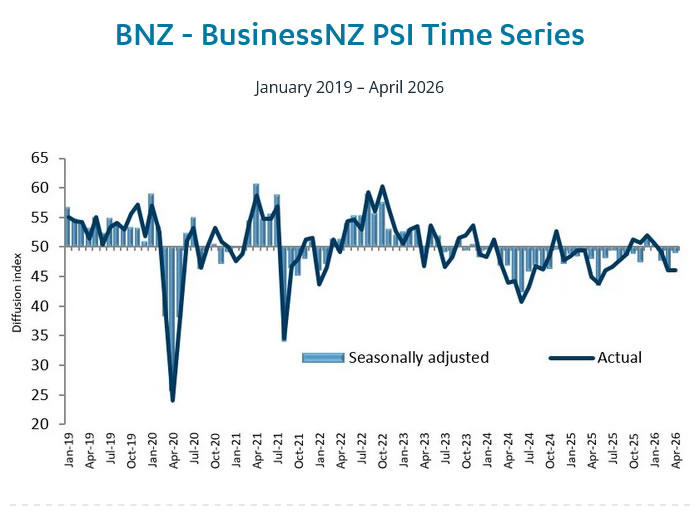

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, though activity remained in contraction territory as firms continued to grapple with rising fuel costs and disruption linked to the Middle East conflict. BusinessNZ Performance of Services Index improved from 46.2 to 48.9, but still below the 50 expansion threshold.

Underlying components were mixed but generally less weak. Activity/sales rose from 44.7 to 48.9, while employment improved from 46.6 to 48.5. New orders/business provided the brightest signal, climbing from 46.0 to 51.2 to return to expansion territory. However, supplier deliveries slipped from 47.2 to 46.6, while stocks/inventories edged up from 46.2 to 47.6.

BusinessNZ Chief Executive Katherine Rich said more than two-thirds of respondents continued to report negative conditions, with many citing fuel prices as a major pressure point. She warned that ongoing disruption to shipping through the Strait of Hormuz made a quick return to sector-wide expansion difficult to envision.

Smaller firms appeared particularly vulnerable, with the micro-business sub-index at just 44.4, while medium-large firms outperformed at 55.5.

| Component | March | April |

|---|---|---|

| Headline PSI | 46.2 | 48.9 |

| Activity / Sales | 44.7 | 48.9 |

| Employment | 46.6 | 48.5 |

| New Orders / Business | 46.0 | 51.2 |

| Stocks / Inventories | 46.2 | 47.6 |

| Supplier Deliveries | 47.2 | 46.6 |