Sample Category Title

USDJPY Still Bullish Above 113.10 Level

The U.S dollar continues to hold firm against the Japanese yen, with price-action currently capped by the 113.69 resistance level. The USDJPY briefly dipped lower on Friday, following the U.S jobs report, but quickly recovered intraday losses, to trade back around the 113.50 region. The pair is currently being driven higher by strong gains in global stock indices, and overall risk-on trading sentiment. The main risk event for the U.S dollar index this week will be the U.S Federal Reserve interest rate decision and U.S monetary policy statement by outgoing Federal Chair Janet Yellen.

The USDJPY pair remains strongly bullish while trading above the 113.09 technical level, intraday buyers may look to test towards the 114 handle.

Should price-action on the USDJPY pair move below the 113.09 technical level, intraday sellers may target towards 112.71 support level.

Light Release Schedule Kicks Off Weekly Trading

The global financial markets will be off to a slow start on Monday, as a dearth of economic data will keep investors focused on a series of upcoming monetary policy meetings from around the world.

At 09:00 GMT, the Italian government will release its monthly retail sales report for October. Receipts at retail stores rose 0.9% during the previous month for an annualized gain of 3.4%.

At 11:00 GMT, Portugal will report on its global trade balance for October. The country reported a deficit of €3.543 billion in September.

Greece is also tentatively scheduled to release its industrial production numbers on Monday.

In North America, the US Labor Department will release the latest JOLTS job openings data for October. The report provides a snapshot of job openings in the world’s largest economy, which is seen as an important proxy for job vacancies.

Later this week, the Federal Reserve, Bank of England, European Central Bank and Swiss National Bank will deliver their final policy verdicts of the year. With the exception of the US Fed, no change in monetary policy is expected.

On the topic of the Fed, interest rates are widely expected to rise by 25 basis points on Wednesday to 1.50%. Market participants should therefore keep a close eye on the US dollar in the days leading up to the vote. The US dollar is coming off its best week of the year, according to Bloomberg.

The dollar index edged lower at the start of the week, and was last seen trading at 93.82.

On Friday, the US Department of Labor said the economy added 228,000 nonfarm jobs in November, following a downwardly revised gain of 244,000 the previous month. That was well ahead of forecasts, which called for a November increase of 200,000. The unemployment rate held steady at 4.1%. Average hourly earnings climbed 0.2% month-on-month.

EUR/USD

Europe’s common currency consolidated Monday after a week of sharp declines. The EUR/USD was last seen trading at 1.1782 for a gain of 0.1%. All eyes will be on monetary policy this week, as both currencies will be highly sensitive to announcements made by the Fed and ECB.

GBP/USD

Cable was trading steady in early week trade as investors rejoiced after the UK and the European Union reached a Brexit breakthrough last week. GBP/USD was last seen hovering at 1.3400. Immediate resistance is found up ahead at 1.3420. On the downside, support is located at 1.3345.

USD/JPY

The dollar-yen exchange rate rose on Monday, as the pair climbed above 113.50 in a new show of strength. The USD/JPY is eyeing a re-test of the 114.40 region, which provides an important gateway to further upside. To get there, the pair will need to cross the 113.65 and 114.00 resistance levels. On the downside, immediate support is located at 113.10.

Forex: Central Bank Meetings Dominate The Week

With no impactful economic data releases on the calendar today, the markets are focusing on a plethora of Central Bank meetings scheduled this week.

Wednesday, December 13th at 19:00 GMT will see the US Federal Reserve release its quarterly economic projections and the Federal Open Market Committee (FOMC) release its statement. The markets have been focusing on the FOMC December meeting and the forecast hike in interest rates by 0.25%.

The Fedwatch tool is projecting the probability of such a hike at just over 90%. With the markets already pricing in a hike, they will be focusing on the tone of the statement to determine the pace of further hikes in 2018. The Fed predicted in September that it would increase rates three times in 2018 and two more times in 2019. However, predicting the future is not an easy task with recent economic reports exceeding expectations, including Friday’s estimate by the Commerce Department that employers added 228,000 jobs in November. Such data raises the possibility that the US economy is continuing to gain strength.

Thursday, December 14th at 08:00 GMT will see the Swiss National Bank (SNB) release its Interest Rate Decision. CHF is estimated by the OECD to be nearly 20% above fair value (PPP), as such, the SNB is nowhere near prepared to move away from its current monetary policy as the Swiss economy is growing steadily and the threat of deflation has been averted.

Thursday, December 14th at 12:00 GMT will see the Bank of England (BoE) release its latest Monetary Policy Committee (MPC) summary. It is widely expected that the BoE will leave UK interest rates unchanged. The BoE has signaled that it will raise rates over the next 3 years but the markets expect them to occur at a gradual pace. With UK inflation above the Banks 2% target, the lackluster economic growth will restrict any imminent hike in rates. The BoE’s economic forecasts are currently based on another two 0.25% interest rate rises by the end of 2020, which would leave benchmark rate at 1% up from the current 0.5%.

Thursday will also see the Bank of Mexico’s new Governor Alejandro Diaz de Leon releasing its monetary policy statement. Mexican inflation hit a 16 year high in August (6.66%) but price increases have slowed in the last quarter. The markets are not expecting any rate cuts until August of 2018 at the earliest.

Thursday, December 14th at 13:30 GMT will see the European Central Bank (ECB) releasing its Monetary policy statement. The ECB is not expected to waiver from its Quantitative Easing program nor increase rates at any time soon. However, the markets will be reading into the statement, as the ECB discloses its 2020 growth and inflation forecasts that may provide clues as to the pace and timing of future interest rate hikes.

Friday, December 15th will see the Bank of Russia releasing its monetary policy statement. After cutting its benchmark rate by 0.25% in October the markets are not expecting any further cuts. With continued western sanctions and the decline in oil prices, the markets will be keen to see the tone of the statement for clues as to the timing of any future rate cuts as Russia recovers from a slight recession.

EURUSD is 0.1% higher in early Monday trading at around 1.1778.

USDJPY is little changed in early trading at around 113.55.

GBPUSD is 0.1% higher in early session trading at around 1.3395.

Gold is 0.12% higher, trading around $1,249.

WTI is 0.3% lower in early Monday trading at around $57.15.

Market Update – Asian Session: RBNZ Names Next Gov

Headlines/Economic Data

General Trend: Equities see muted volatility amid Bitcoin Futures launch and ahead of a week filled with key global macro events, including Wed’s FOMC decision and US CPI

CBOE commented on Sunday’s launch of Bitcoin Futures: Said the opening price was $15,000 and 890 contracts were traded by 7:15 pm CT.

As of 9:10 PM CT, Front Month Bitcoin Futures had risen above $18,000 with over 1,600 contracts traded.

Japan

Nikkei 225 opened +0.4%; closed +0.6%

TOPIX Iron & Steel Index +0.6%

Construction company Obayashi -7% (speculated bid rigging allegations)

Chip-related names decline following Friday’s gains: SUMCO -2.5%, Tokyo Electron -2%

JAPAN Q4 BSI LARGE ALL INDUSTRY Q/Q: 6.2 V 5.8E; BSI LARGE MANUFACTURING Q/Q: 9.7 V 10.0E

Japan Govt is expected to upgrade its FY18 GDP forecast of 1.4% to ~2% with an expanding global economy seen boosting exports and capital investment expected to remain firm

Japan

(JP) Japan companies to receive more than 20% tax reductions if they raise wages - Nikkei

Looking Ahead: BoJ Q4 Tankan Survey due for release on Friday

Korea

Kospi opened +0.2%

Samsung Heavy, +1.5%: Expected to name new CEO after lower forecast - US financial press

Samsung Electronics -0.8%: Expected to hold its global strategy meeting starting from this week to share next year’s goals and strategies under the newly appointed chief executives - Korean press

Automakers decline, Hyundai Motor -5%, Kia Motors -2%: The companies said to target 2018 auto sales at 7.5M units vs 8.25M in 2017 – South Korean Press

Hyundai Motor Think Tank said automakers in South Korea face ‘major’ headwind from weakening Yen in 2018 - financial press

South Korea exports from Dec 1-10th -1.5% - Korean press

South Korea, US and Japan start missile tracking drill today; South Korea Military: No decision has been made on next year's alliance exercise - Korean press

South Korea private think tank Korea Economic Research Institute (KERI): 52-hour workweek to cost businesses KRW2.3T in extra expenses annually due to Govt imposing a 52 hour working week limit - Korean press

(KR) South Korea sells KRW1.1T v KRW1.1T indicated in 10-year bonds: avg yield 2.495% v 2.595% prior

Bank of Korea (BOK) Sells KRW960B 1-yr monetary stabilization bonds at 1.82%

Bank of Korea (BOK) sells KRW800B v KRW900B indicated in 3-month monetary stabilization bonds; avg yield 1.56% v 1.54% prior

(KR) Hyundai Motor Think Tank said automakers in South Korea face ‘major’ headwind from weakening Yen in 2018 - financial press

China/Hong Kong

Shanghai Composite and Hang Seng opened flat

Hang Seng Energy Index +1.2%, Materials +1.1%, Financials +0.7%; Property Index -0.5%

(CN) China 10-year bond yield +3bps

(CN) China to implement new concepts in its 2018 economic work - financial press; To curb leverage ratio in 2018

(CN) PBoC sets yuan reference rate at 6.6152 v 6.6218 prior (1st stronger setting in 11-sessions)

(CN) PBOC Open Market Operations (OMO): injects CNY80B in 7 and 28-day reverse repos v skips prior; Net injections CNY20B

(CN) China Nov Fiscal Spending CNY1.66T, -9.1% y/y v -8.0% prior; Fiscal Rev CNY1.14T, -1.4% y/y v +5.4% prior

(CN) China should examine additional channels for direct financing; should protect interests of convertible bond holders – Chinese Press

(CN) China Banking Regulatory Commission (CBRC) indicates looking at increased rules for interbank asset transfers - China press

(CN) CHINA NOV CPI M/M: 0.0% V 0.1% PRIOR: Y/Y: 1.7% V 1.8%E; PPI Y/Y: 5.8% v 5.8%e; Food inflation: -1.1% (10th straight decline) v -0.4% prior

Looking Ahead: China Nov Fixed Assets Investment, Retail Sales and Industrial Production due to be released on Thursday.

Australia/New Zealand

ASX 200 opened +0.1%; closed +0.1%

(NZ) NEW ZEALAND NOV CARD SPENDING RETAIL M/M: 1.2% V 0.5%E; CARD SPENDING TOTAL M/M: 1.4% V 0.7% PRIOR

(NZ) RBNZ names Adrian Orr as next RBNZ Gov, effective March 27, 2018; Orr is well-known in the business community as the long-running chief executive of the New Zealand Superannuation Fund - NZ press; NZD/USD rises 0.9%

(NZ) NZIER: NZ Economists expect GDP growth averaging below 3% over the next five years; reiterates no urgency for RBNZ to raise rates

(AU) Australia buys back A$500M in 2018 and 2019 bonds

(AU) Australia sells A$500M v A$500M indicated in 3.00% March 2047 Bonds, avg yield 3.2948%, bid to cover 3.23x

TOX.AU Cleanaway to acquire Tox Free for A$3.425/shr cash for A$671M; To raise ~A$590M in a 1 for 3.65 entitlement offering priced at A$1.35/shr; +20%

AWE.AU Confirms all share offer from Mineral Resources at A$0.80/shr (1 new MRL share for each 22.325 AWE shares held); +16%

RFG.AU Series of investigative articles by Fairfax claiming a large number of RFG franchisees are suffering financial trouble and that wage fraud is systemic; -22%

Looking Ahead: Australia Nov NAB Business Confidence due to be released on Tuesday; RBA officials Lowe and Kent due to speak on Wed; Australia’s Nov Employment Data to be released on Thursday

Other Asia

Philippines Peso (PHP) gains over 0.3%: Fitch raised Philippines Sovereign Rating to BBB from BBB- (lowest level of investment grade)

Taiwan’s Hon Hai +3%; Reported Nov Rev +18.5% y/y

Indonesia, Malaysia and Thailand sign local currency FX settlement agreement

(IN) India govt to set up panel to decide on Bitcoin policy

(PH) Philippines sells PHP0B (nil) for 3-month, 6-month and 1-year bills (rejects all bids for second straight auction*)

North America

(US) US Senator Collins (R-ME) reiterates unsure if she will support final version of tax plan, wants to first see the bill – US Media

General Growth Properties (GGP): Said to reject ~$14.8B merger proposal from Brookfield, merger talks expected to continue – financial press

Looking Ahead: US Fed FOMC decision/economic forecasts and Nov CPI data due on Wed.

US Nov Retail Sales due for release on Thursday

Europe

(UK) Dec Rightmove House Prices m/m: -2.6% v -0.8% prior; y/y: 1.2% v 1.8% prior

(IE) Ireland Nov Construction PMI: 56.7 v 54.5 prior

BAE Systems [BA.UK]: Receives ~£5.0B order from Qatar for Typhoon aircraft

Man Group [EMG.UK]: To start quantitative hedge fund in China - financial press

Looking Ahead: ECB, SNB and BoE rate decisions due on Thursday, Dec 14th

Levels as of 01:00ET

Nikkei225 %, Hang Seng +0.7%; Shanghai Composite +0.5%; ASX200 +0.1%, Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 +0.4%

EUR 1.1784-1.1764; JPY 113.69-113.45; AUD 0.7529-0.7504;NZD 0.6911-0.6834

Feb Gold +0.2% at $1,251/oz; Jan Crude Oil -0.4% at $57.13/brl; Mar Copper +0.0% at $2.98/lb

EUR/GBP Is Currently Trading At 0.88

Market movers today

Today, no global market movers are due to be released.

However, we have a very busy central bank week ahead, with the Fed, ECB, Band of England and Norges Bank meetings coming up and the EU summit taking place on Thursday and Friday, where progress in the Brexit negotiations will again be in focus.

In Denmark, the inflation figures for November are due out, balance of payments data, as well as the number of bankruptcies and repossessions for October.

In Norway we get November inflation data this morning where we look for a further rise in the core measure from 1.1% to 1.2% y/y (consensus 1.2%, Norges Bank 1.3%).

Selected market news

Ahead of the EU summit later this week, Brexit remains in focus, as Brexit secretary David Davis (who has been more or less removed from the negotiations as PM Theresa May has taken over herself) said t hat t he agreement on t he Irish border " was much more a statement of intent" than a binding agreement . Michael Gove and Boris Johnson both want a clean split from the EU aft er t hey backed May's deal. The comments highlight that even though the negot iat ions have moved forward, it is too early for markets to really price out a Brexit premium just yet . Despite talks likely moving to transit ion period and future relationship now, we do not know much about what that would look like at the moment . EUR/GBP is currently trading at 0.88.

US President Trump is expected to del iver a speech on the US tax reform on Wednesday, while House and Senate Republicans t ry to sort out the differences in the two tax bills. Also a lot of demonst rat ions and increasing tension in the Middle East after Trump's decision to recognise Jerusal em as Israe l 's capi tal .

Also in the US, Congress passed a short-term funding bi ll to avert a federal government shutdown on Friday. The bill will keep the government open until 22 December. US debt limit has been reinst ated and t he Treasury can now only issue debt using " ext raordinary measures" (basically swapping non-marketable debt t o market able debt ). T he " ext raordinary measures" are expected to run out late Q1 2018, where the US polit icians need to lift the debt limit or resuspend it .

No big movements in the financial markets overnight . Asian stock markets are up this morning and European/US equity futures are also pointing higher. US 10Y Treasury yield is more or less unchanged at 2.4%. EUR/USD is trading slightly below 1.18. Oil slightly down to 63.13 dollars per barrels.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.11; (P) 152.26; (R1) 152.89; More...

Intraday bias in GBP/JPY remains neutral for consolidation below 153.39 temporary top. Further rally is expected as long as 149.74 support holds. Break of 153.39 will resume the medium term up trend and target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. However, break of 149.74 will dampen our bullish view and turn bias back to the downside for 146.96 key support instead.

In the bigger picture, current development suggests that medium term rise from 122.36 is resuming. Sustained trading above 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 146.96 support will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

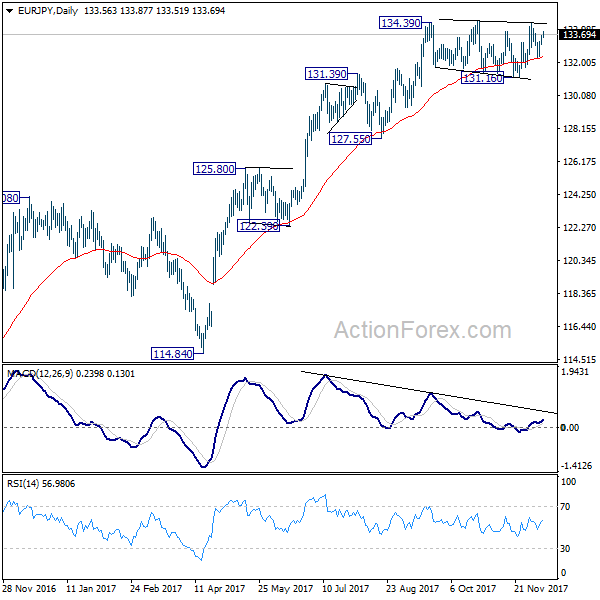

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.24; (P) 133.42; (R1) 133.75; More....

Intraday bias in EUR/JPY remains neutral as range trading could continue inside 131.16/134.48. But further rise will be expected as long as 131.16 support holds. Decisive break of 134.48 will resume medium term rise from 114.84 and target 141.04 resistance next. However, sustained break of 131.16 support will now indicate near term trend reversal and turn outlook bearish for 127.55 key support.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). Sustained break of 61.8% retracement of 149.76 to 109.03 at 134.20 will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will suggest medium term topping and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

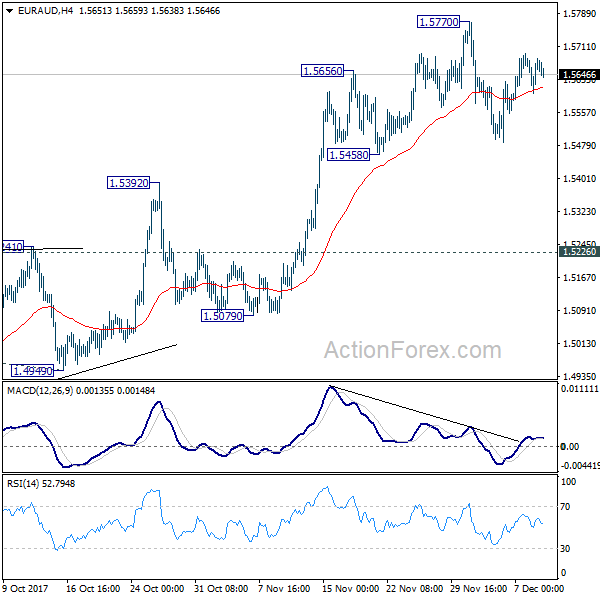

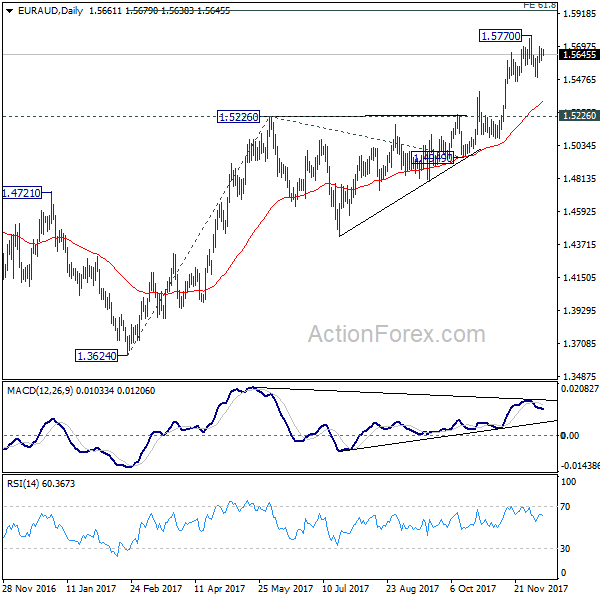

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5617; (P) 1.5650; (R1) 1.5699; More....

Intraday bias in EUR/AUD remains neutral for consolidation below 1.5770 short term top. Deeper decline could be seen and break of 1.5458 support cannot be ruled out. But downside should be contained above 1.5226 key support to bring rally resumption. On the upside, break of 1.5770 will resume the medium term rise and target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8721; (P) 0.8763; (R1) 0.8837; More...

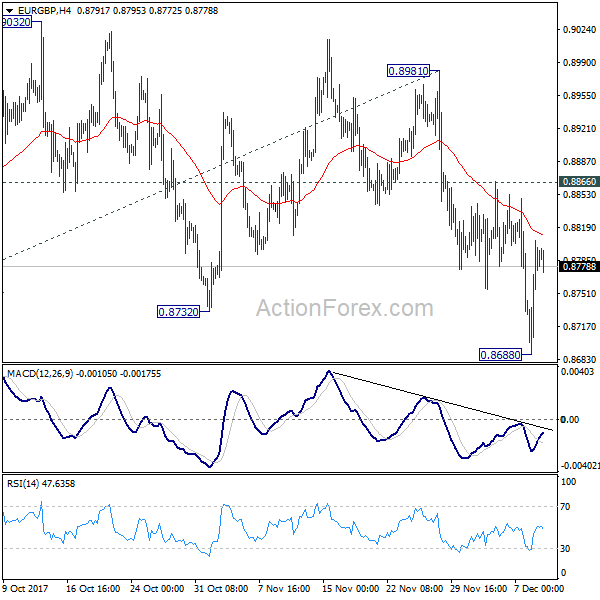

Intraday bias in EUR/GBP remains neutral for consolidation above 0.8688 temporary low. Deeper fall is expected as long as 0.8866 resistance holds. Below 0.8688 will target 61.8% projection of 0.9305 to 0.8745 from 0.8981 at 0.8468 first and then 100% projection at 0.8151 next. However, break of 0.8866 resistance will indicate near term reversal and turn bias back to the upside for 0.8981 resistance instead.

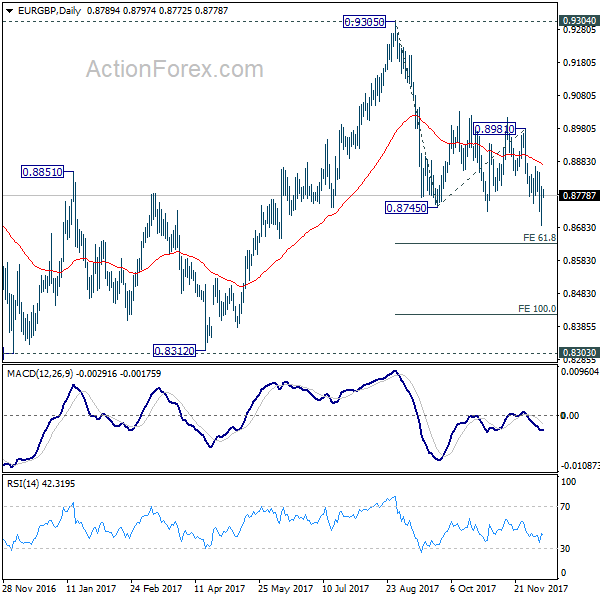

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

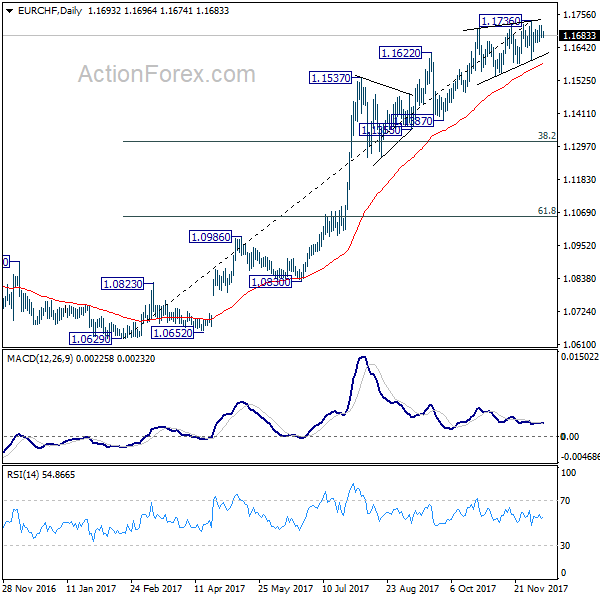

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1662; (P) 1.1691; (R1) 1.1706; More...

Intraday bias in EUR/CHF remains neutral and outlook is unchanged. We maintained the view that EUR/CHF is close to topping, if not formed. This is supported by persistent bearish divergence condition in 4 hour MACD, and rising wedge like structure. On the downside, break of 1.1597 support will will be a strong sign of trend reversal and should turn outlook bearish for 38.2% retracement of 1.0629 to 1.1736 at 1.1313.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.